45 minute read

Three reasons why agrivoltaics could be key renewables sector in

REPORT: AGRIVOLTAICS Three reasons why agrivoltaics could be key renewables sector in India

Geography is a major factor why the country is best to adopt agrivoltaics, IEEFA says.

India has set its target locked on increasing the capacity of renewables to 500-gigawatts by 2050. And one sector that it could tap in its energy transition is agrivolatics or the installation of solar panels in lands used for agriculture, the the Institute for Energy Economics and Financial Analysis (IEEFA) claimed.

To back this up, IEEFA gave three reasons. The most obvious reason would be the country’s geography—the majority of India’s land area is used for farming. Second reason is that this renewable sector will address the expected increase in India’s energy demand growth and, finally, provide socio-economic opportunities, especially for the rural sector.

However, there is a need for implementation of policies that would encourage adoption of agrivoltaics such as allowing non-farming commercial activities in most states, providing incentives, and funding programmes.

Globally, agrivoltaics installed capacity has grown from about 5 megawatts (MW) in 2012 to approximately 2.9GW today, led mostly by Germany, France, and Italy, whose COVID-19 pandemic recovery plan devotes over €1b to establishing 2GW of agrivoltaic projects, said IEEFA Contributor Charles Worringham, citing recent reports.

There has also been an increasing number of research and empirical experience, as seen in the 2021 Agrivoltaics Conference. It is just in its second year but it has already attracted 84 abstracts and delegates from 39 countries.

In India, a joint German-Indian report has listed 16 existing installations, and has also developed a publicly accessible online map of these projects. An additional 7MW solar power project for Gro Solar Energy in Maharashtra with low-height crops between modules has been announced, and others are in various stages of development.

Even at a very early stage and composed mostly of small-scale research and demonstration projects, agrivoltaics remain relevant to India for three reasons according to IEEFA: scale and scope of electricity system growth, geographic, and socioeconomic opportunities for the rural sector.

India is expected to see significant energy demand growth over the coming decades, along with the intensifying calls to accelerate clean energy transition.

The country will see a far more extensive power infrastructure growth of all types and strong incentives to build a geographically diverse and robust network, at speed. This will favour generation types that can be built quickly and at a range of scales, which could favour growth of agrivoltaics.

For the second reason, 60% of India’s land area is farmed, higher than the world average of 39%, according to World Bank data. Whilst areas such as Rajasthan offer especially high levels of generation potential, large tracts of the country are capable of producing solar power in higher quantities and more reliably than almost any European country with the exception of Spain and Portugal.

This also presents socio-economic opportunities to the country’s rural sector. Indian cities are seeing additional growth stress due to large-scale seasonal migration of millions of rural citizens who seek work in cities for that period. As India faces declining farm size, with over 70% of rural households owning less than one hectare of land based on government data and unreliable weather, variable access to market and price instability any innovations that could strengthen the rural economy, stabilise agricultural employment and grow non-agriculture work could contribute to relieving the pressures of rapid growth on India’s cities.

Tech development

Indian conditions may favour particular types of agrivoltaic technology. A variation of special interest to India is the use of bifacial panels arrayed in widely spaced rows, which in addition to the different generation properties explained below, reduces dust accumulation, an important aspect of maintenance, especially in more arid regions.

Vertical bifacial panel arrays, a layout being tried by India’s National Institute of Solar Energy as well as by Germany’s Next2Sun GmbH and Märladalen University in Sweden, have the property of generating maximum power in a morning and an afternoon peak, complementing the typical solar profile of midday peaking.

The late afternoon generation this configuration allows could partly relieve evening peak demand to the extent that loads can be shifted earlier, as may be possible for some residential cooling, or by reducing the time between generation and discharge of batteries, enabling more flexible charging schedules.

A research group at Lahore University of Management Sciences has undertaken extensive modelling of these layouts for relevant latitudes, suggesting high levels of generation relative to conventional configurations. If time-of-day pricing is introduced for feed-in tariffs, as well as on the consumer side, vertical bifacial arrays could be a particularly attractive option for agrivoltaics developers in India.

Meanwhile, in India, several groups have already made a strong start in research to establish the circumstances in which agrivoltaics can be viable. There are

India is capable of producing solar power in higher quantities and more reliably than most European countries

Layout of Vertical Bifacial Panels and Generation Pattern Compared to Coventional Arrays

Source: Author

States should have primary responsibility for agrivoltaics, with support from the Union government

multiple variables whose individual effects and interactions have to be considered, and these are best studied by specialised research organisations.

These include the effects of different panel layouts because maximising power generation favours densely arrayed panels, whilst maximising yield requires dispersing the panels to prevent excessive shading.

Many other factors, especially appropriateness for different crops with varying levels of shade tolerance, interactions with soil and water conditions, maintenance tasks and costs all influence viability. Establishing their effects goes beyond agricultural and technical research, because the financial outcomes require analysis of how optimising the various trade-offs affects farmers’ incomes under different ownership and tariff regimes.

Ensuring food security

The roll-out of agrivoltaics in India cannot proceed without taking account of the need to protect food production and food producers. India accounted for 22% of the global burden of food insecurity, the highest for any country, in 2017 to 2019, it said, citing a report. Median farm size is under one hectare, with high levels of self- consumption of produce, most farm labourers owning no land, and multiple structural and market access issues confronting the sector, according to a report in the Indian Forum.

Any policies governing agrivoltaics must take account of these realities, as well as the needs of the 300 million additional citizens (still anticipated in coming decades despite recent falls in the total fertility rate), and be designed in such a way that farming livelihoods, food quality, and output are all equally sustained.

Balancing energy production and food production is an optimisation exercise. A quantity that has emerged in considering the economics and viability of agrivoltaics projects, which can be estimated for a given piece of land at the proposal stage and potentially used in the approval process, is the Land Equivalent Ratio, which compares the energy output of an agrivoltaics project to that of a pure solar farm, and the crop yield of the agrivoltaics project to that of farming only, all for the same piece of land.

