10 minute read

The big squeeze – rising costs and falling demand pressuring businesses

by AICM

Anneke Thompson MICM Chief Economist CreditorWatch

In February, we were able to get a guide on what listed Australian businesses are anticipating for the year ahead, as reporting season began. While most listed retailers reported strong earnings for the second half of 2022, many downgraded or emphasised caution in their outlook for sales across 2023.

Advertisement

Groups like Adairs, JB HiFi and Baby Bunting all highlighted that sales in the year ahead in many categories were likely to be lower. This year we will see the impact of many more consumers having less to spend each month, as up to 800,000 fixed rate loans on very low interest rates will convert to variable rate loans. We will also see the added impact of housing completions begin to trend down from about the middle of the year. This will affect sales in the furniture, white goods and electrical goods categories.

Business Risk Index points to higher insolvency risk

The CreditorWatch Business Risk Index continues to highlight the higher risk of insolvency for sectors reliant on discretionary spending, with the food and beverage sector topping the list of riskiest sectors at a 7.3% probability of default. This is supported by a recent survey by the Australian Financial Review (AFR), which asked survey respondents if they were cutting back on their expenses, and if so in what categories. In total, 64% of respondents said they were already cutting back, with a further 17% saying they had plans to.

‘Dining out’ was the category top of the list of areas where people were cutting back, with 74% saying they have already reduced spending here. This emphasises the risk of this sector, as business owners will now not only be grappling with high costs, wages, interest payments and rents, but also lower demand.

Inflation the key focus

Inflation continues to be the key metric that the whole world is watching. While many economists believe inflation peaked in Australia in the December 2022 quarter, when it came in at 7.8%, it is still well above the RBA’s target rate of 2-3%, and may not get back to that level until 2025.

“Inflation continues to be the key metric that the whole world is watching. While many economists believe inflation peaked in Australia in the December 2022 quarter, when it came in at 7.8%, it is still well above the RBA’s target rate of 2-3%, and may not get back to that level until 2025.”

Australian Gross Domestic Product (GDP) grew by 0.5 per cent over the Dec quarter, down from 0.7 per cent in September quarter and 0.9 per cent in the June quarter. Importantly, for both the inflation and cash rate outlook, growth in household spending rose by a moderate 0.3 per cent.

This will give the RBA comfort – among other important indicators like monthly retail trade and labour force – that its efforts to reduce inflation are working. Unfortunately, the flip side to this success is continued pain for the Australian consumer and, ultimately, businesses.

Inflation in other economies also seems to have peaked, but is still well above normal levels. This is partly because supply side factors, such as the

Ukraine War and bad weather affecting crop harvests, are out of the control of central banks.

