10 minute read

Fire risk

Prevention is better than cure

The consequences of an engine room fire can be devastating. It can lead to loss of life and severely damage a ship. There is a significant risk to the environment as well. Given the abundant presence of fuel, oxygen and ignition sources in an engine room of a vessel, most fires onboard ships start there. The focus needs to be not just on detecting and fighting a fire but also preventing its ignition argues Siddharth Mahajan, (top left) Senior Loss Prevention Executive, Gard (Singapore) Pte. Ltd, Svend Leo Larsen, (middle) Senior Claims Adviser, Gard AS and Kim Watle, (bottom left) Senior Business Analyst, Gard AS

DA T A I N S I G H T S

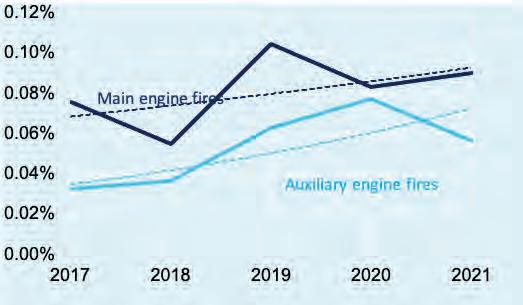

In Gard, when analysing trends, we follow closely the frequency trends of incidents for a given time period as this allows us to account for the growth in our portfolio. For the last five year period, ie from 2017 – 2021, the frequency for the various hull and machinery (H&M) claims areas are showing a downward trend except for fires in engine rooms. Some 60% of these fires originated in the engine room. Key insights from our claims data are as follows: 1. Nearly two thirds of engine room fires occurred on the main and auxiliary engines or their associated components such as turbochargers; 2.For the period 2017 - 2021, the average annual frequency of engine room fires is 0.13%, which means out of every 10,000 vessels, 13 vessels have had one such fire incident each year; 3.As indicated in the graph on page 41, frequency of both main and auxiliary engine fires show a rising trend. 4.If we drill down into different ship segments, then the frequency of such fires on passenger and container ships is almost double that of the Gard 5-year average; and 5.Older vessels are more prone to fires originating in the engine room and frequency peaks for vessels that are between 25–30 years old.

FREQUENCY OF ENGINE FIRES (Gard H&M data)

COMMON CAUSES OF ENGINE ROOM FIRES

Our claims experience indicates that the majority of such incidents were caused by a failure in a flammable oil system, most often in the low-pressure fuel oil piping allowing oil to spray onto an unprotected hot surface.

Below we list some of the most commonly occurring causes of fuel spraying from low pressure piping systems. The list is by no means exhaustive, but a review of past Gard cases has shown that the failures listed below occur frequently: •Piping, piping connections and other associated components, such as o-rings, were not original parts or of a type recommended by the manufacturer. In some cases, modifications had been made by the crew under existing management. In other cases the crew were not aware of such modifications as they had been made under previous ownership or management; • Piping connections had not been tightened to the required torque and, in time, it loosens due to, for example, vibrations. Another reason may be incorrect assembly after maintenance; •Bolts for flanges or filters breaking due to fatigue caused by over-tightening over a period of time. In some cases, securing bolts were also found loose or missing altogether; •Fatigue fracture of pipes. Such pipes are typically not well supported along their entire length, which causes excessive stress caused by vibrations. Lack of support may be attributed to the design or failure to reinstall the holding brackets after maintenance; •Fuel oil filter covers coming loose and displacement of the spindle from the top cover for various reasons; and, •Rupture of rubberized hoses due to degradation caused by the heat generated from nearby machinery. As noted above, oil coming in contact with hot surfaces is a problem. Shielding can either be by insulating hot spots with thermal insulation or anti-splashing tapes and/or by using physical barriers such as spray shields. Some typical issues with insulation which we have seen in our claims portfolio are: •the quality may differ from yard to yard;

•it can deteriorate with age; •it may not have been fixed back properly after maintenance; and •it can become soaked with oil in time due to minor leakages.

As for physical barriers they may not have been part of the original design and therefore not fitted, or where fitted, they may not have been installed back in place after maintenance has been carried out on the oil system.

Another key point is to be aware that older vessels need more attention. One of the factors which must be considered when assessing fire risks in engine rooms is the age of vessels. The risk of leakages from machinery may increase as ships grow older. Some of the main issues that can increase the risk of fire in the engine room on older vessels are as follows: •Protection of hot surfaces may degrade, with the quality of insulation deteriorating thereby increasing the probability of ignition and risk of fires; •Older vessels can face cuts to their maintenance and safety budgets as they near the end of their service life; and, •A vessel may have changed ownership and management a number of times during its life, and this can have a direct impact on the consistency of maintenance in the engine room. It is also useful to be aware of typical hotspots in the engine room. Based on previous fire incidents handled by Gard, we have found that the below listed areas acted as a source of ignition in most cases. The temperature of these areas can easily exceed 500°c which may be well above the oil’s auto ignition temperature: •Exhaust manifold, pipes and associated flanges; •Exposed areas of boilers; •Turbochargers; •Indicator valves on cylinders; •Heater for purifier units; and, •Electrical wires/components and switchboards. Melting or smouldering of cables can also contribute to the transmission of heat.

