Higginbotham Public Sector (866) 914-5202 www.gcisdbenefits.com

Marlena Moreno (817) 251-5577 marlena.moreno@gcisd.net

Allegiance Group #1008109 (855) 999-6808

https://www.ubc-benefits.com/ gcisd-benefits

Clever RX Group #108

Member ID: 1746 (800) 974-3135 www.cleverrx.com/grapevinecolleyville

The Hartford Group #395308 (866) 547-4205 www.thehartford.com

Recuro (855) 673-2876 www.recurohealth.com

(800) 333-9934 www.eecu.org

The Hartford Group #395308 (866) 547-4205 www.thehartford.com

Unum Group #657072 (800) 858-6843 www.unum.com

Cigna Group #3335893 (800) 244-6224 www.mycigna.com

Superior Vision Group #30386 (800) 507-3800 www.superiorvision.com

The Hartford Group #395308 (866) 547-4205 www.thehartford.com CHUBB Group #1000000198 (888) 499-0425 educatorclaims@chubb.com

National Benefit Services (800) 274-0503 www.nbsbenefits.com

Deer Oaks EAP Services (866) 327-2400 www.deeroakseap.com user/password: gvinecolley 403(b)/457 PLANS

National Benefits Services (800) 274-0503 www.nbsbenefits.com

1 www.gcisdbenefits.com

2

CLICK LOGIN

3 Enter your Information

• Last Name

• Date of Birth

• Last Four (4) of Social Security Number

NOTE: THEbenefitsHUB uses this information to check behind the scenes to confirm your employment status.

4

5

Once confirmed, the Additional Security Verification page will list the contact options from your profile. Select either Text, Email, Call, or Ask Admin options to receive a code to complete the final verification step.

Enter the code that you receive and click Verify. You can now complete your benefits enrollment!

During your annual enrollment period, you have the opportunity to review, change or continue benefit elections each year. Changes are not permitted during the plan year (outside of annual enrollment) unless a Section 125 qualifying event occurs.

• Changes, additions or drops may be made only during the annual enrollment period without a qualifying event.

• Employees must review their personal information and verify that dependents they wish to provide coverage for are included in the dependent profile. Additionally, you must notify your employer of any discrepancy in personal and/or benefit information.

• Employees must confirm on each benefit screen (medical, dental, vision, etc.) that each dependent to be covered is selected in order to be included in the coverage for that particular benefit.

All new hire enrollment elections must be completed in the online enrollment system within the first 30 days of benefit eligibility employment. Failure to complete elections during this timeframe will result in the forfeiture of coverage.

For supplemental benefit questions, you can contact your Benefits Office or you can call Higginbotham Public Sector at 866-914-5202 for assistance.

For benefit summaries and claim forms, go to your benefit website: www.gcisdbenefits.com Click the benefit plan you need information on (i.e., Dental) and you can find the forms you need under the Benefits and Forms section.

For benefit summaries and claim forms, go to the Grapevine-Colleyville ISD benefit website: www.gcisdbenefits.com. Click on the benefit plan you need information on (i.e., Dental) and you can find provider search links under the Quick Links section.

If the insurance carrier provides ID cards, you can expect to receive those 3-4 weeks after your effective date. For most dental and vision plans, you can log in to the carrier website and print a temporary ID card or simply give your provider the insurance company’s phone number, and they can call and verify your coverage if you do not have an ID card at that time. If you do not receive your ID card, you can call the carrier’s customer service number to request another card.

If the insurance carrier provides ID cards, but there are no changes to the plan, you typically will not receive a new ID card each year.

A Cafeteria plan enables you to save money by using pre-tax dollars to pay for eligible group insurance premiums sponsored and offered by your employer. Enrollment is automatic unless you decline this benefit. Elections made during annual enrollment will become effective on the plan effective date and will remain in effect during the entire plan year.

Marital Status

Change in Number of Tax Dependents

Change in Status of Employment Affecting Coverage Eligibility

Gain/Loss of Dependent’s Eligibility Status

Judgment/ Decree/Order

Eligibility for Government Programs

Changes in benefit elections can occur only if you experience a qualifying event. You must present proof of a qualifying event to your Benefit Office within 30 days of your qualifying event and meet with your Benefits Office to complete and sign the necessary paperwork in order to make a benefit election change. Benefit changes must be consistent with the qualifying event.

A change in marital status includes marriage, death of a spouse, divorce or annulment (legal separation is not recognized in all states).

A change in number of dependents includes the following: birth, adoption and placement for adoption. You can add existing dependents not previously enrolled whenever a dependent gains eligibility as a result of a valid change in status event.

Change in employment status of the employee, or a spouse or dependent of the employee, that affects the individual’s eligibility under an employer’s plan includes commencement or termination of employment.

An event that causes an employee’s dependent to satisfy or cease to satisfy coverage requirements under an employer’s plan may include change in age, student, marital, employment or tax dependent status.

If a judgment, decree, or order from a divorce, annulment or change in legal custody requires that you provide accident or health coverage for your dependent child (including a foster child who is your dependent), you may change your election to provide coverage for the dependent child. If the order requires that another individual (including your spouse and former spouse) covers the dependent child and provides coverage under that individual’s plan, you may change your election to revoke coverage only for that dependent child and only if the other individual actually provides the coverage.

Gain or loss of Medicare/Medicaid coverage may trigger a permitted election change.

Supplemental Benefits: Eligible employees must work 20 or more regularly scheduled hours each work week.

Eligible employees must be actively at work on the plan effective date for new benefits to be effective, meaning you are physically capable of performing the functions of your job on the first day of work concurrent with the plan effective date. For example, if your 2024 benefits become effective on September 1, 2024, you must be actively-at-work on September 1, 2024 to be eligible for your new benefits.

Dependent Eligibility: You can cover eligible dependent children under a benefit that offers dependent coverage, provided you participate in the same benefit, through the maximum age listed below. Dependents cannot be double covered by married spouses within the district as both employees and dependents.