However Indian policy-makers proceed, it is essential to adopt a carefully considered set of standards and definitions, matched with an approval process that safeguards agriculture. Without an agreed and clear process, many potential projects will wither on the vine.

Similar restrictions could be developed by India’s states to suit regional circumstances, with the possibility that the Union Government might set “backstop” standards as a means of safeguarding agricultural production.

Reforms of land-use classification could give farmers, in most cases, farmers’ groups, the right to own and operate agrivoltaics facilities, rather than energy developers, discoms or other intermediaries, perhaps by enabling them to apply for redesignation of land in a special agrivoltaic land category.

Accelerating agrivoltaics, protecting the country’s farmers

Regional variation in crops and conditions, farming practices and markets for produce suggest that states should have primary responsibility for agrivoltaics, with support from the Union government limited to items such as minimum standards and definitions, incentive schemes, and centrally funded research and development and agricultural extension.

Specific grant schemes could promote the evaluation of current practices in local conditions as well as nurturing a uniquely Indian research programme that can take economic and social, as well as technical, factors into account.

Funding for agrivoltaics programmes within the Agriculture Ministry’s Sub Mission on Agricultural Extension could give farming communities greater confidence in trialling agrivoltaics methods, as has been implemented elsewhere, and state extension organisations should provide localised advice and support.

Most states do not allow non-farming commercial activity on farmland if it is not reclassified as commercial land. States could enable farm communities to establish income-generating agrivoltaic projects whilst retaining Indian farmers’ land ownership, by introducing a specific agrivoltaic land category.

Governments could also give financial incentives for the adoption of agrivoltaics by providing early-stage support to farmers indirectly through loan guarantees via commercial lenders, or by direct support mechanisms, such as extensions to the Union government’s PM-Kusum scheme.

Direct support mechanisms would be the preferred option if small farmers are not to be frozen out of opportunities to adopt agrivoltaics, because additional loans would simply aggravate debt burdens for many.

What analysts say:

Jun Yee Chew Head of Asia Renewables Research, Rystad Energy:

India can study and adapt Japan’s model on agrivoltaics (APV). When Japan introduced favourable [feed-in-tariff] FIT in 2012, APV adoption increased. Since then, the Japanese government has worked actively to promote this area via a series of policies. Effective this April 2022, APV will be given preferential treatment in the FIT amendment. In the second amendment of the FIT Law, one of the requirements for 10 to 50 kilowatt PV assets (which APV would fall under) to fulfill self-consumption of at least 30%. However, APV is waived from this self-consumption requirement. Theoretically, an APV-owner could sell 100% of its generated electricity from 1 April 2022.

Richard Edwards Senior Partner, Asia Clean Energy Partners:

If implemented carefully, agrivoltaics have strong potential in India given the country’s wealth of solar resources, land, and the need to both augment power supply and income for Indian farmers. However, given the predominance of small holder farms in India, it will be critically important in any agrivoltaic development scheme to balance food production with power production. Farmers’ primary business is food production, and it will be important to ensure that the expansion of agrivoltaics does not contribute to further food insecurity in the country by diverting resources from agriculture to power production. If done right, agrivoltaics can complement and even enhance food production.

To ensure that agrivoltaics schemes are viable, local capacity building for product and service providers, along with farmer training in operations and maintenance of the agrivoltaics installed on their farms is essential. The high upfront costs for photovoltaic power systems could be prohibitive, especially for small holders, so access to finance for agrivoltaics on favourable terms is also an important consideration.

Towards a carbon-zero future: the role of natural gas in reducing CO2 emissions

Mitsubishi Power has advocated the use of natural gas in lowering carbon emissions whilst ensuring energy security and flexibility.

Natural gas is one of the keys to APAC’s net-zero transition

Demand for natural gas has seen an increase in recent years amidst environmental concerns around more traditional sources of power such as coal or oil. As many corporations and countries alike have pledged to be carbon-neutral from 2050 onwards, searching for alternative sources of energy has been more critical than ever.

Natural gas, fortunately, just might be one of the keys to gradually transitioning towards net-zero emissions. It provides opportunities and benefits against other sources of energy that produce more carbon emissions and it offers a transitionary solution for the region to explore more zero-carbon sources like hydrogen in the coming decades.

The “Natural Gas and the Clean Energy Transition” report from the International Finance Corporation (IFC) pointed out that gas can be economical even when the capacity is utilised flexibly, leaving room for more renewables.

“PV solar, wind, and natural gas-fired turbines and engines have lower unit capital costs than coalfired equipment, and there are natural incentives to combine solar, wind, and gas such that the required capital expenditure is least-cost compared to a coalheavy mix,” the report stated.

IFC’s report also mentioned that total fuel costs can be minimised since the all-in cost of PV solar and wind in many markets is below the marginal cost of natural gas.

Natural gas emits about 50 to 60% less carbon dioxide (CO2) when combusted in a new, efficient natural gas power plant compared with emissions from a typical new coal plant.

A report from the IEA stated that the flexibility of the global gas market in the coming years will continue to be crucial, as natural gas will play a critical role in the transition towards a cleaner and more sustainable energy system.

This sentiment is echoed by Malakoff Corporation Berhad, Head of Special Projects, Renewable Energy, Ashwin Narayanan.

Citing Malaysia as an example, Narayanan mentioned that there are plans for 2.4 GW of gas power plants planned between 2025 and 2026 to replenish the retiring older plants, together with another 3.3 GW for the years 2029 and 2030.

“There is no doubt that gas would be the fuel for (the) energy transition, and APAC’s best bet to meet the net-zero target in 2050,” Narayanan said.

He added that there would be a combination of combustion technologies coupled with air quality systems within the natural gas power plant to address the transition.

Gavin Thompson, Asia Pacific vice-chairman at energy consultancy Wood Mackenzie, mentioned in his opinion article “What a difference a year makes – Asia’s energy leaders discuss an uncertain future” that whilst support for the acceleration of renewables and a consensus around the role of natural gas in reducing coal demand in Asia are deemed positive signs in the energy transition, the overall pace of change across the region remains “far too slow”.

