2025: AI, ROBOTICS AND SENSOR TECHNOLOGY ARE RAISING THE INDUSTRY TO NEW HEIGHTS

Canadian Beef Industry Works to Navigate Trade Challenges

FCC: Potential Trade Disruptions Dampen Strong Cattle Outlook

Strengthening Food Security in Communities Across Canada

CFIB: Canada Needs to Eliminate Red Tape and Internal Barriers to Trade Food

February 2025

Meat Institute: Dietary Guidelines Should Include Meat as Part of Healthy American Diet

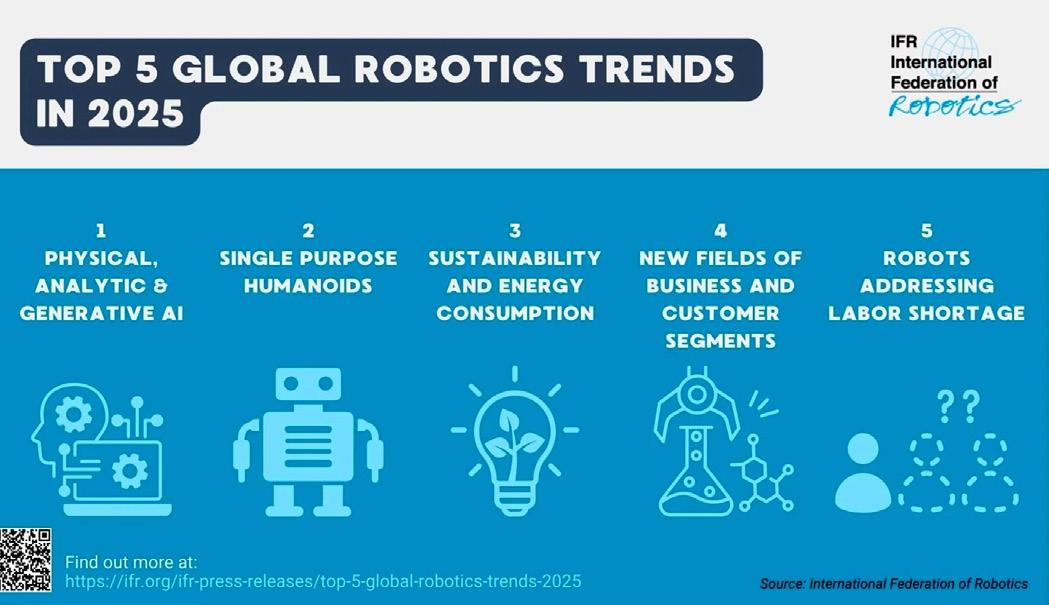

IFFA 2025: AI, Robotics and Sensor Technology are Raising the Industry to New Heights

Canadian Beef Industry Works to Navigate Trade Challenges and Pursue Global Opportunities

5 6 10 12 14 18 20 24

How Shifting Consumer Demand Patterns are Contributing to High Egg Prices

Potential Trade Disruptions Dampen Strong Cattle Outlook

Strengthening Food Security in Communities Across Canada

CattleFax Forecasts

Continued Strong Demand and High Price Outlook for Cattle ProducersClimate Optics?

Canada Needs to Eliminate Red Tape and Internal Barriers to Trade Food

February 2025 Volume 25 Number 2

PUBLISHER

Ray Blumenfeld ray@meatbusinesspro.com

CO-PUBLISHER

Deb Wilson deborah@meatbusinesspro.com

MANAGING EDITOR

Scott Taylor publishing@meatbusinesspro.com

DIGITAL MEDIA EDITOR

Cam Patterson cam@meatbusinesspro.com

CONTRIBUTING WRITERS

Brian Earnest, Leigh Anderson, Juliette Nicolay, Cam Patterson, Jack Roberts

CREATIVE DIRECTOR

Patrick Cairns

Meat Business Pro is published 12 times a year by We Communications West Inc

MEAT INSTITUTE: DIETARY GUIDELINES SHOULD INCLUDE MEAT AS PART OF HEALTHY AMERICAN DIET

The Meat Institute has called on the U.S. Departments of Health and Human Services (HHS) and Agriculture (USDA) to include meat and poultry as part of a healthy American diet noting flaws and contradictions in the 2025 Dietary Guidelines Advisory Committee’s Scientific Report (Report).

“The Committee’s Scientific Report contains contradictory and confusing findings,” said Meat Institute President Vice President of Regulatory and Scientific Affairs, Susan Backus. “Meat and poultry products are nutrient dense foods that help Americans meet their essential amino acid and nutrient requirements and yet the Report recommends a reduction in red and processed meats. When 95% of Americans eat meat, it is important to provide clear dietary guidance to consumers on how they can include the meat products they love in their diets and also produce a positive, measurable health impact.”

The contents of this publication may not be reproduced by any means in whole or in part, without prior written consent from the publisher. Printed in Canada. ISSN 1715-6726

Meat and poultry products provide consumers with a convenient, direct, and balanced dietary source of all essential amino acids. Per serving, meat, poultry, and fish provide more protein than dairy, eggs, legumes, cereals, vegetables, or nuts. Protein is critical for developing, maintaining, and repairing strong muscles; is vital for growth and brain development in children; and is essential to prevent muscle loss during aging.

At issue is the Committee’s Report recommendation for modifications to healthy dietary patterns which emphasizes dietary intakes of beans, peas, and lentils while reducing intakes of red and processed meats.

The Report excludes meat and poultry as part of healthy dietary patterns, the Meat Institute is extremely concerned that consumers will inaccurately perceive meat and poultry products as poor dietary choices, which may lead to a variety of unintended consequences, including nutritional deficiencies in certain subpopulations.

In addition, the Report found that iron is a nutrient of public health concern for adolescent females, women ages 20-49 years; and individuals who are pregnant. The Committee also found that many individuals over the age of one year consume below the nutrient intake requirements for dietary protein, dietary fiber, calcium, potassium, magnesium, iron, zinc and more.

A recommendation to reduce, limit or avoid nutrient dense products like meat and poultry will have significant unintended nutritional consequences across all life stages, especially in those subpopulations of concern.

