14 minute read

Singapore: Yes to wholesale skeptical on retail digital fiat money

EVENT COVERAGE: SFF 2021 Singapore: Yes to wholesale, skeptical on retail digital fiat money

SG’s regulator remains iffy on cryptocurrencies—or in MD Menon’s words, crypto tokens.

MAS is taking a more cautious approach to retail CBDCs (Photo: Ravi Menon, MAS Managing Director, Singapore Fintech Festival 2021)

Whilst the Monetary Authority of Singapore (MAS) sees “much promise” in wholesale central bank digital currencies (CBDCs), they are a lot more hesitant in the retail version due to possible “significant risks to monetary and financial stability.”

Retail CBDCs refer to digital currency issued by the central bank to the general public, essentially a digital version of cash. Meanwhile, wholesale CBDCs are restricted for use within the banking system.

Of the two, Singapore’s regulator seems keener to explore wholesale CBDCs, with MAS Managing Director Ravi Menon noting their potential to radically transform cross-border payments.

MAS is taking a more cautious approach to retail CBDCs. “There could be some disintermediation of the banks, particularly during stress periods if people can switch deposits into risk-free central bank money at the “click of a button,” Menon said in a speech delivered during the Singapore Fintech Festival 2021 held on 9 November 2021.

He warned that if people held a significant portion of their deposits in the form of digital Singapore dollars with MAS, it would considerably reduce our banks’ capacity to make loans.

“On balance, the case for a retail CBDC in Singapore is not urgent,” Menon argued.

“For a subject that has attracted much attention, there are neither strong reasons for nor against a retail CBDC in Singapore. Why do I say that? Physical cash is likely to be with us for quite some time more and so the need for a digital version of cash is moot at this point,” Menon explained.

He added that the financial inclusion benefits of a digital Singapore dollar are not compelling. “A high proportion of Singaporeans have bank accounts and electronic payments in Singapore are pervasive, highly efficient, and competitive.”

Possible currency substitution by foreign digital currencies is a remote tail risk at this point, Menon said.

Menon and MAS consider the issuance of a retail CBDC a socioeconomic rather than monetary consideration.

“Moving to a fully cashless society with all money in the form of bank deposits will not make a significant difference to the conduct of monetary policy. The question is whether the public is comfortable with holding only bank deposits and whether there is public demand for a state-issued currency that is as safe as cash but in digital form. So for now, there is no strong case for a retail CBDC,” he said.

Project Orchid

Despite citing caution in regards to retail CBDCs, Menon said that MAS recognises the possible benefits retail CBDC solutions could bring to the financial sector.

Singapore’s regulator then announced it is embarking on Project Orchid, which aims to build the technology infrastructure and technical competencies necessary to issue a digital Singapore dollar, should Singapore decide to do so in the future.

As a start, Menon said that MAS will build on its Global CBDC Challenge that launched earlier this year, from which they received 300 proposals from over 50 countries in response to the problem statements we posed.

‘Cryptocurrencies are not money’

“Are cryptocurrencies money? So far, the answer must be no,” Menon told the conference attendees, who tuned in either live and live stream format. “Cryptocurrencies have performed poorly as a medium of exchange, a store of value, or a unit of account.”

Menon said that it is more accurate to refer to them as ‘crypto tokens’.

Whilst MAS recognises that crypto can bring many potential

For a subject that has attracted much attention, there are neither strong reasons for nor against a retail CBDC in Singapore

benefits, including making crossborder payments faster, the regulator frowns at using cryptocurrencies or tokens as an investment asset for retail investors.

“The prices of crypto tokens are not anchored on any economic fundamentals and are subject to sharp speculative swings. Investors in these tokens are at risk of suffering significant losses,” Menon said.

Wholesale banks stuck in Web 1.5

The latest iteration of SFF carried the theme of Web 3.0, and the topic was very much at the heart of discussions that took place in the three-day festival.

