7 minute read

The private label scenario

Private Labels: option or NEED?

In a scenario of year by year disruptive and unexpected situations since 2020, companies in FMCG supply chains are increasingly tied to distributors’ choices, who try to ‘normalize’ the pandemic, lose sales volumes (although values grow), compete with the ‘zero point’ of shares (will we actually have a new leader soon?) and seem increasingly similar and interchangeable, simply serving as a flat backdrop to the innovation and success of discounters. Is PL in this context an option or a necessity?

THE SCENARIO

Data over the past twenty years show a slow and constant growth in the share of PL products and a corresponding decline in the share of brand industry products. In recent months, major retailers have raised the bar above 30% and up to 50% of the target PL share of their sales, but it is the 22% share of discounters in Italy that, with Private Label sales accounting for between 60% and 80% of sales, is generating the most significant development, including PLs, in large-scale distribution in Italy.

Data from the first 5 months OF 2022 show an acceleration of the process, exacerbating the crisis of the role of the brand industry that, only in some cases is in partnership with PLs retailers and in many others sells only when the price cut is 50%. And Meanwhile, PL consolidates its role of ‘brand’ in Italy, representing, for example, over 50% of total organic sales in retail (Nielsen, May 2022).

This phenomenon takes place in a context where the rising costs and the consequent inflation result in a (un)negotiation still open on price lists, between the manufacturer and the distributor. Based on a survey conducted by IPLC (2022 Report) on a few dozen PL manufacturers in Europe, a simplified example was developed in early 2022. The example simulated the path of profitability recovery and maintenance undertaken by the manufacturer in relation to the

PICTURE 3.16 THE BRAND INDUSTRY LOSES MARKET SHARE. (Sales in value, Total of Grocery, Iper +super + Lib ser, incidence %)

Leader (First category brand) Follower (from II to IV category brand) Other brands PLs

*Data referred to the first semester Source: Ufficio Studi Coop - Nomisma on Nielsen Data

increases required until January 2022. Just think how severe the problem may have become today after several months of inflation:

But what can we expect in the short and medium term? IPLC has conducted an assessment of scenarios in European countries, and we believe more opportunities rather than threats are on their way from the perspective of PL development for all the players in the supply chain, especially in Italy.

Source: IPLC, January 2022. Simplified simulation based on interviews with European manufacturers

Note: The 6.8% average cost increase negotiated so far by the supplier was not enough to cover the increase in sales costs. In fact, this increase would still bring a loss of €600,000 over the year. An 8.1% increase would see a net profit of 0.4 percent, and a 13.9 percent increase would be required from customers to restore the 4.8% net profit of 2020.

INTERNATIONAL: THE CONSUMER

Consumer behavior has significantly changed in the past three years, and this change has been much faster than the distribution companies’ update. As shown in the table, the search for convenience is not separated from the demand for quality and gratification. And, although to a different extent, this regards all income segments of the population. It was precisely the PL that created a new paradigm of accessibility to value that, in the past, was reserved for the brand industry.

Hence, PL has emerged as a ‘brand’ in Italy, accounting for over 50% of organic sales in retail and helping narrow the price gap between conventional and organic (Nielsen, May 2022) by making the latter more accessible.

INTERNATIONALIZATION: THE MANUFACTURERS

The world of manufacturing, brand industry, PLs and SMEs in Italy has ahead the possibility to play a relevant and essential role for Italian supply chains. There are tremendous opportunities that, regardless of geopolitical dynamics, are already in place in international markets. And this becomes even more relevant and attainable precisely because of the development of PLs in all major countries

around the world. Accessing different markets (also) through PL is a lever that makes internationalization something concrete, even for companies that do not have sufficient know-how and resources for establishing their brands abroad.

