13 minute read

Sean of the South By Sean Dietrich Meeting Shelbylane

Homewood. Supercuts hair salon. The young woman cutting my hair goes by the name Shelby. She is as country as a collard, with an accent like Ribbon cane syrup.

She is 21. She is constantly laughing. She smiles a lot. All the customers here do the same whenever Shelby is around. This girl is Pollyanna.

I ask where Shelby’s originally from.

“Woodstock,” she says. “Not the one in New York. The one in Alabama.”

I would have never guessed.

I ask how she got started styling hair.

Dietrich

“Started cutting hair when I was 10 years old. My mama was a hairstylist, but she didn’t cut men’s hair, so Daddy would hand me the scissors and say, ‘You cut my hair, Shelbylane.’ That’s my real name, Shelbylane. My daddy wanted me to have a double first name like a Southern belle. Do you want me to trim the clumps of hair shooting straight out of your ears?”

“Please.”

While Shelbylane works steadily, I’m trying to imagine a world wherein a grown man would give a 10-year-old child surgically sharpened scissors and allow the child to take a whack at his head.

“Your father trusted you a lot, to let you cut his hair when you were so little.”

She laughs. “Oh, Daddy believed in me so much. His confidence in me made me what I am. When I was a kid, I felt like I could do anything because of his faith in me. Do you want me to trim your unibrow, sir?”

“Please. Does your father live in Woodstock?”

“No, he passed away.”

“I’m sorry.”

“It’s okay. He died when I was 14. I’ve had time to deal with it. But I miss him real bad.”

I know all about daddies dying at young ages. I know all about missing daddies real bad.

“But I have a theory,” says Shelbylane, firing up her electric clippers. “If you lose your parent at a young age, it can either make you a good person or a bad one. I know a lot of people who let it ruin them. But I think Daddy’s death made me a good person. I learned that this life is not all there is.”

“What about your mother?”

“She run off when my daddy died.”

“I’m sorry.”

“I was raised by my grandparents. Did you want me to shave the hair on your neck?

It’s like a carpet back here.”

“Yes. Thank you. I’ll bet your grandparents are proud of how well you’ve turned out.”

“Well, my grandmother died. She had dementia. So now it’s just my granddaddy and my step-sister.”

“Do you like your job?”

She smiles largely. “Oh, yessir. I love my job. I went to school and worked hard to learn to cut men’s and women’s hair. It took a long, long time, I practiced a lot. I am a very hard worker.

“When I got my first job at a local salon, they wouldn’t let me cut hair, they made me do petty jobs, like cleaning toilets and stuff. I didn’t mind, but I kept begging them, ‘Please, let me prove what I can do, let me show you how I cut hair on a mannequin or something.’ But they wouldn’t let me. So I quit, and here I am at Supercuts.”

“Do you like Supercuts?”

“Like it? I love it. I don’t have many regular clients yet, but this is my dream job. I have always wanted to cut hair and be my own boss, and now I’m doing it, right here in Homewood. Of all places. Pinch me.”

“I don’t know many folks who feel about their jobs the way you do.”

“Well, cutting hair isn’t just a job, it’s more than that. It’s about making people feel good about themselves, about helping people love themselves. I’m so lucky to be doing this for a living.”

When she finishes her work, my haircut ranks among the best haircuts I’ve ever received. My hair looks perfect, it’s only too bad about my face. I’ve never been a looker.

When I was a kid, before group photos someone always handed me the camera.

“Do you like your haircut?” she asks, passing me the mirror, spinning my chair.

“I do. Your father was right. You’re an artist.”

“Thank you. Come back and see me again. I need all the new clients I can get.” when it was about $394,000.

Well, Shelbylane, let me see what I can do about that.

Sean Dietrich is a columnist and novelist known for his commentary on life in the American South. He has authored nine books and is the creator of the “Sean of the South” blog and podcast.

