What Are the Costs of Buying or Selling a Home? Homeowners & Investors Need to Know

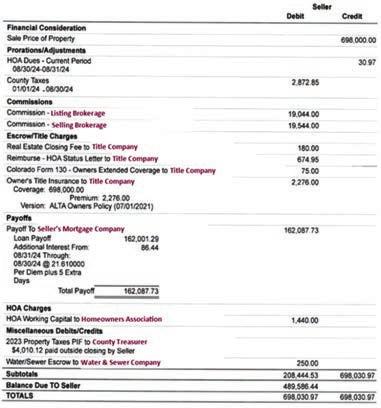

This is one article you’ll want to read at http://RealEstateToday.substack.com, where the buyer and seller settlement statements at right appear much larger on your computer screen. I have anonymized the actual closing statements from a property I sold for $698,000 this year which had an HOA, a seller loan to pay off, and a buyer loan to fund. This should cover most of the expenses that a buyer or seller might encounter when closing on a home sale or purchase.

We’re blessed in Colorado when it comes to the cost of buying and selling real estate. In many states, there are transfer taxes imposed by state or local jurisdictions, but not here by Colorado or in metro Denver. Also, in some states, both buyer and seller need to hire a lawyer, not just a real estate agent to complete a transaction. Long ago the State of Colorado passed a law giving licensed real estate brokers limited legal authority to explain state approved contracts, so it’s rare for a client to spend money on a lawyer. The exception is when a buyer purchases a new home, because builders have lawyers create their own contracts, and we would be practicing law without a license if we were to interpret those contracts and their provisions for our buyer.

ance renewal), but that escrow can't be credited on your closing. You’ll pay for the property taxes at closing and get a refund of your escrow balance from your lender 30 days or so after closing. On this seller’s settlement statement, the HOA dues are also pro-rated to the date of closing, and since the closing was on the 30th of August, the statement refunds two days’ worth of HOA dues, which the seller had paid on August 1st.

The biggest deductions for the seller (other than property taxes) are the real estate commissions and the title insurance policy. The purchase contract specifies whether the buyer or seller will pay for the buyer agent’s commission and the owner’s title insurance, but it is still common for the seller to pay both agents’ commissions plus the title policy, as in this case.

There are HOA fees which can also be paid by either party but are typically paid by the seller. Typically, the title company which is closing the transaction pays those fees (for status letter, documents, transfer fee, and more), so those fees are shown here as being reimbursed to the title company rather than paid to the HOA.

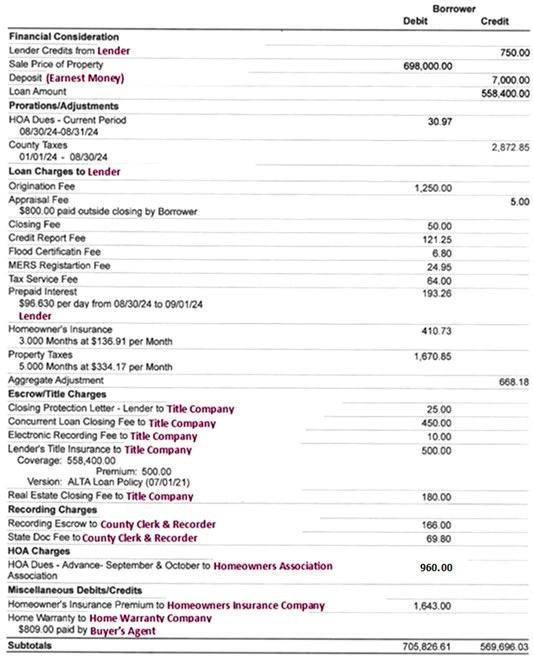

statement. If the buyer were paying cash, he or she would have very few expenses other than recording the deed for $10. The biggest costs associated with buying the home are related to the loan, especially if the seller has paid the buyer’s real estate agent and paid for the owner’s title policy.

So let’s look at the seller’s settlement statement first. Not all the debits on this statement are considered the cost of selling. For example, the property taxes for the current year, pro-rated to the date of sale, are not a cost of selling. Since property taxes are paid in arrears (not due until April of the following year), you’re always going to find that pro-ration of property taxes on the settlement statement. If selling in December, that’s almost an entire year’s tax bill. In January through April, if your taxes haven’t been paid, you will find the full year’s taxes plus a portion of the current year’s taxes deducted from your proceeds.

If you have a mortgage, your lender has probably been charging you each month to escrow for next year’s tax bill (and insur-

In addition to paying off the seller’s loan, based on payoff numbers the title company obtains directly from the lender, the closer will deduct a few extra days of interest to cover the time it takes to get the payoff to the lender. If that’s an overcharge, the seller will get a check for the surplus from the title company within a few weeks.

The title company will also escrow a few hundred dollars to pay the final water and sewer bill (unless water is included in the HOA dues), and will refund the excess after they pay the final water/sewer bill. This is the only utility which the title company pays and transfers on your behalf, because an unpaid water/sewer bill would result in a lien against the property, and the title company’s job is to assure the buyer that they are getting the home clear of any liens.

