30 minute read

Quezon Power supply deal extension in limbo

CEO INTERVIEW Quezon Power supply deal extension in limbo

The power generator’s power purchase agreement is due to lapse in May 2025.

Coal-fired power plant, Quezon Power, which has been in operation for over two decades, is looking for alternative routes with the looming expiration of its power supply agreement (PSA) with local distributor Manila Electric Co. (Meralco).

In a fireside chat with Asian Power Editor-in-Chief Tim Charlton at the Asian Power Thermal Energy Conference, Quezon Power Managing Director Frank Thiel shared the plant is looking at either selling to retail energy suppliers or operating within the wholesale electricity market.

Quezon Power forms part of the EGCO Group from Thailand, which also owns assets around the globe. In the Philippines, Thiel also manages the first supercritical plant, the San Buenaventura power project, on top of the Quezon Power station.

We don’t know yet what the Philippine government will do after COP26. But for Quezon Power Plant, your power purchase agreement (PPA) with Meralco will expire in a couple of years. Could you walk us through how competitive it’s going to be to get renewed? How long is it for?

The agreement is due to lapse in May of 2025. Ten years ago, 15 years ago, when we’re looking at the future, we’re thinking that we’re going to get an extension to our current PPA because we’re a very reliable power station. We’re cost-competitive. Five years ago, we began to realise that market conditions are changing. Three years ago, we said, the world is going to look vastly different from what we anticipated 10,15 years ago.

What do we want to do with Quezon? Do we want to try and get another PPA or PSA? The answer is yes. We embarked on a program to try and determine what would it take to refurbish our plant, to extend the life of the plant beyond the 25 years of the current power supply agreement. In the Philippines, Meralco has instituted what they call a competitive selection process (CSP).

They will look to contract for a certain amount of megawatts (MW) to be delivered on a certain date and go through a very rigorous process. We saw an opportunity for our project for Quezon Power in this case to try and compete. We’re looking to see if there will be room for us in the future when Meralco starts contracting for additional power for 2026, and beyond; If we’re successful, the outcome of that will be perhaps a 20-year PSA. If we’re not successful, because obviously, the CSP is very competitive, then we have to look for alternatives.

The things that we’re evaluating right now involve, perhaps selling our power to retail energy suppliers. Our plant has one advantage, that is that we were fully amortised. At this point in time, we can be very competitive with our power rates. If that’s the case, we may be able to latch on to shorter-term contracts with retail energy suppliers. The other alternative is to operate within the wholesale electricity market here in the Philippines, and basically become a merchant plant. Although there are a lot of challenges, we’re trying to position ourselves as best as we can. We would have to adjust our strategy, or how we operate the plant, how we maintain the plant, depending on what we’re able to get.

Frank Thiel, Managing Director, Quezon Power

Although there are a lot of challenges, we’re hoping to get either a long-term contract with Meralco or shorter-term contracts with retail energy suppliers and the government. Both of them must also be a little bit concerned about energy security, and about effectively cutting off coal-fired power plants without alternatives in place. Do you think that this will be considered to extend the life so they have that energy security?

Within the moratorium, Energy Secretary Alfonso Cusi indicated that any coal-fired plants that were currently in the stages of development will remain in the pipeline. The biggest fear is whether or not you can get financing for those projects. There are about 3,500MW worth of coal-fired plants in the pipeline. But anything after that, the moratorium prevents new coal plants from coming into the Philippines.

The Department of Energy, in particular Secretary Cusi, has been very clear and very vocal about the fact that coal and thermal power has to remain in the energy mix of the Philippines. We’re currently 52% of the energy mix for the country. Secretary Cusi recognises that we’re not going to be able to transition overnight. We’re not going to be able to get away from thermal power for quite some time. I think he realises that the transition is going to take place, but it’s going to take quite a bit of time. Now, our customer, Meralco, is very interested in the most competitive power prices that they can get because, obviously, they want to pass that on to the consumers. That’s where consumers are looking for reliable, inexpensive power. Meralco has different goals in mind. At the same time, Meralco has a mandate on renewable portfolio standards. They have to source a certain amount of their energy from renewable energy sources. So they’re trying to balance those things out.

