17 minute read

Time for a comeback? Hong Kong’s top 50 insurers show a 9.75% surge in assets

Health and wellness will continue to be a trending focus in Hong Kong’s insurance industry

Health and wellness products still remain a priority for the industry.

With the skies clearing, Hong Kong consumers will still make sure they worrying about it. This has been evident in Hong Kong’s Insurance Authority’s (IA) annual report have an umbrella handy—something Hong Kong insurers took note of as they ready health and wellness products for 2022.

Insurance Asia’s 2022 Insurance Rankings has revealed that the industry’s top 50 insurers total assets surged by 9.75% to HK$709b in 2020 from HK$646b.

AIA International continued to retain its number one spot in the rankings despite its total assets declining to HK$126b in 2020 from HK$141b in 2019. This was also the case for Prudential (HK) Life. With its total assets dropping from HK$111b to HK$92b, it still managed to retain the second spot in 2021’s rankings.

China Life took the third spot with HK$67b in assets with Manulife following close behind at fourth with HK$63b. Completing the top five is HSBC Life at $54b.

Going by the numbers

More Hong Kongers are starting to act upon their future, instead of just with the Individual Life business remaining to be the dominant line in the business, making up HK$458.5b or around 87.9% of total long-term business. The report also saw a modest rise in total office premiums for in-force long-term business by 2% to HK$521.4b in 2020. What probably slowed down the long-term business is the 20.9% decrease in office premiums for new individual life business to HK$119.6b in 2020, including HK$106.8b from Individual Life (NonLinked) business and HK$12.7b from Linked business, which recorded a decrease of 23.4% and an increase of 8.8%, respectively. The total number of new policies decreased by 20.8% to 1 million in 2020. Office premiums for the new Individual Annuity business decreased by 36.3% to HK$13.3b. Meanwhile, the general insurance market performed admirably despite the considerable challenges in the past two years. Total gross written premiums recorded a growth rate

More Hong of 8% to HK$59.8b in 2020. Overall Kongers are underwriting profit hit HK$2.3b, a starting to act major increase from HK$869m back upon their in 2019. future, instead The IA said that the biggest of just worrying contributor to the general insurance about it market’s growth was property damage, general liability, and pecuniary loss business. Rate increase and new business continued to fuel property damage and general liability business which both showed double-digit growth of 17.6% and 10.4% each. Upward adjustment of the maximum property values for the Mortgage Insurance Programme propelled forward mortgage insurance business, driving an upsurge of 57% in the Pecuniary Loss business. The pandemic, however, took its toll on direct sales of medical and travel insurance and had dampened the accident and health business, which saw a decline of 3.5% in 2022.

Health and wellness

Despite challenges in sales of medical insurance, however, HSBC Life Hong Kong CEO Edward Moncreiffe said that health and wellness will

continue to be a trending focus in 2022. Moncreiffe said that customers see health across three dimensions, namely physical, mental, and financial health. He added that this was supported by a global study they conducted last year which saw eight out of 10 believe that they need to be both physically and mentally healthy to enjoy their financial wealth.

This was seconded by Damien Green, CEO of Manulife Hong Kong and Macau, adding that retirement funding needs in Hong Kong remain huge, as well.

“Today around 30% of total health care expenditure in Hong Kong is ‘out of pocket’ which represents the big job on our hands to properly insure our community,” Green said.

For Green and Manulife, they are also preparing for an influx in demand from mainland Chinese residents for health and retirement insurance solutions. According to Manulife’s recent customer research, Chinese mainlanders in the Greater Bay Area are eager to visit Hong Kong, with 70% of respondents saying they plan to purchase insurance products whilst in the city.

2021 in a nutshell

In summing up 2021 for HSBC Life, Moncreiffe said it has been a challenging year for the whole industry, with COVID-19 waves persisting throughout and international borders largely closed.