KEY RECOMMENDATIONS

There are three core ways to prevent such fire losses. First, identify sources of leakages. Check fuel and lube oil pipes for loose fittings, missing bolts on flanges, non-metallic hoses in areas where the temperatures can exceed the oil’s ignition point etc., from where oil can spray onto hot surfaces. This should be done regularly and ideally should be part of the vessel’s planned maintenance system.

Second, map hot surfaces using thermography. Owners/ managers can incorporate the use of thermography onboard for detection of hot surfaces and for checking insulation during normal operations. They should consider including thermographic examinations in new-building specifications.

Third, use shielding in hotspots. Owners and crew should carry out regular checks of the insulation since it may degrade over time or become oil soaked. As for spray shields, owners can consider their use in areas identified as a potential ‘source of oil leakage’.

Mind the gap

Anders Johannessen, Head of Special Risks, Lockton Marine, argues that the insurance market must work much harder to find solutions for insurance buyers rather than simply adding exclusions for challenging emerging risks

Global events since 2020 have underlined the need for more comprehensive insurance products. Between the pandemic, war, political tensions, cyber threats and increasing detention risks, every commercial insurance buyer in the world has been kept up at night by one or more of these developments.

This should be driving demand for products that specifically address these risks. In reality, however, it seems that more buyers are now uninsured against more risks by virtue of recent market exclusions. This has to change.

As insurance professionals, we make a living out of risk. It is risk that drives demand for our products and services, and it is risk that must inform our product development - not the other way around.

I believe there is a clear tendency to get the order of these two factors wrong. The resulting effect is that clients remain well insured for risks for which they have a reasonable measure of control and may find themselves wholly uninsured or significantly exposed for risks for which they have zero control.

EASILY OVERLOOKED

Lockton Marine’s special risks team has always been focused on the marine risks that are easily overlooked.

For example, demand for trade disruption, loss of hire and anticipated increased cost of replacement (AICOR) coverages is likely to rise in the coming years as a result of clients seeking non-property damage P&L protection against risks outside their direct control.

Marine special risks purchases are generally triggered by unconventional projects, unacceptable contract conditions,

Anders Johannessen Lockton Marine

non-standard jurisdictions, a political or financial crisis impacting the industry or sub-sector, or the realisation that one charter contract may represent an unacceptably high part of a balance sheet.

Purchasers of marine special risks generally have a welldeveloped risk management strategy and a good comprehension of what the insurance markets can do.

They understand how the insurance industry overlaps and intersects with the financial industry, thus providing two arenas for risk management in addition to what is so often the unintended consequence of passive risk acceptance: self-insurance.

Self-insurance should be an active decision taken after all its implications – and potential mitigations - have been understood.

Other teams across Lockton Marine are advising clients in this same urgent capacity. Our team in Istanbul (Lockton Omni) is clear that their role must go well beyond putting the insurance contract in place and facilitating the claims process. There could be emergent gaps in coverage to be addressed potentially within a single policy.

Freight indices, for example, are key datapoints which impact the value of a vessel. We monitor them closely, as well as the sales and purchase market, to assure comprehensive contractual terms at renewal which deliver the appropriate value increases throughout the policy. The Container Freight index has attracted a lot of attention in the last couple of years, showing the volatility of rates to which insurance arrangements must respond.

CUSTOM SOLUTIONS

We are constantly looking to create custom solutions for newly emergent risk sectors as markets develop. For example, Lockton PL Ferrari has been working to support new boutique start-up entrants into the cruise sector.

While the team works across all sizes of operation, one trend that we continue to see on cruise is that bigger may not be better.

Some of the major brands have tapered off their orders for the largest vessels and we have seen multiple new entrants into the market at the boutique level.

With these new entrants comes new exposures and the need for bespoke insurance solutions.

These can range from custom surety solutions to specifically designed pre-vessel delivery balance sheet protection policies.

The smaller operators have their own unique challenges and we work to understand their risk appetite and address their risk transfer needs.

Smaller operators with only one or even a handful of vessels, have a different balance sheet exposure to cruise lines with larger fleets and various brands. We have worked to create tailored solutions with specialist markets.

These respond not only to the loss of revenue exposure found in a traditional loss of hire policy, but also have the ability to respond in the event an incident does not result in damage to the vessel but ultimately impacts the operator’s revenues.

Furthermore, a malicious cyber-attack is a common exclusion in almost all hull and machinery (H&M) policies and most vessel owners are either not aware of the gap in coverage or are uneducated about the potential solutions available to them.

We work closely with Lockton’s cyber division to quantify the risk and to scour the market for the bespoke, sector and sub-sector specific solutions that our clients need.

Coverage gaps (by exclusion or by omission, across insurance programmes or emergent within particular policies, risks actively retained or more passively accepted) are increasing - challenging the marine insurance sector to do more and do better for our clients.

In a world where coverage of even the simplest of risks can be rendered complex by the destabilization of our global systems, we must continually develop our expertise and ambition. Commoditized products with no specialist flex should be increasingly unappealing to both clients and markets.