Birmingham Economic Review 2022 Chapter 4: Place: Connecting Sustainable Communities Connect. Support. Grow.

Introduction

The annual Birmingham Economic Review is produced by the University of Birmingham’s City REDI and the Greater Birmingham Chambers of Commerce. It is an in depth exploration of the economy of England’s second city and a high quality resource for informing research, policy and investment decisions.

This year’s report provides comprehensive analysis and expert commentary on the state of the city’s economy as it emerges from disruption caused by the pandemic into a new period of high inflation and uncertainty. The Birmingham Economic Review assesses the resilience of the city, its businesses and its people to the set of challenges stemming from the UK’s vote to leave the EU, the coronavirus pandemic and now the energy crisis. It includes an update on the development of the region’s infrastructure and highlights opportunities for growth, building on existing strengths and assets.

The most recently available datasets as of 30th September 2022 have been used. In many circumstances there is a significant lag between available data and the current period. Contributions from experts in academia, business and policy have been included to provide timely insight into the status of the Greater Birmingham economy.

Report Geography

The report focuses on the ‘Greater Birmingham city region’ defined by the boundaries of the Greater Birmingham and Solihull Local Enterprise Partnership (GBS LEP). The GBS LEP area consists of the following local authorities: Birmingham, Solihull, Bromsgrove, Cannock Chase, East Staffordshire, Lichfield, Redditch, Tamworth, Wyre Forest.

References to the ‘West Midlands region’, or ‘West Midlands (ITL1)’, are to the large scale region at International Territorial Level 1 (ITL1). There are nine ITL1 regions in England: North East, North West, Yorkshire & The Humber, East Midlands, West Midlands, East of England, London, South East and South West in addition to Scotland, Northern Ireland and Wales. Note that ITL recently replaced the EU’s Nomenclature of Units for Territorial Statistics (NUTS). Geographies of ITL and NUTS territories generally correspond except for minor differences at local authority level outside the Midlands.

References to the ‘West Midlands metropolitan area’ are to the West Midlands county comprising seven metropolitan districts (WM 7M): Birmingham, Solihull, Coventry and Dudley, Sandwell, Walsall, Wolverhampton.

References to the ‘West Midlands Combined Authority (WMCA) area’ are to that administered by the Combined Authority.

Note that figures may not always total exactly due to rounding differences. Figures in some tables may be undisclosed due to statistical or confidentiality reasons.

1

Foreword and Welcome

Chapter 1. Economy: Crises and Resilience

Chapter 2. Business: Disrupted Markets

Chapter 3. People: Challenging Times

Chapter 4. Place: Connecting Sustainable Communities

Chapter 5. Opportunity: Building on Strengths

2 Index

Place: Connecting Sustainable Communities

The city region is one of the best placed and most well connected areas of the country, both physically and digitally. Continued investment in digital and transport infrastructure alongside the development of high quality places is necessary for future success and sustainability. Improvements in this direction have been taking place for a number of years, leading to outdated perceptions of the city being challenged and changed. The Covid 19 pandemic has complicated the picture by altering mobility and working patterns.

The Levelling Up White Paper set out plans for the West Midlands to become a trailblazer region for devolution of ‘London style’ powers over housing, transport and development. This includes the plans for the West Midlands to become the UK’s first Smart City Region, funding for brownfield regeneration for homes and jobs, a share of the Towns Fund (for Wolverhampton at least), and more say over running local railways. This will enable the region’s leaders to respond to local challenges and needs, not least addressing housing affordability, sustainability and the climate crisis.1

This chapter provides an update on changes to transport mobility patterns and their impact on the city centre and sustainability. The chapter also provides updates on transport connectivity, digital connectivity, housing delivery and the office market.

Transport Connectivity

Transport connectivity continues to improve across the region, with existing projects progressing at pace whilst new plans and funding have been announced for further works.

Construction of the London Crewe High Speed 2 (HS2) route is well underway with almost 25,000 jobs, over 800 apprentices and more than 2,400 UK registered businesses, including 1,700 SMEs, already involved. This includes over 160 suppliers from the GBSLEP of which approximately 130 are SMEs.2 Maintenance of the new trains will take place at sites across the country including at Washwood Heath in the east of Birmingham. The Crewe to Manchester Bill was submitted to Parliament earlier in the year whilst revisions to the eastern leg have been made to speed up delivery and save on cost.3

The Metro network continues to expand. The Westside extension to Centenary Square in the city centre is already open with the completion of the route to Edgbaston Village due to open imminently. The first phase of the Wednesbury to Brierley Hill extension to Dudley town centre is expected to open in 2024. The Eastside extension is well underway with public realm improvements and utility works taking place in Digbeth and the first tracks having been laid over the summer. Future phases will see the Metro extend to the airport and future HS2 interchange station in North Solihull, also serving the NEC and Genting Arena.4

The government’s £96bn Integrated Rail Plan was published in late 2021, setting out investment and delivery plans for the Midlands. The Plan seeks to introduce integrated and contactless ticketing systems in the Midlands and commits to progressing work on the Midlands Rail Hub which would improve connectivity. Capacity between Birmingham and Nottingham and Manchester could treble, whilst journey times could fall dramatically.5

A five year City Region Sustainable Transport Settlement (CRSTS) of £1.05 billion for the West Midlands Combined Authority was confirmed by the Department for Transport (DfT) in the summer. It is intended to support further extension of the Metro, improvements to bus services including Sprint, development of new rail stations, multi modal transport accessibility, sustainable travel, infrastructure maintenance and the delivery of local network improvement plans.6

WMCA press release, Feb 2022, available here

HS2, Supply chain map desktop [accessed September 2022]

HS2, Project update, August 2022 [accessed September 2022]

Midland Metro Alliance, Projects page [accessed September 2022]

DfT, 2021, Integrated Rail Plan for the North and Midlands

DfT, City Region Sustainable Transport Settlements: confirmed delivery plans and funding allocations [accessed September 2022]

3

1

2

3

4

5

6

As one of the first four UK Future Transport Zones, the West Midlands (with £22m DfT funding), has also been leading in trialling new transport technologies including connected and autonomous vehicles, e scooters, demand responsive bus services, Mobility as a Service (and the ‘One App’), mobility credits, and mobility hubs (bringing together eco friendly travel information and options). Trials are delivering data driven insights to help build a more sustainable transport system here, and nationally.

The West Midlands has seen significant improvements in active travel (cycling, walking, and wheeling), following Local Cycling and Walking Improvement Plans, and success gaining shares of the £2bn DfT active travel funding announced in 2020 with the national ‘Gear Change’ vision and target that half of all urban journeys will be active travel by 2030 (the West Midlands Cycle Charter targets 10% of all trips to be by cycle in 2033).

4

Mark Thurston, Chief Executive Officer, HS2 Ltd

Britain’s new high speed railway will link Birmingham, Manchester and London with the biggest cities in Scotland. For the 170 miles of new high speed line between London and Crewe, construction is well underway. We currently have over 340 active sites between Birmingham and London with almost five million hours worked per month.

HS2’s mission is to build the best railway in the best way; levelling up the UK economy, setting new standards for sustainability in construction, and creating opportunities for businesses and individuals to deliver the project.

In January we hit a significant milestone as we deposited the Phase 2b hybrid Bill into Parliament, extending the railway from Crewe into Manchester. The Bill passed its second parliamentary reading in June 2022, winning the vote by a large majority. This is a huge step forward to linking the Midlands to the North of England and opening up further economic opportunities.

