/SECURING THE ROLES OF THE FUTURE FOR THE NEXT GENERATION IN AFRICA

07/2023

Equal opportunities: Securing the roles of the future for the next generation in Africa

By improving the continent’s access to reliable connectivity services, even in some of the hardest-toreach communities, we can help even more access quality learning services that will help them develop the skills needed to thrive in the fast-paced digital jobs market.

By Debbie Mavis

Sports tourism: The key to economic development in Africa

Sports tourism can provide opportunities to jump start tourism and travel economy post COVID-19

By Eugene Nizeyimana

4 6 8

Why group buying is a game changer in Ghana’s real estate

By Louisa Afriyie Afrane Okese

26

African startups making an impact in agriculture

Startups are gaining prominence and significance on the African content. It was reported that in 2020, there were an estimated 6,000 African startups and more than $4.5 billion venture capital was raised

By Talent N. Ndlovu

COVER STORY

LOCATIONS

WEST AFRICA

T: +233 055 642 7966 sales.gh@africathinker.com

SOUTHERN AFRICA

Mobile: +263775202251 lnyangoni@gmail.com

TO SUBSCRIBE subscribe@africanthinker.com

CONTACTS

Editorial & media enquiries

Tel: +263 777 324 651 editor@africanthinker.com

Enquiries

Tel +233 055 642 7966 enquiries@africanthinker.com Contact us africanthinker.com/contact

ISSN 2811-1168 is pulished bi-monthly by African Thinker Media Group Limited

The publishers regret that they cannot accept liability for error or omissions contained in the publication however cuased. The opinions and views contained in this publication are not neccesarily those of the publishers. Readers are advised to seek specialist advice before acting on information contained in this publication, which is provided for general use and may not be apporporiate for the reader’s particular circumstances. The ownership of trademarks is acknowledged. Not part of this publication or any of the content thereof may be reproduced, stored in a retrieval system or transmitted in any form without the permission of the publishers in writing. An exemption is hereby granted for extracts used for the purpose of a fair review.

EDITOR’S WORD

Africa’s growing democracy deficit

Since 2020, Africa, in particular central and west Africa has witnessed eight coups, underlining the complexity of democratic governance on the continent and why legitimacy seems far more relevant than elections.

Coups in Mali, Guinea, Burkina Faso, Chad, and Niger have underlined the region’s instability in the wake of threats from insurgents and weak democratic institutions.

Countries under the Economic Community of West African States (Ecowas) bloc were still grappling to deal with the coup in Niger when soldiers in Gabon announced that they had kicked out long time ruler, Ali Bongo Ondimba from power after disputed polls in the oil rich African country.

The coup attempt came hours after Bongo, 64, was declared winner of an election which critics and the opposition called a sham that would have given him a third term.

The Bongo family has been in power in Gabon for 56 years, and Ali’s father, Omar ruled the country Gabon for almost 42 years, from 1967 until his death in 2009.

Gabon formally abolished the one-party state in 1990, and the presidential election on 26 August was the sixth but like the polls before, it was contentious.

According to critics, some of the issues that dogged the poll includes constitutional, legal and electoral changes ahead of the elections severely undermined the integrity of the vote.

The changes, they said appeared designed to give the incumbent the advantage.

Countries in west Africa and the Sahel are seemingly struggling with democratic governance and insurgent threats and the situation is unlikely to change overnight.

In 2021, United Nations secretary general Antonio Guterres decried what he called “an epidemic of coup d’états” on the continent, and that was before the latest insurrections.

While the southern African region has largely seen elections come and go, few of them have passed regional and international norms.

The region has only experienced one coup in recent times, in November 2017 when military chiefs kicked out long time Zimbabwe ruler, the late Robert Mugabe and replaced him with his one-time deputy, Emmerson Mnangagwa.

Mnangagwa’s reelection has been marred by accusations of poll theft, both in 2018 and August this year.

Zimbabwe this week inaugurated Mnangagwa for another five-year term but his election was far from smooth.

Interestingly, the same issues that dogged the Gabonese poll are similar to the allegations that made for flawed elections in Zimbabwe.

Nevers Mumba, who headed the Southern African Development Community’s election observer mission said some aspects of the election failed to meet Zimbabwe’s own laws, the Constitution or regional guidelines.

The failure to distribute ballot papers to cities, including in the capital Harare, showed a mixture of ineptitude and willful incompetence and chaos on the part of election authorities.

In many African countries, it seems, democracy is now defined by whoever holds the reigns of power, but the consequences are sham elections and coups.

Fostering intra-African integration and removing trade barriers will be critical to Africa’s coming economic transformation. Two agreements, in particular, promise to lower production costs, create new value chains, boost domestic demand, and attract global investment.

5G technology could represent an SIP for healthcare, but all of that is hinged upon how fast we can find uses for it and leverage it for the betterment of our society.

By Denver Ncube

By Shaun Jayaratnam

Global economies are facing a situation where in the West, there is a decrease in those falling into the middle class, yet the South and Africa are booming with an explosion of those falling into this class

By Xebiso Blessing Kamudyariwa

By Pascale Ondoa and Yewande Alimi

By Zubaida Mabuno Ismail

Equal opportunities: Securing the roles of the future for the next generation in Africa

quality is defined as ‘the state of being equal, especially in status, rights or opportunities’ but the digital divide is still holding too many people back from securing equal opportunities in employment.

Africa faces a huge digital skills gap which is inhibiting economic opportunities and development.

By Debbie Mavis

According to research from the International Finance Corporation, 230 million jobs across the continent will require digital skills by 2030.

Access to quality education is the key to unlocking this potential and setting up the next generation in Africa for success. To do that, the digital divide must be addressed.

According to the IMF, only 28 per cent of Africans use the internet. By improving the continent’s access to reliable connectivity services, even in some of the hardestto-reach communities, we can help even more access quality learning services that will help them develop the skills needed to thrive in the fast-paced digital jobs market.

Overcoming societal barriers will create new opportunities

The World Economic Forum published a report on The Future of Jobs and Skills in Africa which revealed employers across the region identified an inadequately skilled workforce as a major constraint to their business. Jobs are becoming increasingly reliant on digital technologies and skill shortages in many of Africa’s main industrial areas are due to a lack of technical knowledge,

insufficient training, and access to quality learning.

At Avanti, we believe connectivity has the power to help overcome societal barriers and democratize learning that will boost skills generation.

One such barrier is gender. It is a sad fact that millions of girls in Africa will never complete primary school. At Avanti, we are committed to using our scale and resources to help more girls to build skills for work, increase earnings and participate in the formal economy.

We have partnered with the Global Partnership for Education (GPE) on the Girls’ Education Awareness Program which addresses barriers to girls’ education through targeted, context-specific awareness and information campaigns. Avanti and GPE recognize that girls’ education is a vital force – not only does it transform the lives of girls, but also has a tremendous ripple effect, with impacts ranging from improved health and stronger economies to the creation of a new generation of leaders.

Other barriers include poverty and instability. For both points, it is critical that businesses work in close partnership with governments and NGOs to help those most in need. To help provide more cost-effective connectivity solutions, we are working with local Mobile Network Operators and Tower Companies to drive down some of the significant costs associated with building on-the-ground infrastructure. At the other end of the spectrum, we are working with organisations such as the UNHCR to deliver and install free solar-powered satellite broadband connectivity and laptops to sites in remote and off-grid refugee settlements in Uganda. This connectivity will help open opportunities to better access education that will transform the lives and livelihoods of individuals and communities traditionally left behind.

Why we need to make a stronger case for quality learning

While improving access to education through connectivity is a good first step, to truly make a difference, we need to ensure educational programmes – whether provided by governments, businesses or not-for-profit organisations – are refocused on learning outcomes.

Focusing on outcomes from the outset places greater emphasis on the relevant, practical knowledge and skills to be gained. Without this quality, practical learning, we cannot hope to address the widening digital skills gap that threatens to alienate even more from the workforce.

At Avanti, we have seen first-hand how a greater focus on outcomes can be transformative. We worked with the Foreign, Commonwealth and Development Office (FCDO) to create and lead a consortium delivering project iMlango – a first-of-its-kind e-learning partnership, created to improve educational outcomes in maths literacy and life skills for marginalised children.

The project provides rural and remote schools with

high-speed internet connectivity as well as tailored numeracy content, girls clubs and teacher training. Over the seven years of the project, we have learned how to deliver an education platform that has enabled thousands of students to improve their “maths age” by 18 months on average.