“Over 70% of the region’s emission footprint is coal-based and with electrification the cornerstone of the energy transition, Asia’s rising power demand risks prolonging dependence on coal for the next decade at least. And the current power crunch is not helping, reminding Asia’s leaders of coal’s dependability in ensuring energy security and grid stability,” Thompson said.

Natural gas ‘in the mix’

Despite these projections, many countries are incorporating more natural gas in their energy mix amidst its proven contributions to reducing carbon emissions and ensuring a stable power supply.

Narayanan noted that when the 1990s approached, it brought with it a natural gas bubble within Southeast Asia. Malaysia, Thailand, Indonesia, Singapore, and Vietnam were amongst the beneficiaries of the grid system, coupled with various gas to power projects.

“These plants were not only cost-effective given the low cost of natural gas but also extremely flexible to operate. Natural gas formed the backbone of energy as industrialisation was at its peak,” he said.

Meanwhile, Mitsubishi Power Asia Pacific Managing Director and CEO, Osamu Ono pointed out that whilst coal has dominated the Asian market over the last two decades, natural gas is already a critical component of Asia Pacific’s energy mix. This is particularly so in countries such as Singapore and Thailand – with demand growing and new liquefied natural gas (LNG) terminals picking up as more markets make the transition toward a more

Osamu Ono, Managing Director and CEO at Mitsubishi Power Asia Pacific

sustainable energy future.

“Under the same power output, combusting natural gas produces less carbon dioxide emissions than coal. The efficiency of gas turbines has also improved over the years – this helps reduce direct emissions from natural gas combustion and lowers costs involved with meeting energy demand,” Ono said.

He added that combusting natural gas also enables the rising adoption of cleaner fuels, such as hydrogen and ammonia, with new innovations that allow gas turbines to utilise these fuels and support the region’s energy transition.

Some Southeast Asian countries are now making commitments towards increasing the share of natural gas in their energy mix.

Indonesia, which has large reserves of natural gas, recently approved plans to develop the Ubadari natural gas field and raise output at the Vorwata gas field using carbon capture utilisation and storage as it continues efforts to reduce carbon dioxide emissions. This has an estimated potential additional recovery of 1.3 trillion cubic feet of gas in total from the new Ubadari field and the enhanced Vorwata field.

Meanwhile, Malaysia is committed to operating gas power plants to replace coal power plants and Malaysian LNG imports are projected to increase by more than 1 million tons annually to reach 4.8 million tons in 2022.

A look into Mitsubishi Power’s expertise

To address carbon reduction goals, energy solutions company Mitsubishi Power combines cutting-edge engineering with its deep knowledge of local needs to accelerate decarbonisation and deliver reliable and affordable power around the world.

The company works closely with power producers in the region to best address their needs.

“Our work in countries across the region has helped guide a shift away from coal to natural gas, and our gas turbine installations have helped reduce carbon emissions in power plants by up to 65% when compared with coal power plants,” Ono said.

To date, Mitsubishi Power has delivered more than 1,600 gas turbine power generation systems globally, with over 650 gas turbines installed in Asia.

Amongst these projects include Southeast Asia’s first M701 JAC gas turbines, which commenced operation in Thailand as part of an order of eight turbines for a power plant in Chonburi Province. This is said to help produce more reliable, stable and cleaner energy for the country.

Mitsubishi Power also completed the installation and commission of a 500 MW natural gas-fired GTCC power generation system for the Muara Karang Power Plant – the most efficient in Indonesia and part of the government’s project to boost power supply capability to 35 GW. It will help meet the rising demand for electricity across the West Java region and facilitate infrastructure development for urban transport systems.

Furthermore, the company has all its J-Series gas turbine designs tested at a grid-connected T-Point 2 facility in Japan before commercialisation, to ensure world-class reliability. They undergo a long-term operation of at least 8,000 hours of validation, equivalent to nearly one year of normal operation. These turbines have amassed over 1.6 million operating hours with 83 units sold worldwide, enabling power plants to achieve the world’s highest power generation efficiency of greater than 64% and offer a reliability of 99.6%.

To further support the energy transition, its heavyduty gas turbines can now also operate on a mixture of up to 30% hydrogen and 70% natural gas with the necessary equipment modifications, and this can be increased to 100% hydrogen in the future.

“This technology is compatible with the use of existing facilities without large-scale modification of power generation facilities, which helps lower costs and ensures a smooth transition to a hydrogen society,” Ono said.

Meanwhile, ammonia has also gained traction as a future fuel in the energy transition as it is a highly-efficient hydrogen carrier and can be directly combusted as a fuel. It is also easier to liquefy than hydrogen and therefore much easier to store and transport.

Leveraging this carbon-free fuel, Mitsubishi Power has commenced the development of a 40 MW gas turbine fueled by 100% ammonia and is targeting commercialisation around 2025. As the firing of ammonia produces no CO2, carbon-free power generation is achieved. “It will also aid in decarbonisation whilst addressing smaller-scale energy needs, such as small to medium-scale power stations for industrial applications, remote islands and more,” Ono said.

Ono also recognises the challenges that come with the production of NOx emissions during the direct combustion of ammonia. To address this, Mitsubishi Power aims to combine selective catalytic reduction with a newly developed combustor that reduces NOx emissions.

Transitioning to a carbon-zero future

Mitsubishi Power acknowledges that the Asia Pacific is home to a diverse and unique mix of people, infrastructure and economic potential, which makes the energy transition a complex one that calls for market-specific approaches to decarbonisation.

In this regard, Mitsubishi Power is a power solutions brand of Mitsubishi Heavy Industries, one of the founding members of the Asia Natural Gas and Energy Association, which is actively helping Asian nations lower carbon emissions by promoting natural gas. The association advises governments as they develop energy policies and solutions vital for a stable, consistent and affordable transition.

The company is also exploring cleaner, alternative fuels to promote a further reduction in carbon emissions.

It has partnered with Indonesia’s Bandung Institute of Technology (ITB) to research next-generation clean energy technologies, as well as how AI and big data analysis can enhance technologies used to diagnose the operation of power plants in Indonesia. Mitsubishi Power also promotes the adoption of biomass co-firing at Indonesia’s thermal power plants.

