2 minute read

FISHER’S JUNE ‘23 REVIEW Market Insights BY JEN ALLEN

• First half single-family home sales (excluding condos, co-ops & 40B or covenant properties) totaled 84 transactions, down 35 percent both year-over-year and as compared to the five-year average of 125 home sales. Aggregate dollar volume declined nearly an identical amount, off 36 percent from 2022 and measuring $352 million.

• While the average home sale price hovered just above $4 million, the median home sale value dropped modestly from 2022 to $2.75 million. The average home sale price is very clearly affected by the record-setting values happening at the top end of the market, now with a new high of $38 million, while the median home sale value is considered a more accurate measure of the broader market. That said, prices aren’t yet declining based on our tracking of resale activity. The slight softening in the median value is largely driven by significantly lower transaction volume combined with less higher end (not just highest end) sales than in the last two years.

• Given that inventory levels are 13 percent lower than one year ago, and 60 percent below 2020, supply is still severely constrained relative to buyer demand. This is creating an extreme environment for pricing wherein buyers are required to pay sizable premiums relative to comparable sales to secure a turnkey property, but where notable price reductions are taking place for properties that are not updated. Record low marketing times are still present for the former while we are starting to see extended marketing times for the latter.

• Despite what some appraisers are reporting through their lens of Banker & Tradesman statistics, we don’t yet see a softening in property values. Yes, the median home sale value is down six percent from 2022 but we don’t believe that directly correlates to underlying property value changes. Rather, we believe the decline in the median home sale value is the result of a forced shift in sales by price point stemming from the limited supply of homes available for sale.

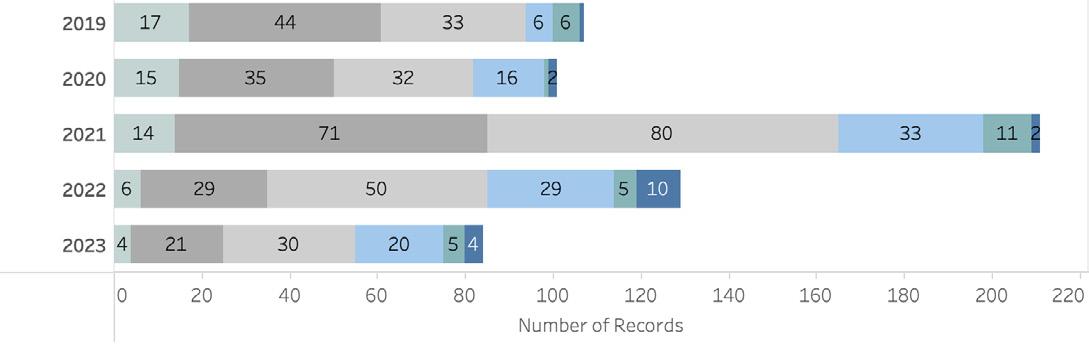

• For example, by this point last year, sales between $3M-$5M totaled 33 transactions. In 2023, that number fell to just 16 sales. With a reduction in market-wide activity, and then a pronounced decline in transactions in the middle of our market, the median home sale value is bound to fall. In years past, we’ve had far more transaction activity, and consistent sales across price points, that resulted in a median home sale value that better aligned with property value trends. The hypothesis that the decline in median home sale value may not be indicative of the broader market is supported by our resale metrics and also current contract trends.

Contract Activity

TIGHT CONTRACTS REMAIN THE NORM

RESIDENTIAL SALES PRICE POINT TREND ARE PRICES REALLY GOING DOWN?

• In a market with constrained inventory, there are bountiful buyers chasing properties with similar characteristics. Which is why, despite a rise in interest rates, we are still seeing several properties per month trade at full asking price or above. In June alone, nearly a quarter of all transactions traded at 100 percent or more of the asking price, while many others were near 98 percent of the asking price.

• Just as has been the case the last two years, purchase contracts have limited contingencies and often solely include an inspection period. We are not seeing many financing contingencies being accepted by sellers, even if buyers still plan to seek a mortgage prior to closing. For properties that have been marketed longer than a few months, the seller’s appetite to accept contingencies typically increases. So is the case as we approach the off-season, where it’s not quite as critical as tying up the property during the peak of summer.