Desiree Solomon and Jasmine Payne

September 2022

Desiree Solomon and Jasmine Payne

September 2022

The Black Dollar Part 2: Cooperative Black Economics in the U.S. CENTER FOR POLICY ANALYSIS AND RESEARCH Economic Opportunity

Desiree Solomon and Jasmine Payne

September 2022

The sum is better than its parts. Throughout history, Black communities have collaborated to sustain themselves and their economies. Millions of enslaved Africans were brought to the United States for generations of forced labor, deprived of the ability to read, write, and support themselves. The freedom to collectively organize was constrained during the trans-Atlantic slave trade. Despite generations of forced migration and intentional disruption of community building, the African diaspora in the United States facilitated cooperative systems to supply community needs and improve their outcomes. Descendants of enslaved Africans in the United States inherited a legacy of collectivist cultural practices and created systems of support to learn trades, escape enslavement, and forge a path to economic independence. Through the wit and innovation in their communities, Black Americans crafted economic networks to combat structural blockades to the pursuit of happiness. Often defined as the pathway to financial success, Black Americans are impeded from attaining this dream through barriers to homeownership and education by systemic policy that perpetuates the American caste system. Despite oppression, Black communities have built systems to create wealth and gain financial independence. These same practices can be applied to facilitate economic prosperity among Black communities today. Surveying collectivist characteristics of Black economies traced back to indigenous African cultural roots and cooperative movements in modern Black history reveals the power of the Black dollar and empowers Black Americans to wield this power with intention.

CPAR

Black Dollar: Cooperative Economics

CPAR

Black Dollar: Cooperative Economics

The sum is better than its parts.

Throughout the 1500-1900s, African people groups were placed in bondage and trafficked across the Atlantic to the Americas. While the trans-Atlantic slave trade shifted the nucleus of international trade to the western hemisphere, colonial hegemons grew more powerful due to free labor and large-scale commodity production. Western Europe and the wealth of its colonies skyrocketed while mercantilism prevailed, and colonizing states circulated currency inward. Forced labor of enslaved Africans distributed wealth among the antebellum south, plantation states, the United States at large, and among growing global economic sovereigns. The United States shifted from being a small infant national economy to a burgeoning market economy on the world stage establishing global economic power structures that remain to this day.

Determined to achieve liberation and financial security, solidarity remained, and cooperation amongst plantation communities thrived in the development of microeconomies. Black Americans persisted by working together to teach themselves trades, forge alliances, and educate themselves; “African Americans as an example—people who

didn’t own their own bodies, didn’t own their labor, weren’t paid—were totally exploited. Yet, on the one day they had off, on Sunday, they would farm small gardens together. Some hired themselves out if they had skills. They found alternative ways to make sure they could feed their families and have some dignity” (Nehmbard, 2014). Communities would acquire goods and skills for themselves to trade.

Collectivist practices abounded; and despite the subjugation and segregation of Black Americans, cooperative economic systems developed swiftly. Sometimes within a plantation, enslaved African communities would embolden themselves—working together to supply mutual needs, purchase another’s freedom, and exchange goods. Small networks emerged to facilitate the exchanging of goods and services. Political Economist Jessica Gordon Nehmbard writes, “all subaltern or marginalized, oppressed people actually, when they think about it, can not only consolidate their own culture and strengthen it, but can also create an economy that will work for them, especially in the face of economies and systems that don’t work for them” (Nehmbard, 2014). Enslaved Africans provided labor that included domestic service, artisanal trades, and agricultural labor. While slave owners used these profits to expand their landholdings and purchase more enslaved Africans, intentional communities emerged within slave plantations. They became communities that invested in each other, teaching and perfecting trades and contributing those skills to a developing micro-economy.

Literacy was an essential skill in the journey to freedom and economic liberation. Extralegal suppression was rampant and new laws emerged to deliberately quell organizing. As early as 1740, states began formally passing slave literacy prohibition laws to stop cooperation. Literate enslaved Africans would provide services to uplift their communities; 1 however, the literacy rates dropped significantly after these prohibition laws were passed, presenting a challenge to communicating between groups.

1 South Carolina Passes Negro Act of 1740; Codifying White Supremacy https://calendar.eji.org/racial-injustice/may/10

CPAR | The Black Dollar: Cooperative Economics

CPAR | The Black Dollar: Cooperative Economics

Black Americans persisted by working together to teach themselves trades, forge alliances, and educate themselves.

In the absence of formal education, slaves in both the rural and urban South often found alternative paths to learning. On plantations, the pursuit of education became a communal effort—enslaved Africans learned from parents, spouses, family, and community members. Some were even personally instructed by their masters or hired tutors. Slaveholders were motivated by Christian convictions to enable Bible-reading among enslaved groups and even established informal plantation schools on occasion in part because of slaveholders’ practical need for literate slaves to perform tasks such as record-keeping. (Thirteen, N.d.)

The table below depicts the importance of literacy in escaping slavery.

Literarcy Characteristics of Literate Runways in Colonial America as Reported by Their Owners, 1730–1776

Colony Read only Write only Read and write Virginia 30.9% 7.3% 61.8%

South Carolina 30.1 69.2 Massachusetts 14.8 5.7 80.0 Pennsylvania 19.0 7.1 73.8

New York 20.0 10.0 70.0

Source: Inter-Colonial Runway Slave Database.

An enslaved African who could read and write could prepare a forged indenture agreement or runaway notice 2 to aid the safe escape of community members. A clear connection between literacy and freedom emerged in a strategy of survival networks. The circulation of Black resources and consequently the Black dollar began to spread beyond the confines of plantation communities, impacting the lives of other indentured servants and white allies. The foundation of economic cooperation among Black communities was not currency based at all. But instead founded in collectivist traditions of mutual aid and intentionally planned cooperative efforts towards freedom.

2 An agreement that establishes who owned what, who borrowed and who sold their property, who worked for whom, who crafted relationships and who had power and who did not. “They narrate the colonization, speculation, and development of land. They tell us how individuals were involved in the slave trade and how money moved across time and space” (Newport Historical Society, N.d)

CPAR | The Black Dollar: Cooperative Economics

Literacy and exchange networks afforded empowerment and posed a real fiscal threat to the antebellum south and state economies. These cooperative structures expanded and developed entities that were pivotal to abolition and freedom. “From mutual aid societies that bought enslaved people’s freedom to the underground railroad network that brought endangered Blacks to the north, cooperative structures were key to avoiding white supremacy” (Nehmbard, 2014). These initial systems of cooperative economics reflect African cultural collectivist traditions.

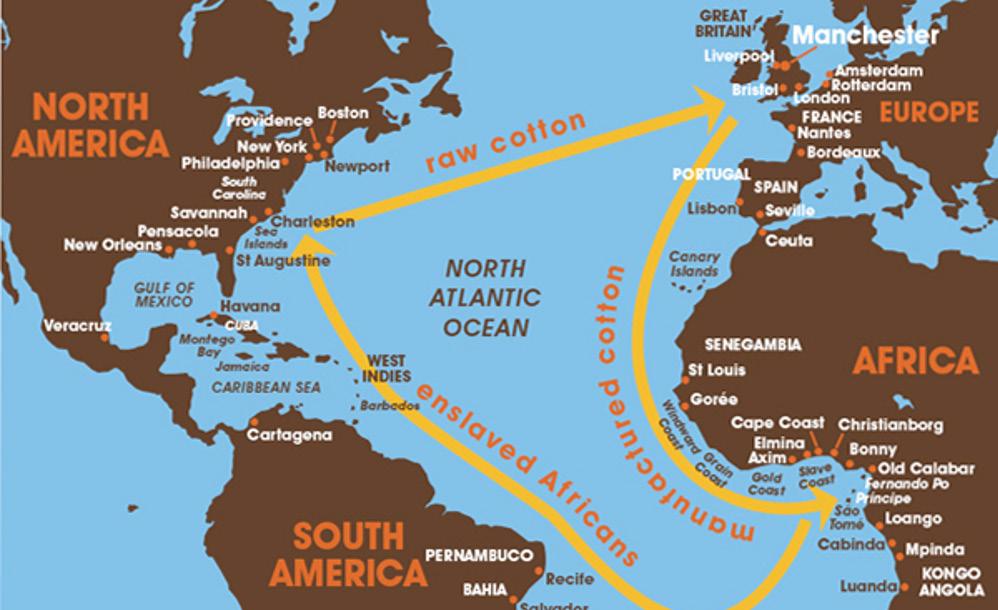

Slave labor financed and propelled the westward expansion. The antebellum south’s economy was dependent on loans backed by enslaved Africans. Planters would leverage enslaved Africans to acquire loans, often called slave mortgages. 3 The westward expansion began with the purchase of Louisiana in 1803, which itself was made possible by Haitian uprisings during this period. The abolition of slavery in France and successful slave uprisings in Haiti degraded King Napoleon’s colonial hold in Haiti and served as a

3 In colonial times enslaved people were used as collateral for mortgages, allowing the lender the right to take the enslaved person if the debtor failed to repay a debt (Nicolaci da Costa, 2019).