PT PP (Persero) Tbk recognised with 2 accolades at the Asian Power Awards

The company continues to gain trust to work on prestigious projects across Indonesia, such as the Gas Engine Power Plant in Bangkanai.

Land clearing started in February 2018. Engine foundation was ready before the first engine arrived at the site in June 2019. Then finally the engine 1 was completely first fired on March, 19th 2020. All engine first firing was completed in November 2020.

GECC Lombok Peaker

Located at the heart of the capital city of West Nusa Tenggara, GECC Lombok Power Plant is the biggest power plant in Lombok Island which can supply 40% of the total Lombok Load at peak time. This power plant uses selected technology which is the largest combined cycle in Indonesia using a gas engine instead of gas turbines and the efficiency is well maintained.

The EPC phase of this project was started in August 2017. Even though the project finished on schedule, it doesn't mean this project goes without a hitch. We encountered some challenges during the construction.

In August 2018, a destructive earthquake struck the island of Lombok. It indeed affected our project works and the plant itself. Besides, the soil condition of the project site is also quite challenging as well as the subsea pipeline works. Then 2 years later, in March 2020, the Corona outbreak was confirmed to have spread to Indonesia. However, this challenging moment did not discourage us to give our best and achieve our goal. The milestone was successfully completed on 24th December 2019 for Simple Cycle-1, followed by completion of Simple Cycle-2 on 27th March 2020 and completion of Performance Test of Combined Cycle on 31st July 2021.

Despite the various challenges, the company maintained safety work in the project. Safety is the priority in all our activities. Overall, Bangkanai and Lombok Power Plant have achieved Best of HSE Implementation for 1.8 & >2 mio. total safe man-hours with Zero LTI (Lost Time Injury). We are optimistic that the completion of Bangkanai Gas Engine Power Plant and Lombok Gas Engine Combined Cycle Power Plant will bring an economic value not only for us or for the Project Owner, but also to the surrounding societies' economy. One of our guiding principles in undertaking our project is persistence. All the challenge is new learning for us and becomes our motivation to provide sufficient electricity in rural areas and its surrounding.

Bangkanai Gas Engine Power Plant

Established in 1953 under the name NV Pembangunan Perumahan, PT PP (Persero) Tbk is entrusted to build houses for the officers of an Indonesian cement company in Gresik. Along with improved performance and growing trust from our customers, the company was able to build large scale projects in Jakarta, Bali, and Yogyakarta.

The EPC Division of PT PP (Persero) Tbk. continues to gain trust to work on prestigious projects across Indonesia, such as in Bangkanai and in Lombok. Up

until now, the company has worked on several types of power plants from coal-fired, simple cycle gas engine, simple cycle gas turbine, and combined cycle to renewable projects such as 72 MW Windfarm in Tolo, 30 MW Geothermal in Kamojang, and 42 MW Solar PV in Lombok & Manado.

Bangkanai Gas Engine Power Plant

Located in Karendan, a village in Lahei District, North Barito Regency, Central Kalimantan where the agricultural sector, palm oil plantations, coal mining, and business trade contribute positively to Central Kalimantan's economic growth. These five sectors grow prospectively supported by adequate natural resources in this world's third-largest island. These sectors consecutively play a significant role in the increasing demand for electricity in Central Kalimantan.

Based on the data presented in the RUPTL 2021-2030, the ratio of the number of households using PLN electricity in Central Kalimantan is still relatively low. Besides, the electrification ratio in Central Kalimantan as of the second quarter of 2021 is the lowest compared to other provinces in Borneo, which is 96.07%, whereas other provinces in Kalimantan have reached 98-99%. So, electricity demand in this area is estimated to be high for the next five years. Therefore, Bangkanai GEPP (Peaker) Stage 2 (140 MW) Project is developed in Central Kalimantan, to provide and enhance electricity supply in this area, especially for the Kalimantan Island.