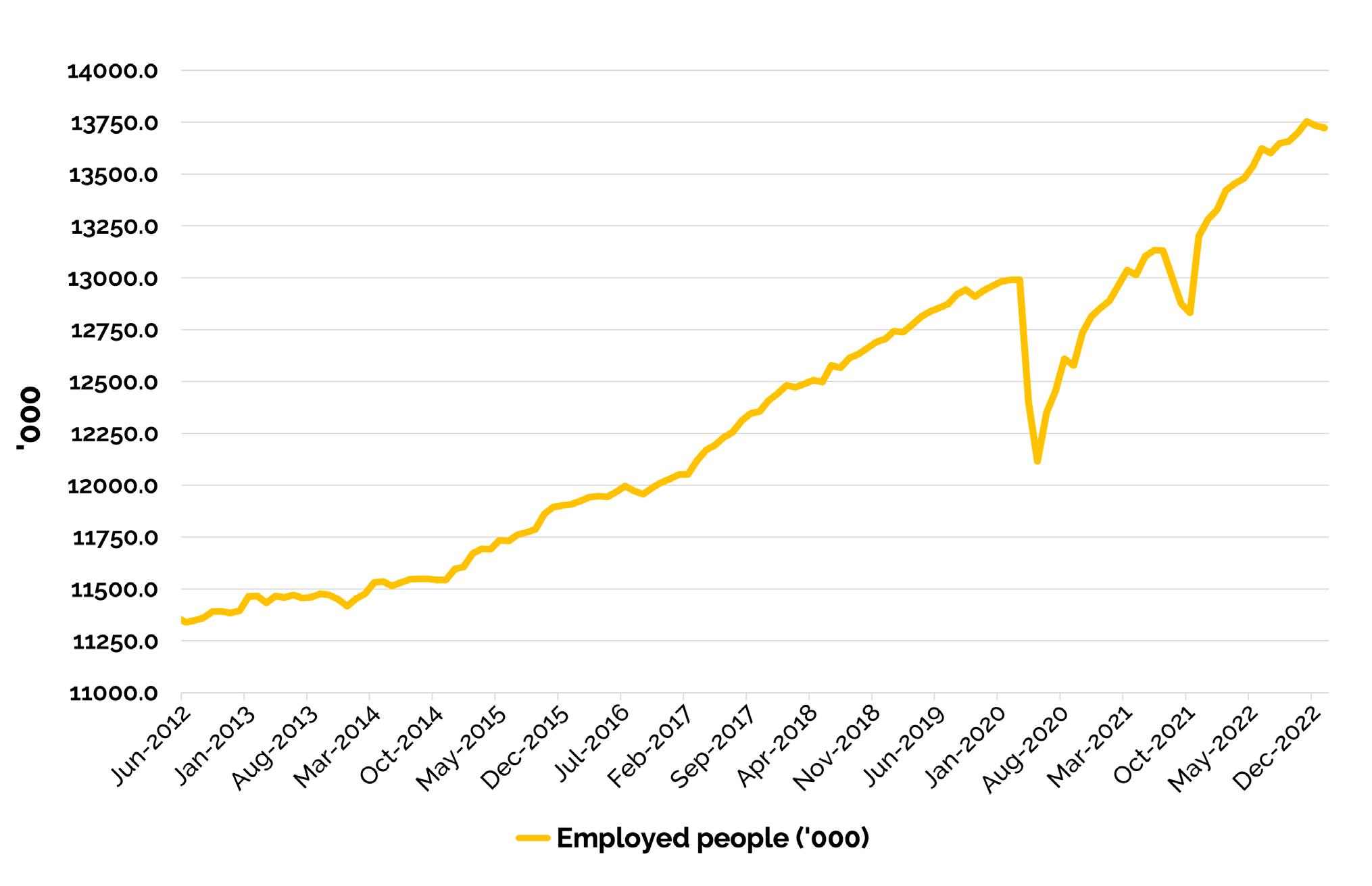

Employment softening

In February the ABS also reported an increased in the January 2023 unemployment rate, rising to 3.7% from 3.5% on a seasonally adjusted basis. While there are still almost 400,000 more employed people in Australia in Jan 2023 than there were in Jan 2022 (or a 3% difference) it is likely that the strong gains in employment that were recorded in 2022 won’t be repeated this year. The ABS has recorded a drop in the number of employed people for two straight months now, suggesting we reached a peak in employment in November 2021.

Businesses will be far more cautious in hiring, although the good news is that at this stage there doesn’t seem to be any increase in mass redundancy announcements. While increasing unemployment is not great news for jobseekers, it is better news for the economy overall, as it greatly decreases the threat of a wage price spiral.

Seek Job ads data for Jan 2023 also show that on a year-on-year basis, almost all sectors have recorded a drop in the number of advertised roles. The biggest year on year drop was recorded in the Information and Communication Technology sector, which was down 24.1%, followed by Hospitality and Tourism, down by 13.8%. The only industries to have a higher number of job ads in Jan 2023 versus Jan 2022 are Education and Training, Community Services and Development and Accounting.

Retail trade, one to watch

Retail trade data for January 2023 revealed a 1.9% seasonally adjusted increase month-on-month. This was after a large fall in December of 4%. On a total dollar value, retail trade in January 2023 was roughly the same as it was in September 2022.