For wholesale banks, the future of payments is going to be 24/7; is going to be invisible to consumers; and is going to happen at virtually zero cost.

But before achieving the financial nirvana promised by the adoption of blockchain systems, artificial intelligence, machine learning, and the whole Web 3.0 lineup, many banks and institutions are hindered with the need to wait for the rest of the business world to finish making their baby steps in digitising their services.

“I would say 80% of our wholesale clients, the global multinational firms, are still somewhere around Web 1.5,” observed Takis Georgakopoulos, head of wholesale payments, JPMorgan Chase, speaking about how Web 3.0 will change the wholesale banking industry.

This is a reality that really dawned for JP Morgan & Chase once COVID-19 set in. “They entered COVID with not very robust supply chains,” Georgakopolos told attendees of a panel discussion livestreamed on 8 November. “They need to solve much more basic issues first, which is, how do I connect to my suppliers? How do I finance my suppliers? How [do] I digitise my payment flows, how I [do I] digitise my treasury function, and so on before they can think about anything else.”

And whilst they do have clients already looking at blockchain solutions, they are in the minority, he added. “A lot of our clients still have a long way to go.”

But the biggest issue is not really on technology, which he noted has reached a level of maturity. Most of the challenges for the wholesale banking industry on adopting Web 3.0 tools have to do with questions on regulation and compliance.

For example, one of the biggest use cases being explored in applying Web 3.0 for wholesale banking is applying it to solve trade finance and supply chains. But a big issue lies in the fact that governments still rely on paper when it comes to trade.

Tan Su Shan, head of institutional banking, DBS said that governments and different legal systems need to be convinced that EBLs or electronic bills of lading are okay, that trade documents can be digitised and put on the blockchain and that by doing so they are immutable, transparent, and trustworthy.

“If you can do that, for trade, that solves a lot of problems. That solves problems around fraud, around potentially long trade finance turnaround time. And I think it’s a great use case for international trade,” she added.

Navigating compliance rules

JP Morgan Chase’s Georgakopoulos also named the different compliance rules per market as another challenge. For example, JP Morgan Chase moves nine and a halftrillion dollars every day in over 100 countries, and they, of course, face having to comply with the rules set by each country.

“The conversations we have with our regulators is, number one, we need more clarity around the rules. And then second, we need more simplicity around the rules. Because the rules as they exist today, they create a huge inefficiency in the system. And the more they’re simplified, the more we can eliminate that inefficiency,” he said.

In five years, both DBS’ Tan and JP Morgan’s Georgakopoulos expect Web 3.0 to make payments easier in the wholesale banking space.

“So five years out, I do believe the blockchain will enable a lot of crossborder payments today,” Tan said, noting that by then payments will no longer be encumbered by holiday breaks or weekends. Blockchain will also help eliminate high friction costs, she added.

Meanwhile, Georgakopoulos believes that government regulations will change little during the next half-decade, if at all.

“So expect a lot of the same controls, especially around wholesale interbank and larger scale payments, to look not too dissimilar to today. They may be blockchainbased, but the governments are going to continue to put all of the controls that they have around them,” he remarked as the panel came to a close.

Are cryptocurrencies money? So far, the answer must be no

Most of the challenges for the wholesale banking industry on adopting Web 3.0 tools have to do with regulation and compliance (Photo: Takis Georgakopoulos, Head of Wholesale Payments, JP Morgan Chase)

EVENT COVERAGE: FSI CONFERENCE Could fintech overtake banks in the digital space with ‘buy now, pay later’?

The Internet boom has pushed 9 out of 10 digital merchants to accept digital payments.

Fintech players are dominating the digital financial service industry but banks still have an ace up their sleeves according to Willy Chang, associate partner at Bain & Company.

Speaking at the panel discussion at the Asian Banking & Finance FSI Conference, Chang explained that Southeast Asia has experienced extremely strong growth in the digital financial service sector however there is still plenty of headroom to go.