For more information, visit https://www.meatinstitute.org/

IFFA 2025: AI, ROBOTICS AND SENSOR TECHNOLOGY ARE RAISING THE INDUSTRY TO NEW HEIGHTS

The meat and protein processing industries are facing major challenges. Pressure on prices, a wide range of products and the ongoing shortage of skilled labour call for efficient working practices if the industry is to remain competitive globally.

Increasing automation and innovative technologies such as artificial intelligence and robotics represent potential solutions: they can boost productivity and cut operating costs. Under the motto ‘Maximum Performance’, the world's leading trade fair for the meat and protein processing industry, IFFA - Technology for Meat and Alternative Proteins, will show what is already possible and demonstrate the course the industry needs to take in the future.

Automation is the name of the game in many branches of industry: it not only improves the performance of machines and systems but also helps avoid production interruptions and save energy and materials. In the food industry, for example, automatic product control and traceability is virtually mandatory to ensure a consistently high level of quality and meet strict legal requirements. It is also an ideal tool for tackling challenges such as rising costs and the shortage of skilled labour.

Process automation in the meat and protein industry ranges from raw material preparation with mixing and grinding, via processing with portioning, filling and moulding, as well as thermal processes such as cooking and cooling, to automatic packaging and intelligent logistics. In many cases, however, the various process stages and production lines are not networked with each other, meaning that data exchange is impossible and cannot be used to optimise the various processes. Fortunately, there is a remedy because web-based process control systems such as MES and ERP often consist of modular software systems that can be retrofitted to existing installations. Thus, the advantages of a fully networked smart factory are not just the preserve of new production facilities.

The foundation of many automatic processes is realtime data collection and analysis. Modern sensors supply precise information regarding temperature, humidity, weight and pressure. For example, temperature and humidity sensors in cold stores are used to prevent the temperature rising and thus avoid the risk of contamination. Weight sensors check the weight of each individual meat product and ensure that the packaging is in line with specifications. This not only reduces the amount of material used but also minimises waste and the return rate. Another example is sensors for monitoring the gas composition in packaging, which ensures the desired conditions are always maintained.

In common with many other industries, the introduction of artificial intelligence (AI) is also transforming the meat and protein industry and taking it to a new level by enabling machines not only to collect data from the various stages of production but also to analyse and deduce potential improvements from it. In the event of disruptions in the production process, AI can identify cause-and-effect relationships and thus rectify problems without stopping the production process or prevent them occurring in the future. This not only boosts efficiency but also means higher levels of certainty for both consumers and companies.

Continued on Page 8

Industrial image recognition and processing is also based on AI models that have been trained for the application in question. For example, it is used to sort meat products in accordance with specific criteria, such as size, shape and structure. This reduces the employee's workload at the same time as increasing precision. If used to identify quality criteria, such as grain or fat content, it can significantly increase the selling price of individual items. AI-aided image processing systems are also employed in quality assurance. Using historical image data, they are trained to inspect the entire production process in real time and detect any irregularities such as colour anomalies, foreign objects or defective packaging.

Predictive maintenance is another area of application. AI-aided systems monitor machine status and predict downtimes so that maintenance work is only carried out when required. According to a McKinsey study, predictive maintenance in the food industry can reduce maintenance costs by as much as 30 percent and increase plant utilisation by 20 percent.

MACHINE LEARNING LIFTS ROBOTICS TO A NEW LEVEL OF DEVELOPMENT

Today, industrial robots are an established feature in the food industry, especially in larger companies. Operating around the clock, they can bring about considerable gains in efficiency and productivity. However, the dividing line between conventional machines and those with integrated robot technology is not clear cut. It can be said, however, that industrial robots are mainly used to perform repetitive tasks, such as those typically found in the meat processing industry, for example cutting, portioning, packing, wrapping, sorting, picking and placing.

AI is also taking robotics to a new level of development. Generative AI can use machine learning to adapt independently to new circumstances and situations, thus enabling industrial robots to act more autonomously and agilely. A good example of this is autonomous mobile robots (AMR). Equipped with cameras and sensors, they can independently assess and analyse their surroundings. For instance, they look for new paths when obstacles block the planned route and act independently in abnormal situations. Accordingly, they are perfect helpers in unstructured production settings, as well as in warehouses or logistics centres where packaging and palletising are involved.

Despite the multitude of items in such distribution centres, AI-aided industrial robots can select and retrieve the right articles, reject faulty or deformed ones and detect packaging formats and weights. Such robots achieve pick rates of 750 to 1,400 items per hour and can, for example, pack up to 200 meat products per minute – a significant increase in productivity compared to manual processes. Robots are also superior to their human colleagues in terms of precision, e.g., they can cut meat faster and more precisely at a very specific cutting angle, as well as portion by weight and ideal shape, which not only speeds up the production rate but also minimises raw-material waste.

Multifunctional robotic work cells hold out the promise of an enormous increase in flexibility and are set to replace traditional line production in the meat industry, too. For example, using AI, the robotic work cell can independently process pork sides in a series of operations, which are carried out all at once instead of a series of small operations. Thus, different products can be processed in parallel, enabling an optimum product mix without the restrictions of line production. At the same time, the robotic work cells form autonomous networks with the AMRs, which react independently when faced with changing requirements.

The meat and protein processing industry is on the cusp of radical change, driven by the use of new technologies such as AI, robotics and sensor technology. These technologies are not only an opportunity to automate processes and increase efficiency but also to enhance product quality and sustainability. Companies that integrate these technologies at an early stage are well prepared to ensure their competitiveness on the global market and meet the increasing challenges of tomorrow’s world. For