Most industry turnover is quite volatile over the summer period, so it is difficult to draw any major conclusions on trends, however, household goods retailing is one sector where

Source: ABS Labour Force, January 2023 trade is well below 2022 levels and is in fact trading at or about the level it was in October 2021. This is likely a result of households pulling back on large expenditure and also a flow on impact of many people making large purchases for their houses during lockdown periods. It is likely that as we see the peak of housing completions reached in around mid 2023, that household goods trading will continue to remain flat or even trend down.

Payment times

Late payment rates for January were, on average, three times greater for small business relative to big business, reflecting differences in the ability of small businesses to enforce payment terms and collect on payment arrears, and the willingness of some businesses to treat smaller suppliers as an interest free bank.

Payment arrears have been slowly trending down across all industries but continue to be a problem in the construction industry due to inherent payment structures that incorporate delayed payments for projects. In January, 11.6% of small

Credit Enquiries

construction businesses had payments that were 60 days or more in arrears compared to just 2.3% of large businesses.

Credit enquiries

CreditorWatch’s Business Risk Index continues to point to businesses acting in an increasingly cautious manner. Data from February 2023 shows that credit enquiries in February 2023 were more than double those in February 2022. This is despite average trade receivables per data supplier decreasing by 10 per cent yearon-year in February 2023. Businesses are clearly more concerned about the financial stability of the businesses they are trading with, given the economic conditions and large decline in consumer sentiment.

The outlook

Overall, the picture for Australian businesses is looking increasingly more complicated as we move through 2023. While the Australian economy is certainly one of the brighter spots when we think about the global economy, there is no doubt that businesses will find trading conditions far more challenging this year than last. On the bright side, it does appear that inflation has peaked. This gives us confidence that pricing data coming through this year should, based on sentiment levels, show continued moderation in growth levels of inflation.

Anneke Thompson MICM Chief Economist, CreditorWatch www.creditorwatch.com.au

Barbara Cestaro MICM Client Manager – Credit Solutions AON

In a recent Aon survey1 79% of C-suite leaders and senior executives expect a recession, though only 35% feel “very prepared” for it. In today’s liquidity crunch with rising interest rates and inflated commodity prices, the role of credit insurance has never felt more relevant.

Market overview

During the COVID-19 pandemic, there was a strong decline in insolvencies (globally, they fell by a cumulative 29% in 2020/20212) mainly due to changes to insolvency legislation (often temporary) to protect companies from going bankrupt and government economic and fiscal support for businesses. In 2021 we observed a partial adjustment to normal, pre-pandemic insolvency levels, a process that continued in 2022; this coincided with the phasing out of government support programs2

Following the tapering of this support and the economic headwinds and inflationary effects brought about by the war in Ukraine, the energy crisis in Europe and now recessionary effects, we expect a significant increase in global insolvencies in 2023 that will happen in countries and trade sectors at different speeds and times.

As a result of the artificial economic environment created over the past couple of years, credit insurers have experienced extremely low levels of loss. Increased trade volumes combined with inflationary effects have seen overall premium levels increase throughout the past 12-24 months2. Therefore, financial reporting at the end of Q3 2022 showed Loss and Combined ratios that have continued at a lower than pre-pandemic level, although these are now starting to trend upwards2

Even though we do expect a future “normalisation” of loss ratios as insolvencies inevitably return, the impact and timing of these also remain so uncertain that it is unlikely to impact insurer results until well into 2023

“In a recent Aon survey 1 79% of C-suite leaders and senior executives expect a recession, though only 35% feel “very prepared” for it.”

Insolvency Growth Forecasts in 2022 and 2023

Source: Aon’s Credit Solutions Q4 2022 Insights, Aon, 2022

Loss Ratio evolution at the earliest. Whilst these more favourable underwriting conditions exist, credit insurers have continued to adopt a much more pragmatic position on both their risk and commercial strategies, whilst attaining high levels of client portfolio retention and profitable growth.

It is important to understand an insurer’s performance when negotiating a renewal as differences in performances can drive differences in underwriting strategies and insurers’ competitiveness with either price or limits (or both) could slightly change year on year accordingly.

Credit Limits

In 2022 insurers’ appetite and capacity have continued to increase, reflecting higher commodity prices and inflation; the aggregate credit limit capacity now exceeds pre-pandemic levels with a rebound seen in all geographic regions and notably in the Americas, APAC and in trade sectors like electronics, chemicals, metals, construction, and transportation/ logistics.

