Celebrating a Legacy of Service in the CPA Profession Introducing our 2023 Life Member AZ CPA March/April 2023 The Arizona Society of Certified Public Accountants y www.ascpa.com

Delivering Results - One Practice At a time GREATEST # of Listings GREATEST # of Buyers UNMATCHED RESULTS! $ 1 billion+ in Deals Closed! Our Best-in-class Brokers will help you achieve YOUR goal! Sherif Boctor Sherif@APS.net 888-783-7822 www.APS.net Scan Here

“CEA has helped my family make my daughter’s education attainable. A quality Catholic education means a lot to us.” -Mom of Scholarship Recipient • 99.4% Graduation Rate • 97% Matriculate to Higher Education, Trade School, or Military Service • 1000s Hours of Community Service • Corporate Tax Credits • Individual Tax Credits Catholic Education Arizona is an IRS 501(c)(3) nonprofit charitable organization and has never accepted gifts designated for individuals. Per state law, a school tuition organization cannot award, restrict or reserve scholarships solely on the basis of donor recommendation. A taxpayer may not claim a tax credit if the taxpayer agrees to swap donations with another taxpayer to benefit either taxpayer’s own dependent. *2020 ADOR Report It’s Quick. It’s Easy. Ask us How! Arizona S & C Corporations, and Insurance Companies that pay premium tax may direct 100% of their Arizona liability through the Low Income and Disabled/Displaced dollar-for-dollar tax credits! Join 130+ corporate contributors investing in future leaders. Corporations Contribute any amount up to: Individuals Changing lives one scholarship at a time. 602-218-6542 WWW.CEAZ.ORG Through your support, we have awarded more than 148,000 scholarships to underserved students over the last 25 years. Did you know your clients can change lives with their Individual and Corporate Tax Dollars? CELEBRATING

YEARS

Year 2022

Year 2023

AZ CPA

The Arizona Society of Certified Public Accountants

President & CEO Oliver Yandle

Editor Haley MacDonell

Advertising Heidi Frei

Board of Directors

Chair Rachael Crump

Chair-Elect Andrea Levy

Secretary/Treasurer Lauren Murro

Directors

Benjamin Cilek

David Collins

Samantha Crum

Tithi Debnath

Glen Evans

Barbara Gonzalez

Joseph Heidleburg

Gabrielle Luoma

Eugene Park

Jesse Porras

Megan Romo

Christopher Tyhurst

Immediate Past Chair Tom Duensing

AICPA Council Members Mike Allen

Jared Van Arsdale

Get Involved Volunteer

Join a volunteer committee to help determine the agenda for a conference or share resources within your practice group.

Make an impact in our advocacy initiatives through our Tax Legislation Committee, which reviews and analyzes tax legislation and provides feedback to lawmakers. Get started: www.ascpa.com/volunteer

Share Your Expertise

Join our line-up of experts by speaking at Converge, the ASCPA’s annual conference. Call for proposals ends March 31. Learn more: www.ascpa.com/speakconverge

Help Solve a Problem

Support your industry peers by answering a question on Connect, our online forum. Read more: connect.ascpa.com

AZ CPA is published by the Arizona Society of Certified Public Accountants (ASCPA) to provide information, news and trends to the accounting profession. It is distributed six times a year as a benefit to ASCPA members. The ASCPA, its members, board of directors and administrative staff assume no responsibility for advertisements herein. The ASCPA and the above people also assume no liability for business decisions made by readers in reference to statements and/or claims in articles or advertisements within this publication. Opinions expressed by contributors are not necessarily those of the ASCPA.