HS2 is now supporting over 25,000 jobs and more than 900 apprentices have started their careers with us. Nearly 2,600 businesses have already delivered work on the project, of which 70% are SME’s.

The West Midlands is at the heart of the new railway. In July, we announced that Laing O’Rourke will build the new Interchange Station in Solihull. This station is key to the growth plans for the region and will support 70,000 jobs and create 650,000 square metres of commercial space. The station will generate an additional £6.2bn of economic activity per annum and bring 1.3m people to within a 45 minute public transport commute of this transport hub.

At Curzon Street station in Birmingham, we received planning consent for the striking new viaducts which will form part of the station area in June. These viaducts will maximise public space and enhance the public realm in Digbeth, as well as being the gateway to Birmingham for visitors travelling on the new railway. The Curzon Street Masterplan (released by the West Midlands Combined Authority) outlines proposals for 141 hectares of regeneration, which will bring £724m in investment into the surrounding area. It envisages the creation of 36,000 new jobs, 4,000 new homes and 600,000 square metres of commercial development.

We are proud of our bold ambition to make HS2 a zero carbon railway both in construction and once our trains start running. Earlier this year we published our Net Zero Action Plan, which outlines how the HS2 project will achieve this by 2035. Our target is to reduce construction carbon by 50% and we want to go further wherever possible.

The good news is we’ve already achieved a 25% reduction. To help us reach our 2035 goal, we want all our sites to be diesel free by 2029 and we’ve already announced our first diesel free site is up and running at our Canterbury Road vent shaft. Part of our diesel free strategy involves the use of pioneering technology, such as electric cranes. There are currently only five of these operating worldwide, three of which are on the HS2 project and one of these is currently at our Curzon Street site.

As part of HS2's Green Corridor, we have successfully planted over 800,000 trees and shrubs and created more than 100 wildlife habitats. This will run alongside the railway, creating a network of bigger, better connected, climate resilient habitats and new green spaces for people to enjoy. As well as trees and shrubs, we’re also planting new woodlands and creating new ponds, grasslands, and meadows, with many new habitats flourishing; all before a single train has started running.

We’ve already made significant progress in 2022, and as we enter peak construction on Phase One, we’ll continue delivering key milestones. One of our three tunnel boring machines (TBMs) has now finished its 1km journey under protected ancient woodland at Long Itchington Wood and will now be dismantled and returned to bore the second tunnel parallel to the first. Our other two TBMs under the Chilterns have made significant progress and over the next 12 months we’ll launch two more TBMs along the Phase One route.

5

We’ll soon be unveiling the design of our trains, following the announcement of the rolling stock contract award to Hitachi Alstom at the end of 2021. These trains will be manufactured in the UK. The design work taking place now in Birmingham will produce some of the fastest, quietest and most energy efficient high speed trains in the world.

From its inception, HS2 has always been more than a railway. HS2 will transform the way people travel around Britain, opening up new opportunities, whilst providing a low carbon alternative to long distance travel. HS2 will leave a lasting legacy on the UK construction industry, setting new standards in health and safety, sustainability, innovation, and skills and employment.

6

Mobility

Current data supports predictions that the pandemic would cause long term change in transport patterns. Whilst car usage returned to near pre pandemic levels quickly following the series of lockdowns, other modes have seen persistent altered usage rates. Structural changes in transport use could affect the attractiveness of future investments in infrastructure and place.

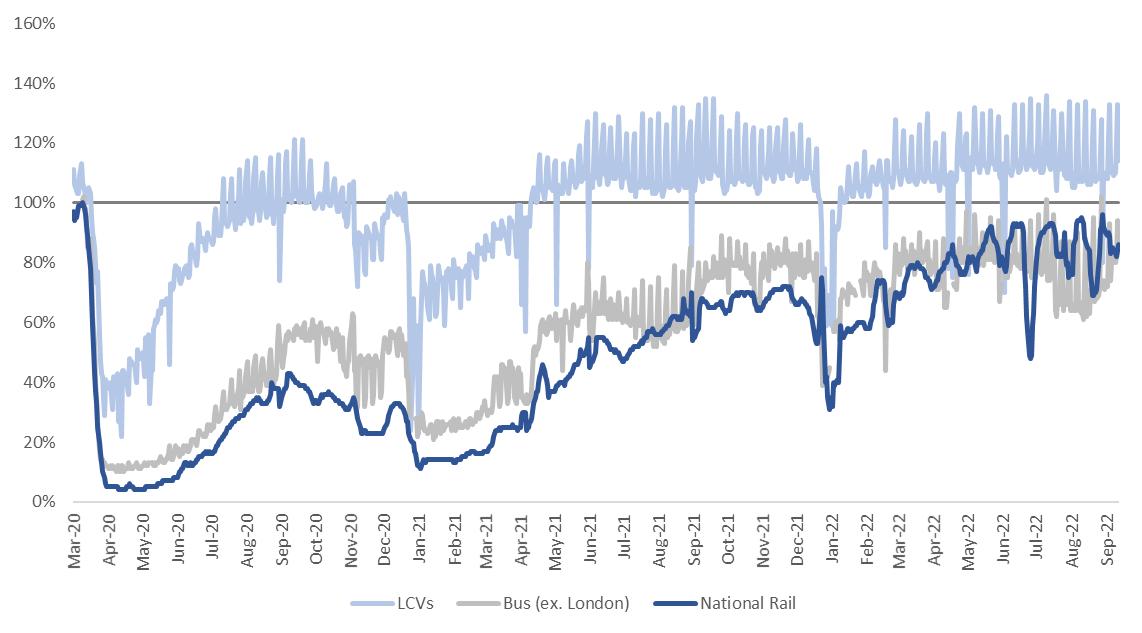

Nationally, public transport usage remains below its pre pandemic level, with both rail and bus usage for the year to mid September being down by almost a quarter. In contrast, light commercial vehicle (LCV) usage remains 16% higher than pre pandemic with seasonality appearing to be only a minor cause.

Transport use by selected mode (Great Britain)

Source:DfT,Domestictransportusebymode:GreatBritainsince1March2020. Dataisindexedtoequivalentdayoftheweekprepandemic.

Trends in the West Midlands look similar, with bus travel still almost 20% below normal demand as of September, although showing a slowly improving trend. Metro ridership looks to have returned to pre pandemic levels, although the data is complicated by the total suspension of services between March and June due to issues with the trams and more recently by increased demand during the Commonwealth Games.

Public transport variance from normal demand across the West Midlands

7

Source:TfWM,Travelpatterns Raildataisbasedonnationaltrends.

Meanwhile micromobility has grown in popularity over the period, with significant numbers of people now using e scooters, and the West Midlands Cycle Hire scheme that now includes e bikes. Everyday cycling and walking surged in popularity at the start of the pandemic, as these were permitted exercise in lockdown, when people were working from home/furloughed in the mild spring weather. Walking increased from a 32% share of personal trips to 86% and cycling from 1% to 4%. Active travel has now returned to more normal levels but still has an elevated share and the West Midlands aims to continue this building on the legacy of the Birmingham 2022 Commonwealth Games.

8

Daljit Kalirai, Sales Director, National Express

Every single day, throughout the whole of the pandemic, National Express bus drivers got their fellow key workers to where they needed to be.

