SYNERGY

CHINA CONSUMER CONFIDENCE RECOVERY

Vision Management Consultants

SYNERGY

CHINA CONSUMER CONFIDENCE RECOVERY

Vision Management Consultants

Dear Members,

As Lois said to Superman “you are one tough act to follow”! I would like to start by thanking Ir Dr Anne Kerr for her selfless dedication to the BritCham cause over her 27 years. That has to be some sort of record, and as she stated at the Annual General Meeting (AGM) on the 18 June, she is only 38 and so it has been a very formative stage of her life! I have thoroughly enjoyed the last 2 years acting as Vice Chair, learning valuable lessons along the way. Anne’s openness, enthusiasm and overwhelming sense of “what is right” has left the chamber with a spring in its step I can only look to continue her legacy “Thank you, Anne – we will miss you”!

At this year’s AGM, a total of fourteen Directors were elected to the General Committee This is a fantastic group of people Along with the co-opted members and the committee chairs we are lucky to have a pool of such influential, capable people voluntarily working to improve the business opportunities in Hong Kong for the membership. Their impact is made possible through the efforts of the Executive Team led by Paul McComb, our very own quantum energy source. In the last 24 months, as Vice-Chair, I have admired from afar the “plate spinning” that needs to go on to maintain the vast array of Chamber initiatives, and it would not be possible without the focused, singular enthusiasm of the Executives for their work Thank you and I so look forward to the year ahead

So, what can we expect this year? Working alongside me, Paul McSheaffrey and Rachel Huf have agreed to take up roles as Vice-Chairs with Keith Pogson continuing to take the reins as Treasurer We will continue to push forward with evolving the Chamber

that was initiated over the last 12 months We have streamlined the committee structure, created a Policy Council that can add weight / content to our Chamber positions and governmental interactions. We will evolve our governance initiatives, and continue to take feedback on any changes we are making to ensure “we are getting it right”. The sole purpose of this work is to address ALL members’ needs.

In the 15 years I have been involved within the chamber, we have always been a well respected body The changes we are making are an attempt to be “future ready” – sorry, corporate jargon, but I hope you get the point!

I know the Chamber is in a great position to grasp the significant opportunities we can see on the horizon, and so areas of focus for the year, at this stage, remain

1.

Hong Kong Government: Continuing building relationships with the HKSAR Government. This is a fundamental activity of the Chamber as we seek to share views and ideas with the intention of making positive and constructive suggestions for the business community to thrive

2

Advocacy: The Policy Council, with input from the committees will set priorities and align our activities to ensure focus and energy leading to impact In particular, we provided suggestions for the Chief Executive’s Policy Address. I attended my first Policy Council meeting, 48 hours into this role, with the Chief Executive’s Policy Unit – a really constructive session.

With the mantra of “HK: where business gets done” and the moniker of “HK: Asia’s World City” ringing in my ears, I look forward to doing my part in this collective effort BUT, all work and no play makes “me” a dull boy! We will continue to find ways to socialise, meet and have some fun Hong Kong is one of the most exciting social and friendly cities in the world – everyone says so It is a fun place to be, and we must celebrate that in the Chamber We have some interesting ideas from the members on how to do more of this and look forward to receiving more.

4

China: We will continue to develop the relationships with the China Liaison Office and other China focused British advocacy bodies.

3. UK: We will continue to work with the British Consulate in Hong Kong, who through our Consul General, Brian Davidson, and Chris Woodward, Director General of trade have been immensely supportive of the Chamber and our work Long may it continue!

5

Business: Through the other Chambers of Commerce in Hong Kong and through British Chambers in the UK, both foreign and domestic, we will ensure active dialogue to positively impact our membership here in Hong Kong. The themes I believe are as before with one or two additions, namely:

A last personal note. I have been in Hong Kong for over 30 years and this week is one of my proudest; as well as being appointed Chair, my eldest son was selected to play in the U20 Rugby World Trophy in Scotland – representing HK – his home and the place he loves. Go HK!

We have everything to work for as a Chamber to ensure the “new” Hong Kong” draws from its strong traditions as it strides toward its future I look forward to working with you all Thank you for your support!

Jeremy Sheldon, FRICS Chair

The British Chamber of Commerce in Hong Kong

d

Hong Kong 2025+: focused on Hong Kong as an IFC, talent attraction, new business (the HK everyone knows) as well as ESG, philanthropy, D&I – the HK people know less a. The Greater Bay Area b Exploring opportunities in ASEAN c A focus on technology, creative industries and what will continue to make HK great into the future

BritCham Hong Kong Summit 2024

Date: 24 September 2024

Venue: The St. Regis Hong Kong

Format: Hybrid

BritCham is pleased to announce its upcoming Summit on 24 September 2024 which will take a forward-looking perspective on the opportunities and ahead for our vibrant and innovative business community. We invite you to save the date.

The BritCham Hong Kong Summit is one of the largest and most important events for the international business community in Hong Kong, bringing together senior leaders and leading experts from all sectors. Hear expert opinions and gain valuable insights from a diverse range of Government officials, industry leaders, entrepreneurs, innovators, and changemakers to explore how technology and innovation plays a critical role in shaping a successful future for Hong Kong.

Delegates will gain valuable insights from keynote speeches, interactive panel discussions and networking sessions on the latest technological advancements, digital innovations and key developments across Hong Kong’s business landscape The Summit will cover practical strategies surrounding FinTech and digital banking to maintaining Hong Kong’s status as a global financial hub, sustainable developments in real estate, and innovations in emerging sectors including HealthTech and biotechnology We will also highlight cross-border collaboration and growing opportunities in innovation and new technology in the Greater Bay Area

In-person and online tickets will be available soon – further details to follow

If you are interested to learn more about the Summit, sponsorship opportunities and how you can get involved, please email events@britcham com

Platinum Sponsors

Eversheds Sutherland, HSBC, Prudential, Standard Chartered

Gold Sponsors

Swire, JLL

Silver Sponsors

Barclays, ICAEW

Bronze Sponsor

AstraZeneca

ByChrisBarford,Partner,FinancialServicesConsulting,EY

FinTechs are essential to the future of an innovative and thriving financial services sector The Hong Kong government states that “Our growing strength in financial services and close ties with markets in the Mainland and overseas will continue to make Hong Kong the ideal hub for FinTech development[1] ” For those not familiar with the term, we define FinTechs as organizations that combine innovative business models and technology to enable, enhance and disrupt financial services.

For FinTechs, scalable and sustainable growth requires access to the right resources, stakeholders and partners, as well as market opportunities at the right time. That includes connections with established banks, insurers and wealth and asset managers that engage FinTechs to transform key operations and processes As one of the world’s leading international financial centres, Hong Kong is a destination that brings together an ecosystem to make the right connections to make these transformations a reality And, Invest Hong Kong estimates that there are over 800 FinTech companies operating in Hong Kong[2]

The combination of FinTechs’ innovative solutions and established organizations’ scale promises to create a more customer-centric, inclusive and prosperous industry To improve their impact, FinTechs must have a plan to scale-up sustainably, and large firms need a clear strategy and strong implementation capabilities. In the context of a wider market of the Greater Bay Area (GBA), scaling requires consideration of language, regulation, customer education, fraud prevention and other key interoperability issues.

