2 minute read

Pressure is still on for Indonesia’s ‘big four’ banks

Bank BNI’s capital position could provide adequate cushion against high credit losses

CONSUMER CREDIT

Indonesia’s four biggest financial institutions—PT Bank Negara Indonesia (BNI), PT Bank Rakyat Indonesia (BRI), PT Bank Mandiri, and PT Bank Perusahaan Pengelola Aset (PPA)—are expected to remain under pressure over the next 12 to 18 months due to the ongoing pandemic-related strains, according to S&P Global Ratings.

Bank BNI’s capital position is expected to provide an adequate cushion against high credit losses.

Bank Mandiri’s credit costs, meanwhile, are expected to stay elevated in 2022 as the pandemic weighs on its earnings.

The bank also faces an elevated, although declining, level of nonperforming assets. But its strong capital buffers and good liquidity cushions should meet short-term obligations, S&P said.

Of the four banks, BRI benefits

Compared to its peers, BRI has strong capital buffers to absorb moderate risks from tough macroeconomic conditions

from superior earnings compared to its peers, thanks to its sizeable exposure in the high-yielding microfinance segment. The bank also reportedly has strong capital buffers to absorb moderate risks from tough macroeconomic conditions, according to S&P.

However, BRI’s higher credit costs relative to its peers will exert pressure over the next 12 months as COVID-19 continues to be prevalent in Indonesia.

Bank PPA’s advantage is that it has a high likelihood of receiving government support should it face financial distress, thanks to being a government-related entity.

On the other hand, Indonesia’s outlook souring also affected Bank PPA, especially given its role as a distressed state-owned enterprise (SOE) manager.

“We expect [Bank] PPA to expand its balance sheet and funding sources as part of its transformation into a more diversified financial services firm, whilst maintaining adequate capitalisation over the next 12 to 18 months,” S&P said.

This transformation comes with risks too. PPA could face further strains should its management make significant strategic or execution missteps during PPA’s transformation phase, which in turn could lead to lapses in risk management or unexpected losses.

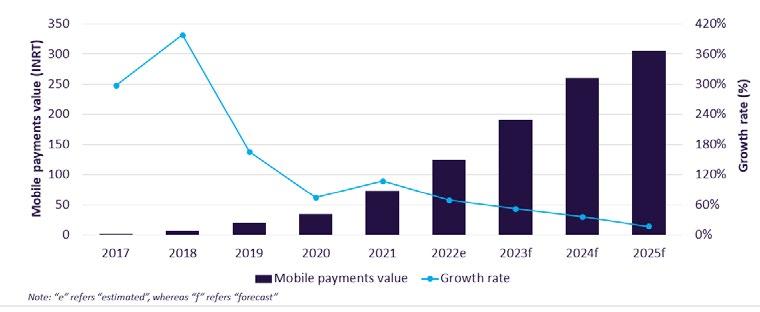

THE CHARTIST: INDIA’S MOBILE WALLET PAYMENTS BECOMING MAINSTREAM

The segment is expected to grow at a compound annual growth rate (CAGR) of 42.7% between 2021 and 2025 and reach US$4.1t (INR305.6t) by the middle of the decade, according to forecasts by data and analytics company GlobalData.

In 2022 alone, payments using mobile wallets are expected to equal a total of US$1.7t in India, a 69.8% growth compared to the previous year.

The availability of high-speed internet facility at low cost, coupled with the rise in smartphone penetration has provided the foundation for mobile payments to thrive in India, according to Sowmya Kulkarni, senior payments analyst at GlobalData.

“Mobile wallets have now become an integral part of Indian consumers payments and are also preferred by merchants of all sizes, from big supermarkets to neighbourhood ‘kirana’ shops,” Kulkarni said. “This growth has been largely driven by state-backed instant payment system UPI, which enables users to make payments directly from their bank accounts using recipients’ mobile number or scanning QR code.”

The significant growth in mobile wallet transactions has seen the proliferation of mobile wallet brands, with each competing to get a pie of this market. Some of the popular brands are PhonePe, Google Pay, and Paytm.

“Mobile wallets market in India is in high growth phase. Government’s push and improving mobile payment acceptance infrastructure will further drive the mobile wallets usage, thereby helping the government’s broader objectives to become a less cash economy,” Kulkarni said.

India: Mobile Payments Value (INRT)