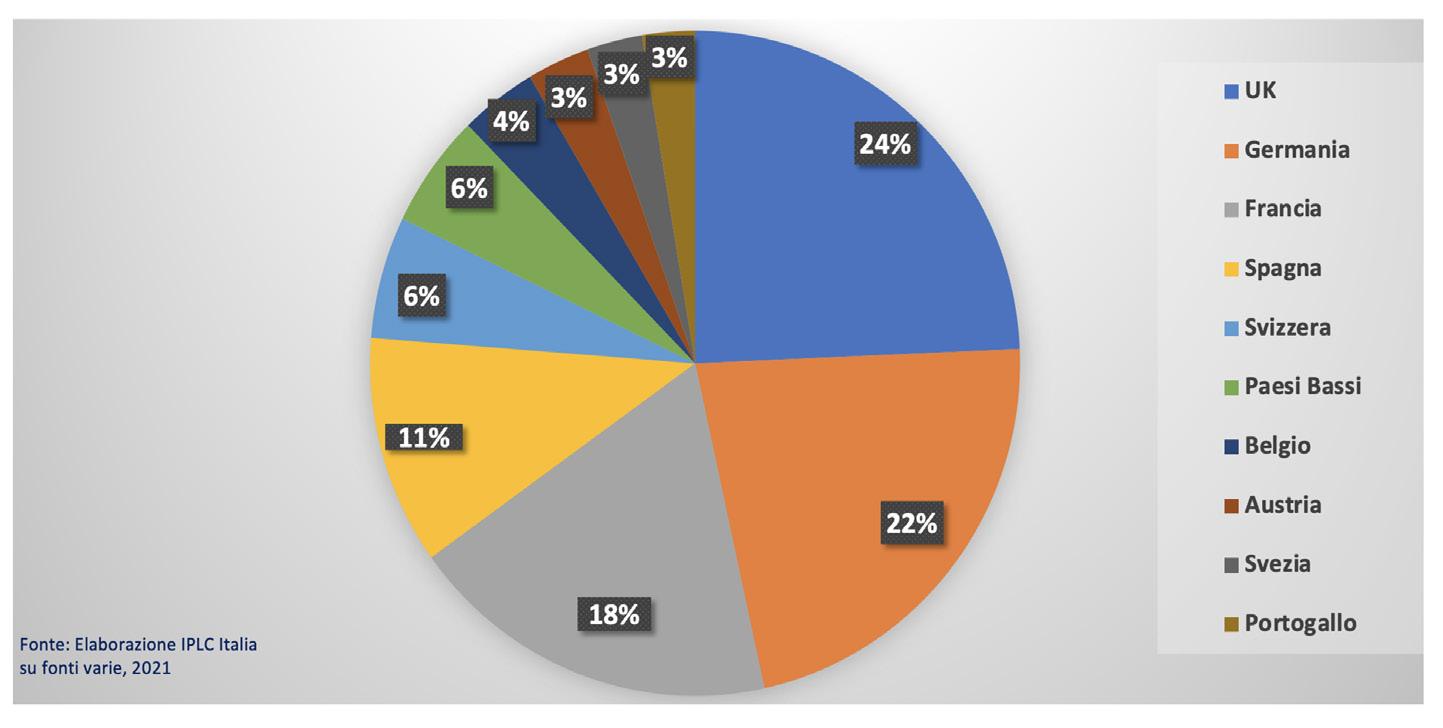

According to an estimate made by IPLC Italy on 2021 data shows the "pie" of PL sales, comprising some of the major countries in Europe, excluding Italy, is more than 250 billion euros, and this value is likely to increase, not only because of the effect of the inflation, but also because of PL’s greater appeal in this point in time.

UK

Germany France

Spain Switzerland

Netherlands

Belgium Austria

Sweden

Portugal

COMPETITION IN LARGE-SCALE DISTRIBUTION: THE DISCOUNT CHANNEL, IMITATION OR DIVERSIFICATION?

The rising inflation, the uncertainty over costs and demand reactions, are leading to a buzz in Italian retail, which sometimes appears ‘unsure’ in defining strategies. Some are turning to partnerships and, when possible, mergers and acquisitions (including from abroad), while others are trying to relaunch strategy and positioning while staying within their own borders. Faced with the demand for saving and the success of discounters, some retailers seek to distance themselves from them as far as possible, establishing their own positioning and business model, opposed to that of discounters. Others, however, seek partial "discounting" solutions to their business model. In this second case, the risk is that retailers with a good identity and not ‘natives discounters’ try to imitate only some aspects that, alone, cannot generate the unique competitive advantage of discounters.

An analysis conducted by IPLC at the European level shows that all the connotative and distinctive elements of the discounter model present in the different stages of the supply chain, up to sales points and retail marketing, lead to a profitable combination of their individual variables (efficiency

of production, logistics, retail, personnel, services, PL assortment, etc.), which is actually up to 5% higher than non-discounter business models.

A percentage that, when compared to an average range of the net profit of retail grocery chains in Europe, can definitely make a difference, especially if this model is still able to adapt, becoming attractive, not only in terms of perceived convenience, but also in terms of accessibility and perceived value. For instance, after three years of its project involving the PL Jack's and PL discount stores launched in late 2018, Tesco's recent experience was a failure. Here again, as happened in Italy, we see that being a qualified retailer is not enough to launch a successful discount chain. To make Tesco stores competitive, the same selling price of Aldi stores has been adopted for a few hundred PL products ("Aldi Price Match" campaign) with a punctual and direct comparative approach in communication that Italy seems to be reluctant to adopt. Tesco claims that the quality of these products hasn’t changed, but has launched a discount product line with a higher perceived quality than the Tesco PL, due to its packaging, as shown in the image below. Shall we speak of confusion or constant experimentation?

Paolo Palomba Managing Partner Expertise on Field/partner IPLC Italy

Source: IPLC

CONCLUSION

With very rare exceptions, a complete, clear, well-articulated and qualified PL supply is not an option for distributors, but rather a need. However, PL is now an opportunity perhaps not only for them but also for SMEs that, thanks to PL products,can enter the market (shelves) more easily, export with zero investments in communication, brands and distribution. Even for the brand industry, PL would be an opportunity, who knows how many have actually noticed that.