6 minute read

KEY LEGAL LEVERS IN THE RACE TO DECARBONISE

KEY LEGAL LEVERS IN THE RACE TO DECARBONISE

As mining companies innovate and collaborate to meet both voluntary and mandated decarbonisation targets, they also need to keep an eye on fast-changing legislation.

Jo Garland, APAC Energy Transition Lead and Partner at HFW, discusses the main legislative levers in the decarbonisation journey and how miners are managing these legal levers.

ENERGY + MINES: How has the first year of the Safeguard Mechanism been for miners and how are compliance strategies evolving?

JO GARLAND: With the first Safeguard Mechanism reports due this October, miners affected by the scheme (i.e. those who produce more than 100,000 tonnes of CO2-e per year) have been considering the availability, cost and timeframe for adopting emissions reductions technologies to meet the mandatory annual 4.9% scope 1 emissions intensity reduction.

The real test of compliance strategies will come when the first reports are due, but these are evolving to:

• Better understand and define the mine’s carbon footprint and what needs to be done to increase confidence in emissions data, including through the use of digital measurement and reporting applications.

• Map where current assets are in their useful lifecycle –and when the desired technology will become available on a mass scale, and at what capital outlay.

• Weigh the timeframes and costs of the available technology with the costs of purchasing Australian Carbon Credit Units (ACCUs) in lieu of the mandated emissions reductions. ACCUs can be used to demonstrate a reduction in emissions intensity, but miners will be required to provide a “written explanation of why more carbon abatement was not undertaken” if their total number is greater than 30% of their baseline footprint. This explanation will be published by the Clean Energy Regulator, with a degree of “naming and shaming” of companies who are heavily relying on offsets. Miners also need to be aware that they are competing with the big oil and gas companies in the race to purchase ACCUs.

Pressure on large miners to decarbonise is also increasing because of the new climate-related financial disclosures regime, under which all Safeguard Mechanism facilities, as well as other large entities that meet threshold tests, will need to publish annual sustainability reports.

Reporting will be mandatory and phased in from 1 July 2024, and much like under the Safeguard Mechanism, there are significant penalties for non-compliance. ASIC has the power to issue directions to test the veracity of statements made in sustainability reports, so directors need to ensure that they have accurate and reliable climate data to meet their reporting obligations.

EM: What are some of the challenges you’re seeing with electric vehicle infrastructure as miners move ahead with electrification? What about the proposed changes in fuel efficiency standards?

JG: In my experience, WA is not currently seen as a particularly attractive market for electric vehicles, because we do not yet have any legislation phasing out fossil fuel cars and heavy freight or requiring manufacturers to report on how many zero emissions vehicles they are selling to a region. Manufacturers of electric vehicles and charging infrastructure are drawn to markets where there is a clear legislated demand. While miners have net zero targets and the biggest emitters have legislated requirements to reduce their scope 1 emissions, this hasn’t been directly tied in with electric vehicles and charging infrastructure.

This may be set to change if the government legislates its proposed fuel efficiency standard, which is expected to come into effect from 1 January 2025. The government is underpinning this with the rollout of funding for charging infrastructure.

However, this is not as simple as just installing electric vehicle chargers along key freight routes: a mine site may have several trucks that it needs to charge en route from a mine site to its destination, and often in regional areas. Each of these trucks needs to fast-charge with more electricity in half an hour than an entire regional town may use on their peak day for electricity use. This may result in congestion and wait times if there is insufficient power capacity within regional areas to charge multiple vehicles simultaneously. So, in addition to installing chargers, we will also need to ensure that there is the surrounding electricity infrastructure and capacity to support short but steep spikes in electricity needs.

Lastly, like many other aspects of renewable energy projects, getting the approvals for electric vehicle charging infrastructure on grid-connected mines can take years. Conversely, off-grid electric vehicle infrastructure that is powered by renewables and supported by BESS needs to be continuously reliable so as to avoid disruptions to operations.