“A variety of approaches should work in parallel for the region to viably decarbonise, progressively introducing more renewable sources into the mix, whilst reducing carbon footprint in existing plants,” Ono said.

REGULATION WATCH New customs duty on solar equipment threatens India’s RE goals

The government will be introducing a 25% rate on solar cells and 40% on solar modules in April.

India’s targets will require between 35GW to 40GW of annual installation of renewable energy (Photo: India One Solar Thermal Power Plant)

India’s pursuit of its ambitious 450-gigawatt (GW) renewable energy target by 2030 is at risk of slowing down with a new measure that will levy custom duties on solar equipment with rates up to 40%, argued Institute for Energy Economics and Financial Analysis (IEEFA) Energy Economist Lead India Vibhuti Garg. She even posed a warning that this could do more harm than good for India’s renewable energy goals.

Beginning 1 April 2022, a 25% basic customs duty (BCD) rate will be imposed on solar photovoltaics (PV) cells and 40% on solar modules. Although these rates are intended as a stimulus to domestic manufacturing, Garg said manufacturers might be unable to meet the demand for renewable energy growth in India.

“The imposition of BCD will increase the costs and thereby tariff from renewable energy projects. The renewable energy developers will find it increasingly difficult to find off-takers for such expensive power,” Garg told Asian Power in an exclusive interview.

She added that a huge resistance is expected down the line as electricity distribution companies that are already burdened with poor financial health also face difficulty in passing on tariffs to ultimate consumers.

Unprepared local manufacturers

India’s targets, according to the IEEFA, will require between 35GW to 40GW of annual installation of renewable energy. The Central Electricity Authority, meanwhile, noted in its Optimum Energy Mix report, that the country will need an additional 25GW of solar energy capacity annually until 2030 to fulfill its target.

This poses a challenge considering India’s manufacturers produce only about 18GW of solar modules and 4.3GW of solar cells. Garg said the country could miss its target because the actual production of solar equipment at any given time is “significantly lesser” as most solar manufacturing facilities in India operate at a capacity utilisation factor of less than 50%.

The country has also been heavily reliant on imported solar equipment. In a report, Fitch noted that in 2021, India imported more than 80% of its solar cells, amounting to 604 million units.

To address this, the BCD on solar PV cells and modules intend to supply chain disruptions, as well as project delays, according to Fitch Solutions. The Ministry of New and Renewable Energy (MNRE) said that the BCD serves as safeguard duties after the country’s solar capacity additions were affected by limitations in trading solar modules and cells.

The MNRE also plans to turn India from an importer of solar equipment to an exporter, providing other countries with an alternative avenue for their solar power needs.

Whilst this is the case, Fitch Solutions shared the view that India’s domestic market “might not be ready for such an aggressive push.”

“Going forward, as duty taxes grow higher and policies on solar equipment imports grow stricter, domestic manufacturers will need to accelerate their manufacturing quantity and product quality,” according to the report.

Fitch forecasted that in the short-term, India could see an average of 11% annual growth in solar power capacity to 140GW in 2031 from 59GW in 2022; but the inability of domestic manufacturers to meet the demand could expose this projection to downside risk—a supply and demand mismatch.

Despite this, Fitch expects the manufacturing industry to overcome this risk as private companies, such as Reliance Industries, invest in India’s renewable manufacturing sector. This is also on top of the move of the MNRE to set quality assurance processes for solar manufacturing to keep the solar panel’s quality within the International Electrotechnical Commission’s standards. Fitch maintains that India is still on the trajectory for a strong solar power generation growth, reaching 221 terawatt-hour (TWh) in 2031 from 93TWh in 2022.

Deferment may be in order

Notwithstanding its concern over the capacity of domestic manufacturers to meet solar equipment demand, Fitch no longer expects India’s government to postpone the effectiveness of the new BCD. But IEEFA’s Garg is of the position that the “government needs to defer its decision to impose BCD,” subject to measures that will protect the interest of domestic developers that could lose cost advantage against their imported counterparts.

“The imported technologies are more efficient. So the government should provide fillip to domestic manufacturing by schemes,” Garg said.

This may be in the form of direct support to the country’s domestic manufacturing, such as the production-linked incentive scheme, access to finance at lower rates or support to scientific and technological research and development.

“This would give a fillip to domestic manufacturing and help the government achieve its goal of self-reliant India and at the same time ensure achievement of renewable energy target,” she added.

“The Indian domestic manufacturing is lagging behind technology, so the government should create conducive policies for technology innovation and availability of finance. Imposition of BCD will not serve any purpose.”

Vibhuti Garg

India is still on the trajectory for a strong solar power generation growth, reaching 221 TWh in 2031

CEO INTERVIEW How running Jawa7 helps in clean energy transition

The coal-fired power plant ensures lower carbon emissions, with 45% efficiency.

Indonesia is veering away from coal as an energy source by committing to a 2060 net-zero emission target, but Jawa-7, a coal-fired power plant, is playing a part in the country’s push towards emissions reduction. The first ultra-supercritical power plant is able to minimise its carbon emissions as it boasts of its plant efficiency of more than 45% and is gearing towards adopting clean and energy-saving measures.

Asian Power sat down with PT Shenhua Guohua Pembangkitan Jawa Bali (PT SGPJB) President Director Zhao Zhigang to talk about the consortium’s coal-fired power plant project, called the Jawa-7. He also shared insights on how the joint venture will gradually work towards carbon neutrality.

PT SGPJB is a consortium owned by China Shenhua Energy (70%) and PT Pembangkitan Jawa Bali Investasi (30%). Zhao said PJB’s clean energy transition plans drove China Shenhua to seek partnership with the electricity and energy investment firm.

“Originally, we knew that PJB had the intention to seek cooperation with power industrial companies from all over the world,” he said, as translated. “Its target is also to seek the transition from traditional power industry to renewable power.”

The power plant, which has the largest installed capacity in megawatts (MW), is also the first coal-fired power plant to operate the longest without shutdown.

