3 minute read

EUROPE-US AIR FREIGHT STRENGTHENS WHILST OTHER MARKETS WEAKEN

Westbound transatlantic air cargo demand up 6% in January, but global uncertainty remains

Despite high inflation and falling US retail sales, westbound air cargo volumes between Europe and North America rose 6% year-on-year in January but overall global air cargo demand continued to fall, down -8%, as an earlier Chinese New Year and economic headwinds subdued other major lanes, according to the latest weekly market intelligence from CLIVE Data Services, part of Xeneta.

The Europe to North America corridor stood out in terms of growth in January, although its average spot rate of USD 3.09 per kg edged down 4% from last month. However, compared to the shrinking volume on ex APAC and inbound Europe trades, transatlantic westbound demand remained buoyant. But growth has decelerated dramatically from the three-digit growth in rates of +124% in April 2021 when compared to the pre-pandemic level.

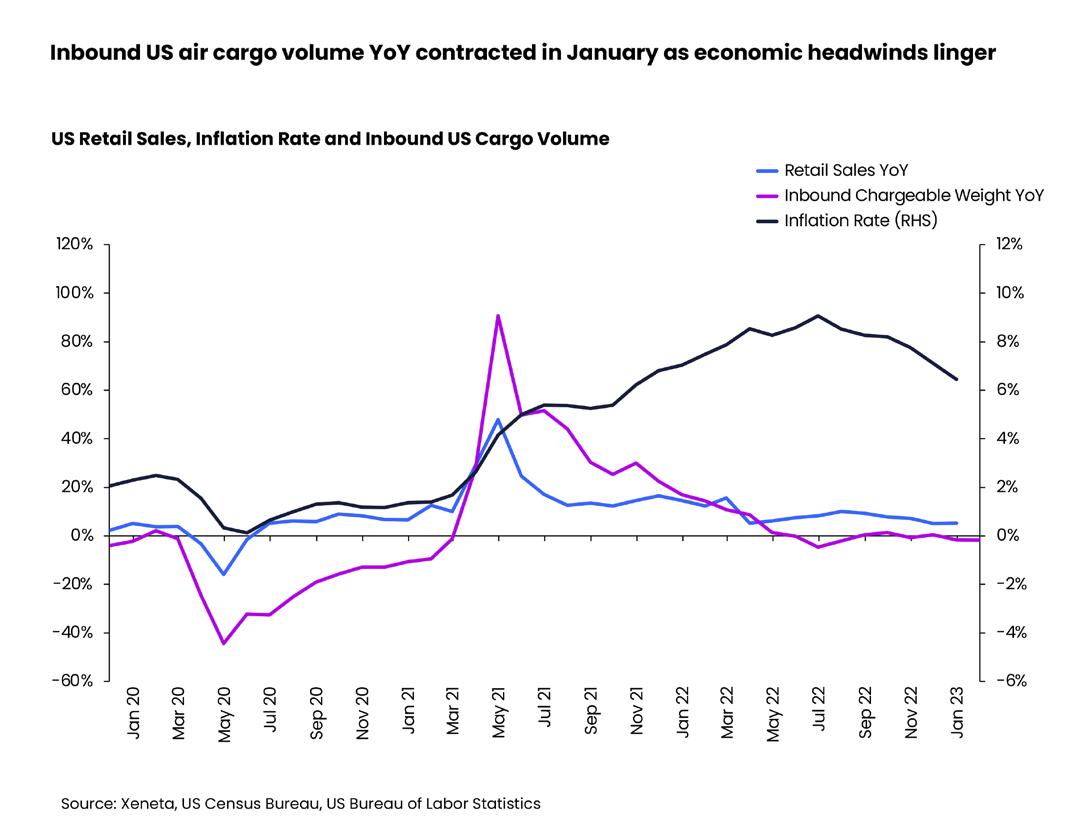

The signs of resilience in westbound transatlantic volumes goes against the continuing economic pressures facing consumers in the US. For instance, US inflation rose above target again in December 2022 (2%) for a 21st consecutive month. It stood at 6.5%, down 2.6% points from its peak in June last year. Although growth had decelerated since July, the impact on inflation persists. The US Census Bureau reported US retail sales have been slowing since July last year, pushing the November inventories-to-sales ratio to the highest level in nearly 2 years.

