4 minute read

Battery prices

Higher Metals Costs to Negatively Impact Margins for OEMs and Global EV Adoption

Electric vehicle battery prices will remain high in 2022 as a result of elevated battery metals prices due to increased demand amid the race to electrify the global vehicle fleet.

Advertisement

BY FITCH SOLUTIONS

As battery metals remain one of the largest contributors to the cost of battery manufacturing, higher prices in 2022 will squeeze the profit margins of battery manufacturers and automakers alike as more electric vehicle (EV) models are deployed. Fitch Solutions therefore expects higher input costs to result in upside risks for battery prices in 2022 as long-term agreements with mining firms for the supply of key metals are entered into at substantially higher prices compared to 2020.

Over the longer term, developments in the increase of battery recycling will lead to a more favourable battery metals supply outlook as a “closed-loop” metals supply environment offers better pricing mechanisms amid more metals being reused in newer EVs going forward. Fitch currently forecasts global EV sales to rise by 40.3% in 2022 as demand remains elevated amid the need to decarbonise the global vehicle fleet.

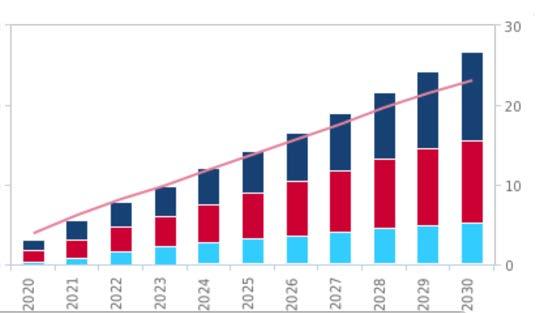

Asia, Europe and North America will remain dominant markets for EVs over the 2021 to 2030 forecast period (see chart on right). These markets offer a large market to tap into while developing countries continue to lag with the possibility of higher EV prices stunting growth in these markets.

In the meantime, the shift towards more cost-effective lithium iron phosphate (LFP) battery chemistries is expected to tame the rising costs associated with more nickel-rich chemistries. Fitch Solutions currently forecasts the global share of EVs that use LFP battery chemistries to rise from 21.1% in 2021 to 30.3% by 2025.

Higher costs of nickel-rich battery chemistries, such as the nickel manganese cobalt (NMC) and the nickel cobalt aluminium (NCA) chemistries, will necessitate the shift towards the more cost-effective LFP chemistry. The demand for battery grade nickel will far outstrip supply as automakers ramp up EV production.

As a result, we expect NMC market share to decline from 51.1% in 2021 to 45.3% by 2025 (see chart below). Going forward metals retrieved from recycling operations will result in the NMC chemistry gaining a foothold once again from 2026 (with a market share of 45.9% rising to 51.4% by 2030) as this chemistry option offers higher energy density levels offering better range capabilities for EVs.

Fitch Solutions

Global: EV sales by battery chemistry type, %. (e/f = Fitch Solutions estimate/forecast)

We have already seen automakers in China making the shift towards more cost-effective LFP chemistries while the likes of Tesla have indicated that it will offer the more affordable chemistry type for its entry-level EV models globally. More automakers are expected to make the shift as higher battery costs stunt the growth of nickel-rich batteries.

Moreover, the move towards cell-to-pack battery structures that remove the need for battery modules will also be more broadly implemented by automakers to ensure that rising costs are limited to the battery cell level and ensure automakers can deploy more EVs amid heightened demand globally. Some of these developments have already gained traction as Ford recently announced that it will utilise cell-to-pack designs as well as LFP battery chemistries to further reduce costs.

While automakers will look to keep prices of fully built EVs constant to raise EV adoption globally, countries without any meaningful consumer-focused incentives will be vulnerable to higher battery costs going forward. Countries in the developing world with lower EV penetration rates (EV sales as % of total vehicles sold) will be affected should OEMs pass on higher prices when compared to more developed EV markets such as China, Europe and North America. This is due to relatively higher incomes in these latter markets and the prevalence of incentives to cut down the initial purchase prices of EVs.

Countries that have little to no support will be vulnerable to further increases in already higher purchase costs of EVs relative to internal combustion engine (ICE) powered vehicles. It is expected that automakers will deploy mild and plug-in hybrid models for lower income markets as a way to cushion consumers from higher EV prices due to high battery costs.

This report from Fitch Solutions Country Risk & Industry Research is a product of Fitch Solutions Group Ltd, UK Company registration number 08789939 (‘FSG’). FSG is an affiliate of Fitch Ratings Inc. (‘Fitch Ratings’).