Can you tell us what sets the Jawa-7 apart from other coal plants in Indonesia?

The Jawa-7 coal power plant has the largest single-unit capacity in Indonesia. Our unit’s capacity is 2 x 1,050MW. The power plant’s efficiency is very high. It’s already above 45% and also our coal consumption efficiency is higher, which has already reached 273 grams per kilowatt-hour. So, this high efficiency is also a measure to reduce carbon emission because our power plant’s power generation efficiency is high.

The other point is that, as far as we know, the previous Indonesian units used imported equipment from South Korea, Japan, and other Western countries. But in our power plants, all of our equipment is imported from China and they are the best equipment in China and they are provided by the companies with mature and advanced technology. In our infrastructure construction periods, we have placed a team from China regarding the construction, the commissioning, and the design. The reliability of Jawa-7 is very high and after the production of our Unit 1, it has run 302 days consecutively. It now has a long continuous operation.

Because our power plant is built next to the sea, we have our coal jetty; and we used advanced technology from China. It is called the belt coal conveyor technology and we have the longest coal conveyor belt in Asia. As for the water resources in the projects, we have also used advanced dissimulation technology provided by our company that has ensured that we have enough water resources for our company.

What is the current progress of the completion of the power plant and how will you ensure it is finished soon?

Right now, we still have some work left to be finished. Whilst still under the influence of the COVID-19 pandemic, some tactical support personnel are having difficulty coming to our sites,

PBJ seeks cooperation with global power industrial companies to transition from traditional to renewable power (Photo: PT SGPJB President Director Zhao Zhigang)

Jawa-7’s coal consumption efficiency reaches 273 g/kWh. This high power generation efficiency is a measure to reduce carbon emission

whether it is from Indonesia or China.

Another problem is those particular financial settlements because we have regulations from our Chinese superior company. We must have second party audits personnel to review our project’s financial settlement progress. But for our targets, our initial plan is to finish the financial settlements next year−the first half of next year.

To ensure the completion of the projects, we introduced two measures. The first one is to coordinate human resources in Indonesia and China. Right now, the pandemic situation in Indonesia is getting better, so it is more convenient for us to have human resources from all sides. The second measure is that for the financial settlements when the pandemic situation gets better, then we will have some professional audit team from China that is assigned by our superior company as we target to finish the plant in the first half of next year.

How will you ensure the reliability and readiness of the plant?

We use three strategies. The first is to improve our employees’ technical skills, especially for our local employees because the major difficulty is the language barrier. So, our Chinese employees have learned English and our Indonesian employees have learned Chinese. It will be easier for our experienced employees and our fresh graduates to exchange information. The second strategy is to enhance our operations, regulations patterns, and also enhance our maintenance standard. The third strategy is about the material supplier, spare parts supplier.

Our strategy is to improve supply chain reliability. Our next

plan is also to find other companies that have the same demand as us and, in that way, we will share the supply chain and share the material and spare parts storage. For our supply chain for the special power plants products, it’s mainly from China, but for other regular resources, we purchased them in Indonesia.

Governments are taking measures to transition to cleaner energy. As you are running a coal-fired power plant, what efforts are you implementing for Jawa-7 to reduce the country’s carbon emissions?

The Indonesian government plans that there will be no new coal-fired power plants in 2025 and in 2040, the current coalfired power plants will be phased out. I think it is very hard for the Indonesian economy to achieve these targets in such a short time. Maybe in the future, we can learn from the Chinese environmental protection policy. The first one is to adopt energysaving measures because if we can use our energy more with higher efficiency, then it will be better for the country’s carbon emission reduction targets.

We can also learn from other countries and from all of the works about carbon emission reduction knowledge. We will also comply with the Indonesian government’s new environmental protection policy to upgrade our coal power plants.

With Indonesia’s potential to phase out coal by 2040, what technologies and strategies are you looking at to comply with the country’s decarbonisation goals?

Recently, Chinese President Xi Jinping has also said that there will be no more overseas coal-fired power plants from China and the world. We will also use the same strategy as what has already been done in China, which includes gradually promoting carbon neutrality and adopting some energy-saving operations in coal-fired power plants to improve the power plant’s efficiency, and then gradually we will phase out the power plants with lower efficiencies. Then maybe in the future, we will also use some more advanced and mature technologies such as carbon capture and other carbon emission-related technologies.

For decarbonisation, the consortium will use the same strategy in China to promote carbon neutrality through energy-saving upgrades. Can you elaborate on these energy-saving upgrades that you are looking at?

I think that the major targets for carbon capture are to capture the carbon dioxide and use high pressure on the grounds so that it can prevent carbon emissions to the atmosphere. If we will promote the carbon emission-related upgrades, later in the future, we will have a special professional team to study the feasibility of this project and the possible projects, and then we can adopt carbon emission reduction-related knowledge to do the upgrade.

The government plans that there will be no new coal plants in 2025 and 2040. It is very hard for the Indonesian economy to achieve these targets in such a short time

Indonesia’s net-zero emission targets

To accelerate investments in renewables, Indonesia may rely on feed-in tariffs and auction schemes

According to the International Energy Agency’s (IEA) Electricity Market Report January 2022, Indonesia’s electricity demand was expected to have grown by 3.6% last year and to continue to grow over 4% this year, whilst the annual electricity demand growth is seen to be slightly above 4% from 2022 to 2024.

The IEA also said that Indonesia’s total generation capacity as of July 2021 was at 74 gigawatts, with coal accounting for the largest share of generation at 58%, whilst the share of renewables remained stable at around 17% for the last four years. The share of solar photovoltaics was around 0.1% last year.

For Indonesia to achieve its renewable target of 23% in 2025, a presidential regulation on renewables could be expected this year. To accelerate investments in renewables, Indonesia may rely on feed-in tariffs and auction schemes.

The agency also noted that the Indonesian government announced its commitment to attaining net-zero emission by 2060 or sooner with financial and technological support from developed nations. To achieve this, the government identified five principles: increasing the share of renewables, reducing the use of fossil fuels, promoting electric vehicles, electrification in the residential and industrial sectors, and using carbon capture, utilisation and energy storage.

