Connect Individual Consulting alexforbes.com Connect with news and insights from Alexforbes Issue 2 • 2024

Time to connect your financial dots (:)

In this edition of Connect we are connecting some financial dots. If you have ever seen a join the dots activity book you know that it is not always possible to see the bigger picture until the very last dot has been joined.

When it comes to the world of finance there are similarities as there are a lot of dots like budgeting, retirement planning and saving for a goal that connect to give you your full financial picture. Sometimes when dots are not correctly connected it makes for rather funny results and a little help is needed to ensure the bigger picture comes out right.

To help you join the dots we address the value added by a financial adviser. We feature recent interviews by some of our advisers on the Expresso Show. We delve deeper into the things to be aware of with the two-pot legislation that is coming on 1 September. We also discuss the importance of having emergency savings so that you don’t have to depend on your savings pot.

Connect with us today and let our quality financial advisors connect your financial dots.

Need more info?

For queries, contact:

Telephone: 0860 66 4444

Email: mymoneymatters@alexforbes.com

Connect with us

Head: Individual Consulting Strategy Rita Cool

Edward Semenya Senior Investment Specialist Alexforbes Investments

Edward Semenya Senior Investment Specialist Alexforbes Investments

The notion of financial advice is an intriguing one.

Its purpose is to assist investors and guide them to make rational, informed decisions for them to achieve their investment objectives. However, the difficulty lies in converting advice into value, in other words, placing tangible value on the opinions and recommendations of another. This is even more pertinent today, where the amount of advice available to investors – whether from friends or news and media outlets – is constantly available, reminiscent of the saying “Opinions are like belly buttons; everybody has one.”

For investors, it is often the case that performance is king. Their pursuit of returns and the desire to match or exceed market benchmarks can create pressure along the investment journey. It is for this reason that research consistently shows that investors who collaborate with qualified financial advisers significantly improve their chances of reaching their financial goals.

But, what yardstick can we use to evaluate the performance of a financial adviser?

A recent study by Russell Investments in the United States titled “Value of an Adviser”, quantifies multiple ways financial advisers add value to a client’s investment portfolio due to a holistic focus. Figure 1 breaks it all down.

*Based on differences in risk-adjusted returns of a typical actively rebalanced multi-asset portfolio held from 2003-2022, and one that was not rebalanced.

*Based on differences in the average US equity investor returns from 2008–2022, and that of the S&P500.

*Based on differential calculated over and above the basic asset management capability of a robo-adviser.

*Based on average differences in return between tax-managed and non-tax managed US equity funds.

Source: Russell Investments (2023)

With global events unfolding, including elevated interest rates, soaring inflation and geopolitical tensions, markets in general are proving tough to predict. There is no greater time to have a financial adviser by your side.

We believe that in addition to the financial and wealth management expertise provided by a financial adviser, it is the provision of discipline and reason to clients

who are often susceptible to behavioural biases such as emotions, that ultimately rewards. The results from the study confirm that behavioural coaching contributes the largest portion (2.54%) of the overall value provided by a financial adviser.

Let’s briefly explore all the areas below.

It is well documented that trying to time the market by selling at the bottom or not getting back into the market until it’s near the top (otherwise known as chasers), can significantly hurt investor performance.

As disclosed in the study, the difference in returns of the average ‘chaser’ in the U.S. equity market over the 15-year period under review and the S&P500 market index was quite substantial.

Figure 2 illustrates that during times of big and long market cycles, investors experience fear and greed. These are two of the main drivers of the biggest behavioural mistakes investors make when investing.

The beauty of behavioural coaching is that when panic sets in or an investor feels the urge to disinvest or invest more in the same thing, the calmness, perception and acumen of an adviser kicks in.

Undoubtedly, this is the largest potential value-add of a financial adviser – helping clients maintain a longterm perspective through different market cycles and discouraging ‘chasing’ – which can save investors from potential wealth erosion.

Source: Alexander Forbes Investments

The demands placed on financial advisers have increased exponentially over the years.

The study discovered that the guidance provided by a financial adviser, helping clients through life’s defining moments, aligning investments with goals, offering expertise on various financial matters like insurance, taxes and retirement planning, holds additional value beyond the basic asset management offered by a robo-adviser.