The power plant uses dual-fuel engine technology

as a main source of electricity. The engine can be operated with natural gas as the main fuel and diesel fuel as backup and pilot fuel.

During the project, the company was facing some obstacles. The major constraint is transportation due to poor access roads. We need extra effort, detailed engineering, meticulous planning and solid team coordination for the execution in shipping the Engine and Generator which was sent from Finland through sea using a mother vessel. Total 16 engines and generators were sent to the Luwe Jetty through the Barito River.

India and Vietnam are projected to increase their wind capacity by 2030

Wind power finds niche in Asian markets, Fitch reports

India and Vietnam are amongst the investment hotspots for the wind power sector, Fitch Solutions reported, as the two Asian markets are poised to see significant growth in their wind capacity in the next decade.

In its Global Wind Power bi-annual report, Fitch Solutions sees India and Brazil as the outperformers in the wind power sector. This comes as the two already large markets are both expected to double their wind power capacity over the coming decade. Vietnam, meanwhile, is the market to watch in the fourth quarter, as the report forecast its capacity growth will increase by over 400% over the coming decade. Fitch said that rapid deployments in both onshore and offshore wind support its outlook, with the latter attracting large scale investments posing further upside risks.

In this case, Fitch Solutions defines ‘outperformers’ as the wind power markets that have a significant capacity base installed, and/or will register substantial growth in capacity over its 10-year forecast period to 2030.

Outperformers

The new climate targets announced at the United Nations’ Climate Change Conference (COP26) summit by Indian Prime Minister Narendra Modi pose an upside risk to the outlook for wind sector growth in the market, Fitch noted. To hit these targets, the market will aim to increase its low carbon power capacity to 500 gigawatts (GW) by 2030 and meet 50% of its total energy requirements with low-carbon energy sources by 2030. The report highlighted that these pledges pose a mounting upside risk to our forecasted 43 GW of wind capacity growth expected between 2021 and 2030.

Despite this growth being the thirdlargest globally and sizable upside risks over the long term, India’s wind power sector is projected to face near-term challenges and underperform relative to government targets for 2022. Notably, India’s wind power sector is forecast to add only 8.2GW of wind power capacity between year-end 2020 and 2022, with wind power capacity set to reach 47GW by 2022–well below the 60GW government target.

The combination of several challenges in the country’s wind power sector will hit near-term growth momentum, including land availability hurdles, grid access bottlenecks, and concerns over the viability of low tender bids. In this light, Fitch’s cautious outlook relative to the government target is informed by the challenges the country is facing in tendering and delivering the necessary capacity to meet ambitious expansion plans.

Delays to the implementation of tendered projects and more muted interest in new auctions, Fitch noted, will present a substantial hurdle to fulfilling these envisioned expansion plans.

Meanwhile, Brazil is a global wind outperformer with 23.7GW of wind power capacity additions expected to begin operations between 2021 and 2030–doubling the market’s installed wind capacity.

Fitch forecasts growth in the segment of 17.1% in 2021 to take capacity to 20.4GW, followed by average annual growth of 8.2% from 2022 onwards to reach a total capacity of 41.1GW in 2030. By the end of the forecast period, wind power is seen to account for 18% of Brazil’s total power generation mix.

The upward revision on the previous forecasts reflects an increasingly strong project pipeline, particularly in the medium term with around 14.5GW due to come online between 2021 and 2025. The sizable pipeline is the result of both private power purchase agreement deals as well as large renewables auctions which have resumed following their suspension in 2020 amidst early impacts from the pandemic.

The Brazilian government awarded 873MW in non-hydropower renewables capacity through the country’s A-3 and A-4 power auctions that concluded in July 2021, including 419.5MW of wind power, Fitch Solutions noted. The projects selected in the A-3 auction are scheduled to begin operations by 1 January 2024 whilst projects from the A-4 auction are set to begin operations by 1 January 2025.

