DIGITAL REPORT 2022 A Transformative Year: LendingClub’s Digital Marketplace Bank

A Transformative Year: LendingClub’s Digital Marketplace Bank 2 lendingclub.com

LENDINGCLUB

The financial health crisis is here. People are suffering amid a rising cost of living and debts are mounting as disposable incomes shrink to cover spiralling living costs. Saving money and lowering outgoings for millions of households, globally, is now a necessity.

Innovation in finance is driven by disruption, and one contender leading the charge began life as a technology company specialising in data but has now transformed into one of America’s fastest growing digital banks.

Strictly speaking, LendingClub defines itself as a technology/financial services company. Founded in 2006, innovation and marketplace disruption is embedded at its core, says Scott Sanborn, CEO, who joined the company in 2010. A passionate advocate of the work LendingClub does, Sanborn says its services have never been needed more than they are now, as consumers find themselves pushed to – and, in some cases, beyond – their financial limits.

At its core, LendingClub offers lowercost lending services to borrowers than traditional banks. It’s able to do this because it acts as a broker pairing institutional investors with would-be borrowers.

Persado is the only Motivation AI platform that enables personalised communications at scale. Leading financial institutions including Ally Financial, JPMorgan Chase, and LendingClub rely on Persado to generate hyper-personalised communications. Persado’s top 30 customers have recognised over $1.5 billion in incremental revenue.

Learn more about Motivation AI at www.persado.com

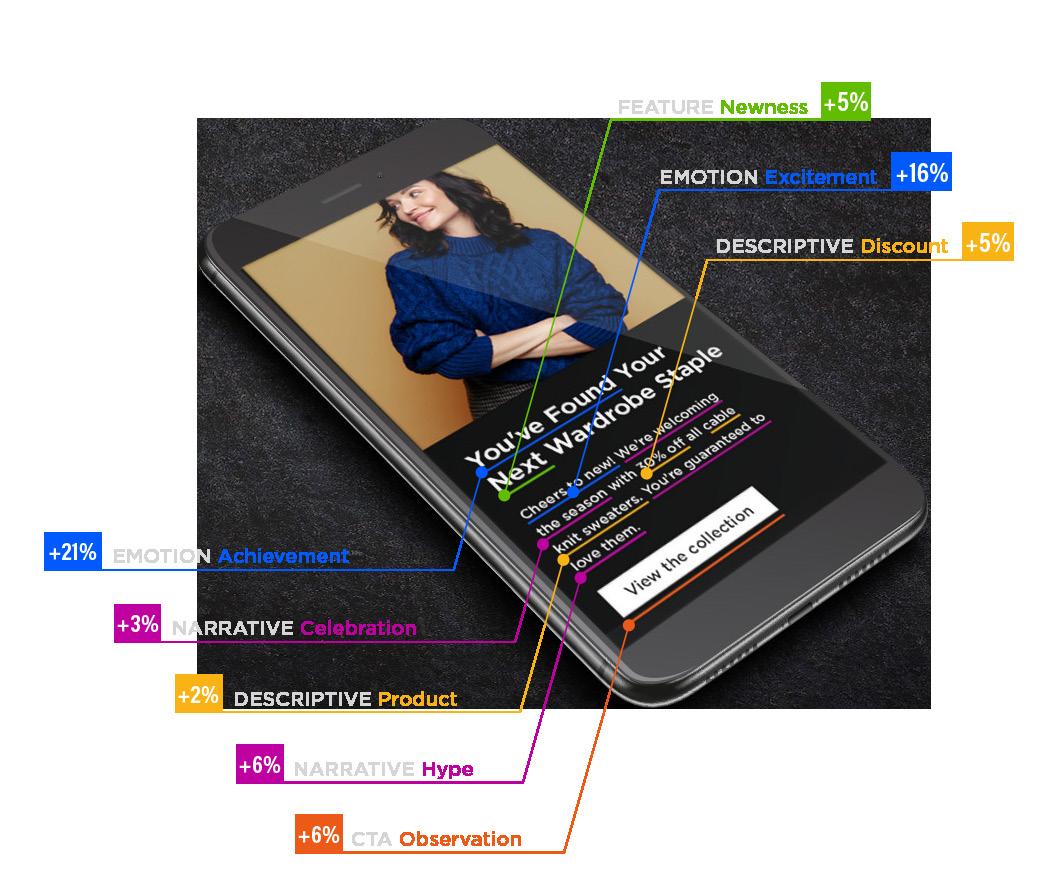

Persado’s Motivation AI platform enables personalised communications at scale, delivering incremental value to global brands

It’s one thing to know about your customers, quite another to utilise customer data to motivate and inspire them. Persado’s Motivation AI platform leverages a vast language knowledge base, advanced AI and machine learning (ML), and a decisioning engine, to deliver the precise message that motivates customers to engage and act. The result has been an impressive revenue lift and hundreds of millions of dollars in incremental value for some of the biggest companies in finance, retail, telecommunications, and other fields. Brands like JPMorgan Chase, Michaels, Gap, M&S, Dropbox, LendingClub, and Verizon rely on Persadoto generate hyperpersonalised communications.