As expectations for customisation and personalisation rise, fuelled by examples like Netflix recommending tailored shows, and as client lives

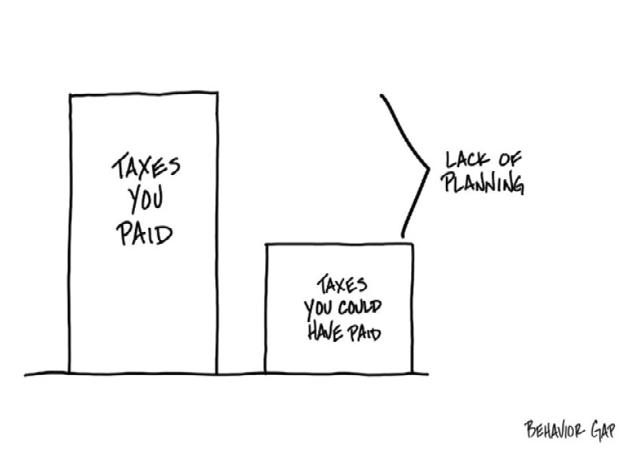

It’s fairly obvious that no one likes taxes, but investors need to fully understand the tax implications of some of their investment choices.

The study analysed how investors lost an average of 2.07% of their return from non-tax-managed US equity products in each of the five years ending 31 December 2022. However, an investor who invested in favourable tax-managed US equity funds would have given up only 0.90%. The difference is significant, and even more so when compounded.

Source: Behavior gap – Carl Richards

and family dynamics become more complex, it’s impossible for any single financial adviser to possess the broad expertise, experience or knowledge needed to address all client needs and priorities today. The ability of a financial adviser to manage these processes and collaborate with experts who share their clients’ interests when necessary, can prove decisive. It is only a financial adviser with a deep understanding of a client’s circumstances, and a genuine care for their family and aspirations, who can truly spearhead their clients’ financial success.

Without proper tax management, many investors end up paying more than they need to every year. The myriad of taxes that can be triggered by investments can include tax on dividends, capital gains tax, securities transfer tax, and so on. Figure 3 attempts to illustrate the saying: “Failing to plan is planning to fail”.

A financial adviser has the ability to proactively manage and implement a tax-conscious approach, to the benefit of their client.

It is clear from the insights above, that significant ‘alpha’ can be generated within an investment portfolio, thanks to the value-enhancing strategies of a financial adviser.

As mentioned in this article, there are many facets to the transformation of the modern-day financial adviser. The value-adding responsibilities of acting as a behavioural coach, providing holistic advice and customer experience, ensuring tax-efficient planning, and crucially, continuing to advise on the technical aspects of investment advice are increasingly in the spotlight.

Juggling all of the above while also being keenly aware that clients are demanding more from their financial advisers as they keep an eye on the fees they are being charged, only adds to increased complexity.

For the financial adviser, partnering with reputable partners for specific needs is a smart move.

While hypothetical scenarios attempt to quantify the value of advice, the reality is that the true worth of financial advisers lies in the tangible actions and unique perspectives they offer clients. It is the appreciation that a client’s time is valuable and that it should be spent partnering with a trusted financial adviser.

We encourage investors to continue to maintain strong relationships with their financial advisers.

It will be time well spent.

Time spent with an Alexforbes financial adviser is invaluable.

Our advisers recently joined the Expresso Show to offer their insights, underscoring their dedication to providing top-notch guidance. This series highlights our financial advisers’ commitment to making the most of every moment with clients by delivering meaningful advice, understanding each unique situation, and crafting personalised plans.

You can watch this six part series here

The two-pot system has been signed into law and will come into effect on 1 September. This legislation affects all members of retirement funds like pension funds, provident funds, retirement annuities and preservation funds. It does not apply to Living Annuities. There is a lot of information available in anticipation of this change, so we’ve put together some fast facts to help you connect the dots…

Register for AF Connect

Savings pot withdrawal claims from Alexforbes retirement funds must be submitted on AF Connect. Other service providers will have their own procedures. Register for AF Connect here.

pot

Your retirement money is for you to live on at retirement. The only cash payment you can get on your retirement is from your savings pot. Remember save your savings pot for your future self.

Money in your savings pot on 1 September 2024

Restricted to one withdrawal in a tax year (1 March to 28 February) –R2 000 withdrawal minimum amount. A small amount of your savings from your existing retirement savings (vested pot) will be moved to your savings pot on 1 September 2024.

This amount is 10% of your retirement savings. This first amount in your savings pot can’t be more than R30 000.

This is a once-off event and won’t happen again. Your ongoing contributions after 1 September will feed your savings pot.

The two-pot system is a lot to take in. If you still don’t know what it is or need help understanding it we’ve got you covered with these easy ways to get help.

Get the info you need, when you need it, at your fingertips.

We have a dedicated two-pot system information page on the My Money Matters Toolkit website.

This site gives you access to simple explainer videos, a very useful list of frequently asked questions and much more.

Keep coming back to the site as we update information all the time.

Call center

If you have a query or need assistance with any of the information here, contact our Call Centre at 0860 896 768 or email twopotqueries@alexforbes.com

Our call centre agents are fluent in English, Afrikaans, Zulu, and Sesotho. They are ready to help you understand the two-pot system.