Now let’s look at the buyer’s settlement

Moving, Even Locally, Can Cost You a Lot

At Golden Real Estate, we like to save you money wherever we can. For example, we have a handyman who can help you get your home ready to show or fix inspection issues at a client-only rate of $30/hour.

We also have a box truck which you can use prior to, during and after closing, not just for moving to your new home, but making those dump runs or runs to Goodwill for donating all that stuff you accumulated over the years!

packing material, including bubble wrap, so don’t buy any of those items yourself.

We’ve been offering the use of this truck since 2004. In fact, this is our second truck. It’s hard to estimate how much money this perk has saved both our buyers and sellers, but it must be several hundred thousands of dollars.

We also provide free moving boxes and

We also make the truck available free to non-profits and local organizations, such as Family Promise and BGoldN, which uses it to pick up food from Food Bank of the Rockies for their Golden food pantry.

Those loan costs are large and varied, as is detailed in the buyer’s settlement statement above. There’s the origination fee, from which the loan officer is paid. There is also the cost of appraising the home (in this case paid prior to closing), underwriting, credit report, flood certification, and a couple other lesser fees.

The buyer’s lender wants to be sure the home is insured, so you see that debit on the last line of the buyer’s settlement. (A cash buyer might choose not to insure.)

Not only does the buyer have to pay all those expenses, the buyer is charged for a title policy that covers the lender for the amount of the loan ($500 in this case) and a loan closing fee ($450). The lender will probably want to escrow for property taxes and insurance and will require a deposit for both those expenses that will vary depending on when in the calendar year the clos-

Each year, the FHA raises the limits on its federally guaranteed loans. The limits are based on the median sale price of homes in each county.

Because the Denver metro area’s median home price was calculated by FHA at $710,000, the loan limit for single-family homes was raised to $816,500 this year. That is the loan limit, not the purchase price, although FHA only requires a 3.5% down payment.

The loan limit for a duplex/2-family home was raised to $1,045,250. For a three-family home it was raised to $1,263,500, and for a four-plex, it was raised to $1,570,200.

Boulder County’s limits in each category are slightly higher, starting at $856,750 for a single-family home.

In the country’s lowest-cost counties, the loan limit is $498,257 for a single-family home, and in the highest-cost areas (Alaska, Hawaii and the U.S. Virgin Islands), the limit is $1,724,725, rising to $3,317,400 for a 4unit property. (Whether 1-unit or 4-units, the borrower has to live in the subject property.)

ing takes place. In this case the buyer is being debited for 3 months of insurance coverage and 5 months of property taxes. There is one big credit which the buyer receives from the seller. The funds which were deducted from the seller’s proceeds for the current year’s property taxes are credited to the buyer, not paid to the county. That’s because the buyer will paying the current year’s entire property tax bill when it becomes due. You see that credit — almost $3,000 — near the top of the above settlement statement.

There could also be a concession for repairs that the seller agreed to in the inspection resolution, although not in this case. Sometimes that concession takes the form of a price reduction, which does not appear as a line on the settlement statement.

Notice that the closing services (notary) fee of $360 is shared 50/50 in this case, as is commonly done, $180 for each party. As mentioned above, visit our blog for more readable copies of those documents and more discussion of transaction costs.

Non-FHA (“conventional”) loan limits are slightly lower for 2024. In most areas, the conforming conventional loan is limited to $766,550. Alaska, Hawaii and high-cost areas have a conforming conventional loan limit of $1,149,825 for a single-family home.

FHA loans are attractive because they only require a 580 credit score (as low as 500 with a 10% down payment), and your debt-toincome ratio only needs to be below 57%.

The biggest negative of FHA loans is that they require a mortgage insurance premium (MIP) of 1.75% at closing, plus an annual premium which varies based on your loan-tovalue ratio. MIP is for the life of the loan, unless your downpayment is at least 10%, and remains in effect no matter how low the loan-to-value ratio falls (i.e., how much your equity increases). If your down payment was 10% or higher, the MIP goes away after 11 years. Otherwise, most 15- or 30-year FHA mortgages should be refinanced once the owner can qualify for a conventional loan, hopefully at a better interest rate, to get rid of the MIP.

George “Ron” Ronald Neely

April 7, 1936~ November 28, 2024

George Ronald Neely, beloved husband, father, grandfather, great grandfather, uncle, and friend, passed away on November 28, 2024. He was born in Ogallala, Nebraska, on April 7, 1936, along with his twin brother, Don, to Glenn and Mary Ann Neely. e family lived in Nebraska for a brief time before moving back to Colorado when Ron’s father found work as a meat cutter in Ft. Lupton. e Neely family then settled on Ron’s grandfather’s farm in Wattenberg, where Ron spent much of his childhood.

coach and junior high sports coach. Ruth continued her nursing career in Burlington, Colorado. ey purchased and moved into an 8’x42’ trailer, as housing was scarce in the area. Teaching and coaching in Stratton presented challenges, but Ron’s coaching made a lasting impact on the students, and he was proud of their team successes and achievements.