Market to watch

Fitch Solutions expects Vietnam’s wind power capacity to increase from under 3GW in 2021 to just under 13GW by 2030.

This growth is supported by project momentum across 2021, despite initial expectations for supply chain disruptions. State-owned entity Vietnam Electricity (EVN) reported that there are over 106 wind projects with a total combined capacity of over 5.6GW that have registered to begin commercial operations before 1 November 2021. Fitch Solutions noted that this is as the feed-in tariffs for wind projects expired after this date, and as such developers rushed to complete the projects to attain more favourable power purchase rates.

In addition, Vietnam is looking to establish a new goal of developing 3GW to 5GW of offshore wind power by 2030 and 21GW of offshore wind by 2045. This will be supported by an offshore wind power purchase mechanism to stimulate the market and there are major projects that are in development.

India and Vietnam amongst wind power markets that will register substantial growth in capacity over a 10-year forecast period to 2030

Huadian Fuxin Guangzhou Energy Co., Ltd recognised with Gas Power Project of the Year - China at Asian Power Awards

It manages China’s first SGT 8000H Gas Turbine Power Plant in commercial operation

Huadian Fuxin Guangzhou Energy Co., Ltd

To pursue the policies of promoting clean energy utilisation, accelerating decarbonisation, improving gas power projects and advancing central heating, the first H-class gas turbines project in China with total installed capacity of 1340MW had been put into commercial operation successfully on 30 September 2020 by Huadian Fuxin Guangzhou Energy Co., Ltd. (Huadian Fuxin). The launch marks the largest Combined cooling, Heating and Power (CCHP) project in China.

As the pioneer of H-class gas turbine power plants in China, the project is equipped with Siemens Energy state-of-the-art SGT5-8000H gas turbines, SST5-5000 steam turbines, SGen52000H generators and SGen5-100A generators. The plant’s efficiency of pure condensing mode exceeds 62%, and its efficiency of energy utilisation surpasses 76%, contributing around 4.4 billion kWh of electricity per year. Its high-pressure main steam parameter reaches 16.7Mpa (a) / 600 ℃ / 610 ℃, the highest one of the combined cycle units in China ever. In addition, the waste heat boiler is equipped with SCR denitration devices which makes the average NOx emission less than 10mg / Nm3. Each year, it contributes to the reduction of smoke and dust emission by 1437 tons, CO2 emission by 2.4 million tons and SO2 emission by 2230 tons, equivalent to planting 5 million trees. Moreover, the gas and steam turbines of the project are arranged in a combined main building at a medium position with separate shafts, which represents the first of its kind worldwide. Thanks to the excellent design and high management standards, the land use index of the power plant is only 0.073sqm/KW, 10% less than that of similar projects, and the unit kilowatt cost of the project is lower than 2000 RMB /KW, reaching the advanced level nationwide.

The unit also applied Siemens Energy SPPA-T3000 control systems, ensuring the maximum reliability, the highest efficiency, and the largest flexibility of the power plant’s control system. Furthermore, the power plant developed a set of digital platforms, such as APS (Automatic Plant Start-up and Shut down System), trends early warning systems, performance monitoring and analysis systems, robot inspection etc., which make the power plant stand for the highest intelligence level in China.

In late 2020, China’s government announced its commitment by reaching carbon peak in 2030 and carbon neutrality in 2060, which will bring a profound change in production and lifestyle, and will reshape the pattern of China’s energy and power industry. Clean energy production and electrification will become an inevitable trend. Huadian Fuxin’s project, located in Zengcheng District, Guangzhou City, Guangdong Province, is playing a key contributory role in support of the development of the Guangdong-Hong Kong-Macau Greater Bay Area with a supply of clean energy.