CANADIAN BEEF INDUSTRY WORKS TO NAVIGATE TRADE CHALLENGES AND PURSUE GLOBAL OPPORTUNITIES

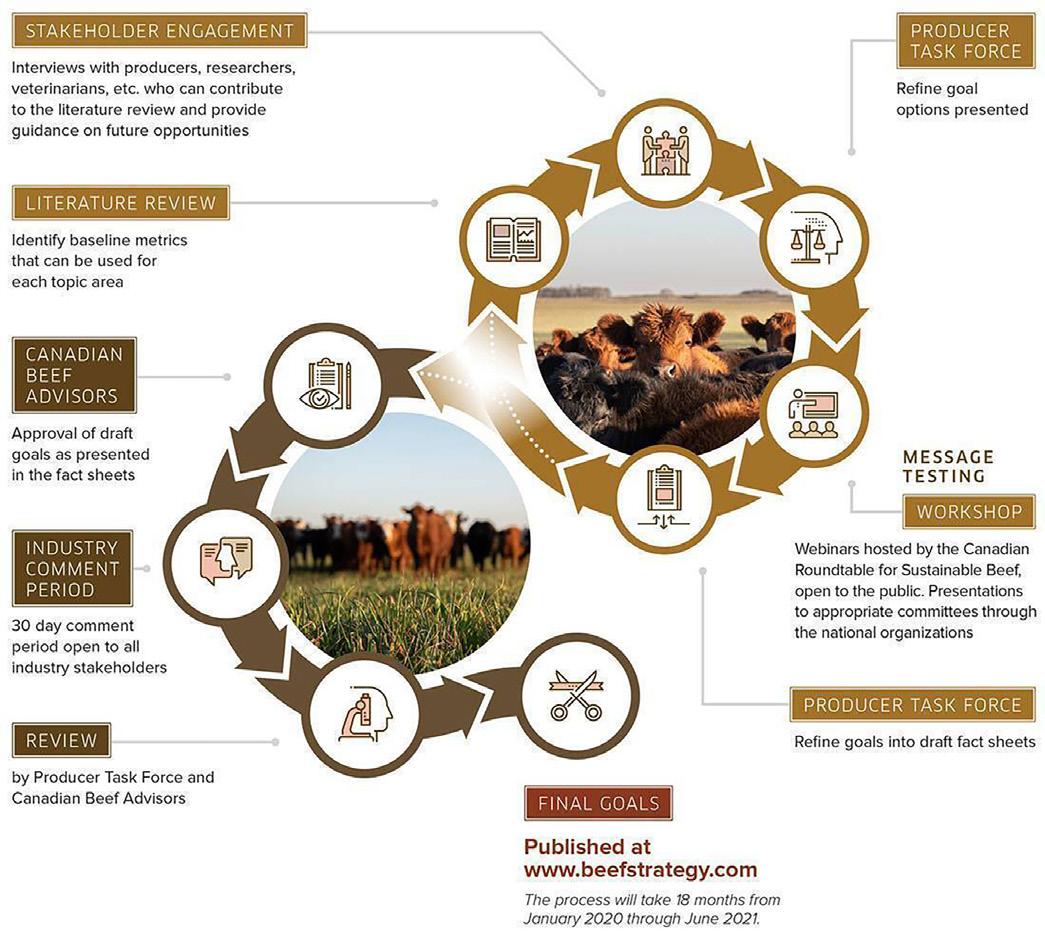

The Canadian Beef Advisors recently released their 2025-30 National Beef Strategy. The strategy positions the Canadian Beef Industry for greater profitability, growth and being a high-quality beef product of choice in the world. “The National Beef Strategy is about the future. We want people to know that the beef industry is preparing the way for the next generation,” states Bob Lowe, Chair of Public and Stakeholder Engagement.

The Canadian Beef Advisors believe a united industry is a stronger industry which benefits all those working in it today and into the future. This collaboration is key as industry works together to navigate current trade challenges and pursue global opportunities. The National Beef Strategy facilitates collaboration and coordination between the national organizations to leverage available resources on behalf of producers and processors.

Substantial progress was made under the 2020-24 strategy, and the intention is to continue building on the momentum. Nathan Phinney, Chair of the Canadian Beef Advisors comments that “tracking goals has been a productive exercise. We are seeing wins, and the Beef Advisors are excited about where we can go next.”

There have been significant strides made toward recognizing the important role beef cattle play in environmental sustainability. However, it is also acknowledged that producers have faced a multi-year drought, along with higher interest rates and input costs that have shifted cost structures. Cross border engagement and maintaining a strong Canada-U.S. trade relationship is a key priority. Staying on top of advocacy issues continues to be a strong focus and there are also bottlenecks to work on.

The National Strategy has been developed to achieve the Beef Industry 2030 goals. These are aligned with our shared vision and mission of a dynamic, profitable Canadian cattle and beef industry that produces the most trusted and competitive high-quality beef in the world, recognized for our superior value, safety, innovation and sustainable production methods. Calvin Vaags, from the Canadian Meat Council notes that “a growing population and middle class means that the demand for protein is outpacing production, driving prices higher. The protein pie is getting bigger and Canada, as a relatively low emissions intensity producer,1 deserves a seat at the table.”

The Canadian Beef Advisors consist of elected leaders and staff representation from the seven national beef organizations responsible for policy, marketing, research and sustainability. This diverse group of experienced industry representatives is responsible for advancing the strategy with the industry stakeholders, providing recommendations on future direction and reporting results toward strategy goals and objectives.

Learn more about how stakeholders can achieve a dynamic and profitable Canadian cattle and beef industry at www.beefstrategy.com.

The National Beef Strategy is a collaborative effort by Canadian national beef sector organizations including the Beef Cattle Research Council, Canadian Beef Breeds Council, Canada Beef, Canadian Cattle Association (and its provincial member associations), Canadian Meat Council, Canadian Roundtable for Sustainable Beef, and the National Cattle Feeders’ Association.

HOW SHIFTING CONSUMER DEMAND PATTERNS ARE CONTRIBUTING TO HIGH EGG PRICES

By Brian Earnest

U.S. consumers are facing a prolonged period of higher U.S. consumers are facing a prolonged period of higher egg prices that will likely extend through the Easter holiday and well into 2025. Rising egg prices and increased volatility in the market are largely attributable to supply challenges brought on by Highly Pathogenic Avian Influenza. Since the current outbreak began impacting U.S. poultry farms in 2022, nearly 100 million table egg laying hens have been affected.

However, HPAI is not the only factor contributing to the supply and demand imbalance driving egg prices higher. Consumer demand for eggs has skyrocketed in recent years, with per capita consumption growing 20% from 2016-2019. Demand has also shifted away from conventional eggs as more consumers are choosing cage-free and other types of specialty eggs – further complicating the supply challenges. Also, nine states have enacted laws that require eggs sold in their states to be from cage-free hens.