Please note, limits and exclusions may apply when obtaining coverage as a married couple or when

Potential Spouse Coverage Limitations: When enrolling in coverage, please keep in mind that some benefits may not allow you to cover your spouse as a dependent if your spouse is enrolled for coverage as an employee under the same employer. Review the applicable plan documents, contact Higginbotham Public Sector, or contact the insurance carrier for additional information on spouse eligibility.

FSA/HSA Limitations: Please note, in general, per IRS regulations, married couples may not enroll in both a Flexible Spending Account (FSA) and a Health Savings Account (HSA). If your spouse is covered under an FSA that reimburses for medical expenses then you and your spouse are not HSA eligible, even if you would not use your spouse’s FSA to reimburse your expenses. However, there are some exceptions to the general limitation regarding specific types of FSAs. To obtain more information on whether you can enroll in a specific type of FSA or HSA as a married couple, please reach out to the FSA and/or HSA provider prior to enrolling or reach out to your tax advisor for further guidance.

Potential Dependent Coverage Limitations: When enrolling for dependent coverage, please keep in mind that some benefits may not allow you to cover your eligible dependents if they are enrolled for coverage as an employee under the same employer. Review the applicable plan documents, contact Higginbotham Public Sector, or contact the insurance carrier for additional information on dependent eligibility.

Disclaimer: You acknowledge that you have read the limitations and exclusions that may apply to obtaining spouse and dependent coverage, including limitations and exclusions that may apply to enrollment in Flexible Spending Accounts and Health Savings Accounts as a married couple. You, the enrollee, shall hold harmless, defend, and indemnify Higginbotham Public Sector from any and all claims, actions, suits, charges, and judgments whatsoever that arise out of the enrollee’s enrollment in spouse and/or dependent coverage, including enrollment in Flexible Spending Accounts and Health Savings Accounts.

If your dependent is disabled, coverage may be able to continue past the maximum age under certain plans. If you have a disabled dependent who is reaching an ineligible age, you must provide a physician’s statement confirming your dependent’s disability. Contact your Benefits Office to request a continuation of coverage.

You are performing your regular occupation for the employer on a full-time basis, either at one of the employer’s usual places of business or at some location to which the employer’s business requires you to travel. If you will not be actively at work beginning 9/1/2024 please notify your benefits administrator.

The period during which existing employees are given the opportunity to enroll in or change their current elections.

The amount you pay each plan year before the plan begins to pay covered expenses.

January 1st through December 31st

After any applicable deductible, your share of the cost of a covered health care service, calculated as a percentage (for example, 20%) of the allowed amount for the service.

The amount of coverage you can elect without answering any medical questions or taking a health exam. Guaranteed coverage is only available during initial eligibility period. Actively-at-work and/or preexisting condition exclusion provisions do apply, as applicable by carrier.

Doctors, hospitals, optometrists, dentists and other providers who have contracted with the plan as a network provider.

The most an eligible or insured person can pay in coinsurance for covered expenses.

September 1st through August 31st

Applies to any illness, injury or condition for which the participant has been under the care of a health care provider, taken prescriptions drugs or is under a health care provider’s orders to take drugs, or received medical care or services (including diagnostic and/or consultation services).

Description

Health Savings Account (HSA) (IRC Sec. 223)

Approved by Congress in 2003, HSAs are actual bank accounts in employees’ names that allow employees to save and pay for unreimbursed qualified medical expenses tax-free.

Employer Eligibility A qualified high deductible health plan

Contribution Source Employee and/or employer

Account Owner Individual

Underlying Insurance

Requirement

Minimum Deductible

Maximum Contribution

High deductible health plan

$1,600 single (2024)

$3,200 family (2024)

$4,150 single (2024)

$8,300 family (2024) 55+ catch up +$1,000

Permissible Use Of Funds

Cash-Outs of Unused Amounts (if no medical expenses)

Year-to-year rollover of account balance?

Does the account earn interest?

Portable?

Employees may use funds any way they wish. If used for non-qualified medical expenses, subject to current tax rate plus 20% penalty.

Flexible Spending Account (FSA) (IRC Sec. 125)

Allows employees to pay out-of-pocket expenses for copays, deductibles and certain services not covered by medical plan, taxfree. This also allows employees to pay for qualifying dependent care tax- free.

All employers

Employee and/or employer

Employer

None

N/A

$3,200 (2024)

Reimbursement for qualified medical expenses (as defined in Sec. 213(d) of IRC).

Permitted, but subject to current tax rate plus 20% penalty (penalty waived after age 65). Not permitted

Yes, will roll over to use for subsequent year’s health coverage.

Yes

Yes, portable year-to-year and between jobs.

No. Access to some funds may be extended if your employer’s plan contains a 2 1/2 –month grace period or $500 rollover provision.

No

No

Major medical insurance is a type of health care coverage that provides benefits for a broad range of medical expenses that may be incurred either on an inpatient or outpatient basis.

For full plan details, please visit your benefit website: www.gcisdbenefits.com

The GCISD medical plans with Allegiance, offer a range of coverage options allowing you a great deal of flexibility to best meet the needs of you and your family.

ID Card replacements maybe ordered by calling Allegiance or online at: www.AskAllegiance.com/UBC-LevelFundedPlans>FORMS

Carrier Contact information on page 3 of this guide.

Prescription questions may be directed to 800.933.0765 or rxbenefits.com.

Medical plan questions may be directed to help@ubc-benefits.com.

Basic HD is the only GCISD plan that is compatible with a health savings account (HSA).

A Health Savings Account (HSA) is a personal savings account where the money can only be used for eligible medical expenses. Unlike a flexible spending account (FSA), the money rolls over year to year however only those funds that have been deposited in your account can be used. Contributions to a Health Savings Account can only be used if you are also enrolled in a High Deductible Health Care Plan (HDHP). For full plan details, please visit your benefit website: www.mybeneitshub.com/sampleisd

www.gcisdbenefits.com

A Health Savings Account (HSA) is more than a way to help you and your family cover health care costs – it is also a tax-exempt tool to supplement your retirement savings and cover health expenses during retirement. An HSA can provide the funds to help pay current health care expenses as well as future health care costs.