Since the beginning of 2022, nearly 90% of fare paying passengers have returned to our buses. But inside that overall figure, we have seen some real changes in travel patterns.

Older people

About 70% of our older customers have got back on the buses. Across the UK, there are about 15% fewer people travelling on OAP passes than fare paying passengers.

But interestingly, at National Express we see that 66 72 year olds are travelling morethan they were before the pandemic. And their travelling times suggest they are commuting.

It’s the over 72s who are going out much less some of them hardly at all. We think this partly due to a continuing fear of getting Covid and the related drop off in activities that used to get them out and about like clubs and get togethers with friends.

New ways of working

Since the pandemic, there’s been a 10% drop in bus passes that are longer than a week. And an 8% increase in people buying day tickets. We still sell about as many weekly passes as we did in 2019.

In September 2020, National Express introduced flexible “bundles” of digital tickets so customers only pay for the travelling they do. Using our flexible tickets saves a customer over £2,500 a year compared to Top Gear’s famous “reasonably priced car” that red Vauxhall Astra 1.6.

Cost of living

Buses are the mode the most deprived people in our society rely on. DfT data shows that bus passengers are less male, less white, less able bodied and less educated than the average. 77% of all job seekers and 87% of young jobseekers have no access to a car, van or motorbike and are completely reliant on local bus networks.

So National Express is working hard on ways to help all our customers tackle the rising cost of living.

Everyday low fares

National Express is part of the West Midlands Bus Alliance. One of the main deliverables of that is an agreement to keep fares low.

When pandemic social contact restrictions were lifted In June 2021, we cut the price of the peak day ticket from £4.60 to £4. This gives us the cheapest bus fares in England. So adults can now travel anywhere on our entire West Midlands bus network for less than the cost of a burger and the same price it was in 2014. The average commuter is saving over £130 a year on bus travel.

Contactless technology

Contactless payment has been available on National Express buses since 2017. Daily capping means customers can use their bank cards every time they travel on our buses and never pay more than the £4 daysaver.

In June 2021, to help our customers with hybrid work patterns, we introduced contactless weeklyticket price capping. Customers travel as much as they like and at the end of seven days, they are charged no more than the cost of a weekly ticket however many journeys they made.

9

National Express West Midlands was the first company outside London to offer this kind of flexibility.

Discounted bus travel for NHS workers

National Express works closely with all our NHS hospital trusts and ICSs to support the relief of pressure on car parking at hospitals, help staff with the cost of living and help the NHS meet their Scope 3 emissions.

National Express provides bespoke online “portals” to hospital trusts, where their staff can get an exclusive 10% discount on bus travel.

Results

Throughout the pandemic and afterwards, bus patronage recovery in the West Midlands has been consistently 3 5% ahead of the national average. Our patronage is 6% better than our closest comparator, and still growing. KPMG analysis of our low fares strategy showed that our fares cuts have grown passenger numbers by 9%.

National Express’ focus on low fares for our customers is also helping cut carbon emissions and air pollution. A recent TfWM survey shows that the cost of living crisis is changing behaviour in a way that benefits the environment:

● 54% of people are now using the car less.

● 39% of people are using public transport more.

● 45% of people are already modal shifting and a further 29% are considering doing so.

Just as in the pandemic, our bus driver key workers are still getting young people to education, getting adults to work and getting older people to medical care. And they’re helping to save the planet too. Buses remain absolutely crucial to the prosperity, health and happiness of our communities.

10

Charles Prothero, Transport Planning Officer, Transport for West Midlands

Covid 19 disrupted many aspects of society, including local travel. Government lockdowns to suppress the virus, meant a swift, prolonged reduction in travel, although movement of goods continued and public transport operated for key workers.

We are now ‘living with Covid’ freight and public transport networks operate without restrictions but personal travel in our city region looks different than in 2019. This article asks what has changed in our travel and why, and how Transport for West Midlands (TfWM), the transport arm of the West Midlands Combined Authority (WMCA) is addressing the positive and negative implications.

What has changed in our local travel?

Before Covid, in local data from the National Travel Survey (NTS), our average resident made around 900 trip stages annually (each time you change mode or service is a trip stage), a number which had been falling slowly. The share by mode was:

Active travel cycling and walking 33%

Car and motorcycle 57%

Public transport including taxi 10%

Public transport fell 90% at the beginning of the unprecedented lockdowns, rising and falling subsequently with changing restrictions. Active travel saw a boost as legal outdoor exercise and as a way to travel with fewer virus safety concerns. NTS data for 2020 (latest available) with all its restrictions showed only 700 stages with a very different share:

Active travel cycling and walking 46% Car and motorcycle 46%

Public transport including taxi 8%

Current data shows further change, but no return to pre Covid numbers. Public transport use has been recovering, but in places is plateauing below pre Covid. Car travel is nearly at pre Covid levels, and general traffic higher in places (more van traffic with online deliveries). Data also suggests some of the active travel growth seen in Covid has been maintained. Overall, trip stage numbers are higher than before but with less morning peak travel to key centres, especially at the start and end of the week, and a stronger weekend travel recovery.

Why is our travel changing and what are the implications?

Many factors underlie these changes. Early in the pandemic, once TfWM had helped secure continued public transport operation for key workers, attention turned to the eventual exit from restrictions, and uncertainty about how local travel was changing. Scenario planning was used to manage this uncertainty, and identify the range of possible local travel futures. This meant identifying the factors (and likely movement in them) behind the changes. Factors include: economic; effects on employment, and consumer spending; social; ongoing fear of the virus, persistence of online adaptations (work, education, shopping), strength of environmental concerns; state; including financial support for public transport.

Scenario planning also made clear that no automatic return to the pre Covid local travel picture was likely in the wake of movement in these factors.

Instead, scenarios suggested some very negative implications were possible; more car use, and less public transport use and active travel, meaning in turn more carbon emissions (jeopardising #WM2041 targets), noisier and more congested roads and streets, reduced access to jobs and services, public transport cuts and fare rises (in a cost of living crisis), and poorer health outcomes from more accidents, worse air quality and less exercise from active travel. More

11

positive implications, like the fewer car miles and stresses on transport networks from reduced commuting, need managing too with their financial challenge for public transport.

How TfWM is addressing these implications?

So, with no default return to ‘normal’ in post pandemic, and some very challenging implications of likely scenarios, TfWM is actively working with partners to realise the more positive of these.