“Despite this, HSBC Life demonstrated extremely resilient performance with our Annualised New Premiums and Value of New Business growing 20% and 34%, respectively. As the Hong Kong population continues to adjust to new ways of living as a result of COVID-19, our strategic investments in digital propositions have continued to yield positive results,” Moncreiffe said.

For Manulife, it has been a busy year as they report a 17% increase in core earnings in 2021 compared to 2020.

“Our leading high-value Agency franchise continued to be a key contributor to our strong results, accounting for 66% of total annualised premium equivalent sales. On top of this, we achieved leading growth in our overall number of agents last year. We had more than 11,600 agents by the end of the year, representing 9% growth over 2020,” Green said.

Looking ahead

Moncreiffe said that this year, HSBC Life will be gearing up to tackle the aftermath and uncertainties caused and left by the pandemic.

“We expect this will continue to manifest in multiple ways. It will continue to emphasise the need for operational resilience, it will change the way that customers look to buy and service their insurance policies, and it will increase the expectations that customers have for their insurers to be agile, always-on, fair and transparent,” Moncreiffe added.

Inflation is also a growing concern. Moncreiffe said there will be entire generations of savers who for the first time are exposed to wealth-erosion effects of inflation.

“Life insurers, and their intermediaries, will need to anticipate this fast, help their customers understand how to plan financially in such a climate, and make sure that they can offer long-term savings and retirement solutions that protect against these risks,” Moncreiffe added.

Moncreiffe said HSBC Life is in the business of making promises and they would continue to deliver by meeting the health, protection, retirement, and legacy needs of their customers.

“We write High Net Worth life insurance coverage to US$100m per individual, and yet we also provide term coverage that can be as low as below HK$2 per day. It is this ability to serve the needs of all segments of Hong Kong society that keeps us close to our customers and will ensure that we stay at the vanguard of exciting new product developments in 2022,” Moncreiffe explained.

2022 and beyond

Meanwhile, Manulife Hong Kong is arming itself to be ready for the upcoming strong demand from mainland Chinese visitors. Green said they accelerate investments in Hong Kong and Macau by enhancing their customer service and upgrading their self-serviced digital platform. They are also aiming to hire more agents with knowledge and connections in the mainland to better capture business prospects in the GBA areas.

“Once the border with mainland China reopens, we are well-prepared to serve our customers across the region by ensuring their access to high-quality health protection and retirement offerings,” Green said.

Though the aftermath of the pandemic will remain a challenge, Manulife Hong Kong continues to make preparations such as being on track with its HK$400m investment in 2021 and 2022 to further transform its digital applications for its agents and customers as well as improve virtual face-to-face interactions with customers.

“Manulife is the longest continuously operating life insurer in Hong Kong today, and this year we are celebrating our 125th anniversary in the city. Over the years, as we navigated the ups and downs together with the city, we are proud of our longstanding commitment to Hong Kong’s development and we will continue to cement Manulife as a household name in the city,” Green said.

Edward Moncreiffe

Damien Green

There will be entire generations of savers who, for the first time, are exposed to wealth-erosion effects of inflation

Inflation is a growing concern. Life insurers must anticipate this fast and help their customers plan financially

2021 RANKING

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 INSURANCE COMPANY

AIA INTERNATIONAL PRUDENTIAL (HK) LIFE CHINA LIFE MANULIFE (INT'L) HSBC LIFE BOC LIFE SUN LIFE HONG KONG AXA CHINA (BERMUDA) FWD LIFE (BERMUDA) TPLHK HANG SENG INSURANCE FTLIFE YF LIFE BUPA AXA GENERAL BEA LIFE CTPI(HK) FWD LIFE (HK) HONG KONG LIFE CHUBB LIFE AIA INTERNATIONAL AXA CHINA (HK) BOC GROUP INSURANCE GENERALI SWISS RE (ASIA) QBE HKSI ZURICH INSURANCE TLIC AIG INSURANCE HK BLUE CROSS FUBON LIFE HONG KONG HKMC ANNUITY CIGNA WORLDWIDE GENERAL LIBERTY INT' AXA CHINA (HK) ASIA INSURANCE PRUDENTIAL (HK) GENERAL TPRE TARGET BLUE CHUBB INSURANCE ALLIED WORLD UTMOST WORLDWIDE ZURICH INTERNATIONAL MSIG INSURANCE LLOYD'S SUN HUNG KAI AGCS SE AIA (HK) AETNA Classification