Ultra-low-cost renewables have been extremely disruptive for the Indian power market (Photo by Simone D. McCourtie)

India readies for cross-state electricity trading

This could pave way for cheaper power, but hurdles surrounding profitability remain.

The Government of India’s plan to commission 450 gigawatts (GW) of renewable energy capacity by 2030 has set the country’s power market on a transitionary path. Ultra-low-cost renewables have already been extremely disruptive for the Indian power market.

Whilst the expensive and emissionintensive coal-fired power generation assets have been affected most by the disruption, some has also trickled down to India’s power distribution sector, wrote Institute for Energy Economics and Financial Analysis (IEEFA) Analyst Kashish Shah.

India’s state-owned power distribution companies (discoms) are now confronted with the challenge of adhering to contractual obligations of legacy coalfired power purchase agreements (PPAs) whilst there is an availability of solar and wind power in the market at 40% to 50% cheaper tariffs than that of coal-fired power.

The response to this challenge by the discoms has been regressive to a large extent, IEEFA believed. Discoms have cancelled auctions that resulted in already low-cost renewables striking deals at even lower prices.

In some cases, PPAs have been cancelled or forced to be negotiated to bring tariffs lower than the signed PPAs. This has significantly derailed India’s near-term target of 175GW of renewable energy capacity by the financial year 2021-2022; the renewables capacity stood at about 100GW as of July 2021.

The Ministry of Power’s recent proposal of a market-based economic dispatch (MBED) mechanism for procuring bulk power to begin in April 2022 aims to optimise the country’s power generation resources. By moving away from just state-level pooling of resources and dispatching power through a central clearing mechanism, MBED aims to reduce power procurement costs by Rs12,000 crore (US$1.6b) annually.

A recent study from the Council for Energy Environment and Water found that the newer coal-fired power plants, commissioned between five and 10 years ago, had lower plant load factors in the 30 months leading up to the COVID-19 pandemic in India, despite having lower variable costs than some of the 20- to 35-year-old coal-fired power plants.

Similarly, plants younger than five years old operated at plant load that was 20% lower, despite having a lower variable cost than some of the oldest plants. The uncontracted capacity is, either, typically treated as merchant power and sold on the exchange or through other open market mechanisms.

The open market transactions contribute about 10% of the total procurement of electricity in the country.

Discoms need to pay fixed charges to thermal plants for the capacity contracted, regardless of the amount of power drawn from the plant. The variable charges are only paid for the quantity of power drawn from the plant. Once the discoms have committed the sunk cost of the fixed charges, then it is about choosing the lowest variable cost for drawing power. So even renewable energy sources with zerofixed charges but slightly higher variable charges would be more expensive than contracted coal-fired plants.

India’s power system

Discoms in India currently schedule generation on a day-ahead basis from amongst their portfolio of contracted generators. Self-scheduling has proven to be a suboptimal outcome for the power system in the country, with relatively higher costs being borne by ratepayers and, eventually, consumers. In some instances, it is also noted that the states have violated their own merit dispatch orders.

Self-scheduling restricts the discoms to share the generation resources across the country. This also leads to technical constraints on the amount of variable renewable energy (VRE) that a state can deploy within its boundaries. Centralised market-based scheduling and dispatch will ensure enlarging of the balancing area from the state boundaries to regional or national boundaries, bringing the desired flexibility for reliably deploying much higher levels of VRE.

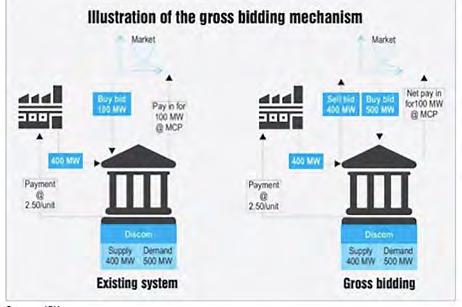

As the market becomes more competitive, cheaper plants will get dispatched first, raising the stranded asset risk on expensive thermal power plants. The Indian Energy Exchange (IEX) has suggested an alternative mechanism of gross bidding to overcome the regulatory and structural changes required to implement the MBED model.

