55 minute read

OPENERS

from FORUM Magazine - May 2022

by Advocis

Fodder For the Water Cooler

INDUSTRY ASSOCIATIONS AND DEI INITIATIVES

Two of Canada ’ s professional membership groups for financial advisors and planners have instituted guidelines on the complex issues of diversity, equity, and inclusion (DEI), but they aren ’t prepared to go as far as the CFA Institute in instituting a code for members to develop and adopt.

“What the CFA Institute has done is good work, but I’ m not sure we want to copy their approach, ” says Tashia Batstone, president and CEO of FP Canada. “It’ s early days for us in terms of whether a code is an appropriate strategy. We are considering whether there are other things that we should be doing to build confidence and trust in financial planning for a more diverse population of Canadian consumers. ”

Advocis also doesn ’t believe in mandating that all individuals participate in its strategic plan for DEI, though president and CEO Greg Pollock says there is tremendous interest in the entire project.

“My observation of our association is that it wasn ’t really reflective of the Canadian fabric. When I looked at the membership of the organization, I realized we are missing something and wondered why we don ’t have greater representation from diverse groups. ”

In February, the CFA Institute brought in its DEI code with companies signing on to integrate their own policies and statements, with governance from senior team members within two years of signing.

In its 2017 strategic plan, Advocis brought in eight imperatives, one of which was diversity. It retained a consultant a couple of years ago and put on a number of seminars and workshops on DEI. But

Continued on page 10

HELOCS AND MITIGATING RISK

Fixed rate, variable, or a home equity line of credit (HELOC)? The market has been such lately that depending on your client’ s requirements and their capacity to deal with risk, any one of those three options might fit.

According to Steve Meldrum, CEO of Swell Private Wealth in Medicine Hat, Alta., many people like the security that comes with a locked-in rate.But when the Bank of Canada raised its rate to 0.5% rate in early March, he says many turned to even lower variable rates to get the best deal they could.

A HELOC can provide more options than a fixed or variable rate, such as locking in just a portion of a mortgage. With a HELOC, a person can lock in say, $200,000 of a $300,000 mortgage with some of it going for a two-year mortgage and the remainder for a five-year mortgage.

“The idea is that you ’ re just trying to mitigate risk, ” says Meldrum. “For example, you also have the risk that if rates don ’t go up then you ’ ve lost all that opportunity cost. So, I think that sometimes having a blend is good for people. ”

And in the right situation, it’ s a HELOC that can be the perfect combination.

“If I treat a HELOC as a chainsaw I think it works wonderfully to get rid of debt, and when people have free cash flow they can pay down their obligations very quickly, ” he says. “But if I give that chainsaw to someone who is not disciplined, it can be dangerous and they can get hurt, because the HELOC interest rate is slightly higher than a regular mortgage. ” But some people compare a HELOC to leasing a vehicle. They want to pay the lowest rates and if those rates go too high, they will simply sell their home, says Meldrum.

HELOCs also offer investors the ability to take money out and put it into a business, but if things turn, they can take that money and put it back into their line of credit.

BRANDING & SOCIAL MEDIA

BY ERIN BURY

LANDING THE DRAGON

I’ ve always been a big fan of startup pitch shows Shark Tank and Dragons ’ Den, even before I became an entrepreneur. I loved watching entrepreneurs share more about the problem they faced that sparked a business idea, and seeing how investors would grill them before making a deal — or not. When my husband, Kevin Oulds, and I started Willful in 2017, it was always a goal of ours to make it on to Dragons ’ Den. We finally realized that goal in 2021, when we pitched on the show and secured a deal with techfocused investor Michele Romanow. The process for applying for the show, preparing for our pitch, filming, and promoting our appearance led to a lot of takeaways that are applicable for young advisors looking to grow their business. Here ’ s what we learned:

DON’T ASK, DON’T GET

People often ask us how we made it on to the show, and I always reply with a very simple answer: we applied. The application process for Dragons ’ Den was quite simple — we filled out an online form and attached a short video pitch. It probably took about 45 minutes to fill out the form and film the video — a very small investment of time. I’ ve always been someone who puts my hand up for opportunities, whether it’ s speaking at an event, doing a media interview, or pitching to the Dragons — and many people, especially women, can be reticent to put themselves forward for fear that they won ’t be good enough, or that they don ’t deserve it. I’ m here to tell young advisors to put yourself forward for awards, speaking engagements, partnerships, or other opportunities to build your profile — the worst someone can say is no! You won ’t get the opportunities you don ’t chase. The caveat is that we knew we were ready for Dragons ’ Den — we didn ’t apply in month one of our business; rather we applied when we knew we had the traction that would impress them.

PREPARATION IS KEY PERFECT YOUR PITCH

Every business has an elevator pitch — ours is that we help Canadians get a will online in less than 20 minutes. What’ s yours? And how is it differentiated from the advisor down the street? We prepared a one-minute pitch for the Den, and we asked ourselves some crucial questions as we developed it: How can we get our message across so anyone watching can understand it? How will the audience know what sets us apart? And how can we ensure we ’ re building trust that our platform is a great option for getting a will done? You ’ re likely pitching your business daily to potential employees, potential clients, partners, and other stakeholders, and you need to have your elevator pitch nailed down.You should also be able to deliver it consistently and confidently anytime — a dinner party, at a conference, or even to the Dragons.

LEVERAGE YOUR TIME IN THE SPOTLIGHT

We were thrilled to make it onto Dragons ’ Den, and we didn ’t want to waste this opportunity to promote our appearance and get Willful in front of more Canadians. We developed a full promotional plan that included media outreach, digital ads, video testimonials from Michele Romanow, and a variety of other tactics. You should be doing the same for any promotional opportunities — if you ’ re quoted in a media article, a guest speaker at an event, or the recipient of an award, make sure you highlight it on your website, in your marketing materials, in your email signature, and on your social media channels. Clients are always looking for proof points that you are a trusted, legitimate business,so these types of trust signals are amazing ways to build confidence.

When we stepped onto the Dragons

’ Den set to film, I expected to be extremely nervous. But Kevin and I both felt quite calm because we overprepared. We practised our one-minute intro pitch about a thousand times, tweaking it with the help of our friends at speaker training company Speaker Labs. We watched past seasons of Dragons ’ Den, compiled a list of about 50 potential questions we could be asked, and mapped out and practised our responses. We rehearsed in front of fake Dragons — our team members, friends, and family — and had them grill us. Most importantly, I reviewed our numbers and knew them like the back of my hand. All of this prep paid off, because we felt confident on stage, prepared to answer any question they threw at us, and we knew our business metrics. If you have a big pitch, speaking engagement, or something else you ’ re nervous about, overprepare to ensure your nerves don ’t get the best of you.

ERIN BURY is the CEO at willful.co, an estate planning startup that provides an affordable, convenient, and easy way for Canadians to make a will online. Willful works with financial planners across Canada to help their clients get a solid estate plan in place.

OPENERS

Continued from page 8 bringing in a diversity and inclusion plan is not easy.

“There ’ s no magic bullet when it comes to these topics, ” says Pollock. “So, for example, the discussion in Toronto might be different than the discussion elsewhere in the country. We want to reflect the fabric of the community. ”

Advocis also did a survey of its staff a year ago, with 40% identifying themselves as racialized, a significant majority identified as being women, and its executive management team split up evenly between men and women.

FP Canada has also ensured there is inclusion at its board level and is putting together a policy that will outline its commitment to DEI from a governance perspective.