Investing in the young and lifelong learning vital to boost Africa’s economy

Africa has the world’s young–est population, with a median age of 19.7 years old. Young people in Africa account for 60% of all of Africa’s jobless according to the World Bank. This figure is often blurred by Africa’s overall high employment rates, but the bigger picture is that often the work is informal, and many are not able to escape poverty due to low wages and a lack of training and a social safety net.

As one of the youngest populations in the world, it is imperative that adequate steps are taken to invest in young people to ensure they are prepared for the world of work and to help boost the overall economy.

We also believe education doesn’t just stop at school, and people should be able to continue to learn and expand their skills throughout life. This allows these communities to access new working opportunities and gain new skills that they can use in all aspects of life and become specialised in an area of employment that will be expanding across the continent.

We know this because Avanti doesn’t just work with partners to train people in Africa, we employ them ourselves. We are very proud of our diverse and inclusive workforce, with 26 nationalities represented worldwide. We aim to create employment opportunities for local people in all the regions in which we operate and 15% of our workforce is now based in Africa.

At Avanti, we believe connectivity has the power to help overcome societal barriers and democratize learning that will boost skills generation.

Allowing children to access the best education, and adults access the best training, will set them up with vital skills that will help them secure employment.

What more can be done

As the transformation of work unfolds in Africa, policymakers, business leaders and workers must be prepared to work together to help manage this period of transition and fill the gaps in Africa’s skillset. Investment in the younger generations will be key in the future expansion of Africa’s economy and help create a workforce who are prepared for the future of work.

Global inequality needs levelling out and the time has come for connectivity to take centre stage in tackling the education crisis. Satellite technology has the power to ignite real change and we have seen the positive impact that strategic partnerships can have on improving the digital divide, improving levels of education and helping connect millions of communities.

SPORTS TOURISM

Sports tourism:

The key to economic

development in Africa

Of a variety of ways to develop an economy, sports and tourism are major contributors to social and economic development in most countries. There are many types of tourism opportunities that countries invest in, to propel and initiate development strategies. One of such tourism types is sports tourism. Sports and Tourism have a major socio-economic impact, appreciated in most civilian societies, and increasingly recognised by governments and global business communities.

Sports tourism is, and has been in the last decade, one of the growing sectors in tourism across the world. Sporting events attract tourists, participation and supporting business communities in many forms, where host communities exhibit and showcase local culture and talent in diverse forms to distinguish themselves and provide authentic local experiences.

Grand sporting events such as the Olympics, World Cups and Commonwealth Games have been a driving force for tourism development in many countries and leveraged for destination branding, infrastructure development and other economic and social benefits. Research reveals that there are opportunities for sports to be leveraged for the promotion of domestic tourism and culture to drive commercial and economic growth activities.

Sports tourism and the African continent People from several professional backgrounds, athletes, sports management, businesses, authorities and officials of the game, media, creative entrepreneurs, innovators, and audiences, are drawn to host cities as a result of these sporting events. They support to boosts travel, hospitality and night economy as well as the extended support service provision and the entertainments. The activities associated with such events create enormous opportunities for the tourism and related industries. A great example in Africa are the 1995 World Cup and 2010 FIFA World Cup in South Africa. The Commonwealth Games 2022 in Birmingham was a golden opportunity and unique moment to strengthen existing UK-Africa relationships, open new links and build legacy. The event has supported to unlock multiple opportunities to drive and increase regional (specifically the Midlands) commercial connectivity, relationships and strengthen economic ties, boost trade and investment. In addition, has accelerated innovation and cross border entrepreneurship. Furthermore, initiatives such as African Business Chamber (AfBC) Midlands – Africa Business Forum hosted during The Games, supported by several partners Sports tourism can provide opportunities to jump start tourism and travel economy post COVID-19, harness community togetherness, accelerate cultural and diaspora linkages with African countries

By Eugene Nizeyimana

including Brand South Africa and government officials from Kenya, Uganda, Ghana etc are great platforms to harness continued discussions, showcase economic opportunities, drive trade actions, investment flow, cultural relations and international stakeholders’ engagement highlighted by Eugene Nizeyimana, Pumela SalelaUK Country Head, Brand South Africa and other guest speakers at the forum.

These events can generate significant opportunities in many sectors of the economy to achieve legacy and longterm benefits, including engineering, real estate, creative, technology, education, visitor economy, business services, mobility, hospitality, culture and innovation so on. Also, they involve significant expenditures for facilities, infrastructure construction and maintenance, and service personnel that support to create employment, new talent pools and skills. Additionally, substantial revenues are generated through various fees, concessions, television rights, tickets, Intellectual Properties (IP) and marketing promotion of consumer goods and services.

Based on several studies and outcome reports from past events in host nations, hosting rights affords the opportunities to increase tourism revenues that sporting events drive. African nations may not have been fortunate enough to earn their share of the benefits of hosting these major global events, which would have allowed them to gain significantly from the associated tourism and businesses to boost the economic prospects, standard of life, created more employment opportunities and the general well-being of African countries.

Sports tourism can provide opportunities to jump start tourism and travel economy post COVID-19, harness community togetherness, accelerate cultural and diaspora linkages with African countries during the games and beyond. Sports Ministers across the African Continent, such as H.E Nathi Mthethwa - Minister of Sport, Arts and Culture, Government of South Africa have been highlighting the importance of leveraging global sports and cultural events such as The Commonwealth Games to drive long-term economic benefits for sustainable growth and development and further promote South Africa to the world as a sport, cultural and tourism hub. African countries, business communities, investors, sports professionals, and the diaspora communities must pool resources and work collectively to bid for such global sporting events to be held in continent. The key steps are to establish strong economic environment, robust infrastructure and provision of sufficient investment for sporting activities to ensure a stable political economy, safety and strengthened participation if they are to host such events successfully. Furthermore, support upcoming 2023 Netball World Cup in South Africa and the 2025 world road cycling championships in Rwanda.

Sports tourism: The key to

UK.

Commonwealth Games - Athletics

- Women’s 4 x 100m Relay - FinalAlexander Stadium, Birmingham, Britain - August 7, 2022

Nigeria’s Nzubechi Grace Nwokocha and England’s Daryll Neita in action during the final REUTERS/John Sibley/File Photo

Photo:

Cyclists compete at the 2022 Commonwealth games in the

Getty Images

Why group buying is a game changer in Ghana’s real estate

By Louisa Afriyie Afrane Okese

With Ghana on its way to economic resurgence, exploring different options to reach your life’s goals are highly critical to the finances of individuals looking to be home-owners. It is even more crucial, with increasing inflation on various goods, for individuals with a dream to own a home to explore the option of group buying.

Group buying is an exciting new trend gathering attention from stakeholders in the real estate market across the globe. Uncommon to the Ghanaian society, this may well be the ticket owning your dream home. The idea is to have a group of like-minded friends or family, with a mutual goal of owning a home, to pool their resources together. These days, group buying has become worthwhile for home buyers looking forward to getting significant discounts. It is about time Ghanaians explored that option.

Group buying offers the opportunity to approach real estate developers either directly or through an agent to negotiate prices, land sizes, home spaces, discounts, among others, which would otherwise be impossible for individual home buyers to achieve. This new trend has worked well since it ignited, and it is spreading like wildfire. It is seen as a win-win proposition.

The two biggest parts of the entire process is the desire of the home buyers and the negotiation. Once potential home buyers are set, they may connect through a third-party agent or a brokerage company and form a group. The company then goes to the developer with orders and negotiates for possible discounts. The developer, sensing a ready market to sell some properties, would agree to the discount or propose one. Normally, there is negotiation on discount which is higher than what is offered on individual purchase basis.

For buyers, instead of waiting for offers, would look to grow the buyers group size to build cumulative bargaining power. This presents a rich market size to negotiate better discount rates or price drops.

Group buying offers the opportunity to approach real estate developers either directly or through an agent to negotiate prices

For developers, a ready market to sell many properties without spending anything on customer acquisition, advertising and marketing in general, is a dream and a gamechanger as they get to reduce the cost of selling. These savings on brand marketing can be transferred onto the home buyers as extra discount. It makes absolute sense to negotiate with groups of buyers and strike a deal that brings in substantial amounts of much-needed liquidity immediately than approaching single potential buyers at huge, committed marketing expenses. It affords developers the chance to sell faster and invest into other real estate immediately.