As an example, Chang mentioned how overall consumer expenditure on e-wallets grew from 1% to 4%.

“It’s a small number, but the relative growth is huge. And if you look at players like Shopee or Grab, and many other players, that kind of usage growth and value has Panel Discussion during the FSI Conference 2021 been tremendous,” Chang told the conference attendees who tuned in last 1 December 2021.

Fintech’s vast customer reach

Chang said that fintech’s biggest advantage over banks is their reach. Fintech may have millions of customers registered to it or actively engaging with it on a daily basis.

However, Chang noted that fintech does not have or is still starting to build the capability to assess creditworthiness or even have competitive sources of wholesale financing.

“And that’s where banks have a different set of strengths. They may not have 20-30 million customers that they engage with on a daily or monthly basis, but they are more sophisticated in terms of credit scoring, in taking deposits and providing financing,” Chang said.

It’s only a question of how fintech and banks play to each other’s strengths through partnerships, according to Chang.

Digital payments eroding cash’s dominance in SEA

Cash may remain king however digital payments are starting to wear down its dominance as the internet economy in Southeast Asia highlights the popularity of digital services like e-commerce, ride-hailing and food delivery according to Chang. Speaking in a separate panel, Chang emphasised how digital payments are starting to gain momentum on the back of the growth of the internet economy. According to Chang, the internet economy continues to attract new consumers every year with 40 million in 2020 and another 20 million in the first half of 2021. This is not surprising as nine in 10 new users from 2020 continue to be digital consumers today. Given these available data, Alessandro Magarini Montenero, Partner at Bain & Company posits that digital payments are eroding cash’s dominance with growth expected to further accelerate by 2025. Digital payments also see a boost from SEA as e-wallet adoption starts to take pace. According to Montenero, SEA is the home to

Banks may large underbanked and unbanked not have populations, which e-wallets can 20-30 million help leapfrog challenges in obtaining customers that cards and bank accounts. For many, they engage it is their first experience with digital with like payments.

fintech, but they are more BNPL more needed in markets with sophisticated credit under penetration

in terms of Buy now, pay later (BNPL) services banking services are not “urgently” needed in Singapore’s financial and payments sector, according to a senior executive from UOB’s digital banking arm. Speaking in the ABF FSI Conference, UOB’s TMRW Digital Group Chief Commercialisation Officer Jimmy Koh noted that there is no urgent need to roll out BNPL services in such a mature market, as compared to other underbanked markets. “[The] reason we started in Indonesia is that there is a certain unbanked population in Indonesia, there is low credit card penetration, where only like 10% [use a card], whereas Singapore is a fairly mature market,” Koh told attendees of the conference when asked whether UOB

has plans to roll out BNPL services in the Lion City.

“To be honest, do I need buy now, pay later in Singapore? It is not as urgent as those countries in which there is significant credit under penetration,” he added.

The BNPL trend

The digital arm of UOB recently launched a BNPL product in Indonesia, called TMRW Pay.

“In fact, we are the first [to] actually have a buy now pay later product in the market because most of these buy now pay later [products] sits with the technology companies, and then the bank will facilitate in terms of the funding,” Koh said.

“But having said that, we are not doing that in every market yet.”

Instead of launching their own BNPL service in every market, UOB TMRW may instead opt to partner with companies.

“The same company that you [working] with, you could be complementing in one market, you could be collaborating in another market, you could be competing in another market because we don’t have a lot of runway,” Koh noted, adding that banks need to you need to do as much as possible in the BNPL space in the next two to three years in order to really get the most out of the product.