[1] Source: FSTB website on FinTech, https://www.fstb.gov.hk/en/financial_ser/financial-technology.htm , accessed 10 July 2024

[2] Source: InvestHK, https://www.info.gov.hk/gia/general/202211/14/P2022111100646.htm , accessed 10 July 2024

While FinTechs have shown remarkable expansion recently, they must persist in evolving and innovating to ensure continued progress, given that the next few years will see profound changes in business models across financial services as technology advances and customer expectations rise.

One of the major areas of FinTech innovation that we observe is in the use of artificial intelligence (AI), particularly generative AI (GenAI) Existing FinTechs, and new entrants, are now looking to this new technology frontier

GenAI is revolutionary For financial services firms, transforming the business means both understanding and acting, while carefully managing the risks Value creation from GenAI will come not only from cutting-edge technology, but from a data culture that invests in foundational capabilities and develops a framework for risk management. Successful initiatives will manifest from a combination of industry domain expertise and a culture of innovation that envisions new ways of doing business through the convergence of GenAI and other next-generation technologies.

From our perspective, we understand that GenAI might just be the transformative moment that changes everything.

While AI has been widely used in financial services firms for years, GenAI stands poised to redefine the future of financial services from front to back office. As such, financial services firms must ensure their governance frameworks are aligned to the new risks that emerge from AI use cases being implemented throughout the enterprise Implementing GenAI requires heightened board-level attention to issues of ethics, trust and bias, along with renewed vigour for cybersecurity and data integrity FinTechs offer the capabilities, innovation and customer-centric perspective that can help to transform traditional financial services industries, that have also been innovating themselves.

Within this context, and drilling down to two key areas for Hong Kong, InsurTechs (FinTechs focusing on the insurance industry) and those FinTechs focusing on banks, were considered as part of two 2023 EY surveys around GenAI.

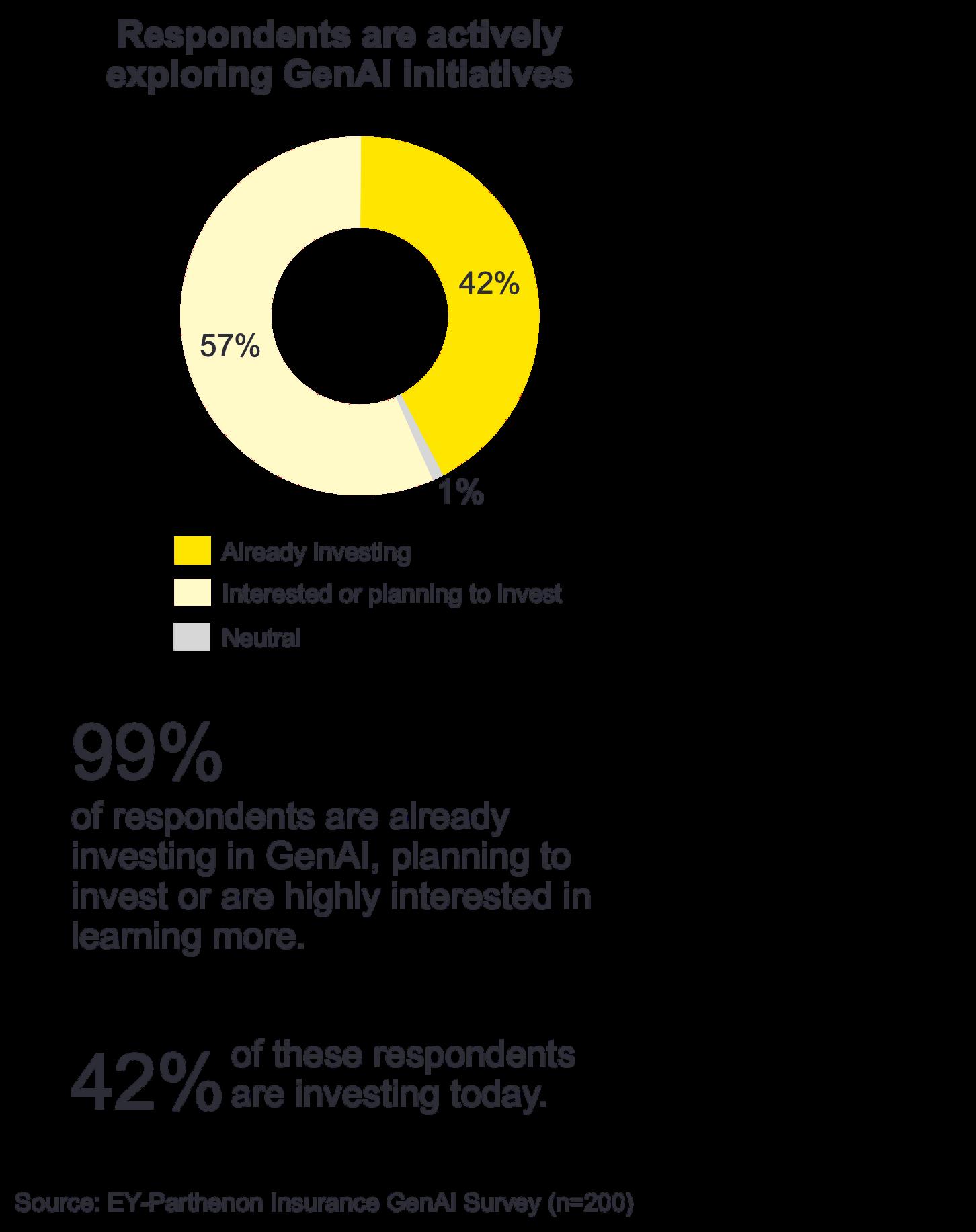

Based on an EY survey of 200 senior insurance decisionmakers, virtually every insurer around the world is focusing on GenAI, with 42% of respondents saying they’re already investing in GenAI and 57% making plans to do so.

Within this adoption story is significant opportunity for FinTechs, due to the need to deliver rapid results. Most respondents (69%) are prioritizing use cases to transform a specific part of the value chain, such as underwriting or distribution, with an emphasis on quick wins; 30% of insurers prioritize use cases that deliver near-term value, as opposed to 17% that prioritize solely long-term benefits.