Alex Olesen, head of Persado’s vertical strategy practice, says: “We underwrite every client partnership to project how much incremental revenue Persado can drive for our clients. We also build real-time performance reporting so our clients can see the actual uplift we are driving throughout the duration of the partnership.”

Persado is the only Motivation AI platform that enables personalised communications at scale. Digital communications present the largest opportunity to attract and build customer lifetime value. However, digital overload causes conversion rates to degrade quickly.

“It is typically not that an organisation’s offer or value proposition is unappealing, but that the brand needs to go the next step to motivate engagement and action,” Olesen says. “With the

Motivation AI platform, the top 30 Persado customers alone have recognised over US$1.5bn in incremental revenue.”

Marketers are tasked with driving growth and opening up channels of revenue. Few realise that inspiring and motivating customers to act contributes the majority of the conversion attribution. For example, Persado is working with LendingClub’s marketing department to help manage campaigns across all channels and banking products and develop optimised messaging across emails and marketing campaigns.

In 2021, LendingClub drove growth through marketing campaign enhancements enabled by Persado’s Motivation AI platform.

Customers can take advantage of an array of lending products from personal and business loans to auto refinancing and patient solutions.

The system is remarkably effective – and, says Sanborn, routinely cuts loan repayment interest charges significantly, because it puts the customer's interests first regarding their finance requirements.

He explains: “Imagine you’re going to buy a car from a dealership. Currently, in the majority of the sales, you are going to pay more for the finance than your risk would indicate. The dealer adds a markup. There's no cap on how big that markup can be. And they are not required to pass you to the lender that gives you the best deal. They may also be passing you to the lender that gives them the best fee break or rate or incentive. So, you spend all this time picking a car, negotiating the price, but you don't negotiate the cost of your financing. You drive off the lot paying more than you otherwise should.

“That’s where LendingClub comes in: using its technology platform, it can match borrowers with the best lending plans, making them vital savings in the process.”

SCOTT SANBORN CEO, LENDINGCLUB

Consumers now see banking as a thing you do, not a place you go, and they are increasingly saying that the strength of the mobile experience is what should be the driver of choice

LOCATION: SAN FRANCISCO, USA

Scott is the CEO of LendingClub, the only full-spectrum digital marketplace bank at scale, which has helped more than 4 million Americans save billions of dollars since it was founded in 2007.

Appointed CEO in 2016, he is responsible for leading 1,000+ employees to achieve the company’s vision to put members on a path to financial success, as the business evolves beyond its personal loan heritage to serve a broader set of customers’ needs by taking advantage of its technology and data-driven marketplace.

Scott joined LendingClub in 2010 and has been a driving force in the management and development of the organisation. With executive roles as Chief Marketing Officer, Chief Operations Officer, and President, he helped steer the company through a prolonged period of tripledigit growth running up to its 2014 IPO, the largest tech IPO that year. Prior to LendingClub, Scott held leadership positions as the Chief Revenue Officer for publicly-traded eHealth Insurance, President of RedEnvelope, Inc., and SVP at the Home Shopping Network.

He holds a BA from Tufts University.

Experian Marketplace is helping consumers to save money in tough times, thanks to its D2C business, its credit bureau and its partnership with LendingClub.

Within Experian’s direct-to-consumer (D2C) business, Experian Marketplace, it has assembled a network of lending partners who allow the company to serve offers to its broad consumer base. The core Marketplace mission centres around data, personalisation, and how they can be used to improve financial inclusion and restore financial power for consumers.

Marketplace uses its relationship with Experian’s credit bureau to prop up unparalleled advantages, including the ability to scale pre-approved programmes quickly. It also allows Experian to operate across multiple verticals including credit cards, personal loans and – since the acquisition of Gabi in November 2021 – digital insurance.

That variety ensures consumers receive the support they need to save money –something which is really important in light of current macroeconomic conditions.