Black Dollar: Cooperative Economics Source: National Park Service What is the Underground Railroadcatalyst propelling the sale of the Louisiana Territory to Thomas Jefferson. As the U.S. territory expanded, the government overhauled its administration of the newly acquired territories and faced stark opposition. Northern states wanted abolition and southern states exceedingly relied on the slave economy.

The free labor of enslaved Africans was critical in the development of the modern U.S. economy and the fight for abolition resulted in civil war due to the economic implications of emancipation. The weight and influence of Black labor was so heavily felt that the issue of slavery led to the American Civil War. The consequences of the American n Civil War unraveled both domestically and abroad as the production of a fundamental commodity hung in the balance, cotton. Cotton rose to prominence in U.S. trade exports, constituting 61% of the value of all U.S. products shipped abroad (Yu, 2014). The U.S.’s major trade partners were internal mercantilist in nature. This meant that the changes to the U.S. cotton market directly impacted Western Europe;

“By the late 1850s, cotton grown in the United States accounted for 77 percent of the 800 million pounds of cotton consumed in Britain. It also accounted for 90 percent of the 192 million pounds used in France, 60 percent of the 115 million pounds spun in the Zollverein, and 92 percent of the 102 million pounds manufactured in Russia” (Yu, 2014).

The stall of cotton production impacted jobs abroad as well. According to University of Liverpool historic records , “the manufacture of cloth and thread was Great Britain’s largest industry in the mid-nineteenth century, employing more than 600,000 people in England directly, indirectly one-sixth of the English population, were dependent on cotton for their livelihoods” (Williams, Et al., Nd). Plantation labor drove the production of major commodities during this time and inventions such as Eli Whitney’s cotton gin, propelled the industrialization of agricultural trade and the integrated Atlantic economy.

The United States was quickly swept into a civil war at the onset of the Lincoln presidency when several southern states moved to form the confederacy to protect southern economies. A division decidedly based on the economic value that the slave labor system afforded the antebellum south. The American Civil War ensued in a defining

CPAR | The Black Dollar: Cooperative Economicsmoment for the United States taking place from 1861to 1865 and was the deadliest war in American history.

Source: College of Charleston Digital History Initiative https://ldhi.library.cofc.edu/exhibits/show/liverpools-abercrombysquare/britain-and-us-civil-war/impact-cotton-trade

“If slavery was the corner stone of the Confederacy, cotton was its foundation. At home its social and economic institutions rested upon cotton; abroad its diplomacy centered around the well-known dependence of Europe…upon an uninterrupted supply of cotton from the southern states.” – Frank L. Owsley Jr.

In 1863 President Abraham Lincoln issued the Emancipation Proclamation , formally abolishing slavery in each confederate state. The United States Congress made progress in acknowledging and legally protecting Black Americans’ rights and passed the Thirteenth Amendment in 1866, and consequently ratified the Fourteenth Amendment redefining birthright citizenship and the enfranchisement of descendants of African

CPAR | The Black Dollar: Cooperative Economicsslaves. During this period, the United States government aimed to reintegrate the southern states into the Union, but the legal status and rights of Black Americans were not fully protected. Major existential changes pervaded the Black communities through this era of reconstruction.

For centuries, Black Americans made incremental progress in economic advancement, but the social response to the Reconstruction Era exacerbated previous challenges and created new roadblocks, establishing systemic barriers to hinder and undermine success. One of the most insidious methods was through Jim Crow Era policies and Black Codes. A pivotal event that helped to shape these policies was the Compromise of 1877 in which Democrats agreed to the Republican demand of ending their postcivil war occupancy in the South in exchange for Democratic candidate, Rutherford B. Hayes, becoming president. On February 26th, at the Wormley Hotel, a Black-owned, internationally renowned venue patronized by dignitaries and political delegations, the Compromise of 1877 was signed. Policies resulting from the Compromise revoked rights for Black Americans, including James Wormley the owner of the hotel, William Wormley, and made southern Black communities more vulnerable to attacks by southern whites in favor of the confederacy. Democratic politicians who controlled state governments in the South wanted to see Blacks in conditions as close to subservience as legally possible. Contrasting Wormley’s successful hotel, the impacts of the agreement disrupted Black business interactions and interstate travel as Black Americans were not permitted in many white establishments causing long-lasting effects that ushered in the Nadir Period of the Jim Crow Era from 1890 to 1920 (National Museum of African American History and Culture, n.d.).

In 1896, the U.S. Supreme Court’s Plessy v. Ferguson legalized segregation. Despite the advancements of the Reconstruction, the Nadir period ushered in an era of harsh quasilegal discrimination and subjugation. This period was characterized by horrendous violence, lynching, and racial terror;

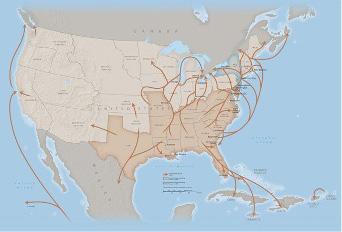

CPAR | The Black Dollar: Cooperative EconomicsAlthough Black Americans were legally freed, this did not stifle the white American majority’s attempt at controlling movement, voting, and other means of life. “Separate but equal,” segregation reigned supreme and echoed from education and work opportunities to real estate communities legally stifling Black American financial progress. In pursuit of a more just way of life, Black communities embarked on the largest documented organized wave of migration since that of the underground railroad. This Great Migration took place from 1916 to 1970 when six million Black Americans from rural Southern states moved to urban Northern states to escape racial violence and pursue educational and economic advancement. The migration of Black communities during this period filled a critical labor gap during World War I and World War II while simultaneously weakening southern economies. Moving in large networks, migrant Black communities established community welfare groups. Among these, faith communities thrived as pillars in economic cooperation as the Black Church and Mosque communities served as welfare centers, and schools, and in some instances provided loans to members.

Historians and economists often reference the development of the Black Church as a point of change in Black cooperative economics. The Black Church is heralded as a central location for the exchange of goods, services, and community investment. W.E.B. Dubois states, “it was in the church, too, or rather the organization that went by the name of church, that many of the insurrections among the slaves from the sixteenth century down had their origin; we must find in these insurrections a beginning of co-operation which eventually ended in the peaceful economic cooperation” (Dubois, 1868). Black church leaders served in the financial development vanguard in setting up Community Development Corporations—community-based, community-controlled entities of empowerment Congregations and coalitions of congregations entered business together, and these faith communities began to purchase property, and build community wealth. These church-based coalitions circulated resources and provided jobs for example, “One Baltimore shipyard, financed by a church, built small cargo ships for 20 years (Clay and Wright 2000). Opportunities Industrialization Centers—an international network of job

CPAR | The Black Dollar: Cooperative Economics“Lynchings reached an all-time high during this period and were often the result of “minor “offenses”—talking back, having too much money, failing to be deferential. Lynchings were economic acts, acts of economic envy. And the economic legacy of lynching is seen in today’s wealth gap” ( Malveaux, 2021 ).

training and business development—created cooperative group information networks and provided opportunities to congregate and craft liberation strategies.

The Mosque, quite similarly, served as a mainstay for Black wealth and community planning. Elijah Muhammad led this effort through the economic programs of the Nation of Islam (NOI). In 1954, Muhammad introduced the Three-Year Economic Plan (National Savings Plan) identifying methods to achieve economic prosperity. The plan called for united spending habits, fiscal discipline, and solidarity.

Under this plan, he urged Black communities to sacrifice for three years where they could only purchase up to three suits a year never to exceed $65 in cost. A pair of shoes could not exceed $16 in cost. He urged Black communities in America to spend only according to their income and save money (Muhammad, 2010).

The funds saved during this three-year period were to be allocated to a community economics savings program. Muhammad’s plan was to redistribute this wealth into the Black community in an equitable way. The Nation of Islam founded numerous businesses throughout the United States. These businesses served as all elements of a community’s need. Muhammad consistently and famously took the stance that internal change was the path to financial liberation; “We do not believe that America will ever be able to furnish enough jobs for her own millions of unemployed, in addition for jobs for 20,000,000 Black people” (Muhammad, 1965).