For majority of Ghanaians, real estate is the most expensive purchase they will ever make and payment options such as homes loans and mortgages are still misunderstood. Hence, the individual’s reluctance to find suitable options to buy a home. Even so when the economy is quite volatile under the circumstances. Before jump straight into a group purchase, make sure you understand the terms and intricacies of the negotiations and discounts.

Photo by Faith Lehman on Unsplash

Investing in Africa’s Health

COVID-19 has reversed some of the progress made in the fight to eradicate AIDS, malaria, and tuberculosis in Africa. But, despite high inflation and an uncertain economic outlook, African governments can take several steps to strengthen local health systems and bolster the continent’s defenses against future epidemics.

There was a time, not so long ago, when an HIV diagnosis was a death sentence. AIDS, together with tuberculosis and malaria, killed millions of people and overwhelmed health systems worldwide – especially in Africa.

But the world came together and fought back. The Global Fund to Fight AIDS, Tuberculosis, and Malaria, established in 2002, is an unparalleled success story. Cooperation between developed and developing countries, the private sector, civil society, and affected communities has saved 44 million lives, and the combined death rate from these three diseases has been reduced by more than half.

Saving these many lives has had a huge economic impact. The Global Fund estimates that an investment of $1 through the health programs it supports will result in $31 in health gains and economic returns over three years. And since most of its investments are in Africa, the benefits will spread across the continent. But the COVID-19 pandemic curtailed this rapid progress.

While the death rate on the continent has not been as catastrophic as many feared, the pandemic has had a profoundly negative impact on Africa’s health systems and on the fight against AIDS, TB, and malaria. Testing, diagnosis, and treatment for these diseases have been severely affected, threatening the gains made in previous decades. Worldwide deaths from malaria, for example, increased by 13% in 2020, to a level not seen since 2012.

Unless things change, the gap in health and economic outcomes between Africa and the rest of the world will widen. Overseas aid remains vital. If we are to reverse the losses created by the pandemic and continue to do lifesaving work, the Global Fund needs to meet its fundraising target of $18 billion over the next three years.

The Fund’s Replenishment Conference this month will bring together representatives from donor countries, the private sector, and civil-society groups seeking to renew commitments and ensure overarching support for the fight against AIDS, TB, and malaria. But domestic investment is also crucial for securing health sustainability, especially given the impact of recent global shocks on both advanced and emerging economies.

To this end, the Global Fund supports initiatives like the African Union’s African Leadership Meeting (ALM), which advocates for increased domestic resources for health. While the Global North can look forward to the post-COVID economic recovery, Africa is still lagging behind the rest of the world in vaccine access and uptake.

The continent will need more time to recover fully from the pandemic. How, then, in the face of an uncertain economic outlook – with African GDP dropping, inflation rising, and food and energy costs soaring – can governments realistically increase health spending?

By Donald P. Kaberuka

While there is no silver bullet, we have identified several actions that governments can take to promote investment in the health sector. For starters, economic recovery is a virtuous circle: GDP growth enables great-

er investment in health, and a healthier population is more productive.

The next few years could be challenging as the longer-term consequences of the pandemic and the ripple effects of the war in Ukraine adversely affect investment and trade. But fully implementing initiatives like the African Continental Free Trade Area (AfCFTA) could help reduce Africa’s dependency on food and fuel imports. Another way to prop up local health systems would be to increase tax revenues.

Many African governments face a significant “tax gap” – the difference between what their tax laws should, in theory, deliver and what governments manage to collect. Removing loopholes and reinforcing the efficacy of tax administration are powerful ways to make more money available for health. Governments should also allocate more funds to public health.

Very few African countries currently devote 15% of their national budgets to the health sector – the target set by the 2001 Abuja Declaration. This, in turn, impedes their ability to ramp up efforts to eradicate AIDS, TB, malaria, and other epidemics, and thus reduces their chances of achieving the 2030 Sustainable Development Goals (SDGs).

Below:

In Magude district in southern Mozambique, Zaidina Antonio Zwane gives her 2-year-old son Ernesto a glass of water to wash down his malaria treatment.

TOMMY TRENCHARD/ PANOS PICTURES/ REDUX

The private sector must do its part as well, whether through corporate taxes, employer-led health insurance, or workplace health schemes. Private companies benefit enormously from a healthier population and – as we have seen during the COVID-19 pandemic – can suffer dramatic losses when infectious diseases run wild.

Of course, it is also important to make health spending more efficient. This would involve coordination between finance and health ministries.

Finance ministries can support planning, budgeting, and spending by providing a clear indication of available resources over the medium term and by being responsive to changing needs, including health emergencies.

Meanwhile, health ministries can design more streamlined and cost-effective public programs. Pulling these levers requires political leadership and sustained effort. The Global Fund directly supports African communities and governments as they work to strengthen local health systems.

But only a combination of international aid and domestic financing can turbocharge the efforts to eliminate AIDS, TB, and malaria by 2030. And only by ending these epidemics can we propel Africa’s economies, bolster the world’s defenses against future outbreaks, and free millions from the burden of disease.

Answering the challenges posed by antimicrobial resistance

Africa, like every other continent, has an AMR problem. But Africa stands out because we have not invested in the capacity and resources needed to determine the scope of the problem, or how to fix it.

The World Health Organization (WHO) has repeatedly stated that AMR is a global health priority—and is in fact one of the leading public health threats of the 21st century. A recent study estimated that in 2019, nearly 1.3 million people died because of antimicrobial resistant bacterial infections, with Africa bearing the greatest burden of deaths. A high prevalence of AMR has also been identified in foodborne pathogens isolated from animals and animal products in Africa.

By Pascale Ondoa and Yewande Alimi

Staphylococcus aureus is the source of a skin infection that can turn deadly if drug resistant. Estimates regarding the most common resistant variation, methicillin-resistant Staphylococcus aureus (MRSA), exceed 100,000 deaths globally in 2019.

But up until recently, we did not have a solid grasp on how much of a problem MRSA—or any other antimicrobial resistant pathogen—was in Africa. It turns out, after testing 187,000 samples from 14 countries for antibiotic resistance, our colleagues found that 40% of all Staph infections were MRSA.

Africa, like every other continent, has an AMR problem. But Africa stands out because we have not invested in the capacity and resources needed to determine the scope of the problem, or how to fix it. Take MRSA. We still don’t know what’s causing the bacteria to become resistant, nor do we know the full extent of the problem.

We are failing to take AMR seriously, perhaps because it is not glamorous and relatable. The technology that we currently use to identify resistant pathogens is not fancy or futuristic looking. Combatting AMR does not involve miracle drugs, expensive treatments, or fancy diagnostic tests. Instead, we have bacteria and other pathogens that are commonplace and have learned how to shrug off the good old medicines that used to work.

The global health and pharmaceutical industries do not seem to consider solving this problem to be very profitable. Compare that to the urgency of solving COVID-19, which has been embraced—and interventions such as diagnostics subsidized—by governments eager to end the pandemic. The COVID-19 response has been characterized by innovations popping up literally every other week.

Why can’t we mobilize resources and passion for AMR? Are resistant pathogens too boring? Is it too difficult to solve through innovations? Does this make prospects for quick wins and fast return on investment too elusive for AMR, especially when compared to COVID-19 or other infectious disease outbreaks?

Collectively, these numbers suggest that the burden of AMR might be on the level of—or greater than—that of HIV/AIDS or COVID-19. The growing threat of AMR is likely to take a heavy toll on Africa’s health systems and poses a major threat to progress made in attaining public health goals set by individual nations, the African Union and the United Nations. And the paucity of accurate AMR information limits our ability to understand how well commonly used antimicrobials actually work. This also means we cannot determine the drivers of AMR infections and design effective interventions in response.

We have just wrapped up a project that gathered data on many of the scariest pathogens in 14 countries, revealing stark insights on the under-detected and under-reported depth of the AMR crisis across Africa. Less than two percent of the medical laboratories in the 14 countries examined can conduct bacteriology testing, even with conventional methods that were developed more than 30 years ago.

While providing national stakeholders with critical information to advance their policies on AMR, we have also trained and provided basic electronic tools to more than 300 health professionals to continue this important surveillance. While a strengthened workforce is critical, many health facilities on the continent are coping with interrupted access to electricity, poor connectivity, and serious, ongoing workforce shortages.