The state-owned electricity company, PT Perusahaan Listrik Negara, has also announced that it will not build new coal plants after 2023, when all plants under its 35GW programme and 7GW Fast Track Programme are expected to be completed, according to the report.

It noted that under Indonesia’s recent electricity supply plan, around 5GW of coal-fired capacity from independent power producers were expected between 2024 and 2030. However, no new fossil power plants will be built beyond 2030, with the first stage of coal-fired plant retirements starting in 2031.

IEA added that interconnection and grid development are amongst the key challenges in Indonesia both between islands in the country and across borders, noting that grids are “an important flexibility resource for integrating renewables in a reliable and cost-effective manner.”

The country’s net zero plan indicates that interisland interconnection should start commercial operation in 2031, the report further said.

Overall, electricity demand was estimated to have risen by 2.8% in 2021 and a stronger recovery is expected from 2022, with an annual demand growth close to 5% from 2022 to 2024.

Coal continues to hold the lion’s share in Southeast Asia’s electricity supply as it accounts for around 43% of the supply mix, followed by gas at 31%, and renewables at 25%. The agency, however, said that the share of both coal and gas in the mix dipped last year, whilst renewables saw an increase by over two percentage points.

“While renewables growth is set to continue up to 2024, we expect the sum of coal- and gas-fired generation to meet around two-thirds of new demand over this period,” according to the report.

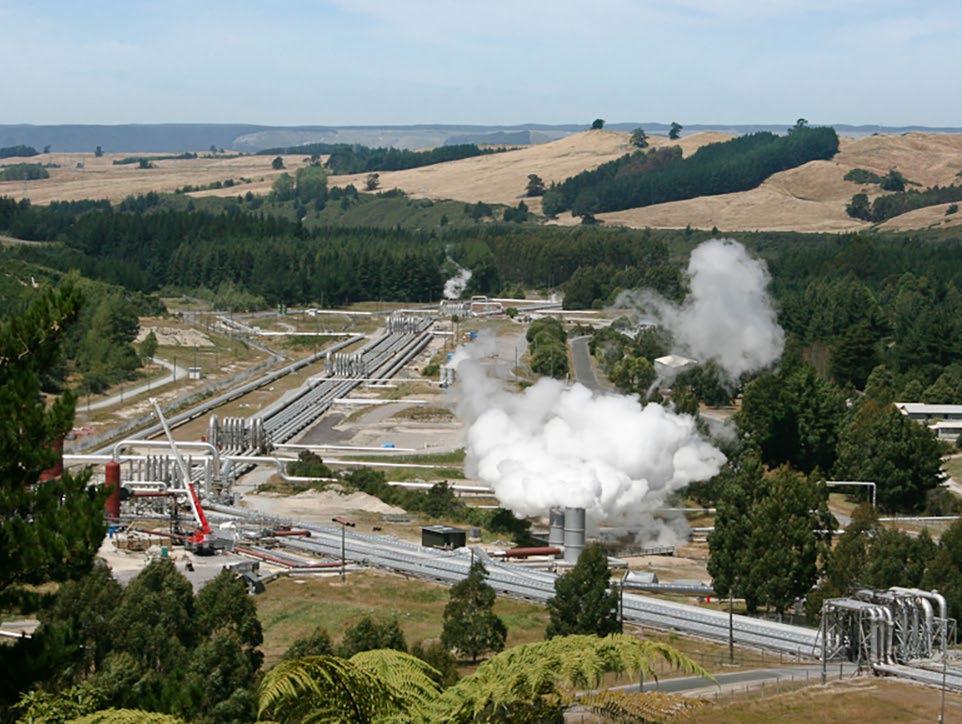

It is important for Indonesia to seek ways of developing geothermal power whilst still protecting its forests and environment (Photo: Geothermal Power Station of Ulubelu Unit 3-4, Lampung Province, Indonesia)

Geothermal power needs policy boost to stay on the net-zero track

Its annual capacity additions averaged only 500MW annually in the last five years.

The geothermal power sector, whose share in the global power mix remains small, will need a boost from policies that will reduce cost and cushion pre-development risks to drive the industry closer to the net-zero track.

In its Tracking the Clean Energy Progress report, the International Energy Agency (IEA) estimated that geothermal electricity generation grew by only 2% year-on-year to approximately 200 megawatts (MW) in 2020. This is below the 500MW average growth recorded in the last five years.

“This technology is not on track with the Net Zero Emissions by 2050 Scenario, which requires 13% annual increases in generation over 2021-2030, corresponding to average annual capacity expansions of ~3.6 gigawatts (GW),” the report read.

Growth in geothermal electricity generation will be driven by Turkey, Indonesia, and Kenya, which are all expected to take the lead in geothermal due to the countries’ abundant resources that remain untapped. In this light, the IEA recommended that policies, which help reduce costs and mitigate pre-development risks, are needed to increase geothermalbased power generation.

Global geothermal capacity, according to Fitch Solutions projection, will grow by 4.5GW over the next decade, increasing at an annual average rate of 2.8% to 18.7GW in 2030. This growth will largely come from the Asian region, particularly Indonesia and Turkey, and Central and Eastern Europe. This comes as the regions are expected to have 1.8-GW and 1.1-GW net capacity additions, respectively.

Sustaining geothermal power

The contribution of geothermal power in the global power mix has historically, which will likely be sustained despite growing interest in the technology coming from Asia. According to Black & Veatch, the sector could retain its current allocation in the global energy portfolio through investments in oil industry technologies that improve the economics of geothermal. This includes technologies, such as geological sensing, horizontal drilling, and high-intensity fracturing.

New technologies, like enhanced geothermal energy, and closed-loop systems, also have the potential to alter the economics of geothermal energy as it enables the energy resource to be drilled from anywhere in the world.

“Capitalising on these market factors will also require clear policy support and regulatory frameworks for financial incentives that will improve project bankability and enable Asia to increase its geothermal capacity,” Black & Veatch Executive Vice President and Managing Director for Asia Power Business Narsingh Chaudhary told Asian Power.