And our work is directed by the West Midlands Local Transport Plan (LTP), developed by TfWM and partner local authorities as our long term vision and strategy. Its ‘Big Moves’ are a plan to address all the negative implications discussed in a ‘triple access system’ that seeks to improve accessibility with the best mix of travel with digital connectivity and intelligent land use. Meanwhile, recent funding wins from government provide the means: £17m from ‘Active Travel 3’ for cycling and walking; £31m of Zero Emission Bus Regional Area funds for one of the largest hydrogen bus projects globally (Birmingham already has hydrogen buses on the road); £90m for our Bus Services Improvement Plan of better simpler fares (building on work with operators to keep these low for younger people), and better buses (integrated network improvements, and more Safer Travel uniformed officers);

and >£1bn from the City Region Sustainable Transport Settlement for a five year programme of active travel and public transport improvements, connecting key centres but also benefitting local neighbourhoods and communities across our area;

And these will build on many other recent achievements including: a programme (the largest nationally) of transport innovation, a Future Transport Zone with new kinds of demand responsive bus services (West Midlands On Demand), Mobility Credits trials to promote sustainable travel choices, work to decarbonise road transport via electrification and access to charging, and exploring the future of Connected and Autonomous Vehicles;

a Regional Transport Coordination Centre (RTCC) for incident response and coordinating public works, ready for the 2022 Commonwealth Games (itself a test and a springboard for sustainable transport plans); an expanded Swift payment platform the biggest outside London with best value capping of bus and Metro fares;

essential bus service and Ring and Ride support as public transport recovers, and concessionary fares and the Coventry All Electric Bus City; expansion of our Metro and our new Sprint Bus Rapid Transit network;

investment in a statutory 605km Key Route Network (KRN) with local authorities; rebuilt rail stations at Perry Barr and University and building three new stations in Birmingham, and two in the Black Country unlocking brownfield land for redevelopment in the Walsall Wolverhampton Inclusive Growth Corridor;

the West Midlands Cycle Hire scheme (90,000 miles covered in year one), Emergency Active Travel Fund schemes in response to Covid, and work on our 500 mile active travel Starley Network.

Covid has certainly changed local travel, and ‘pre Covid’ will not return. Not all the implications are yet clear, and not all are positive, but by the range of activity above (only a selection) TfWM and partners are showing how uncertainty can be managed through interventions that will contribute to sustaining positive change in any scenario towards a better connected HS2 ready region, meeting the needs and aspirations of our communities, and LTP and WMCA goals of levelling up, and sustainable and inclusive economic growth

12

Air Travel

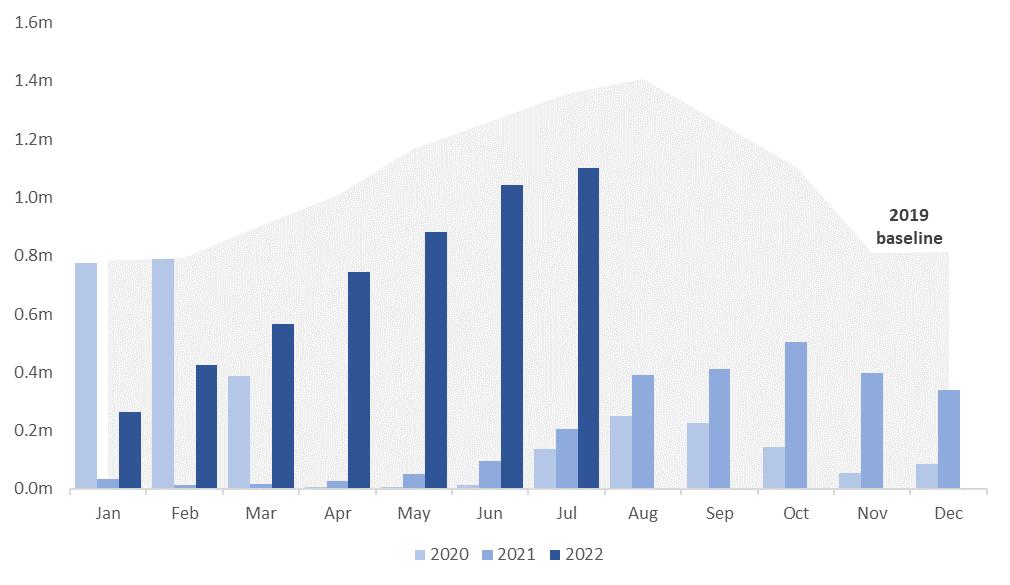

Air travel was very heavily impacted by the pandemic, with passenger numbers through Birmingham airport dropping to virtually zero in the second quarter of 2020. A proper recovery did not get underway until the second half of 2021, although passenger numbers were still only a third of that for the corresponding period in 2019. 2022 has seen a continued, albeit incomplete, recovery with passenger numbers just over 80% of their pre pandemic level in June and July. The number of passengers through the airport in 2019 was 12.7m. There have been 5m passengers through the first seven months of 2022 according to data from the UK Civil Aviation Authority.

Birmingham airport passenger numbers by month

13

Source:UKCivilAviationAuthority,UKairportdatabymonth.

Theshadedarearepresentsthe2019baselineforpassengernumbersbymonth.

Nick Barton, Chief Executive, Birmingham Airport

Potential. That word sums up Birmingham, the wider West Midlands region and its airport.

The gleaming moments of the Commonwealth Games, beamed around the globe, cemented this in people’s minds. That Birmingham is the UK’s second city. A city in a region on the rise. An economic powerhouse on a clear curve of growth turbo boosted by improved rail connectivity from HS2. A tourist destination. A globally significant city worth travelling to, moving to, visiting. One whose best days are yet to come.

Birmingham Airport (BHX) exists not just for the benefit of BHX but to facilitate and support the strong trajectory of growth that Birmingham and the West Midlands are on. We are uniquely placed to do this. Using our existing runway capacity, we’re on course to serve +18m customers a year by 2033. That’s 50% more than the 12m we served in 2019 (before Covid effectively closed down aviation and reduced our customer volumes and revenue by more than 90%, and our workforce by 43%).

This growth in customer journeys in and out of BHX can be achieved without the need for more runways but, rather, by utilising the existing runway capacity we already have. Our terminal building will need modifying and extending. But the runway will be the same.

In 2019, BHX was estimated to add £1.5bn a year to the West Midlands economy and support a total of 30,900 jobs. By 2033, this is expected to rise to £2.1bn and 34,400 jobs. If links to manufacturing are considered, the number of jobs supported by BHX could be as high as 38,600 by 2033.

Milestones along the way include the construction of our new security hall complete with state of the art scanning machines enabling customers to leave liquids and large electrical items in their bags. This will enable BHX to process more customers more quickly at peak times.

Another enabler is the construction by HS2, starting in 2026, of an automated air rail shuttle train linking the new Interchange station, on the new railway, directly into the BHX terminal. BHX will be 37 minutes from central London (Euston) and 31 minutes from West London (Old Oak Common). HS2 makes BHX a feasible ‘local’ option for millions more people in the South.

In the coming decades the major potential blocker for aviation is carbon emissions. We have this existential threat clearly in focus. By 2033, we aim to have become a net zero carbon airport by implementing genuine low carbon operations and minimal use of offsets. This is aligned with the Government’s Jet Zero strategy, which targets zero carbon airport operation by 2040. A scary target but one we cannot duck. The consequences of climate change spiralling are unthinkable. We know how to achieve the first two thirds of this. But the final third of our journey to net zero is very challenging. We will need help from innovative minds across this region.

In the near term, there’s a cost of living crisis to contend with. If you were to look around the BHX terminal right now and use it as a measure for Britain’s economic health, you’d be forgiven for thinking all was well. People have saved up. Many have not been away for three years. The buzz of getaway joy in the terminal perhaps belies the economic reality.

Since Government scrapped Covid travel restrictions in March, demand for air travel has bounced back strongly. In June we served more than 1m customers. The first +1m month since October 2019. Bookings remain strong well into the autumn. We’re currently at 80% to 85% of pre pandemic volumes.

We’re seeing strong demand for low cost travel. In June 2022, Jet2, Aer Lingus, Air France, TUI, Turkish Airlines, Vueling Airlines and Wizz Air all flew more people than in June 2019. Business travel is also bouncing back. Demand for long haul destinations, notably to India and North America, is building, too. This will be reflected in the routes we serve in future.