The WhatsApp self-service solution provides the right information and support you need around the two-pot system.

Save our number to your contacts: +27 60 043 9601

Type Help, select Register and follow the menu prompts

The self-service options are available 24/7, 365 days a year

With Alexforbes WhatsApp you can also: request your fund balance track the status of a claim register on AF Connect or reset your password access to financial education

We know that life is uncertain and we are bombarded with negative news articles at home and abroad that underscores this.

A high inflationary environment, international tensions, economic uncertainty, a local power crisis and a bumpy stock market are just some of the things affecting our finances.

This once again highlights the need for a solid emergency fund as part of your financial plan. It allows your primary investments to stay on track when an emergency strikes. Too often people who don’t have an emergency fund are forced to withdraw funds from investments not intended or designed for emergencies. This causes these investments to veer off-course and fall short of their investment goals and in some cases cause even more financial distress.

Without an emergency fund your entire financial plan can be susceptible to failure during economic hardships that none of us are immune against.

Emergency funds should ideally be saved in cash, earning a competitive interest rate and not exposed to market fluctuations.

Emergency funds must be easy to access and should pay out relatively quickly. They should not be locked away, incur any penalties or have other restrictions when you need to access these funds.

These funds must be highly regulated and protected. No risky business or high risk assets belong in an emergency fund. Sometimes investors are distracted by the notion of high returns yet do not completely understand the risk they are taking.

• To cover at least three times your monthly gross salary is a good start, however each person is different and seeking proper financial advice is recommended.

• As cash is mostly used for an emergency fund, tax will apply. The good news is that SARS allows an interest exemption (tax free interest) amount meaning you don’t pay tax on the first amount of interest earned in a tax year. Your emergency fund should ideally not exceed this SARS limit. If you are under 65 years you can earn tax free interest up to R 23 800 and R 34 500 if over 65 in a tax year.

• Everyone who is economically active – An emergency fund is like insurance in that it can bail you out and protect you from financial loss. With the bonus that if you don’t need the emergency funds, you still have cash saved up and available to use as you please.

The time for emergency funds is NOW!

• The best time to build an emergency fund quickly is when interest rates are high – as they are currently in South Africa.

• Jack earns R 25 000 per month and needs at least 3 times his monthly salary saved for emergencies. He starts saving R 2 000 per month. If he gets 8% interest per year it will take him 2 years and 10 months to save R75 740. By increasing the monthly amount to R3 000 it will only take him 2 years to reach his goal.

• Once he has built up his emergency fund, he can stop contributing and the money will continue to benefit from compound interest.

• Funding waiting periods for disability cover

• Medical related emergencies and additional ad hoc costs

• Unexpected school tours and trips

• Funding Insurance excesses

Be savvy and secure your financial future with a low risk tax efficient emergency fund as a matter of urgency. Speak to a

Macro highlights:

Geopolitical tensions took center stage in April, with Iran and Israel firing missiles at each other. However, both attacks seem to have been calibrated to minimise damage, with the oil market shrugging off the escalation.

Inflation data for March was another key focal point for investors. Headline inflation in the euro area and the United Kingdom (UK) continued to trend lower but picked up in the United States (US) –raising fears that the US Federal Reserve (US Fed) may need to keep rates higher for even longer.

Market highlights:

April proved to be a challenging month for both global equities and fixed-income investors. A surprise uptick in inflation, coupled with macroeconomic indicators indicating US GDP growth falling short of expectations and a resilient labour market, prompted market downturns.

Developed markets equities declined for the first in over five months, while global bonds experienced their most significant sell-off since September 2023.

While global assets experienced a downturn throughout April, commodities demonstrated modest returns.

On the macro front, inflation remains elevated, which makes us believe the easing cycle is likely to be shallower than we initially expected.

Read the complete commentary here.

Disclaimer:

Please note that while care has been taken to ensure that the information provided in this article is correct, it represents an overview of the topic under discussion and as such does not constitute advice.

While Alexforbes has taken reasonable effort to ensure that the information contained herein is true and correct it will not be held liable in respect of any loss arising from any advice provided arising out of the contents of this circular.

We suggest that you contact your financial adviser before taking any decisions based on the information herein.

Locally, equities continued their upward trajectory, propelled by the surge in resources. The rand also strengthened against major currencies, helping bond yields to compress.

Alexander Forbes Financial Services (Pty) Ltd is an authorised financial services provider (FSP 1177 and registration number 1969/018487/07), an approved retirement fund administrator (24/472) and an accredited Council for Medical Schemes organisation (ORG468).

The following businesses are licensed financial services providers: Alexander Forbes Financial Planning Consultants (Pty) Ltd (FSP 31753 and registration number 1995/012764/07)

Alexander Forbes Investments Limited (FSP711 and registration number 1997/000595/06)