CPAR | The Black Dollar: Cooperative Economics

CPAR | The Black Dollar: Cooperative Economics

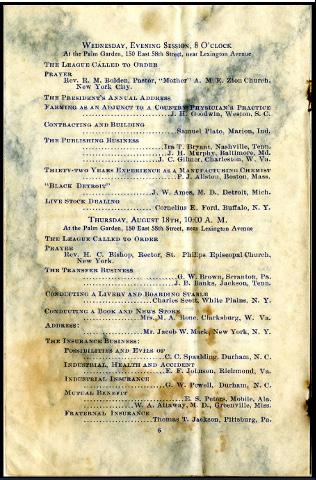

Black leaders sought unity through organization and worked to create organizations such as the National Association for the Advancement of Colored People (NAACP) in 1909 and the National Negro Business League in 1900 (National African American Museum of History and Culture, n.d.). Four other core civil organizations emerged as leaders of the Black liberation movement, The National Urban League in 1910, The Congress of Racial Equity (CORE) in 1942, the Southern Christian Leadership Council (SCLC) in 1957, and the Student Nonviolent Coordinating Committee (SNCC) in 1960. These produced beneficial partnerships where Black scholars enlightened students, journalists informed citizens through the Black press, Black business owners provided needed goods and sponsored initiatives, and the community supported the businesses. After emancipation, economists and civil rights activists wrote about the collective strength found when a culture bans together to take care of its own and be self-sustaining. Black leaders such as W.E.B. Du Bois, Booker T. Washington, and Ida B. Wells furthered the concept of cooperatively uniting for advancement and believed that education and political agitation were the best ways for Black Americans to achieve progress.

Source: National Negro Business League, https://www.jstor.org/stable/community.31983315

Jim Crow Era policies worsened conditions for Black communities spurring a shift to selfpreservation; therefore, the Nadir Period was characterized by disillusionment as people shifted from external advocacy in Reconstruction to internal improvement and self-help (National Museum of African American History and Culture, n.d). The period caused a pivot from concentrating on financial growth post-slavery to survival. Jim Crow Era activities

CPAR | The Black Dollar: Cooperative Economics“To be a poor man is hard, but to be a poor race in a land of dollars is the very bottom of hardships” (Dubois, 1903).

became more violent with lynchings and insurrections. White and Black relations worsened and disrupted the progress of flourishing Black collectives. Two paramount instances occurred in Wilmington, South Carolina and Greenwood, Oklahoma during a period known as the Red Summer of 1919. Wilmington, South Carolina was heralded as “the most progressive city in the post-emancipation South” due to the relative equality and integration with Black leaders in municipal government and public service jobs such as firefighters and police. In 1898 that changed as white businessmen grew infuriated with Black political and economic competition. To regain power and concentrate wealth, white businessmen began a coup and massacred many in the Black community (Ward, 2022). Nearly 20 years later, a similar situation occurred in the Greenwood district— a Black community in Tulsa, Oklahoma. In 1921, the commercial district many recognize as “Black Wall Street” housed 108 Black businesses, hotels, movie theaters, newspapers, nightclubs, libraries, schools, and restaurants. Greenwood had Black leadership and epitomized Black excellence amidst segregation as an independent Black city within a hostile white Tulsa. After an alleged rape case turned into an attempted lynching, white Oklahomans stormed Greenwood killing at least 300 people and destroying more than 1,000 Black homes and businesses during the 18-hour riot (Ruffin, 2021). According to the Tulsa Race Riot report describing people walking into Black Wall Street after the insurrection, “what they found was a blackened landscape of vacant lots and empty streets, charred timbers and melted metal, ashes, and broken dreams. Where the African American commercial district once stood, was now a ghost town of crumbling brick storefronts and the burned-out bulks of automobiles” (Tulsa City-County Library, n.d.). Massacres like Wilmington and Greenwood arose all over the country in 1919 as the “Red Summer” was coined to describe the period of violence in Washington, D.C., Chicago, Illinois and Elaine, Arkansas.

The terrorism that ensued during the Red Summer inspired further community organizing. According to historians:

“[t]he Red Summer of 1919 did not intimidate African Americans into submission, as their tormentors had hoped. Instead, African Americans emerged from the violence of the bloody year with a greater sense of shared purpose, identity and pride, which served as a vital foundation for the civil rights movement to come” (National World War I Museum and Memorial, n.d.).

The influx of Black veterans returning from war was a major catalyst of Black unity through Red Summer and similar periods of violence. Black soldiers enlisted in the military to acquire all the most important liberties of citizenship—the right to defend their families,

CPAR | The Black Dollar: Cooperative Economicsearn respect and to provide financial support to their communities. They refused to allow the riots to obstruct their efforts to secure a new life back at home in America. Black veterans who returned home from war were frequently perceived as a threat resulting in white rage that invoked the riots; whites feared that returning Black veterans would be dangerous to them because they were military trained, living abroad with more rights and knowledge and would not be willing to resubmit to traditional discrimination and subjugation (Archives.org). These fears manifested as Black veterans demanded respect for their service and refused to be relegated to marginal treatment. They trooped together with Black business owners and residents to create a resistance against white attacks on their communities. The presence of a Black soldier in uniform was so alarming to white Tulsans that the first shots in Tulsa occurred because a white man tussled with a Black soldier holding a rifle in efforts to prevent a lynching (Tulsa City-County Library, n.d.). Irrespective of the germ of the riots, Black veterans fought in various cities defending the communities they built.

Following the riots, violence shifted from physical to more de jure or by law tactics. Black communities were blocked from homeownership, education and banking systems that cemented boundaries between racial groups. Lynchings and other physical violence continued to prevent physical work and invoke emotional distress, but barriers erected through policy slowly disenfranchised Black communities in discreet methods that were more difficult to prove and disband. Consequently, the policies and their effects remain today.

Great economic disparities between Black and white communities in the U.S. persisted throughout history and are systemically perpetuated in the American caste system through education and homeownership, two major economic drivers. In discussing Du Bois’ assertion that a “somber veil of color” exists in the United States, scholar Angela Simms says that “this curtain’s threads are the interconnected barriers White-controlled

CPAR | The Black Dollar: Cooperative Economics

CPAR | The Black Dollar: Cooperative Economics

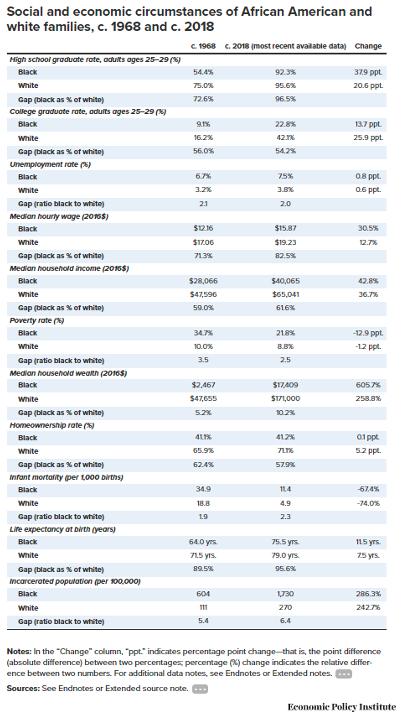

Source: (Economic Policy Institute, 2018) https:// www.epi.org/publication/50-years-after-the-kernercommission/

government and market institutions erected to prevent Black people from realizing their citizenship rights on equal terms with White Americans” (Simms, 2019). The impacts of these barriers are reflected in Black homeownership rates. In 1968 a commission was formed to assess social and economic equity in the Black community, the group was called the Kerner Commission.4 In its concluding findings, the Kerner Commission found that racism led to unemployment and housing discrimination. In a report detailing the socio-economic progress of the Black community since 1968, Economic Policy Institute (EPI) found that many U.S. housing policies remained inequitable. In addition, Black homeownership rates have remained almost the same between 1968 and 2018 with 41.1% in 1968 and 41.2% in 2018. In contrast, white homeownership increased 5.2 percentage points up to 71.1%. The diagram below further illustrates the juxtaposition.

The stagnation in homeownership was largely due to redlining and white flight from Black communities. The Home Owners’ Loan Corporation (HOLC) used real estate data to grade neighborhoods from A to D. Communities received a “D” based on explicitly racist criteria as “D” areas were “hazardous” and had “undesirable population or infiltration of it.” As a result, the Federal Housing Administration (FHA) refused to provide insurance for home loans. This became known as redlining due to the red outlines for communities graded a “D” (Miltko, 2020). Consequently, Black families could no longer buy homes unless they possessed large sums of cash to pay for the homes and white families were financially discouraged from buying in these communities with an FHA loan. When Black families moved into white neighborhoods, often white homeowners would move due to racist beliefs and the fear

4 The Kerner Report. (1968). Google Books. https://books.google.com/books?id=-qrPCgAAQBAJ&printsec=frontcover&d q=the+kerner+report&hl=en&sa=X&ved=0ahUKEwjIn8Tb0pnZAhWIl-AKHVGYCtQQ6AEIJjAA#v=onepage&q=the%20 kerner%20report&f=false

CPAR | The Black Dollar: Cooperative Economicsthat their home value would depreciate. Communities flipped from predominantly white to predominately Black in a process known as white flight. When white residents left, they took community resources with them as their homes were valued higher and produced property taxes to support public goods.5 At times white property owners maintained their real estate property as landlords and sellers with predatory conditions that cost Black renters and buyers more. Black families were required to pay for upkeep, repairs and taxes in agreements called installment land contracts (ILCs) or rent-to-own housing contracts. Black communities leaned on each other even more to survive the soaring prices amidst limited opportunities for good-paying jobs to compensate. Without the funding for public goods that white community members received, Black communities were forced to pool resources and have multiple generational or multi-familial homes for survival and protection. To combat ILCs, a group of Black Americans, socially progressive Catholics and white college students formed the Contract Buyers League (CBL). They organized and sued homeowners for unfair laws. Their efforts contributed to the end of redlining and pressured sellers to permit the renegotiation of ILCs. Coupled with the passage of the Fair Housing Act in 1968, these efforts made home-buying more accessible. Redlining, white flight and other discriminatory civil rights era lending practices continue to constrain Black wealth. The integration difficulties due to decades of housing segregation and inconsistent home valuation continue to pose a challenge to Black homeownership.

