9 minute read

The economic case for the mining industry to support carbon taxation

Anglo American Plc

Anglo American Plc, Kumba Iron Ore, Sishen.

Advertisement

The economic case for the mining industry

to support carbon taxation

As governments try to navigate a path to a safe climate in the 21st century, the public debate has focused on net zero, carbon taxes, electrification and renewable energy. Mining is rarely an anchor point of the discussion, even though renewable energy infrastructure and low-carbon technology require vast amounts of metals and minerals.

BY SALLY INNIS, BENJAMIN COX, JOHN STEEN, NADJA KUNZ*

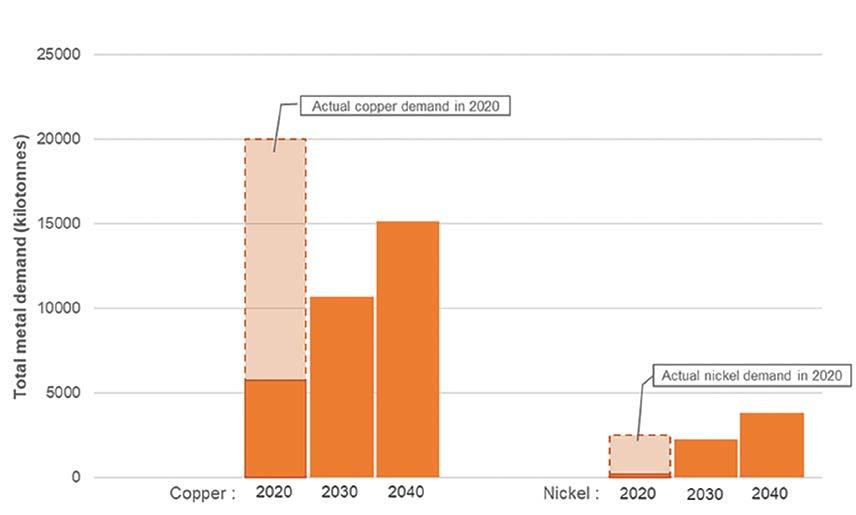

Nickel, for example, is essential for electric vehicles and battery storage. The amount of nickel required by 2040 for the energy transition alone will be equal to the total demand for nickel across all industries in 2020, according to the International Energy Agency.

There is widespread consensus among economists that carbon taxation is one of the most effective policies to reduce carbon emissions. Presently, 27 countries have enacted carbon taxation policy at the national level, however only seven of these are leading mining countries, and mining companies and industry organisations oppose carbon taxes in many of these countries.

Addressing climate change requires a coalition between

Cox et al. 2022

industry and government. The idea that the industry supplying the technology for renewable energy is also opposing the economic policy needed to curb emissions is counterproductive. Simple economic modelling proves that resisting a carbon tax is the wrong strategy for the industry.

METALS OUT, A LITTLE CO2 IN

There are many factors throughout the mining process that contribute to carbon emissions. The commodity being mined heavily influences the number of emissions and where the emissions are generated throughout the mining process.

For iron and steel most emissions are generated in the later stages during smelting. Mining copper ore, on the other hand, generates most of its emissions in the earlier stages during the crushing, grinding and hauling of ore.

One way to look at the impacts of carbon taxation in mining is to compare the commodity’s carbon footprint to its economic value. For example, the average carbon footprint of copper is 3.83 tons of carbon dioxide per ton of copper.

So, for each ton of carbon dioxide emitted, 261 kilograms of copper worth US$1 700, using 2019 copper prices, are produced. This is a relatively high value. The same cannot be said for other

Anglo American Plc Projected demand change for copper and nickel requirements for energy transition technology. The solid bars show the amount of metal demand projected for the energy transition, while the transparent bar shows the actual total demand for copper and nickel across all industries in 2020.

industries, like animal agriculture, where a ton of carbon emissions corresponds to about US$125 of wholesale beef (using equivalent 2019 pricing).

HOW WOULD A CARBON TAX AFFECT MINING?