14

In March this year, we faced a struggle to re hire the staff needed to serve the many customers now wanting to fly. By the start of the Commonwealth Games in late July, we had recruited all the operational staff we needed. Meanwhile our industry partners still have berths to fill.

I’ll dare to say it: We’re getting back to normal again. While we bear the scars of two torrid Covid years, we’re determined to seize this bounce back moment for our region as together we fulfil our potential.

15

City centre

The pandemic had a disproportionately negative effect on city and town centres with many businesses and services located in these locations suffering major disruption. New patterns of mobility, work and tourism have become embedded as remote and hybrid working has become the norm in some sectors and professions. Google Community Mobility Reports show commuting for work was still down by 30 40% on weekdays in Birmingham as of August/September this year. Travel for retail and recreation was also still down but by less than half that amount.7

This profound shift could change the role and function of the city centre. Potential scenarios include an eventual return to work, a shift towards more culture, leisure and retail, but also, and worryingly, general decline. The latter scenario would have negative impacts on the built environment, high street and local businesses, posing a serious challenge to the levelling up aim of improving pride in place.8

Despite these trends, Deloitte’s annual Crane Survey demonstrated some recovery in city centre construction activity in 2021. Whilst the number of schemes under construction was equal to 2020 at 34, the number of new starts almost doubled from 10 to 18. New starts included 14 residential, two offices, one hotel and one student accommodation scheme.9

16

7 Google, COVID 19 Community Mobility Report for 18 September 2022 8 WMREDI, Megatrends and the West Midlands 2021 9 Deloitte, Birmingham Crane Survey 2022 [accessed August 2022]

Johannes Read, Policy and Data Analyst, City REDI, University of Birmingham.

One year on from the publication of the Future Business District study report, Johannes Read examines the data, trends, and policies to compare how Birmingham city centre is shaping up in 2022.

If only we could be like Doctor Who. To travel into the future to see how city centres could change in the face of the pandemic. Businesses would be able to eliminate uncertainty, workers could plan to meet up colleagues, transport planners would know just where, when, and how people would be moving around the urban area. Looking into the future is something many of us wished we could do to cope with the uncertainty at the onset of the pandemic. Looking into the future of city centres, whilst recognising the limits of us non Time Lords, is part of the approach of the Future Business District study, undertaken by City REDI/WMREDI at the University of Birmingham, the Office for Data Analytics at West Midlands Combined Authority, and Colmore Business District.

The Future Business District project had two overarching medium and longer term aims:

2.Howcanweensuretheyremainsuccessfulasplacestoattractbusinessesandpeopleand

From Ghost Town to City Playground

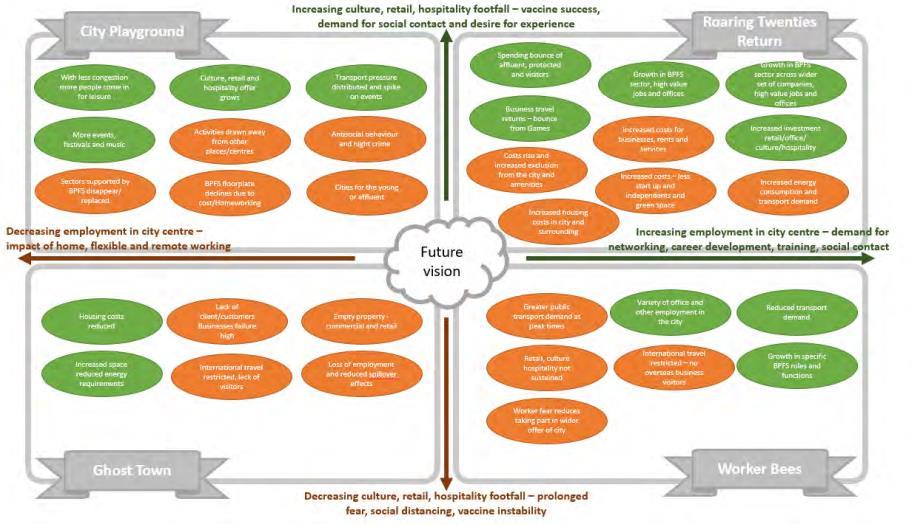

Amidst the uncertainty of the pandemic, the Future Business District study built on work on ten Megatrends in the West Midlands to form a range of potential outcomes for future city centres. The scenario mapping is outlined in Error! Reference source not found. with the horizontal and vertical axes based on two main trends: an increase/decrease in cultural, leisure and hospitality; and an increase/decrease in employment in city centres. Analysing the data can identify whereabouts on this map Birmingham currently sits.

Figure 1: Scenario mapping from Future Business District study

Source:Green,A.,Riley,R.,Smith,A.,Brittain,B.,Read,H.(2021)TheFutureBusinessDistrict. CityREDI,UniversityofBirmingham.Availableat<https://futurebusinessdistrict.co.uk/wp content/uploads/2021/10/20211011FutureBusinessDistrictreportaccessiblefinalversion.pdf> (Accessed20.07.2022).

17

1.WhatisthelikelylongtermimpactoftheCovid19pandemiconcitycentrebusinessdistricts?

contributetovibrantcitycentres?

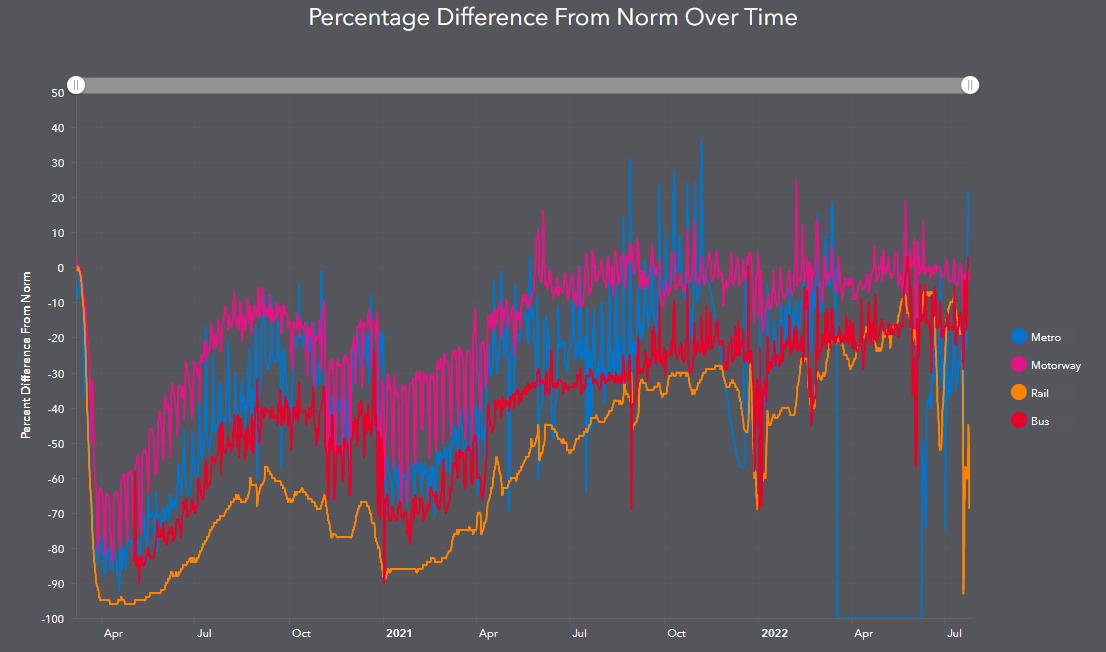

During the trough of the lockdowns, Birmingham was firmly in the Ghost Town quadrant. Footfall had plummeted and very few people were coming into the centre to work. But now, two and a half years from the onset of the pandemic, there is a sign of change. Data from Transport for West Midlands in Figure 1 shows that, in July 2022, metro, motorway, rail, and bus journeys are all converging towards their pre pandemic peaks. Although Birmingham has not moved totally to the pre pandemic levels, the trends shows that travel around Birmingham will move the city out of the Ghost Town and towards a City Playground scenario as the recovery continues.