According to a new report from CoBank’s Knowledge Exchange, the increase in overall demand for eggs, combined with the growing preference for specialty eggs, is exacerbating the impact of tight supplies precipitated by HPAI. The confluence of all three factors is prolonging the timeline for bringing egg supply and demand into closer alignment. Until then, retail egg prices will remain elevated.

“Egg demand was relatively stable in the early 2000s and seasonality played a much bigger role in peak demand periods than it does today,” said Brian Earnest,

lead animal protein economist with CoBank. “While seasonality remains an influencing factor, egg use has grown dramatically over the last 20 years. “Eggs have become a staple item for innovation in quickservice restaurant entrees, and marketing trends like the emergence of all-day breakfast have significantly boosted egg demand.”

Rising demand for cage-free eggs has also outpaced supply in recent years. Currently, more than 120 million or roughly 40% of the table egg layers in U.S. commercial flocks are housed in cage-free production systems. That compares with just 30 million layers housed in cage-free systems in 2015. While the growth in supply of cage-free eggs has been substantial, more will be needed to adequately meet demand projections.

Total egg laying hen inventories, including conventionally raised hens, have not been substantially depleted from where they were at the beginning of the HPAI outbreak. Commercial operators who have been impacted have moved swiftly to repopulate hens. Through January 2025, the U.S. egg industry has 8% fewer egg-laying hens than it did two years ago. But HPAI has evolved to become a persistent, year-round threat to production.

“The last widespread outbreak of HPAI in 2015 was largely seasonal with most cases occurring during the winter and spring migration periods for wild birds,” said Earnest. “That seasonality appears to be gone. During the current outbreak, HPAI has been detected in birds or other species nearly every month since the outbreak began in February 2022.”

Avian influenza may be the biggest factor driving egg prices higher, but rising consumption and demand for specialty eggs are also playing role.

https://www.beaconmetals.com

POTENTIAL TRADE DISRUPTIONS DAMPEN STRONG CATTLE OUTLOOK

By Leigh Anderson, Senior Economist, Farm Credit Canada

The cattle market continues to reach new highs. Canadian cattle operations after prolonged periods of drought and expensive feed ended last year optimistic about 2025.

Cattle prices are record high, feed availability has increased and feed costs are easing.

Even with record high cattle prices and strong profitability, the Canadian beef herd in 2024 reached a three-decade low, while the number of replacement heifers was near an all-time low. The U.S. herd is in a similar situation as cow numbers declined through 2024, which were reflected in the January 1, 2025, beef herd estimate of 73.4 million head. We’re expecting a drop in the Canadian cattle herd as well.

As we outlined in our top trends to monitor in 2025, cow and heifer slaughter rates will need to decline below 47% of slaughters before we are likely to see any herd growth. We expect some easing of the number of heifers heading to slaughter but not enough to rebuild the herd. Overall, the small North American cattle herd is expected to continue driving prices, leading to yet another year of strong cow-calf profitability in 2025

While the supply and demand fundamentals create a positive outlook for cattle prices, uncertainty around potential trade barriers is being closely watched by the sector. Any tariffs applied to Canadian exports will impact the Canadian-U.S. livestock sector given the highly integrated North American market. Canada exports 17% of its total cattle production, with Canadian exports to the U.S. making up 99% of all exports. Of those cattle being sent to the U.S., 70% are destined for slaughter. Canada also imports feeder cattle to fatten until they are ready for slaughter. Over half of all Canadian slaughtered beef is exported with majority of it heading to the U.S. We also rely on some U.S. beef imports to meet Canadian demand. This interconnectedness between the two countries means tariffs or any other trade barriers will significantly disrupt cattle operations on both sides of the border.

TABLE 1: CATTLE PRICES PROJECTED TO REMAIN STRONG IN 2025

PROPOSED TARIFFS ARE EXPECTED TO PRESSURE CANADIAN CATTLE PRICES

DF: I don’t think being on the island has really impacted us negatively one way or the other. We’ve traveled a lot, met a lot of other farmers and livestock producers in other parts of Canada, and we all seem to have the same issues and same concerns.

CMB: I understand that your farm was the first in Atlantic Canada to be involved in the TESA program.

DF: Yes, I think we were the first farm east of Ontario as far as I understand.

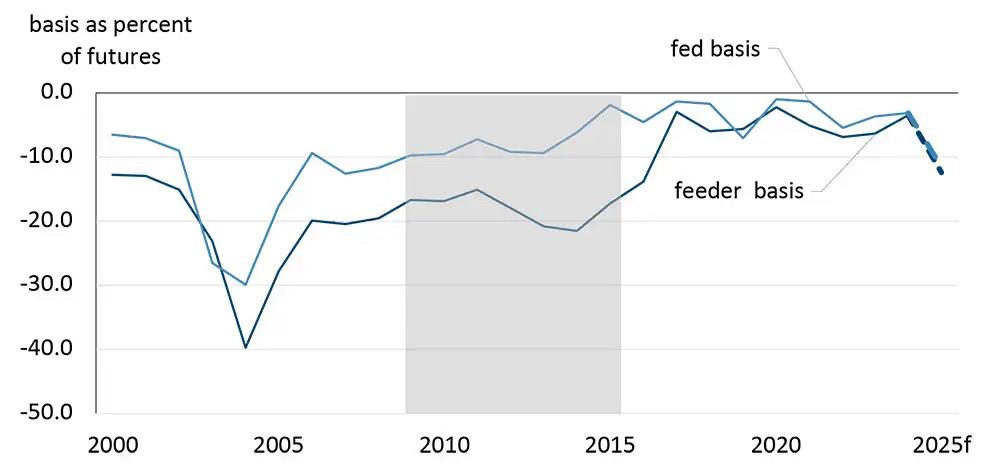

Canadian fed cattle prices and feeder cattle prices follow trends of both live cattle and feeder cattle futures, both priced in U.S. dollars. The difference between the Canadian cash price and the futures prices is known as the basis (cash price – futures price = basis). If tariffs are introduced, then basis levels are likely to widen as the costs induced by tariffs will be passed from buyers to sellers.

I’m not sure why the eastern associations wouldn’t have previously nominated anybody because there are many farms here on PEI doing every bit as much as we are as to attain a high level of sustainability. Anyway, we were very surprised when the PEI Cattleman’s Association nominated our farm.