Arizona Society of CPAs 4801 E. Washington St., Suite 180 Phoenix, AZ 85034-2040

Telephone (602) 252-4144

AZ Toll-Free (888) 237-0700

www.ascpa.com

EDUCATION

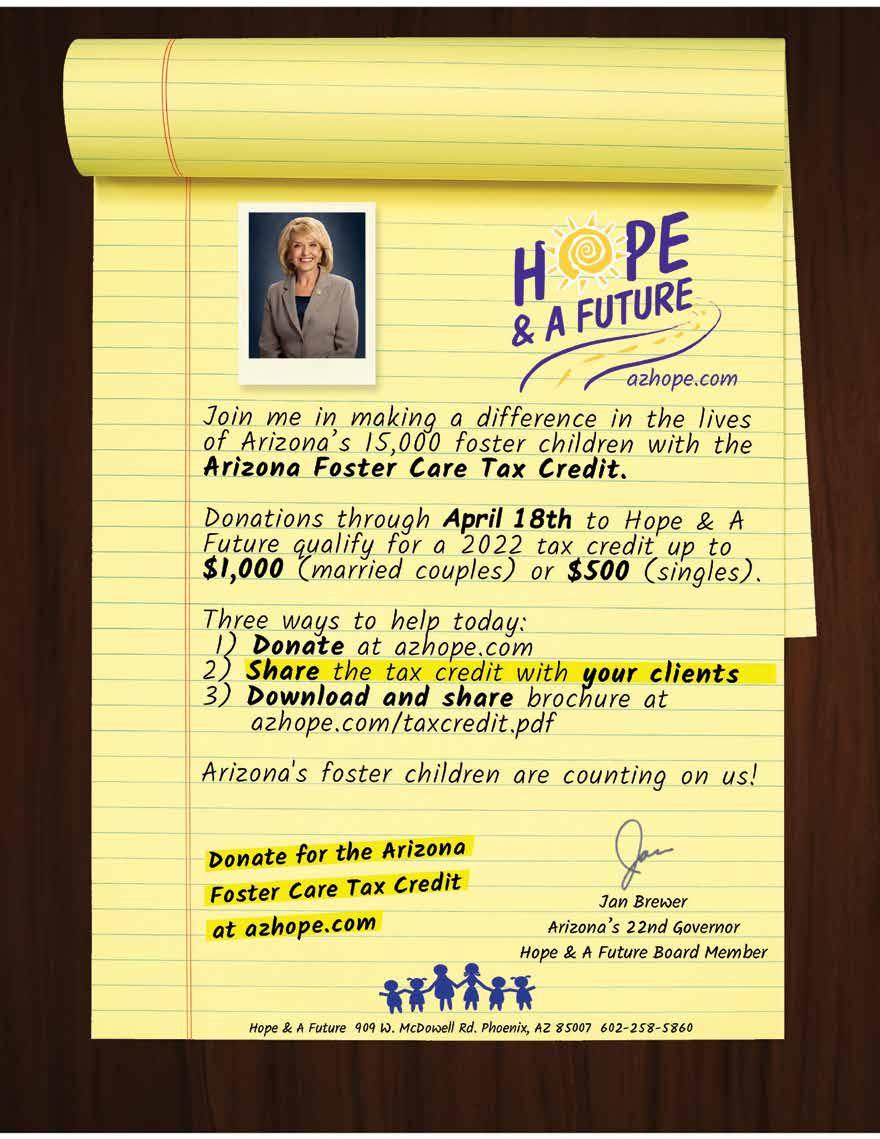

Take the Credit FOR

$1,243 for individuals $2,483 for married couples $1,307 for individuals $2,609 for married couples Provide scholarships by supporting the JTO through Arizona’s dollar-for-dollar private school tuition tax credit Deadline for 2022 support is April 18, 2023 or when you file your taxes, whichever comes first Help your clients maximize their tax credits! NOTICE: A school tuition organization cannot award, restrict or reserve scholarships solely on the basis of donor recommendation. A taxpayer may not claim a tax credit if the taxpayer agrees to swap donations with another taxpayer to benefit either taxpayer’s own dependent. Consult your tax advisor for specific tax advice. Call for corporate tax credit information 480.634.4926 | JTOphoenix.org

4 AZ CPA MARCH/APRIL 2023

Suzanne Holl

Patricia J. Elder, CPA

9 Karen K. McCloskey, CPA, Earns Life Member Status 9 Karen K. McCloskey, CPA, Earns Life Member Status by

13 Arizona CPA Foundation for Education & Innovation Donors 15 Key Steps for Tax Risk Management

18 What’s Happening at the ASCPA? 21 Guiding Clients to Their Lasting Legacy

24 The Death of Deducting Litigation Expenses: What’s Next? By

Columns & Departments Chair’s Message by Rachael Crump, CPA, CGMA 6 Member News 7 Quick Quiz 27 AZ CPA Features Volume 39 Number 2 March/April 2023 4801 E. Washington St., Suite 180 Phoenix, Arizona 85034-2040 www.ascpa.com MARCH/APRIL 2023 AZ CPA 5

Haley MacDonell

By

By

William Rothrock, CSSC

Rachael Crump, CPA, CGMA Chair, Arizona Society of CPAs Senior Vice President, Global Corporate Controller and Principal Accounting Officer at Insight

Moments in Time

I would like to thank everyone for your readership and your support of the ASCPA during my tenure as chair for the 2022-2023 fiscal year. As I reflect on my time, the preparation leading up to this commitment created just as much impact as my year as chair itself.

One moment during my year as chair that sticks out was our first in-person Annual Meeting & Awards Luncheon in three years! I’m so lucky to have that honor, especially watching both Ginny and Tom adapt through their chair terms to virtual events. This fiscal year coincided with a calendar period that frankly MANY events, venues and old routines returned to what we knew prior to the onset of the pandemic in early 2020. We began to gather together for work, leadership, service and extended family events. We talked about making plans again in advance –something I always did, but stopped in 2020 ... I’m not entirely back on that path yet and not sure I will ever return as I work to prioritize my precious time and attention.

There were many great moments from this year, including the AICPA council meetings in Austin and Chicago. The reunion was a fantastic treat to be together as a group, and I reconnected with colleagues who serve in other state societies. We received relevant updates on the profession – many of which we brought back to you for a series of Professional Issues Updates across the state. Both events provided insights into two highlighted areas: the CPA pipeline and diversity and inclusion. Both topics affect every one of us – regardless of the firm or organization that we serve as valuable advisors.

In August, the ASCPA kicked off the first update in Flagstaff. Oliver met with CPAs, while I quarantined at home with the first known COVID-19 case in our household! It wasn’t a peachy time, but I was grateful to be among those who recovered from home without medical intervention.

In November, I joined Oliver to visit CPAs in Prescott and learned about their challenges as well as the opportunities coming out of expanded offerings at Prescott College. December took us both to Yuma for a conversation with local industry professionals about similar difficulties in a smaller economic environment.

In January, Oliver rounded out our statewide visits in Tucson. A huge thank you to everyone who spent an hour out of your busy days sharing your perspectives.

Overall, my service on the board, executive committee and now as chair granted me the incredible opportunity to connect with each of you in some way – and for that I am grateful and honored. I am fulfilled from my time and took far more from this service than I provided. I want to thank the staff and board members I’ve had the privilege to work with during the last several years – some of whom have retired during this time. It’s something I keep looking forward to in my last quarter of my career.

In this issue, you’ll meet our newest life member, Karen McCloskey, and read about her own history of service not just to the ASCPA, but to the accounting profession and the state of Arizona. As you may have noticed in my writing, I enjoy reflecting and pulling forward these wonderful life moments. Please be sure to read about Karen’s journey and see where the moments of reflection take you. l

Best, Rachael Crump

ASCPA Chair’s Message 6 AZ CPA MARCH/APRIL 2023

Member News

Todd A. Keilen, CPA, is promoted to shareholder at Hunter Hagan & Co. Ltd.