IEEFA referenced the example provided by IEX to explain the gross bidding mechanism: Assume that a discom has a demand of 500 megawatts (MW), has entered into a PPA with a generator, and contracted a capacity of 400MW at energy charges of Rs2.50 per kilowatt-hour

India’s stateowned power discoms are confronted with the challenge of adhering to contractual obligations of legacy coal-fired PPAs

Gross Bidding Mechanism

Source: IEX

(kWh).

As per the existing practice, the discom will self-schedule 400MW of capacity under the PPA and will look to buy the additional 100MW capacity from the open market. In the proposed gross bidding mechanism, the discom will place sell bids of 400MW at Rs2.50/kWh in the market and buy bids of 500MW.

The discom would ideally choose to buy the 400MW at a price equal to or lower than its contracted tariff of Rs2.50/ kWh and the remaining 100MW at the best price available in the open market. Similar to the MBED practice, the settlement of capacity charges for thermal generators will happen on a bilateral basis between the discoms and the generators.

Depending on the demand and supply scenario, the sell bids of 400MW will get cleared and the generator will be despatched.

Consider a scenario where the MCP in the spot market is Rs3/kWh and the PPA tariff from the discom’s contracted generator is Rs2.5/kWh: Since the PPA price is lower for the contracted 400MW capacity, the discom will choose the contracted capacity at a tariff of Rs2.5/kWh. The discom will incur a procurement cost of Rs24m per day for buying power at Rs2.5/kWh and Rs7.2m per day for buying 100MW of capacity from the spot market.

In the gross-bidding scenario, the discom’s sell bid of 400MW will get cleared as it would be offered at a lower tariff of Rs2.5/kWh. On paper, the discom will sell this power to the open market and pay Rs24m per day to the generator while buying the additional 100MW from the spot market at a tariff of Rs3.0/kWh, incurring a cost of Rs7.2m per day.

Under either mechanism, the discom’s total power procurement cost turns out to be Rs31.2m per day. Hence, discoms neither gain nor lose in the scenario where MCP is higher than the PPA. The below table compares discoms’ gain and loss between the two mechanisms for different scenarios for tariffs from the open market and the PPA.

To get the discoms and the generators up to speed on this new mechanism, India’s Central Electricity Regulatory Commission has planned for a phased implementation. India’s largest stateowned power generation company, NTPC, will begin operating through the MBED route with its thermal generation fleet on 1 April 2022.

A similar pilot entailing securityconstrained economic despatch (SCED) of interstate thermal generation capacity was performed between April 2019 and January 2021. The pilot registered savings of Rs1,624 crore (US$210m) of generation costs.

Battery development in India power plants

The Frequency Control and Ancillary Services (FCAS) Regulations to Drive Up Battery Deployments There are currently two utility-scale batteries operating in India. A 10MW/10MWh (megawatthour) battery is operated by Tata Power’s power distribution business in Delhi. An 8MWh battery is reportedly being commissioned by L&T and owned by the Niyveli Lignite Corporation of India Ltd in the Andaman & Nicobar Island, colocated with a 20MW solar plant.

Recently, the Solar Energy Corporation of India rolled out a tender to procure 2,000MWh of a stand-alone energy storage system. Similarly, NTPC has issued a similar tender to procure 1,000MWh of capacity. Other battery projects are being developed by Renew Power, supported by long-term, timeof-day differentiated tariffs with 25-year PPAs. There also are more than 4GW of operational pumped hydro storage (PHS) projects with roughly 3GW under

Kashish Shah

construction.

The tariffs for the operational PHS projects exceed Rs7/kWh and are typically operated by the states to meet peak demand. Batteries and PHS projects could be supported by long-term price signalling and would predominantly operate to shave peak-demand loads. The profitability of these battery assets is reliant on price arbitrage—charging during the time of low-price periods and dispatch during the high-price, peak demand periods.

