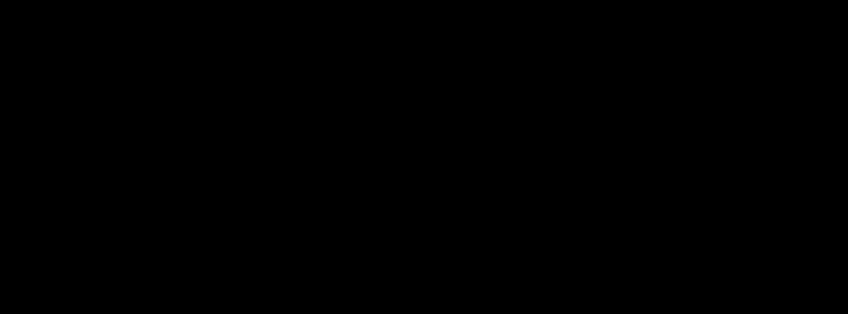

Inflation has reached its highest level since 1976.

The Russian invasion of Ukraine and its repercussions have significantly deteriorated economic conditions. Due to its reliance on energy imports, Europe is severely affected, and Belgium is no exception. While GDP held up well in the first three quarters of this year, continued high inflation is expected to cause GDP to stagnate in the final quarter of the year and the first quarter of 2023. The most recent figures indicate annual GDP growth is expected to be 2.44% in 2022, decelerating to at best 1.03% in 2023.

Despite the economic downturn, employment growth remained strong in the first half of 2022, building on the momentum of 2021 with an unemployment rate down from 6 26% last year, creating an additional 100,000 jobs for the year and 39,000 jobs in 2023. In concrete terms, the unemployment rate is expected to be 5.55% at the end of the year, dropping to 5% by the end of 2023.

Inflation has reached its highest level since 1976 Following a brief pause in July, inflation increased again in August and September As a result, inflation has been revised upwards to reach a sky-high 9 35% for 2022 This level will decelerate in 2023 to 6.40% before broadly closing in on the ECB’s 2% target from 2024.

Regarding our outlook, Cushman & Wakefield forecasting has elaborated a baseline short-term mild recession scenario in the Eurozone (50% probability). In this scenario, persistent inflationary pressures push the ECB to raise rates aggressively, see more here, stalling business investment and consumer spending The Euro area economy would enter a mild recession beginning in Q4 2022 with three quarters of negative growth, before returning to moderate growth in the second half of next year.

GDP GROWTH AND UNEMPLOYMENT RATE INFLATION RATE

M A R K E T B E AT Office Q3 2022 BRUSSELS 230,778 YTD Take Up (sq m) 7.95% Vacancy Rate €340 Prime rent (€/sq m/year) 5.55% Unemployment rate 2.44% 2022 GDP Growth 9.35% Consumer Price Index Source: Moody’s Analytics and Federal Planning Bureau, October 2022 ECONOMIC INDICATORS Q 3 20 22 12 Mo. Forecast 12-Mo. Forecast YoY Chg YoY Chg Please note the economic data can vary significantly from one source to the other. Therefore, the figures provided should merely be used as an indication or trend. 3.85% Prime yield

Sources: Moody’s Analytics, BNB, Eurostat, October 2022 Sources: Moody’s Analytics and Federal Planning Bureau, October 2022 -6% -4% -2% 0% 2% 4% 6% 8% 2018 2019 2020 2021 2022 2023 2024 2025 GDP Growth Unemployment Rate 0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 2018 2019 2020 2021 2022 2023 2024 2025 inflation

Office Q3 2022 BRUSSELS

Slow take-up on the Brussels office market.

In Q3, less than 100,000 sq m of take up was recorded on the Brussels office market which brings the total take-up year to date to 230,000 sq m for 2022 This could confirm our earlier prediction of moving to a lower annual average take-up this year

Transactions are taking longer to be concluded International companies, in particular, make the decision to move after all departments have given the go ahead. The current geopolitical and economic situation, combined with the aftermath of COVID 19, are the main reason it is taking so long.

Other companies choose to stay on the sidelines and renew their current lease, with or without a space reduction.

Public and non-profit sectors contribute to 30% of the activity.

In Q3, public and non-profit sectors contributed some 24,000 sq m which account for one quarter of the total take up. Most of the activity is driven by the Brussels Administration. Notably, Citydev confirmed a 5,200 sq m letting of the City Center, and the CPAS/OCMW of Watermael Boitsfort purchased 4,000 sq m for its own use in Office Garden, located on Boulevard du Souverain

However, the Brussels office market is waiting for the EU institutions’ decision with bated breath Indeed, the EU commission’s search for 100,000 sq m of new office spaces for the 2022-2026 period is becoming pressing. Some very large public transactions could take place in the coming months, particularly in the Leopold and North districts.