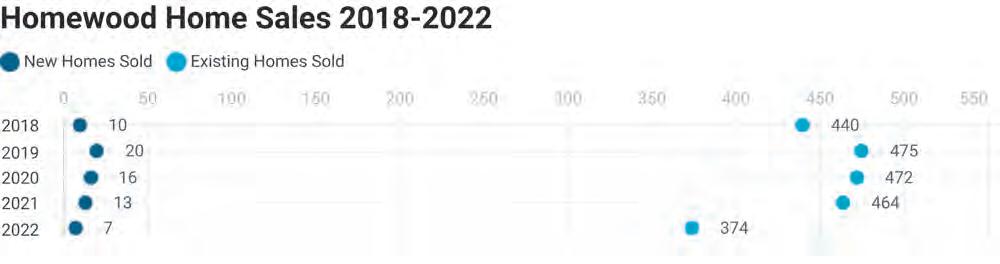

While the price has gone up, square footage has remained about the same. In 2018, the average square footage of a home in Homewood was about 1,990 square feet. 2020 was the highest average of square footage, reaching just under 2,100 square feet. Last year, the average home sold was just under 2,000 square feet.

However, new homes being built have averaged more than 3,000 square feet since at least 2018, according to MLS data.

MLS data also measures the monthly supply of homes in each city, and Homewood has no supply of new homes, with so few built last year. There is just under a month’s supply of existing homes, with 26 homes on the market as of Jan. 10. Eleven homes were pending.

William Siegel with Twin Construction said he is seeing “zero slow down” in any part of the market. The Edgewood neighborhood, in which Siegel lives, has been especially popular, he said.

“It’s a great spot to live,” Siegel said.

While there is much thought that there is a market-wide slow down, Siegel said he isn’t seeing that.

Most new construction in the city involves teardowns and rebuilds rather than empty lots, he said. His group has also seen a lot of major renovations, he said.

Mortgage rates have not been a problem in Homewood, despite their upward trend since the COVID-19 pandemic, Siegel said.

The average interest rate for a 30-year fixed mortgage had fallen below 3% after the COVID-19 pandemic hit, dropping as low as 2.65% in January 2021. That was the lowest rate in history and encouraged many people to move or build because they could borrow money at a lesser price and afford a bigger house.

But the Federal Reserve steadily raised short-term interest rates throughout 2022 in an effort to control inflation. The result was that the average 30-year mortgage rate edged up from 2.75% in December 2021 to 4% in March, 5.25% in May and 7% in October, according to Freddie Mac. The Federal Reserve lists the current interest rate in the U.S. at 4.5%.

Siegel said most people are able to get what they want as far as layout. In Homewood, that typically means four bedrooms with 3.5 baths, Siegel said.

The market is still a seller’s market with low inventory, Siegel said, with a majority of sales coming from Edgewood, though he is hopeful that West Homewood can see more sales as well.

Realtor Julie White echoed Siegel’s comments that inventory is indeed low. Because of that, homes are selling “pretty quickly,” White said, and she expects to see more of the same in the coming months.

Realtors Katie and Gusty Gulas said they are seeing homes flying off the market once they are posted. The median time a home has spent on the market was three days, Gusty Gulas said.

The overall market is healthy, Katie Gulas said.

“I believe our interest rates are continuing to come down from November highs,” she said.

White added that out of the 11 homes she sold in January, only one went for under the asking price.

Housing costs have gone up, White said, pricing some people out of the market. Those looking for homes under $400,000 have begun to look to Shelby County or other areas in Jefferson County, such as Irondale.

It is definitely a seller’s market, White said. She said there has not been a better time in recent memory for those looking to sell their home.

However, with mortgage rates increasing, those who do not have to move may not move, including those who refinanced several years ago when mortgage rates were lower, White said. With higher mortgage rates comes lower buying power, she said.

Those looking to upgrade their homes may have to choose between making renovations or moving, White said.

“You want your home to be your home and be reflective of you and your lifestyle,” White said.

West Homewood is growing, though the homes in that area are smaller, White said. Edgewood remains very popular, she said.

“Homewood’s just a place that everyone wants,” White said.

Katie Gulas said living in Edgewood, she understands the reason people want to live there and in Homewood in general. There is close proximity to downtown Birmingham, a nice atmosphere, coffee shops, bookstores and an ability to “entertain kids without a car.”

“That’s what a lot of the buyers are looking for,” she said.

– Community Editor Leah Eagle contributed to this story.