Our work has painted the dire reality of the AMR surveillance situation, informing concrete recommendations for improvement that align with the new continental public health ambition of the African Union and Africa Center for Disease Control (CDC). The challenge is to find the funding to expand this initiative to cover the entire African continent.

AMR containment requires a long-term focus—especially in Africa, where health systems are chronically underfunded, while also being disproportionately challenged by infectious threats. More funding needs to be dedicated to the problem and this cannot only come from international aid.

We urge African governments to honour past commitments and allocate more domestic funding to their health systems in general, and to solving the crisis of AMR in particular. We also call upon bilateral funders and global stakeholders to focus their priorities on improving the health of African peoples. This might require more attention to locally relevant evidence to inform investments and less attention to profit-driven market interventions, as well as prioritizing the scale-up of technologies and strategies proven to work, whether or not they are innovations. Containing AMR means we have to fix African health systems. The work starts now.

Photo by Mike Von on Unsplash

The key to unlocking Africa’s economic potential

Fostering intra-African integration and removing trade barriers will be critical to Africa’s coming economic transformation. Two agreements, in particular, promise to lower production costs, create new value chains, boost domestic demand, and attract global investment.

Africa is on the cusp of an economic transformation. By 2050, consumer and business spending on the continent is expected to reach roughly $16.1 trillion. The coming boom offers tremendous opportunities for global businesses – especially US companies looking for new markets. But unless African policymakers re-

move existing barriers to regional trade and investment, the continent’s economy will struggle to reach its true potential.

Two major trade agreements – the African Growth and Opportunity Act (AGOA) and the African Continental Free Trade Area (AfCFTA) – will make it easier for African countries to trade with one another, and with the United States. Together, the agreements promise to remove longstanding impediments to industrialization.

AGOA, passed by the US Congress in 2000, gives countries in Sub-Saharan Africa preferential trade access, allowing them to export tariff-free products to the US. Although it will expire in 2025, US President Joe Biden’s Sub-Saharan Africa strategy, unveiled in August, highlights its positive impact and promises to work with Congress on ways to proceed after AGOA lapses.

AfCFTA, on the other hand, is an intra-African trade agreement with no expiration date. Established in 2018, its goal is to deepen trade ties between African countries by removing tariff and non-tariff barriers.

Although these agreements’ scope, focus, beneficiaries, and structure differ significantly from each other, they are essential to strengthening African regional in-

tegration. Rather than viewing them as separate or competing agreements, policymakers and investors should recognize how they can complement each other in creating, sustaining, and transforming value chains across the continent.

Value creation is critical to Africa’s economic transformation. In 2014, manufactured goods accounted for about 41.9% of the trade between African countries, compared to 14.8% of their exports to the rest of the world. Greater regional integration will provide Africa with a larger supply market, which will accelerate manufacturing specialization and make African producers more competitive globally. More robust manufacturing industries will provide jobs for low-skilled workers – particularly those not currently integrated into the formal economy. This, in turn, will increase average household incomes, boost domestic demand, spur innovation and diversification, and help protect local economies against external shocks.

AGOA has already created some opportunities for cross-border value chains. Yet despite some success stories like Madagascar’s apparel industry, which relies on an extensive regional supply chain, such opportunities remain limited. While integration has improved since AGOA’s implementation, particularly since 2015, it remains somewhat superficial: less than 17% of Africa’s commercial value is currently generated through intra-African trade.

The real game changer is the AfCFTA. By removing tariffs for a wide range of products across the continent, it will lower production costs and shift foreign direct investment toward manufactured goods, while also reducing transit costs and shortening supply chains – major benefits in a globalized economy.

The International Monetary Fund projects that, under the AfCFTA, Africa’s expanded goods and labor markets will become more efficient, driving a significant increase in African countries’ competitiveness. By creating a true continental market that increases intra-African trade and impels African countries to participate in “production sharing” at a higher rate, the AfCFTA will likely provide a further incentive to US-based multinationals, which will be able to access a larger market and establish a major global hub. AGOA has already spurred many companies to invest in Africa, and the successful implementation of the AfCFTA will strengthen this trend.

The challenge for policymakers is to accelerate this process and ensure that the two programs complement each other. One way to do this is to deepen and broaden communication channels between Africa and the US, making it easier for investors interested in doing business in Africa to be better prepared for the expected growth in demand for regionally-sourced products.

IMF projects that, under the AfCFTA, Africa’s expanded goods and labor markets will become more efficient

Supporting individual countries in implementing the AfCFTA would also help streamline the process.

A key problem that remains to be addressed is AGOA’s eligibility criteria, which are set on a country-by-country basis. These criteria can be detrimental to regional integration, as one country’s removal could affect another country’s supply inputs, thereby creating a ripple effect. For example, when Madagascar was removed from the AGOA-eligible list in 2010 following a coup d’état, the five African countries from which it had been sourcing apparel inputs were also punished. Considering the broader effect of country-specific sanctions will help prevent unintended investor risk. Effective regional integration is essential for Africa. Without it, the continent will continue to be overlooked and outpaced globally in manufacturing, information technologies, and agriculture. When considering the future configuration of both AGOA and the AfCFTA, policymakers should regard them as complementary mechanisms for ensuring Africa’s long-term economic development.

The simple steel box changing lives in Ghana

The adaka billa (small box) – is a communal savings box that helps small groups in villages across Ghana save and manage their money.

Memunatu Salifu, in her late fifties, sits in the centre of her courtyard in the small town of Sagnerigu in Ghana’s northern region, functioning as a makeshift kitchen for her daughter-in-law.

By Zubaida Mabuno Ismail

She wakes up early to get ready for the day before heading to the local shea processing centre to process the order for the week, the family’s economic lifeline. She is about to be served her favourite morning meal;tuo-zaafi,a local staple composed of maize and eaten with a green vegetable soup called ayoyo.

Her daughter-in-law, too, rises early to prepare the meal that will keep off Salifu’s hunger pangs for the better part of the day.

As Salifu waits for her daughter-in-law, her son is busy getting ready for the local market where he will trade his fowls, his contribution to the upkeep of the family. He emits a high-pitched sound to entice the fowl with grains to capture the big ones.

Salifu, a widow and mother of five, is, by all means, living comfortably compared to many in the village; she has a business and a five-bedroomed house. Though the house is not fully complete, she is spared the constant anxiety of struggling to raise the monthly rent.

At the processing centre, other women, most of them shea seed sellers, tell her how lucky she is.

“Naawuni zogo, nyin gbam ma. Ti gba di nya ayili maa, ti na vogue (Salifu, you are a lucky woman… we wished we had a house like yours).”

But she often off dismisses such remarks when she looks back at what she went through after her husband died; left on her own– and still grieving— with five children to feed, clothe, and send to school and on top of that, pay rent, she was not sure what the fate had in store for her.

Salifu says she faced each day, one day at a time. Her one source of security was a little metal box.

The adaka billa (small box) – is a communal savings box that helps small groups in villages across Ghana save and manage their money. It functions as a village microbank and is changing lives and empowering many in rural communities, especially women.

Though it was initially introduced among women small-scale traders to save and borrow at minimal interest, it has opened its doors to all people– the unbanked majority in both rural and urban communities – who not only lack access to banking but collateral to borrow from formal institutions.

For Salifu, it has been a slow but progressive journey. She borrowed from the Idaka billa to buy the land on which she later built her home when her spouse was alive.

As she started building, she ran out of money before she could roof it. She went back to the little steel box to borrow more to complete her project.

“I borrowed money with interest from the adaka billa and used it to buy two bundles of roofing sheets; my son likewise bought two bundles, and we managed to roof the house and move in,” said Salifu.

Salifu isn’t the only one who has been spared the humiliation of financial insecurity. The steel box, according to small-time trader Sanatu Mohammed, enabled her to purchase school supplies for her child to enrol in high school.

“I borrowed money from the box to buy groceries for my last child who had earned admission to Tamale Senior High School last year,” she said.

While Salifu is widowed, Mohammed is dealing with the cost of care for a bedridden husband and children, and no amount of money could be spared. Both Salifu and Mohammed are petty traders, and their lives rotate around their daily sales and building up their savings to enable them to invest.

The Sagnerigu residents are beneficiaries of the little steel banking system run by 90 women.

“This system allows us to start small and grow our little savings from our daily sales. Borrow to address immediate family needs such as school fees, medical expenses, expand business or invest in income generating projects,” said Mohammed.

“It is also our fallback insurance when crops fail because of rain and we have a food shortage.”