“Currently, 76% of consumers will see a pre-approved offer,” says Rakesh Patel, SVP – Marketplace for Experian. “We want to take that to 100% of all consumers.”

Patel, who started life at Experian 15 years ago, knows there are parts of the credit ecosystem that are broken: “In the US, when you want to start a credit relationship, the easiest way is to apply and get declined. That’s not a consumer-friendly value proposition. Experian has tackled that by saying people no longer need to get declined for anything in order to start a credit relationship. They can come directly to Experian through Experian Go and start their credit relationship on a positive note.”

Experian has a longstanding relationship with LendingClub, which has allowed it to create unique experiences for consumers. Patel believes the partnership will transform how Experian engages with customers: “LendingClub and Experian Marketplace have a vested interest in putting consumers at the heart of everything we do. With our vision of financial empowerment for all, LendingClub gives us that ability to provide proactive engagement with our consumers around offers they may be pre-approved for.”

SCOTT SANBORN CEO, LENDINGCLUB

Sanborn says that, at a customer level, LendingClub makes significant monthly savings on outgoings. “On average, we're saving customers about $80 a month versus their car loan. Imagine – you drive the same car, pay it off in the same time frame, but have $80 more a month in your pocket.”

Expanding financial services through M&A Clearly, the formula is working. To date, the fintech has helped more than four million

customers and is the US market leader in one of the fastest-growing categories of lending: credit.

In 2021, LendingClub also bought into the banking sector through its acquisition of Radius Bank, where it obtained their bank charter. This event has seen the company expand significantly, transforming its identity within the fintech industry. So, is it a fintech, a digital bank, or something else entirely?

How should finance industry marketers respond to an uncertain economy? Marketing budgets may have been cut, but not expectations for results. Read Quad’s latest white paper, “The New Lending Landscape,“ for a comprehensive review of changing consumer behaviors and strategies that will help FI marketers succeed.

“I would say we are a technology company… but we're a technology company with a banking charter, making us a fully-digital marketplace bank. We are something truly different. There are some direct-to-consumer banks, but we are becoming a digital marketplace bank at a time where there's a lot of change in consumer preference.”

Sanborn points out that, a decade or more ago, what drove customer preference for banking was the location of a bank branch. The landscape is now significantly different. “Consumers now see banking as a thing you do, not a place you go, and they are increasingly saying that the strength of the mobile experience is what should be the driver of choice. So, our transition to digital

banking is at a time when consumers are valuing the digital experience, and we can therefore provide a tremendous amount of value to our customers.”

The disruption of traditional lending LendingClub has a history of disruption within lending and Sanborn believes the disruption of traditional credit models has been long overdue because, fundamentally, it charges the customer far more than it should. “If you look at credit cards as an example, credit card companies separate their customers into two categories.

Revolvers – those are people who don't pay off the credit card balance; they have a loan. And then there's transactors – those are the people who use the card as a convenience mechanism and they pay it off every month. Those transactors are getting benefits. They're getting rewards, miles, cashback, and all of those things. The revolvers have to pay for that.

“So, you have one half of the customer base paying for the other half of the customer base. That's structural inefficiency. If you just looked at that customer and said, ‘Hey. What is the true cost of credit that you need?’, you'd find that it's lower. That's what we do with personal loans.”

As well as taking a dynamic approach to lending, LendingClub is unusual in that its core business model increases financial inclusion by expanding access to lower cost credit. The company takes the approach that current customers and the system are ripe for a revamp. While LendingClub’s marketplace model enables it to seamlessly serve a broad range of customers, its core customer has a relatively high FICO score of around 700 and an annual income north of $100K. The team focuses on providing borrowers that are charged over the odds by lenders, such as women and minority groups, with a far better deal.

“Our customer is highly banked,” he says. “In fact, they're 100% banked. They're just not well-served. It's working out better for the banks than it is for them. What we are doing for them is providing a nationwide digital solution that disproportionately helps people who are living in areas where bank branches are closing, because more and more bank branches are closing every year.”

LENDINGCLUB HAS SERVED MORE THAN FOUR MILLION CUSTOMERS AND IS THE MARKET LEADER IN ONE OF THE FASTEST-GROWING CATEGORIES OF LENDING: UNSECURED CREDIT.

From FinTech’s early days, TransUnion has proudly partnered with LendingClub — helping expand financial inclusion to millions of consumers through leading trended credit and alternative data. We celebrate LendingClub’s success and our collaboration which continues to deliver state-of-the-art innovation and growth.