2020 TOTAL ASSETS*

2020 RANKING

2019 TOTAL ASSETS LIFE $126b 1 141b LIFE LIFE LIFE LIFE LIFE LIFE LIFE LIFE LIFE LIFE LIFE LIFE $92b 2 111b $67b 3 76b $63b 5 59b $54b 4 59b $39b 6 38b $32b 11 16b $30b 7 30b $28b - -

$20b 10 16b $18b 8 21b $13b 12 12b $10b 13 11b GENERAL $10b 20 4b GENERAL $9b 17 4b

LIFE $8b 14 7b GENERAL $6b 23 3b

LIFE $4b 9 21b

LIFE LIFE

$4b 25 2b $4b 16 5b GENERAL $4b 30 2b

LIFE $4b 19 4b GENERAL $4b 27 2b GENERAL $3b 33 1b GENERAL $3b - -

GENERAL $3b 35 1b GENERAL $3b 24 4b

LIFE $3b - -

GENERAL $3b 26 2b GENERAL $3b 34 1b

LIFE $3b 18 4b

LIFE

$3b GENERAL $3b GENERAL $3b - -

GENERAL $2b 19 4b GENERAL $2b - -

GENERAL $2b 39 1b GENERAL $2b - -

GENERAL $2b - -

LIFE

$2b 45 879m GENERAL $2b 32 2b GENERAL $2b 43 1b

LIFE $2b - -

LIFE

$2b 29 2b GENERAL $2b 41 1b GENERAL $1b - -

GENERAL $1b - -

GENERAL $1b 44 929m

LIFE $1b 40 1b GENERAL $1b -

-

TOTAL 709B

ANALYSIS: CLIMATE RISK Climate risk is burning billions and Asia remains vulnerable

In 2021, the costliest recorded natural disaster in the region topped $2b.