“In addition, developers will need to adapt many of the emerging technology innovations and project management best practices to improve overall project economics and help geothermal compete with other evolving generation options like nuclear and hydrogen.”

Chaudhary added renewable energy mandates, as well as reports that indicate geothermal energy companies are getting support from investors, could also help the geothermal market.

The near-term development of geothermal power in Asia, Chaudhary further emphasised, will depend on the policies and programmes that governments in the region will put in place as well as the rate that new technology is adopted in the energy market.

The future of geothermal will also vary on its cost competitiveness, in comparison to other renewable energy sources. In addition, partnering industry leaders experienced with every aspect in the lifecycle of projects from early financing through commercial operation will also be a key to convert promising geothermal potential to commercial facilities serving the grid and customers throughout Asia.

Narsingh Chaudhary

The near-term development of the geothermal sector in Asia will depend on the policies and programes that governments will put in place, as well as the rate that new tech is adopted in the market

“As a non-intermittent renewable energy resource, geothermal energy can generate stable baseload power and be paired with intermittent renewable energy sources to accelerate Asia’s energy transition. The key is understanding the right mix in a balanced energy portfolio,” Black & Veatch’s Chaudhary said.

He explained that accommodating an increased capacity of intermittent renewable energy, like solar and wind power, needs a new, integrated suite of solutions across generation, energy storage, transmission and distribution to sustain safe, reliable and resilient power that makes our modern economies and communities work. The deployment of gas-fired generation and continued advancements in hydrogen and nuclear are options that could contribute to the more diverse and balanced mix of power generation technologies, he added.

Challenges to geothermal

The development of geothermal energy in Asia, however, could be dampened by high development costs that make other renewables, such as solar and wind power, more cost-competitive. The difficulty in securing permitting and other processes in relation to tariffs and the bankability of power purchase agreements, and unattractive incentives packages may also prove to be a challenge.

“Taken even further, like many other renewable energy sources, geothermal generation capacity is often located far from major demand centres. The development would need planning and financing for any effective integration of new geothermal facilities into regional or national power grids,” Chadhaury said.

GlobalData Practice Head Pavan Kumar said the geothermal development has a higher stake risk whilst the payoff only comes long-term. He further explained that it is more likely that energy investors will lean towards other renewable energy sources without financial incentives like subsidised power rates, competitive feed-in tariffs, or tax incentives.

According to GlobalData, geothermal capacity across the globe grew at a compound annual growth rate (CAGR) of 3.15% and at 2.9% in the Asia Pacific region between 2000-2020. “It is expected that global geothermal capacity will increase at 5.3% CAGR and Asia Pacific region will increase at 5.8% CAGR during 2020-2030,” Kumar said.

“Geothermal power has a miniscule share in the global power capacity mix at 0.2% in 2020 and will be in the same range with a share of 0.22% in 2030. Similarly, the share of geothermal in the Asia Pacific region is 0.16% in 2020 and its share is expected to be around 0.17% in 2030.” The market is expected to attract some $23b during the next five years at an average annual investment of $4.6b.

The case of Indonesia

Indonesia’s renewable power market reached around 4.772.92MW by end-2020 from 3,126.10MW in 2010. It is expected to grow at a rate of 12.81% from 2020 to 2030 and reach installed capacity of 15,940.16MW by end-2030, according to GlobalData’s Geothermal Power in Indonesia report.

Geothermal power leads the country’s renewable power market with a total installed capacity of 2,130.70MW as of 2020 and is seen to reach 5,872.94MW by 2030 at a CAGR of 10.67%.

“The renewable power market in Indonesia is dominated by geothermal power which held a share of 44.6% in total renewable capacity in 2020. Although this share is expected to decline to 36.8% in 2030; geothermal power will continue to hold the largest share in Indonesia’s renewable capacity mix,” the report read.

Total renewable electricity generation rose to 27,515.33 gigawatt-hours (GWh) in 2020 from 16,296.73GWh at a CAGR of 5.38%. The total generation is expected to reach 66,622.07GWh by 2030 at a CAGR of 9.25%.

Geothermal energy is also leading in terms of electricity generation, reaching 14,832.80GWh in 2020 from 9,357GWh in 2010. Its electricity generation is also expected to reach 40,758.20GWh by 2030 with an annual growth rate of 10.64% over the same period.

The Indonesian Government backed the development of geothermal power which in turn also helped the growth of the energy sector’s technology.

The New Geothermal Law No. 21 in 2014 removed geothermal activities from the mining activities classification which resulted in the rapid growth of the technology as it allows geothermal activities to be conducted in high conservation value forest areas, it said.

The government also provided a $275m Geothermal Fund in 2017 and has also found support from the World Bank, the Green Climate Fund and the Clean Technology Fund through loans of around $278m in 2019 to boost investments for the power sector.

“The development of geothermal energy has led to environmental concerns in Indonesia. Majority of the country’s geothermal reserves are in conserved forests, and the development of projects in these areas requires a presidential decree,” it said. “Therefore, it is important for Indonesia to seek ways of developing geothermal power whilst still protecting its forests and environment.”

Geothermal power leads Indonesia’s renewable power market and is seen to reach 5,872.94MW by 2030

Pavan Kumar

Geothermal power has a miniscule share in the global power capacity mix at 0.2% in 2020 and will be in the same range with a share of 0.22% in 2030

COUNTRY REPORT: SOUTH KOREA Renewable energy growth is lagging in South Korea

This could be due to geographical barriers, prices, and the presidential election.

For South Korea, renewable energy deployment remains an uphill battle as the country scours to find space for it. With a total land areas of 223,170 square kilometres, South Korea consists of mountains and narrow plains that prove difficult to install cleaner energy sources, an expert claimed.

Even the government’s active efforts to achieve carbon neutrality appear to fall short. One example is the Presidential Committee on Carbon Neutrality’s two new road maps calling for the abolition of coal-fired power generation, with one framework seeking to eliminate liquefied natural gas (LNG) and the other opting to retain LNG with carbon capture technologies. Despite this, Rystad Energy still sees South Korea’s coal capacity increasing in the short term as additional coal power units are currently under construction. Whilst natural gas, which has a much lower carbon footprint, is projected to become its largest power source by the late 2020s.