According to the project coordinator, Tahindu Damba, the idea, which targeted women, was to inculcate in them a culture of saving and investment in a community plagued by financial challenges despite their hard work.

“The traders were living from hand to mouth because they had no idea how to save. So, we helped them to enhance the money box concept, which some of them were trying to use,” said Damba.

However, the conventional money box in Ghanaian homes lacked security features. A steel box was to be fabricated by a local welder.

“We were advised that if we saved in a bank, we would need three signatories to offer optimal safety for our savings. So, we localised the concept, purchased three padlocks, and distributed the keys to three distinct women,” Salifu revealed.

A daily saving of 2 Ghanaian cedis (GHS), the equivalent of 20 US cents, was decided upon by the women. Salifu says she had saved up to GHS 300 (nearly US$30), making her eligible to borrow to complete her project.

However, the purpose of adaka billa goes beyond just advancing individual goals. It also provides a sense of agency and control over their lives, for the women, according to one of group’s leaders, Abiba Zakaria.

“We utilise our funds to address our immediate needs and investments. It has really changed our lives,” she explained.

To keep track of their daily savings, all members are provided with a booklet to record either their daily or weekly savings. Initially, this was a challenge, but with

The simple steel box changing lives in Ghana

$32,500

Male artisans, with a membership of 90 saved a total of GHS 324,000 (nearly US$ 32,500).

time the members have become adept bookkeepers.

“We were taught how to record our daily savings and how to deposit the money in ‘our bank’ each week,” said Salifu.

Saving money in a money box is nothing new in Ghana. The moneybox challenge, which is largely for those who live more comfortably and can afford to pour a few cedis into the box, is a social media phenomenon in which groups of women show off their savings at the end of the year.

Unlike other saving practices, however, the adaka billa sees the box handed to one member of the group each month, rather than personal savings being kept in the home. The small box provides choices and security.

Over a thousand people are currently involved in the adaka billa movement throughout the north, from shea processors to tailors, mechanics, food vendors and commercial vehicle owners.

For Salifu and the Pasung Sha Processing community in downtown Sagnerigu, it has cured them of endless anxiety about school fees and medical expenses for themselves and family.

Though initially a project for the small-scale women traders, adaka billa has spread and embraced people across the informal economy.

Last year, the three groups comprised of male artisans, with a membership of 90 saved a total of …. GHS 324, 000.00 (nearly US$ 32,500). Each member’s daily average was between GHS 10 and GHS 50.

“With the money I saved last year, I took it and bought a 13-seater bus, locally known as 207 which has boosted my economic power, ” said Alhassan Yakubu, a vehicle mechanic

The adaka billa is spreading beyond Sagnerigu to the neighbouring Abofu communities in the Ashanti region and parts of the Bono region, all in northern Ghana.

“I believe that in the near future, the little steel box system will soon be the first port of call for those in the formal sector who need to borrow money. Perhaps, it could even lend money to the government,” concluded Damba, with a smile. Bird Story Agency

Africa is paying dearly for the Russian-Ukraine conflict

Inflation, recession and possibly a global recession - these are words haunting the best of us of late.

By Shaun Jayaratnam

These fears have dominated the trade with equity markets and affected nearly all commodities. As consumers are faced with rising food and fuel prices many are cutting back on purchases, demand taking a back seat as fears of recession continues to impede consumer confidence to spend.

In the beginning of July crude oil price tumbled hard 10% down and broke the USD100/barrel mark. Industrial metals were also on a melt down with copper, aluminium, zinc all also had fair share of price drop from their recent record highs.

Additionally, a sharp rally in the U.S. dollar was also seen as negative for commodity futures. Euro at the lowest level against USD since 2002, Yen sinks near 24 years low again.

Is there any good news, anything to look forward to? Doubtful, unless there’s an end to the war in Ukraine. An end to the war without a pull out of Russian troops or with Russia still controlling the supply chain may just make things worse.

But hold on, following lengthy negotiations mediated by Turkey and the UN, Russia has agreed to unblock Ukrainian ports to allow the export of grain. Since then, approximately 30 vessels have left the largest Ukrainian ports in the Black Sea.

Fundamentally, this is bearish news as it said there’s still a minimum of 20 million to 25 million metric tonnes of last season grains crop that is yet to be released to the world. This is on top of this season crop, with sunflower seed and wheat currently being harvested now with corn harvesting starting in September. If all goes well, this will also mean

Russian fertilisers would also be able to find her way out of the Black Sea ports. This is positive news for next season plantings.

While the fear of fertiliser shortage has somewhat disappeared, at least for now, but the cost for next planting season certainly have risen by over 150%.

The US economy is slowing. US inflation rate was an average of 3% per annum for several years but accelerated to over 40 years high of 9.1% in June 2022, falling to 8.5% in July. US Fed raised interest rate for the 4th time so far this year, amounting to a total of 225 bps thus far. Some expect Federal Open Market Committee (FOMC) to raise rates by another 100-150 basis points during the remaining months of 2022.

Sluggish demand in China is pulling down Asia equities. China GDP is expected to post its lowest quarterly growth rate in more than 2 years. With mounting Covid-19 costs, soft consumer spending, slower manufacturing activities; economist are sceptical even a rebound in 2nd half of 2022 China may not be able to achieve her minimum 5.5% growth target. With China off-take predicted to fall further, global demand for feeds is not likely to increase.

With 2022 Africa regional inflation expected to be at 12.2 percent and 2023 projected at 9.6 percent, the effect of the war is starting to impact growth

Premier Li was quick to announce a $75 billion infrastructure pending/stimulus plan to revive the flagging Chinese economy. However, it’s unlikely to reverse global metals meltdown. Unlike in the past where Chinese stimulus played major role in rescuing industrial commodities from the slumps in 2008, 2015 and arguable in 2020, there appears to be more caution this time.

These extra funds from special bonds sales will likely be used to plug Covid-era budget gaps and won’t tackle the bigger issue for metals demand as China real estate is still in the grip of a long downturn and the scale of infrastructure spending is uncertain along with export demand that global recession which may slow down factory output.

As China continues to see sporadic outbreaks of Covid-19 virus and pursues a zero Covid policy, this year’s stimulus will be certainly weaker than the previous ones. Poor Chinese manufacturing index indicate that China economy continue to be challenging, prompting crude oil to crack below the $100/barrel range citing poor future economy growth.

All of this is a severe and exogenous shock to countries across the African continent. The continent’s policy makers are not well position for more shocks when existing policies has always been a juggling act between more development spending, increasing tax revenues, and ever-increasing debt settlement.

Many African countries depend on Russia and Ukraine for most staples. The sanctions and blockage of exports caused by the war has resulted in a surge in food and fuel prices threatening economic outlook. Several

African countries, including Angola, Nigeria and South Africa, export a substantial volume of their raw mineral to China.

China’s industrial slowdown has halted demand for these materials. As a result, imports from Africa to China disrupted and prices fell, ultimately resulting in production cuts, heavy losses in export earnings and an exacerbated trade deficit for African economies.

Just when Africa was starting to slowly recover from the economic slowdown caused by Covid-19 pandemic it’s now facing another daunting challenge.

Around 85 percent of the region’s wheat supplies are imported. Input costs in the sub-Saharan African region have been on an upward trend since mid-2021, driven by increasing global commodity prices. The war amplified the global input costs rise and ultimately price pressures for food, crude oil, and fertilizers given Russia and Ukraine’s prominence in the global supply of these commodities.

Higher fuel and fertilizer prices are already affecting domestic food production within the continent and outside of it. Africa’s oil-importing fragile states will be hit hardest, worsening trade imbalances, increasing transport and other consumer cost.

Most currencies in the sub-Saharan African region had weakened against the US dollar by the second quarter of 2022 due to US dollar resilience, a worsening overall current account position as import demand for fuel and food grew, and tighter global financial market conditions. The Ghana cedi has depreciated by 35 percent against the US dollar this year, making it the second worst-performing currency in the world. Furious borrowing has seen Ghana’s debt-to-GDP ratio soar to almost 85%.

More than 50% of sub-Saharan African countries in IHS Markit’s medium-term sovereign risk score series are ranked in the Actual or Possible Default Scenarios category. Moody’s David Rogovic said in a Reuters report dated July 16th, 2022, that Kenya, Egypt, Tunisia and Ghana are the most vulnerable just because of the amount of debt coming due relative to reserves, and the fiscal challenges in terms of stabilising debt burdens.