Jeanne M. Bentley, CPA, is promoted to principal at Hunter Hagan & Co. Ltd.

Katherine Shell, CPA, is promoted to audit manager at Heinfeld, Meech & Co, P.C.

Makaela Rae Clapp, CPA, is promoted to senior associate at Heinfeld, Meech & Co, P.C.

Jason C. Cook, CPA; Lydia Hunter, CPA, CGFM; Travis T. Jones, CPA, CFE; and Victoria L. Meyer, CPA, SHRM-CP are promoted to principal at BeachFleischman.

Alec Guadalupe Carbine, CPA, and Mukhtar Almukhtar, CPA, are promoted to senior audit associate II at REDW LLC.

Desylina Christensen, CPA, is promoted to Tax Supervisor at REDW LLC.

Update Your ASCPA Account If you changed your address or email, please update your ASCPA account online. Don’t miss out on your member benefits and important account updates. Get started: www.ascpa.com/my-cpa/profile 520.512.5438 ibescholarships.org Largest Educational Tax Credit Ask About S-Corp 162 Deduction C & S Corps | Insurance Companies | LLC's with S Election Hurry, Cap is Almost Met! Solicit STO Funds While on ESA* Largest Individual Tax Credit Kids | Schools | General Fund Online Application AZ Corporate Tax Credit AZ Individual Tax Credit Help Arizona Kids Phone | Chat | Email Support | Pay With Credit Card Simple 5 Minute Process Notice (A.R.S 43-1603): A school tuition organization cannot award, restrict, or reserve scholarships based solely on a donor’s recommendation. A taxpayer may not claim a tax credit if the taxpayer agrees to swap donations with another taxpayer to benefit either taxpayer’s own dependent. *if eligible

MARCH/APRIL 2023 AZ CPA 7

– Cantor Forensic Accounting, PLLC

Trusted by accounting industry professionals nationwide, CPACharge is a simple, web-based solution that allows you to securely accept client credit and eCheck payments from anywhere.

65% of consumers prefer to pay electronically

62% of bills sent online are paid in 24 hours

Get started with CPACharge today cpacharge.com/ascpa AL: $3,000.00 *** PAY CPA 22% increase in cash flow

online payments

with

CPACharge is a registered agent of Wells Fargo Bank N.A., Concord, CA, Synovus Bank, Columbus, GA., and Fifth Third AffiniPay customers experienced 22% increase on average in revenue per firm using online billing solutions

+

CPACharge has made it easy and inexpensive to accept payments via credit card. I’m getting paid faster, and clients are able to pay their bills with no hassles.

Karen K. McCloskey, CPA, Earns Life Member Status

by Haley MacDonell

by Haley MacDonell

When Karen K. McCloskey, CPA, MST, learned she had been awarded Life Member status at the ASCPA, she had just returned from the trip of a lifetime. She and her husband Bill left Tucson, Arizona, in June 2022 and drove west to San Francisco with their travel trailer to visit their children and grandchildren. It was the first stop on a four-and-a-half-month adventure on the road that spanned the entire country. They hiked in Maine, visited national parks like the Badlands and stayed to see the peak of gorgeous, fall foliage in the White Mountains of New Hampshire.

MARCH/APRIL 2023 AZ CPA 9

Continued on next page...

“We discovered a lot of beauty that we hadn’t seen in this country,” she remembers. “We searched out the best lobster roll. Even though there is no right answer for that, the search was worth it.”

Their favorite was ultimately Connecticut style with fresh lobster and melted butter.

“Part of that trip comes to me every single day, in the freedom that Bill and I had together,” McCloskey says. “We were just discovering what’s around us and what we want to do. I love the freedom of that, to be an explorer on the road.”

After 30 years in public accounting, McCloskey has started to slow down from a busy career, generous service to nonprofits and essential work on the Arizona State Board of Accountancy. The Road

to CPA

After graduating with a degree in social sciences, McCloskey turned to a career counselor for advice.

“Why don’t you sign up for the federal exam?” McCloskey remembers the counselor say. It would set her up to work in a government job. She took the exam and checked every available box for a position. The Internal Revenue Service was the first agency to call and schedule an interview with her for a tax auditor role. With the encouragement of her career counselor, she went to practice her interview skills and ended up with a job offer.

“I’ve always had a propensity toward numbers, calculations and the law, so it fit naturally,” she says. “There were fledgling women’s programs and opportunities for career advancement. That’s when I started taking accounting courses to be qualified to sit for the CPA exam.”

McCloskey worked at the IRS for six years and in that time followed her then-boyfriend, now husband Bill to Santa Barbara, California.

As McCloskey studied accounting – eventually culminating in her master’s degree in taxation — and her husband, worked on his Ph.D., they had a rhythm to their routine. They’d

have dinner together and then go study at the library.

McCloskey knew she didn’t want to be an enforcer, but she remembers being told that if she left the IRS for public accounting, it would be too difficult for her as a woman and as a mom. The only CPAs she had interacted with were the men in suits who came to the IRS to represent their clients.

In Her Community

Ultimately, she followed her ambition and joined BeachFleischman in 1998. Over the next 24 years, she took on more responsibility, mentored other staff and became a subject matter expert in not-for-profit accounting. She loved solving challenges and helping clients. Behind each transaction was an important, human moment –divorces, marriages, business mergers and entire livelihoods.

“She became one of the first real not-for-profit CPA experts in the state of Arizona,” recalls Bruce D. Beach, CPA, who was a managing partner at BeachFleischman at the time. “She was very technically competent, and we had her build a not-for-profit team that really catered to that industry.”

BeachFleischman, which had traditionally been a general practice, began to have a specialized team in not-for-profits, led by McCloskey. Since then, the organization has expanded into other niches, like construction and real estate.

“The firm still functions at a high level in part because of the people she trained and mentored during her years there,” Beach explains.