A type of personal savings account, an HSA is always yours even if you change health plans or jobs. The money in your HSA (including interest and investment earnings) grows tax-free and spends tax-free if used to pay for qualified medical expenses. There is no “use it or lose it” rule — you do not lose your money if you do not spend it in the calendar year — and there are no vesting requirements or forfeiture provisions. The account automatically rolls over year after year.

You are eligible to open and contribute to an HSA if you are:

• Enrolled in an HSA-eligible HDHP (High Deductible Health Plan) Not covered by another plan that is not a qualified HDHP, such as your spouse’s health plan

• Not enrolled in a Health Care Flexible Spending Account, nor should your spouse be contributing towards a Health Care Flexible Spending Account

• Not eligible to be claimed as a dependent on someone else’s tax return

• Not enrolled in Medicare or TRICARE

• Not receiving Veterans Administration benefits

You can use the money in your HSA to pay for qualified medical expenses now or in the future. You can also use HSA funds to pay health care expenses for your dependents, even if they are not covered under your HDHP.

Your HSA contributions may not exceed the annual maximum amount established by the Internal Revenue Service. The annual contribution maximum for 2024 is based on the coverage option you elect:

• Individual – $4,150

• Family (filing jointly) – $8,300

You decide whether to use the money in your account to pay for qualified expenses or let it grow for future use. If you are 55 or older, you may make a yearly catch-up contribution of up to $1,000 to your HSA. If you turn 55 at any time during the plan year, you are eligible to make the catch-up contribution for the entire plan year.

If you meet the eligibility requirements, you may open an HSA administered by EECU. You will receive a debit card to manage your HSA account reimbursements. Keep in mind, available funds are limited to the balance in your HSA.

• Always ask your health care provider to file claims with your medical provider so network discounts can be applied. You can pay the provider with your HSA debit card based on the balance due after discount.

• You, not your employer, are responsible for maintaining ALL records and receipts for HSA reimbursements in the event of an IRS audit.

• You may open an HSA at the financial institution of your choice, but only accounts opened through EECU are eligible for automatic payroll deduction and company contributions.

• Online/Mobile: Sign-in for 24/7 account access to check your balance, pay bills and more.

• Call/Text: (817) 882-0800 EECU’s dedicated member service representatives are available to assist you with any questions. Their hours of operation are Monday through Friday from 8:00 a.m. to 7:00 p.m. CT, Saturday 9:00 a.m. to 1:00 p.m. CT and closed on Sunday.

• Lost/Stolen Debit Card: Call the 24/7 debit card hotline at (800)333-9934.

• Stop by a local EECU financial center: www.eecu.org/ locations.

Download your Clever RX card or Clever RX App to unlock exclusive savings.

Present your Clever RX App or Clever RX card to your pharmacist.

ST EP 1:

Download the FREE Clever RX App. From your App Store search for "Clever RX" and hit download. Make sure you enter in Group ID and in Member ID during the on-boarding process. This will unlock exclusive savings for you and your family!

ST EP 2 :

Find where you can save on your medication. Using your zip code, when you search for your medication Clever RX checks which pharmacies near you offer the lowest price. Savings can be up to 80% compared to what you're currently paying.

FREE to use. Save up to 80% off prescription drugs and beat copay prices.

Accepted at most pharmacies nationwide ST AR T SA VI NG TOD AY W

100% FREE to use

Unlock discounts on thousands of medications

Save up to 80% off prescription drugs – often beats the average copay

Over 7 0% of peopl e c an benefi t fro m a pre sc rip ti on sav ing s c ard due t o high dedu ct ible heal t h plan s, high c opa ys , and being unde r in s ured or u ni ns ur ed

ST EP 3 :

Click the voucher with the lowest price, closest location, and/or at your preferred pharmacy. Click "share" to text yourself the voucher for easy access when you are ready to use it. Show the voucher on your screen to the pharmacist when you pick up your medication.

ST EP 4:

Share the Clever RX App. Click "Share" on the bottom of the Clever RX App to send your friends, family, and anyone else you want to help receive instant discounts on their prescription medication. Over 70% of people can benefit from a prescription savings card.

TH A T IS N O T ONLY CL EVER, I T IS CL EVE R RX .

DID Y OU KNOW?

Ov er 3 0 % of

This is an affordable supplemental plan that pays you should you be inpatient hospital confined. This plan complements your health insurance by helping you pay for costs left unpaid by your health insurance. For full plan details, please visit your benefit website: www.gcisdbenefits.com

The Hartford’s Hospital Indemnity (HI) insurance pays a cash benefit if you or an insured dependent (spouse or child) are confined in a hospital for a covered illness or injury. Even with the best primary health insurance plan, out-of-pocket costs from a hospital stay can add up. The benefits are paid in lump sum amounts to you, and can help offset expenses that primary health insurance doesn’t cover (like deductibles, co-insurance amounts or co- pays), or benefits can be used for any non-medical expenses (like housing costs, groceries, car expenses, etc.).

Claim form is on the benefit website, group number and carrier contact details on page 3 of this guide.

You have a choice of three hospital indemnity plans, which allows you the flexibility to enroll for the coverage that best meets your needs. Benefit amounts are based on the plan in effect for you or an insured dependent at the time the covered event occurs.

Dental insurance is a coverage that helps defray the costs of dental care. It insures against the expense of routine care, dental treatment and disease.

For full plan details, please visit your benefit website: www.gcisdbenefits.com

Coverage is provided through Cigna. Two levels of benefits are available with the DPPO plan: in-network and out-ofnetwork. You may select the dental provider of your choice, but your level of coverage may vary based on the provider you see for services. You could pay more if you use an out-of-network provider.

You can request your dental ID card by contacting Cigna directly or go to www.mycigna.com and register/login to access your account. In addition, you can download the “MyCigna” app on your smartphone and access your id card right there on your phone. Group Number and carrier contact information on page 3.