As the air cargo market tends to be more sensitive to economic cycles than the general market, air volume decline led the decline of retail sales by 2 months, and the market outlook remains uncertain. The total inbound US air cargo market registered its first negative growth in May 2022 and stayed in negative territory for five out of the seven remaining months of last year. In January 2023, global air cargo volumes into the US continued to fall, down 2% from a year ago.

Looking at its major competitive mode, the transatlantic eastbound ocean freight spot rate increased 230% to USD 6148 per 40DC in January compared to the 2019 level. In comparison, the January air spot rate was only 41% above pre-pandemic levels, which was also 14% points below the ratio for the global average air spot rate.

The average spot rates on the APAC to North America corridor slid 13% from last month to USD 4.74 per kg in January, 48% above prepandemic levels. For ex Southeast Asia trades, average spot rates fell more noticeably, -17% to USD 4.06 per kg, only 24% above prepandemic levels.

The economic headwinds blew even harder on the European market. Due to the knock-on effects of the Ukraine war, inflation rates have seen double-digit growth since August 2022. Although European inflation rates might have reached their peak, they remain highly elevated (+10.4%) compared to the immediate pre-pandemic periods. Both retail sales and general air cargo volumes were hit hard by this. Inbound Europe chargeable weight fell for a 13th consecutive month year-on-year in the first month of 2023, with January air cargo volumes down 9% from one year ago.