“When it comes to renewable development, South Korea has been lagging compared to its peers,” Rystad Energy Analyst Fabian Rønningen said.

Renewable barriers

According to Rystad Energy, amongst the key factors behind the slow development of renewable energy in South Korea is its geography. Largely consisting of mountains with small valleys and narrow coastal plains, South Korea offers very little space for the deployment of renewable energy sources, such as solar and wind power.

On top of this, spaces that could potentially be suitable for renewable energy sources are already densely populated, making it even difficult for the country to transition.

“That is one of the reasons the country has put so much emphasis on the development of hydrogen and ammonia use in the power sector, as already existing infrastructure can be used, and thermal power plants have a much smaller footprint than large scale solar and wind farms,” Rønningen said.

Fuel mixing with less polluting fuels, like biomass, is a solution to reduce the damage caused by operating coal-fired power plants. In South Korea, ammonia mixing in coal-fired power plants is expected to become increasingly more important as the country set a “very ambitious” target to generate 22 terawatthour through ammonia by 2030. “The pathway to this is yet to be seen,” he said.

The Lantau Group partner, David Kim, based in Seoul, likewise raised South Korea’s natural environment as “not very favourable” for the deployment of solar photovoltaic and wind generation. This is considering the high cost of land where new sources can be deployed as well as the weak insolation, which could in effect slow down the transition to cleaner energy sources, Kim said.

“But we cannot stop the shift. As more renewable energy is generated, the key issue will be how we manage and operate the electricity market in Korea,” Kim said.

“At the moment, the wholesale market and the retail market are not fully linked. There is a lack of price signals between generators and consumers, which disincentivise the improvements and the innovations in the energy market.”

Kim said that to attract more investments and talents, South Korea also has to devise a way to operate the electricity market in the long run.

Apart from geographic hurdles, South Korea also struggles with the cost of renewable energy sources, a challenge that most countries have now moved beyond. Despite this, the country has already made strides in renewables driving demand for coal and LNG down. Rystad Energy expects this to lead to a large reduction in emissions, but not quite enough to bring it down to zero.

South Korea’s natural environment as “not very favourable” for the deployment of solar photovoltaics and wind generation

The presidential election will have an effect on the direction the country will take in the clean energy transition

Fabian Rønningen

David Kim

“This is where green hydrogen and ammonia come into the picture,” Rønningen said, adding the Green New Deal and Ninth Basic Plan, as well as the proposed Emissions Trading Schemes, could help speed up renewables growth in the country.

“If the South Korean Energy Agency is arranging capacity auctions with larger volumes, a faster deployment can be achieved. The continued cost reduction of renewables, especially floating offshore wind in non-utility scale solar PV will help South Korea transition faster,” he said.

Presidential election

The presidential election in March is expected to have an effect on the direction the country will take in its clean energy transition targets.

“I believe that the goal for the greenhouse gas reduction and the clean energy transition will be firmly pursued in the long term view,” Kim said.

In a report, Fitch Solutions noted that the country’s policies over its clean energy transition will continue changing, particularly around nuclear energy as South Korea remains “politically divided” over the subject.

“As such, we are seeing increasing pressure around the continued need for nuclear power, which might be reintroduced in a new administration, presenting some upside risks to our current outlook,” according to Fitch Solutions.

“Nonetheless, there remain significant uncertainties around South Korea’s future power mix, and we will continue to monitor developments closely and revise our forecasts accordingly if necessary.” dominated by coal, gas, and nuclear, Lantau Group’s Kim said.

At present, South Korea targets to keep the share of natural gas down to only 19.5% of its power generation; which Rystad Energy’s Rønningen sees as a difficult pursuit as natural gas is seen to have a higher share in 2022.

Coal accounted for the largest share in the current power mix, which is expected to decline amidst phase-out plans. Meanwhile, the nuclear output is expected to grow near-term with several new units in the pipeline, but will likewise play a reduced role in South Korea’s power sector in the long run as the country’s nuclear fleet ages. This will then leave South Korea to rely on other sources of power to meet the generation gap created by the reduced output from coal and nuclear power.

“Overall, the long-term expected reduction of both coal and nuclear means that other sources will need to meet power demand, and that is expected to be natural gas and renewables, such as solar, wind,

South Korea’s new draft green taxonomy, K-Taxonomy, classifies liquefied natural gas as ‘green’

hydrogen, and ammonia,” he said.

Early this year, the South Korean government published the K-Taxonomy, a new draft green taxonomy, which classified LNG as “green.” This opens opportunities for new LNG-to-power projects as the “green” classification qualifies these projects for green financing and tax incentives. The draft taxonomy, however, does not classify nuclear energy source as “green.”

Fitch Solutions in a report said that the new classification could lead to a large number of new gas-fired power plants in the market, especially as ageing coalfired power plants are replaced by gas. This could bring the share of coal energy source down to 30.1% from 36.7% and the share of gas up to 30% from 26.7% of the power mix by 2031.

Rystad Energy’s Rønningen said the reduced role of coal and increase in gas will have a “drastic” impact on demand for both sources, especially considering South Korea has a relatively young fleet of coal-fired power plants. An important factor for coal in South Korea is the relatively young fleet of coal power. Phasing-out coal could pose risks of stranded assets for a large proportion of the power plants.

He added this could be addressed through refurbishment projects that allows fuel to switch from coal to natural gas directly. In contrast, the new classification could increase the demand for gas, which Rønningen said exposes South Korea to global energy markets, which has been a rollercoaster for the entire year of 2021.

“Switching from coal to gas would result in a deep cut in emissions and depending on the future pricing in the gas and coal will reveal if it is also the correct financial decision if costs of electricity will rise as a result in South Korea,” he said.

South Korea’s power mix

The country’s energy sector largely consists of imported fossil fuels such as oil, coal and natural gas. It is also known for being amongst the largest power sectors,