To search for a dentist on Cigna.com, visit the site and click “Find a Doctor, Dentist or Facility.” Follow the prompts on screen and when asked to choose your plan, select “DPPO/EPO > Total Cigna DPPO.” Or call Cigna for assistance, group number and contact information on page 3.

In-network dentists will file claims on your behalf. Claim Reimbursement forms on benefits website, group number and carrier contact on page 3.

GCISD Cigna Dental Choice Plan Summary

Please see plan documents for details and limitations

Preventive and Diagnostic Care Exams, cleanings, X-rays, fluoride treatments, sealants, space maintainers

Basic Restorative Care

Fillings, minor oral surgery, Emergency Care to Relieve Pain

Major Restorative Care/Implants Crowns, dentures, bridges, periodontics, endodontics, implants

Not a dental insurance plan, QCD is a discount dental program which offers discounted services through QCD Affiliated Dentists. This program is provided to enrolled employees for $0 cost, one dependent may be added at $10 per month or family coverage is $14 per month. Need more information, please visit www.qcdofamerica.com or call 800-229-0304.

Vision insurance provides coverage for routine eye examinations and can help with covering some of the costs for eyeglass frames, lenses or contact lenses.

For full plan details, please visit your benefit website: www.gcisdbenefits.com

Our vision plan provides quality care to help preserve your health and eyesight. In addition to identifying vision and eye problems, regular exams can detect certain medical issues such as diabetes and high cholesterol. You may seek care from any licensed optometrist, ophthalmologist or optician, but plan benefits offer better value if you use an in-network provider. Premium contributions are deducted from your paycheck on a pretax basis. Coverage is provided through Superior Vision.

Visit www.superiorvision.com select “Find an Eye Care Professional”. Coverage Info is “Insurance Through Your Employer” then Choose Your Network “Superior National” or call 1 (800) 507-3800 for assistance. Group Number and additional Carrier information found on page 3.

• Scratch Coat (factory)

• Polycardonate for deps to age 18

• Anti-reflective coarting (standard)

• Ultraviolet coating

Disability insurance protects one of your most valuable assets, your paycheck. This insurance will replace a portion of your income in the event that you become physically unable to work due to sickness or injury for an extended period of time.

For full plan details, please visit your benefit website: www.gcisdbenefits.com

Disability insurance combines the features of a short-term and long-term disability plan into one policy. The coverage pays you a portion of your earnings if you cannot work because of a disabling illness or injury. The plan gives you the flexibility to choose a level of coverage to suit your need. This coverage is provided by The Hartford.

CLAIMS: Call The Hartford Claims at 866-547-9124 to file a claim, group number on page 3.

Effective Date: Coverage goes into effect subject to the terms and conditions of the policy. You must satisfy the definition of Actively at Work with your employer on the day your coverage takes effect.

Benefit Amount: You may purchase coverage that will pay you a monthly flat dollar benefit in $100 increments between $200 and $7,500 that cannot exceed 66 2/3% of your current monthly earnings. Earnings are defined in The Hartford’s contract with your employer.

Elimination Period: You must be disabled for at least the number of days indicated by the elimination period that you select before you can receive a Disability benefit payment. The elimination period that you select consists of two numbers. The first number shows the number of days you must be disabled by an accident before your benefits can begin. The second number indicates the number of days you must be disabled by a sickness before your benefits can begin. For those employees electing an elimination period of 30 days or less, if your are confined to a hospital for 24 hours or more due to a disability, the elimination period will be waived, and benefits will be payable from the first day of hospitalization.

Definition of Disability: Disability is defined as The Hartford’s contract with your employer. Typically, disability means that you cannot perform one or more of the essential duties of your occupation due to injury, sickness, pregnancy or other medical conditions covered by the insurance, and as a result, your current monthly earnings are 80% or less of your pre-disability earnings. One you have been disabled for 24 months, you must be prevented from performing one or more essential duties of any occupation, and as a result, your monthly earnings are 66 2/3% or less of your pre-disability earnings.

Pre-Existing Condition Limitation: Your policy limits the benefits you can receive for a disability caused by a pre-existing condition. In general, if you were diagnosed or received care for a disabling condition within the 6 consecutive months just prior to the effective date of this policy, your benefit payment will be limited, unless: You have not received treatment

for the disabling condition within 6 months, while insured under this policy, before the disability begins, or You have been insured under this policy for 12 months before your disability begins. If your disability is a result of a pre-existing condition, the carrier will pay benefits for a maximum of 4 weeks.

Maximum Benefit Duration: Benefit Duration is the maximum time for which the carrier will pay benefits for disability resulting from sickness or injury. Depending on the age at which disability occurs, the maximum duration may vary. Please see the applicable schedules below based on the Premium benefit option.

Age Disabled Maximum Benefit Duration

Prior to 63 To Normal Retirement Age or 48 months if greater

Age 63 To Normal Retirement Age or 42 months if greater

Age 64 36 months

Age 65 30 months

Age 66 27 months

Age 67 24 months

Age 68 21 months

Age 69 and older 18 months

General Exclusions: You cannot receive Disability benefit payments for disabilities that are caused or contributed to by:

• War or act of war (declared or not)

• Military service for any country engaged in war or other armed conflict

• The commission of, or attempt to commit a felony

• An intentionally self-inflicted injury

• Any case where your being engaged in an illegal occupation was a contributing cause to your disability

• You must be under the regular care of a physician to receive benefits

*If because of your disability you are hospital confined as inpatient, benefits begin on the first day of inpatient confinement.

What is disability insurance? Disability insurance protects one of your most valuable assets, your paycheck. This insurance will replace a portion of your income in the event that you become physically unable to work due to sickness or injury for an extended period of time. This type of disability plan is called an educator disability plan and includes both long and short term coverage into one convenient plan.

Pre-Existing Condition Limitations - Please note that all plans will include pre-existing condition limitations that could impact you if you are a first-time enrollee in your employer’s disability plan. This includes during your initial new hire enrollment. Please review your plan details to find more information about preexisting condition limitations.