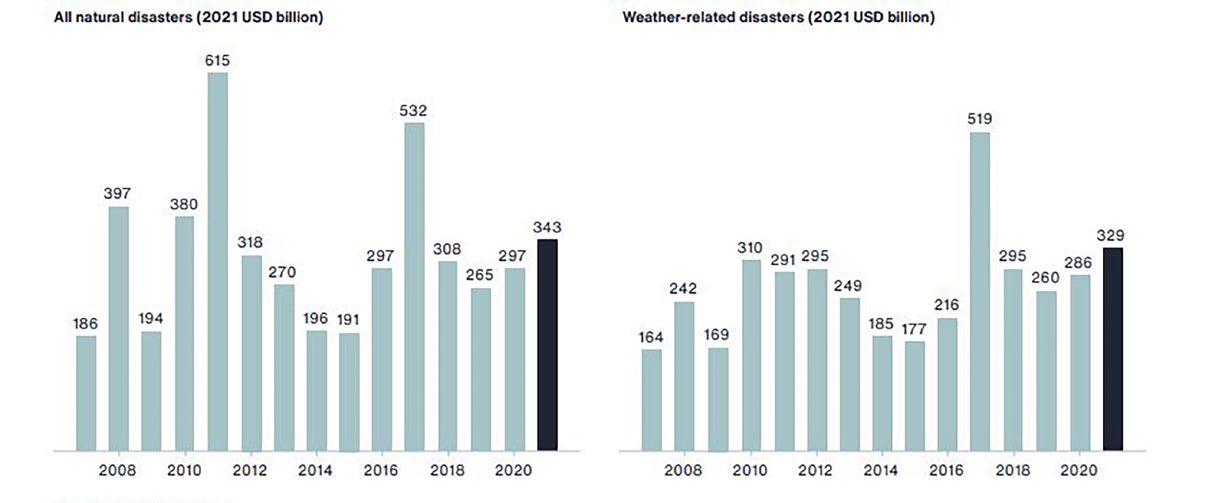

Natural disasters are definitely inevitable, but what continues to worry insurers is that these catastrophes are costing them a heftier price tag than ever. In Aon’s Weather, Climate, and Catastrophe Insight, global economic losses for 2021 alone were estimated to be around $343b with only $130b insured. This marks the seventh costliest year on record, with a protection gap of at least 62%.

Whilst this is not a recordbreaking year, far below the peak losses of $615b in 2011 and $532b in 2017, it was still above the average of $272b and the median of $265b of the 21st century. Comparing the last decade, between 2011 to 2020, economic losses were just 4% higher than the average and 15% higher than the median.

Economic losses were found to be solely resulting from weather- and climate-related events defined as atmospheric-driven phenomena, totalling $329b. This is the thirdhighest loss on record.

Aon pointed out that driving the cost of these economic losses that topped the $20b global threshold were just four individual environmental events, namely Hurricane Ida, the July Flooding in Europe, the Summer Season Flooding in China, and the February Polar Vortex in North America.

These four economic losses collectively topped $300b. If this continues, it would be impossible for insurers to properly cover these losses without a hike in premiums.

Asia’s vulnerability

Speaking at the Willis Towers Watson (WTW) Asia Pacific Risk Virtual Conference, Gillian Tan, Assistant Managing Director of the Development & International Group of the Monetary Authority of Singapore, stressed the urgent need for climate action, especially in Asia, as it is geographically prone to natural catastrophes.

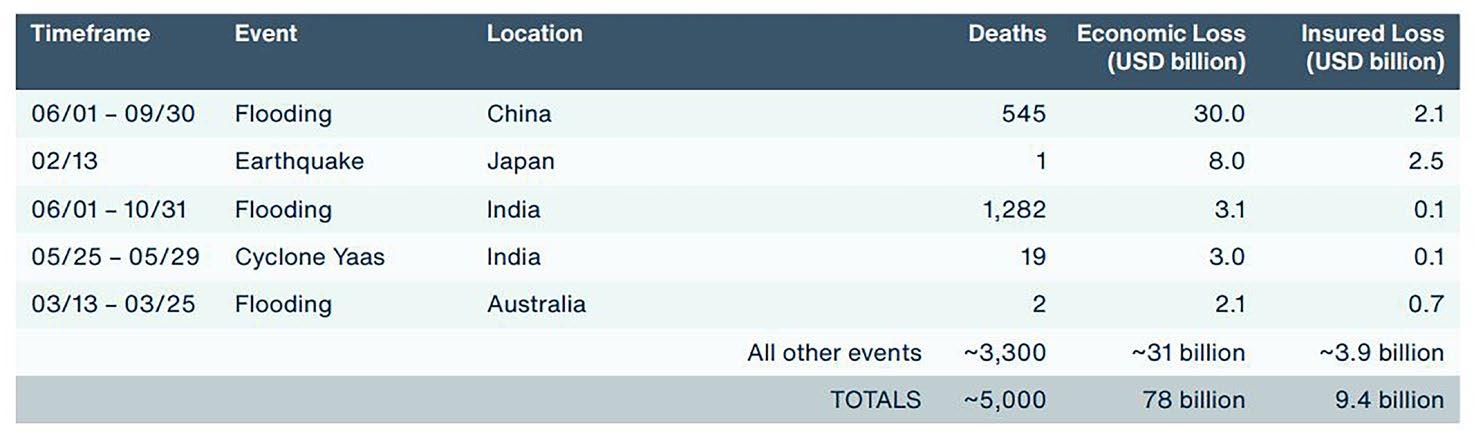

“The costliest natural disaster in 2021 was the flood in Henan province in July which resulted in a total economic cost of over $2b as of September last year, and this number is only expected to head north,” Tan said.

