7 minute read

CANADA GAINS ACCESS TO JAPANESE BEEF MARKET

It was announced in late March that for the first time in two decades, Japan is reopening its doors to Canadian processed beef.

This accomplishment ushers in a new era for Canada and its second-largest market for beef and beef products: expanding market access for Canadian exporters -- while also benefiting Japanese consumers who will have greater access to Canada's high-quality beef products.

Nathan Phinney, President of the Canadian Cattle Association stated, "Cattle producers are grateful for the removal of trade barriers for processed beef in Japan, our second-largest export market for beef. Our industry will continue to support global food security by providing some of the most sustainable and highest quality beef in the world. We look forward to continuing to work with the Government of Canada to further remove remaining trade barriers and expanding our trade capacity in the Indo-Pacific region."

The development also removes the last restrictions on Canadian beef that Japan put in place in 2003, after the discovery of a case of bovine spongiform encephalopathy (BSE) in Alberta.

Under the new Indo-Pacific Strategy, the Government committed to seizing economic opportunities for Canada by strengthening its regional partnerships, including with Japan. The Canadian Food Inspection Agency, with the support of Agriculture and Agrifood Canada, has worked tirelessly over the past few years to assert the highest production standards and quality assurance of Canadian beef in order to reopen full access in key markets, like Japan.

Japan is an important market for Canada and the world. In 2022, the Japanese market for Canadian beef and beef products had an estimated value of $518 million, largely due to Canada's preferential access under the Comprehensive and Progressive Agreement for TransPacific Partnership (CPTPP).

"The Canadian Meat Council is very pleased to see this expansion of our beef access to Japan. Our members view this as a critical market for their products, including processed beef and beef patties. This agreement will allow our industry to further build on the recent successes they have enjoyed in Japan since the CPTPP was ratified. Thank you to Ministers Bibeau and Ng, and the hard work done by CFIA to achieve this new opportunity,” said Christopher White, President and CEO of the Canadian Meat Council.

This expanded market access opportunity follows another loosening of restrictions in 2019, when Japan approved imports of Canadian beef from cattle older than 30 months.

• Japan is Canada's third-largest market for agriculture and food.

• Under CPTPP, Japan's 38.5% tariff on beef imports (including primary processed products like ground beef patties) will decrease to 23.35% by April 1, 2023, and will go down to 9% by 2033. Tariffs on further processed beef products will be reduced even more and in some cases – eliminated altogether. This change provides Canadian exporters with a clear tariff advantage over our key competitors.

• According to Statistics Canada, the total value of Canadian beef exports to all countries in 2022 was over $4.6 billion.

FCC: 2023 FOOD MANUFACTURING MARGINS UNDER PRESSURE

By Kyle Burak, Farm Credit Canada Senior Economist

The annual FCC Food and Beverage Report reviews last year’s economic environment and highlights opportunities and risks for Canadian food and beverage manufacturers for 2023. It includes projections of annual industry sales and new gross margin index forecasts by sector.

INDUSTRIES FEATURED IN THE REPORT ARE:

• Grain and oilseed milling

• Sugar and confectionery products

• Fruit, vegetable preserving and specialty food

• Dairy products

• Meat products

• Seafood preparation

• Bakery and tortilla products

• Soft drinks and alcoholic beverages

Key Takeaways

Inflationary pressures hit the Canadian economy in 2022, and the food sector was not immune to their effects. Significant increases in commodity prices amid pressures on supply chains and labour shortages led to higher input costs and wage increases. In response to inflation, the Bank of Canada raised its benchmark interest rate numerous times, applying further pressures on profit margins in 2023; many of these challenges persist while demand challenges emerge. Here are three key observations from this year’s report.

SALES GROWTH WAS STRONG IN 2022; PROJECTED TO GROW MODESTLY IN 2023

Food and beverage manufacturing sales rose 10.6% to $156 billion in 2022 (Figure 1). Growth largely resulted from selling price inflation in the face of higher costs, but we did see healthy volume trends in certain industries. Meat product sales growth is estimated to have come primarily from higher foodservice volumes. Baked goods were one of the only categories to see volume growth at the grocery store despite elevated retail prices.

Sales growth decelerated in Q4 2022, with several categories reporting sales declines YoY in December. This deterioration in growth is injecting uncertainty into our projections. FCC Economics forecasts food manufacturing sales to increase 2.2% YoY in 2023 to $160B. Any rebound in the deceleration observed at the end of 2022 could lift these projections. We expect the larger industries covered in this report, like grain and oilseed milling and meat product manufacturing, to outperform, while animal food, plant-based protein products, seasonings/dressings and snack products (not covered) to record declines.