By LOYD MCINTOSH

When the Federal Reserve raised interest rates in early February to combat inflation, one area of concern for many potential homebuyers was how the Fed’s actions would affect mortgage rates and their ability to afford a new home.

However, Clint Thompson, a mortgage officer with Fairway Independent Mortgage Corp. in Inverness, says the perception that mortgage rates automatically increase following a rise in interest rates is incorrect. “There is always misinformation out there when people hear what the Federal Reserve is doing. They think, 'Oh gosh, mortgage rates jumped a quarter of a percent,’” Thompson said.

While it is true that interest rates and other signals from the Federal Reserve influence the economy, Thompson said mortgage rates are more closely related to inflation rates than direct action from the Federal Reserve. Thompson explained that the interest rate hike should eventually have the opposite effect on mortgage rates if inflation slows.

“Mortgage rates can come down when the Fed makes a hike, because overall it's more about inflation than interest rates,” Thompson said. “You may see that 30-year mortgage rates actually improve because the markets interpret that as a positive move.”

Largely due to government spending during the COVID-19 crisis, the U.S. inflation rate grew at a rate of 6.5% in 2022, according to data published by the U.S. Department of Labor in mid-December, after growing to 7.1% in 2021. Among the areas the government spent additional funds, according to Thompson, were mortgage-backed securities and treasuries, which kept mortgage rates from organically adjusting to market forces, a concept known as “quantitative easing.”

“The Fed basically ignored the whole inflation factor and continued to buy treasuries and mortgage-backed securities,” Thompson said. “That artificially kept interest rates down close to 3%.”

As the government slowed quantitative easing measures over the past 12 months and raised interest rates in February, mortgage rates rose from an average of 3% for a typical 30-year mortgage to just over 6% in under a year, While the rapid rise may create sticker shock among homebuyers, Thompson said the market is responding organically to the Federal Reserve’s policies and, although mortgage rates spiked to more than 7% recently, potential homebuyers should start seeing rates lower in the second and third quarter of 2023.

”We'll just have to see how it all plays out, but the consensus is we should see 30-year mortgage rates close to 5%, maybe even just a fraction below 5%, sometime this summer,” Thompson said.

Fred Smith, owner and operator of The Fred Smith Group RealtySouth agency in Crestline, said the Federal Reserve’s interest rate hike may finally return the local real estate market to a much-needed state of normalcy. Smith said the economic conditions of 2020 through 2022 created unnatural conditions in the market that should stabilize now that mortgage rates have risen.

“People are getting used to the rates. It's not like they've gone up to something that's unreasonable. They've normalized,” Smith said.

“2019 was the last normal market. Then we had 2020, and we worked our way through that market, then we entered a seller's market in 2021 and 2022 with bidding wars and all that kind of stuff,” Smith said. “Now, I feel it's going to be a normal 2023.”

With 30-year fixed mortgage rates hovering at 6.9% and housing prices on the rise, what do the current conditions mean for the average homebuyer? Smith and Thompson both recognize that affordability is a factor in many cases but said there are solid reasons to purchase a home now, especially if you’re renting.

“All of the great reasons for buying a house still exist,” Smith said. “We haven't seen as good of a time to buy for renters, with rent rates going up 20 to 30% in the last two years.”

For homebuyers for whom a one-point or twopoint rise in rates could cause monthly-payment sticker shock, Smith suggested a couple of strategies. First, he said an interest rate buydown is a viable option or an adjustable rate mortgage, especially for new homebuyers likely to move within five years of their purchase.

“In Crestline, the average homebuyer lives there less than seven years,” Smith said. “If they get a seven-year ARM and they're moving about every five years, why have a 30-year fixed rate when you can take advantage of a lower interest rate?”

Thompson, who said he believes mortgage rates should settle back down to 3 or 4% over the next few years, suggests a two-for-one buydown mortgage. This option allows the homebuyer to pay 2% lower than the actual rate for the first year of the mortgage, then 1% lower for the second year, then the rate increases to the regular rate in the third year.

At current rates, a homebuyer would pay 4.9% in year one, 5.9% in year two, then 6.9% for the remainder of the loan or, Thompson said, refinance prior to year three.