With 2022 Africa regional inflation expected to be at 12.2 percent and 2023 projected at 9.6 percent, the effect of the war is starting to impact growth, erode standards of living and macroeconomic imbalances.

According to IMF Managing Director Kristalina Georgieva, “the war further exacerbates pre-existing price and food supply pressures. Some countries and regions, which were already food insecure and facing emergencies, are now confronting additional price increases and supply disruptions for imported food, fuel, and fertilisers. Early estimates suggest that at least 10 million more people could be pushed into poverty in Sub-Saha-

Africa is paying dearly for the Russian-Ukraine conflict

ran Africa due to higher food prices alone.”

Policy makers need to formulate policies to address these challenges to protect the most vulnerable households. But - How does Africa get her economies back on track? How does she finance the recovery? How does she address inequality? Start replacing the short-term myopic view with long-term future focused policies and regional cooperation.

The war further exacerbates pre-existing price and food supply pressures. Some countries and regions, which were already food insecure and facing emergencies, are now confronting additional price increases and supply disruptions for imported food, fuel, and fertilisers.

IMF Managing Director Kristalina Georgieva

IMAGE: TURKISH DEFENCE MINISTRY/ REUTERS

Middle Class in Africa

Global economies are facing a situation where in the West, there is a decrease in those falling into the middle class, yet the South and Africa are booming with an explosion of those falling into this class

The concept of a growing middle class especially in Africa has become fashionable in recent years. After all, a strong middle class is a good indicator of a stable society. They drive consumerism, promote economic growth and prosperity, while encouraging investment and entrepreneurship. As a collective they can bring about better governance, higher education expectations and where possible political stability. In Africa, South Africa has stood as a strong example of democracy and stability and a cursory examination of the country seems to confirm this construct, yet a deeper look shows that this is more of a Western ideal than reality on the ground.

Global economies are facing a situation where in the West, there is a decrease in those falling into the middle class, yet the South and Africa are booming with an explosion of those falling into this class. In Africa especially, this seems to suggest that a narrative of development and opportunity in the continent has been spun, convincing many that they are middle class and better off than what they actually are.

By Xebiso Blessing Kamudyariwa

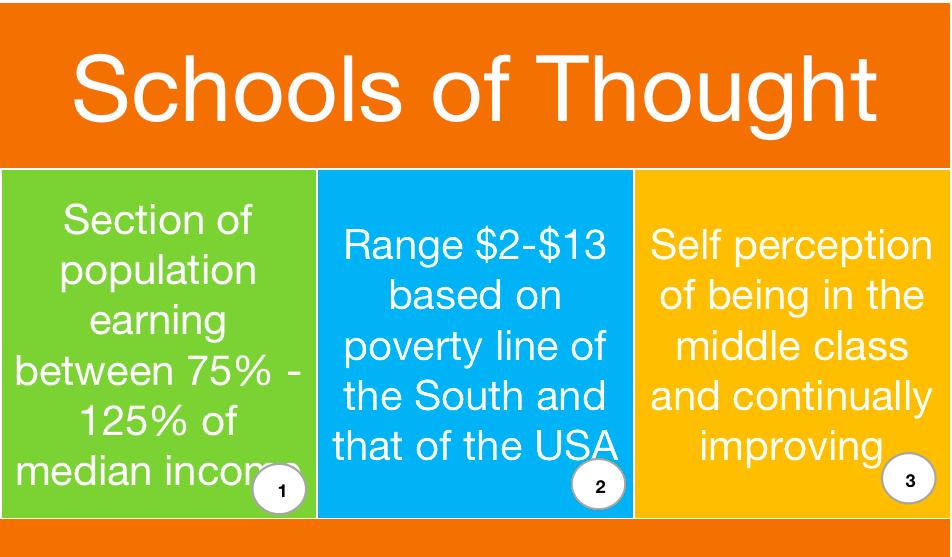

A pertinent issue becomes that of defining the middle class. Does it actually exist in Africa? If it does in what form? Can its construct truly be compared to that of the Western world? In 2012, the African Development Bank (ADB) put the number of people in the middle class at about 300 to 500 million people, approximately a third of the continent’s population. How is such a number derived, what criteria enter individuals into the middle class? In South Africa the numbers of the middle class have at times even been touted as above 50% of the population yet the extent of poverty and the country’s fall in Gini coefficient seem to belie this supposed fact.

Most definitions of the middle class are built from Marxist or Weberian theory. The former classifies according to those to work for themselves and are owners or propertied, while the other looks at characteristics such as education and income. Both these theories though fail to properly accommodate the exact context in which Africa finds itself. In truth, no specific theory has been able to properly classify the middle class in Africa as it is still a developing concept.

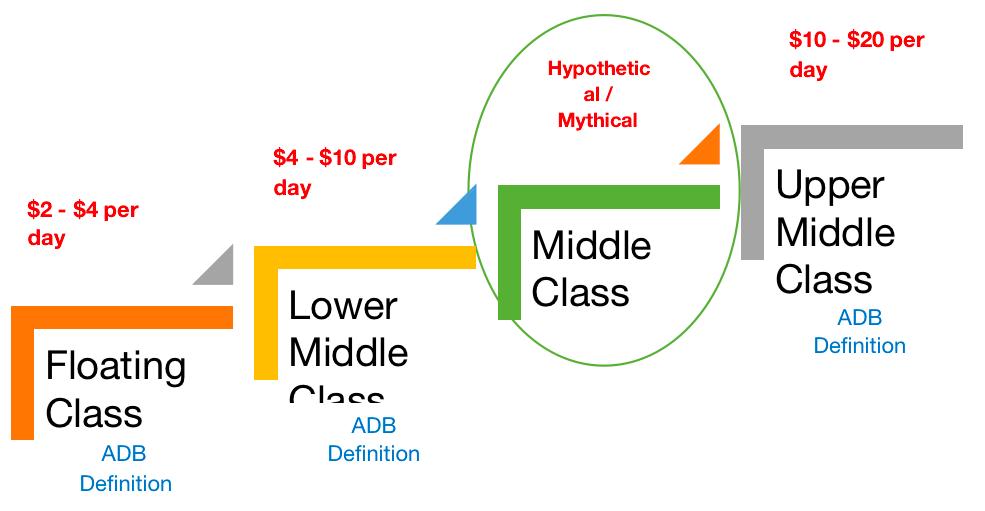

AfDB defines economic categories as shown below while various authors define the middle class as hypothetical or even mythical. Defining the middle class as starting from those with a daily expenditure of $2 (this is at 2005 PPP[ PPP – Purchasing Power Parity] US dollars, could be estimated at $2.94 today) requires quite a stretch of the imagination in South Africa. Many in the floating category defined as emerging middle class are simply at not starving status and easily fall back into the poor category. With rising inflation and a declining economy, the lower middle class finds itself at risk each day, barely surviving.

The upper middle class by this categorisation are a part of the population that are currently finding themselves over indebted, unable to save and likely just about making ends meet.

A more realistic economic definition of the middle class keeping the Western context in mind could be that found in Credit Suisse’s Global Wealth report that considers middle class as individual wealth between US$50,000 and US$500,000. This categorisation drastically reduces the continent’s middle class to about only 18.8 million people. While this would be a third of South Africa’s population, SA makes up only 5% of the continent’s population.

From the schools of thought below, the more accurate middle-class definition would be that using median income. In South Africa for example, the median income is just under R30,000, at almost $2,000. They can truly be counted as consumers and driving entrepreneurship. They are typically educated, have a car, own property and for many, work in the public sector. The development of this class has been well noted especially in racial terms with the majority of this class shifting to black as opposed to white. As of 2012, using these criteria, of the 8,3 million people making up the middle class 4,2 million were black. This the group which will be referred to as the middle class moving forward as they more closely meet the original Western construct of the middle class.

In recent years, various studies have shown the shrinking of the middle class and with it an accompanying downturn of South Africa’s fortunes. The question is, is there a causal relationship or it is more of correlation? In South Africa, does the middle class actually play the role its purported to or there are other factors at play? Are

there similar patterns in other strong economies on the continent to make this more of an African trend than an isolated occurrence?

Over the last 2 years, stability has become a concept that many more are grappling with regardless of their income status. Besides simple bread and butter issues, more are reconsidering their thoughts on the economic and political future of South Africa. With incomes reduced, livelihoods lost, for many it feels like the struggle has just begun. Where before there was hope, it looks as though reduced circumstances are here to stay and things will not be better for a while if ever at all.