Food And Beverage Manufacturing Sales Increased

OVER 10% IN 2022

Margins Have Deteriorated In The Face Of Higher Input And Labour Costs

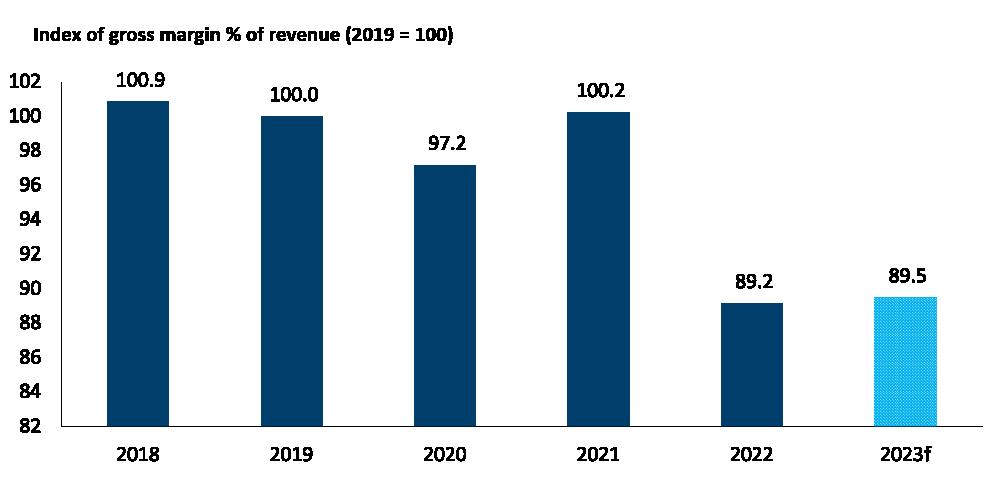

Higher costs pressured food and beverage manufacturing margins. Gross margins as a percent of sales fell to their lowest level in over 20 years in 2022

Manufacturers have always struggled to pass on higher costs in 2022. FCC Economics is forecasting gross margins to improve slightly in 2023. Important to note that trends in margins differ widely across different industries.

GROSS MARGINS DECLINED TO RECORD LOWS IN 2022; THEY’RE FORECASTED TO SEE SMALL GAINS IN 2023

Continued on page 10 https://www.yesgroup.

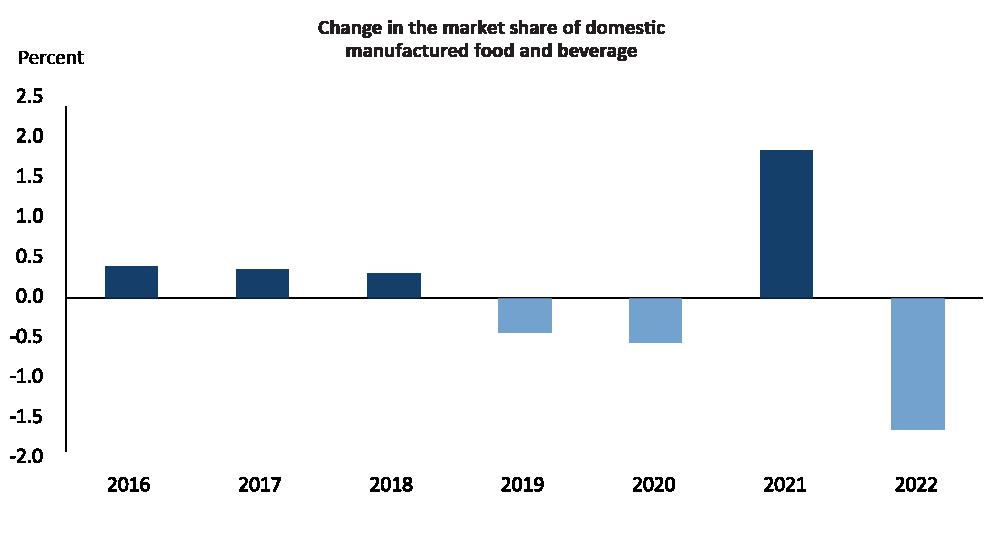

Food Imports Gained Market Share In Canada In 2022

As the year progressed, higher food prices and declining savings led consumers to cut back on discretionary spending. This meant fewer purchases of premiumpriced foods, including smaller-batch and locally-made foods for which manufacturers couldn’t lower costs and control prices. Consumption of Canadian-made food in 2022 (measured in dollars relative to total consumption) reverted to the trend observed before the pandemic. A larger percentage of food dollars spent in Canada was allocated toward imported foods (Figure 3). Several economic and demographic factors dictated an opportunity for domestic food manufacturers. FCC Economics estimates that, had Canadian manufacturers been able to meet the same level of domestic demand as in 2021, total sales would have been over $2.3 billion higher in 2022.