The vast majority of insurers (95%) are prioritizing administrative and back-office use cases. A significant number (43%) are awaiting further development and testing before deploying GenAI in client-facing, frontoffice applications. Not surprisingly, InsurTechs will likely be the first movers for front-line deployments; 56% of respondents from InsurTechs say they are very excited about client-facing use cases for GenAI

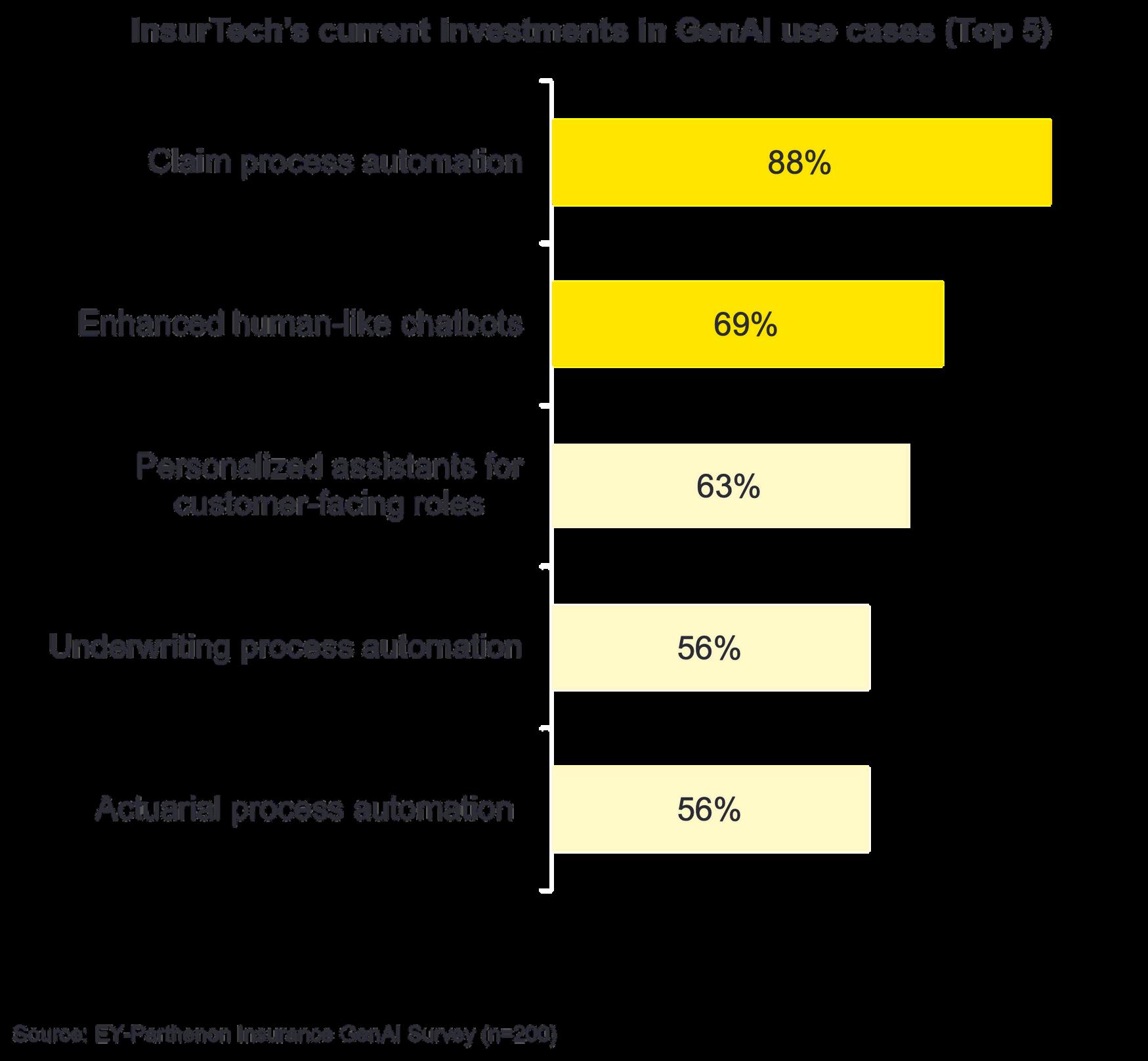

The primary motivators to implement GenAI technologies for InsurTechs are, unsurprisingly, revenue optimisation (63%) and customer experience enhancements (50%) And in terms of revenue growth and acceleration, 50% of InsurTechs expect to gain an uplift in revenue above 21% by implementing GenAI within core insurance functions Use cases that are being explored include claim process automation (88%), enhanced human-like chatbots (69%) and personalised assistance for customer-facing roles (63%).

In short, insurers and their customers should hopefully be able to significantly increase their revenue and customer experience by using InsurTechs enabled by GenAI

The Hong Kong banking industry has been exploring the use of FinTechs for a considerable length of time, stimulated by the HKMA’s FinTech 2025 strategy for “all banks go FinTech[3]” that launched in 2021

For many banks, partnering with a FinTech to access innovative capabilities can be faster, cheaper and more commercially viable than building or buying At a time when many FinTech firms’ valuations have declined, partnering also can be a good way to understand potential acquisition targets in greater depth.

In an EY-Parthenon survey last year, 55% of banks said they expect partnerships to play “very important” roles in their strategies by 2025, compared with 32% in 2023. Another 36% said working with fintech firms would be “important” within three years

[3] Source: HKMA, https://www.hkma.gov.hk/eng/news-and-media/press-releases/2021/06/20210608-4/, accessed 10

This is why, when it comes to GenAI, banks should explore an ecosystem approach to access new technology and talent. The Hong Kong government has also paid attention with initiatives such as the Talent List including professionals in FinTech.

The many banks that need to update their technology could take the opportunity to leapfrog current architectural constraints by adopting GenAI However, for GenAI to be useful in the workplace, it needs to access operational expertise and industry knowledge

Given the newness of GenAI and the limited tech capabilities of many banks, acquisitions or partnerships may be necessary to access the necessary skills and resources GenAI’s ability to work with unstructured data makes it easier to connect and share data with third parties via ecosystems Half (51%) of banks in the EYParthenon survey said they prefer partnerships as their go-to-market approach for GenAI use cases, as opposed to in-house development.