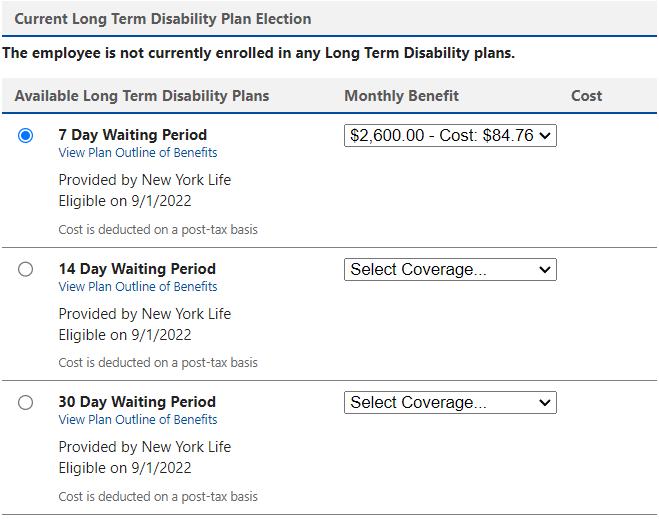

How do I choose which plan to enroll in during my open enrollment?

1. First choose your elimination period. The elimination period, sometimes referred to as the waiting period, is how long you are disabled and unable to work before your benefit will begin. This will be displayed as 2 numbers such as 0/7, 14/14, 30/30, 60/60, 90/90, etc.

The first number indicates the number of days you must be disabled due to Injury and the second number indicates the number of days you must be disabled due to Sickness

When choosing your elimination period, ask yourself, “How long can I go without a paycheck?” Based on the answer to this question, choose your elimination period accordingly.

Important Note- some plans will waive the elimination period if you choose 30/30 or less and you are confined as an inpatient to the hospital for a specific time period. Please review your plan details to see if this feature is available to you.

2. Next choose your benefit amount. This is the maximum amount of money you would receive from the carrier on a monthly basis once your disability claim is approved by the carrier.

When choosing your monthly benefit, ask yourself, “How much money do I need to be able to pay my monthly expenses?” Based on the answer to this question, choose your monthly benefit accordingly.

Choose your desired elimination period.

Choose your Benefit Amount from the drop down box.

Do you have kids playing sports, are you a weekend warrior, or maybe you’re accident-prone? Accident plans are designed to help pay for medical costs associated with accidents and benefits are paid directly to you.

For full plan details, please visit your benefit website: www.gcisdbenefits.com

With Accident insurance provided through The Hartford, you’ll receive cash benefits when injuries, medical treatment and/or services occur as the result of a covered accident. You can use the payment in any way you choose – from expenses not covered by your major medical plan to day-to-day costs of living such as the mortgage or utility bills.

Claims forms available Benefit Website. Group number and carrier contact information is on page 3.

Cancer insurance offers you and your family supplemental insurance protection in the event you or a covered family member is diagnosed with cancer. It pays a benefit directly to you to help with expenses associated with cancer treatment.

For full plan details, please visit your benefit website: www.gcisdbenefits.com

A cancer diagnosis and treatment can be an emotionally and physically difficult time. Chubb is there to help support you by providing cash benefits paid directly to you. Benefits are paid if you are diagnosed with cancer, but also help cover many other cancer-related services such as doctor’s visits, treatments, specialty care, and recovery. However, there are no restrictions on how to use these cash benefits—so you can use them as you see fit.

Cash benefits for every step of the way. Choose the right level of coverage during the enrollment period to better protect your family. Following is a sample of the benefits provided, please review plan documents on the benefit website for details.

First cancer benefit

Diagnosis of cancer

Hospital confinement

Hospital confinement ICU

Radiation therapy, chemotherapy, immunotherapy

Skin cancer initial diagnosis

Heart attack or stroke

$100 paid upon receipt of first covered claim for cancer; only one payment per covered person per certificate per calendar year

$5,000 employee or spouse

$7,500 child(ren)

Waiting period: 0 days

Benefit reduction: none

$100 per day – days 1 through 30

Additional days: $200

Maximum days per confinement: 31

$600 per day – days 1 through 30

Additional days: $600

Maximum days per confinement: 31

Maximum per covered person per calendar year per 12-month period: $10,000

$100 per diagnosis

Lifetime maximum: 1

$5,000

Recurrence benefit: $2,500

Waiting period: 0 days

Benefit reduction: none

$100 paid upon receipt of first covered claim for cancer; only one payment per covered person per certificate per calendar year

$10,000 employee or spouse

$15,000 child(ren)

Waiting period: 0 days

Benefit reduction: none

$300 per day – days 1 through 30

Additional days: $600

Maximum days per confinement: 31

$600 per day – days 1 through 30

Additional days: $600

Maximum days per confinement: 31

Maximum per covered person per calendar year per 12-month period: $20,000

$100 per diagnosis

Lifetime maximum: 1

$10,000

Recurrence benefit: $5,000

Waiting period: 0 days

Benefit reduction: none

Bone marrow or stem cell transplant

First bone marrow transplant: $6,000

Additional transplant: 50%

Lifetime maximum transplant(s): 2

First stem cell transplant: $600

Additional transplant: 50%

Lifetime maximum transplant(s): 2

Surgery Up to $3,000

Breast TRAM flap: $2,000

Breast reconstruction: $500

Reconstructive surgery

Skin cancer surgery

Specialty Care Benefits

Family member transportation and lodging

Home health care

Pre-existing conditions limitation

Breast symmetry: $500

Facial reconstruction: $500

$100

First bone marrow transplant: $9,000

Additional transplant: 50%

Lifetime maximum transplant(s): 2

First stem cell transplant: $900

Additional transplant: 50%

Lifetime maximum transplant(s): 2

to $4,800

Breast TRAM flap: $2,000

Breast reconstruction: $500

Breast symmetry: $500

Facial reconstruction: $500

Maximum benefits per calendar year: 2 $100

Maximum benefits per calendar year: 2

Family transportation: $100 per trip

Maximum trips per calendar year: 12

Family lodging: $100 per day

Maximum days per calendar year: 100

$100 per day not to exceed the number of days confined

Maximum days per calendar year: 30

Family transportation: $100 per trip

Maximum trips per calendar year: 12

Family lodging: $100 per day

Maximum days per calendar year: 100

$300 per day not to exceed the number of days confined

Maximum days per calendar year: 30

A condition for which a covered person received medical advice or treatment within the 12 months preceding the certificate effective date.