The presence of a formal FCAS market puts value and merit to accuracy and speed of response to grid management requirements, further improving grid reliability. It would eliminate the grid operator’s cheapest avenue of managing the grid in adverse grid events—load shedding. The development of a formal FCAS market will open up another substantial revenue stream for utilityscale batteries and allow them to operate as an important grid management asset.

Coal Power Plants Age, PLFs, Variable Costs

Source: CEEW

Based on the demand and supply situation in the spot market, three different scenarios may emerge: Market clearing price (MCP) < energy charge: In this scenario, sell bids will be rejected, since power will be available at a cheaper price at the exchange. Discoms will buy the entire 500MW from the market at a price lower than the contracted energy charges. As the sell bid will not get cleared and the generator will not get despatched, the discom will not pay any energy charges to the generator. Discoms will gain in this scenario by procuring power at a cheaper price. MCP = energy charge: In this scenario, both buy and sell bids will get cleared. The discom will buy from the market at the same price as energy charges and pass it on to the generator under the PPA. The discom will not have any loss or gain. MCP > energy charge: In this scenario, both buy and sell bids will get cleared. However, the pay-in and pay-out of the discom will get exactly netted out with no additional obligation for the discom.

COUNTRY REPORT: PHILIPPINES The Philippines is poised to lead Southeast Asia in sustainability

It could 'leapfrog' to be a regional leader with renewables projected to be worth $30b by 2030.

Southeast Asia could find a new leader in the Philippines in sustainability, should it reap its renewables’ potential projected to grow into a $30b market by 2030, Bain & Co. reported.

Bain & Co’s Perspective on the Green Economy report, conducted with Microsoft and Temasek, noted that of this projected renewable market, around 35% will be solar power. This could pave the way for investors to build infrastructures, such as electric grids and photovoltaic (PV) recycling plants.

The Philippines could also rise as a wind energy powerhouse with a 160-gigawatt (GW) wind energy potential in offshore areas within 200 km of its shores, making it one of only eight emerging markets across the globe. On top of this, it is also an ideal destination as global wind technologies can easily be adapted in the Philippines, considering it has no technological transfer limitations.

The Philippine government has yet to join Southeast Asian countries, like Indonesia and Laos, that have committed to net-zero. Despite this, the Philippines has set a 2030 target to reduce its carbon emissions by 75%. It has also planned to raise the total installed renewable capacity to 38% by 2035.

Further, into its clean energy plans, the government declared in November 2020 a moratorium on new coal-fired power plant projects. This is followed by reports that the Philippines spent approximately $64b (P318b) in green projects, whilst its central bank invested some $550m in sustainable bonds.

Phasing out coal

Currently, the Philippines is pushing to reduce emissions by phasing out coal and attracting green financing, Bain and Co’s report read in part. It added that in line with the government’s commitment, private firms have also taken part by being signatories to Science Based Targets Initiatives or setting their own net-zero or carbon-neutrality targets.

The moratorium will result in the suspension of about 8 GWs of prepermitted coal projects, the majority of which are expected to come online by 2026, according to Fitch Solutions, citing government sources.

Meanwhile, the coal projects that have been able to comply with environmental requirements will still be allowed to proceed. Nearly 20-GW coal-fired capacity were in pre-completion stages as of end-2020, which is around 39% of the total capacity in the pipeline.

Also emphasising that coal is still the cheaper and more reliable option to meet the Philippines’ demand surge, Fitch predicts that coal will still dominate the energy mix in the country, reaching 59% by 2029.

“We now forecast coal-fired power generation to increase by an annual average of 5.2% between 2020 and 2029, amounting to approximately 93.6terawatthour by 2029,” it said. Fitch, however, said that its forecasts are subjected to “significant downside risks” as coal projects are being opposed by the public. It also noted that key utilities in the country, such as AC Energy and Meralco, have intended to shift from coal.

