5 minute read

Common Cents

Common Cents Cash Flow & Budgeting Simplified

Ending the Endless Failure of New Year’s Resolutions! Part II

Advertisement

By Elliot Pepper, CPA, CFP®, MST

As a recent college graduate entering the workforce, married with two young children, and the proud new title of CPA after my name, I recall vividly exclaiming to my wife, “Don’t worry, you are married to an accountant, I am going to meticulously track our budget in a beautifully maintained spreadsheet and every dollar will be carefully accounted for!” I had a whole plan - every month, I was going to download PDFs of my credit card and bank statements and track all of my income and spending by category. I even had Excel formulas that would change colors depending on the direction of my cash flow for the month. I had a plan, I started to follow it, and by the end of March, I was done…

Fast forward 12 years and while I have added some letters to my professional name, lost some hair, and gained a few pounds, that spreadsheet is still only stubbornly updated though March 2010.

This article is not about how great it is to just “wing it” when it comes to money management nor is it about how failure to account for every penny spent every month is a cardinal sin. This article is about appreciating the fact that most people would prefer spending Saturday nights watching a movie or spending time with friends and family (or writing their personal finance blog ;)) rather than reconciling credit card statements. Yes, it is possible to get your Saturday nights back without sacrificing fiscal responsibility, and this article will tell you how.

The “Gut Check” Cash Flow: From 10,000 feet

While it is easy to get caught up in the short term volatility of cash flow in our accounts, the simple rule is that, over time:

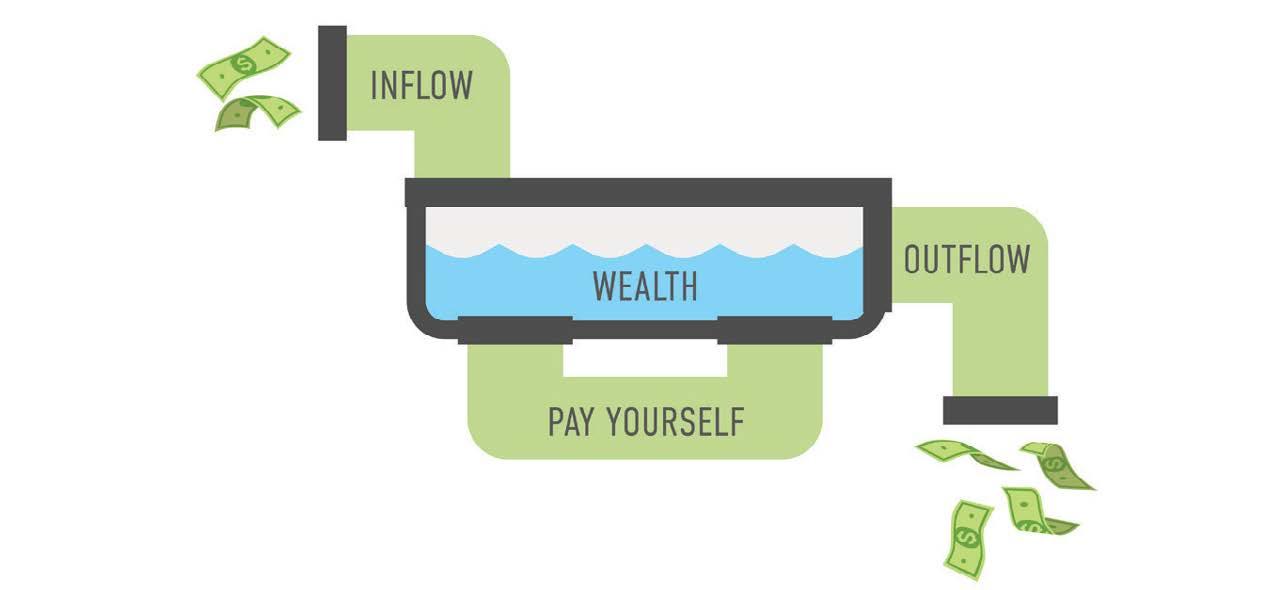

Cash Inflows + Savings/Investment > Cash Spending

A perfect way to test your adherence to this rule is to simply tally up the total balance in your checking and savings account on the first statement of 2021 and then again for the last statement. Add any amounts that you transferred to another savings or investment account, but not if those were deducted from your paycheck. If the change is positive - congrats! You met the simple rule for 2021. If not, it’s time to understand why, and fix it.

You have three choices, listed in order of preference: 1. Increase Inflows: Find ways to increase your income 2. Decrease Spending: Reduce spending on those items that you can 3. Decrease Savings/Investment:

Ignore this step until you have honestly addressed #1 & #2

You can do this easily on a piece of paper or in a simple spreadsheet. E-mail commoncents@Northbrookfinancial.com for a copy of our very easy to use Excel “Cash Flow at 10,000 Feet” template.

The Review & Automated Guardrails

The Review: Review your annual credit card statement report, or download the last 3 months’ worth of bank and credit card statements. Categorize your monthly (or annual) spending by the necessary “have to”s and the discretionary “want to”s. Pay attention to these categories and cut out any unnecessary expenses you see (subscriptions you never use) and see if there are any necessary expenses that can be revisited (internet/cable, car insurance). These are the “low hanging fruit” of personal finance and are simple enough tasks that can be done once or twice a year. Automated Guardrails: Set up an automatic monthly transfer from your checking to your savings or investment account. How much? Well, for starters, consider taking the difference between income and spending and automate that as a monthly transfer. An automated savings strategy provides so many benefits: • Keeping yourself to the simple rule from above: Cash Inflows + Savings/Investment > Cash

Spending • Continuously purchasing investment assets, no matter the market conditions. • Shifting from cash to assets that will turn into more cash in the future • Potentially saving on taxes • Strengthening your net worth

More important than the amount that you contribute is just doing it. The habit of automated savings will pay huge dividends (literally!). If you already have a fully funded Emergency Fund, start contributions to an investment account (IRA, 401K, Brokerage). Invest early, and invest often!

You can use many free online budgeting apps to help with both the “Gut Check” and “The Review& Automated Guardrails” referenced above. Email commoncents@Northbrookfinancial.com for an Excel version of our “Review Template.”

Tracking spending, savings, and investing is important. Being realistic about what one should do and will do is just as important. If you are having trouble meeting the “Simple Rule” identified above, then yes - getting into the weeds of your spending habits is important, but it is not a lifelong sentence. Once you are compliant with the Simple Rule, you can step back and feel good that your spending habits are not going to bankrupt you, and can use the automated guardrails to go from a stagnant net worth to a growing net worth. While managing spending is important, the real goal is to manage cash flow today and set a foundation to accumulate wealth. By focusing on this goal, less time can be spent on tedious expense tracking, allowing for more time spent on setting financial milestones and tailoring behavior to reach them. A practical understanding of Cash Flow Management will let you stress less about money, leaving more room to just enjoy life!

Take back your finances in 2022 without spending endless hours crunching numbers. Follow the Simple Rule of Cash Flow, make some tweaks and set up your guardrails - and enjoy that movie with your family this Saturday night!

Cash Inflows + Savings/Investment > Cash Spending

The decision to start saving and investing is yours, but the “how” can be hard. We suggest speaking with a “fee only” financial planner operating as a fiduciary - having a CPA or tax background is a huge plus. Email commoncents@northbrookfinancial.com to schedule a free financial planning consultation with our team.

Elliot Pepper, CPA, CFP®, MST is Co-Founder of Northbrook Financial, a Financial Planning, Tax, and Investment Management Firm. He has developed and continues to teach a popular Financial Literacy course for high school students.