Continuity of coverage

Continuity of coverage is included for employees remaining on the same level plan. Pre-existing condition limitation applies for those changing plan levels or enrolling for the first time.

No benefits will be paid for a date of diagnosis or treatment of cancer prior to the coverage effective date, except where continuity of coverage applies.

No benefits will be paid for services rendered by a member of the immediate family of a covered person.

We will not pay benefits for other conditions or diseases, except losses due directly from cancer or skin cancer.

We will not pay benefits for cancer or skin cancer if the diagnosis or treatment of cancer is received outside of the territorial limits of the United States and its possessions. Benefits will be payable if the covered person returns to the territorial limits of the United States and its possessions, and a physician confirms the diagnosis or receives treatment.

You keep coverage for a set period of time, or “term.” If you die during that term, the money can help your family pay for basic living expenses, final arrangements, tuition and more.

AD&D Insurance is also available, which can pay a benefit if you survive an accident but have certain serious injuries. It can pay an additional amount if you die from a covered accident.

Your employer is offering you this coverage at no cost to you.

What else is included?

A “Living” Benefit

If you are diagnosed with a terminal illness with less than 12 months to live, you can request 75% of your life insurance benefit (up to $500,000) while you are still living. This amount will be taken out of the death benefit and may be taxable.

Waiver of premium

Your cost may be waived if you are totally disabled for a period of time.

Portability

You may be able to keep coverage if you leave the company, retire or change the number of hours you work.

Employees or dependents who have a sickness or injury having a material effect on life expectancy at the time their group coverage ends are not eligible for portability.

can

If you are actively at work at least 20 hours per week, you can receive coverage for:

If you are actively at work at least 20 hours per week, you can receive coverage for:

You: You can receive 1 times your earnings up to a maximum of $50,000.

You: You can receive 1 times your earnings up to a maximum of $50,000. You can get up to $50,000 with no medical underwriting.

You can get up to $50,000 with no medical underwriting.

Who can get Accidental Death & Dismemberment (AD&D) coverage?

You: You can get 1 times your earnings of AD&D coverage up to a maximum of $50,000.

No medical underwriting is required for AD&D coverage.

Actively at work

Eligible employees must be actively at work to apply for coverage. Being actively at work means on the day the employee applies for coverage, the individual must be working at one of his/her company’s business locations; or the individual must be working at a location where he/she is required to represent the company. If applying for coverage on a day that is not a scheduled workday, the employee will be considered actively at work as of his/her last scheduled workday. Employees are not considered actively at work if they are on a leave of absence or lay off.

Employees must be U.S. citizens or legally authorized to work in the U.S. to receive coverage. Employees must be actively employed in the United States with the Employer to receive coverage. Employees must be insured under the plan for spouses and dependents to be eligible for coverage.

Exclusions and limitations

Life insurance benefits will not be paid for deaths that are caused by suicide occurring within 24 months after the effective date of coverage or the date that increases to existing coverage becomes effective. This exclusion standardly applies to all medically written amounts and contributory amounts that are funded by the employee including shared funding plans.

AD&D specific exclusions and limitations:

Accidental death and dismemberment benefits will not be paid for losses caused by, contributed to by, or resulting from:

• Disease of the body; diagnostic, medical or surgical treatment or mental disorder as set forth in the latest edition of the Diagnostic and Statistical Manual of Mental Disorders (DSM)

• Suicide, self-destruction while sane, intentionally self-inflicted injury while sane or self-inflicted injury while insane

• War, declared or undeclared, or any act of war

• Active participation in a riot

• Committing or attempting to commit a crime under state or federal law

• The voluntary use of any prescription or non-prescription drug, poison, fume or other chemical substance unless used according to the prescription or direction of your doctor. This exclusion does not apply to you if the chemical substance is ethanol.

• Intoxication – “Being intoxicated” means your blood alcohol level equals or exceeds the legal limit for operating a motor vehicle in the state or jurisdiction where the accident occurred.

Delayed effective date of coverage

Employee: Insurance coverage will be delayed if you are not in active employment because of an injury, sickness, temporary layoff, or leave of absence on the date that insurance would otherwise become effective.

Age reduction

Coverage amounts for Life and AD&D Insurance for you will reduce to 65% of the original amount when you reach age 65, and will reduce to 50% of the original amount when you reach age 70. Coverage may not be increased after a reduction.

Termination of coverage

Your coverage under the policy ends on the earliest of:

• The date the policy or plan is cancelled

• The date you no longer are in an eligible group

• The date your eligible group is no longer covered

• The last day of the period for which you made any required contributions

• The last day you are actively employed (unless coverage is continued due to a covered layoff, leave of absence, injury or sickness), as described in the certificate of coverage

This information is not intended to be a complete description of the insurance coverage available. The policy or its provisions may vary or be unavailable in some states. The policy has exclusions and limitations which may affect any benefits payable. For complete details of coverage and availability, please refer to Policy Form C.FP-1 et al or contact your Unum representative.

Life Planning Financial & Legal Resources services, provided by HealthAdvocate, are available with select Unum insurance offerings. Terms and availability of service are subject to change. Service provider does not provide legal advice; please consult your attorney for guidance. Services are not valid after coverage terminates. Please contact your Unum representative for details.

Underwritten by: Unum Life Insurance Company of America, Portland, Maine

© 2022 Unum Group. All rights reserved. Unum is a registered trademark and marketing brand of Unum Group and its insuring subsidiaries.