Kelly L. Meltzer, CPA, is one of those mentees. As Meltzer took her first job in the industry after earning her degree, she crossed paths with McCloskey in 2000 at BeachFleischman. She remembers brainstorming solutions together and flipping through McCloskey’s paper copies of the Internal Revenue Code and the treasury regulations.

“She sparked enthusiasm in me for working with nonprofit clients, and that was the specialty I ended up

pursuing,” remembers Meltzer, who is a senior manager at the company. “She has the best reputation with the nonprofit community, and anybody who’s ever worked under Karen has always felt how much she wants to see people succeed.”

Outside of BeachFleischman, McCloskey volunteered her time with local nonprofits including the Tucson Botanical Gardens (TBG) where she served on the board for 15 years, including as president and treasurer.

“The Tucson Botanical Gardens, in my mind, is world class,” McCloskey says. “People come to Tucson to see venues like the this, and it’s one more place that helps me have a deep appreciation for the beautiful Sonoran Desert. To me, it was the most important charity work that I’ve done.”

She was treasurer during the economic downturn in 2008 and 2009. Only one year later, TBG was audited unexpectedly by the IRS.

“Karen is a nonprofit director’s dream board member,” says Michelle Conklin, executive director of the Tucson Botanical Garden. “[The audit] was made so much easier under the guidance of Karen. She lifted the burden off our shoulders.”

For the Profession

One of McCloskey’s most notable contributions to the profession was her 10 years with the Arizona State Board of Accountancy, including five years on the Law Review Committee and as president from 2013-2014.

The Law Review Committee updated the Board’s statutes related to the regulation of firms to make them more consistent with the Uniform Accountancy Act, and many updates were needed. Before the updates, the law still had the expectation that the exam would be penciled in on paper forms. Because of the significance of the updates, the Law Review Committee didn’t meet for the several years after, a testament to the committee’s diligence.

During that time, McCloskey spent a lot of time with ASCPA leadership

10 AZ CPA MARCH/APRIL 2023

as she navigated commitments to the Board and attended National Association of State Boards of Accountancy meetings. She also served on the ASCPA Board of Directors during the early months of the COVID-19 pandemic.

“The ASCPA is the only organization whose mission is to help the profession with their education, their reputation and applicable legislation,” McCloskey explains. “The connection between the CPA community and the Arizona Legislature is critical, and they’ve done such a good job at making that connection.”

Mark Lawrence Landy, CPA, served with McCloskey for several years on

both the State Board of Accountancy and the committee, which met monthly for 18 months to tackle the massive undertaking.

“Karen’s attention to detail and her listening skills made her an invaluable member of both the State Board and the Law Review Advisory Committee,” Landy says. “When she spoke, it was always to ask a pertinent question or provide a thoughtful solution.”

McCloskey is a firm believer that trust in the CPA profession is valued above all else.

“I have a real appreciation and gratitude to the profession that maintains the public trust; it makes me proud to be a CPA,” she says. l

Share your CPA Story

Be a part of Member Monday on LinkedIn and Facebook. This series highlights what ASCPA members and Arizona CPAs are passionate about when they’re not in the office, and you can get involved! Visit www.ascpa.com/ membermonday to fill out the interest form.

MARCH/APRIL 2023 AZ CPA 11

”

“The ASCPA is the only organization whose mission is to help the profession with their education, their reputation and applicable legislation.

Master This Tax Season

We can help. Paychex offers resources and tools to make tax season simpler.

Accountant Knowledge Center go.paychex.com/az-ahq

Free resources to help you stay current on information vital to tax season

•U.S. Master Tax Guide®, the authoritative tax resource

•Sales and use tax rate changes chart

•Payroll state and local withholding rules, forms, and tools

•Monthly spotlight and news links on industry topics

•Federal and state forms library and more

AccountantHQ go.paychex.com/az-ahq

• Manage clients’ payroll and HR data online from a single platform

• Acces s robust reporting, insights, benchmarking data

• Enhance your advisory role, at any time and from anywhere

Tax Facts: Tax Season Tools go.paychex.com/az-tax

• Ready-to-post listings of federal and state payroll and retirement rate information

• Customize with your firm’s name and address to send directly to clients

© 2023 Paychex, Inc. All Rights Reserved. | 02/09/232

of

HR

Paychex is proud to be the preferred provider

payroll, retirement, and

solutions for the ASCPA.

Help to Simplify Tax Season is Here | (877) 534-4198

Arizona CPA Foundation for Education & Innovation Donors

Thank you to our members for your generous contributions to the Arizona CPA Foundation for Education & Innovation in 2022. Your donations support accounting students on their path to becoming CPAs.

$1,000

Anita F. Baker

Linda M. Carneal

$750

Mark L. Landy

$500

Brenda A. Blunt

Glen C. Evans

Rufus Glasper

Vanessa R. Makridis

Cheryl J. Stanislawski

$100-$400

Jeanne M. Bentley

Rebecca K. Ciscel

David Allan Collins

Anne Cornelius

Rachael Crump

Thomas F. Duensing

Tyler J. Hamelwright

Julie A. Hein

Adela E. Jimenez

Kent D. Krueger

Gregory T. Leopard

Andrea B. Levy

Gabrielle M. Luoma

Philip J. Martens

Linda G. Murray

W. Gregory Nelson

David H. Richardson

Tess L. Ridgway

Eric J. Splaver

$50-$99

Melissa A. Coy

James V. Danovich

Tithi Debnath

Jeannette A. Delster

Vincent R. Gosz

Michael P. Kasten

James Marmel

Leonard Miller

Bejan Noorani

Carolyn S. Sechler

Kathryn J. Stroy

Linda S. Tansik

Luis R. Teran

Nancy Thomas

Michael A. Zongolowicz

Thank

Donor Spotlight

In September 2022, Cathy Laganosky completed a year-long leadership academy with Small Giants, targeted at not-forprofits and growing businesses looking to develop through investments in their customers and their teams. Paul Spiegelman, one of the Small Giants cofounders, gifted Laganosky with a grant to invest back into her community. She chose the Arizona CPA Foundation for Education & Innovation. Laganosky, chief financial officer at Pioneer Title Agency, is passionate about supporting accounting students.