Figure 1: Multi modal comparison

The Future Business District study showed that people want to travel with purpose, to meet, collaborate, socialise and enjoy leisure time. Whilst it is still too early for the data to show exactly where Birmingham is right now, data from the West Midlands Data Lab shows that prior to 2020 employment in the arts, entertainment, and recreation sectors in Birmingham grew compared to stagnant job growth overall. Nationwide, the Local Data Company found the proportion of leisure units in city centres had also grown from 2016 2021. Despite the backdrop of a sharp economic downturn from Covid, the trend data shows that Birmingham is moving in the direction of a City Playground scenario with increasing culture, leisure, and hospitality offerings in the city.

Shaping a Future City Centre

Places and economies evolve and change over time. The emerging trends in Birmingham city centre show there is some level of growth in leisure and cultural amidst in the backdrop of public transport converging to just below pre pandemic levels. As with all scenarios outlined in

Figure 1 1, this offers some positive outcomes, as well as negatives.

One of those changes is that hybrid working is here to stay. For many office workers, potentially long commutes were inefficient and unfavourable. Especially when compared to the quality of life benefits that flexible working can bring. However, on the downside, there is a threat that cities can become just places for the young and affluent professionals.

It is important to recognise that, if places and economies change over time then, by the same token, they will continue to do so in the future. Economies and places can be shaped by policy

18

Source:TfWM,HubforDataInsightintheWestMidlands.[URLhttps://community

engagementtfwm.hub.arcgis.com/pages/covid19(Accessed20.07.22)].

and by people. These are the trends outlined in the research, but is this where Birmingham wants to be? And who decides? People who live and work in the city should be involved deeply in shaping the vision of the future of Birmingham.

Colmore BID’s response to the study, titled The Space Between, outlines six overarching pillars which encompass these big questions. The report goes further and 30 practical steps to achieve these goals (Figure 2). These have been the focus of activity for Colmore BID and jointly with other city centre BIDs over the past year. Particular progress is being made on agreeing the scope of a new role to ‘curate’ city centre spaces and foster greater collaboration between the Council and other agencies active in the city centre. Having analysed the data one year on, we have identified a City Playground emerging. By tracking the emerging trends in Birmingham, through data sources collated by the West Midlands Data Lab, in conjunction with the actions identified by Colmore BID, is it possible to build on the legacy of the Commonwealth Games, cultural festivals and demand of collaborating and coming together to ensure that the city ecosystem enables the future Birmingham to flourish too.

Figure 2: Six pillars of The Future Business District

19

Source:ColmoreBID(2021).TheSpaceBetween.ColmoreBusinessDistrict10 10 Available at: https://futurebusinessdistrict.co.uk/wp content/uploads/2021/10/Future Business District October 2021.pdf

Office Space

Changes in working practices have had major implications for the office market. In May, the ONS reported that 24% of workers were hybrid working and 14% were working exclusively from home. Very few had intentions of returning to the office full time.11 Whilst some employers are pushing for a more regular return to the office, this is being met with resistance from staff now accustomed to a different working pattern and more favourable work life balance.12 A survey by infinitSpace found that two fifths of UK business leaders were seeking new workspace to meet changing needs and that flexible working and downsizing were on the minds of around half.13

Deloitte’s Crane Survey 2022 for Birmingham shows that the total volume of office space under construction continues to fall from the high in 2016 and was approximately 25% below the ten year average of approximately 800,000 sqft in 2021. However, strong demand for office developments just outside of the city centre survey area was noted as sites in the city centre become increasingly rare.14

Birmingham Office Market Forum statistics show office space take up was 26% higher in 2021 than the previous year but was still short of its pre pandemic level. Take up for the first half of 2022 was 292,860 sqft, 16% up on the same period last year but still 27% lower than 2020 which was bolstered by a strong first quarter.15

Birmingham city centre office take up

Year Total Sqft YoY No. Deals YoY 2019 780,095

2020 520,810 33%

2021 656,735 +26%

Source:BirminghamOfficeMarketForum,Officetakeup

Major moves over the past year have seen law firm Shoosmiths, workspace provider X+Why, law firm Browne Jacobson and financial services firm RSM all take space at the recently completed landmark 103 Colmore Row. In March, Grade A office development One Centenary Way topped out and will see built environment consultancy Arup relocate its Midlands office and 1,000 staff to the building in 2023. Meanwhile, professional services firm Atkins moved its Birmingham office to the nearby Two Chamberlain Square development also at the Paradise development.

Office Market Forum,

20

116

50 66

94 +44

11 ONS, 2022, Is hybrid working here to stay? 12 FT.com article, available here 13 InfinitSpace blog, Bichl, 2022, How are businesses managing the big return? Our research reveals all 14 Deloitte, Birmingham Crane Survey 2022 [accessed August 2022] 15 Birmingham

Office take up [accessed August 2022]

Standing outside the entrance of One Centenary Way, Arup Birmingham Office Leader Mark Jones has just signed the lease for the new Arup Birmingham office.

‘Wehavecomealongwayinthiscityregion.Ournewinvestmentbuildsuponover50yearsof Arupactivelydesigning,advisinganddeliveringintheMidlandsregion,includingmanyofthe majorregenerationdevelopmentsinBirminghamandsupportingmajornationalclientslikeHS2, NationalHighwaysandNetworkRail.’

‘Our business is all about delivering excellence in the built environment and, whilst we collaboratewith17,000colleaguesglobally,wehavearealregionalandUKnationalfocusfrom thisoffice.Ournewworkspacehasbeendesignedbyusandforusandwillbethethirdlargest Arupofficeglobally digitallysmartanddesignedtosupportanArupglobalambitiontoreach netzerocarboninoperationsby2030.’

‘We play an influential part in the regenerative opportunities in the city region. Having successfullycollaboratedwithArgentontheBrindleyPlacedevelopment,wenowremainvery activesupportingMEPCintheParadiseDevelopment.Wehavegrownasabusinesstonearly 900peopleandthisinvestmentmakesusmoreconnected toclientsandcollaborators and showstheclearwillingofAruptoinvestinthefutureofBirmingham.’

‘Enhancingourabilitytoattract,retainandthendevelopthebesttalentisamajorfactor.This September,werecruited42newgraduatesandapprentices thevastmajorityofwhomcome via our strong relationships with regional universities and colleges. This helps underpin our diversity.Itisoneofthebestpartsofbeingaleader beingabletowelcomenew,talented colleaguesandhelpthemtofulfiltheirpotential.’