More recently, Black homeowners’ pre-existing vulnerability exacerbated financial challenges during the Mortgage Crisis of 2008. The crisis led to 3.5 times higher foreclosure rates in Black neighborhoods than in white neighborhoods from 2005 to 2009 (Loh, 2020). This risk is especially perilous for Black families, as homeownership is a major component of wealth. Redlining and white flight begot racist perceptions leading to the devaluation of Black homes today. Still, homes in predominantly Black neighborhoods are valued $48,000 less than white neighborhoods which is a cumulative $156 billion in equity loss (Perry, 2020). Additionally, the average home devaluation in Black communities is over 22% and homes in areas that have at a plurality of Black residents are valued at half of those with no Black residents (Perry, 2018). The home valuation disparity directly contributes to the

CPAR | The Black Dollar: Cooperative Economics 5 The presence of white neighbors sometimes presented a level of security. In Tulsa, Oklahoma, the Black homes intermixed with white homes were spared because white rioters did not want to burn down white-owned homes. (Ruffin, 2021)Black wealth disparity with housing as the largest asset and the biggest factor in a wealth portfolio for most homeowners. The slow rate of growth often varies between white and Black neighborhoods as well. The Department of Housing and Urban Development found that the homes of high-income white families appreciate an average of $4,460 per year while homes of low-income minorities appreciated only $1,712 per year (Department of Housing and Urban Development, 2004). Further exacerbating these disparities is the lack of Black appraisers. Studies find that only 2% of appraisers are Black (Neal, 2021). The history of redlining and designating Black neighborhoods as too risky to lend still cripples credit scores and wealth (Mitchell, 2018). The lasting impact of these issues are present in community infrastructure and public goods such as schools.

Housing is important not only as a critical part of security and survival but because it funds public education. Public schools rely on property taxes and government funding to fund school systems (Ray, 2021). While governments have formulas that attempt to create equal funding per student in school districts, the amount of funding per student varies depending on the amount of property tax that can be distributed per student in a community. Considering the devaluation of home values in primarily Black communities, less money is distributed to Black school districts funded by the housing taxes. As a result, this influences the amount and quality of teachers, resources, and cocurricular opportunities. Hindering homeownership directly affects the next generation of Black Americans and stifles socioeconomic mobility that perpetuates the cycle of barriers to homeownership (Simms, 2019).

Strong education systems are also pathways for wealth building, thus limited educational resources can hinder Black students. In 2018, the EPI found improvements in Black education with 90% of Black Americans graduating from high school by age 29 than the previous 56% in 1968. Today, Black Americans are also more than twice as likely to have a college degree than in 1968 (Jones, 2018). Yet, Black Americans are half as likely to have a college degree than white Americans. School integration has a crucial effect on education outcomes as historically resources were typically only available for white students. In many states, school integration was the primary pathway toward education equity as segregated

CPAR | The Black Dollar: Cooperative Economics

CPAR | The Black Dollar: Cooperative Economics

schools lacked resources and infrastructure for students to thrive. Scholars found that “residential segregation facilitates the extraction of wealth and other vital resources that fuel economic and social mobility. The loss of wealth in Black communities hastens a downward socioeconomic spiral” (Ray, 2021). The lack of resources is seen starkly in funding in nonwhite school districts. Predominately Black, Latin[e]6 and Asian school districts receive $23 billion less than white districts (Ed Build, 2019). According to the Brookings Institution, this difference equates to Black students being seven times as likely to attend high poverty schools than their white counterparts (Loh, 2020). As Black communities strived to attain equal education access, they worked cooperatively to use education as a vehicle for economic mobility and to redistribute wealth back into their communities.

A direct way to contribute to the Black community is to support Black businesses. Black businesses support their larger community as they tend to employ Black workers. This income extends to employees’ families and community systems (Stoll, 2001). Black businesses can also produce generational wealth by equipping their children with an inheritance of skills. Family members participate in the business based on a communal connection and familial bond wanting their whole family to prosper. Black children develop lifelong experiences, learn business processes, and establish built-in mentors through family members preparing them for succession (Jackson, 2016). Historically in Tulsa and other communities, Black business owners gave back to their communities through philanthropic community support and donating meeting space. More recently, Black business owner Robert F. Smith founder of Vista Equity Partners paid $34 million to cover the debts of the Morehouse College Class of 2019 stating, “On behalf of the eight generations of my family who have been in this country, we’re going to put a little fuel in your bus. This is the challenge to you, alumni. This is my class — 2019. And my family is making a grant to eliminate their student loans.” In addition, he gave $50 million to launch the Student Freedom Initiative, a project to help students from minority-serving institutions enter diverse work opportunities unburdened from student debt (Morehouse College, n.d.). Smith’s donation exemplifies financial success, leadership, and the importance of reinvesting in one’s community.

CPAR | The Black Dollar: Cooperative Economics 6 A 21st century gender-neutral alternative to Latina or Latino and used to describe a diverse group of people who have roots in Latin America.Despite the positive impact of Black businesses on the Black community, too few remain. Black Americans own less than 2% of businesses (Weller, 2021). Further, Black-owned businesses’ median annual revenues are a seventh ($125,371) of white businesses (Crawford, 2020). Many factors contribute to low business ownership rates among Black Americans. Black entrepreneurs have less access to capital and are more likely to use personal financing such as homeownership which has already been hindered by redlining (Loh, 2020). Further, Black homeowners are more likely to leverage home equity to build a business than their white counterparts. Consequently, Black businesses are throttled by low homeownership rates and wealth (Ray, 2021).

Additionally, scholars find that “white households have been able to build wealth for themselves and their descendants, while whatever wealth Black families could amass was regularly stripped away. Private businesses and governments institutionalized racism and discrimination” (Weller, 2021). These factors compound to a cycle of divested wealth and capital from the Black community and a huge opportunity cost for potential generations. One opportunity cost manifests through the decrease of jobs for Black adolescents, as fewer Black businesses are present to prioritize their employment and training. White Americans benefit from generations of business ownership as their network and cooperation create employment pipelines. White Americans also have access to more affluent networks to help them obtain jobs for themselves and their children (Weller, 2021). In the context of the global Covid-19 pandemic, the disparities in Black businesses have deepened. The Coronavirus, Aid, Relief and Economic Security (CARES) Act funding furthered disparities because it only gave funds to employer firms, and 95% of Black owned firms are non-employer businesses compared to 78% of whites (McManus, 2016). In fact, 40% of Black businesses closed during the Covid-19 pandemic according to a Stanford University study (Fairlie, 2020). With little recourse, Black communities turn inward to circulate finances and build wealth within themselves to attain financial security. A popular method is through savings clubs and Black financial institutions.

The involvement of both formal and informal Black financial institutions is essential to Black business growth. Spanning West African history, Black people have congregated to create unified financial arrangements. Collectivist cultural practices thrived amidst generational barriers to financial achievement. The collectivist practice of community financing is a distinct heritage afforded to Black communities, both those who were descendants of enslaved Africans and those in the Black diaspora. Sou-sou circles were formed from West African and Afro-Caribbean collectivist tradition, and East African Mahaber groups were

CPAR | The Black Dollar: Cooperative Economicsformed and anchored in traditional practices of communalism. These collectivist financial groups are known as Rotating Savings and Credit Associations (ROSCAs). A ROSCA is an informal savings group comprised of community members who establish an agreedupon amount of contributions to a fund and take turns using the savings. During slavery, ROSCAs were also a way for freed and enslaved people to save any money that they acquired amidst banking and saving being illegal (Stoffle, 2014). ROSCAS also provide resistance to banking systems that shut out Black communities and/or women. Women especially use ROSCAs as a form of agency, savings, and community. ROSCA money can be used to finance a house, pay college tuition, or other family and community projects. The community financing allows for financial transactions to take place debt-free as participants may borrow from the funds the ROSCA cumulatively amasses instead of a bank. ROSCAs are also a form of accountability that creates a social bond with members and incentivize retention in commitment to each other; unlike a bank where borrowers solely represent themselves or their family.

