3 minute read

The EV push gains pace

MARKET INSIGHTS

Time to power up

As the EV push gains pace amid miner production shortfalls, the battery metals sector is in need of a jump-start.

Guy Le Page

GUY LE PAGE

Battery metals – principally lithium, graphite, cobalt, and nickel – can all be expected to attract increases in demand owing to the electrification of global transport with battery electric vehicles (BEV) projected to reach 50% of all vehicles by 2035 (Figure 1).

Many established car manufacturers such as General Motors are also looking to phase out petrol/diesel by 2035.

A typical lithium-ion battery (NMC532) contains approximately 8kg of lithium, 35kg of nickel, 20kg of manganese and 14kg of cobalt, however amounts of these inputs vary significantly.

The good news for motorists is that batteries are now 30 times cheaper and more portable than their predecessors in the 1990s with Bloomberg NEF projecting that lithium-ion EV batteries should drop below US$100 per kilowatt-hour by next year which could see price parity by the mid-2020s.

While lithium and graphite are abundant in the Earth’s crust, sourcing nickel and cobalt even before the trend towards electrification was challenging to say the least, with a heavy reliance, in the case of nickel, on direct shipping laterite ore from Indonesia, The Philippines and New Caledonia together with expensive High Pressure Acid Leach plants processing nickel laterite ores. Cobalt sources outside of the DRC (who don’t meet the West’s ESG standards) are even harder to come by and mostly a byproduct of nickel sulphide/nickel laterite mining. Graphite production is currently dominated by China, but the growth in demand will likely require filling from East African deposits.

Not surprisingly manufacturers are looking to cut down on the intensity of use of these inputs by improving battery recycling; a significant challenge.

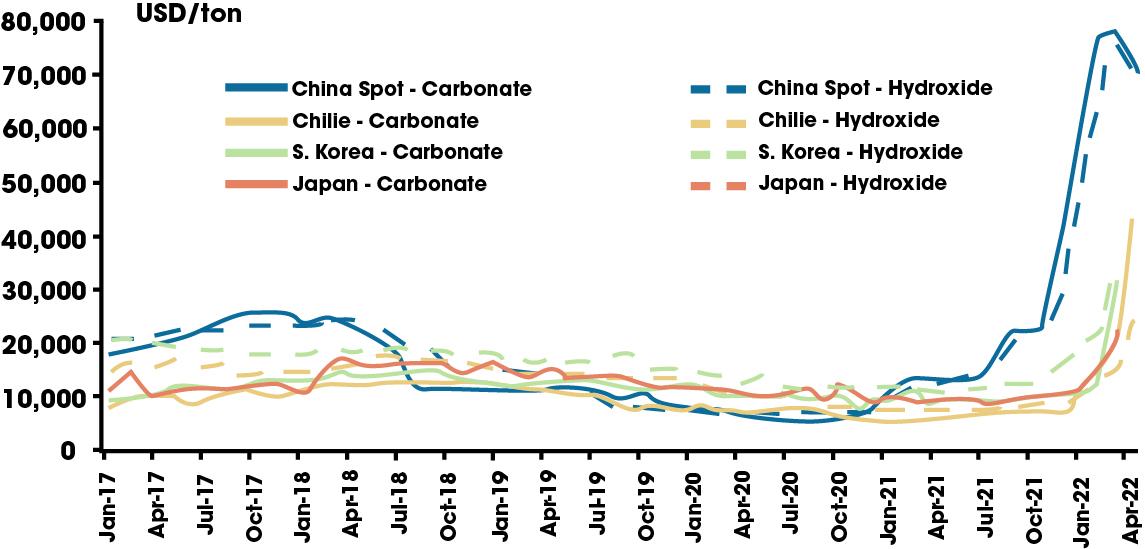

Lithium has taken most of the limelight over the last few years. Lithium equities (Figure 2) began with a market capitalisation base of $1 billion in 2015 (Argonaut, 2022), then rose sharply resulting in an outsized Western Australian spodumene supply response. This resulted in lithium carbonate prices falling below US$10,000/t, representing a critical incentive price for the industry.

Cumulative market capitalisation in the lithium industry exceeded $36 billion in early 2022, as demand growth accelerated. The majors made their first forays with Rio Tinto (ASX:RIO) investing in the Jadar Project in Serbia and recently acquiring the Rincon project in Argentina.

The question then is: is the market accurately assessing the likely lithium demand-supply balance in the coming years, and if so, are equities appropriately valued?

Goldman Sachs (May 2022) considers the battery metals bull market is over on the basis that the supply response will deliver a near term surplus. However, unlike in 2017-18, a couple of low technical and jurisdiction-risk Australian hard-rock assets will not be sufficient to meet growth in demand.

Some of the recent market darlings have drawn skepticism from short-sellers who have questioned many developers’ production forecasts. These include J Capital on Vulcan Energy (ASX:VUL) and Lake Resources (ASX:LKE), and Hindenburg Research on Standard Lithium (CVE:SLI). Jurisdiction risk has also reared its ugly head with Rio Tinto’s Jadar Project and AVZ Minerals’ (ASX:AVZ) Manono Project.

It appears the unstoppable EV momentum is upon us and is likely to continue to drive battery metal prices higher for the medium term at least as many miners fail to meet their production forecasts.

Figure 1: Global electric vehicle projections. (Source: LMC automotive, Autodata, CAAM, EAFO, Macquarie Research, July 2022)