New prime rents are now a reality.

The Brussels office market recorded an increase in prime rents this quarter. Indeed, the law firm Willkie Farr & Gallagher confirmed the 1,100 sq m letting in the Science 12 project at a rent of €340/sq m/year, the new prime rent. The North district too saw an increase in prime rents, which are now back to the level of the fourth quarter of 2020 at 250€/sq m/year

For the other districts, prime rents remain unchanged. However, due to sky high inflation, current passing rents are rising faster than prime rents, which are initial rents and therefore not affected by indexation. Occupants may choose to relocate from ageing buildings where rents will be indexed by 10% this year and a minimum of 6% next year to a more environmentally responsible building where they will pay a higher base rent that will not be indexed due to timing. As a result, prime rents are expected to rise again next year, by an average of €20/sq m/year across all submarkets. Then, by the end of 2023, we confidently predict a prime rent of €360/sq m/year for the Brussels office market

TAKE-UP BY QUARTER (000s SQ M)

PUBLIC AND PRIVATE TAKE-UP (000s SQ M)

PRIME RENTS (in EUR/SQ M/YEAR)

M A R K E T B E AT

0 100 200 300 400 500 600 2018 2019 2020 2021 2022 Q1 Q2 Q3 Q4 0 100 200 300 400 500 600 2018 2019 2020 2021 2022 Private Public 100 150 200 250 300 350 400 2018 2019 2020 2021 2022 2023 CBD Decentralised Periphery

BRUSSELS

Speculative pipeline required for market to thrive.

In 2022, 180,000 sq m of new projects have already been delivered, and 32,000 are still under construction and scheduled for completion in the fourth quarter of the year, with nearly 60% already prelet. Although an important development pipeline is foreseen for the coming years, 64% is already prelet. This shows the interest of occupiers in ESG compliant buildings. The fact that new (re ) developments must be regularly added to the stock to meet occupiers’ demand due to ESG requirements is a certainty

Like this year, 2023 will be a dynamic year with no less than 215,000 sq m of new projects completed, including a healthy number of speculative deliveries The biggest ones being the Chancelier, Luxia both located in the Centre district or The Wings in the Airport district. However, an additional 275,000 sq m could be added to the market by 2025 as many projects have building permits, but developers and owners may be tempted to wait for an anchor tenant to begin construction due to the uncertain economic climate.

The vacancy rate is increasing.

The vacancy rate increased again in the third quarter to 7.95%. The large number of buildings arriving on the market partially empty, combined with occupiers’ concerns about inflation, is leading a slowdown in activity and, as a result, an increase in vacancy.

Despite a significant proportion of pre-let developments, the above trend is expected to continue in the coming months, resulting in a vacancy rate of 8.3% by the end of 2023. Projections of a return to a more favourable economic environment in 2024 should allow the market to absorb a chunk of the vacancy, finally reaching a level of 8% by 2025.

Brussels office buildings in the crosshairs.

While some companies are considering relocating to the city centre in order to reduce their energy footprint by using public transportation rather than driving, the city of Brussels has just implemented new measures on office building taxes, which are now twice as high last year.

No doubt theses new measures are contrary to commercial real estate’s neutral carbon target. This tax increase will definitely lead some companies to stay in the outskirts instead of moving back to the city centre, but it will also cause others to relocate to a more “tax friendly” region, and thus further promote

use of company cars.

OFFICE PIPELINE (000s SQ M)

VACANCY RATE (%)

M A R K E T B E AT Office Q3 2022

the

0 50 100 150 200 250 2022 2023 2024 2026 Pre-let Available 6.0% 6.5% 7.0% 7.5% 8.0% 8.5% 2018 2019 2020 2021 Q322 2023 2024 2025

Q3 2022 BRUSSELS

OFFICE INVESTMENT VOLUMES BY QUARTER (MEUR)

Mega deals boost Brussels investment market.

In the third quarter of 2022, EUR 1 07 bn has been invested on the Brussels office market This represents the best Q3 ever recorded. This brings the total invested volume in 2022 to nearly EUR 2.4 bn, a record despite difficult geopolitical and economic conditions.

These figures were heavily influenced by the closing of large transactions, especially this quarter with the purchases of the Pole Star by Whitewood and the Egmont I&II by UBP for 392 MEUR and 385 MEUR respectively.