‘OneoftheemergingArupleadersinthecityregenerationspaceisJamesWatts.Jameshasled ourrelationshipswithmanyoftheleadingcitydevelopersandhasbuiltareputationforbeing abletounlockcityinfrastructure.’

James summarises: ‘Bycommittingtoadeepunderstandingofwhatthecityneedsandby collaboratingwithBirminghamCityCouncil,FederatedHermes,GBSLEPandwithMEPC we havebeenabletoshowthebestwaytounlockvaluebycapturingoftendisparatedataand collatingthiswithinasinglerepository.Thishasenabledustoworkwithdeveloperstoidentify the unknowns, and therefore key risks, in a way that the team can systematically address; thereby improving our knowledge and understanding of the site constraints that in turn increasescertaintyandreducesrisk.’

We can see many more of these complex types of city development opportunities such as Smithfield, Digbeth and East Birmingham. Many of which are already emerging, and we look forward to exporting the regenerative effect of our creative design thinking, particularly as we look to re purposing existing city assets helping the city region move towards a more positive net zero carbon future.

James writes: ‘AsArupProjectDirectorofourdesignoftheBirminghamCommonwealthGames AlexanderStadium,IamverypleasedtohaveusedourcreativityalongsidethewiderPerryBarr

21

Mark Jones, Birmingham Office Leader, Arup, James Watts, Associate Director, Arup and Alex Phillips, Property Development Director, Arup

regeneration opportunity via our collaboration with Birmingham City Council. Working with ArupdevelopmentexpertAlexPhillips,wehavehelpedputfullconfidenceinthedesignand deliveryofthePerryBarrResidentialScheme.’

Arup Property Development Director, Alex Phillips writes: ’Ourclient,BirminghamCityCouncil, hasputinplaceanambitiousregenerationprogrammeforPerryBarrsupportedbyover£700m of public sector investment in transport upgrades, new homes, and community facilities. By bringingtobearourexperienceofcomplexresidentialprojectsandplaceshaping,wehave supportedtheCouncilanditspartnerstorepositionthePerryBarrResidentialSchemewitha developmentstrategythataimstoestablishagenuinelymixednewcommunity,whilebalancing commercialviabilityandmaintainingfullfocusontheCouncil’scoreplaceshapingprinciples.’

The initial phases will deliver nearly 1,000 new homes for sale and rent across a variety of tenures and kickstart the wider Perry Barr regeneration. By setting a new benchmark for quality,andasharpfocusondeliveryofhighqualitypublicrealm,PerryBarrisanexemplarfor strident, local authorityled development that delivers longterm economic and social value. Thisfutureambitionhasbeencapturedinanewlyadoptedmasterplanwhichwascocreated byArupandtheCouncil,"PerryBarr2040:AVisionforLegacy". Themasterplanhasreignited and refocussed the area’s commercial and leisure offer and has identified a series of much needed new residential development opportunities alongside new schools and community facilities.’

Alex adds: ‘Thekeytocreatingandunlockingvaluehasbeenthecollaborationbetweenthe Council and Arup to cocreate a robust, deliverable placebased vision, supported by a thoughtful,pragmatic,andbalancedapproachtoriskandcommercialreturns.Weareexcitedto seePerryBarrcontinuetobuilduponitsenergy,promise,andpossibility.’

Mark adds: ‘Wecanallseethetransformationaleffectoftherecentinvestmentinthecity.Our investmentmakesthisagloballysignificanthubforArup.Wehopethisactsasafurthersignal of our confidence in the city region not only for an outstanding office but also for the confidence thatwehaveindevelopingpeople,creatingnewjobsandskillsandbeingatthe forefront ofthe BuiltEnvironment for thenext 25yearhorizonofcitygrowthandwiderUK infrastructureinvestment.TheregionreferstotheGoldenDecadepostGamesandIthinkthat istherightambition butweseeitgoingwaybeyondthat.’

‘Movingintoanewexemplarofficethatwehavedesigned,havingbeensoextensivelyinvolved withParadiseformorethantenyearsnow,isaveryexcitingprospectformanyofourstaff.It alsopresentsuswithauniqueopportunitytoharnesstheenthusiasmofourcolleagues,tobuild newrelationshipswiththelocalcommunityandmakeameaningfulcontributiontoBirmingham inthewidestpossiblesense.’

22

Dr. James Davies, Research Fellow, City REDI, University of Birmingham.

The announcement in August 2022 that the BBC16 is intending to relocate the headquarters of BBC Midlands to a new home at the old Typhoo Tea factory, located in the Digbeth Creative Quarter at the heart of Birmingham, offers a great opportunity to consider the key role that creative industries can play in post pandemic recovery, the variety of assets and strengths Digbeth possesses, and the implications and applications of creative growth beyond the immediacy of the sector itself. In the ten years prior to the pandemic, creative industries in the UK grew in GVA by almost double the rate of the UK average across the economy17. In 2016, the creative industries were worth nearly £92bn to the UK economy. Within the creative economy, only ‘IT, software and games’ contributed more to that growth than ‘Film and Television’. Across the WMCA region, creative industries were estimated to have contributed more than £4bn in GVA in 201918. The colossal impact of the pandemic over the past two years, both on the region and on the sector has been written about extensively, both on these pages and elsewhere, and so instead I want to focus in this piece on the significance of the BBC Midlands relocation as we look ahead to the role creative industries can play in post pandemic economic recovery.

Spurred primarily by the phenomenal success of ‘Peaky Blinders’, the West Midlands, and Digbeth in particular, is becoming known as a home of a variety of high end scripted and unscripted television. A well established creative and cultural cluster, with historic specialisms including arts, music and design, the district is now home to a number of production hubs and spaces. Key among these include the Custard Factory, a 60,000sqm creative and digital workspace, and Fazeley Studios, a creative workspace and event space. Even prior to the BBC move, film and TV was the second largest creative subsector in the Digbeth cluster19. Though it will be the largest, the BBC Midlands headquarters will not be the only BBC presence in the city, with Birmingham home to BBC3, the BBC Academy, and plans to relocate the Asian Network and Newsbeat teams to the city, as part of its five year Across the UK plan20

Filming of hit BBC show ‘Masterchef’21 is being relocated to Digbeth too. The development of a 50,000 sqft, £18 million Creative Content Hub22, which includes £3 million worth of investment from the greater Birmingham and Solihull local enterprise partnership (GBSLEP) is underway in the Creative Quarter, promising to be a content hub for independent television productions, as well as being the headquarters of Create Central, an industry led, creative industries focused skills and training initiative, including £150 million worth of investment from the WMCA, running boot camps and programmes to boost content production skills across the West Midlands. Create Central, was also highlighted in the BFI Skills Review in 202223 as an exemplar of good practice in creative industries focused skills and training provision.