Batstone says FP Canada also wants to encourage more diverse populations to explore financial planning as a career. “We want the financial planning professional to be reflective of the demographics of the Canadian population, so we are looking at our recruitment strategies differently, ” she says.

“But it’ s also broader than that — it’ s making sure that we ’ re looking at our certification program to ensure there are no unintended barriers that are going to exclude people from being able to get a CFP or QAFP certification. ” She also adds: “When working with a financial planner, Canadians often want to work with someone who looks like them, understands their culture, and in many cases, speaks their language. ” — Susan Yellin

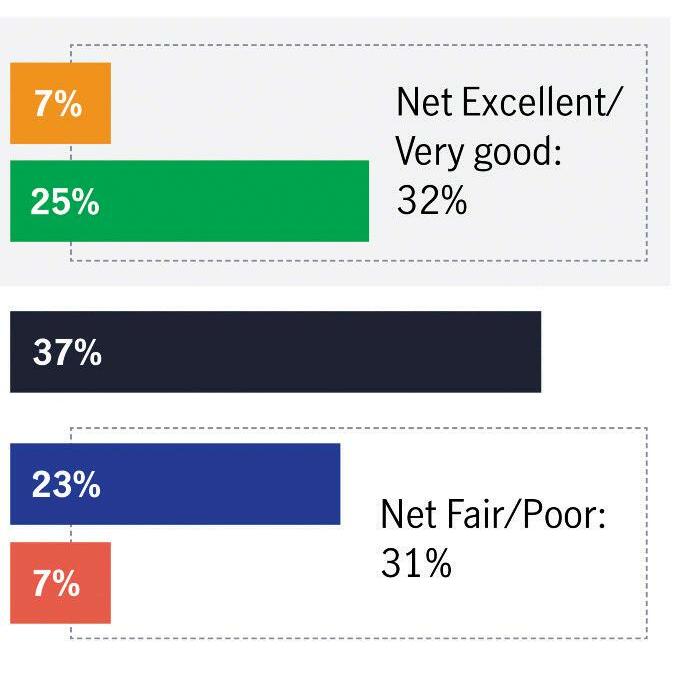

DID YOU KNOW?

7/10 rate their current financial situation as good or better. However, >1/10 rate their financial situation as excellent.

Excellent

Very Good

Good

Fair

Poor

At the same time, twice as many report major general or financial stress during the pandemic, compared to before the pandemic, which presents a somewhat contradictory scenario.

The study also makes clear the economic effects of the pandemic have not been uniformly experienced. Some groups, including men, those with household investable assets, those under the age of 36, and Canadians with employer financial wellness plans were all more likely to cite their financial situation as excellent or very good.

Women and those under the age of 36 report being more concerned about finances adding stress to their lives.

SOURCE: MANULIFE CANADA RETIREMENT STUDY, 2022

Workers are concentrated most on paying off debt, ensuring savings are invested wisely, and planning for retirement in the short term.

SHORT-TERM GOALS

Pay off debt Ensure my savings are invested wisely Plan for retirement

Save for short-term needs (car, vacation) Create an emergency fund Save for a new home

Create a monthly budget Gain a better understanding Protect my family in the event of my illness or death Save for a child’s education

Plan for health-care costs (now or in retirement) None of the above

Don’t know/not sure

2% 1% 22% 21% 21% 19% 17%

18%

36% 35% 33% 29% 45%

Adjusting to Retirement

Retirement is about more than having enough assets. Kira Vermond explores the psychological effects of transitioning to the next chapter

One weekend earlier this spring, Judith Cane looked up at her husband and uttered two words: “I’ m done. ”

Cane, a money coach in Sackville, N.B., and former longtime Advocis member who once sat on the national board, just turned 65, and for the first time in her life was truly serious about retiring. It just felt right. With a roster of more than 50 clients, she planned to scale back to about 25 who were still on the maintenance side of her six-month coaching program. Eventually, she would wind that part of the business down, too.

Besides, her husband, Ian, was set to retire on June 6, 2022 so the timing was ideal. But his impending retirement was only one reason Cane made the decision when she did. Like many Canadians living altered lives as the COVID-19 pandemic delivers wave after wave of high case counts around the world, she started focusing on what truly mattered to her. There was her elderly mother with whom she wanted to spend quality time.And Cane already had loads of hobbies, from quilting to playing music to curling. In an era of lingering uncertainty, there was a real sense of “if not now, then when?”

“I have to tell you how I felt, ” she says. “The minute I said,

‘I’ m done, ’ and I wasn ’t going to take any more full-time clients, it was like the shoulder I’d been working on with my chiropractor, massage therapist, and physiotherapist suddenly started feeling better. ”

Cane is hardly the only person to make a sudden decision about taking retirement these days. Between Omicron variant spikes and war in Europe, many Canadians are feeling a sea change when it comes to their future. Some, like Cane — not to mention overwhelmed frontline workers — can ’t wait to trade in their 9 to 5 for a less-hectic life rich with purpose and meaning (or just a few months watching Netflix and recovering). Others are having their retirement dreams dashed in the wake of high inflation, real estate spikes, and a turbulent market. Others lost businesses and have wiped out nest eggs. According to a 2021 Fidelity Retirement Report, 21% of pre-retirees have decided to put retirement off later than originally planned.

TECHNICAL ANSWERS NOT THE ANSWER

Whether they fall into the “ retire now ” or

“ retire later ” camps, Julia Chung, partner and senior planner at Spring Financial Planning in Surrey, B.C., isn ’t surprised that many are rethinking their longterm plans.

“A lot of people felt there was certainty about where they were going [before the pandemic], ” she says. “And that certainty really feels like it’ s gone. There ’ s just this underlying sense of unease. ”

That anxiety runs deep. Client worries range from recognizing their own mortality to concerns about having enough money to retire. The possibility of paying for long-term care someday is top of mind, too. Some of her clients are even trying to determine if they have money to support their Ukrainian family members when they arrive in Canada as refugees or worry about giving enough to the local Ukrainian church.

Still, other people are feeling frozen at the thought of making any financial moves at all as decision fatigue sets in, she explains.

“You ’ re making decisions every single day. Do I put on my mask or not? Do I send my kids to school? Those daily calls we ’ re making are harder and more intense. That leaves us with less emotional room to make long-term decisions, ” says Chung.

She calls what Canadians are feeling, “trauma. ”Even those who haven ’t lost jobs and can work from home are still experiencing chronic stress from months of isolation and upended plans. Humans are social animals and without those connections to family and community, they ’ ve lost a key component of what makes them happy and whole. It’ s a bigger loss than many realize, she says.

For advisors, that means client discussions about retirement now should focus just as much on the emotional aspects of their

Judith Cane

“The minute I said,

cicea.ca

William McBay, CFP, CLU, CHS, CEA

Philip Sallaj Julia Chung

next phase of life as the financial ones. In fact, too much concentration on the technical side of asset management, pension plans, and a Registered Retirement Income Plan (RRIF) could actually backfire. While important, they don ’t always lead to peace of mind.

“The math and rules don ’t change that much but how we talk to clients does change, ” she says. “We call them soft skills, but they ’ re not remotely soft. It’ s really hard. It’ s about uncovering the question beneath the question. What is it they ’ re actually anxious about? Inflation? Or that they ’ re going to run out of money?”

Even after running the numbers and determining there will be plenty to retire comfortably on, some still feel stressed. Uncovering what’ s behind the fear takes listening skills.

WHY BOTHER RETIRING NOW?