In Aon’s report, economic loss from flooding events between 1 June to 30 September 2021 in China stood at $30b. This makes it the number one most significant natural disaster event in 2021 in the Asia Pacific (APAC).

Aon said flooding events make up 55% of the economic losses in 2021, with China flooding events being the most significant natural disaster event for the second year in a row.

What is even more alarming is that, out of the $30b, only $2b were logged as insured losses. Out of the $78b of economic losses, only $9.4b or around 12% were covered by insurance. This highlights the underinsurance gap in the region.

“Amidst this sobering backdrop, what has been taken for granted all along is now clear: our interconnected and interdependent global system is incredibly fragile and vulnerable,” Tan said.

Losses in 2022

In Aon’s Global Catastrophe Recap, global preliminary loss for the first quarter of 2022 is now at $32b, with public and private insurers covering around $14b.

“The first quarter is typically the quietest of the year, though 2022 marked the sixth consecutive year to record more than $10b in insured losses,” Aon said.

What contributed most to the global loss is fluctuations in temperatures and precipitation influenced by the continued effects

Our interconnected and interdependent global system is incredibly fragile and vulnerable

The costliest natural disaster in 2021 was the flood in China’s Henan province with a total economic cost of over $2b

Global economic losses

Source: Aon (Catastrophe Insight)

Gillian Tan

of La Niña across the central and eastern Pacific Ocean. These influences resulted in notable hazard events, including prolific and record-setting rainfall along Australia’s East Coast, continued severe drought conditions in parts of Africa, South America, and the western United States, and an earlier start to severe weather season in the United States.

APAC logged the highest percentage of first quarter economic losses at more than $15b, followed by Europe, Middle East, and Africa at $8b and the US at $6b. Aon predicts that economic loss totals will continue to develop in the weeks and months ahead due to many large-scale and impactful climate events in March.

Demand for resiliency

In her speech, Tan said there is a demand for resilience capabilities, as well as opportunities for the insurance and finance sector amidst the rising cost of climate calamities.

The obvious danger that climate risk brings is that it will result in structural shifts to many firms’ riskreturn profiles.

“More frequent catastrophic events can cause severe impairment to business models, lead to substantial income and productivity losses, and make certain tail risks uninsurable, or insurable only at unaffordable rates,” Tan explained.

According to a research released by Swiss Re Institute, it was estimated that if no action on climate change is taken, Asia’s economy would be 26% smaller in 2050 whilst ASEAN’s economy would shrink by 37%.

“Asia’s insurance markets are growing, but the pace of growth will not be able to match the region’s growing protection needs from natural catastrophes. A distinct lack of high quality and standardised data to accurately quantify risk exposure for climate risks or to build reliable models also remains a key challenge,” Tan said.

Tan pointed out that countries, communities, and corporations are keen to build resilience capabilities across multiple dimensions – human, financial, operational, and technological. These are done through different methods, such as partnerships between insurers and tech players, to help widen the reach of insurance through a more accessible medium.

“Beyond these resilience capabilities, which all governments and corporates need to urgently develop, there will be opportunities for insurers and reinsurers to help build societal and corporate resilience and manage ever-present risks,” Tan said.

Green financing

For Tan, it is not enough to close the underinsurance gap. Insurers, themselves, must shift focus to greener financing.

Insurers provide risk financing, which is instrumental to the functioning of key sectors and infrastructure, including the energy and chemicals, aviation, and shipping sectors.

“Some of these sectors form a sizeable part of global and Asian economies but are not inherently ‘green’. Risk financing and insurance can be an important lever in engaging the relevant stakeholders and supporting a progressive low-carbon transition of these sectors,” she said.