With formal banking institutions, the absence of savings presents a challenge to acquiring loans. Individuals are encouraged to enter ROSCAs with a mindset of “all for one and one for all.” Participants may even switch their turn to receive money when their family experiences hardship. In addition to accountability, the groups build community, working together on their businesses or teaching each other skills to help all members advance. Many people pass their membership on to their children creating intergenerational savings circles and establishing a legacy of the money saved and community built. As communities join together “turning a penny,”— a concept of investing in products, skills, or goods to help you make more money—they help establish economic stability and advance economic mobility. When discussing the impact of ROSCAs in the Caribbean, researchers in the scholarly journal Ethnology note, “meeting turn money is important in creating economic stability for an individual or family (and potentially the community) through micro-entrepreneurial activities” (Stoffle, 2009). By relying on each member of the group, people can save money and then make a purchase debt free meaning that everything they receive from their business may profit. Many continue to participate in ROSCAs even after they have met their financial goal because of their commitment to helping others reach the same success. This is the spirit of cooperative economics.

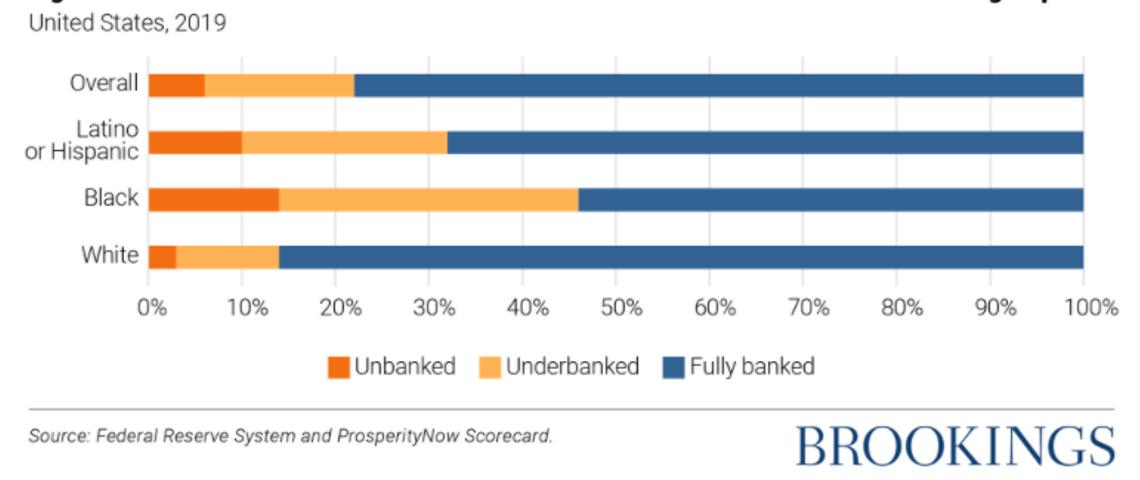

The access and cooperation opportunities ROSCAs create are still needed today as Black communities are continually barred from financial systems. Historically, Black Americans who were unable to access formal financial banking were more likely to face discriminatory lending with the legacies of redlining and underinvestment (Ray, 2021). The impact of

CPAR | The Black Dollar: Cooperative Economicsdistrust and mismanaged funds continues today as Black borrowers (46%) are three times as unbanked as white borrowers (14%). Studies find that 54% of minorities are unbanked leading to other issues with payday lenders, money orders, check cashers, and financial managers. The table below illustrates these gaps.

Inability to access banking services can affect credit, savings, and overall wealth. Studies show that access to banking services could save Black Americans $40,000 in their lifetime (Noel, 2019). Scholars also find that “in the short term, for those with low and unstable income, lack of credit can make it impossible to pay for an unexpected immediate expense. In the long term, without access to the credit needed to fund wealth-creating activities such as educational, workforce, and small business investments, communities of color continue to be harmed by the historical legacies of intentionally discriminatory financial practices” (Ray, 2021).

In the footprints of ROSCAs, several modern non-profit organizations are creating similar financial systems to further economic empowerment. Cooperative for Assistance and Relief Everywhere (CARE), a global humanitarian organization, has a similar program to ROSCAs called the Village Savings Loan Associations (VSLA). VSLAs are a key program at CARE in their work across the globe. They bring people together to save money that CARE stores in a lockbox. The unity of the savings group encourages people to discuss financial goals and the impact of social norms on their well-being. The program coupled with other community initiatives built through VSLAs, resulted in a 50% decline in domestic violence and a 20% income increase within the groups (CARE, 2021). CARE has recently launched the programming to the United States through Community Lending Circles where women in the United States are instructed to follow the same model (CARE, n.d.).

CPAR | The Black Dollar: Cooperative EconomicsThe Young Women’s Christian Association (YWCA) also has a program like the communitycentered approach central to ROSCAs. Their website features a Community Development Financial Institution (CDFI)7 map to help women and families receive the financing they need. Their website describes the initiative by noting, “CDFIs are placed-based organizations with deep roots in the communities they serve. They leverage community insights and partnerships to develop tailored financial tools and services for a wide range of projects” (YWCA, n.d.). CDFIs are focused on community members and engage the community by having them as board members to maintain alignment with their mission. Community groups and savings and credit associations like these helped to bridge the gap in building financial wealth when Black Americans were denied bank loans and needed financial support to purchase land, launch entrepreneurship plans, and build wealth.

Entrepreneurship and homeownership are major pathways to financial success in the United States, and banks are the drivers of wealth creation. Born out of necessity, the first Black banks were a direct result of racist banking practices in the United States. Capital Savings Bank was the first bank organized and operated by Black Americans in the United States, and it opened over two decades after slavery ended. Black-owned banks were formed to aid communities in overcoming financial challenges after the reconstruction. These banks served as an essential source of credit for Black families who were rejected by other financial institutions. They directly allocate resources back into Black communities by providing pathways to homeownership through mortgage loans and to entrepreneurship with small business loans. Banking Black is a pathway towards greater cooperative economics and increased financial security in Black communities. There are now 20

7 “CDFIs can be banks, credit unions, loan funds, microloan funds, or venture capital providers. CDFIs are helping families finance their first homes, supporting community residents starting businesses, and investing in local health centers, schools, or community centers. CDFIs strive to foster economic opportunity and revitalize neighborhoods.” What are CDFIs? (n.d.). United States Department of the Treasury. https://www.cdfifund.gov/sites/cdfi/files/documents/cdfi_ infographic_v08a.pdf

CPAR | The Black Dollar: Cooperative Economics

CPAR | The Black Dollar: Cooperative Economics

Black-owned banks in the United States, and several have earned national prominence by providing financial services to states across the nation. According to a report by the Urban Institute:

“In 2016, 67 percent of the mortgages made by Black-owned banks to Black borrowers were either FHA mortgages or mortgages held in portfolio, reflecting a strong devotion by these banks to the riskiest borrowers in their community, as well as a willingness to incur a high level of institutional exposure to risk from mortgage nonpayment” (Neal, Walsh, 2020).

A skilled workforce is essential to facilitating cooperative economics and Historically Black Colleges and Universities (HBCUs) are a key workforce pipeline. HBCUs both train and socialize students to contribute to the Black community. Supporting Black businesses requires the presence of Black professionals—doctors, business owners, technicians, engineers—to employ and patronize. HBCUs are key educators for that workforce and the importance of supporting the Black community. Born out of the lack of opportunity, HBCUs exist because at the time of their inception (many during the mid to late 1800s) white schools would not accept Black students. They were created to help formerly enslaved Africans acquire skills and training. Today, 20% of all Black graduates and 25% of all Black Science, Technology, Engineering and Math (STEM) graduates come from HBCUs even though there are only 106 (3% of all colleges and universities) in the country (Lomax, 2015). They annually generate $14.8 billion in national economic impact, as well as 134,090 jobs for their local and regional economies altogether (Lomax, n.d.). According

CPAR | The Black Dollar: Cooperative Economicsto the United Negro College Fund, “Every dollar in spending by an HBCU and its students produces positive economic benefits, generating $1.44 in initial and subsequent spending for its local and regional economies. Many HBCUs are in regions of the country where overall economic activity has been lagging, making the colleges’ economic contributions to those communities all the more essential” (United Negro College Fund, n.d.). HBCUs practice cooperative economics by training students, encouraging them to support local (often Black) communities and equipping students to reinvest from the businesses they create and lead after graduation. Equipped with greater earning capacity through college degrees, HBCU alumni contribute to their communities through the ability to buy from Black businesses and support the larger Black community.