For Philip Sallaj, principal and managing partner for the Planning Group NB Inc., in Moncton, N.B., more practical concerns abound. Some clients put off retiring once they realize how much they ’ll have to pay for health benefits once their group insurance expires. In some cases, the clients could be looking at $500 to $600 per month that they hadn ’t planned for. Just the week before, a 62-year-old client decided to work for two more years just to remain on their company health plan.

“A lot of times you never read about this issue or hear [an advisor] talking about the loss of benefits. But it’ s an adjustment for some clients, ” he says.

In other cases, the pandemic has had a direct result on clients ’ decisions to retire later due to travel restrictions, and fear over contracting the coronavirus while abroad and away from Canadian health care and family support. Sallaj points to one couple he counselled whose retirement plans were put on hold when the pandemic hit, scuttling jet-setting dreams. Without them, what was the point of quitting their jobs? “They ’ re the prime example where people are going, ‘I can ’t travel during the pandemic. Might as well keep working, ’” he says.

For those afraid to retire now due to global instability and the spectre of an impending recession, Sallaj does his best to put fears to rest. Particularly for his long-term clients who have been with him for decades, he points to other times of market volatility — Y2K, 2008, and March 2020 — and reminds them that they still came out ahead by holding fast.

Besides, it’ s not as though retirees need to draw on all of their

cicea.ca

Mark Albert, CEA

funds at once. Rather than taking a million-dollar Registered Retirement Savings Plan (RRSP) portfolio invested in a balanced mandate and moving it all to a moderate mandate for their RRIF, it makes sense to just move enough for the next three to five years of income. If the client is young enough, the rest can remain in their RRSP and continue to grow for their long-term income needs, he explains.

Meanwhile, Al Jones, senior advisor at A. Jones Wealth & Estate Planning in Barrie, Ont., points to clients who have decided to postpone retirement for more satisfying reasons: they love working from home. Forget long commutes and dealing with difficult bosses face-to-face. Office politics are dampened somewhat too when everyone is online. Some have even moved out of the city to buy a home in nearby Collingwood, a stay-and-play community complete with a cute downtown, beaches, ski resorts, and golf courses.

“It’ s really de-stressing. They ’ re finding they ’ re enjoying it, ” he says.

“People want to feel like they ’ re contributing and they ’ re saying to me, ‘Al, this is pretty good. I don ’t have the strain of the commute anymore, I still enjoy the work, and the income is good. ’”

What are the benefits of those extra couple of years working? It means more money in the bank for even more fun when the pandemic finally recedes.

GET ME OUT OF HERE

On the flipside, others cannot wait to trade in their career for permanent weekends. Jones has some clients who are frontline workers who are exhausted after the last couple of years and just want to get out. They ’ ve put in their time. They deserve it. Even so, Jones is adamant that they take the necessary steps to think things through. Even if they have some money in their retirement fund, it’ s sometimes not enough. At least not yet.

“They ’ll say, ‘I’ ve got the money, ’ and yeah, that’ s great but you ’ re 45 or 50. So let’ s talk about what you ’ re going to do for the next 15 years. You ’ re not going to be on a golf course because you can ’t afford to do that every day, or travel all the time. So how can we transition?” he says.

Jones explains that the conversation revolves around purpose and meaning in retirement. If a frontline worker feels recharged by helping others, is there another way to create that feeling? In some cases, the client simply needs a change. So rather than quitting, they reduce hours or work somewhere new. Recently, he spoke to a former airline pilot who is now driving a shuttle for a car dealership. He didn ’t need the money, but he enjoyed having contact with people.

The key to smooth transitions is to be proactive and pre-emptive,

Al Jones

cicea.ca

“I refer advisors to CICEA. The technical component is invaluable to advisors and their clients. It is undeniably one of the best courses for training advisors on how to gain new clients through referrals and introductions, brought about through the estate planning discussions. Whether you’re a rookie advisor or a veteran in the industry, the CEA designation will absolutely help you grow your business. ”

Daniel Collison, BA, CFP, TEP Managing Partner I Advice2Advisors

says Michael Nichols, president of Compass Private Wealth in Guelph, Ont., an institutional money manager that focuses on institutional investments and alternative investments. When he first sits with his high-net-worth clients, they discuss 60 life events that could be on the horizon, from the birth of a child to lifethreatening illness and retirement. Then they make a plan to address them.

Many clients also come up with an age range for retirement, say, 62 to 65, rather than a single number. So instead of scrambling if a client suddenly wants to retire, he says the firm is ready.

“Every year or two we go through the list with them and make sure we ’ re up to date. That means it’ s very unusual for us to have a client who would call us with something that is unexpected, ” says Nichols, admitting that “ a worldwide pandemic ” was never on the list. Still, he says almost all of his clients kept calm in March 2020. Invested very conservatively and with little market fluctuation, assets held steady.

HITTING THE ROAD

Chung also likes to talk to her soon-to-retire clients about maintaining purpose in the face of extreme change. For some, particularly essential health-care workers and teachers who are driven to help others, retirement is bittersweet. They want to move on but feel they ’ re abandoning their community and what gives their lives meaning.

“But they ’ re so burned out. They ’ ve spent the last two and a half years just killing themselves. They don ’t know what’ s on the other side — just that there ’ s the relief from stress, ” she says. Because they may not be thinking clearly, she wants them to consider what will make them feel valued if work is no longer there for them. “What are you going to do to find purpose? I know this is an escape from — but what are you escaping to?”

Some make the switch easier than others, simply because their life ’ s priorities have changed. She says a few clients are thinking seriously about living on a fraction of their usual income. They don ’t care about having the nicest house on the block because no one visits these days. Travelling the world isn ’t important either, now that they ’ ve gotten used to staycations and hitting the road in Canada.

That’ s precisely what Cane is planning to do when she retires. Putting her financial planning skills to work on her husband, she asked him what would give his life meaning and purpose after he leaves his job with the Red Cross. He chose to travel and planned a trip this summer that will take them from the Acadian Peninsula in New Brunswick to Quebec City, and the Finger Lakes region in New York to a national park in Maine.

Thrilling? Yes. But what Cane is most excited about is saying goodbye to long workdays.

“I want to be able to decide if I’ m just going to lie in bed for an hour and read. Or if I’ m going to drive 30 minutes down to the ocean and watch the sunrise, ” she says, sounding wistful. “I want to be able to have the freedom to do whatever I want and not be tied to a 6 o ’ clock alarm going off anymore. ”

KIRA VERMOND is a writer and editor based in Guelph, Ont.

Canadian Taxation of Life Insurance, 11th edition

Does anybody really understand how life insurance is taxed? The experts at Manulife do. This book is a must-have for anyone who sells insurance or is involved in financial or estate planning.

Florence Marino, Head of Tax, Retirement & Estate Planning, Insurance B.A., LL.B., TEP, explains:

“Manulife is the only insurer in Canada that publishes information as extensive as this and we’re proud to be the leading experts in our field. Advisors know they’re getting our best thinking, and their clients know be the leading experts in our field. Advisors know they’re getting our best thinking, and their clients know their advisors are backed by industry-leading knowledge.”

Order yours today

Visit https://bit.ly/3rNLdfF

www.ppi.ca

LAUNCH YOUR PRACTICE INTO THE STRATOSPHERE

Our world changed dramatically over the past two years, from the way we work to the way we connect with one another. This forced all of us to reconsider how we want to live our lives and how we can best serve those who depend on us.

At PPI, these changes led us to think about how to elevate support for advisors. We believe that more than ever, it is critical that you have the best digital tools to serve your clients… across all markets, wherever you are, and however you want to work.