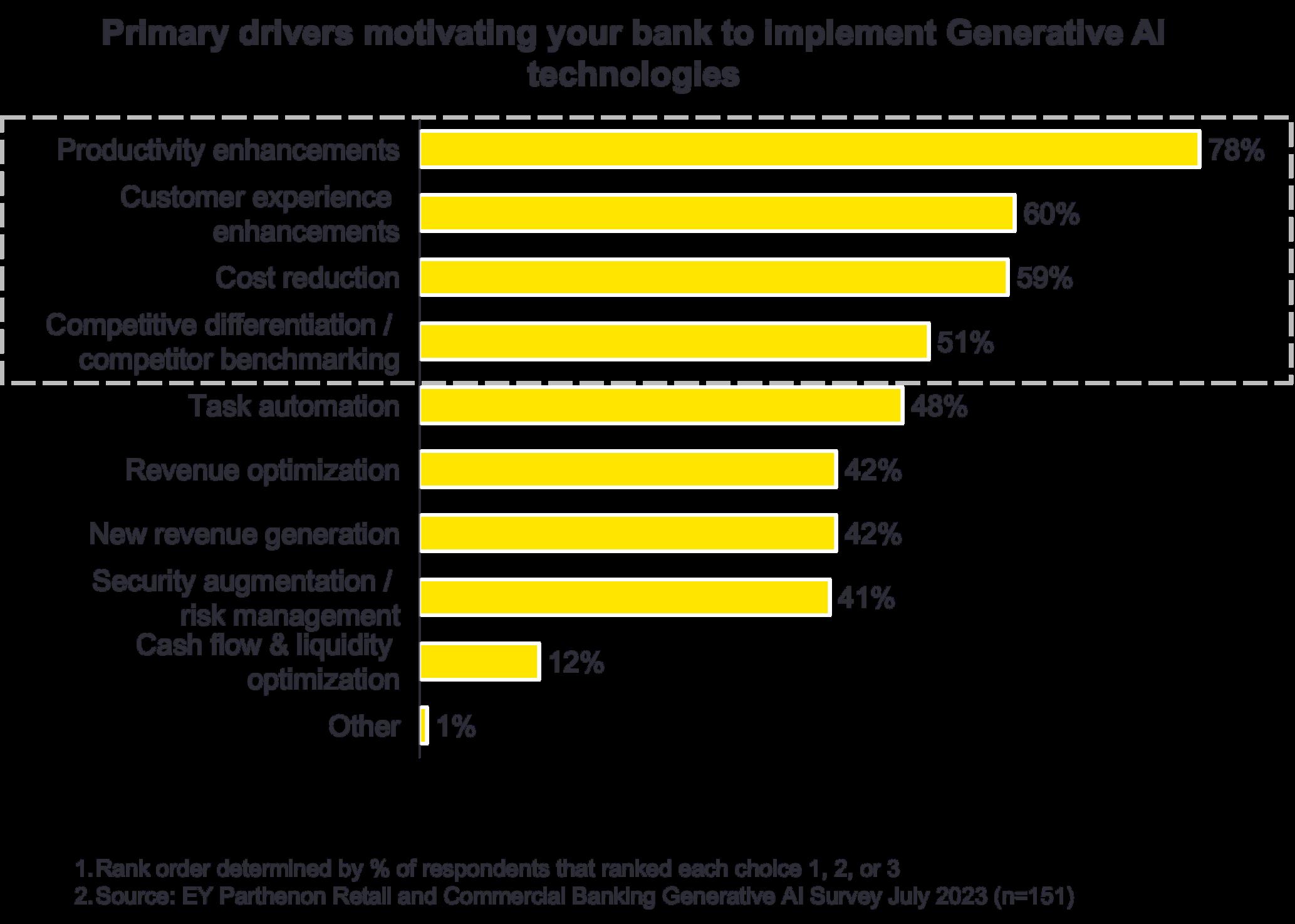

In 2023, we also surveyed 191 banking executives on how they saw GenAI transforming their business. Respondents cited three main areas where GenAI is changing ways of working at their banks:

Enabling greater productivity by automating sales-related activities (66%)

Enhancing existing technological capabilities (63%)

Accelerating broader innovation (54%)

While it’s no surprise that productivity and automation top this list, banking leaders clearly see how the value of GenAI extends beyond process improvements and cost savings and can help them strengthen their capabilities and foster more and faster innovation.

In shaping their GenAI strategies and plans, banking leaders must recognize GenAI’s position alongside Web3, blockchain, quantum computing and other disruptive technologies. Long-term roadmaps must reflect how these technologies, when deployed in the right combinations, can transform core business functions (e g , operations, finance, risk management, product development and sales) More importantly, they can also open new revenue streams and create entirely new value propositions.

Taking advantage of the transformational power of GenAI requires a combination of new thinking about a longstanding challenge for banks how to innovate while keeping the lights on. But banks clearly understand the urgency; a huge majority are already dedicating resources to GenAI, with 90% of respondents noting that their banks have dedicated resources to GenAI exploration or deployment.

However, one area that financial services do need to continue to focus on, and cannot rely on FinTechs for, is addressing regulatory concerns. So whilst the HKMA is preparing a regulatory sandbox for GenAI, due to launch in the latter part of 2024[4], the industry must focus on self-regulation and governance frameworks We look at this through our principles of Responsible AI and our EY ai Confidence Index to drive confidence in data, technology and processes that form the infrastructure of your AI ecosystem.

Hence, as financial services firms and FinTechs make further investments in GenAI capabilities and develop new use cases, they’ll need to assess the unique challenges and risks associated with the tooling and adjust governance and controls for each individual use case New use cases will bring new ongoing requirements for testing and assessments for hallucination, bias and other risks.

We have published a number of global articles on this topic that you may find of interest:

How to revolutionize the insurance value chain with generative AI

Five priorities for harnessing the power of GenAI in banking

How banks can fix broken fintech partnership models

Five generative AI initiatives leaders should pursue now

EY.ai Confidence Index: driving value through responsible AI adoption

[4] Source: HKMA, https://www.hkma.gov.hk/eng/news-and-media/speeches/2024/05/20240523-1/ , Accessed 10 July 2024

EY exists to build a better working world, helping to create long-term value for clients, people and society and build trust in the capital markets.

Enabled by data and technology, diverse EY teams in over 150 countries provide trust through assurance and help clients grow, transform and operate.

Working across assurance, consulting, law, strategy, tax and transactions, EY teams ask better questions to find new answers for the complex issues facing our world today.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients, nor does it own or control any member firm or act as the headquarters of any member firm Information about how EY collects and uses personal data and a description of the rights individuals have under data protection legislation are available via ey com/privacy EY member firms do not practice law where prohibited by local laws

For more information about our organization, please visit ey com

© 2024 Ernst & Young, China.

All Rights Reserved.

APAC no. (SCORE number)

ED 0727

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, legal or other professional advice. Please refer to your advisors for specific advice.

ey com/china

About EY

Chris Barford Partner

Financial Services Consulting

EY is committed to building a better working world – with increased trust and confidence in business, sustainable growth, the development of talent in all its forms, and greater collaboration. EY aspires to build a better working world through actions and by engaging with like-minded organisations and individuals. This is the EY purpose – and why EY exists as an organisation. Visit us at www.ey.com

Finance professionals play an essential role in creating and maintaining trust in capital markets Ethics and trust are a core priority for the profession So, what impact does the growth in the use of artificial intelligence (AI) and AI tools and processes mean for this imperative?

According to the ACCA (the Association of Chartered Certified Accountants) report Enabling Trust in an AIenhanced World, people should be able to trust in the expertise and ethics of a professional so that they don’t need to verify the details themselves.

AI raises significant questions around the use of data, accountability and reliability

‘Just as we trust doctors to take care of our health without understanding the intricacies of medicine,’ says the report, ‘businesses, regulators and capital markets trust accountants and auditors to ensure the integrity of financial statements without scrutinising every figure themselves.’

The report examines the new dynamics that AI introduces into traditional trust mechanisms, and sets out why AI poses challenges to trust.