You choose the amount of coverage that’s right for you, and you keep coverage for a set period of time, or “term.” If you die during that term, the money can help your family pay for basic living expenses, final arrangements, tuition and more. AD&D Insurance is also available, which pays a benefit if you survive an accident but have certain serious injuries. It pays an additional amount if you die from a covered accident.

Why is this coverage so valuable?

If you buy a minimum of $10,000 of coverage now, you can increase your coverage in the future up to $200,000 to meet your growing needs. There would be no medical underwriting to qualify for coverage.

What else is included?

A ‘Living’ Benefit — If you are diagnosed with a terminal illness with less than 12 months to live, you can request 75% of your life insurance benefit (up to $500,000) while you are still living. This amount will be taken out of the death benefit, and may be taxable. These benefit payments may adversely affect the recipient’s eligibility for Medicaid or other government benefits or entitlements, and may be taxable. Recipients should consult their tax attorney or advisor before utilizing living benefit payments.

Waiver of premium — Your cost may be waived if you are totally disabled for a period of time.

Portability — You may be able to keep coverage if you leave the company, retire or change the number of hours you work.

Employees or dependents who have a sickness or injury having a material effect on life expectancy at the time their group coverage ends are not eligible for portability.

If you are actively at work at least 20 hours per week, you may apply for coverage for:

If you are actively at work at least 20 hours per week, you may apply for

Choose from $10,000 to $500,000 in $10,000 increments, up to 7 times your earnings. You can get up to $200,000. This is the amount of coverage you can qualify for with no medical underwriting.

You: Choose from $10,000 to $500,000 in $10,000 increments, up to 7 times your earnings. You can get up to $200,000. This is the amount of coverage you can qualify for with no medical underwriting.

Your spouse: Get up to $500,000 of coverage in $5,000 increments. Spouse coverage cannot exceed 100% of the coverage amount you purchase for yourself.

Your spouse: Get up to $500,000 of coverage in $5,000 increments. Spouse coverage cannot exceed 100% of the coverage amount you purchase for yourself.

Your spouse can get up to $25,000 with no medical underwriting, if eligible (see delayed effective date).

Your spouse can get up to $25,000 with no medical underwriting, if eligible (see delayed effective date).

Your children: Get up to $10,000 of coverage in $2,000 increments if eligible (see delayed effective date). One policy covers all of your children until their 26th birthday.

Your children: Get up to $10,000 of coverage in $2,000 increments if eligible (see delayed effective date). One policy covers all of your children until their 26th birthday.

The maximum benefit for children live birth to 6 months is $1,000.

The maximum benefit for children live birth to 6 months is $1,000.

You: Get up to $500,000 of AD&D coverage for yourself in $10,000 increments to a maximum of 7 times your earnings.

Your spouse: Get up to $500,000 of AD&D coverage for your spouse in $5,000 increments, if eligible (see delayed effective date).

Your children: Get up to $10,000 of coverage for your children in $1,000 increments if eligible (see delayed effective date).

No medical underwriting is required for AD&D coverage.

Calculate your costs

1. Enter the coverage amount you want.

2. Divide by the amount shown.

3. Multiply by the rate. Use the rate table (at right) to find the rate based on age. (Choose the age you will be when your coverage becomes effective. See your plan administrator for your plan effective date. To determine your spouse rate, choose the age the employee will be when coverage becomes effective. See your plan administrator for your plan effective date.)

4. Enter your cost.

Enter the AD&D coverage amount you want.

Divide by the amount shown.

3. Multiply by the rate. Use the AD&D rate table (at right) to find the rate. 4. Enter your cost.

limitations

Actively at work

Eligible employees must be actively at work to apply for coverage. Being actively at work means on the day the employee applies for coverage, the individual must be working at one of his/her company’s business locations; or the individual must be working at a location where he/she is required to represent the company. If applying for coverage on a day that is not a scheduled workday, the employee will be considered actively at work as of his/her last scheduled workday. Employees are not considered actively at work if they are on a leave of absence or lay off.

An unmarried handicapped dependent child who becomes handicapped prior to the child’s attainment age of 26 may be eligible for benefits. Please see your plan administrator for details on eligibility. Employees must be U.S. citizens or legally authorized to work in the U.S. to receive coverage. Employees must be actively employed in the United States with the Employer to receive coverage. Employees must be insured under the plan for spouses and dependents to be eligible for coverage.

Exclusions and limitations

Life insurance benefits will not be paid for deaths caused by suicide occurring within 24 months after the effective date of coverage. The same applies for increased or additional benefits.

AD&D specific exclusions and limitations:

Accidental death and dismemberment benefits will not be paid for losses caused by, contributed to by, or resulting from:

• Disease of the body; diagnostic, medical or surgical treatment or mental disorder as set forth in the latest edition of the Diagnostic and Statistical Manual of Mental Disorders (DSM)

• Suicide, self-destruction while sane, intentionally self-inflicted injury while sane or self-inflicted injury while insane

• War, declared or undeclared, or any act of war

• Active participation in a riot

• Committing or attempting to commit a crime under state or federal law

• The voluntary use of any prescription or non-prescription drug, poison, fume or other chemical substance unless used according to the prescription or direction of your or your dependent’s doctor. This exclusion does not apply to you or your dependent if the chemical substance is ethanol.

• Intoxication – ‘Being intoxicated’ means your or your dependent’s blood alcohol level equals or exceeds the legal limit for operating a motor vehicle in the state or jurisdiction where the accident occurred.

Delayed effective date of coverage

Insurance coverage will be delayed if you are not an active employee because of an injury, sickness, temporary layoff, or leave of absence on the date that insurance would otherwise become effective.

Delayed Effective Date: if your spouse or child has a serious injury, sickness, or disorder, or is confined, their coverage may not take effect. Payment of premium does not guarantee coverage. Please refer to your policy contract or see your plan administrator for an explanation of the delayed effective date provision that applies to your plan.