CMB: And then you were attending the Canadian Beef conference in Calgary and you won.

DF: Yeah! That was a very nice moment for us. But I don’t like to use the word win actually. However, being recognized for our commitment was a real honour. If you want to know the truth, it was a pretty humbling experience. As I said to CBC when they phoned me after the conference, I was just floored, really couldn’t believe it.

Past trade restrictions from the U.S. can provide guidance as to possible price impacts of tariffs. The presence of bovine spongiform encephalopathy (BSE) in Canada from 2003-2005 and mandatory country of origin labelling (mCOOL) from 2009-2015 illustrate how wide basis levels could get (Figure 1). We estimate Canadian cattle prices could decline 5-10% with 25% tariffs applied at the U.S. border. For example, our feeder 850 lb price forecast would decline to a $320-$340 per cwt range. As wide as basis levels could get, expressed as a percentage of future prices in Canadian dollars the impact won’t be as severe as experienced during BSE. Nonetheless any trade restriction will reduce Canadian cash prices. However, if tariffs are short-lived the impact will be smaller.

CMB: So now that you have been recognized, do you think that will draw more attention and garner more nominations out of Atlantic Canada going forward?

Prince Edward Island. We are small players in the national beef industry

https://www.yesgroiup.ca

FIGURE 1: CANADIAN FED CATTLE AND FEEDER BASIS LEVELS EXPECTED TO WIDEN

The impact of tariffs on the Canadian cattle supply chain will vary based upon supply and demand fundamentals, exposure to the U.S. market and the length of time tariffs are in place. At the cow-calf level, the impact will be seen in a wider basis as cattle bids decline to offset the increased risk of exporting to the U.S. Feedlots, especially those involved in exporting to the U.S., face uncertainty regarding whether potential tariffs will still be in place or escalated by the time feeder calves are finished and ready for slaughter. U.S. packers are likely to adjust their bids and volumes of purchases of Canadian cattle. For Canadian meat processors, export sales of boxed beef to the U.S. will also face risks and will likely be discounted as a result to compete in the U.S. market.

Overall, given current healthy margins, the cow-calf sector is better positioned to cushion the blow from potential U.S. tariffs, although profitability will likely be reduced. The feedlot sector, which is poised to see improved profitability this year, would be at risk of recording lower returns depending on the magnitude and duration of the tariffs. The complexity of the tariff's impact depends on how different players in the supply chain respond to mitigate their risks.

For instance, U.S. and Canadian beef packers may adjust their strategies. The cattle sector is currently taking a wait-and-see approach, limiting new sales of cattle to the U.S. to mitigate the downside risk of tariffs being in place by the time cattle are ready for slaughter. They are staying current on marketings while being cautious about placements into feedlots. Imports of feeders are likely to slow as fewer feeders are exported and feedlots turn to domestic supplies.

While potential U.S. tariffs are the largest factor impacting our cattle outlook this year, there are other trends to monitor as well.

TRENDS TO MONITOR IN 2025

1. CONSUMER DEMAND

The beef consumer has been resilient. How long will consumers continue to purchase beef at record high prices? Do beef consumers have a tipping point and how is their consumption behaviour impacted by prices of competing meat proteins? If consumers back away, then we can expect cattle prices to reach their limits. Until we see consumer demand start to drop off, cattle markets will continue to stay strong.

VALUE OF THE CANADIAN DOLLAR

NEW SURREY SLAUGHTERHOUSE

The Canadian dollar will have an impact on the value of cattle and feed costs. Any depreciation in the Canadian dollar will provide a boost to cattle prices received by farmers but may also boost costs of feed grains. We estimate that a 1% depreciation of the dollar increases cattle farm cash receipts by about 0.6%.

in the U.S. to be labeled “Product of USA” (currently, companies in the U.S. are allowed to import Canadian animals, raise and/or slaughter them, and use a “Product of USA” label). While January 2026 may seem like a long way away, feeder placement decisions will be felt much sooner as some calves head to the feedlot up to nine months prior to when they will be ready for slaughter. This policy, while voluntary, could result in weaker demand for Canadian cattle heading south and widen basis levels here in Canada. U.S. slaughter plants will begin adjusting procurement of cattle to gear up for the changes. As we progress through 2025, more U.S. beef slaughter plants are expected to implement changes.

‘WOULD OPEN DOOR’ TO NEW BEEF MARKETS

Proposed 30,000-square-foot beef abattoir in Cloverdale would be B.C.’s largest such facility

A federally licensed beef processing facility is in the works

“There’s a new building coming forward, a new abattoir, I think that’s the French pronunciation of slaughterhouse,”

the ability to not have to ship an animal to Alberta to have Agricultural and Food Sustainability Advisory Committee.”

3. VOLUNTARY COUNTRY OF ORIGIN LABELLING (VCOOL)

The facility is proposed on a 25-acre property within the Agricultural Land Reserve at 5175 184th St. The planned 30,000-square foot abattoir in Cloverdale would process up to 100 head of cattle per day.

Further complicating the outlook for exports of cattle to the U.S. is the vCOOL requirement that will be coming into effect on January 1, 2026. The rule requires animals to be born, raised, slaughtered, and processed

According to a city report, that would make it larger than any other processing facility in B.C.. But it would still be small by industry standards, compared to the largest meat processing plants in Alberta that process 3,000 heads of cattle per day.

The proposed facility would be fully enclosed and designed

BOTTOM LINE

the proposed abattoir, to become a federally registered meat establishment and expand the operation. This would allow the meat products to be transported beyond B.C.’s boundaries.

The Canadian cattle sector is poised for another year of strong prices and increasing profitability driven by strong market fundamentals (including the small herd size) and strong demand. The outlook is however clouded by potential U.S. tariffs and other looming trade disruptions.

“Our focus is on trying to bring a more efficient, sustainable local product to the market, realizing we can do that now in a very limited sense,” said Les. “I caution people when talking to them and they say, ‘What a big plant, that’s going to go allow you to go mainstream.’ Well, yes, if you look in the context of B.C., but this is still a very niche plant and we’ll serve a niche industry for producers and for the market. It’s certainly not going to be a monstrosity of a plant but it’ll be a big upgrade from the site currently.”