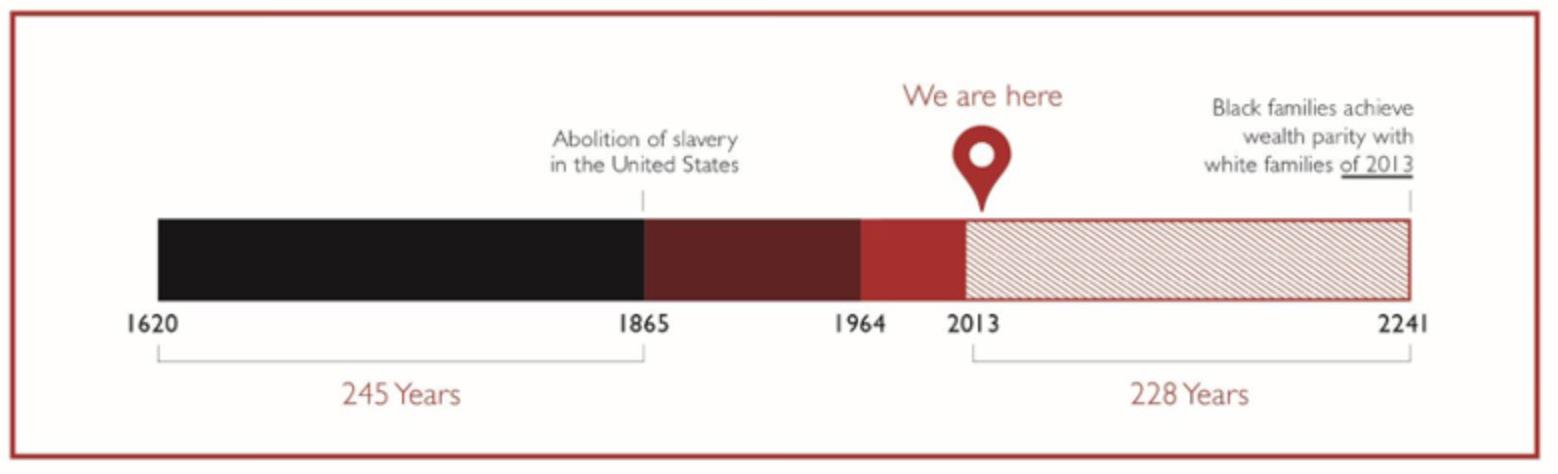

According to analysis from the Corporation for Enterprise Development and Institute for Policy Studies, it is estimated that it will take 228 years for Black Americans to reach the level of wealth white households enjoy today. According to Prosperity Now analysis , “Individual behavior is often seen as the cause of this racialized wage and wealth divide. However, there is compelling evidence that racial economic inequality is primarily the result of long-term investment in some communities and a lack of investment in others” (Prosperity Now, 2022).

Source: Institute for Policy Studies https://ips-dc.org/wp-content/uploads/2016/08/The-Ever-Growing-Gap-CFED_IPSFinal-2.pdf

Further trends highlighted in the Institute for Policy Studies (IPS) 2016 report identify that the wealth gap may never close. If policy and social trends continue as they are, the racial wealth divide will continue to get worse. 8

8 The Ever-Growing Gap https://community-wealth.org/content/ever-growing-gap-without-change

CPAR | The Black Dollar: Cooperative Economics

CPAR | The Black Dollar: Cooperative Economics

Several economic indicators highlight this disparity, such as median household income, net worth, and the likelihood of carrying student-loan debt. The contributors to the disparity in financial wellness is multifold. In 2019, the Teachers Insurance and Annuity Association (TIAA) conducted a survey called the Personal Finance Index (P-Fin Index) which measured eight key areas of personal finance knowledge: earning, consuming, saving, investing, borrowing and managing debt, insuring, comprehending risk and uncertainty, and go-to information sources. According to the report, Black adults answered 38% of the P-Fin Index questions correctly, compared to 55% of white adults. 9

Black Americans scored highest in the areas of borrowing and debt management but scored lowest on questions relating to insuring. Black Americans scored comparatively low on questions related to comprehending risk, investing, and identifying financial information sources. The report states that low levels of financial literacy in insuring and comprehending risk are especially troubling.

• “Insuring” is the least understood area of personal finance among Black Americans, followed closely by “comprehending risk,” “investing,” and “identifying go-to information sources.”

• “Borrowing and debt management” is the area of highest personal finance knowledge among Black Americans.

• A lack of financial resilience was more common among Black Americans than whites in 2019, before the onset of COVID-19 and its economic consequences.

Financial literacy is the inherent ability to read, write and speak the language of finance and is a lynchpin along the path to financial security and economic empowerment. Key pillars to achieving financial security include debt, budgeting, saving, and investing.

Growing these skills among the Black community is crucially important to closing the wealth gap and achieving financial security. Understanding the function and language of finance can empower generations to not only build wealth but maintain and grow it beyond the next generation and become dynastic wealth. Impediments to financial security include employment market trends, federal and state policy, and debt accumulation. Wealth is a household’s assets minus its debts, “the difference between

CPAR | The Black Dollar: Cooperative Economicswhat families own—for instance, their savings and checking accounts, retirement savings, houses, and cars—and what they owe on credit cards, student loans, and mortgages, among other debt” ( Maxwell, Et al., 2019 ). While financial literacy alone may not be enough to close the wealth gap it can help generations navigate barriers to financial security and build lasting wealth.

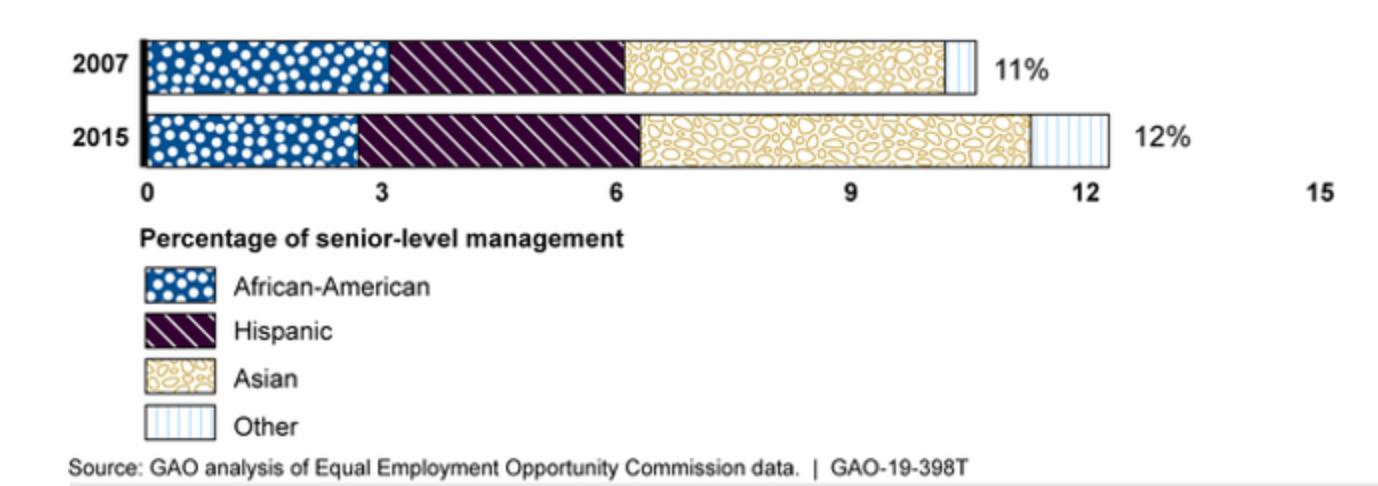

Financial literacy is typically greater for those with formal education and higher incomes. Additionally, the lack of Black representation in the financial services industry demonstrates a key function of the financial literacy issue. According to reports by the U.S. Government Accountability Office, Black Americans only comprise a fraction of minority representation in leadership within the financial services industry. 10 In the graph below, the US. Government Accountability Office data represents minority groups in senior management within the financial services sector between 2007 and 2015.

Source: https://www.gao.gov/products/gao-19-398t

Sources for financial education can take many forms: family, k-12 education, college, workplace, or other financial literacy training opportunities. According to 2022 data from the Council for Economic Education, 25 states currently require high school students to take a course in personal finance. 11 Mandatory personal finance education in public schooling is a key opportunity area to address the persisting wealth gap; however, in surveys spanning 10 years, from 2011 to present there has not been much movement among states expanding financial literacy courses in the classroom. Further, every

10 Trends in Management Representation of Minorities and Women and Diversity Practices, 2007-2015 https://www.gao. gov/assets/gao-18-64.pdf

11 Council for Economic Education, Survey of the States- 2022 https://www.councilforeconed.org/survey-of-thestates-2022/

CPAR | The Black Dollar: Cooperative Economics

CPAR | The Black Dollar: Cooperative Economics

district’s personal finance requirements differ as budgets are determined state by state, which presents demonstrable inconsistencies in the quality and effectiveness of courses.

This is a socioeconomic issue as structural policies and systems contributing to the wealth gap, such as property valuation, pay inequity, redlining, education inequity, and the achievement gap, contribute to and facilitate the perpetuated state of Black financial security. According to the 2016 report by IPS, “Had the average wealth of Black households grown at the same rate over the past 30 years as that of [w]hite households, the average Black household would have an extra $38,000 in wealth today” ( AsanteMuhammed, Collins, Et. Al, 2016 ).