We’re excited to announce Stratosphere. Instead of a single application, it’s an ecosystem of leading proprietary tools for prospecting, analysis and presentations, complemented by exceptional third party offerings curated to help your business ascend to new heights.

Our goal is to empower you to choose the tools that work best for your practice and make them work together better with smart two-way connections, utilizing your brand, so they are more than the sum of their parts.

We support you with a team of digital sales enablement experts – from training to trouble-shooting – available to help you get started, and they’re just a phone call away to lend a hand. Talk to us today.

Unparalleled Resources. At Your Command.

Vancouver Edmonton Ottawa Halifax Burnaby Winnipeg Montréal St. John’s Surrey Mississauga Brossard Calgary Toronto Québec City

Lifein

Retirement

Three former advisors tell FORUM about how they “ rewire ” their days

Ann Richards, Toronto Retired: May 2019 Years in the business: 25

There are always advisors who say, “Let me just get through this market correction, and then I’ll look at retirement. ”But we all know something can happen to throw us off our game.And I just didn ’t want that. I wanted to be proactive.

I went through withdrawal for a while — always wanting to go into the office or watch the markets, or clients would come to mind all the time. And I would reach out to my successor and say, “This client came to mind. Is everything OK?” But eventually, time does its job and I can let go more and more.

Losing a certain work status is very hard. When I was an advisor, some mutual fund companies would include you in special events and all of a sudden, you ’ re not a member of that kind of exclusive club anymore. And that is a bit of a loss but you can ’t have it both ways. Those are the things you have to let go.

You need to know what you are retiring to. My husband retired a few years earlier than me, and we wanted to retire to travel. Now with COVID, that didn ’t happen as much as we liked but we did have some trips to England and Vancouver to see our parents. Now that travel is opening up, we are planning a trip to Sicily in May.

You need structure to your life to replace the structure you had at work. My structure includes doing some part-time work for a consulting engineering company. I don ’t know about engineering but I know about client relationships and account management. Every tax season, I volunteer through CPA Ontario and prepare income tax returns for low-income families. I also lead a walking group from my condo on Tuesday and Thursday mornings. We do it at 6:15 a.m. so the people who work have time to get to their offices. The retired folk are generally up and ready to go at that time of day anyway. It’ s a nice group and I enjoy contributing to the community.

Angela Knight vanSchaayk, North Bay,Ont. Retired: March 2020 Years in the business: 30

The year before I retired, I had a health scare and I realized that I needed to get work stress out of my life. I spent my whole life helping business owners with their own succession plans. Sometimes, it behooves us to do plans for ourselves but the health scare was my wakeup call.

I was concerned about what was going to happen to my clients because they are also my friends. And I wanted to make sure that they were well taken care of with someone who was really qualified. I’d found somebody who was knowledgeable and had been in the business long enough to know group insurance. My successor had been interested in my business for years and it was finally the right time.

Like most retired people,we had planned on doing a lot of travelling and we had just returned from Cozumel, Mexico, when COVID hit. It was a bit of a shock because I had just closed my office. If we can ’t go anywhere, what to do during the lockdown? Luckily enough for me, I was the president of the Rotary Club of North Bay, and we had just moved all our meetings to Zoom. So that really helped to fill a void. I was also still doing investments and life insurance for family.

That’ s how I started filling my time up. I’ m also on the economic development committee in the Municipality of Ferris, just south of North Bay, and am involved with various charitable committees. And I just got appointed to the North Bay Regional Hospital board. Even now that we can fly, my husband doesn ’t know if my schedule will free up enough time so we can go away.

In the summer months, I’ m on the lake. I’ m an avid boater. If we ’ re not on the lake, we get into my blue Mustang convertible and we drive to Algonquin Park. Ten years ago, I had a mid-life crisis and bought the Mustang, which has an eight-cylinder engine and Roush after-market performance parts. It’ s a big rush to drive it — just what I needed.

Both of my parents died young of colon cancer in their early sixties. I’ m going to have the biggest party when I turn 65 because I’ll be the first person in my family to make it to that age.

Jim Kennedy, Mississauga, Ont. Retired: September 2019 Years in the business: 46

Travel was one of the big things I wanted to do in retirement but the pandemic put a hole in those plans. In October 2019, my wife and I did take a trip to Vienna and Budapest for 10 days. We were lucky to get that in.

When the pandemic started, we spent quite a bit of time looking after grandchildren so our children and their spouses were all able to continue working. Daycares weren ’t open during the first wave. My two grandchildren were toddlers at the time and we had them five days a week at our house. During the summer months, we were able to go up to our cottage and the kids and grandkids came as well. So, the grown-ups all worked from the cottage and we continued to babysit the grandkids. We now have four grandchildren.

It was a lot of work, but I wouldn ’t trade the experience for anything. The bond with our grandchildren is truly special. Our kids were concerned about me getting COVID, but we were all dedicated to our family bubble.

You have to be ready both financially and psychologically for retirement.Your income is going to be less and you have to learn to live within a tighter budget. Some experts say that your expenses are less but I didn ’t really find that. If you ’ re taking a 50% pay cut your expenses don ’t go down by 50%. That’ s why it’ s important to make sure you ’ ve done good planning.

The psychological part was a struggle for me. Many people, myself included, feel very defined by their occupation, and all of a sudden you ’ re not doing that anymore. As a wholesaler, I was communicating with a lot of people every day, and then all of a sudden, I wasn ’t. In fact, after two years of retirement, I decided that I really can ’t get out of the business. I keep a small practice of clients I’ m able to work with. I’ ve aligned myself with a firm that specializes in working with families with special needs children. I help them co-ordinate available resources and things like that. It’ s learning something new and making a difference.

I’ m also involved with a couple of charitable organizations, and I’ m still on the Advocis Peel Halton board as past president and treasurer. That’ s kept me in touch with the industry.

If you have a hobby, it will probably make the transition into retirement easier.

LONG-STANDING CLU DESIGNATION HOLDERS

The Institute for Advanced Financial Education honours longstanding CLU® holders – those who have held their designation for 25 years or more—demonstrating a longtime commitment to excellence in fi nancial advice. We are honouring CLU designation holders who are celebrating 25, 30, 40, 50, 60 & 65 year increment milestones in 2022.

