4 minute read

Are you at risk of surprise sales tax?

ll rfosr BUSTNESS LEADERS are comIYlfortable discussing things like risk, ROI, and market share. They are less comfortable discussing sales tax, but it's a conversation that needs to happen.

States are getting increasingly creative about finding new revenue sources through sales tax. Businesses can easily incur "surprise" tax liabilities without realizing it. Assuming sales tax rules are the same across all your territories can be a costly mistake.

What is Nexus?

Sales tax starts with something called "nexus." Nexus is the relationship a business must have with an authority (like a state or local government) in order for that authority to collect taxes. Let's simplify that. Imagine you have a store in Nebraska: you own your building, pay employees, and complete business transactions in the state. All these things give you nexus in Nebraska, and the state will collect sales tax from your business.

Say you have a customer, Jim, who works in Iowa, but comes to Nebraska to purchase his materials. You probably don't have nexus in Iowa just because your customer works there. But let's change the situation. Jim calls in his orders from Iowa and your employees deliver materials to his jobsites in that state. Now Iowa might argue you have nexus in their state and you owe them sales tax.

The problem businesses face lies in the words "probably" and "might." Each state has different nexus triggers. If your Nebraska store sells an item to people in two different states, you may have nexus in one but not the other. Things like buildings and equipment are almost universal triggers, but many states are starting to define nexus based on activity rather than physical presence. Sending an employee to a trade show, industry conference, or training seminar can all give you nexus in a state. You can establish nexus in Arizona if an employee spends two days of the year there. If your Nebraska store has a lot of Iowa customers like Jim, Iowa might argue you have an "economic nexus" in their state, even if all your sales take place in Nebraska.

Delivery of Goods

Delivering purchased items is a common nexus trigger, but there are a variety of ways states approach the issue. In Georgia, the "taxable event" takes place at the ship-to location, but in Kansas, it occurs at the ship-from location. In some cases, just delivering an item may not trigger nexus, but offering a service can. (lt's the difference between delivering a door, and delivering and installing a door.) The method of transportation may be a trigger as well. Are you using your own fleet, a common carrier like FedEx, or a third-party vendor? The bedding store Mattress World is an excellent cautionary tale about ignoring delivery-related sales taxes. Mattress World is located on the Oregon-Washington border. Many Washington residents would cross the border to purchase and pick up mattresses. Mattress World started offering delivery and set-up service to their Washington customers through a third-party vendor. But hiring and sending that vendor across state lines created nexus under Washington's tax code. The company didn't plan for this and ended up with a $ I .7 million (plus tax) debt to the state.