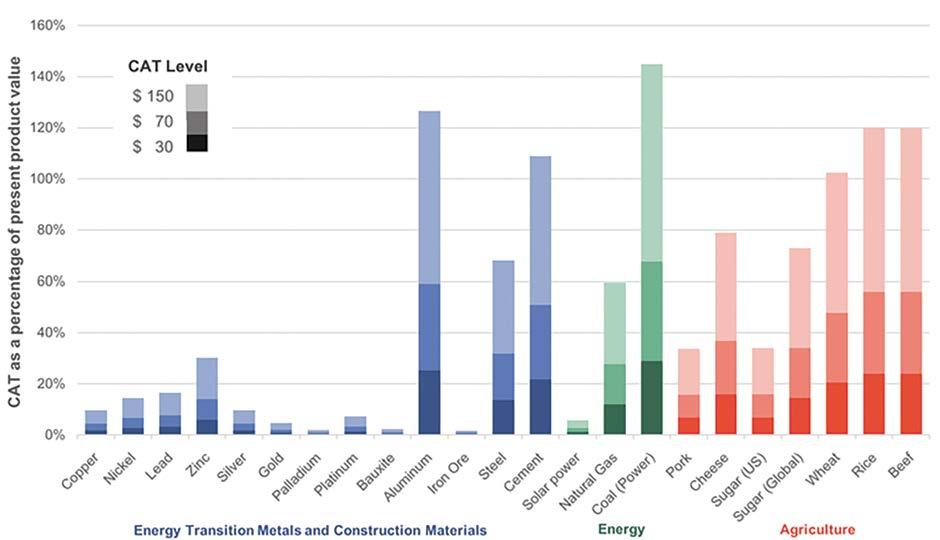

The basics of a carbon tax are that more carbon-intensive industries will be taxed more. Our study tested three levels of carbon taxation: US$30, US$70 and US$150 per ton of carbon dioxide, and compared them against commodity prices in 2019.

MINING FOR CARBON TAXES

Outside of aluminum refining and steel mills, the mining industry will perform better with a carbon tax than it would without one. This is because the carbon tax would increase the price of fossil fuels relative to renewable energy and the materials required for renewable energy technology.

For example, the costs of coal used for energy production will more than double, making electricity from coal increasingly uncompetitive. The rising demand for solar and wind power will drive further increases in the consumption of base metals for wind turbines and solar panels.

If implemented on a global scale, a carbon tax would not change the underlying cost of the base metal business, but it does have vast financial benefits for the mining sector. These benefits come from the increased demand for metals from the energy transition, paired with a relatively lighter percentage of global carbon taxes, in comparison to other industries.

Rather than opposing carbon taxes, the mining sector should become a global advocate for aggressive carbon targets, the harmonisation of international carbon taxes and pursue further reductions to emissions such as the electrification of fleets or carbon offsets.

The Conversation under Creative Commons License

The impact of three levels of carbon taxation (US$30, $70 and $150) modelled as a percentage of present product value for selected commodities. This shows that most mining industry and energy transition commodities will not be taxed to the same degree as other commodities.

These levels closely follow the Pan-Canadian approach to carbon pollution pricing, which are currently set to $50 per ton and increase $15 per year to $170 in 2030.

We modelled the impact of a carbon tax on a range of commodities. Our model included all Scope 1 and Scope 2 emissions – direct emissions from the source and indirect emissions associated with heating, cooling or electricity. The production of some commodities is more carbon-intense than others, which affects the impact of the carbon price.

In some cases, the carbon tax can be greater than the product’s value. When the price of carbon is US$150, coal is taxed at 144% of its value. Copper, on the other hand, is taxed at 10% of its value. Two metals are outliers to the industry: aluminum and steel. The mining of the raw materials is not carbon intensive. Bauxite and iron ore generate 0.005 and 0.02 tons of carbon dioxide per ton of product respectively but smelting these ores into metals emits more carbon in production.