25-YEAR

CLU DESIGNATION HOLDERS

Susan D Olynyk, CLU, CH.F.C. Michael Y. C. Wong, CLU, CH.F.C. Michael T. Washburn, CFP, CLU, CH.F.C. J. Mark Gouws, CFP, CLU, CH.F.C. David G. Tompkins, CLU John R. Lanning, CH.F.C., CLU, REBC, CFP Kelvin A. McGillivray, CFP, CLU, CH.F.C. With more than 5,000 CLU® and CHS designation holders in good standing. The institute for advanced fi nancial education is the leading designation body in canada for fi nancial services practitioners in the specialty areas of advance estate and wealth transfer, and living benefi ts. The institute provides a platform of standards and advanced knowledge through designation programs and accreditation services. Institute destinations speak powerfully of a practice that is built on knowledge and a belief in the Jeanette McPherson, CFP, CLU, CH.F.C., TEP Chau Chan, CFP, CLU, CH.F.C. continuous refi nement of that knowledge. Geo rey E. Nanton, CLU George Ranisau, CLU, CH.F.C. William G. McTaggart, CFP, CLU Peter J. Izzio, CLU Robert J. Gaudet, CLU, CH.F.C. Malcolm T. Smith, CFP, CLU, CH.F.C., CHS Kevin M. Spence, CFP, CLU Dale F. Schnell, CFP, CLU Donald W. Hall, CLU Darcy W. Hermary, CLU, CH.F.C. CHS CFP Fred K. Sundquist, CFP, CLU, CH.F.C. David F. Kraemer, CLU, CH.F.C., CHS Perry R. Pellegrini, CLU, CFP, CH.F.C., CFA David Ho, CLU, CH.F.C. Mario D. Lalonde, CLU Robert J. Ingram, CLU, CH.F.C. Gus Macdonell, CLU Julianne C. Leith, CLU Mohamad H. Mahdi, CLU, CH.F.C. Brion C. Fahey, CLU Gary E. Harwardt, CFP, CLU, CH.F.C. Ellard Delaney, CLU Neil Bocking, CLU, CH.F.C. Mark A. Wadey, CLU, CH.F.C. Don Wood, CLU, CH.F.C., EPC Angelo Venetsanos, CFP, CLU Neil A. Paton, CLU, CHS Blair MacLean, CFP, CLU, CHS Allison P. Mcphail, CFP, CLU, CH.F.C. Robert N. White, CLU Kenneth J Blows, CFP, CLU, CH.F.C. Keith W. Leech, CFP, CLU, CH.F.C., CHS Irv Wilson, CLU Lorne A. Zalasky, CLU Sonia Schneider, CLU, CH.F.C. Glenn Ayrton, CFP, CLU, CH.F.C. Lisa L. Wong, CLU, CHS Mark J. Colosimo, CFP, CLU, CH.F.C. Gary F. Regel, CFP, CLU, CH.F.C., CHS Libby A. Wildman, CLU Robert P. Young, CFP, CLU, TEP Frank R. Tooton, CFP, CLU, CH.F.C. Ray J. Anders, CLU, CH.F.C. Thomas E. Bryan, CFP, CLU, CH.F.C. Paul H. Craft, CLU Heather E. Collingridge, CFP, CLU, CH.F.C. Barry E. Mount, CLU Raymond C. K. Cheung, CLU Vivian E. Saunders, CFP, CLU, CH.F.C. Thomas D. Martell, CFP, CLU Michel J. Lemaire, CLU, CH.F.C., CHS Scott R. Sisson, CFP, CLU, CH.F.C., CHS Chris B. Dietz, CFP, CLU, CH.F.C., CHS Stuart Crawford, CLU Annemarie Haapala, CLU, CH.F.C. Ian F. Doughart, CLU Jane E. Blaufus, CLU Peter Brian Friesen, CLU, CFP Andrew E. Macdonald, CLU, CHS Eugene V. Schmidt, CFP, CLU, CH.F.C., CHS J. Richard Kennedy, CLU, CH.F.C. Kevin J. E. Gi n, CFP, CLU Gerry C. Cabunoc, CFP, CLU, CH.F.C. Mathew L. Braganca, CLU Ronald Fredericks, CLU, CHS, CFP Kerry C. Deachman, CLU Chung-Kid Hu, CLU, CH.F.C. Michael H. Gilchrist, CFP, CLU, CH.F.C. Barry E. Jackson, CFP, CLU, CH.F.C. Bruce E. Biggar, CFP, CLU Allan McGlade, CFP, CLU Marc L. Madore, CFP, CLU, CH.F.C., CHS Michael B. McCormack, CLU, CH.F.C. Terence G. Amy, CLU, CH.F.C. Gary A. Wardrop, CLU, RHU Ashmead Khan, CFP, CLU, CH.F.C. Shaun Khorsandi, CLU Steve L. Steinman, CFP, CLU, CH.F.C. Carol Wood, CLU, CH.F.C., CHS Marc G. Bouchard, CFP, CLU, CH.F.C., CSA Harold (Ken) A. Steele, CLU, CH.F.C. Marie Heddle, CFP, CLU, CH.F.C., CHS Graham M Carter, CLU Bradley C. Charlton, CLU, CH.F.C., CHS Paul T. Craievich, CLU, CH.F.C. Theresa J. Zavitz, CFP, CLU, CHS, GBA, EPC Abbie M MacMillan, CLU Rick Y. L. Lam, CLU, CH.F.C. Magdalen Pik Sung Ng, CLU, CH.F.C. Margaret Nilevsky, CLU Wesley D. B. From, CFP, CLU, CH.F.C. Jurgen K Rudolph, CFP, CLU Dwayne F Day, CLU, CH.F.C. Mark J. Feeney, CFP, CLU, CH.F.C. Teresa Y. K. Tang, CLU Glen D. Oliver, CFP, CLU, CH.F.C. Allan Williams, CLU, CH.F.C. Michael J. Couture, CLU, CH.F.C., TEP James Virtue, CFP, CLU, CA Ejaz Uddin Nadeem, MA, CFP, CLU Ian M. Johnson, CFP, CLU Jill M. Koehler, CLU, CH.F.C., CHS

Holding a CLU designation is proof of commitment to higher standards. Even under the most di cult economic circumstances, longstanding CLU designation holders have continued to help Canadians build and preserve their wealth.

David T. Robinson, CFP, CLU, CH.F.C. Robert A. McCullagh, CFP, CLU, CH.F.C., CHS Alexander ODonnell, CLU, CH.F.C. Mark D. Lipman, CLU Paul F. Crema, CFP, CLU, CH.F.C. David V. Deverall, CLU Brian M. Pritchard, CFP, CLU, CHS Leslie M Szilagyi, CLU Robert A. Whiton, CLU, CH.F.C. Jean G. MacDonald, CLU, FLMI Kevin R Netterfi eld, CLU Rene P. Sauve, CLU Brent J. Rich, CFP, CLU, CH.F.C., CHS

30-YEAR

CLU DESIGNATION HOLDERS

David Ong, CFP, CLU, CH.F.C. Lucien J. Bossuyt, CLU, CH.F.C. Timothy J. Ramsay, CLU, CH.F.C., CFP, CPCA James W. Brownlee, CLU, CH.F.C. Patrick S. O’Connor, CFP, CLU, CH.F.C, FEA Troy Shelemey, CLU, CH.F.C. Eric E. Schenstead, CLU Doug A. Foster, CFP, CLU, CH.F.C., RFP T. Kevin Brady, CFP, CLU, CH.F.C. Doug W. McMechan, CFP, CLU, CH.F.C. Dave D. Foley, CH.F.C., CLU, CHS Douglas C Markewich, CLU, CH.F.C., TEP Derek A. Graham, CFP, CLU Greg Simmonds, CFP, CLU, CH.F.C. Mark S. Borts, CFP, CLU, CHS, CH.F.C. Ronald K. Pugsley, CFP, CLU, CH.F.C., CHS Richard J. Reaney, CFP, CLU, CH.F.C. Del G. Baycroft, CFP, CLU, CH.F.C. Stephen R. Campbell, CFP, CLU, CH.F.C. Martin L. Sobocan, CFP, CLU, CH.F.C., CHS Brigitte E. Kandert, CLU, CH.F.C., FCSI,Pl. John Lanni, CFP, CLU, CH.F.C. Daniel P. Lynch, CFP, CLU, CH.F.C. Robert N. Long, CFP, CLU, CH.F.C. Michael P. Deboski, CLU, CH.F.C. Ernest G. Cerson, CLU, CH.F.C. Patrick J. Kelly, CFP, CLU, CH.F.C. S Neil Schloss, CFP, CLU, CH.F.C. Neil Feigelsohn, CLU, CH.F.C. Gregory D. Abbott, CFP, CLU, CH.F.C. Imelda Harris, CFP, CLU, CH.F.C. Donald C S Rea, CFP, CLU, CH.F.C. Richard A. Benson, CFP, CLU, CH.F.C., CHS Michael A. T. Hajmasy, CFP, CLU, CH.F.C. Roderick W. Abbott, CFP, CLU, CH.F.C. David W. Faulkner, CFP, CLU Mario Paolucci, CLU, CH.F.C. Richard R. Dobel, CLU Mark A. Woofter, CFP, CLU, CH.F.C. Peter F. Creaghan, CLU Pierre Roy, CFP, CLU, CH.F.C., CHS Thomas D. Sullivan, CFP, CLU, CH.F.C. Vincent S. Wiegers, CFP, CLU, CH.F.C. Michael H. J. Evers, CFP, CLU, CH.F.C. Hal D. Gillrie, CFP, CLU, CH.F.C. David G. Draper, CFP, CLU, CH.F.C., EPC Peter H. Vogelsang, CFP®, CLU, CH.F.C., CHS