Coverage amounts for Life and AD&D Insurance for you and your dependents will reduce to 65% of the original amount when you reach age 65, and will reduce to 50% of the original amount when you reach age 70. Coverage may not be increased after a reduction.

Termination of coverage

Your coverage and your dependents’ coverage under the policy ends on the earliest of:

• The date the policy or plan is cancelled

• The date you no longer are in an eligible group

• The date your eligible group is no longer covered

• The last day of the period for which you made any required contributions

• The last day you are actively employed (unless coverage is continued due to a covered layoff, leave of absence, injury or sickness), as described in the certificate of coverage In addition, coverage for any one dependent will end on the earliest of:

• The date your coverage under a plan ends

• The date your dependent ceases to be an eligible dependent

• For a spouse, the date of a divorce or annulment

• For dependents, the date of your death

Unum will provide coverage for a payable claim that occurs while you and your dependents are covered under the policy or plan.

This information is not intended to be a complete description of the insurance coverage available. The policy or its provisions may vary or be unavailable in some states. The policy has exclusions and limitations which may affect any benefits payable. For complete details of coverage and availability, please refer to Policy Form C.FP-1 et al or contact your Unum representative.

Life Planning Financial & Legal Resources services, provided by HealthAdvocate, are available with select Unum insurance offerings. Terms and availability of service are subject to change. Service provider does not provide legal advice; please consult your attorney for guidance. Services are not valid after coverage terminates. Please contact your Unum representative for details.

Unum complies with state civil union and domestic partner laws when applicable.

Underwritten by:

Unum Life Insurance Company of America, Portland, Maine

© 2022 Unum Group. All rights reserved. Unum is a registered trademark and marketing brand of Unum Group and its insuring subsidiaries.

returns); (b) your taxable compensation; (c) your spouse’s actual or deemed earned income.

“Register” in the top right corner, and follow the

An Employee Assistance Program (EAP) is a program that assists you in resolving problems such as finding child or elder care, relationship challenges, financial or legal problems, etc. This program is provided by your employer at no cost to you.

For full plan details, please visit your benefit website: www.gcisdbenefits.com

The Deer Oaks Employee Assistance Program (EAP) is a free service provided for you, your dependents, and household members by your employer. This program offers a wide variety of counseling, referral, and consultation services, which are all designed to assist you and your family in resolving work and life issues in order to live happier, healthier, more balanced lives. From stress, addiction, and change management, to locating child care facilities, legal assistance, and financial challenges, our qualified professionals are here to help. These services are completely confidential and can be easily accessed 24/7, offering you around-the-clock assistance for all of life’s challenges.

9 Program Access: You may access the EAP by calling the tollfree Helpline number, using our iConnectYou App, or instant messaging with a work-life consultant through our online instant messaging system.

9 Telephonic Assessments & Support: In-the-moment telephonic support and crisis intervention are available 24/7 along with intake and clinical assessments.

9 Short-term Counseling: Counseling sessions with a qualified counselor to assist with issues such as stress, anxiety, grief, marital/family challenges, relationship issues, addiction, etc. Counseling is available via structured telephonic sessions, video, and in-person at local provider offices.

9 Referrals & Community Resources: Our team provides referrals to local community resources, member health plans, support groups, legal resources, and child/elder care/daily living resources.

9 Advantage Legal Assist: Free 30 minute telephonic or inperson consultation with a plan attorney; 25% discount on hourly attorney fees if representation is required; unlimited online access to a wealth of educational legal resources, links, tools and forms; and interactive online Simple Will preparation.

9 Advantage Financial Assist: Unlimited telephonic consultation with an Accredited Financial Counselor qualified to advise on a range of financial issues such as bankruptcy prevention, debt reduction, financial planning, and identity theft; supporting educational materials available; unlimited online access to a wealth of educational financial resources, links, tools and forms (i.e. tax guides, financial calculators, etc.).

9 Alternate Modes of Support: Your EAP offers support alternatives in addition to traditional short-term counseling including telephonic life coaching, AWARE stress reduction sessions, and virtual group counseling. During your call with one of our counselors, ask if these programs would be right for you.

9 Work-life Services: Our work-life consultants are available to assist you with a wide range of daily living resources such as locating pet sitters, event planners, home repair, tutors, travel planning, and moving services. Simply call the Helpline for resource and referral information.

9 Child & Elder Care Referrals: Our child and elder care specialists can help you with your search for licensed child and elder care facilities in your area. They will discuss your needs, provide guidance, resources, and qualified referral packets. Searchable databases and other resources are also available on the Deer Oaks member website.

9 Take the High Road Ride Reimbursement Program: Deer Oaks reimburses members for their cab, Lyft and Uber fares in the event that they are incapacitated due to impairment by a substance or extreme emotional condition. This service is available once per year per participant, with a maximum reimbursement of $45.00 (excludes tips).

Contact Us:

Toll-Free: (866) 327-2400

Website: www.deeroakseap.com

Email: eap@deeroaks.com

Username/Password: gvinecolley

Enrollment Guide General Disclaimer: This summary of benefits for employees is meant only as a brief description of some of the programs for which employees may be eligible. This summary does not include specific plan details. You must refer to the specific plan documentation for specific plan details such as coverage expenses, limitations, exclusions, and other plan terms, which can be found at the Grapevine-Colleyville ISD Benefits Website. This summary does not replace or amend the underlying plan documentation. In the event of a discrepancy between this summary and the plan documentation the plan documentation governs. All plans and benefits described in this summary may be discontinued, increased, decreased, or altered at any time with or without notice.

Rate Sheet General Disclaimer: The rate information provided in this guide is subject to change at any time by your employer and/or the plan provider. The rate information included herein, does not guarantee coverage or change or otherwise interpret the terms of the specific plan documentation, available at the Grapevine-Colleyville ISD Benefits Website, which may include additional exclusions and limitations and may require an application for coverage to determine eligibility for the health benefit plan. To the extent the information provided in this summary is inconsistent with the specific plan documentation, the provisions of the specific plan documentation will govern in all cases.