While AI has undoubted benefits – through enhanced processes and improved efficiency – there are significant questions around the use of data, accountability and reliability, which could have a profound impact on trust Common issues that emerge include cloudy decision-making due to the complexity of AI models (outputs that cannot be adequately explained or justified are less likely to be trusted), and bias and errors

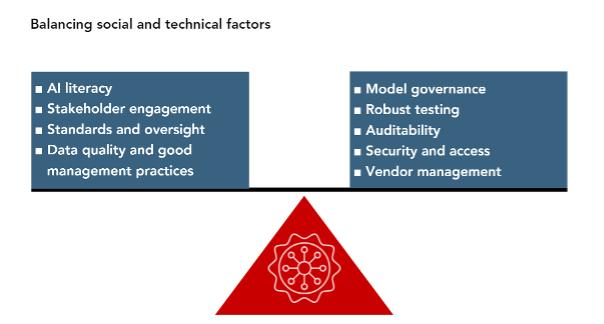

The report points out that the risks surrounding the use of AI in the profession will vary, as will the techniques used to mitigate those risks (and in many cases, it adds, existing practices may provide enough oversight). In analysing these risks, the report looks at the two interlinked elements: the operation of specific technologies or tools; and human interaction, including how AI-derived information is employed by the user.

On the second point, for example, over-reliance on AI tools and the reduced application of human judgment could blur the lines of accountability

The report argues that accountancy and finance professionals should view trust ‘as a socio-technical challenge’ that requires a combination of sound governance with internal control frameworks, and technical practices (such as machine-learning operations) in critical uses.

‘Trust is ultimately rooted in how people work together,’ it says, ‘but we build mechanisms to help us sustain trust in complex and uncertain environments ’

The report goes on to set out the steps that organisations can take to support employees and stakeholders as AI becomes more prevalent

Governance mechanisms, it says, should reflect the actual use of AI across the organisation, and management should consider governance frameworks (including for the procurement, development and use of AI systems, and a solid framework of data governance) to support implementation.

There also need to be clear policies around validation of AI models (to ensure performance remains reliable

The complexities and challenges of AI in the profession will vary according to how and where it is used, and that should influence mitigating actions The report argues, for example, that where AI is used for compliance, reporting or the distribution of goods and services but could potentially breach regulations, management should prioritise making its use explainable and interpretable.

In other cases, it adds, ‘the speed and impact of AI on decision-making under conditions of uncertainty may be more important than achieving the highest levels of accuracy’.

over time), and detailed audit trails and decision logs should be kept so that AI outcomes can be monitored and examined These steps will all help to promote trust

In addition, the report looks at the role of machine learning operations (MLOps), which can embed governance standards into the implementation and running of AI systems. ‘Essentially,’ it says, ‘MLOps can provide a technical backbone in critical use cases where trust may give way to requirements for additional verification.’

In the context of accountancy and finance this may include, for example, maintaining comprehensive data and version histories to enable the results of AI models to be traced and reproduced This would allow users to trace financial forecasts back to the exact AI model version and training data that generated it

Monitoring dashboards that track AI model performance and the fairness of metrics can also help to alert risk management teams to potential issues ‘CFOs and senior accountancy and finance professionals may not need to understand all the technical details of MLOps,’ says the report, ‘but they should be aware of the governance and trust implications as well as key metrics for review when required.’

The role of finance professionals in the age of AI is to focus on the outcomes driven by technology

Where to start? Read the full report which recommends the initial steps for senior leaders, as AI governance and risk management become more frequent topics for the boardroom.

ACCA Learning – a world of online resources and learning solutions – helps you stay up-to-date in a continuously changing and growing world Invest in AI literacy and skills development now:

Introduction to AI (online learning with 1 CPD unit)

Certificate in Ethical Artificial Intelligence (online learning with 12 CPD units)

Exploring the frontier of fintech skills (on-demand webinar with 1 free CPD unit)

Machine learning: an introduction for finance professionals (online learning with 7 CPD units)

We are ACCA (the Association of Chartered Certified Accountants), a globally recognised professional accountancy body providing qualifications and advancing standards in accountancy worldwide

Founded in 1904 to widen access to the accountancy profession, we’ve long championed inclusion and today proudly support a diverse community of over 252,500 members and 526,000 future members in 180 countries.

ACCA now has over 29,000 members and 125,000 future members in China, with representative offices and contact points in 11 cities including Beijing, Shanghai, Guangzhou, Shenzhen, Chengdu, Shenyang, Qingdao, Wuhan, Changsha, Hong Kong SAR and Macau SAR

Our forward-looking qualifications, continuous learning and insights are respected and valued by employers in every sector They equip individuals with the business and finance expertise and ethical judgment to create, protect, and report the sustainable value delivered by organisations and economies

Guided by our purpose and values, our vision is to develop the accountancy profession the world needs Partnering with policymakers, standard setters, the donor community, educators and other accountancy bodies, we’re strengthening and building a profession that drives a sustainable future for all.

Find out more at accaglobal.com/hk or follow ACCA Hong Kong on social media: www.facebook.com/ACCA.HongKong www.instagram.com/acca hk |www.linkedin.com/showcase/acca-hong-kong WeChat ID: ACCA China

The Post-Covid recovery in China has not been as positive as people expected. A major reason has been weak consumer confidence. There is a greater bias than existed prior to Covid to saving over spending. Since the beginning of 2020, family bank balances have risen 79%, a net increase equal to US$9 1 trillion, which is more than a year of China’s retail sales The problem is not that consumers don’t have money

The problem is that they are not spending it

Weak consumer confidence is due to the confluence of a number of factors. The 4 main ones are:

The Covid experience has rattled consumers It lasted longer than in other places and consumers didn’t get the fiscal support many received in other countries Much of the growth in the US economy in the past few years has been due to Covid money (which is now fading out and possibly leaving that economy exposed in the near term) The Chinese economy and Chinese consumers have not had this fiscal support Perhaps more importantly the Covid experience appears to have ‘unsettled’ many Chinese people and left them feeling somewhat less optimistic and confident about the future

The property correction has also hurt. Chinese consumers are more likely to be homeowners than in many other countries (currently around 90%) and their assets have taken a big hit and consequently their perceived level of personal wealth has fallen. Many people understand that this correction needed to happen and that longer term it will make the sector healthier. However right now most homeowners are feeling less wealthy.

There are fears that plummeting FDI, stories of supply chains moving overseas, and declining exports will lead to increased unemployment. While the overall unemployment rate at 5% is not that bad the youth unemployment rate is a real concern (20% at mid-year when the Government suspended the release of age specific data rate). This high rate has dented the optimism which has been characteristic of previous generations of young Chinese who believed that hard work and an education provided unlimited opportunity.

The 4th reason commonly mentioned is the continuing poor performance of the stock market In 2023 China’s CSI 300 was down 11 8% for 2023 and the Hang Seng was down 14% Net foreign investment in China listed shares dropped 87% This dismal performance just contributes to the gloom

Outside of these four primary reasons there are a few other factors impacting confidence.