40-YEAR

CLU DESIGNATION HOLDERS

Donald P. Gordon, CFP, CLU, CH.F.C., TEP G. Philip Fisher, CFP, CLU, CH.F.C., RHU Heather Bethune, CLU, CH.F.C. Jim Steeden, CFP, CLU, CH.F.C., CHS Bruce D. Peckover, CLU, CH.F.C. Drew L. Stewart, CLU, CH.F.C., CEA Zachary J. Cattiny, CFP, CLU, CH.F.C. W R Lyle Garrett, CLU, CH.F.C., EPC Charles C. Cu ari, CFP, CLU, CH.F.C. Fernand H. Robichaud, CLU, CH.F.C. Johan C. Mares, CLU Rudy G. Fedorowich, CLU Patricia M. Gilding, CLU, CH.F.C. J. Bradley Stenning, CFP, CLU Peter Anthony Wouters, CFP, CLU, CH.F.C., CHS

50-YEAR

CLU DESIGNATION HOLDERS

Edward A. Misurka, CFP, CLU, CH.F.C. Edward W. Polci, CLU Douglas K Clarke, CFP, CLU, CH.F.C. Larry R. M. Terrace, CFP, CLU, CH.F.C. David C. Chescoe, CLU, CH.F.C. David J. Reckin, CFP, CLU, CH.F.C. Paul A. Paleczny, CLU, CH.F.C. Larry R. Mandseth, CFP, CLU, CH.F.C. Edward J. Topolniski, CLU

60-YEAR

CLU DESIGNATION HOLDERS

Paul V. Sabourin, CLU Stanley Tucker, CLU

65-YEAR

CLU DESIGNATION HOLDERS

Carl F. Woodward, CLU

For more information on the CLU designation, please visit www.iafe.ca/clu

CLIENT COMMUNICATIONS Best Behaviour

Todd Fithian explains how advisor behaviour impacts client decision-making

he financial services industry has become laser-focused on client behaviour. Understanding why clients do what they do is important, but many advisors are missing an opportunity to take a careful look at their own practice approaches to ensure the experience they ’ re creating for clients truly reflects the client’ s needs, wants, and desires — and not the advisor

T’ s.

When advisors engage with clients in ways that make relationships easier and bring clients closer, the trust that is built affects behavioural factors that drive client decision-making. When advisors build these trusting relationships, clients will not only seek advice, they will follow it, because why would they choose to do anything else? They trust the advisor who has helped them discover their values, clarify their vision for the future, and helps them develop a plan to achieve their specific goals. They are unlikely to be influenced by social media or cultural factors because they understand why they have made the decisions they ’ ve made. They know that their plan reflects their values and vision, which may be very different from someone else ’ s values and vision.

I believe three components, when used together, best represent the priority of engagement that forward-thinking advisors implement with their clients. 1) leading with empathy; 2) seeking to understand; and 3) delivering informed planning. Empathy is about building a relationship with deep care and respect for the client and their vision for the future. This step may require advisors to slow down and truly listen with the intent to learn. While some people are born empathetic, I’ ve come to understand that for many advisors empathy is a skill that must be learned. It’ s not that empathy doesn ’t exist within us all, it’ s that we don ’t always value it. What you learn by listening with empathy, and how you apply the knowledge gained, can help you build powerful, trusting client relationships.

Many advisors have been taught to problem solve. Gathering financial data and offering solutions is a habit that has become deeply ingrained. However, offering solutions to the client before you understand — and before the client understands — what they really want doesn ’t build a strong relationship. The good news is that bad habits can be changed and advisors can build new neural pathways by following a client-centred advice model consistently. Change takes time, effort, and willingness to be accountable.

When you are empathetic, you learn what matters to your clients and understand why it matters. The key is listening. When they tell you about their experiences, listen. This isn ’t the time to sell or to communicate planning solutions. Learning to lead with empathy, and truly leading with it, will differentiate your practice and allow you to move closer to the centre of your clients ’ lives. When you commit to enhancing your empathy skills, you begin to create a process that can be replicated and will become instinctive. Understanding is about gaining awareness and appreciation for the circumstances that are impacting the client. It is a qualitative discovery process that goes far beyond the traditional fact finding and data gathering that is essential to advising and serving clients. You need to think differently when gathering that information. Your client-facing moments should be dedicated to learning more about your clients, what they want, and the decisions they need to make to achieve their goals. By engaging all stakeholders in these conversations, you become the advisor at the centre of their lives.As trust grows,they won ’t make a financial move without you.

Empathy and understanding are essential components when creating powerful relationships with clients. Some say that seeking understanding is soft stuff. I disagree. An advisor ’ s ability to help clients clarify what they want and why they want it will affect the strength of the relationship. Planning brings quantitative and qualitative analysis, assessments, modelling, and forecasting together. This is where things get interesting. Through empathy and understanding advisors gain qualitative knowledge that will inform the quantitative analysis. The first step is to overcome the bias toward quantitative planning that pervades our industry. Quantitative factors are important, but they must reflect the qualitative data that comes from conversations around client values, vision, and goals. All too often, qualitative information lives in a file or, worse, becomes a distant memory when advisors work on and present solutions. Combining qualitative and quantitative data makes it possible for advisors to deliver actionable advice that leads to appropriate client action. When advisors lament that clients fail to act on the plans they ’ ve presented, I suggest they go back to their files and see whether the solutions presented reflected the clients ’ values, vision, and goals for the future.

While the industry is focused on understanding human behaviour, I believe the advisor of the future will create a new client experience. They will employ empathy, seek understanding, and develop plans that are built with qualitative and quantitative factors in mind. These steps are designed to lower client tension, giving clients time and space to gain clarity around what they want and why they want it. Once they understand these things, you can help them understand what it will take to achieve their goals and offer a plan that can help take them there.

By focusing on the client and what matters to them, you will have all of the opportunities you want to present solutions.You may be thinking that this sounds like a lot of work,that the process has more steps than your current approach, and that it could add considerable time to your current approach. First, let me confirm that I hear this concern frequently, and I have found that it does not hold true. The trust, rapport, and clarity built by moving slowly at the beginning of the relationship improves the decisionmaking ability of your clients and speeds up implementation. What’ s even better is that your clients will become fans of your work and they ’ll boast about you to everyone who will listen.

TODD FITHIAN is the co-founder and managing partner of The Legacy Companies, which help advisors grow their businesses. He can be reached at todd@think-legacy.com. Advocis and The Legacy Companies have formed a partnership to bring Legacy ’ s courses to Advocis members.