2.

STRENGTHENING FOOD SECURITY IN COMMUNITIES ACROSS CANADA

Kids need access to nutritious food at school so they can learn, grow, and reach their full potential. That is why the Government of Canada is taking action to strengthen wider community and local food systems through investments in infrastructure that expand the reach and impact of school food programming.

Lawrence MacAulay, Minister of Agriculture and AgriFood, recently announced the 10 initial recipients of the $20.2-million federal School Food Infrastructure Fund (SFIF). As part of the $62.9-million announcement in Budget 2024, Agriculture and Agri-Food Canada (AAFC) is delivering the SFIF over the next year to support the purchase and installation of infrastructure and equipment that increases the capacity of community organizations to produce, process, store, and distribute food for school food programs.

"No child should go hungry at school,” stated Minister MacAulay. “We're working with the provinces and territories to deliver our National School Food Program and partnering with trusted not-for-profit organizations to build up the infrastructure and purchase the equipment needed for school food programs across the country. Together, we can make sure our kids have the healthy meals they need to succeed in the classroom and beyond."

The initial recipients include Breakfast Club of Canada, Farm to Cafeteria Canada, Food Banks Canada, Food Depot Alimentaire, Food First NL, Mazon Canada, Saskatchewan School Boards Association, Second Harvest, United Way BC and United Way East Ontario.

These initial recipients will further distribute funding to eligible not-for-profit organizations (known as ultimate recipients) through individual application intakes. Eligible community-based organizations are encouraged to use the SFIF Initial Recipient Finder to determine

which organization best serves their geographic area and needs.

QUICK FACTS

• The SFIF is delivered as a complement to both the National School Food Program, and the guidance provided under the National School Food Policy.

• Launched on September 6, 2024 by Minister MacAulay, the SFIF uses a further distribution of funds model that allows AAFC to leverage the expertise and networks of not-for-profit organizations that are active in the school food programming space. AAFC will rely on the expertise of the initial recipients to select the organizations and activities (ultimate recipients) to be funded.

• Projects and final funding are subject to negotiation of a contribution agreement.

• As another component of the $62.9-million announcement in Budget 2024, AAFC is delivering Local Food Infrastructure Fund (LFIF), which mobilizes up to $42.7 million to support production-focused projects that improve community food security and resilience through the purchase and installation of infrastructure that will increase access to local, nutritious and culturally-appropriate food.

• Announced in Budget 2024, the National School Food Program will feed hundreds of thousands of kids across Canada every year. The Program will also be a safety net for the kids who are most impacted by the lack of access to food, including lower-income families and some Indigenous communities. This funding will provide up to 400,000 additional children per year across Canada access to nutritious food at school.

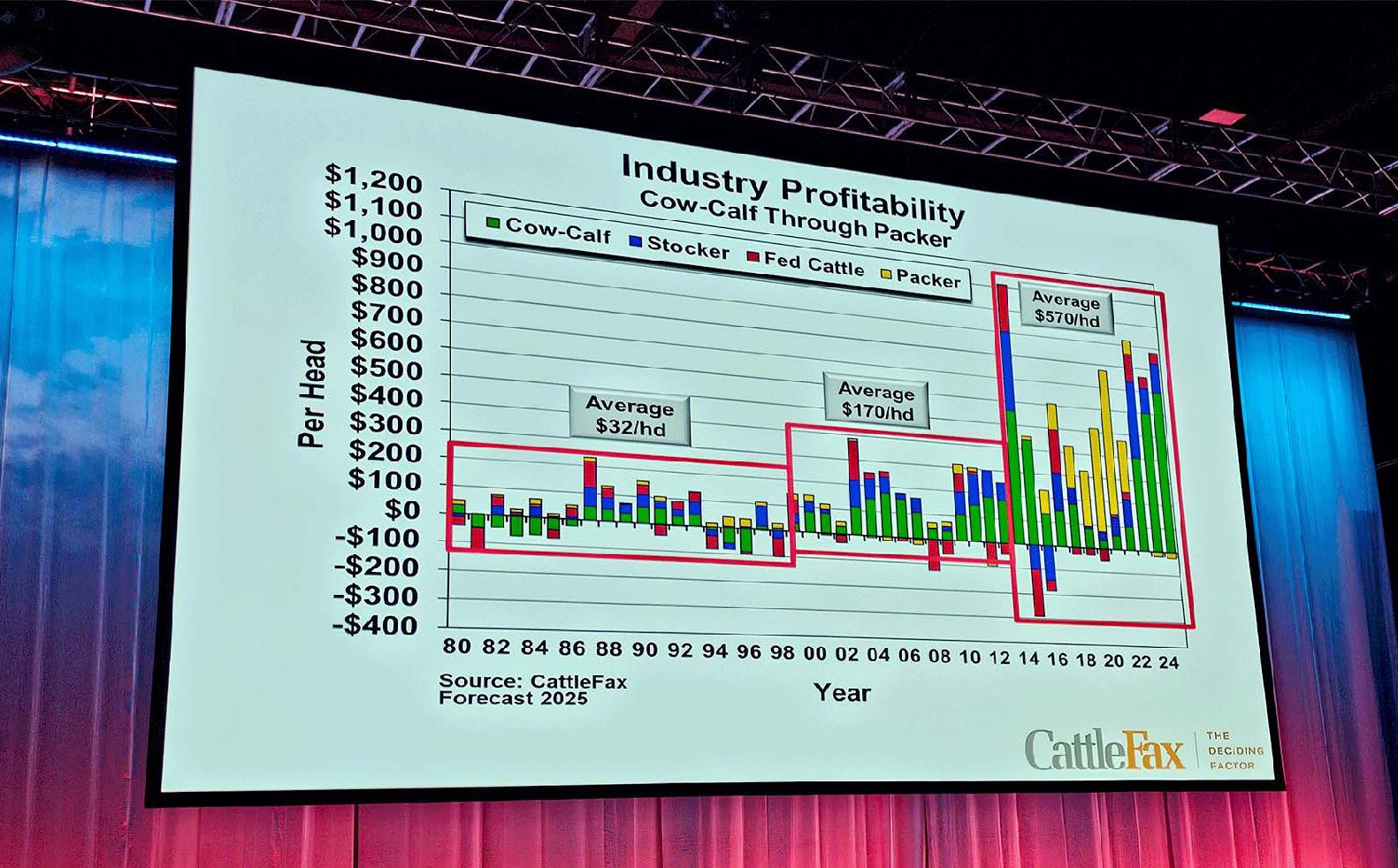

CATTLEFAX FORECASTS CONTINUED STRONG DEMAND AND HIGH PRICE OUTLOOK FOR CATTLE PRODUCERS

The popular CattleFax Outlook Seminar, held as part of the recent CattleCon 2025 in San Antonio, Texas, shared expert market and weather analysis.