In times of war and high inflation, a record investment volume might seem paradoxical, but much of this is the result of previous negotiations. For instance, negotiations for the sale of the North Galaxy concluded in Q2 2022, started in the past with a failed offer in 2021

Some investors' strategies have evolved in response to a more uncertain economic climate. German investors, for example, have "paused" their investments and are returning to Germany On the contrary, Belgians, particularly family offices, may be able to benefit from this to take advantage of some attractive positions, while the fall of the Euro may attract foreign investors despite the economic context.

Prime yields have been revised upwards.

Triggered by rising inflation, the European Central Bank has delivered two consecutive rate hikes in recent months, totaling 125 bps, and is expected to proceed with more rate increases in the coming months, according to its President. Markets have been anticipating an interest rate hike for a while, which led to Belgium’s 10-year bond yield rising after the announcement

However, the commercial real estate market is only now beginning to adapt to this increase, and as in the rest of Europe, Brussels is experiencing longer and more difficult transactions, a growing gap between asking and offering prices, and transaction repricing and/or asset withdrawals from sale because offers have not met expected price levels

As a result, prime yields have been revised upwards. Prime yields, just like the 10 year bond, are rising, albeit to a lesser extent The Brussels prime yield is currently standing at 3 85% and could rise to 4.10% by the end of the year.

PRIME OFFICE YIELDS IN BRUSSELS (%)

M A R K E T B E AT Office

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 2018 2019 2020 2021 2022 Q1 Q2 Q3 Q4 -1% 0% 1% 2% 3% 4% 5% 6% 7% 8% 2018 2019 2020 2021 Q3 22 Q4 22 Central Decentralised Periphery LT Prime 10y. Bond

Brussels

2,499,310

Brussels (North) 1,672,663

Brussels (Louise) 875,282 44,678

Brussels (Midi) 605,903 14,006

Brussels (Decentralised) 2,580,377 301,055

Brussels (Periphery) 2,179,469 398,889

Brussels (Overall) 13,794,554 1,096,676

66,885

4.00%

4,453 68,330 €250 4.85%

17,122 32,600 €275 4.10%

5,689 6,785 €195 5.10%

13,498 27,772 83,310 €200 6.50%

34,874 92,364 91,567 €175 6.15%

230,778 390,305 €340 3.85%

CÉDRIC VAN MEERBEECK

BENJAMIN DEVIE

Belgium &

A CUSHMAN & WAKEFIELD RESEARCH PUBLICATION

& Wakefield (NYSE: CWK) is a leading global real estate services firm that delivers exceptional value for real estate occupiers and owners. Cushman & Wakefield is among the largest real estate services firms with approximately 50,000 employees in over 400 offices and approximately 60 countries.

the firm had revenue of $9.4 billion across core services of property, facilities and project management,

capital markets, valuation and other services.

omissions

M A R K E T B E AT Office Q3 2022 BRUSSELS

Cushman

In 2021,

leasing,

© 2022 Cushman & Wakefield. All rights reserved. The information contained within this report is gathered from multiple sources believed to be reliable. The information may contain errors or

and is presented without any warranty or representations as to its accuracy. MARKET STATISTICS cushmanwakefield.com

Head of Research and Marketing | Belgium & Luxembourg +32 477 98 11 83 cedric.vanmeerbeeck@cushwake.com

Research Analyst |

Luxembourg +32 495 11 35 10 benjamin.devie@cushwake.com KEY INVESTMENT TRANSACTIONS Q3 2022 KEY LEASE TRANSACTIONS Q3 2022 *Renewals not included in leasing statistics SUBMARKET STOCK (SQ M) AVAILABILITY (SQ M) VACANCY RATE Q3 2022 TAKE UP 2022 YTD TAKE UP UNDER CONSTRUCTION (SQ M) PRIME RENT (€/sq m/year) PRIME YIELD Brussels (Leopold) 3,381,550 136,929 4.05% 18,767 42,337 47,613 €340 3.85%

(Centre)

104,719 4.19% 14,512 39,945

€260

96,400 5.76% 4,453

5.10% 4,512

2.31%

11.67%

18.30%

7.95% 96,305

PROPERTY SUBMARKET TENANT SQ M TYPE Excelsiorlaan 79 81 Airport Workways 6,000 Purchase City Center Centre Citydev.brussels 5,200 Letting Poincare 76 78 Midi Veolia 4,800 Letting CBTC Walloon Brabant LIMS 4,500 Letting PROPERTY SUBMARKET SELLER / BUYER Volume (in MEUR) Pole Star & North Light North Samsung Hyundai / Whitewood 392 Egmont I&II Centre Korean Investors / UBP 385 Marquis Building Centre AEW / CDC 55 Silver Building North East Allianz / Private 42.5 AGC HQ Walloon Brabant AXA / Savills IM 35