With her service on education committees, she has seen the benefits of both scholarships and mentorship firsthand. Several former students from her time teaching business and accounting courses have gone on to be hired at her organization.

“I’ve learned how scholarships can impact their whole life and career,” she says. “I’m a firm believer that you are responsible to touch people’s lives as you go, knowing that many people helped me get to where I am today.”

The Arizona Foundation for Education & Innovation supports future accountants and grants scholarships to high school, undergraduate and masters’ students pursuing accounting. Since 1999, the Foundation has granted scholarship to more than 345 students across Arizona.

ascpa.com/foundation

If you are an Arizona CPA Foundation for Education & Innovation donor who would like to share their story, please email hmacdonell@ascpa.com.

MARCH/APRIL 2023 AZ CPA 13

you also to our members who donated other amounts throughout the year and with their annual dues renewal.

To learn more or to donate, go to www.

Right

now, there are thousands of victims of domestic violence living in fear across Arizona. Many of these innocent people will lose their lives at the hands of their abuser, unless we take action as soon as possible. You can donate your Arizona Charitable Tax Credit to A New Leaf and save the lives of domestic violence survivors across the Valley by providing safety and shelter. Donations to A New Leaf qualify for the Arizona Charitable Tax Credit up to $800 for a married couple, or $400 for singles. A New Leaf' QCO i Your donation will save a life by providing: Safe, secure shelter Food & basic needs Legal advocacy Counseling services 24/7 hotline support You can end domestic violence! Donate at TurnaNewLeaf.org/TaxCredit Your support can save families like Jessica and her daughter Emma from abuse! Save a life by making a tax credit donation or share this tax credit with your clients

Key Steps for Tax Risk Management

By Suzanne Holl

By Suzanne Holl

CPA liability exposures during tax season are always a concern. However, liability exposures during this tax season are even more exacerbated given the added complexities with increased economic and tax-specific relief measures. As a reminder, here are some actions that practitioners can take to successfully manage risk exposures.

Defensive documentation is essential to successfully manage risk exposures; practitioners need to be proactive, not reactive, with their written documentation in today’s litigious environment.

My experience in liability insurance shows that many high-exposure tax claims have certain characteristics in common, primarily as follows:

• The services for which clients engaged the CPA were unclear.

• The CPA did not clarify his or her role or the client’s expectations, usually because an understanding between the CPA and the client was never reached or adequately documented.

• A lack of clarity and documentation made the CPA’s services difficult to satisfactorily complete.

• Inadequate documentation makes it difficult to defend the CPA in future malpractice actions.

Continued on next page... MARCH/APRIL 2023 AZ CPA 15

Documentation, or the lack thereof, is always a critical factor in any claim, and the engagement letter is the first line of defense. A welldefined engagement letter clarifies the services that you will render, describes the scope and limit of the engagement, and delineates, in limiting language not only the scope of the engagement, but you and your client’s responsibilities.

Documenting the understanding between you and the client minimizes the likelihood of litigation, because a well-constructed engagement letter leaves little or no room for misunderstandings which could result in “expectation gaps” – the root cause of many lawsuits. If you do find yourself in the middle of a lawsuit, then the engagement letter will evidence the duties your firm was to perform.

Always try to receive a signature on the engagement letter. Failure to do so may be interpreted by the courts as the client not agreeing to the terms of the engagement. Proceeding with the requested work without a signature could also suggest that you completed the engagement under terms different from those contained in the unsigned engagement letter. In limited situations like lower risk tax engagements, the use of a well-crafted unilateral clause may be appropriate as it establishes actions that if taken, acknowledge the client’s acceptance of the engagement letter’s terms and conditions. Although this type of clause is not quite as compelling as having a client signature, it provides some protection.

Defensive Documentation

Always follow up on significant client meetings and discussions with defensive documentation. Provide attendees with a synopsis that includes the date, the participants’ names, the matters discussed, the action items and who is responsible for each. Following up significant meetings or discussions with documentation will ensure that you and the other parties are proceeding with the same expectations and

assumptions and will provide excellent defensive documentation should someone later allege that something else was discussed, they weren’t present or you were responsible for taking actions you had not agreed to.

Client notifications are a helpful risk management tool to document your communications regarding updates of significance. Jury research shows that the public, including clients, perceive that the CPA’s fundamental job is to “advise and warn” – to advise clients of opportunities and to warn them of risks. The fast pace of change adds complexity and challenges to tax compliance. It is important to have written documentation with clients to avoid expectation gaps. For example, critical changes to the application of economic and tax relief measures and the new rules associated with sales and local tax workaround initiatives are important issues to communicate in writing to clients to mitigate the possibility of client expectation gaps.

Draft additional engagement letters when necessary. New engagement letters are sometimes needed to avoid engagement creep and/ or client expectation gaps when the additional services require management to acknowledge and accept certain terms and conditions not stipulated previously. When CPAs carefully memorialize an expanding engagement, it is significantly more difficult for clients to hold CPAs responsible for matters outside the scope of the engagement letters.

Informed Consent Letters

In certain situations where there may be different tax alternatives available to the client such as estate tax planning, CAMICO encourages the use of “informed consent letters.”

The informed consent letter clarifies what the CPA advises and informs, and the client ultimately decides which action they wish to take. Without such a letter, claimants can allege that the CPA made the decisions on behalf of the client.

This type of defensive documentation minimizes potential liability exposures were the client to later assert that your firm is responsible for unexpected events or less than optimal results.