Jurisdictional Boundaries

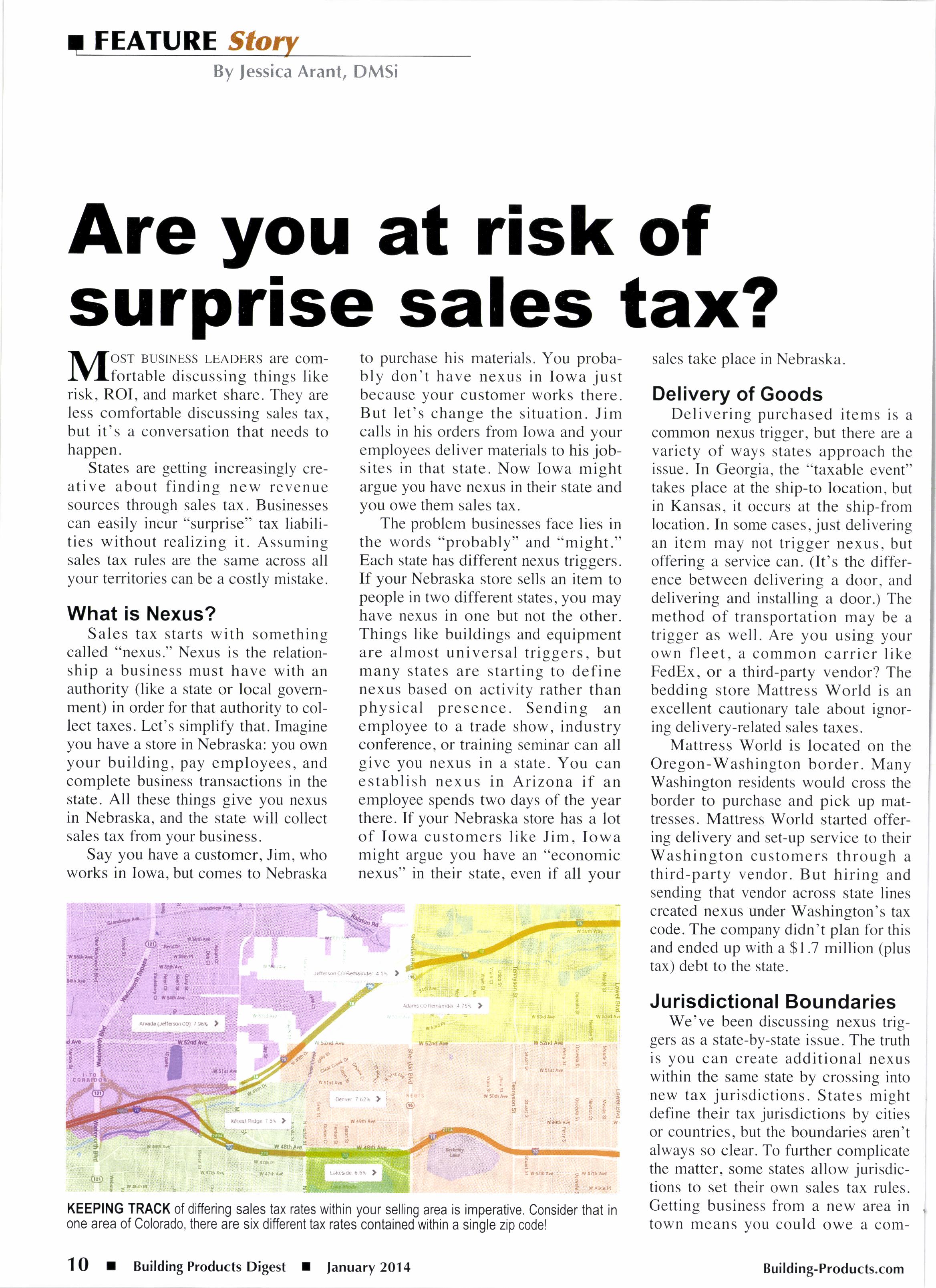

We've been discussing nexus triggers as a state-by-state issue. The truth is you can create additional nexus within the same state by crossing into new tax jurisdictions. States might define their tax jurisdictions by cities or countries, but the boundaries aren't always so clear. To further complicate the matter, some states allow jurisdictions to set their own sales tax rules. Getting business from a new area in town means you could owe a com- plctely new sales tax to a complctcly ncw authoritl'. Colorado is notorious ftrr this: thcy hal'e sir diffbrent ratcs in a singlc zip codel

What's in a Name

Definitions lrre onc of the stickicst points in sales tar. ir"r part bccausc they can seem so albitrary and absent of ct-rr.r'rn'ron sensc. KitKats, Twizzlers and Whoppcrs arc not "candy" under thc Strcamlined Salcs Tax dcfinition bccausc they all contain flour. Indiana catcgorizcs marshnrallows as "candy" (taxable) and r.narshmallow crdme as "foocl" (exempt). Pennsylvania docs not tax clothing. but does tax "ful articles," which include "articlcs made olwoven animal hnir or wool that rescmblcs fur in appcarancc." (Prcsumably a wool swcatcr u'ould bc cxcr.npt. but a coat with shccpskin trirn would not.)

Culifrrrnil's 20 l.l trrx ()n "ccltirin lumber ancl cnginccrccl wood proclucts" is a gfcat examplc of definitiorrrclated chaos. Under this lule. "tcncing, railing and decking" are sub.ject tcr the tirx. htrt humboo lr'rrcing. plc-c()nstructecl railin-e sectit'r.rs. and "deck packagcs" are exempt. Retailcrs spcnt countlcss I.rouls clctcrrlining w'hich items in their catakrgs were taxablc. It r"'as a huge invcstnrent of tirlc and monc)' lbr the businesses. but it needed to bc done. Shortly befbrc cna.^ting this ncw rule, Califbrnia announced a plan to hire 3(X) auditors. Businesses arc held responsible for complying with tax rulcs. clen if thosc rules are alnrost impossi ble tcl undclstand.

The Take-Away

Chet'k tltc tte.rus trigg,crs .fbr evtrt' tcrritory \'out' ( onlputl ittlct'ttcts vitlt. Don't assun'rc you ncccl a buildin-u or permanent cmployee in a state to owe sales tax thcrc.

. Clteck tlte tu.r rula.s regorditt.e, rleliveric.r fitr etart urcu tort dclircr 1o. You rnay need kl collect additional sllcs tirr lfonr eusl()mers in strtttc areas but not others.

. Cltcck the .iurisdictiottul boLtttdaries,for aver)' .\tolc t'ou tlo lttt.sittess lri. Make surc you'rc collectin,g the corrcct amount ol' salcs tax for each juriscliction and rcmittin-c payrrent tc) the corlcct authofity.

. Pu)' attctttiott ttt da.fittitittrt.s dttu(ltc(l lo sulcs 1a.res. TI'rc distinctiortr hetrr ee rr tlrr;lhle lrrrtl excmpl itcrns rnay seenr arbitraly' and silly. bul thc state is going to bc vcry serious about collecting fincs and pcnalties. Sales tax is incredibly cornplicatecl. You neecl a good tax consultant to rnake surc you fbllow the rules in all jurisdictions where you have r"rcxr"rs. But once you know what you're supposed to do. the ncxt step is doing it consistently.

Automating tax calculation is a creat strategy because it virtually eliminates the risk of human crror. Serviccs like Avalara work with your ERP system and calculate the appropriatc rate for each transaction. Your software platfbrms should be robust, yet flcxible enough to handle the inevitable changes in sales tax rules.

California's lumber tax impacted products so inconsistently that most POS programs couldn't apply it correctly. Miinl businesscs resorted to calculating sales tax by spreadsheet. Agility softwarc was one exception. It adaptcd to thc change easily. and Llsers likc Petcrman Lumber. Fontana, Ca.. and S&J Lr-rnrber. Madera. Ca.. w'cre able to incolporate thc tax 'u"ithout a problern.

You nrav not want to think about this topic. but it's far better to discuss sales taxcs now witl'r your collcagucs. rather than later with an auditor'.

Jt rr1q 11 .\t'ttttt i.t ( (tlllltllttlit (tlit'll t rtt'l' clitttttrtr lltt DMSi Softttare, Ontultu, Ne. Rcu c lr ltc r ot jurutt t Cl' tt rrt.si.t ottt.