Chinese consumers are aware of and worried by the geopolitical tensions (although they largely blame the US)

Many perceive the risk of war over Taiwan as being a real one (and again largely blame the US for escalating ambiguity on their stance on One China)

Some also mention restrictive regulation in areas like data transfer, gaming or private tutoring which may have created uncertainty and impacted private investment in different areas (although some people think that longer term much of this policy is probably right)

Reduced global demand and diminished export performance During 2023 China exports fell by 4 6% to US$3 8 trillion This was the first decline in seven years

Over capacity across most sectors is also a concern This has been exacerbated by low consumer demand growth The result is too much competition and downward pressure on prices which means thin margins

While the Post-Covid performance has not been what people had hoped it has not been a disaster either. The IMF predicts a GDP growth of 4.6% in 2024, making China the fastest growing country after India. Retail sales in 2023 were up 16% vs 2019 and 5.2% in the first quarter of 2024, industrial value-added is higher than PreCovid and export performance is strong with 5% growth in the first quarter In 2023 China’s share of Global Export Value is still high (at about 14%) GDP also came in at 5 2% which was a little bit above expectations

Some of the positive take-aways include:

The consensus seems to be that the housing market has bottomed Although the correction will probably take years rather than months to fully play out In first tier cities like Shanghai there are indications that the smart money is already moving to buy prized assets

Overcapacity is not necessarily a permanent thing. It is largely the result of a long-term investment momentum that has now softened, but again may take years to balance out

There are green shoots in mid-tier cities, where consumers often have higher disposable incomes (incomes marginally lower than in Tier 1 but cost of living significantly lower) where spending activity is showing signs of vitality

While some people believe that the Government may have made mistakes, or could have done more, they still think that pragmatism inevitably wins (political goals don’t get achieved without economic growth) –Recent public statement of supports for the real estate section seem to confirm this

Overall Post-Covid economic recovery has been disappointing, but it is not all bad news There is still growth, most businesses are still making money, and there are indications that things are improving rather than getting worse So, looking forward there is reason for cautious optimism

We believe the narrative, from some commentators, that the ‘China economic miracle’ has peaked and is now in decline is more wishful thinking than reality. We believe the key underlying dynamic (the formation of a middle class and the growth in the number of affluent consumers) has years left to play out. China will be the main scale growth opportunity in the world at least for the next decade. Despite all the talk about trade restrictions, the economist Andy Rothman noted that in 2023, 83% of China’s GDP came from final consumption and net exports (Exports minus Imports) accounted for 1% of its GDP. China is an economy driven by domestic demand.

It is true that China is facing some serious challenges. It is also true that the ‘China model’ has unique tensions and contradictions. But neither of these truths are new. It has always been a bumpy ride and pragmatism always seems to prevail

Our view is that growth and confidence will return But most likely it will be gradual This year will be a little better than last year and 2025 better again

The key thing that could accelerate the process is the Government taking more active steps to restore confidence To date Beijing has avoided large scale monetary and fiscal stimulus but these options remain

Beijing’s support for the private sector, markets, and transparency in the regulatory environment. Recent messaging suggests steps in this direction.

In any case it is clear that the Government has a strong interest in restoring confidence and stimulating growth. Our view is that at the end of the day Beijing will most likely prioritize economic growth and stability over most other interests.

Vision Management Consultants is a boutique consulting and advisory firm focused on helping international companies develop their businesses in Asia. We bring a unique combination of deep Asia experience and practical problem solving and business development capability.

Frank Gibson Principal, Vision Management Consultants

Frank has been advising international companies on Asian business issues for three decades.Over this time he has undertaken assignments with more than one hundred different international companies doing business across these dynamic and challenging markets. The majority of this work has been dealing with complex business problems across a mix of market entry, strategy development, marketing, and sales and distribution issues. He also has extensive experience in assisting multinationals to acquire local operations and assets.

Prior to entering the private sector, Frank held a number of senior economic policy positions in the Australian Government (Foreign Affairs and Trade and Social Security) He lives in Shanghai with his wife Zhang Heyi and their two children

Xavier Naville Principal, Vision Management Consultants

Xavier Naville started Creative Food, a key supplier to major restaurant chains in China (e.g. McDonalds, KFC, Starbucks). He grew the company to what is now an organization with 9 factories serving 6,500 restaurants a day and $150m in revenue

He sold the company to Bakkavor PLC from the UK in 2007 and ran the business until 2011

Xavier is now a principal at Vision Management Consultants and works on numerous strategy and M&A projects in the food sector for multinationals in China and other countries

As a CEO & Leadership Teams coach, he also helps small and mid-size business leaders to scale their organizations faster with measurable results He is the author of The Lettuce Diaries, a business memoir about his years in China’s food industry He currently lives in Taipei (Taiwan) and allocates his time between Asia and the West Coast of the United States He was previously a member of the French Junior national fencing team. He speaks fluent French, English and Chinese and is proficient in German.

In 1976, billionaire recluse Howard Hughes died on a flight from Acapulco back to Houston in the US He did not have a valid will and his estate at the time was estimated to be worth between US$169 million and 1 1 billion - the wide variation due in part to large tracts of prime, undeveloped land between Los Angeles and Las Vegas which would not have concrete values until sold and/or developed When the dust finally settled over five years later, Probate Judge Pat Gregory had had to deal with a circus-like court where he managed more than 600 would-be heirs and their claims, including a purported clairvoyant daughter who insisted 25 men with great big necks were following her (her claim was denied)

Hughes' estate was ultimately awarded to 16 paternal first cousins (71.5%), three granddaughters of Hughes' uncle (19%) and two stepchildren of Hughes' uncle (9.5%).

Expats may be posted for months, years or even decades in a foreign country, where their legal place of domicile may change. When deaths occur on foreign soil or even mid-flight like in Hughes' case, family members and loved ones may be confronted with foreign intestacy situations i e , dying without a will away from one's original country and/or domicile We

have identified a few highlights of the laws of intestacy in a number of popular expat jurisdictions (up to the inheritance level of spouse and children) in the hopes that expats and people with assets abroad remember to complete their estate planning and at a minimum, have valid legal wills in place, to avoid falling into intestacy situations

In Australia, the laws of intestacy are determined by each state/territory. The general distribution pattern is firstly to any spouse/domestic partner, then to children, parents, siblings and finally to more distant relatives

In South Australia for example, the Administration and Probate Act 1919 sets out the order of distribution where there is no will - where there is only a spouse, the spouse is entitled to the entire estate Where there is both a spouse and a domestic partner (and this is a possible finding) with no children, the spouse and domestic partner share equally including the deceased's personal belongings. Where there are assets over AU$100,000 and there are children, the spouse/domestic partner would be entitled to the first AU$100,000, half the estate balance and all personal belongings The children would share equally in the other half of the estate balance.

Part VI of the Civil Code governs the distribution of intestate estates First order legal heirs include spouse, children and parents Second order legal heirs are siblings and grandparents Children would include those born in and outside of wedlock, adopted as well as step children. It is interesting to note that parents may include biological parents, foster parents, step parents and adoptive parents.

In principle, heirs of the same order would inherit equal shares but Part VI of the Civil Code also provides that heirs who are unable to work and have financial difficulties may inherit larger shares Conversely there is a principle of "unworthiness to inherit" whereby statutory heirs can be disowned.