While it is always expected that the poor are especially vulnerable to shocks, the pandemic has shown that things are not so clear cut. The middle class, the one class expected to be able to weather shocks, to have savings, generally live an easier life has suffered unexpected setbacks from prior to covid. Some who were living relatively comfortable lives before found themselves with their income completely gone or drastically reduced. This is a trend that goes beyond the private sector as government has also found itself in dire straits in its various parastatals.

Unfortunately for South Africa, its middle class is not sitting back and patiently waiting for things to improve. With only about 30% of the middleclass believing things will improve, about 27% are looking to emigrate within the next 5 years.

Statistics show worry over this class was becoming a focal point from as early as 2018. While studies may differ slightly concerning the actual size of the middle class, in 2019 a SALDRU study found that only 20% of South Africans belonged to the “stable” middle class. The implication is that it can be a transient class, something especially Covid has proven true.

Old Mutual rightly states that instead of focusing on the size of the middle class, focus should be on their state. South Africa’s economic sustainability is at risk with a relatively limited middle class facing high levels of indebtedness and a heavy tax burden. A model developed by Eunomix Business & Economics Ltd. Shows South moving from upper middle income to lower middle-income status. This is understandable considering that due to lockdown restriction at least 200,000 middle class jobs were lost in what has been termed “class suicide”. These numbers may seem relatively modest until one considers that South Africa is a working-class society consisting of a small middle class. Shedding this many jobs and reduced income in some cases have severely affected the standing of the middle class with debt income ratios for some sitting as high as 152%.

Unfortunately for South Africa, its middle class is not sitting back and patiently waiting for things to improve. With only about 30% of the middle-class believing things will improve, about 27% are looking to emigrate within the next 5 years. Basically, professionals are seeking greener pastures elsewhere. Where before it was the white minority that was looking at emigration, the black majority are increasingly looking to leave the country too. The wealthier, upper middle class have also been identified as

SPECIAL REPORT

those jumping ship as they seek more stable economies elsewhere. The SARS commissioner has even flagged the fact that money and skills are leaving the country at unprecedented levels which will result in long term brain drain and tax base erosion issues.

The major question becomes how South Africa has come to be in a position where in recent years its middle class has shrunk by over 50% and is moving to lower income status. In addressing this issue, the Eunomix model points at political and economic decline. The country is headed towards failed state status because of its reduced tax base, policies that are not growing the economy, violence and rising discontent among the citizens. The stability fostered by a thriving and stable middle class is slowly being eroded.

One study focused on what keeps South Africans up at night zeroed in on these top three factors in order, crime, corruption, covid. A significant number of participants indicated intentions to leave as there was more focus needed on safety, governance and prosperity and it seems as though there is no will from government to improve the situation. The country has been so focused on commissions and reports, yet no practical or tangible action seems to be taken against offenders. Corruption has become a byword, something expected in all facets of society that it seems an insurmountable obstacle to progress. A quick glance of headlines shows the levels of violence experienced in this country, the crimes that are a daily occurrence, this sense of life being worth very little in this country. It is no wonder that those with the means are more than willing to look for better prospects.

Where before South Africa sat as the bastion of democracy and opportunity in Africa, attracting foreign talent from all over the continent and the world, today it is struggling to pull itself out of the doldrums of inefficiency, monetary wastages, a corrupt political base, policies that have benefited the few at the expense of the many and xenophobia against their black foreign counterparts. Skills that would have come to South Africa from within Africa are looking at Western shores an outcome likely to be lauded by those who do not understand the need for scarce skills and the shortcomings the country is facing with its labour force.

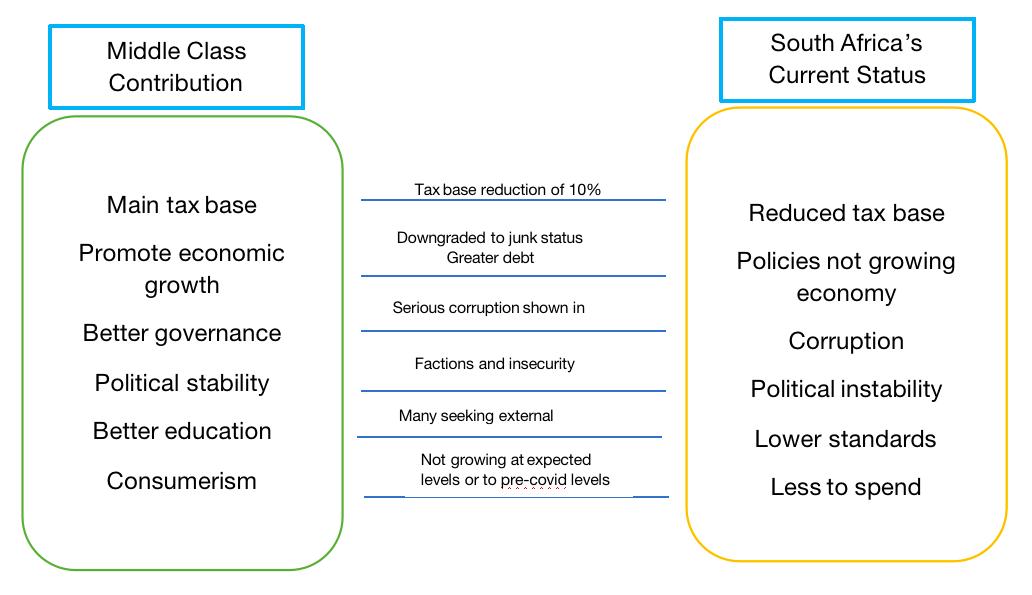

These problems revert one back to whether the middle class actually occupies the position it is said to or whether there is more to a country’s stability than their strong presence. The figure below shows what the middle class supposedly contributes and the current state of South Africa.

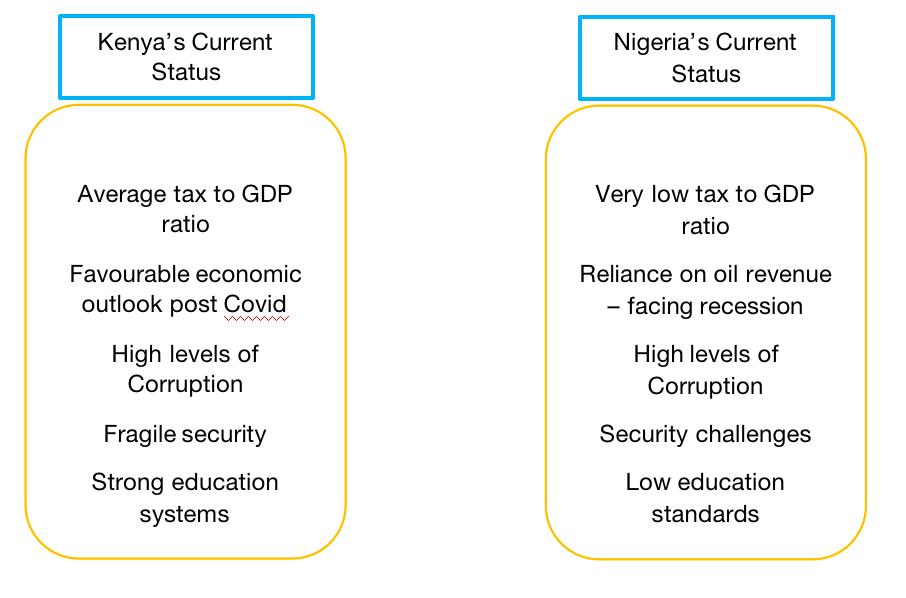

It is important to determine whether the state of the middle class is endemic to South Africa. On the continent, Kenya and Nigeria from East and West Africa respectively can be considered. Over the last two decades both countries have experienced growth in their middle class achieving middle class income country status.

From 2010, Kenya moved towards political stability with a new constitution that embraced a multi-party system. That stability has unfortunately not translated into greater security as its porous borders with Somalia, South Sudan and the Great Lakes Region leave it at risk from insurgents. Notwithstanding these challenges, the country has continued to develop.

Currently Kenya boasts the second largest economy in East Africa after Ethiopia. Agriculture has always strongly contributed to the GDP, but this has gradually decreased to just under 25%. Industry on the other hand has increased its contribution to about 21% and services are at about 50% of the GDP. Between 2014-2018, Kenya’s GDP went up 5,7% driven by the service sector in terms of real estate, finance and insurance, wholesale and insurance, education, transport and storage.