By 2033, based on Rystad Energy Research, coal capacity in the Philippines is expected to have reached its peak and will be set to decline. Coal’s share in the country’s power capacity mix will likely drop to approximately 35% by 2030 and further down to 13% by 2050.

“The decline in baseload coal generation will need significant

The Philippines has set a 2030 target to reduce carbon emissions by 75% and raise total installed renewable capacity to 38% by 2035

Addressing rural electrification issues will be critical to create opportunities for distributed power generation

Coal moratorium has been widely lauded by anti-coal groups and climate change advocates

compensating capacity from solar and wind sources,” Rystad Energy Senior Analyst Harshid Shridhar said.

Shridhar backed the report’s findings that the Philippines could lead the region with the appropriate financing and technology transfer terms as it set “ambitious” targets in PV module recycling and wind turbine recycling. He added that the emphasis on green energy sources could benefit businesses, as well as manufacturing entities through incentives, such as the imposition of a reduced carbon tax.

According to a separate report by the Economic Research Institute for ASEAN and East Asia, coal generation could peak at 56% by 2030 despite the moratorium, due to power plan project developments that have already been approved.

“Whilst the coal moratorium has been widely lauded by anti-coal groups and climate change advocates, its effects will not be instantaneously felt,” Asia Clean Energy Partners Research Associate Ralph Justice Apita claimed.

“But with increasing public pressure, continued downward trend in the cost of renewable energy technologies, likely ADB financing for coal power plant retirements, and full foreign ownership of geothermal exploration in the Philippines, continued construction of even the greenlit plants will come under pressure, and the share of coal generation in the country’s power mix will decline.”

Attaining ambitious targets

“For the country to achieve its ambitious sustainability targets, they will need to start with effective government leadership in establishing a research body like the Philippine Energy Research and Policy Institute, and soliciting groundlevel opinions from think tanks, to complement existing and upcoming policies with a scientific and evidencebased approach for a well-thought-out public policy,” Apita said. He added the government should follow through with stricter implementation and constant monitoring. New administrations should also opt to recommit to these programmes to ensure continuity, instead of focusing on “less effective populist programmes.”

Moreover, the Philippines could also invest more in its grid capabilities as well as address challenges in giving far-flung areas access to electricity, as recommended by Black & Veatch’s executive vice president and managing director, Asia Power Business, Narsingh Chaudhary, and associate vice president for management consulting business in Asia, Harry Harji.

The Philippines will require increased grid flexibility and management capabilities to respond to sudden fluctuations in supply caused by changes in weather and time of day.

One way to approach this is by developing distributed energy resources (DER), such as solar and battery energy storage systems, Chaudhary and Harji said. These could also include wind, microgrids, combined heat and power systems, backup generators, as well as technologies that enhance demand response offerings.

“These solutions are often installed behind the meter and funded by utilities, capital markets, or customers themselves,” Chaudhary and Harji said.

Rural electrification

Addressing rural electrification issues, which is prominent in the Philippines as an archipelagic state, will also be critical as this will create opportunities for distributed power generation. For instance, microgrids can provide the power reliability that remote locations need whilst ensuring the facilities are commercially viable.

In addition, Black & Veatch said renewable energy can be paired with energy storage to enhance grid resilience. It can also be integrated into grid balancing solutions to balance generation variability whilst meeting decarbonisation targets. DER can also boost energy resilience by functioning as independent nodes to support interconnected power and grid solutions distributed across traditional networks.

“Whilst nations, like the Philippines, build their sustainable energy portfolios, they will also need to review their opportunities to transition away from coal,” Chaudhary and Harji said.

Black & Veatch noted coal plant owners may also consider the long-term economic viability of their facilities which have several alternatives, such as a full or partial fuel conversion to fuel sources like natural gas, biomass or hydrogen, retrofitting emissions control equipment or adopting carbon capture, use and storage solutions, and decommissioning aged coal assets for repurposing or repowering.