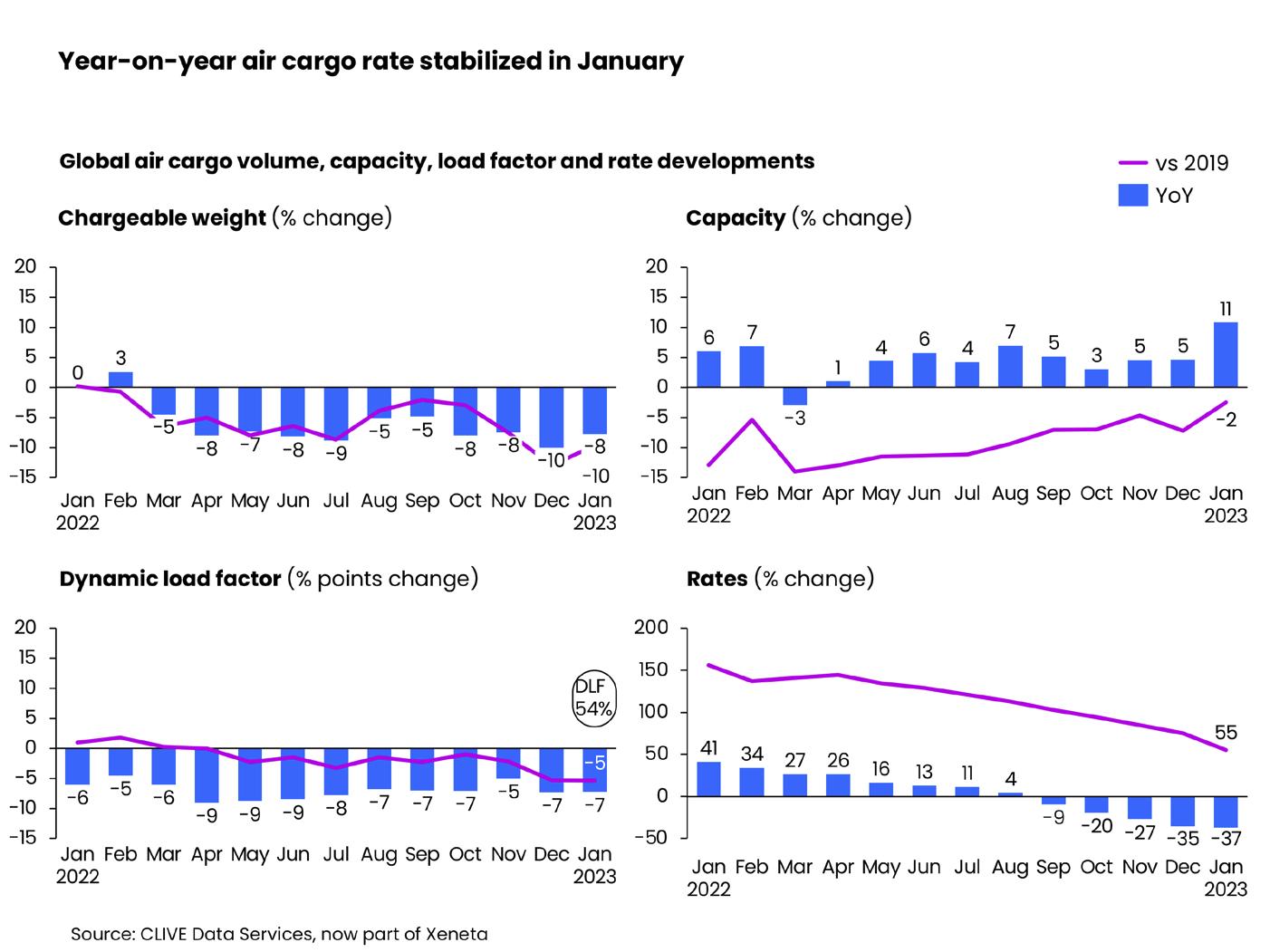

Overall global air cargo growth continued to slow last month. The -8% fall in demand, down 10% on the same month in pre-Covid 2019, contributed to the -37% decline in the global airfreight spot rate to USD 2.89 per kg, narrowing the gap to the pre-pandemic level to +55%. Global air cargo capacity restored a noticeable 11% year-on-year, 2% below the 2019 level.

The global average dynamic load factor, measuring cargo load factor by considering both volume and weight perspectives of cargo flown and capacity available, stood at 54% in the first month of 2023. With the capacity increase and the volume decrease, this resulted in a load factor decline of -7% pts compared to a stronger New Year in January 2022. Compared to 2019, it was also down 5% pts as the demand/supply balance started to lean towards oversupply.

Given the earlier Lunar New Year in 2023, January is not the best month to judge APAC market performance. While the average spot rate from APAC to Europe dropped 11% month-over-month to USD 4.18 per kg, it remained 72% above pre-pandemic levels, partly due to the rate impact of rising operating costs caused by the Ukraine war.

The early Chinese New Year might be causing some noise in the January air cargo data with factories there closing ahead of the New Year, contributing further to a weak global market producing load factors at a level we haven’t seen for some time. So, there is still a high level of uncertainty but, if rates haven’t yet reached the 2019 level in value in the current climate, and with an expectation that inventory levels will need restocking at the end of Q2 and Q3, then it’s unlikely we will see spot rates return to the pre-pandemic level unless this happens soon. But this, of course, partly depends on consumers spending in a similar fashion as we have seen recently.

Niall van de Wouw, Chief Airfreight Officer, Xeneta

Elsewhere, although Latin America to North America airfreight volume was down 7% year-on-year in January, this was 29% higher than the 2019 level. Its average spot airfreight rate of USD 1.43 per kg in January also dipped 7% on the previous month, leaving the January 2023 air spot rate only 13% above the pre-pandemic level, the lowest among all corridors after having been one of the high-growth trade lanes evolving from the pandemic. Capacity on this lane in January rose 36%.