We celebrate our 15+ year partnership with TransUnion. TransUnion has actively listened to our needs and proactively introduced new strategies and capabilities to help fuel our innovation and growth. We look forward to continuing this important partnership as TransUnion introduces innovative data and solutions that help us continue to serve the evolving needs of our members.

– Ronnie Momen, Chief Consumer Banking Officer, Lending ClubSanborn points to the flurry of global bank branch closures and the fact that certain demographics are penalised by the current system using auto loans as an example, although it is true of all credit. “It's been long documented that women and minorities end up paying a higher price at the used car dealer for their financing than others. So, we're addressing some of those systemic inequities. But, primarily, we're making it easy to access low-cost credit that is structured in a responsible way.”

Becoming a digital marketplace bank has driven this process forwards. “We don't have to support bank branches, which is another structural inefficiency. We don't have any of that – and it creates savings in our

model. We also have the highly profitable marketplace and can pass those savings back to the consumer and still be highly profitable. The combinations of our bank, marketplace and large and loyal customer base is truly unique in banking.

The importance of digital partnerships LendingClub’s stratospheric success has been bolstered by the fintech’s robust network of partners. Currently, they are collaborating with a handful of partners including Persado, Experian, Narmi, TransUnion and Quad, all of which are providing essential services that aid LendingClub as it disrupts traditional banking.

“The amount of innovation happening everywhere, including in financial services, means that being effective requires constant examination of the landscape to see where innovation is happening – and how you can harness it. Persado helps us unlock that with personalised language and content that's driving incremental activity, which is good for the company and – given the nature of our products – also good for the customer,” says Sanborn, who embraces the notion thata digital ecosystem serves the needs of an evolving environment.

“No one company can possibly do everything. There's so much happening in optical character recognition of documents,

SCOTT SANBORN CEO, LENDINGCLUB

SCOTT SANBORN CEO, LENDINGCLUB

fraud prevention and data aggregation using differentiated sources. Part of excellence is being able to have a finger on the pulse of where innovation is happening while also creating a culture, a structure, that can identify partners and implement with them to drive the business.”

Essentially, Persado offers a powerful platform that helps LendingClub pinpoint what is motivating customers so they can find the right product and put out the right message that is tailored to the right audience. “Persado enables us to be predictive in what we’re doing, to drive the right outcome,” he says.

Part of excellence is being able to have a finger on the pulse of where innovation is happening – and creating a culture, a structure, that can identify partners and implement with them to drive the business

LendingClub has been partnered with TransUnion – acting as LendingClub’s primary credit bureau – since it was founded. Recently, they also added Experian to the space where they are embarking on the next growth horizon focused on providing transparency, confidence and relevancy to the consumer.

Other partners include Narmi, a provider of digital banking technology, and Quad, which provides a postal marketing service

that is, Sanborn says, remarkably effective. “Some analogue marketing is still very important. People are often surprised by that, but it's a great consumer experience.”

As the fintech and all-digital banking continues to expand globally, there are no shortages of opportunity for companies offering disruptive services. LendingClub, since its acquisition of Radius Bank in

SCOTT SANBORN CEO, LENDINGCLUB

Our customer is highly banked. In fact, they’re 100% banked. They’re just not well-served. It’s working out better for the banks than it is for them

February of 2021, is now positioned perfectly for growth. At this point of post-acquisition, the digital marketplace bank has all its lending products in-house and is now issuing them through the bank. “We’re funding personal loans, auto loan refinance, and our purchase finance business through the bank,” says Sanborn.

“We also have launched high-yield savings accounts and CDs. That's gathering deposits to help fund the loans that we hold on our balance sheet. The next big frontier

SCOTT SANBORN CEO, LENDINGCLUB

It’s been long documented that women and minorities end up paying a higher price at the used car dealer for their financing than others

will be working on a core set of banking experiences that are really targeted at our consumer.”

It’s a bright future – not only for LendingClub, but also for their customers, who are reaping the benefits of choice in a climate where controlling outgoings has never been more crucial to daily survival.

“Our core consumers are highly banked with a high income, usually of over 100,000. They have a high FICO score, between 700 and 710. But they're also high debt. We help them lower the cost of their

debt, manage their spending and help them find savings.”

He adds: “We’re moving towards a banking experience that makes it easy for people to spot where in their lives they could find additional savings. If they squirrel away those savings, they won't need to use their credit card if an emergency happens. That’s our core aim – and the big series of investments we'll be making next.”