The U.S. beef industry is poised for another year of strong market performance, driven by tight cattle supplies and robust consumer demand. As the beef cowherd enters a stabilization phase following years of contraction, the resulting supply constraints have shifted market leverage decisively in favor of cattle producers.

Weather conditions will remain a critical factor influencing grazing availability, herd expansion and cattle prices. Meteorologist Matt Makens said La Niña this winter brings rather volatile weather changes across North America with the majority of weather extremes affecting those in the Central to Eastern U.S. For Mexico and the Southwestern U.S., producers will see drought acreage increase as it has nationwide since June.

“Drought will likely increase across the Western U.S. this spring and into the Pacific Northwest, Northern Plains, and Canadian Prairies through this summer. To watch will be the North American monsoon and how much drought relief it can provide to Mexico, the Southwest, and parts of the Plains,” he said. “Current data show the monsoon is likely to produce more moisture this year than last. A strong enough monsoon can decrease precipitation across the central Corn Belt, watch July closely. Late in the year, the focus turns to the development of La Niña or El Niño.”

Shifting the discussion to an outlook on the economy, energy and feed grains, Troy Bockelmann, CattleFax director of protein and grain analysis, noted that inflation eased in 2024, ending the year at 2.9%, a significant drop from the 9% peak in 2022 but still above the Federal Reserve’s 2% target. To address this, the Fed cut interest rates three times in the latter half of the year, bringing the Prime bank loan rate to 7.5%.

The labor market remained strong, with unemployment briefly rising midyear before falling to 4.1% as job creation outpaced expectations. Combined with solid consumer spending and wage growth, the U.S. economy is expected to see healthy GDP growth of 2 to 2.5% in 2025.

“The Federal Reserve’s rate cuts helped stabilize inflation and support economic growth, but we’re still above target,” Bockelmann said. “Despite economic headwinds, consumer confidence and spending have remained resilient. However, lingering inflation and potential trade uncertainties may limit the extent of further interest rate cuts this year and inflation remains a key factor to watch in 2025.”

CattleFax shared that National Dec. 1 on-farm hay stocks were up 6.3% from a year-ago at 81.5 million tons with hay prices averaging $175/ton in 2024. Corn stocks-to-use at just over 10% and should support the spot market towards $5.00/bu. with a yearly average spot future price of $4.40/bu. expected.

“An increase in corn supply for the new crop year is expected as smaller beginning stocks are offset by larger production levels due to corn regaining acres from soybeans. Stocks-to-use have the potential to be above 13 percent which implies a price range of $3.75 to $5.15/bu. for the 2025 market year,” Bockelmann said. “There is a strong correlation between corn stocksto-use and hay, and we expect hay prices to follow corn and trend a bit higher in the coming year.

On the energy front, he noted, for 2025, not much will change. Average crude oil prices are expected to be near steady with 2024 though risk remains for a reduced U.S. market share of global product due to potential trade policy impacts. He also expects ethanol production to continue to stay strong.

Kevin Good, vice president of market analysis at CattleFax, reported that U.S. beef cow herd is expected to see the cycle low to start 2025 at 28 million head, 150,000 head below last year and 3.5 million head from the 2019 cycle highs.

“We expect cow and bull slaughter to continue declining in 2025, with overall numbers down by about 300,000 head to 5.9 million head total. Feeder cattle and calf supplies outside of feedyards will also shrink by roughly 150,000 head, while cattle on feed inventories are starting the year slightly below 2024 levels at 11.9 million head,” he said. “With a tighter feeder cattle supply, placement pace will be more constrained, leading to a projected 700,000-head drop in commercial fed slaughter to 24.9 million. After modest growth in 2024, beef production is expected to decline by about 600 million pounds to 26.3 billion in 2025, ultimately reducing net beef supply per person by 0.8 pounds.”

Beef prices continued their upward trend in 2024, averaging $8.01/lb., the second-highest demand level in history. While demand may ease slightly in 2025, retail prices are still expected to rise to an average of $8.25/ lb. Wholesale prices will follow suit, with the cutout price projected to reach $320/cwt.

“Retail and wholesale margins are historically thin, making strong consumer demand essential to maintaining higher price levels,” said Good. “While opportunities for further leverage gains are limited, the market remains favorable for producers.”

Inflation remained moderate in 2024, but high consumer debt, elevated interest rates, and competition from more affordable protein options could impact purchasing decisions. However, foodservice demand showed resilience, ending the year stronger as samestore sales and customer traffic improved.

“Despite economic pressures, consumers continue to pay premiums for higher-quality beef,” Good added. “Choice grade or better remains in high demand, reinforcing the strength of the premium beef market.”

Turning to global protein demand, Good noted that the outlook for animal proteins remains strong, although U.S. beef exports are projected to decline by 5% in 2025 due to reduced production and higher prices. Conversely, U.S. beef imports are expected to grow as lean beef supplies tighten.

“The global outlook is currently an interesting scenario as trade policy developments, including potential tariffs, could pose risks to international markets. While growth is expected this year, it may be limited to global competition supply constraints and an uncertain tariff environment,” Good said.

Mike Murphy, CattleFax chief operating officer, forecasted the average 2025 fed steer price at $198/ cwt., up $12/cwt. from 2024. All cattle classes are expected to trade higher, and prices are expected to continue to trend upward. The 800-lb. steer price is expected to average $270/cwt., and the 550-lb. steer price is expected to average $340/cwt. Utility cows are expected to average $140-/cwt., with bred cows at an average of $3,200/cwt.