Avoiding Collection Problems

The best way to avoid having a collection problem is to detail your fees, billing and collection policies in your engagement letter. Consider including a fee estimate, noting that unforeseen circumstances or changes in the engagement could necessitate revisions.

Retainers and Deposits

Most ongoing engagements lend themselves to the use of retainers or deposits. These options may be best for clients that are slow paying, financially stressed or have yet to establish a payment history with you. The engagement letter clause should clearly state that retainers are not an estimate of the total cost of the engagement, do not earn interest, must be paid before work begins and if depleted, must be replenished before work continues.

Stop-Work and Disengagement Clauses

CAMICO encourages the use of a stop-work/disengagement provision which can be enforced if a client doesn’t pay in accordance with the terms of the engagement letter. The clause stipulates that if the client does not pay the firm, the firm can stop services without incurring any liability to the client for doing so. The enforcement of this clause significantly reduces the risk that your firm feels compelled to continue to incur ever growing fees when the client has yet to pay for prior services. The closer to a deadline this clause is triggered, the greater the exposure to the firm. Don’t wait until right before deadlines or due dates to stop work. Work stoppages close to a deadline increases the likelihood the client will claim you (not they) breached the contract.

16 AZ CPA MARCH/APRIL 2023

Alternative Dispute Resolution

When used appropriately, mediation and arbitration can significantly reduce the cost and the emotional rollercoaster of disputes. CAMICO recommends adding clauses to engagement letters calling for mediation to resolve all disputes and then binding arbitration for fee disputes not resolved during the mediation.

When there is a fee dispute, the firm should inform the client in writing that, unless paid within a specified number of days, the firm will initiate mediation to settle the matter. Using the mediation and arbitration process to settle fee disputes is more effective than litigation, though there is no guarantee that the whole amount owed will be collected. The process itself may prompt some clients to pay some or all the outstanding fees. Filing suit to collect outstanding

fees often triggers a countersuit. CAMICO’s claims history indicates binding arbitration to resolve fee disputes is the safer and more effective alternative.

We advise CPAs not to use a general arbitration clause in an engagement letter. Most engagements, when in dispute, tend to produce complex, high-risk, high-dollar disputes that are better managed through litigation than arbitration. An effective legal defense can be restricted and impaired by arbitration.

Suzanne M. Holl, CPA (licensed in CA), is senior vice president of Loss Prevention Services with CAMICO ( www.camico.com ). With almost 30 years of experience in accounting, she draws on her Big Four public accounting and private industry background to provide CAMICO’s policyholders with information on a wide variety of loss prevention and accounting issues.

Looking For New Business? As a member, you can register for the Find a CPA referral directory. The directory is a free resource for you and the public. If you are already listed, review your information to ensure it is up to date. Access your account by logging into your ASCPA profile and selecting the Join a CPA Referral Service button. Learn more: www. ascpa.com/find-a-cpa OF THE LOOKING TO GET OUT FAST LANE? www.apexcpas.com CONTACT US TODAY! 623.250.6544 JAMES CHAKIRES CPA, CVA Managing Partner revenue and are looking to merge? We are interested in Do you own a successful accounting firm up to $1 million in WE CAN HELP! and business. Reach out today to start the conversation. commitment to success, you can trust Apex with your clients exploring that opportunity with you. With our relentless MARCH/APRIL 2023 AZ CPA 17

l

What’s Happening at the ASCPA?

Governmental Accounting Conference

FEBRUARY 3, 2023

For over 35 years, GAC has updated ASCPA members and accounting professionals on the industry’s hot topics. This year, the hybrid event had sessions on the GASB, inflation, corruption and more.

Thank you to our Governmental Accounting Conference planning committee for their insight and support!

Board Meeting

JANUARY 25, 2023

The ASCPA Board of Directors received updates on the Arizona legislative session, trends in learning needs and CPE, and results from student research at the latest board meeting.

Behind the Scenes at Reid Park Zoo

JANUARY 6, 2023

Members went behind the scenes at Reid Park Zoo in Tucson. They enjoyed a private, after-hours tour of the zoo and met two animal ambassadors. Reid Park Zoo’s President & CEO Nancy Kluge presented on their unique public-private partnership that unites vendors, nonprofit organizations and governmental entities to conserve wild animals and wild places.

18 AZ CPA MARCH/APRIL 2023

CPA Day at the Capitol

FEBRUARY 6, 2023

The second annual CPA Day at the Capitol connected ASCPA members and Arizona legislators. The ASCPA continues to be a resource for all Arizona policymakers on matters of accounting, finance, tax and business. We have our dedicated members to thank for sharing their expertise. Our volunteers were also treated to a tour with Arizona State Treasurer Kimberly Yee.

Get Involved

Legislative Scoop

March 17, 2023

www.ascpa.com/scoop

Each 30-minute webinar brings you inside the Arizona policymaking process with our advocacy team and a state legislator. The biweekly series will keep you updated on the impacts to the profession until the end of June.

Phoenix Tax Workshop

April 22, 2023 I ASCPA Learning Center & Webcast

www.ascpa.com/ptw

Professional Issues Update, Tucson

JANUARY 10, 2023

President & CEO Oliver Yandle made his final stop on the Professional Issues Update tour in Tucson at Pima Community College’s downtown campus. Those in attendance learned about and discussed pipeline and recruiting, emerging audit and tax issues, the changing landscape of technology and the current legislative and regulatory environment.

Annual Meeting & Awards Luncheon

May 18, 2023 I Arizona Biltmore

www.ascpa.com/annual

Celebrate the past fiscal year of achievements with the ASCPA! Our premiere event of the year brings together honorees including our outgoing chair, our newest Life Member and the 2023 Excellence in Teaching recipient.