Growing up on the farm was a formative experience for Ron, as he worked alongside his grandfather and great uncle farming with horses. e family had three teams of horses, and limited use of tractors, making it a truly hands-on, oldfashioned farming life. Ron and his twin brother attended Wattenburg Elementary School through the 8th grade before moving on to Ft. Lupton High School, where they graduated in 1954. Both were active in athletics, playing football, basketball, wrestling and track. Ron and Don both played on the 1953 state championship basketball team and then the 1954 state runner-up team.

During the summer months, Ron and Don helped their parents in the family-owned grocery store, Neely’s Grocery, in Commerce City. ey also worked on the Stieber farm during the haycutting season, where Ron learned the value of hard work, family and community.

After high school, Ron attended Colorado State University (CSU) on a basketball scholarship for a year before transferring to the University of Northern Colorado (UNC). While in college and during summer he worked part-time at the Safeway warehouse, spending 13 years in the frozen food department.

In 1955, Ron met Ruth Ann Dahl on a blind date arranged by his brother, Don. ey dated for two years before marrying on June 8, 1957. June 8th was a signi cant date for Ruth’s family, as it was the wedding anniversary of Ruth’s grandparents, parents, aunt and uncle, Ruth’s younger sister, Pat, and then their daughter Pam.

After Ruth completed her nursing program at St. Luke’s Hospital and University of Denver in the spring of 1957, the newlyweds moved to Greeley. Ron then continued his studies at UNC and Ruth began her nursing career at Weld County Hospital. In the nal two years of college, Ron worked as an evening manager at Gordon’s Downtown Food Liner.

After he graduated in 1959, the couple moved to Stratton, Colorado. Ron began his teaching career as a high school science teacher, varsity wrestling

In 1961, Ron and Ruth celebrated the birth of their rst child, Jerry. at same year, they left Stratton and moved to Prospect Valley. Ron taught high school biology and chemistry and coached wrestling at Weld Central High School. e family later moved to Brighton, where Ron continued teaching science and coaching wrestling, football, and track at South Junior High (now Vikan Middle School). Over these years, the family grew with Sherry, Greg and Pam joining Ron and Ruth’s home.

In 1967, Ron transitioned from the classroom to the assistant principal role, serving in that capacity for seven years before becoming the principal of Vikan Middle School. In 1971, Ron earned his master’s degree in Secondary Education from Adams State University. He served as principal until his retirement in 1991.

During retirement, he enjoyed spending his time in various hobbies, including traveling the world, hunting, shing, wood working, gol ng and decorating for holidays. He spent many days building elaborate holiday displays, especially for Christmas, with sixteen wooden reindeer and a gingerbread cottage populated by Santa’s elves. Ron also loved attending athletic events, never missing a family member’s game. He was in almost every high school and college gym in Colorado following his children and grandchildren to hundreds of basketball games. He also endured numerous freezing and scorching softball, baseball, and football games and track events. If they played, him and Ruth were going to attend. He enjoyed spending time with his grandchildren talking about school and sports. He was very proud they all received college degrees and with all their athletic success.

Ron is preceded in death by his parents, Glenn and Mary Ann Neely, his wife, Ruth and twin brother, Don. Ron is survived by his four children Jerry (Deb) Neely, Sherry (Tim) Barnard, Greg (Sandy) Neely, Pam Smith, along with six grandchildren Alexandra (Omar), Curtis (Ashley), Caitlyn, Kylie (Trent), Courtney, Mick, one step-grandchild Stephanie (Zach), three greatgrandchildren Audra, Nakoa, Henry, one stepgreat-grandchild Trace, his sister-in-law Patricia Lambert and by many nieces, nephews, cousins and close friends who will miss him deeply.

as 1 day! Affordable prices - No payments for 18 months! Lifetime warranty & professional installs. Senior & military discounts available. 1-877-5439189

Become a published author We want to read your book! Dorrance Publishing trusted since 1920. Consultation, production, promotion & distribution. Call for free author`s guide 1-877-7294998 or visit dorranceinfo.com/ ads

Miscellaneous

Prepare for power outages today with a Generac Home Standby Generator. Act now to receive a FREE 5-Year warranty with qualifying purchase* Call 1-855948-6176 today to schedule a free quote. It’s not just a generator. It’s a power move.

Jacuzzi Bath Remodel can install a new, custom bath or shower in as little as one day. For a limited time, waving ALL installation costs! (Additional terms apply. Subject to change and vary by dealer. Offer ends 12/29/24.) Call 1-844-501-3208

Home break-ins take less than 60 seconds. Don’t wait! Protect your family, your home, your assets now for as little as 70¢/ day! 1-844-591-7951