TRIBUTE

Remembering Harley Lockhart

(1947–2022)

By Kris Birchard

On February 10, the industry lost one of its most passionate members — a man of utmost integrity and a great leader. It was a pleasure to serve on the Advocis board of directors with Harley Lockhart and an honour to call him a friend.

Harley was a practising advisor in the Okanagan Valley of British Columbia. He commenced his career after graduating from Acadia University in Nova Scotia, the province he grew up in, teaching junior high school, and then went to work at Scotiabank. In 1980 he was transferred to Calgary where he met his wife, Dale. By 1990, Harley and his family were living in Kelowna, B.C., and during his time there, his more than 30-year career as a financial advisor began to blossom. Harley not only went above and beyond serving his clients, he did the same for the industry. He served as president of the North Okanagan Chapter, was the first chair of the Chapter Leadership Council, and in 2012–2014 served as the chair of the TFAAC board of directors. Harley also served his community. He was treasurer of Trinity Baptist Church in Kelowna and served on the board of the Kelowna Mission Thrift Store. He also coached many minor sports. Harley believed in raising the professional bar and was committed to continuous education. As such it is fitting that he was awarded the Leslie Dunstall Medal. In recognition of his contribution to the industry and the community, the Thompson Okanagan Chapter awarded Harley the Peter Newton Award.

Harley was a very unique individual. He was a man of deep convictions and strong opinions, but also had a great sense of humour that was punctuated by his wry and sometimes sarcastic smile. In the words of Todd Alstad, an Advocis colleague, “Harley had a pointed tongue and was the ultimate heckler. ”

Past Advocis chair Caron Czorny commented that Harley had a “ great way to really listen then think about an issue and be bold in his comments when he felt strongly about an issue. He was also quick to support and smile. ”

“Actions spoke louder than words. If you spoke up then you better back those words up, ” noted Advocis colleague Rob Bauml about Harley. “He was definitive that way and easy to follow as a leader because there were no inconsistencies in what he said or what he did. ”

Past chair Robert McCullagh observed, “I learned a great deal from him both in business and as a person. ”

When Harley retired, his son Jake continued to this day to manage the practice and serve the clients of Quail Ridge Financial Services. Like his father, Jake has also been awarded the Leslie Dunstall Medal. Past chair Randy Reynolds has been referring clients to Jake because he knows they will

receive outstanding service “just like his dad. ”

Harley believed in doing the “ right things ” and constantly quoted the Advocis slogan non solis nobis, not for ourselves alone.

Let me share an example of Harley ’ s leadership. In the early 2000s, there was a case going to the Supreme Court of Canada that involved the chartered banks and licensing requirements in the western provinces. The banks argued that they were regulated federally and not provincially and were therefore not required to be licensed provincially to sell creditor insurance in their branches. Interested parties in the western provinces requested that Advocis apply for Intervenor Status in relation to the Court’ s hearings on the case. It should be noted that applying for this status, and if granted, the execution thereof, came with a hefty cost of close to $150,000, at a time when financial resources,although available,were somewhat stretched.

Harley spoke strongly to his board colleagues in favour of making the application despite the cost. Harley ’ s reasons were non solis nobis. He said it was the right thing to do for our members and, more importantly, for the protection of their clients. The board heeded Harley ’ s advice and made the application.The Supreme Court granted the Intervenor Status and asked for an oral submission as opposed to the more common written submission. The reason the court gave for granting Intervenor Status was that they saw Advocis as a credible spokesperson for the Canadian consumer.

When the court rendered its decision, it was in favour of the provincial licensing regime. In their decision the justices cited seven reasons for doing so. Five of those reasons were contained in the Advocis brief. This decision is positive evidence of the relevance of Advocis and was a direct result of Harley ’ s commitment to doing the “ right thing ” and to non solis nobis.

Finally, consider past chair Al Jones ’ s insightful thoughts on Harley. “Harley, a Maritimer as salty and grizzled as the Atlantic Ocean, ” he wrote. “A true mariner who weathers the storm and whose honesty at times was a detriment to himself. Harley often referred to me as a ‘brother from another mother ’ as we share Nova Scotia roots. His blatant honesty and salty black humour seemed to cross the abyss of political correctness; however, to me it resonated his care and passion for his beliefs and a genuine commitment and loyalty to his family, friends, and colleagues. He was a mentor and lighthouse beacon to me and our industry. Non solis nobis. ”

Harley was a man of faith. His love of the Lord and the Bible guided his actions and decisions. His Kelowna colleagues told me that Harley would say, “When I am gone, I hope the world will be better because I was here. ” Harley, it is safe to say that your hope was realized. May you rest in peace. W hat an exceptional time to begin a career in financial advice. The recent introduction of Bill 157, the Financial Advisors Act, in the Ontario legislature is a huge step toward the creation of a bona fide profession for advisors and planners on the same level as doctors, lawyers, nurses, and accountants.

Advocis has long championed a professions model. Serving the public is, after all, the key to our success. Being a financial advisor can be a great career for the right person. Foundational to being the right person is having integrity and focusing on the well-being of clients. Understanding from the beginning that it’ s not about you sets your career in a positive direction. If you have the right character, it is up to you to maximize your chances of success — to “ start strong ” as you begin your career.

A strong first step is membership in an association such as Advocis, which demonstrates a willingness to be accountable to your peers for the benefit of the public. The mandatory Advocis Code of Professional Conduct establishes that anything less than the consumer ’ s best interest is not acceptable. From its inception in 1906, the association has always focused on the well-being of others — non solis nobis (not for ourselves alone). If you ’ re a new advisor, find a mentor who not only knows the ropes but has proven him or herself time and again. A quality mentor can help you identify challenges and potential roadblocks, flesh out a short- and/or long-term plan for success, and give you pointers on building your professional network.

While I can ’t speak for all advisors of my vintage, it has been my experience that seasoned practitioners are happy to mentor those starting out. Next to mentorship is education. Our industry is intensely competitive, and no matter how good you think you are, there will always be half a dozen others who are just as good, if not better. Naturally, motivation and organization will come into play — planning your work and working your plan — but by focusing early in your career on increasing your knowledge, you set yourself up for a bright future.

Here ’ s a tip: Never be satisfied with how much you know. Always be looking for that next educational challenge. Got your CFP? Great — now go get your CLU. Got your CFP and your CLU? Excellent — now grab your CHS and attend some conferences. You see how it works? Nothing replaces hard work in this profession, and the best way to distinguish yourself is by increasing your knowledge in areas that are relevant to your specialties or goal specialties. I’ m not recommending you become a designation collector; instead, collect knowledge and, most importantly, learn how to apply it. It’ll never let you down and will pay you back many times over throughout your career.

Perhaps the most important part of your makeup as an advisor is patience. Becoming a success in this industry takes time. This doesn ’t mean we can ’t enjoy a boost once in a while. If Bill 157 becomes law in Ontario (and is eventually rolled out nationwide), you and your peers will benefit. But in my experience, success comes more readily — and often more swiftly — to those who are organized and have a clear vision for their future.

Worth Repeating: IN HARLEY LOCKHART’S OWN WORDS FROM MARCH 2014

John A. Tory

AWARD 2021

THE INSTITUTE CONGRATULATES 2021 JOHN A. TORY AWARD WINNER

QI LU, CFP, CLU FOR ATTAINING THE TOP MARK IN CANADA.