BOTTOM LINE: LET’S NOT LOSE SIGHT OF OPPORTUNITIES

Despite these recent challenges and weaker margins, the food and beverage manufacturing sector remains healthy and has a positive long-term outlook. We are seeing promising innovations and technology implemented in food manufacturing plants, and global demand for Canadian-produced food is growing rapidly. Canada is uniquely positioned to expand its reach into new, growing and very profitable food industries.

https://www.beaconmetals.com

EGGFLATION: WHAT HAPPENS AFTER EGG PRICES REACH HISTORIC HIGHS

By Nan-Dirk Mulder, Senior Analyst, Rabobank

Global egg prices have reached historic high levels and this has a big impact on the egg supply worldwide. How long will this situation last and are there ways to stabilize supply? We expect prices to stay relatively high throughout 2023, especially in markets heavily impacted by avian flu, high costs, and regulatory changes. In other markets there will be some drop in prices, but not to pre-2021 levels, as lingering high input costs are keeping prices higher. One of the main tools to stabilize markets is better value chain cooperation, especially greater commitment from buyers to offset farmers’ high production risks. The other main strategy is to better control avian flu in heavily affected countries.

High Prices Shaking Up Global Egg Supply Chains

Egg prices have reached record-high price levels in many markets. Rabobank’s global egg price monitor reached a new record in Q1 2023, with the index now peaking above 250, which means prices are 2.5 times higher than the reference year of 2007, and have increased more than 100% since this time last year. Between Q1 2022 and Q1 2023 prices in the US and EU increased by 155% and 62%, respectively, while egg prices in Japan reached JPY 235 in March, their highest level since 2003.

Prices in many other markets have reached historic highs as well, including in Thailand, the Philippines, Israel, New Zealand, Nigeria, Kenya, Brazil, Mexico, and Argentina. These sudden price increases have a big impact on players in the egg supply chain – from breeders to producers and further along to customers in retail, foodservice, and food processing.

Historically, egg prices have roughly followed the FAO Food Price Index. Some periods have seen divergences, such as 2007 to 2013, when the industry struggled to pass on high and volatile feed prices. And in 2013 to 2019, egg prices were slightly higher than index’s movements, as demand for eggs was relatively strong while feed costs normalized.

Egg prices followed the food price index when feed prices rose in 2021 and accelerated in 2022, after Russia invaded Ukraine. Since then, egg prices and the food price index have again diverged: Egg prices have kept rising while food prices have started to drop. Some markets, like China and India, are less bullish (so far), with prices up by only 15% to 20%. In Brazil, potential future avian influenza (AI) outbreaks – given cases reported in nearby Argentina, Uruguay, and Bolivia where there is a high concentration of egg production, is hit.

WHAT DRIVES EGGFLATION?

These high global egg prices reflect a combination of six supply and demand factors. The relevance of each factor differs a bit by region, but in most markets currently facing peaking prices, a combination of the following factors is affecting prices.

1. Upward movements in feed costs. Feed represents 60% to 70% of a layer farmer’s costs. Any change – and especially any uncertainty – surrounding feed costs affects egg prices. Global feed prices doubled between mid-2020 and mid-2022. This has had a big impact on the egg industry, as it has been difficult for producers to pass on these higher costs to customers.

2. The impact of avian influenza outbreaks. AI pressure has been very high over the past two years. In the US, more than 40m layers were depopulated during 2022. In Japan, more than 15m layers have been affected, and in Europe the laying hen flock is down by 3% to 5%.

3. The aftermath of Covid-19 market disruptions. Many operations scaled down after Covid-19 measures restricted people’s movement, which highly impacted demand.

4. Regulations. The introduction of male chick culling at the hatchery level in Germany in 2012, for example, has had a big impact on the market. According to market data agency MEG, Germany lost 20% of its laying hens due to this restriction. As Germany is Europe’s largest importer of eggs, this affects the wider EU egg market. Similarly, the introduction of a cage ban for producers in New Zealand has led to a 5%-to-12% drop in laying hens in the country.