While this upward trend might continue at a lower rate in the shortterm and maybe plateau during 2023, the market continues to innovate to provide capacity and solutions related to some of the more complex and larger risk exposures mainly through the adoption of new technologies to improve process and decision making2

Industry trends

Approval rates across all sectors except Agribusiness continue to linger behind December 2021 levels but are overall 400 basis points higher than pre-pandemic levels.

Retail/Wholesale and Food & Drink sectors both show a 200 basis points reduction in approval rates as input costs rise and consumer confidence is hit by inflationary pressures and higher interest rates2

Supply chain issues continue to impact the Automotive sector along with low consumer confidence and high fuel costs; this translates to approval rates increasing by 200 basis points quarter on quarter but remaining 50 basis points behind December 2021 rates2

Manufacturing and Technology both declined in approval rates because of higher energy and wages costs combined with a fall in demand that has lowered confidence within the manufacturing sector, whilst supply chain issues and falling consumer confidence continue to stall progress in the technology sector.

We have observed approval rates stalling for the Steel and Construction sectors. Energy costs are negatively impacting the steel sector, driving up production costs, while demand for automotive, white, brown and yellow goods declines. Construction is also feeling the impact of a global slowdown, especially in the APAC region2

Sector Acceptance Rates

“Supply chain issues continue to impact the Automotive sector along with low consumer confidence and high fuel costs; this translates to approval rates increasing by 200 basis points quarter on quarter but remaining 50 basis points behind December 2021 rates 2 . ”

Australian trends

In Australia we have observed the approval rates return to 2019 levels; however, the overall amount of credit limits granted is higher, reflecting high commodity prices and inflation2

We read a lot about the construction sector woes in 2022 and the forecasts for insolvencies in this space in 2023 are not positive. One would think this would translate in lower acceptance rates, but we have seen the overall acceptance rate increase and exceed pre-pandemic times.

Australia Acceptance Rates Australia – Construction Acceptance Rates

Aon’s TradingDesk provides our teams with access to an automated data interface with insurers’ buyer limits systems. It holds data for more than 1.5 million unique buyers, and it helps to identify possible capacity and maximise credit limit approvals. We can quickly identify and manage uninsured exposures, closing the gap between insured risk and uninsured risk for more comprehensive coverage.

How Aon helps businesses make better decisions

Now more than ever, senior executives are required to make enterprise-wide business decisions at speed, facing challenges that are complex and highly interconnected. From the pandemic and geo-political instability to hyperinflation and supply chain disruption, it seems volatility is becoming the norm. Luckily Aon’s periodic Market Insights Reports aim to help businesses navigate credit insurance market dynamics. Our reports enable us to support our clients in seeking the best outcomes for their insurance program.

More reports and data are available on www. aoninsights.com.au. Feel free to visit to explore the latest information not only on trade credit insurance, but also on M&A, Cyber, Marine Cargo insurance.

Barbara Cestaro MICM Client Manager – Credit Solutions

E: barbara.cestaro@aon.com

1 Making Better Decisions in Uncertain Times: Aon’s 2022 Executive Risk Survey, Aon, October 2022

2 Aon’s Credit Solutions Q4 2022 Insights, Aon, 2022

© 2023 Aon Risk Services Australia Limited ABN 17 000 434 720 AFSL no. 241141 (Aon). The information provided in this document is current as at the date of publication and subject to any qualifications expressed. Whilst Aon has taken care in the production of this document and the information contained herein has been obtained from sources that Aon believes to be reliable, Aon does not make any representation as to the accuracy of information received from third parties and is unable to accept liability for any loss incurred by anyone who relies on it. The information contained herein is intended to provide general insurance related information only. It is not intended to be comprehensive, nor should it under any circumstances, be construed as constituting legal or professional advice. You should seek independent legal or other professional advice before acting or relying on the content of this information. Aon will not be responsible for any loss, damage, cost or expense you or anyone else incurs in reliance on or use of any information in this publication.