ALBERTA

Scott C. Robertson, CFP, CLU, CHS Roger D. Stevenson, CFP, CLU Braden Pennycook Neda Jeddi, CLU, QAFP Rhealynne Ries, CLU Courtney Alcock, CFP, CLU Harvey H. Agustin, CFP, CHS Louis J. Rouleau Jos Herman, CFP, CPA Tara L. Schneider Stephanie Dwyer, CFP, CHS Thomas Carrozzier, CFP Derek G. Nicoll, CFP, CHS Adegboyega A. Olatunde, PFP® Mo Zhou Julia Best

BRITISH COLUMBIA

Scott A. Grant, CLU Pavel Dyadin, CLU Shengbin Yang, CFP®, CLU, PFP® Jordan Rausch, CLU, QAFP™, CIM Clay E. Gillespie, CFP,CIM Huiqiang Peng, CHS Herby Desriveaux, CFP Clive Agyar, CFP John L. Hakkarainen Qi Lu, CFP Daniel Sitar, CFP Mackenzie Seeley, CFP Jason F. Netherton Kelvin Yee Hang Lam, CFP® Colton Elmer Hope, CFP Harpreet K. Bains Brett Clark Ahmad Soleiman-Panah, CFP Yubing Li, CFP

MANITOBA

Sheryl Troup, CFP, CLU, CPA, CA Richard H. Reif, CFP, CLU Angela C. Wittmann, CFP Travis Gesell, CFP

NEW BRUNSWICK

Justin P. Richard, CFP, CLU

NOVA SCOTIA

Jason E. Malloy, CLU Keith MacKay, CFP, CHS, RCIS Chad Allan Relf, CFP, CLU

ONTARIO

Nickolas A. Cassis, CFP, CLU Debra L Hamilton, CLU, CHS Lucie Larocque, CFP, CLU Sean Warburton, CLU Chunhua Shi, CLU Je rey Poirier, CLU, CHS David A. Cooke, CLU Luxmihaasan Lucky Rasappah, CLU, CHS Naoshad S. Pochkhanawala, CLU Rachel L. Bough, CLU, CHS Chad Larmond, CLU, RHU Patrick J. Buscar, CFP, CLU Suzanne Schultz, CFP, CLU Timbo Lam, CFP Gary R. Armstrong, CPA, CGA Rob A. Polci Jianguo Duan Bruno Daniel Fortin, CFP Johnny Gialamas, CFP Shobana Varatharasa Terry T. Marek, CFP,CLU, R.F.P. Geo S. Douglas, CFP, CLU Viresh C. Mathur, CLU John A. Kodric, CLU Michael S. Madeira, CLU David H. Sutherland, CLU Stephen D. Palmer, CLU Eric Allan Simpson, CLU, CHS Min Juan Zheng, CLU Elias Soltani-Aski, CLU, CHS Julia Lee Dicks, CLU, RHU, CPCA Matthew R. Dam, CLU Mark J. Levitt, CLU Anthony Visconti, CFP, CLU, CHS Rushelle S. Irons-Vamos, CLU Paul Douglas Gaulton, CLU Katie Lee Deering, CLU Brock A. A. Schultz, CLU, CHS Qing A. Wang, CLU Tom James, CLU Steve G. Adams, CLU, BBA, MBA Donald N. Mason, CLU Andrew Dennis, CFP, CLU Marilia Liana Carvalho, CLU Lucia Solomon, CLU Thien Tu Nguyen, CLU Paul N. Scheib, CLU Brian D. McCreery, CLU, CIM Timothy Howard, CLU, CHS Timothy Schonberg, CLU Katina Michelis, CLU, CHS Christopher H.M. Lee, CLU Namrata Patel, CLU Patrick C R MacDonald, CLU, CHS Fei Jiang, CLU Michael Mcca rey, CLU Charu Mathur, CLU Je rey Bernstein, CLU Satheeskumar Nagalingam, CLU Maureen McBratney, CLU, PFA Dobrinka Zhivkova Nikolova, CLU Jason D. Fast, CLU Shawna Clarkson, CLU Luigi Costa, CLU Alynn Godfroy, CLU Amy Kate Wickenden, CLU Diane D.G. Guo, CLU Qian Li, CLU Yin Shen, CLU Rebecca McGrath, CLU Marc Gabriele, CLU Domenic Larizza, CLU Victor Schuliakewich, CLU, CHS Joshua Alvin Davie, CLU Jigarkumar V. Patel, CLU Kevin John Moniz, CHS, CLU

By obtaining the CLU® designation, you have demonstrated exceptional commitment to your career and clients, and have elevated your practice to a level that distinguishes you among your peers. www.iafe.ca

Katherine Ann McConnell, CLU Adriano Beghin, CLU, QAFP Carrie Yutien Wang, CLU Geethanjali Subramaniam, CLU, CHS Thomas E. Juha, CLU, CHS Edward Hambarchian, CLU Randy I. Rosenblat, CLU Shan Lu, CLU Tracy M. Tronchin, CLU Dwayne Anthony Gordon, CLU Sarah P. Cumpson, CLU Matthew E. Thomas, CLU Zheng Max Liu, CLU Anupreet Malik, CLU Yan Dou, CLU Zhuming Yi, CLU Michael D’Angelo, CLU FenFang Tong, CLU Dayun Huang, CLU Dongwen Huang, CLU Sean George, CLU Mosunmola Sami, CLU Li Jiang, CLU Mitchell Donald Fox, CFP®, CLU Jennifer J. Trevor, CLU Jingwei Sun, CLU Atul R. Patel, CLU Narinder Singh Lobana, CLU Tigest D. Gulbet, CLU Jaswinder S. Minhas, CLU Devendra Kumar, CLU William Hurley, CLU Hanjun Chen Kun Wang Stephanie Epstein Dylan Brown, CFP Gregory M. Toner, CPA John C. Stephen, FSA Yinghui Meng Jacqueline Soong, CFP Jessica A. Kemp Amanda M. Bieber, CFP Jeanette M. Molloy, CFP Sandra Shoebridge, CHS, QAFP Dalia Hamdy Oluwashayo J. Oretan, CFP, TEP Shengbin Chu, CFA Garry L. Goodwin, CFP, CHS Duncan E. Presant, CFP Patrick Michael Fitzgerald, CFP, CHS Marija Vuckovic Mr. Kevin A. Dineen Liya G. Tewelde Andrew Hill, CFP David Davies Irina Yugay Zhiling Pu Elena Yazeva, CFP Adam Lachance Peter B. Gillespie Jung-Hee Kim, CFP, TEP Li Jiang, CLU

QUEBEC

Salomon Gamache, CLU, Pl.fi n, CIM Samuel Platel, Pl. Fin Liliana Danila

SASKATCHEWAN

Jason M. Arden, CLU, CHS Sean Purdue, CFP

UNKNOWN

Adi Bartal, CLU Peter Lacey, CLU Pascale Hansen, CLU Devin K. Block, QAFP

Leslie W. Dunstall

AWARD 2021

THE INSTITUTE SPECIALLY RECOGNIZES THE 2021 DUNSTALL PRIZE WINNERS FOR ATTAINING TOP MARKS IN THEIR RESPECTIVE PROVINCES:

ALBERTA

Braden Pennycook, CFP, CLU

MANITOBA

Sheryl Troup, CFP, CLU, CPA, CA

NEW BRUNSWICK

Justin P. Richard, CFP, CLU

NOVA SCOTIA

Keith MacKay, CFP, CLU, CHS, RCIS

ONTARIO

Jennifer J. Trevor, CLU

QUEBEC

Salomon Gamache, CLU, Pl.fi n, CIM

SASKATCHEWAN

Sean Purdue, CFP, CLU