Tan urged insurers to work closely with their clients in these sectors as part of the underwriting process. This will help them better understand and engage them on climate risk exposures, transition plans and pathways, and support them with risk management analytics and insights.

“Ideally, insurers should journey alongside clients so that they make concrete and progressive improvements in their environmental performance over time,” Tan said.

Some of these sectors form a sizeable part of global and Asian economies but are not inherently ‘green’

Top 5 most significant events in Asia Pacific

INSURTECH WATCH: GOALSMAPPER Why this SG-based fintech firm is ending the pen-and-paper era of financial advisors

GoalsMapper used its cloud-based platform to support more than 80,000 financial advisors.

GoalsMapper, a Singaporebased fintech software-asa-service firm, said that the pen-and-paper era for financial advisors and financial consultants should be over and done with as traditional methods lack the accuracy to cater to a client’s needs.

This was based on the experience of GoalsMapper co-founder Dato’ Wayne Chen. 14 years ago, Wayne was an independent financial advisor. During those times when he was offering his services to clients, he found it difficult to prepare materials that would accurately capture a client’s financial snapshot and instead found himself relying on a standardised presentation and script.

“Due to the lack of clarity of a client’s situation, the product that I recommend to them during a meeting might not be the best fit for them. What I have observed is that I will require more meetings with a client before getting the right solutions to them as I will require more time on the side to prepare calculations and materials in order to help clients visualise the possibilities in the solutions,” Wayne explained during a quick chat with Insurance Asia.

He quickly identified the problem: a lack of real-time digital tools. This was the spark that motivated him to build GoalsMapper.

The platform

To address and solve the traditional problems of financial advisors, GoalsMapper created three important products for its more than 80,000 users called GM Planner, GM Brand, and GM Connect.

The GM Planner is a financial planning tool with goals and scenarios projections via interactive charts that allow clients to stress test and visualise their portfolios. This means financial advisors can create a simulation of how clients’ can achieve their financial goals.

“GM Planner allows financial providers personalised financial

To address the traditional problems of financial advisors, GoalsMapper created the GM Planner, GM Brand, and GM Connect

Dato’ Wayne Chen

There is an urgent need to close the financial literacy gap for normal everyday people and the financial consultants

advisory, taking into consideration the client’s goals and different life scenarios,” Wayne explained.

Meanwhile, GM Brand was created to help the image of the financial advisor. It helps them create personalised websites in just a few clicks. Wayne added that GM Brand was tailor-fitted for financial advisors to help them enhance their brand and image.

The last product, GM Connect, helps financial advisors maintain communication with their clients. It helps automate post-sales engagements like premium reminders and policy reviews.

GM Connect is essentially a task manager that stores notes of appointments with clients, helps financial advisors remind clients about premium dates, and stay in communication with clients.

An interesting product they created was the recently launched GM Rewards. This product was created through the focus group GoalsMapper has created to get more ideas from platform users on how to improve their product.

GoalsMapper found out that a lot of financial advisors have difficulty giving tokens of appreciation to clients, especially on holidays. This is especially true for financial advisors who have between 100 to 300 clients.

“We came up with GM Rewards, where financial advisors can easily give gifts to their clients. The feature allows financial advisors to collate their gifting orders, customise it for clients, and coordinate delivery as well,” Wayne explained.

Expansion

Every year, since its inception, GoalsMapper expanded its reach from Malaysia, Thailand, and the Philippines. Most recently, it landed in Indonesia.

Wayne said they see a lot of potential for its Indonesian expansion because of its low insurance penetration rate at 3.23% and a financial literacy rate of 15.8% in the underserved market.

“There is an urgent need to close the financial literacy gap between normal everyday people and the financial consultants. We see a potential 600,000 life insurance agents that the platform could support,” Wayne added.