While Kenya has a vibrant private sector, it has a dichotomous structure. The formal business sector is strong but concentrated in few firms while there is a massive, informal, low productivity small business sector. While it did lose its gains in the Global Competitiveness Index, it still has viable business opportunities and attracts foreign direct investment for private sector investors. It has a variety of international organisations such as the United Nations, Coca Cola, General Electric, IBM and the World Bank regionally headquartered in Nairobi and recently Google announced it was setting up its first Africa product development centre there. The presence of such firms has helped foster the middle class which stands at 24% of the population according to the Kenya National Bureau of Statistics.

While the middle class have been improving in numbers, socially there are still high levels of poverty, limited access to basic services, inequality and unemployment. Kenya’s Gini index though fares better than that of South Africa at about 41%.

The role of the middle class in Kenya has also been exaggerated by onlookers and failed to meet expectation. The class has proved rather fluid, based largely on economic parameters, and still bound by the cords of ethnicity and status quo especially in political matters. The growth of the middle class has been reflected in the economic

growth of the country, with increases especially in consumerism. With economic success in hand, most tend to be wary of any change that could possibly reverse their fortunes which makes the middle class more accepting of the status quo to ensure their survival.

Nigeria on the other hand is a new middle-income country with an impressive GDP. As in Kenya, the services sector is the largest contributor to the GDP at 46% through financial and business services and real estate; creative arts and entertainment and information, communication and technology (ICT). Agriculture’s contribution is also decreasing and a decrease in tourism has also been noted. Nigeria is unique in that its budding entertainment industry actually contributes up to 2,3% of its GDP making it one of the largest employers in the country after agriculture. Final household consumption makes up about 80% of the country’s nominal GDP with this increase reflecting a growing middle class that makes up 23% of the population.

Above: In this photo taken, Sunday, Feb. 10, 2013 customers wait to buy Cold Stone ice cream in Lagos, Nigeria. As Nigeria’s middle class grows along with the appetite for foreign brands in Africa’s most populous nation, more foreign restaurants and lifestyle companies are entering the country.

( AP Photo/Sunday Alamba)

Unfortunately, the country still faces myriad challenges in security, fragility, slow growth, infrastructure deficit, low level human capital development, poverty, high inequality and rising youth employment. It is currently facing an economic recession due to volatile crude oil prices from pandemic. Its greatest challenge is diversifying from economy dependence on oil revenues.

As with Kenya, the private sector is dichotomous with large enterprises and a massive number of mostly informal Micro, Small and Medium Enterprises (MSMEs). Of the 41.5 million MSMEs, only 0,25 of these are Small and Medium Enterprises (SMEs). The micro enterprises make up 86,1% of the national workforce in the country. Even with such entrepreneurship the poverty numbers remain quite high with over 53% of the population surviving on less than $2 per day, and 92% on less than $6 a day.

Nigeria’s middle class has notably been indifferent to any forms of activism concerning the challenges in the country. The middle class has been missing from the po-

litical arena since return to democratic civilian rule in 1999 where they were expected to promote democracy and its ideals. They have failed to act in the face of programs and policies that have proved detrimental to the class and its growth. Some feel the middle class has even worked against possible gains by siding with government in its failures, propping them up in spite of overwhelming evidence of incompetence in terms of health systems, security, education and corruption. Instead of holding government to account, they tout its failures as opportunities for foreign investment. The middle class is accused of ensuring the subjugation of the working class and ensuring the system works for a few at the expense of many. It is only in recent time they have been showing signs of trying to shake up with status quo especially with recent elections and the #EndSARS movement. As with South Africa though, the middle class is steadily emigrating as they look abroad for greener pastures.

An overview of Kenya and Nigeria is summarised as follows:

In all of three countries, it is clear how the middle class has tied its success to that of the ruling elite. Former ANC Secretary General, Gwede Mantashe famously said the black middle class must remember they were beneficiaries of the progressive policies of the ANC and while not indebted, they must vote consciously. He in essence voiced what most of the middle class acknowledge and live by. Where the middle class is supposed to ensure proper governance and keep government in check, they tend to be kept in check by the elite they uphold. Efforts to break free of the stranglehold of government have yielded limited results as seen by the 2016 South African elections where the ANC lost major metros to the opposition but managed to regain some of them when coalitions fell apart, the last elections in Nigeria where quite a number of independent candidates ran for office but faced defeat and the elections in Kenya where the middle class voted by ethnicity lines. With the dawn of democracy, activism has become more of a grassroots endeavour as the middle class shows

apathy to the various challenges besieging their nations. All the ideals expected from their emancipation have failed to yield the expected results.

There is a need for the middle class to be independent of its governments. The fact that in Africa, the government is the largest employer and thus the foundation of the middle class means breaking free will be difficult for the middle class. Economies in the West are driven by massive employment in the private sector, and business prospects that are not dependent solely on government tenders.

The size of the middle class has been substantially reduced by the pandemic in sub Saharan Africa. This means more people have fallen into the poor income bracket. As long as accountability and activism are not a priority, the situation will continue to deteriorate. While not in the majority, the middle class holds the advantage of being the intellectual asset of the nation, they provide skills and knowledge that are critical for positive change. They need to find a way of leveraging their status, looking beyond the comfort of self and focusing on improving the standing of the working class. The middle class needs to come together as one cohesive unit for change to be realised otherwise they remain a myth creating mythical utopias while the reality is more dystopian.

Above: Hugo Boss Opens Luxury Store in Nairobi to Tap Growing Middle Class. PHOTO: Kenyan Wallstreet

Photo by Martino Pietropoli on Unsplash

African startups making an impact in agriculture

Startups are gaining prominence and significance on the African content. It was reported that in 2020, there were an estimated 6,000 African startups and more than $4.5 billion venture capital was raised

Astartup can generally be described as a young company that is based on a creative idea or offers a new way of doing business, meeting a specific need in the world, and financed by external investors. While the rate of startup success is generally low, when successful, startups can grow into large entities that are influential and or

By Talent N. Ndlovu

generate large and even billion-dollar revenues. Some of the most renowned entities in today’s world that began as startups include Airbnb, Uber, WhatsApp, Snapchat, ByteDance; the parent company of TikTok, SpaceX, Canva, Pinterest, Instagram, Mailchimp, Netflix, Facebook, and LinkedIn, all of originating in countries such as China, USA, and Australia and outside Africa. One of the most talked about African startups is the Kenyan Mpesa.

In recent years, startups are gaining prominence and significance on the African content. It was reported that in 2020, there were an estimated 6,000 African startups and more than $4.5 billion venture capital was raised, double the amount raised in the previous year. The countries with the highest numbers of startups are Nigeria, South Africa, Kenya and Egypt. African startups cover different sectors including financial, health, education, agriculture, transport and logistics, with financial startups being the most prevalent.

Recent years have also seen an increase in agricultural startups. In this paper, I will describe five agricultural startups that are amongst the most significant and high-impact startups on the African continent. These startups are; AgriPredict, Hello Tractor, AgriProtein, FarmCrowdy, and ColdHubs.

1. AgriPredict

Effective pest and disease risk management is essential for the success of agriculture, without which farmers can lose produce, the quality of produce can deteriorate, all resulting in loss of revenue, food, and export earnings. In Africa, the changing climate, particularly the warmer temperatures, appear to have increased the severity of pest and disease challenges. Examples of pests that are causing havoc in African agriculture include the fall armyworm, the Banana bunchy top virus, and maize lethal necrosis. These pests are causing massive damages across the continent, for example, the fall army worm is estimated to destroy more than 400 000 hectares of crop, worth $3 billion annually.

AgriPredict is a Zambian app that provides farmers with access to accurate, real-time pest and disease identification and management advice. Using this app, a farmer can upload an image of the pest, disease affected part of the crop. Using machine learning, AgriPredict then identifies the pest or disease on the image and suggests the most effective control method, and the nearest agricultural dealer. This information is then sent directly to the farmer, giving the farmer an opportunity to address the challenge timeously and effectively. This real-time service gives farmers a chance to detect and control pests and diseases early, hence, reducing the likelihood of crop damage and losses. This app could be highly beneficial for rural farmers, who rely mostly on the public extension services system, which is known to be poorly resourced, unreliable and unable to reach often remote, distanced rural farmers.