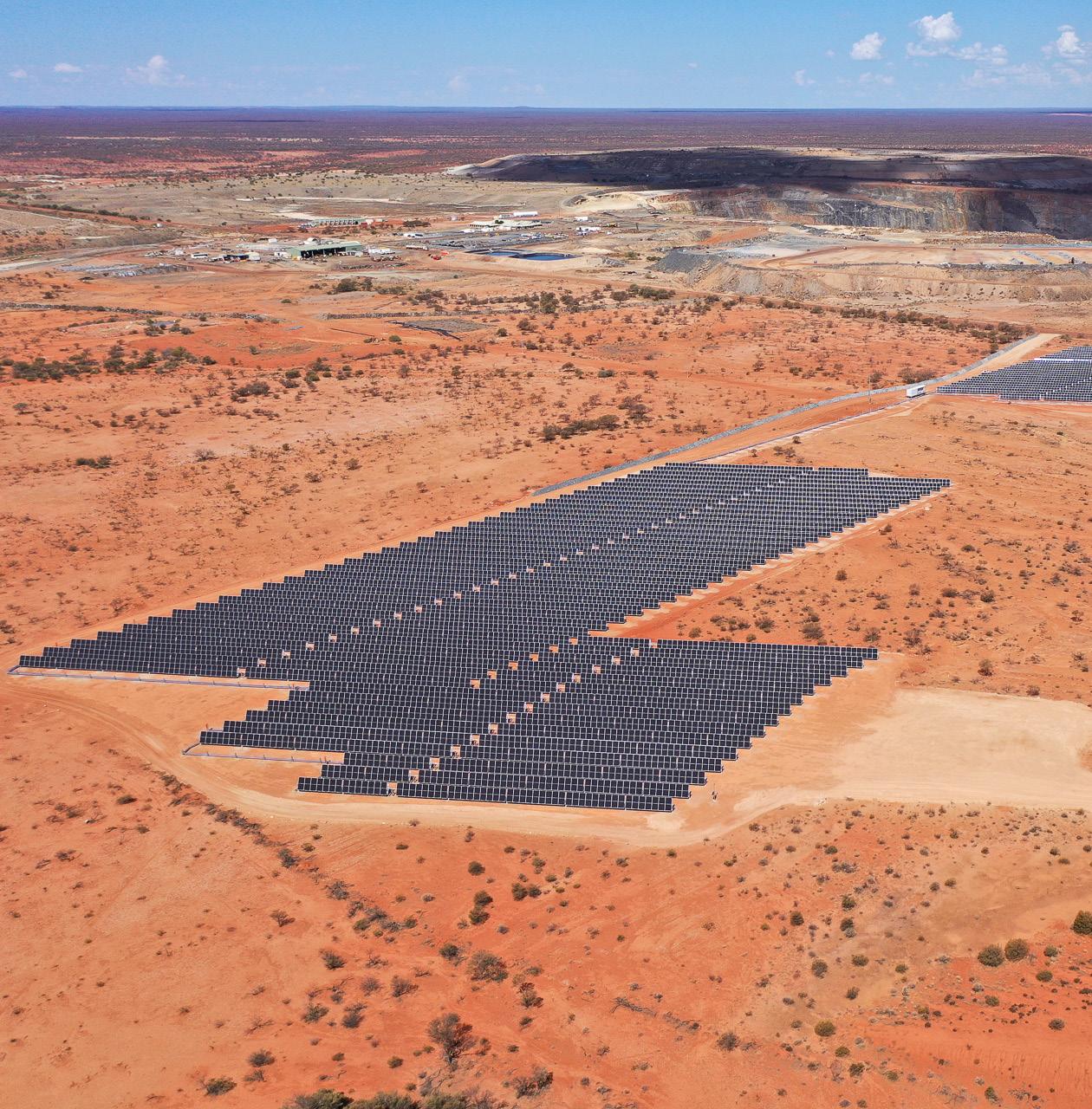

EM: How would you say deal structures for hybrid/renewable mine power systems have changed since you were involved in the first remote hybrid power system for the DeGrussa mine?

JG: The ambition, scale and renewable energy penetration levels have increased exponentially since DeGrussa, which was just under 10 years ago. We’re seeing more phased developments starting with gas, solar and potentially BESS – and then looking to wind in later phases. Single standalone systems are being replaced with smart renewable microgrids at scale, with very high levels of renewable energy output.

The main contracting structures of build, own, operate (BOO) or a variation of that, or straight EPC model are still the most used – but we’re seeing more parties involved in the construction and technology provision (larger and more complex) projects. Tariff structures still don’t seem to have progressed as much as they potentially could – and guarantees offered seem to be settling into an industry norm.

EM: Do you see opportunities for collaboration on renewables for mining companies in WA, and what are some of the legal implications of joining forces on infrastructure?

JG: Opportunities in the Pilbara will only grow, especially with the $3billion rewiring the nation to fund transmission in the Pilbara, the proposed hydrogen hub in Maitland and other mega-renewable hubs.

Collaboration around power for the mid-tier miners will depend on location, but we could potentially see shared electric vehicle or hydrogen fueling infrastructure. There are also many opportunities for forward-thinking mid-tiers to partner with technology providers and energy developers to pilot the new decarbonisation or renewable energy technology – benefiting the mine and advancing the technology to scale. Joining forces on infrastructure needs to be carefully managed from a legal perspective. Australian competition law prevents any arrangements that could substantially lessen/foreclose competition, be seen as an attempt to fix prices or terms between competitors or as an abuse of market power by one party. Who owns intellectual property or improvements on that IP from pilots also needs to be worked through and parties collaborating should be clear on what they want to get out of the collaboration.