Join this elite group of tax professionals for a Saturday CPE/CLE sessions on trending hot topics in tax. Want to try a session before committing to the annual series program? Attend a single session for $70. If you decide to register for the annual series, the single session’s fees will be applied toward your annual fee.

MARCH/APRIL 2023 AZ CPA 19

18 May 2023 11:30 a.m. - 1:30 p.m. ascpa.com/annual ANNUAL MEETING AWARDS LUNCHEON & Join us at the Arizona Biltmore for the annual celebration! Karen K. McCloskey, CPA, MST 2023 Life Member Rachael Crump, CPA, CGMA Outgoing Chair To Be Announced Excellence in Teaching Award To Be Announced Keynote Speaker AWARDEES & INNOVATORS PREFERRED PROVIDERS

Guiding Clients to Their Lasting Legacy

By Patricia J. Elder, CPA

CPAs have a wonderful opportunity to help clients realize their philanthropic vision. As a trusted advisor, you hold unique knowledge of their personal and financial goals, but do you know about their charitable goals? Having a meaningful discussion and exploring the possibilities for planned gifts can provide them advantages today and serve to deepen your relationship.

Continued on next page... MARCH/APRIL 2023 AZ CPA 21

In my role as a nonprofit hospital foundation planned giving officer, I work with individuals that wish to leave a gift to charity through their estate plan, most often through their will or trust. In many cases, they are already deeply connected to a charity, having made gifts of support but wish they could do more.

It can be enlightening when clients learn the many different opportunities available for making a significant planned gift with greater impact than is possible for them today. A planned gift enables them to leave a lasting legacy by providing for the people and causes that matter most to them. It can serve to express their loyalty or gratitude to a charity or may represent how they wish to be remembered.

By introducing your clients to the wide variety of planned gift options available, together you can determine what tool best meets each individual’s needs and preferences. Gift plans range from simple to complex, current or deferred, and some provide financial and tax benefits today. Here are some of the most common types of planned gifts:

• Bequest: A bequest is an easy and flexible way to provide a gift to charity by documenting your intentions in a will or trust. The gift may be a percentage of the estate, a specific dollar amount or other asset, or the residue of your estate. The gift will transfer to the charity upon death and is not subject to federal tax. A bequest provides flexibility in that it can be changed, and you can use and control your asset throughout your lifetime.

• Beneficiary Designation: The most simple and affordable way to leave a gift to charity is to designate it as a beneficiary on a retirement, investment or bank account, or life insurance policy. As with a bequest, you maintain

full control of these assets during your lifetime and have the flexibility to make changes at any time. Gifts of IRA and retirement assets transfer tax-free to charity.

• Charitable Gift Annuity: This is a gift made to charity that provides you and/or your beneficiary with fixed payments for life. You receive a charitable income tax deduction for the charitable gift portion of the annuity. The charity receives the remainder after all payouts have been made. For a charitable gift annuity funded with cash, a significant portion of the annuity payment will be tax-free. A gift of appreciated securities can also be used to fund a gift annuity and avoid a portion of the capital gains tax.

• Charitable Remainder Trust: This gift also provides income and tax benefits. When you transfer cash or an asset to fund a charitable trust, you receive a charitable income tax deduction for the charitable portion of the trust. If the trust is funded with appreciated assets, the trust will then sell the asset tax-free and provide you or any other beneficiaries with income for a life or lives, a term of up to 20 years or a life plus a term of up to 20 years. At the end of your life or the trust term, the remainder of the trust will pass to the charity or charities that you have named as beneficiaries.

• Charitable Lead Trust: This trust allows you to pass on assets to your family while reducing or eliminating gift or estate taxes. You can fund a lead trust which pays income to charity for a number of years and receive a gift or estate tax deduction at the time of the gift. Your family receives the remainder of the trust assets plus any additional growth in value at the end of the trust term.

• Real Estate: You can deed your property outright to charity or implement a Life Estate strategy which provides you with a current charitable income tax deduction for making a future gift of your home, vacation home, farm or ranch to charity now, while allowing you the right to continue to use the property for the rest of your life.

When your clients include charity provisions in their estate plan, they will have peace of mind supporting a cause important to them and live every day knowing they have done something meaningful, something lasting. You can play an important role by incorporating philanthropic planning in your conversations.

As a CPA you may also want to consider volunteering with a nonprofit and lending your expertise on their planned giving committee. For example, at HonorHealth Foundation our Financial Health Advisor Council is comprised of CPAs, attorneys, trust officers, certified financial planners and insurance professionals. Our Real Estate Committee manages donations of real property. Both groups provide valuable counsel, explore strategies on gift planning and complex gifts, and facilitate introductions between their connections and our organization. I encourage you to explore nonprofits and foundations that support causes you’re interested in to find opportunities that are a good fit.

Volunteering with a charity in this way builds your professional expertise, and directly benefits your clients. But more importantly, your guidance will provide your clients with a sense of peace and pride that their careful planning will leave a lasting legacy. l

22 AZ CPA MARCH/APRIL 2023

Patricia J. Elder, CPA, MBA, CAP®, is Vice President of Planned Giving at HonorHealth Foundation. She can be reached at pelder@ honorhealth.com.

Desert Willow Conference Center and via webcast · June 23, 2023

KEY TOPICS

AUDIT

ENDOWMENTS

INSURANCE FORECAST

FRAUD

See full agenda at ascpa.com/npcagenda

Platinum Sponsor

FRIDAY, JUNE 23, 2023

Register: ascpa.com/npc

Are you a CPA or professional working with nonprofit organizations? NPC provides specific, practical coverage of critical nonprofit accounting, tax and legal issues. In one day, our knowledgeable experts and speakers will get you up to speed on the most pressing issues of the industry.

Gold Sponsors

CBIZ & MHM

CLA (CliftonLarsonAllen)

Fester & Chapman, PLLC

Heinfeld, Meech & Co., P.C.