Tech-savvy all-around

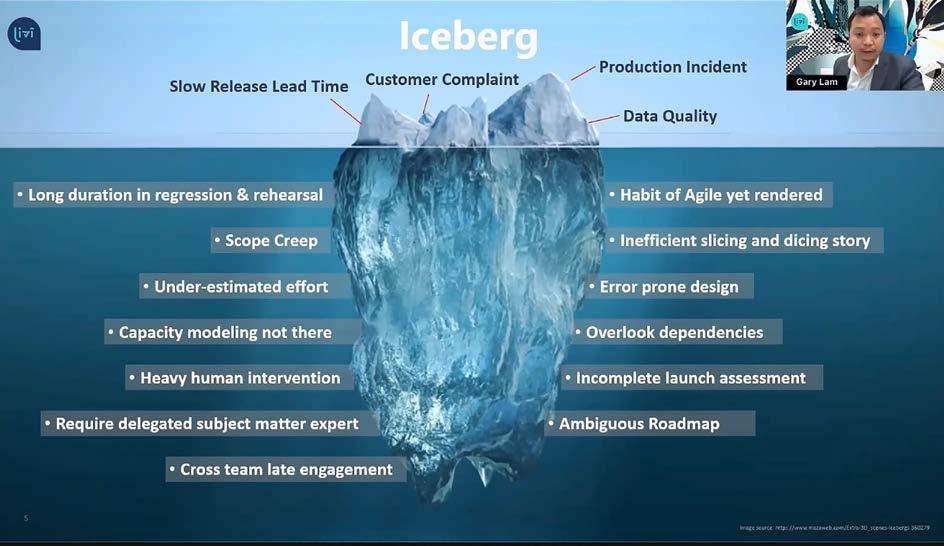

The current digital climate calls for all members of a banking team to become tech-savvy, according to the tech head of one of Hong Kong’s virtual-only banks.

Gary Lam, chief technology officer of Livi Bank, said that banks and financial companies who wish to do digital transformation should also prepare to have all their employees be technologically savvy.

“If you want to do [a] digital transformation of a digital company, I would urge that every single member in your team--not only the technology team--they should be technical savvy. They need to stay on top of the technology trends. What are the major market events? How can the team quickly adapt to the changes in the market? How does the team use new technologies to enable new business opportunities?” he asked.

Lam added that financial institutions need to strike a balance between their technical roadmap and their feature roadmap. “Whether the balance is 50-50 or 70-30 is up to you. It depends on your product characteristics and your market segments.”

The current digital climate calls for all members of a banking team to become tech-savvy

Gary Lam speaking at the FSI Conference 2021

Buy now, pay later (BNPL) services are not “urgently” needed in Singapore’s financial and payments sector, according to a senior executive from UOB’s digital banking arm.

UOB’s TMRW Digital Group Chief Commercialisation Officer Jimmy Koh noted that there is no urgent need to roll out BNPL services in such a mature market.

“[The] reason why we started in Indonesia is because there is a certain unbanked population in Indonesia, there is low credit card penetration, where only like 10% [use a card], whereas Singapore is a fairly mature market,” Koh told attendees of the Asian Banking & Finance FSI Conference held virtually on 1 December, when asked whether UOB will roll out BNPL services in the Lion City.

“To be honest, do I need buy now, pay later in Singapore? It is not as urgent as those countries in which there is significant credit under penetration.”

The digital arm of UOB recently launched a BNPL product in Indonesia, called TMRW Pay.

“In fact, we are the first [to] actually have a buy now pay later product in the market because most of these buy now pay later [products] sits with the technology companies, and then the bank will facilitate in terms of the funding,” Koh said. “But having said that, we are not doing that in every market yet.”

Instead of launching their own BNPL service in every market, UOB TMRW may instead opt to partner with companies.

“The same company that you [working] with, you could be complementing in one market, you could be collaborating in another market, you could be competing in another market because we don’t have a lot of runway,” Koh noted, adding that banks need to you need to do as much as possible in the BNPL space in the next two to three years in order to really get the most out of the product.

Popularity of BNPL services are on the uptick in SEA. According to the FinTech in ASEAN 2021 report, deferred payment services have emerged as a popular digital payment in the region, with one in three consumers indicated that they have used or will use such payment methods.

BNPL services are not “urgently” needed (Source: TMRWbyUOB.com)