1 minute read

Market Insights BY

JEN ALLEN

Property Sales By Price Point

Consistent Demand Despite Decline In Sales

• Transaction volume across all property types was significantly lower than in previous years during February. Sales by price point thereby dropped in every pricing category except for sales above $10 million, which saw one more transaction than in 2022 for the same period.

• On a percentage of sales basis, sales between $2 million and $3 million saw the most significant increase during this short timeframe. Time will tell if this trend continues, but this price point tends to see the highest concentration of sales in any given year so 2023 is off to a consistent start. The recent sale of 2 Hiawasse Lane illustrates just how strong demand continues to be as multiple offers resulted in a sale price $275,000 above the list price.

Residential Sales Activity Steep Decline In Transaction Volume

• Single-family home sales (excluding condos, co-ops, multi-family & covenant properties) saw a dramatic decline during February, tallying just six transactions totaling $14.5 million. This is the lowest number of monthly transactions posted during any year since 2009. Current conditions are currently quite different as this decline in activity stemmed largely from the lack of home inventory meeting buyer demand.

• The highest sale during the month was the $3.8 million sale of 79 Polpis Road, which is artificially low as there was a separate, private construction contract for the dwelling which reportedly totaled an all-in price of $8 million.

• Monthly sales metrics remained solid with the average marketing time and sales discounts stronger than they were one year ago.

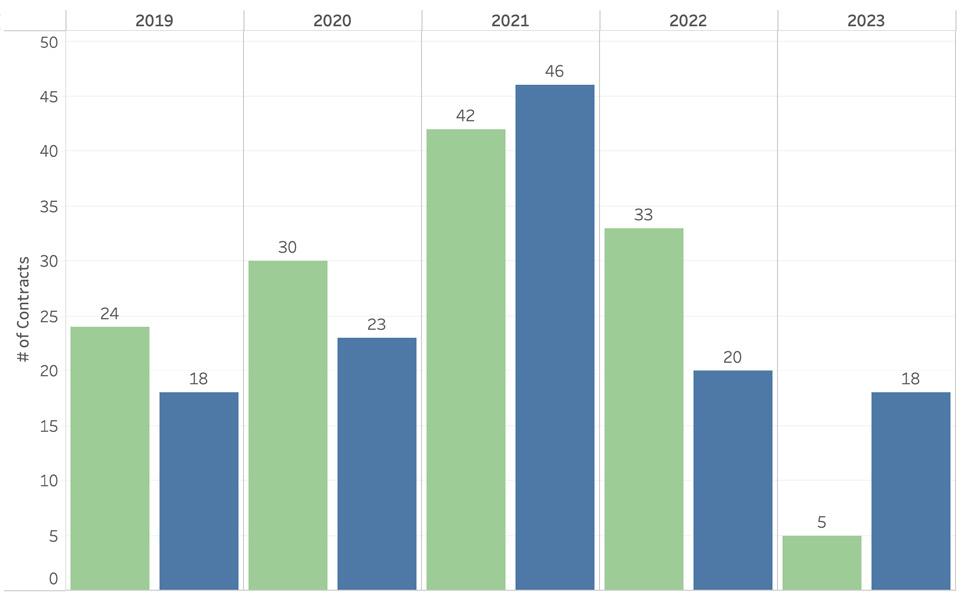

Contract Activity New Purchases Rebounded

• After a dip in monthly contract activity in January, February’s recorded contracts (Offers to Purchase and Purchase & Sale Contracts excluding duplicates) rallied to 18 newly contracted properties, right in line with monthly activity over the last few years.

• Of these recorded contracts, four were for properties last listed above $5 million, signaling a continued strength in the upper end of the market.

• This new activity suggests we should see a modest bump in transaction activity as we head into the spring market.

Sfh Inventory By Price Point Modest Growth Across The Board

• Although property inventory remained at historic lows, February represented the second month of the year with a slight increase from 2022 levels. As of February 28, 2023, there were just 87 properties listed for sale including residential, commercial, and vacant land listings. By isolating single-family homes for sale by price point, nearly every price point saw an incremental increase in listed properties from 2022.

• The total months’ supply, or how long it would take to sell all listings based on trailing 12-month sales, measured two and a half months, an increase from 1.1 months at this time last year.