2 minute read

BIGGEST& BROADEST DffPESI

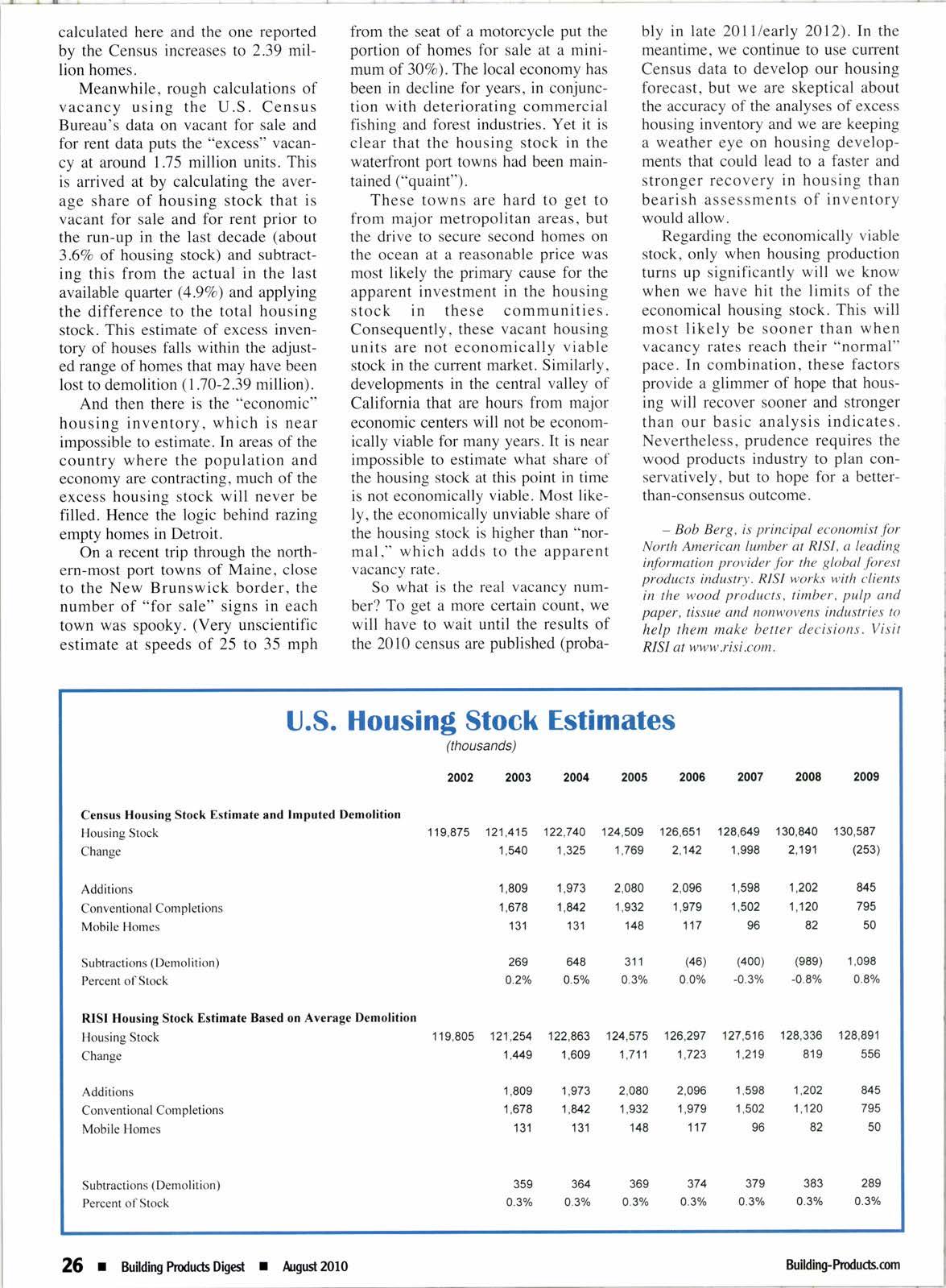

calculated here and the one reported by the Census increases to 2.39 mlllion homes.

Meanwhile, rough calculations of vacancy using the U.S. Census Bureau's data on vacant for sale and for rent data puts the "excess" vacancy at around 1.75 million units. This is arrived at by calculating the average share of housing stock that is vacant for sale and for rent prior to the run-up in the last decade (about 3.6Vo of housing stock) and subtracting this from the actual in the last available quarter (4.9Vo) and applying the difference to the total housing stock. This estimate of excess inventory of houses falls within the adjusted range of homes that may have been lost to demolition (1.70-2.39 million).

And then there is the "economic" housing inventory, which is near impossible to estimate. In areas of the country where the population and economy are contracting, much of the excess housing stock will never be filled. Hence the logic behind razing empty homes in Detroit.

On a recent trip through the northern-most port towns of Maine, close to the New Brunswick border, the number of "for sale" signs in each town was spooky. (Very unscientific estimate at speeds of 25 to 35 mph from the seat of a motorcycle put the portion of homes for sale at a minimum of 3lvo).The local economy has been in decline for years. in conjunction with deteriorating commercial fishing and forest industries. Yet it is clear that the housing stock in the waterfront port towns had been maintained ("quaint").

These towns are hard to get to from major metropolitan areas, but the drive to secure second homes on the ocean at a reasonable price was most likely the primary cause for the apparent investment in the housing stockin these communities. Consequently, these vacant housing units are not economically viable stock in the current market. Similarly, developments in the central valley of California that are hours from major economic centers will not be economically viable for many years. It is near impossible to estimate what share of the housing stock at this point in time is not economically viable. Most likely, the economically unviable share of the housing stock is higher than "normal ," which adds to the apparent vacancy rate.

So what is the real vacancy number? To get a more certain count, we will have to wait until the results of the 2010 census are published (proba- bly in late 20lllearly 2Ol2).In the meantime, we continue to use current Census data to develop our housing forecast, but we are skeptical about the accuracy of the analyses of excess housing inventory and we are keeping a weather eye on housing developments that could lead to a faster and stronger recovery in housing than bearish assessments of inventory would allow.

Regarding the economically viable stock, only when housing production turns up significantly will we know when we have hit the limits of the economical housing stock. This will most likely be sooner than when vacancy rates reach their "normal" pace. In combination, these factors provide a glimmer of hope that housing will recover sooner and stronger than our basic analysis indicates. Nevertheless, prudence requires the wood products industry to plan conservatively, but to hope for a betterthan-consensus outcome.

- Bob Berg, is principal economist for North American lumber at RISI, a leading information provider for the global forest products industry. RISI works with clients in the wood products, timber, pulp and paper, tissue and nonwovens industries to help them make better decisions. Visit RISI at www.risi.com.

U.S. Housin$ Stock Estimates