Despite the wage, gap deficiencies in financial literacy, and other structural barriers to financial achievement, the purchasing power of the Black dollar remains influential.

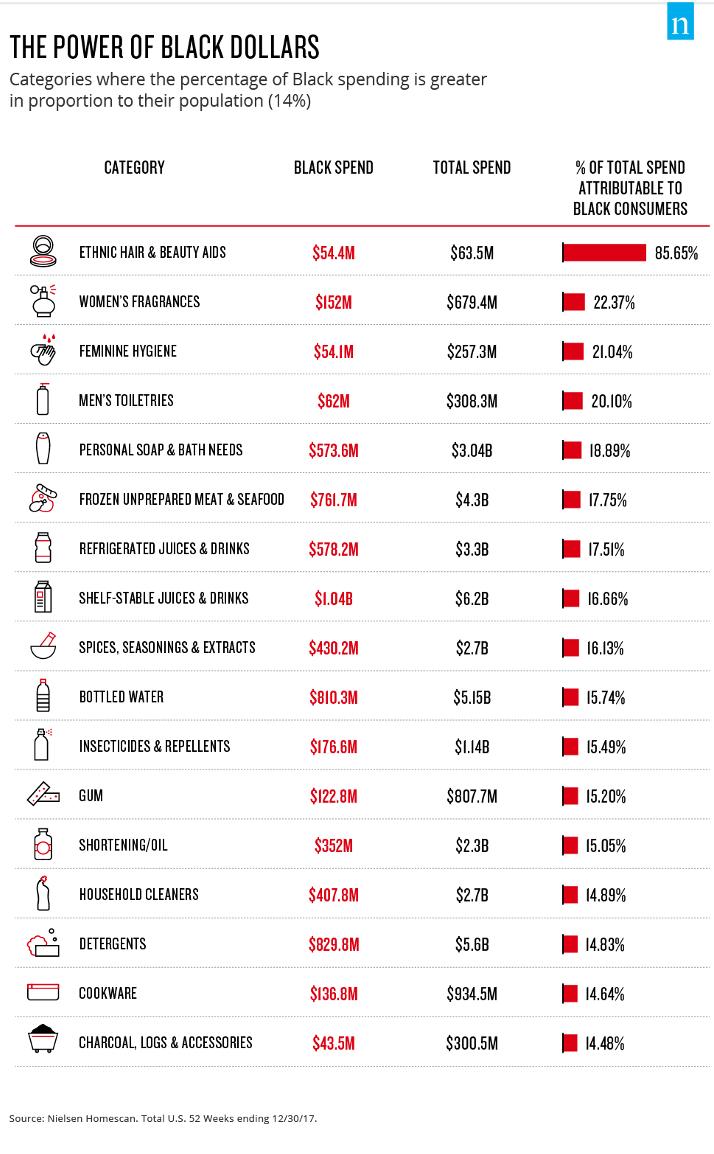

According to Forbes reports, “At 47.8 million strong, African Americans are the secondlargest consumer group, presenting businesses with a $300 billion opportunity stake in this community ( Forbes, 2021 ).

From the exceptional ability to influence pop culture to social justice boycott movements. Black communities have a unique influence to mainstream markets.

Source: Nelson Homescan, Total U.S. 52 Weeks ending 12/30/17

CPAR | The Black Dollar: Cooperative EconomicsData from the University of Georgia indicates that in 2020, the ten states 12 with the largest Black American markets are:

• Texas ($149 billion)

• New York ($141 billion)

• Georgia ($118 billion)

• Califor¬nia ($118 billion)

• Florida ($116 billion)

• Maryland ($86 billion)

• North Carolina ($75 billion)

• Virginia ($67 billion)

• Illinois ($63 billion)

• New Jersey ($57 billion)

Black consumers are younger, more engaged on social media, and prepared to organize spending power. According to a McKinsey report, “The median age of Black Americans is 34, a decade younger than the median for white Americans. Black consumers are more likely to own a smartphone and use their phones 12% more than white Americans. They are nearly three times more likely than white Americans to expect the brands they use to align with their values and support social causes ( Chui, Et. Al, 2021 ). According to a 2018 Nielson study , 37% of Black Americans between the ages of 18 and 34 and 41% of those aged 35 or older say they expect the brands they buy to support social causes, 4% and 15% more than their total population counterparts, respectively. 13 Moreover, Black consumers’ brand preferences are increasingly becoming mainstream choices, which illustrates that the investment in connecting with Black consumers can often yield sizeable general market returns.

The Black community at large is a niche audience. There are ample business opportunities to fill the niche space of serving the vastly diverse needs of Black communities in the U.S. from beauty supply stores and fashion to financial services academia, and other community needs. While working to reimagine and reconstruct current financial systems and pursuing equity in these various areas, Black communities can wield the power of the Black dollar to redistribute wealth. The increase of Black representation in the finance sector, investment in diversity, equity and inclusion across industries, and federal policy initiatives, such as the Minority Business Development Act of 2021 (MBDA) , are signs of systemic change. However, more significant reform is needed to enact community-rooted

12 Consumer Buying Power is More Diverse than Ever https://news.uga.edu/selig-multicultural-economy-report-2021/

13 Black Impact: Consumer Categories Where African Americans Move Markets https://www.nielsen.com/us/en/insights/ article/2018/black-impact-consumer-categories-where-african-americans-move-markets/

CPAR | The Black Dollar: Cooperative Economicsand centered solutions that direct the Black dollar and redistribute wealth back into Black communities. Reforms such as state mandated financial literacy sources, increased diversity in the financial sector, and reparations as a formal accounting for the role of the transatlantic slave trade in building American wealth.

Black Americans have the power to redistribute wealth into their communities and build generational and dynastic wealth. By building financial wealth in assets owned versus owed and circulating the Black dollar in Black micro-economies such as Black-owned businesses, firms, banks, HBCUs, and brands, Black communities can wield the power of the Black dollar to uplift the generational inheritance of economic enfranchisement.

By investing in critical community infrastructures, sharing resources, and circulating the Black dollar with Black systems, the global Black community can reach financial security together. The Black community is akin to each other in a way that is different from any other community. The history of cooperative economics through intra-African trade and clandestine systems created to overcome wealth extraction facilitated by the transAtlantic slave trade have ingrained an interconnectedness that supersedes nationality.

Through collaboration and persistence, the global Black community has combatted and overcome systematic and structural inequities and has reconstructed strategies to obtain financial success. Continued intentional partnerships among Black communities through methods that build wealth in the industries most integral to day-to-day life are essential in wielding the power of the Black dollar, building generational wealth, and greater realization of liberation.

CPAR | The Black Dollar: Cooperative EconomicsArchives.org. (last reviewed June 28, 2021). “Racial Violence and the Red Summer.” https://www.archives.gov/research/ african-americans/wwi/red-summer

Asante-Muhammed, D., Collins, C., Hoxie, J., Nieves, E., (2016). The Ever-Growing Gap. Institute for Policy Studies. https://ipsdc.org/wp-content/uploads/2016/08/The-Ever-Growing-Gap-CFED_IPS-Final-2.pdf

CARE, USA. (2021, April 20). Village Savings & Loan Associations Annual Report 2020. CARE, USA. https://www.care.org/ news-and-stories/ideas/village-savings-loan-associations-annual-report-2020/

CARE, USA. (n.d.). CARE Community Supper Toolkit. CARE, USA. https://www.care.org/wp-content/uploads/2019/03/CARE_ Package_Toolkit_11.10.20.pdf

Chui, M., Gregg, B., Kohli, S. (2021). A $300 Billion Opportunity: Serbing the Emerging Black American Consumer. https://www.mckinsey.com/featured-insights/diversity-and-inclusion/a-300-billion-dollar-opportunityserving-the-emerging-black-american-consumer?cid=other-eml-nsl-mip-mck&hlkid=258a1690736 b4235b9516ec07e94ed71&hctky=12200560&hdpid=e14a281e-1383-40

Crawford, D. & Das, K. (2020, January 28). DC Fiscal Policy Institute. How the District’s History of Exploitation and Discrimination Continues to Harm Black Workers. https://www.dcfpi.org/all/black-workers-matter/ Dattel, E., (2008) Cotton and the Civil War. Mississippi Department of Archives and History. https://mshistorynow.mdah. ms.gov/issue/cotton-and-the-civil-war

Dubois, W.E.B. (1868). Economic Co-Operation Among Negro Americans. The Atlanta University Press. 54-72. https://archive. org/details/economiccooper00duborich/page/n7/mode/2up?ref=ol&view=theater

Gordon Nembhard, J. (2014). Collective Courage. The Pennsylvania State University Press.