Innovest Portfolio Solutions, LLC

R.O.I. Properties

Your Part-Time Controller, LLC

23

NOT-FOR-PROFIT CONFERENCE

P

N

The Death of Deducting

Litigation

Expenses: What’s Next?

By William Rothrock, CSSC

Over the next three-plus years, can you help your corporate clients defray litigation costs that lost deductibility after 2017?

Examining the different sections of the Tax Cuts and Jobs Act (TCJA) illuminates the enormity of the change. However, looking beyond the TCJA provides a possible solution to the loss in deductions.

24 AZ CPA MARCH/APRIL 2023

Section 11045 of the TCJA eliminated the deductibility of all expenses subject to the 2-percent rule through the year 2026. Sections 13306 and 13307 further refine eliminating deductible expenses related to litigation. Specifically, identifying fines, whether punitive or penal legal fees, and the inclusion of “non-disclosure” agreements in cases of a sexual nature are no longer deductible expenses. A recent court case further narrowed the deductibility of legal expenses as capital versus immediately expensed.

Case Precedent

In Mylan v. Commissioner, 156 T.C. No. 10 (April 27, 2021), the IRS took the position that the legal cost of defending a patent infringement case needed to be capitalized. The line determining the deductible status of litigation expenses starts at the nature of the litigation. What types of litigation apply after the passage of TCJA? If litigation arises in pursuit of profit-seeking activity, the cost of litigation can be expensed. Does the Mylan case indicate a clear understanding of what constitutes profit-seeking behavior? Mylan’s litigation defense against patent infringement arose through the pursuit of profit indirectly, forcing them to capitalize the expense. Mylan’s litigation expense was directly attributable to creating a generic drug and qualified for an immediate expense by the company.

What Remains Deductible?

The litigation costs incurred defending a company from the government, plus remedial or compensatory damages, continue to be deductible. However, fines, penal or punitive, are not deductible. Thus, profit-seeking and government-related litigation are deductible. But what about employeerelated litigation mentioned above? Clearly, defense against allegations of sexual harassment and abuse does not qualify as profit-seeking behavior. However, the TCJA explicitly addresses this form of litigation.

The TCJA eliminates the deductibility of all the associated litigation expenses for cases related to actions of harassment and abuse. Notably, including a non-disclosure agreement as a settlement term reinforces the non-deductibility of litigation expenses.

The CPA’s Role

How can CPAs help clients mitigate the cost of litigation? First, consider 26 U.S. Code § 104 –compensation for injuries or sickness. Employee cases related to harassment, sexual and otherwise, and sexual abuse do not qualify under 26 U.S. Code § 104. The proceeds the employee receives in settlement from the company constitute income taxable at the state and federal levels. The tax issue allows a CPA to help the defense litigation team reduce the settlement expense. Moreover, introducing a structured settlement for the client’s consideration allows the defense to reduce the actual cost of settling the case. Why? The constructive receipt doctrine determines when the income realization occurs for the plaintiff. When considering this doctrine, the savings become clear to both parties when using a simple settlement. Consider the following example:

• A settlement of $1 million taxed at a federal applicable rate for those married filing jointly leaves the plaintiff with $693,478.75 in disposable income before state tax.

• Using an annual payout over three years reduces the tax liability, thus increasing the disposable income by $109,635.63 to $803,113.38.

• In addition, if the parties agree to split the benefit, it reduces litigation costs by 5.48 percent for the defense.

• Using a structured settlement, the plaintiff’s disposable income increases by $54,817.32. The defense sees their cost to fund the settlement reduced by the same amount.

When structured settlements originated, this form of needs-based cooperation represented an industry standard. Although larger insurance carriers know structured settlements, they are less aware of this particular strategy.

The TCJA severely restricted the deduction of litigation expenses where only the pursuit of profit and government defense remains deductible. Utilizing strategies like offering the plaintiff a structured settlement option opens avenues to reducing the client’s litigation cost. l

William Rothrock, CSSC, is a settlement consultant at Brant Hickey and can be reached at wrothrock@branthickey.com. Reprinted with permission of the New Jersey Society of CPAs, njcpa.org

MARCH/APRIL 2023 AZ CPA 25

Fees: Members: $25 Nonmembers: $40

Online Access

Go to www.ascpa.com/quickquiz to access links to all active quizzes. Once a quiz is purchased, a link and password will be emailed to you. Your results will be sent immediately after completion, and certificates are emailed within five business days.

Looking for the Classifieds? Visit the ASCPA website to find the Classifieds section and posted jobs. You might find a practice for sale or your next big career move. Go to the Classifieds: www.ascpa.com/ classifieds

one hour of CPE credit in specialized knowledge by completing the AZ CPA Quick Quiz, available online. Receive a score of 70 percent or more about this issue’s articles for credit.

that easy!

Earn

It’s

You’ve Read It, Now Get Credit MARCH/APRIL 2023 AZ CPA 27

AZ CPA Quick Quiz

4801 E. Washington St., Suite 180 Phoenix, AZ 85034-2040

CONNECT

to your ASCPA community resources

The ASCPA Connect site is a resource that can help you solve professional conundrums. A network of over 4,400 colleagues and 20 specialty communities can help guide you when you need it most.

Get started: connect.ascpa.com/home

Find answers & more on Connect:

We are looking for a web-based 1099 provider that we can use to process 1099s for clients. Any suggestions?

How would the S-corp return be prepared if U.S. GAAP financial statements are now prepared starting back a couple years and for subsequent periods?

Is there a way that this second home might be a business expense?

What is the deductibility of assisted living costs as expenses?

Who is responsible for Fbar reporting, the nonprofit or the individual or both?

PRSRT STD U.S. Postage PAID

ADDRESS SERVICE REQUESTED

Phoenix, Arizona Permit No. 952