SA CARBON TAX

South Africa introduced a carbon tax in June 2019 as part of a package of policy measures to help achieve the Nationally Determined Contribution commitments submitted under the Paris Agreement. To assist industries to transition to sustainable and low-carbon practices in a cost-effective manner, a carbon offset tax-free allowance is provided to companies under the Carbon Tax Act (No 15 of 2019) to help reduce their carbon tax liability and encourage additional investments in eligible lowcarbon offset projects.

*Sally Innis, PhD candidate, Benjamin Cox, PhD student, mining engineering, John Steen, ey distinguished scholar, global mining futures, Nadja Kunz, Canada research chair and assistant professor, mining, all from University of British Columbia.

MINING UNDER PRESSURE TO DECARBONISE OPERATIONS

In 2021, President Ramaphosa recommitted South Africa to a series of steps aimed at reducing the country’s carbon footprint because “the world is facing a climate crisis of unprecedented proportions”. South Africa joins the world in this urgency as it races to achieve net zero targets over the coming decades.

Sameer Singh, research analyst at Old Mutual Wealth Private Client Securities, says that to reach the goal of carbon net zero, industry at large, and diversified miners specifically, can expect increased stakeholder pressure and must plan for business process transformation to remain both relevant and profitable.

“Mining, as an extractive activity, leaves a long-lasting mark on the environment. Additionally, the processes of extraction and refining emit a substantial amount of greenhouse gases. The mining industry specifically will see dramatic shifts in both the demand for their products and the regulatory environment. For some it will signal the beginning of the end, while for others it will be the start of a new growth trajectory,” says Singh.

One miner plotting the path of mining for the future is Anglo American. For much of the company’s existence, it had been about expansion. The 21st century ushered in a phase of consolidation, which saw the group shifting from operating eight business units with multiple commodities to four key business units and six commodity groups.

Anglo’s strategic shift started in 2015 when the miner recognised both a change in demand as well as the inevitable need to define a relevant and more responsible mining industry of the future.

Singh says increased demand for platinum group metals (PGMs) is far more than a cyclical commodity trend. “Renewable energy, electric vehicles and battery storage, electricity networks and other clean energy technologies require significantly greater amounts of critical minerals than we are currently consuming. Transitioning to and meeting this increased demand will be a key focus for all miners over the next few decades. PGMs are integral to the energy transition value chain, where hydrogen plays a big role too,” he says.

Singh says the miner’s vision, which aims to build connected, intelligent, automated and waterless mines, should see the miner achieve “less waste, fewer inputs, reduced energy consumption and lower capital intensity, which are all earnings accretive”.

Anglo is focusing on renewable energy generation, switching from diesel for fuel to hydrogen, battery energy storage, limiting methane emissions, pursuing carbon efficiency and implementing emission compensation strategies.

“When investors look at the medium and long-term prospects of mining companies, they should do so with a future-oriented lens and track where the miner is going relative to where the world is going, and what stakeholders will demand,” adds Singh.

Anglo has already secured 100% renewable energy for all its South American operations and is currently testing the mining industry’s first hydrogen-electric haul truck.

“From an investor’s perspective, Anglo is doing all the right things and is executing them well,” explains Singh. He adds that 8% of the company’s long-term incentives are linked to greenhouse emission reductions and 5% of annual bonuses are tied to key environmental programmes.

Operationally, the group has realised an 8% improvement in energy efficiency and a 22% saving in greenhouse gas emissions. Earlier this year, the group concluded the spin-off of its South African thermal coal business and announced the sale of South American thermal coal.

By 2030 Anglo is targeting a 30% improvement in energy efficiency, a 30% net reduction in greenhouse gas emissions, aims to have eight carbon neutral sites and by 2040 the group aims to be carbon neutral across all its operations.

Anglo American has signed a MoU with EDF Renewables, a global leader in renewable energy to work together towards developing a regional energy ecosystem in South Africa. While there is an abundance of solar and wind power in our country, there is limited renewables infrastructure to harness it.

Anglo American Plc, Platinum, water testing at Der Brochen, South Africa.

Anglo American South Africa PGM operations, such as Mogalakwena (featured), are increasingly using treated effluent, or grey water, rather than drawing on freshwater supplies.