“While the cyclical upswing in cattle prices is expected to persist, the industry must prepare for market volatility and potential risks. Producers are encouraged to adopt risk management strategies and closely monitor developments in trade policy, drought conditions, and consumer demand,” Murphy said.

2025 USDA All-Fresh Retail Beef prices are expected to average $8.25/pound and, which will continue the balancing act for retail between high prices and reduced supply. Murphy noted that the key is to avoid setting prices too high, especially in light of competition from more affordable proteins.

Randy Blach, CattleFax chief executive officer, concluded the session with an overall positive outlook, and noted that strong margins in the cow-calf sector have set the stage for cowherd expansion to begin, with heifer retention likely back near a more normal pace, relative to minimal retention in recent years. Drought and pasture conditions are now the key factors influencing the rate of expansion with a slower herd rebuild anticipated compared to the last cycle. This more measured expansion pace implies a positive outlook for producer returns over the next several years. Strong consumer demand also remains a bright spot for the industry.

“We have to remember where we came from,” Blach said. “Continued improvements in quality and meeting consumer expectations with a safe, nutritious product and a consistently good eating experience have had tremendous impacts on moving the needle for this industry. We’re moving in the right direction, and we need to keep paying attention to that signal.”

For

CANADA NEEDS TO ELIMINATE RED TAPE AND INTERNAL BARRIERS TO TRADE FOOD

Agri-businesses in Canada are caught in the crossfire of escalating trade tensions between Canada and the U.S. They are facing lost or delayed contracts with U.S. customers, limited access to alternative markets, concerns over perishable goods, and eventually rising cost of doing business. According to a survey from the Canadian Federation of Independent Business (CFIB), in December 2024, 67% of agri-businesses were involved in importing or exporting directly with the U.S. –compared to 51% for all sectors. To reduce uncertainty, mitigate the impact of potential tariffs on Canadian businesses and consumers, effective measures are needed.

Several ideas were put on the table, including “pandemic-style support”. While it may be tempting for governments to focus on widespread assistance programs, as they did during the pandemic, we need decision-makers to be focused on the long-term impact. Instead of focusing on temporary stimulus, Canada’s leaders should view President Trump’s tariff threat as an opportunity to be seized to improve the business climate in Canada. Long term and impactful measures include reducing red tape and eliminating Interprovincial trade barriers.

Businesses in Canada are contending with a complex regulatory landscape. According to CFIB’s 2025 cost of regulations report, more than one-third (35%) of those regulations are excessive. Red tape not only disrupts business owners’ daily operations but also carries a total cost of $17.9 billion annually. It also consumes valuable time, in fact, business owners spend 32 days — an entire month — navigating bureaucratic hurdles every year. Removing red tape doesn’t cost governments anything. All it takes is political leadership.

With regards to interprovincial trade barriers, they limit market opportunity for Canadian businesses. Only $530 billion worth of goods and services move across provincial and territorial borders annually. Should, internal trade barriers be eliminated, it would add $200 billion to the economy, boosting the national economy by four to eight per cent.

In 2024, according to a CFIB survey 42% of agribusinesses agreed that provincially/territorially licensed or inspected products should be sold across provincial/ territorial borders, up to 54% in Manitoba. Nonetheless, barriers to the movement of food have become increasingly more difficult to overcome. This is in part because of the 2019 Safe Food for Canadian Regulations (SFCR), which has added new requirements for businesses. In fact, according to preliminary data from a CFIB survey on CFIA, 58% of agri-businesses highlighted an increase in the overall burden of regulations from the Canadian Food Inspection Agency (CFIA) since the introduction of the SFCA. Even if it is just to trade to another province within Canada, they must navigate licensing requirements and pay Safe Food Canada fees every two years while ensuring products meet labeling, packaging, and traceability standards and preparing a Preventive Control Plan (PCP).

With rising obligations, it is no surprise that 31% of agribusinesses reported a negative impact on their business from the implementation of the SFCR. More specifically, 79% of agri-businesses say excessive government regulations significantly reduce their productivity and ability to grow and 73% say it impedes their business’s ability to compete with larger firms. Therefore, cutting red tape around the SFCR should be a priority for governments to facilitate the interprovincial trade of food and support businesses.

One way to reduce red tape around food, while ensuring safety and health is to expand upon the Regulations Amending the Safe Food for Canadians Regulations (City of Lloydminster). This exemption allows businesses in Lloydminster, which straddles both Alberta and Saskatchewan, to trade across provincial lines within the city without having to comply with the SFCR requirements, treating the city as if it were entirely within one province.

If one product is good enough to be manufactured, sold, or used in one province, it is good enough to be sold and used in other provinces, without having to meet any additional requirements. This is why government should implement mutual recognition of food product regulations with the provinces and territories to allow Canada’s food products to reach all parts of the country.

In July 2024, the CFIA, federal, provincial, and territorial Ministers of Agriculture agreed that efforts be made to accelerate pilot projects for interprovincial trade in meat. Now is the time for them to deliver on this promise. While the SFCA is not the only barrier to internal trade that needs to be addressed, it is an important one.

Nicolaÿ is a Bilingual Policy Analyst for the Canadian Federation of Independent Business (CFIB). CFIB is Canada’s largest association of small and medium-sized businesses with 97,000 members (4,900 agri-business members) across every industry and region. CFIB is dedicated to increasing business owners’ chances of success by driving policy change at all levels of government, providing expert advice and tools, and negotiating exclusive savings. Learn more at cfib.ca.

Juliette

https://www.yesgroup.ca

201 Don Park Road Unit 1, Markham, Ontario, L3R 1C2 Phone: 905-470-1135 1-800-465-3536 Fax: 905-470-8417

Website: www.yesgroup.ca email: sales@yesgroup.ca

Remco and The Yes Group Protecting

your Customers

Remco products are colour-coded to help divide the production cycle into different zones. By identifying these zones as different cleaning areas, the movement of bacteria around the production area can be blocked.

Our products were developed with the Hazard Analysis Critical Control Point (HACCP) in mind.

No matter what colour-coding plan is implemented, Remco Products from The Yes Group provides significant added value at no additional cost. From scoops to squeegees, from brushes to shovels, we have the products and the colours to enhance any professional quality assurance program.