“If the experts are right,” he said, “that person's never going to make a payment in the sixes because interest rates will have come down close to 5% and we would have refinanced down before then. So, a two-for-one buydown option can help with affordability.”

Smith also offered one more piece of advice, reminding potential homebuyers they are allowed to write their home’s interest off their taxes. “I'm not going to say it doesn't matter, but the benefit of being able to write off that additional interest is a wash,” Smith said. “It almost doesn't matter, because that interest deduction can overcome the difference in that increased interest rate.”

BOOKSTORE

CONTINUED from page A1

When Robinson and her husband Jonathan bought Little Professor in 2020, they began looking for a long-term partner to build out a new space. So when Nadeau moved into the former Cahaba Cycles location nearby, the furniture store’s previous space became available, much to the Robinsons’ excitement.

Being across from the Valley Hotel is a great location and the design of the store’s new building will help beautify the city even more, Robinson said.

Aesthetically, in addition to more open space, the new location will offer new shelves similar to those at their Pepper Place store, all-natural surfaces like marble and wood, Robinson said. The changes will make the bookstore more “warm and inviting,” she said.

Robinson said she hopes people not only come to buy books but to sit in the space, to “reset [their] day” and to use it as a space to decompress.

The square footage is about the same, but with less back-of-house space for offices and storage, it will look like more, Robinson said. There will be about 20% more inventory and about 50% more seating space. The children’s area will also have expanded inventory, she said.

The pillar of Little Professor is to be a community hub, Robinson said, not just a place of transaction.

“You walk in and you want to sit and stay,” Robinson said.

Kathleen Wylie has been working at Little Professor for a little more than eight years and is excited to see the store move into its new home.

“I think it will be a good move,” Wylie said.

As customers come into the existing location and hear about the move, they’re excited as well, Wylie said.

There will be some jobs opened up with the new location, Robinson said, though the core team from the existing Homewood location is transferring over.

Having the recently opened second location be helpful during the transition. While there are no plans to have interruptions in the service in Homewood, Robinson said Pepper Place will be available if need be. The store will also continue offering local delivery within five miles.

The downtown location has served as an inspiration for what the owners want with the new Homewood location, Robinson said.

“It feels like a space where we accomplished what we’re trying to do in Homewood,” she said.

The plan is for the new space to open in early spring, Robinson said, but the move itself is 50 years in the making.

Little Professor began at what is now The Cottage Basket, before moving to a building that has since been replaced by the Valley

18th Street location.

People come in to get a book, but they know they’ll be helped by someone who also loves books, Wylie said. Every staff member is knowledgeable and loves reading, she said.

“I really do believe it’s the human element,” Wylie said.

Not only do people connect with staff members, but they also connect with others. Wylie said the staff recently saw a man ask a woman on a date in the store.

“It was so cute,” she said.

The store is a “fun, positive” place, she said. During the COVID-19 pandemic, it served as a respite not only from lockdowns and the loneliness of the pandemic, but a break from the television, Wylie said.

Wylie said.

Robinson said the store has always enjoyed a base of “legacy” customers, in addition to longtime employees like Wylie. So when the Robinsons bought the store, they were “building on a rich history that was already there,” she said.

The “currency” in business, especially at Little Professor, is relationships with customers, Robinson said. The store has become a bit like the bar in “Cheers,” a place “where everybody knows your name.”

“Even if you’re just running in for coffee,” Robinson said.

The hope is that customers walk out feeling brighter than they did before, she said. Customers aren’t being served by an online algorithm but by their fellow Homewood residents.

*Offers cannot be combined, some promotions may be limited to select sets. Not responsible for errors in ad copy. Quantities and selections may vary by location. Mattress images are for illustration purposes only Gifts with purchase (including gift cards and rebates) are not valid with any other promotions except special financing for 6 or 12 months.** Monthly payment is based on purchase price alone excluding tax and delivery charges. Credit purchases subject to credit approval. Other transactions may affect the monthly payment. *** 0% APR for 60 months financing available with purchases of $1999 or over and does not include sales tax. ** The special terms APR of 8.99% will apply to the qualifying purchase, and 48 monthly payments equal to 2.5090%

Summer Camp

Guide B8

Metro Roundup B12

Calendar B14 bedzzzexpress.com

MarCh 2023