In an intestacy the deceased's estate is divided equally amongst the children if there is no spouse Surprisingly, civil unions are not recognised and therefore civil union partners inherit nothing in the event of intestacy. If there is a spouse and children, they share the estate after the spouse has exercised his/her matrimonial property rights and after opting for usufruct (right to enjoy the use and benefits of assets) or full ownership of one quarter of the estate

Even partners in a registered partnership are not entitled to inherit although they may claim a legacy of a temporary and gratuitous right to enjoyment of the family home (including the furniture) for one year, provided the partner and the deceased were residing in the family home at the time of death.

Pursuant to the Intestate's Estates Ordinance and where there are no children, a surviving spouse will inherit the estate unless there is a judicial separation in place. Where there are children and a surviving spouse, the surviving spouse is entitled to all personal assets and the first HK$500,000. After that the estate

is divided into two, with the surviving spouse taking one half and the children sharing the other half.

The surviving spouse is also entitled to priority in deciding whether to inherit the matrimonial home if owned by the deceased The surviving spouse must pay into the estate if there is a shortfall between the value of the matrimonial home owned by the deceased and the surviving spouse's entitlement.

If a parent passed away after 19 June 1993, illegitimate children are treated in the same manner as legitimate children. Legally adopted children or children adopted according to Chinese law and custom prior to 1 January 1973 are also treated in the same manner as biological children

Under Japanese inheritance law, the spouse and children share the estate in equal portions.

If there are two or more heirs without a valid will, the estate will belong to the heirs in co-ownership, which can only be terminated upon an out-of-court agreement or after a formal court procedure

In the US, each state determines its own laws of intestacy For example, in New York state, the Estates, Powers & Trusts Chapter 17-B Article 4 Part 1 sets out the spouse inherits the first US$50,000 plus half of the balance of the estate The children would share the other half of the balance of the estate

Legally adopted children will enjoy the same rights as biological children. Hence foster children and stepchildren must be legally adopted to inherit under the laws of intestacy

The Intestate Succession Act 1967 sets out the rules for inheriting estates of persons without wills other than Muslim estates which are governed by Muslim law.

Spouses and children share the estate in equal parts. As it is possible to have multiple wives, where there is one than more wife, they would share equally in the estate in respect of the one portion that would have been allocated to the wife had there only been one wife

There are five types of wills pursuant to the Civil Act of Korea - holographic (handwritten), recorded, secret, written and wills by dictation Each type of will must conform to the requirements of the Civil Act to be valid

Perhaps the most intriguing of these is the secret will, where the testator (will writer) delivers his/her will in a sealed envelope to at least two witnesses whereupon the date of delivery is written upon the envelope and then delivered to the court clerk within five days to receive a "fixed date" stamp

First-tier relatives are defined as one's spouse, children and grandchildren, second-tier relatives are defined as one's parents and third-tier relatives are defined as one's siblings under the Civil Act. If there are no first-tier children, the spouse must share the estate with the second-tier relatives. In South Korea, those who may inherit an estate or portion thereof are given the opportunity to renounce their inheritance within three months of being notified as they must also take on the debts of the deceased

Intestate succession is considered a norm in Taiwan due to the cultural taboo or phobia about all matters related to death Pursuant to Article 1144 of the Taiwan Civil Code, a spouse inherits a portion equal to the lineal descendants of the deceased

If the deceased leaves more liabilities than assets, heirs are entitled to "succession with limited liability" pursuant to Article 1248 of the Civil Code - the extent that heirs must take on the deceased's debts is limited to their inherited share of the estate Heirs may also renounce their right to inheritance within three months of being made aware of the death of the deceased, pursuant to Article 1174 of the Civil Code

In Thailand, any person over the age of 15 years with a "healthy" mental state can validly write to will, which is younger than in most other countries

Pursuant to Section 1635 of the Civil and Commercial Code, a surviving spouse is entitled to inherit the same share as surviving children. Spouses who are separated and living apart even for extended periods of time do not lose their rights as surviving spouses.

Section 1622 of the Civil and Commercial Code states that Buddhist monks may not be statutory heirs unless they leave the monkhood and enforce a claim within the period prescribed Any property acquired by a monk during monkhood becomes the property of the monastery of domicile.

The laws of intestacy as applied in each jurisdiction are all generally consistent insofar as defining a person's closest relatives for the purposes of inheritance The application of this principle also depends largely upon the specific cultural and social norms of that jurisdiction. More importantly, each person's closest loved ones may be a unique mix of relatives and/or friends without statutory rights of inheritance It is far better to have a valid will and avoid leaving out loved ones as well as avoid bitter legal (or otherwise) disputes than to rely upon the laws of intestacy

DISCLAIMER - The information contained herein is for general guidance and informational purposes only and should not be relied upon or treated as a substitute for individual legal or any other advice Oldham, Li & Nie accepts no responsibility for any loss which may arise from reliance on any of the information contained herein. No representation or warranty, express or implied, is given as to the accuracy, comprehensiveness, timeliness or validity of any such information

Gordon Oldham Senior Partner

Oldham, Li & Nie (OLN) is a highly regarded businesscentric service law firm. With many years of experience practising in Hong Kong, the firm's diverse global employees, who embody the rm’s East-West culture, are adept at delivering an integrated suite of legal and business solutions. Founded in 1987 by Gordon Oldham, OLN has over 45 lawyers, admitted to one or more urisdictions, including Hong Kong, the United Kingdom England and Wales), several US states, Australia, several provinces in Canada, France, and Japan

Helena Hu Consultant

To find out more, please visit www oln-law com

Oldham, Li & Nie is the first law firm in Hong Kong to have a dedicated Elder Law Practice, catering to the holistic egal needs of older adults For further information on this practice area, please visit https://oln-law com/practice-areas/elder-law/

The integration of artificial intelligence (AI) and financial technology (FinTech) into financial services has already brought about significant changes, such as robo-advisers Simply put, a robo-adviser is an online platform or mobile app that makes use of financial technologies to give automated financial advice to clients with little or no human involvement These platforms can efficiently allocate assets, rebalance portfolios, and even provide generically tailored recommendations based on what an individual thinks their risk profile and financial goals are

The increasing prevalence of automated wealth management platforms such as robo-advisers and AI-powered financial planning tools has led some to question whether there is still a place for human financial advisers in this newly transformed landscape The undeniable benefits of these innovations – including increased efficiency, cost-effectiveness, and accessibility – have led many to speculate that human financial advisers may soon become obsolete. After all, if technology can handle most of the financial planning and investment management tasks, what value can advisers still provide?

However, the current capabilities are quite limited – if we are giving information to a computer, so it can give us advice, it’s only as smart and complete as the information we put into it.

The ability and personalised guidance of experienced financial advisers remain invaluable, even in an AI and FinTech-dominated world In fact, the human touch is more important now than ever in helping individuals and businesses navigate the complex and constantly evolving financial landscape

How are AI and FinTech changing financial services?

AI-powered financial planning tools are becoming increasingly sophisticated, allowing users to input their financial information and receive detailed projections, insights, and recommendations on everything from retirement planning to debt management. FinTech startups have also disrupted traditional banking and payment systems, offering innovative digital solutions that are often more convenient and accessible than legacy services.