Hale, K. (2021). The $300 Billion Black American Consumerism Bag Breeds Big Business Opportunity. Forbes. https:// www.forbes.com/sites/korihale/2021/09/17/the-300-billion-black-american-consumerism-bag-breeds-big-businessopportunities/?sh=2746ffdc34fc

Jackson, P. R. (2016). A Tale of Two Legacies: Career Narratives of the Black Family Business. Journal of Black Studies, 47(1), 53–72. http://www.jstor.org/stable/24572959

Jones, J.L. (2019) “The Red Summer of 1919.” Chicago History Museum. https://www.chicagohistory.org/chi1919/

Jones, J., Schmitt.J & Wilson, V. (2018, February 26). “50 Years After the Kerner Commission.” Economic Policy Institute. https://www.epi.org/publication/50-years-after-the-kerner-commission/ Loh, T.h., Christopher, C. & Buthe, B. (2020, December 16). The great real estate reset- Separate and unequal: Persistent residential segregation is sustaining racial and economic injustice in the U.S. Brookings Institution. https://www.brookings. edu/essay/trend-1-separate-and-unequal-neighborhoods-are-sustaining-racial-and-economic-injustice-in-the-us/

Lomax, M. (2015, December 14). Six Reasons HBCUs Are More Important Than Ever. United Negro College Fund. https://uncf. org/the-latest/6-reasons-hbcus-are-more-important-than-ever

Lomax, M. (n.d.). Why HBCUs Still Matter. United Negro College Fund. https://uncf.org/the-latest/why-hbcus-still-matter

Malveaux, J. (2021). Lynchings Real and Imagined. Journal of the Center for Policy Analysis and Research, 2, 37. https://issuu.com/congressionalblackcaucusfoundation/docs/africa-america_2021_re-envisioning_liberation_ for_?fr=sMGUzYTMyODUzNjU

Maxwell, C., Solomon, D., Weller, C.E. (2019) Simulating How Progressive Proposals Affect the Racial Wealth Gap. Center for American Progress. https://www.americanprogress.org/article/simulating-progressive-proposals-affect-racial-wealth-gap/ Melancon, M. (2021). Consumer Buying Power is More Diverse than Ever. University of Georgia. https://news.uga.edu/seligmulticultural-economy-report-2021/

Miltko, C. M. (2020). “What Shall I Give My Children?”: Installment Land Contracts, Homeownership, and the Unexamined Costs of the American Dream. The University of Chicago Law Review, 87(8), 2273–2319. https://www.jstor.org/ stable/26939846

Morehouse College. (n.d.). Student Freedom Initiative: Robert F. Smith. https://www.morehouse.edu/academics/programs/ student-freedom-initiative/robert-f-smith/

Muhammad, N.H. (2010). Perceptions and Experiences in Elijah Muhammad’s Economic Program: Voices from Pioneers. Georgia State University. https://scholarworks.gsu.edu/cgi/viewcontent.cgi?article=1000&context=aas_theses

Muhammad, E. (1965). Message to the Blackman in America. Secretarius MEMPS Publications.164.

National Museum of African American History and Culture. (n.d.) Dealing and responding to Jim Crow. https://nmaahc. si.edu/sites/default/files/images/dealing_with_jim_crow_6.pdf

National World War I Museum and Memorial. (n.d). “Red Summer-The Race Riots of 1919.” https://www.theworldwar.org/ learn/wwi/red-summer

Noel, N., Pinder, D., Stewart, S., and Jason Wright. (2019, August). “The Economic Impact of Closing the Racial Wealth Gap.” McKinsey & Company. https://www.mckinsey.com/~/media/mckinsey/industries/public%20and%20social%20sector/ our%20insights/the%20economic%20impact%20of%20closing%20the%20racial%20wealth%20gap/the-economicimpact-of-closing-the-racial-wealth-gap-final.pdf.

Nicolaci da Costa, P. (2019) America’s First Bond Market Was Backed By Enslaved Human Beings. Forbes. https:// www.forbes.com/sites/pedrodacosta/2019/09/01/americas-first-bond-market-was-backed-by-enslaved-humanbeings/?sh=24139531888e

Perry, A., Rothwell, J. &Harshbarger, D. (2018, November 27). The devaluation of assets in Black neighborhoods. Brookings Institution. https://www.brookings.edu/research/devaluation-of-assets-in-black-neighborhoods/

Prosperity Now. (2022). Prosperity Now Scorecard: 2022 Policy Update. African American Financial Capability Initiative. https://scorecard.prosperitynow.org/main-findings

Slavery and the Making of America: The Slave Experience. (2004). Thirteen Media With Impact. https://www.thirteen.org/ wnet/slavery/experience/education/history2.html

Queen II, E. L., (2000). Serving Those in Need: A Handbook for Managing Faith-Based Human Services Organizations. Jossey-Bass A Wiley Company San Francisco.

Ray, R., Perry, A., Harshbarger, D., Elizondo, S. & Gibbons, A. (2021, Sept. 1) “Homeownership, Racial Segregation, and Policy Solutions to Racial Wealth Equity.” Brookings Institution. https://www.brookings.edu/essay/homeownership-racialsegregation-and-policies-for-racial-wealth-equity/

Ruffin II, H. (2021, May 26). “We Can Best Honor Our Past by not Burying it: The Tulsa Race Massacre of 1921.” Black Past. org. https://www.blackpast.org/african-american-history/perspectives-african-american-history/we-can-best-honor-ourpast-by-not-burying-it-the-tulsa-race-massacre-of-1921/

Simms, A. (2019). The “Veil” of Racial Segregation in the 21st Century: The Suburban Black Middle Class, Public Schools, and Pursuit of Racial Equity. Phylon (1960-), 56(1), 81–110. https://www.jstor.org/stable/26743832

Stoffle, B. W., Purcell, T., Stoffle, R. W., Van Vlack, K., Arnett, K., & Minnis, J. (2009). Credit, Identity, and Resilience in the Bahamas and Barbados. Ethnology, 48(1), 71–84. http://www.jstor.org/stable/20754010

Stoffle, B.W., Stoffle, R.W., Minnis, J. & Van Vlack, K. (2014). Women’s Power and Community Resilience Rotating Savings and Credit Associations in Barbados and the Bahamas. Caribbean Studies. 42. 45-69. 10.1353/crb.2014.0020

Stoll, M., Raphael, S. & Holzer, H.J. (2001). Why Are Black Employers More Likely than White Employers to Hire Blacks? Institute for Research on Poverty. https://www.irp.wisc.edu/publications/dps/pdfs/dp123601.pdf

Tulsa City-County Library. (n.d.). “Tulsa Race Riot: A Report by the Oklahoma Commission to Study the Tulsa Race Riot of 1921.” Tulsa City-County Library. http://digitalcollections.tulsalibrary.org/digital/collection/p15020coll6/id/515

United Negro College Fund. (n.d.) HBCU’s make America strong: The positive economic impact of historically Black colleges and universities. https://cdn.uncf.org/wp-content/uploads/HBCU_Consumer_Brochure_FINAL_APPROVED.pdf

United States Department of the Treasury. (n.d.). What are CDFIs? United States Department of the Treasury. https://www. cdfifund.gov/sites/cdfi/files/documents/cdfi_infographic_v08a.pdf

United States Government Accountability Office. Financial Services Industry: Representation of Minorities and Women in

CPAR | The Black Dollar: Cooperative Economics

Management and Practices to Promote Diversity. United States Government Accountability Office. https://www.gao.gov/ products/gao-19-398t

Ward, G. K. (2022). Recognition, Repair & the Reconstruction of “Square One.” Daedalus, 151(1), 153–169. https://www.jstor. org/stable/48638136

Washington, R. (1997). The Freedman’s Savings and Trust Company and African American Genealogical Research. Federal Records and African American History (Summer 1997, Vol. 29, No. 2). https://www.archives.gov/publications/prologue/1997/ summer/freedmans-savings-and-trust.html

Weller, C. & Roberts, L. (2021, March 9). Eliminating the Black-White wealth gap Is a generational challenge. Center for American Progress. https://www.americanprogress.org/article/eliminating-black-white-wealth-gap-generational-challenge/

Williams, C., Powell, J., Kelly, J. (2015). Liverpool’s Abercromby Square and the Confederacy During the U.S. Civil War. College of Charleston Lowcountry Digital History Initiative. https://ldhi.library.cofc.edu/exhibits/show/liverpools-abercromby-square/ britain-and-us-civil-war/impact-cotton-trade

Yakobosk, P.J., Lusardi, A., Hasler, A. (2022). How Financial Literacy Varies Among U.S. Adults. Teachers Insurance and Annuity Association, Global Financial Literacy Excellence Center. https://gflec.org/wp-content/uploads/2022/04/TIAAInstitute-GFLEC-2022-Personal-Finance-P-Fin-Index.pdf?x70470

YWCA CDFI Map. (n.d.). Young Women’s Christian Association. https://www.ywca.org/what-we-do/ywca-data-maps/ ywca-cdfi-map/

Zinn Education Project. “Sept. 30, 1919: Elaine Massacre.” (n.d.) Zinn Education Project- Teaching the People’s History. https://www.zinnedproject.org/news/tdih/elaine-massacre/