By eliminating or minimising human participation and other expenses of a brick-and mortar-business, roboadvisers should be able to offer financial advisory services at a much lower cost than traditional financial advisers Robo-advisers are often available 24/7 as long as you have an internet connection Less queuing in banks can only be a good thing when working out how to save time and streamline your life

Robo-advice relies on the information provided by the clients, commonly through an online questionnaire. A robo-adviser would not be able to probe for more information nor can it sense you had more to say. We also don’t know what we don’t know, or how to articulate emotions, dreams and desires. The lack of interaction is a major limitation.

On the flipside, a human adviser can consider factors that are relevant to a client in a more qualitative and holistic way A human adviser can prompt clients for more information and read emotional cues Money is an emotive subject and our feelings towards it can be complex and hard to put into words

When you are nervous about the market conditions and your investments, a human adviser would be able to explain how the investment markets work and address your concerns

The client also needs to be comfortable with technology, computers, and mobile apps since everything is online Those who are not familiar with the digital environment may find it daunting to deal with a robo-adviser

Clearly, the need for experienced, human financial advisers remain strong. In fact, a recent survey by Vanguard found investors believe they are 16% closer to their financial goals with a human adviser, compared to being 5% closer via AI and FinTech tools [1] It’s a stark reminder that the machines can only go so far

Another research from Fidelity Investments' 2021 Women and Investing Study revealed that 77% of women believe that “if they had a financial adviser to help them invest, they'd be more confident about their financial future ”[2]

There are several key reasons why financial advisers continue to play a vital role:

AI and FinTech tools are excellent at crunching numbers, analysing data, and providing standardised recommendations. However, they often lack the nuanced understanding of an individual's unique circumstances, goals, and priorities that a human adviser can provide.

Experienced financial advisers take the time to truly get to know their clients, gaining a deep understanding of their financial situation, risk tolerance, time horizon, and long-term aspirations Furthermore, human advisers can provide holistic, integrated advice that considers the various aspects of a client's financial life, from investments and retirement planning to insurance, tax, and estate planning This big-picture perspective helps clients make informed decisions that align with their overall financial well-being

The financial landscape is constantly evolving, with new regulations, market conditions, and life events constantly reshaping the best strategies for individuals and businesses. While AI and FinTech tools provide live

[1] Vanguard, 2021 https://advisors.vanguard.com/advisors-alpha/advice-that-clients-value#role-of-age [2] Fidelity, 2021 FidelityInvestmentsWomen&InvestingStudy2021.pdf

data updates, they often lack the adaptability and flexibility of human advisers, who can quickly pivot their approach in response to changing circumstances.

Experienced financial advisers bring a wealth of knowledge and expertise; they can identify and navigate potential risks and opportunities, and proactively adjust their clients' plans accordingly. This agility and responsiveness is especially crucial during times of uncertainty and volatility, when automated systems may struggle to provide proper guidance.

Financial decisions are rarely 100% rational; we’re all guilty of being guided by emotions, biases, and psychological factors Successful financial planning requires not just technical ability, but also the ability to understand and address the behavioural and emotional aspects of money management

Financial advisers excel at this, using their emotional intelligence and people skills to guide clients through the psychological challenges of financial planning. They can help clients overcome common behavioural biases, such as loss aversion or overconfidence, and provide ongoing coaching and accountability to help them stay on track with their financial goals.

AI and FinTech considerably lack the tools to replicate this intelligence, as they often lack the nuanced understanding of human psychology and the ability to empathise with clients' emotional needs.

Building trust is essential in the financial services industry, as clients are entrusting advisers with their most sensitive financial information and long-term goals Human financial advisers have a unique advantage in this regard, as they can develop deep, long-lasting relationships with their clients based on mutual understanding, respect, and transparency.

This trusted adviser-client relationship is particularly valuable when it comes to advocating for the client's best interests, especially in complex or contentious situations. Automated systems and FinTech platforms, on the other hand, often lack the personal connection and advocacy capabilities that are so highly valued by clients. While they may be efficient and cost-effective, they cannot replace the trust and confidence that comes from working with a dedicated human financial adviser.

The best of both worlds: what does the future hold?

The rise of AI and FinTech in financial services does not signify the demise of human financial advisers Rather, it presents an opportunity for these two elements to work in harmony, with advisers using the power of technology to enhance their services and better serve their clients

By embracing AI and FinTech tools, financial advisers can streamline their operations, automate routine tasks, and free up more time to focus on the higher-value, personalised aspects of financial planning and client relationships. Automated portfolio management, for example, can be used to handle the day-to-day monitoring and rebalancing of investments, while having the ability to generate initial projections and recommendations which advisers can then refine and customise based on their deep understanding of the client's unique

circumstances is no doubt useful – to a certain degree This synergistic approach allows advisers to use the efficiency and data-driven insights of technology, while still maintaining the vital human touch that clients find so valuable

Ultimately, the future of financial advice will likely be a blend of AI, FinTech, and experienced human advisers working together to provide comprehensive, personalised, and accessible financial services. By embracing this integrated approach, financial advisers can not only remain relevant in the digital age but also enhance their ability to help individuals and businesses achieve their financial goals.

By leveraging the power of technology while still maintaining the human touch, financial advisers can deliver a superior level of service and support that helps clients navigate the complex and ever-evolving financial landscape. As we all continue to navigate the changing financial environment, the value of working with experienced, human financial advisers will only continue to grow.

Eleanor Coleman Principal

The Financial Empowerment Group; Vice Chair of Women in Business Committee, BritCham HK

Eleanor coleman@sjpp asia +852 9885 2192

The Financial Empowerment Group is a Associate Partner Practice of St James’s Place (Hong Kong Limited) St James’s Place is the UK’s largest financial advice provider with nearly one million clients and over £179 billion in assets under management

The Financial Empowerment Group aims to help women and members of the LGBTQ+ community to achieve financial freedom through education, planning and action

We aim to provide straight-talking, simple financial advice. Avoiding financial jargon and making you feel good about your choices at every stage of the journey.

This document is issued by St. James’s Place (Hong Kong) Limited (‘SJPHK’). The content of this document has not been reviewed by any regulatory authority in Hong Kong.

The ‘St. James’s Place Partnership’ and the titles ‘Partner’, ‘Adviser’, ‘Partner Practice’, or any variations thereof, are marketing terms used to describe representatives of the St. James’s Place Group (‘SJP Group’).

St. James’s Place (Hong Kong) Limited (‘SJPHK’) is a licensed Insurance Broker Company regulated by the Insurance Authority (’IA’), a Licensed Corporation regulated by the Securities and Futures Commission (’SFC’) and Principal Intermediary registered with the Mandatory Provident Fund Schemes Authority (’MPFA’), in Hong Kong.

IA Licence No. FB1075. SFC Central Entity No. AAV439. MPFA Registration No. IC000852.

Registered Address: 1/F Henley Building, 5 Queen’s Road Central, Hong Kong.

SJPHK is part of the SJP Group.

Members of the St. James’s Place Partnership in Hong Kong are appointed by SJPHK to act in a licensed and regulated capacity and may facilitate business with other companies within the SJP Group.