The growth of Digbeth’s Creative Quarter, therefore, looks only set to continue as we look ahead to post pandemic recovery. The relocation of BBC Midlands shows a real vote of confidence in the growth and development of the cluster, and in conjunction with the efforts of the Creative Content Hub, and Create Central the future of both public service broadcaster (PSB) and independent television production appear to be very bright indeed. creative goods and services also possess high, an instant, in the case of digital content, export potential. Almost £38 billion worth of services were exported by creative industries in the UK in 2019, and over 20 billion in goods, service exports growing by more than 10%, and goods by more than 1/324. but there are applications and potential beyond just the creative industries themselves. A

23

16 BBC news article, available here 17 WMCA, 2019, West Midlands Local Industrial Strategy 18 WMCA, 2019, Creative Industries: Full evidence slides 19 See https://beta.wmca.org.uk/media/o5mfd0dj/economic report web.pdf 20 BBC, 2021, The BBC across the UK, 2022 2027 21 CreateCentral news article, available here 22 GBSLEP news article, available here 23 BFI, Skills Review 2022 24 Creative Industries Policy & Evidence Centre, Led by Nesta, The Creative Industries in the UK’s export strategy

combination of stuttering lockdown schedules and demand for content across Streaming Video on Demand (SvoD) services such as Netflix and Amazon Prime have precipitated an unprecedented demand for content, and provided the demand for personnel can be met, there is a real ‘post Covid boom’ in television production25

The previous West Midlands Local Industrial Strategy highlighted the cross sectoral collaborative potential of creative services, for example the application of AR and VR in aerospace automotive and healthcare sectors. Levelling up white paper has already demonstrated a prioritisation of regional, place based policy making, and as we await the publication of the UK government's sector vision later in 2022, it is hoped priorities will reflect the huge collaborative potential creative talent has outside of its own industries. as the digital revolution continues to envelop all aspects of work and life, and the skills and competencies for all forms of digital production (film, television, video games, AR/VR) share more and more commonalities, Digbeth is well placed to return to, and exceed, its pre pandemic growth.

24

25 ScreenSkills, 2022,

High end Television in the UK: 2021/22 workforce research

John Webber, Head of Business Rates, Colliers

As the region emerges from the economic shock of Covid it would be nice to think that the burden of business rates would be one problem that would be removed from the list of uncertainties facing companies across Greater Birmingham.

The annual amount collected across the city pre Covid was £500 million. With various Covid reliefs granted over the last couple of years that amount was reduced, but £500 million is unsustainable, and with a commitment from our new Prime Minister and Chancellor, there must not be a return to that figure.

The debate over tax cuts was a major battleground for the PM contenders but for the retail and hospitality sector in the city, paying the correct business rates bills next year following the 2023 Rating Revaluation is not some state handout but a basic entitlement that should be passed on without debate.

The sector will see large reductions in rateable value. In some locations retail rental levels have fallen 50 or 70 % since the 2015 valuation date for the current rating list and this should hopefully mean rates bills will come down dramatically for many in the sector. This drop will make a massive difference to a business’s running costs.

However, this will be meaninglessif the government does not allow business rates reductions to be implemented immediately rather than spreading them over the years of the list in a transitional arrangement, as it did in the last list of 2017. Such phasing will deliver a severe blow to any retail recovery, plans to level up or breathe life back into our communities.

Our new Prime Minister Liz Truss has a great opportunity to be the first PM to turn the tide of decline in our town centres. What a great legacy that would be and requires little action. It is not even controversial business paying the correct tax who would think it!

The worry is that in the political turmoil these important issues are lost in the noise.

As well as believing the Government has a moral and economic responsibility to completely remove downward transition in Revaluation 2023, we also believe it should restrict the increases for those businesses that have seen significant growth in values since the last list, particularly those in the industrial and logistics sector.

Given the pressure on business from spiralling energy costs, wage growth as well as other tax increases announced by the Conservative Government, we believe no business should have to pay more than a 15% rise including inflation. For smaller and medium sized businesses, these increases should be limited to no more than 5/10% including inflation.

And indeed, the impact of the worst inflation figures for 40 years cannot be ignored. The levels of any proposed reductions or increases will be heavily influenced by potentially double digit inflation.

As an example, if the 2023 downward TR scheme mirrors the 2017 one when bills in Year One (2017/18) for large properties reduced by only 4.1% less inflation, then rate bills in 2023/24 would actually go up by at least 6%. Equally, increases for large properties compatible to 2017/18 would go up by 42% plus inflation in Year One post Revaluation thus giving an increase well more than 50%.

A rating system which is linked closely to inflation increases could very quickly reach even more ridiculous levels than it currently is. Again, this cannot be right or make economic sense if we are looking to stimulate growth.

As well as the above our manifesto for the government remains

25

• Reduce the multiplier to £0.30p for all properties. Business rates at £0.51p are unsustainable

• Reduce the Rateable Values of all premises affected by Covid 19

• Reduce the Rateable Values of all properties affected by tram works in the City Centre ASAP

• Introduce an online / delivery levy to pay for the shortfall in any tax take.

We also believe the Birmingham City Council also has a responsibility to help businesses by putting pressure on HMRC that will send the right signals to encourage people to locate in the city, stay in the city and grow in the city.

In a post European Union world, the Government can no longer hide behind state aid rules they have the control to carry out whatever measures are needed to fire up the engines of the Midlands economic machine. We really hope they listen and do so.

26

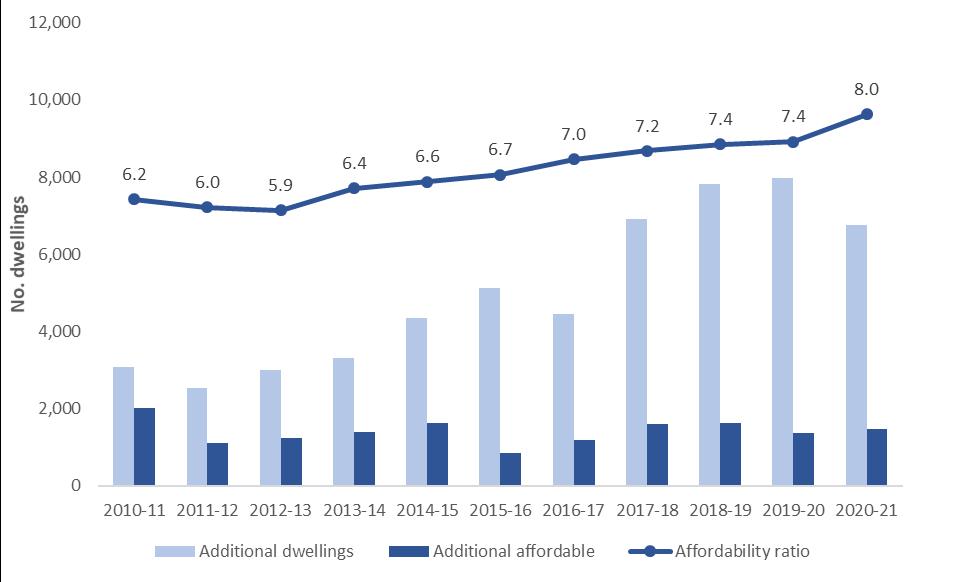

New Homes

The affordability of housing continues to worsen whilst the delivery of new homes has slowed over the past year.

The number of new homes delivered in the city region declined in 2020/21 to 6,748 from a high of 7,974 the year before, although the rate of delivery has been steadily increasing over past decade. The delivery of affordable homes increased to 1,469 up from 1,368 the year before. However, the percentage of new homes classed as affordable has averaged just 21% over the past six years and has declined over the past decade.

The affordability (house price to earnings) ratio continues to worsen and reached a multiple of 8.0 in 2021. Affordability varies across the region with Bromsgrove, Solihull and Redditch having multiples above 9.0 whilst Birmingham is at 7.1 and Cannock Chase the most affordable at 6.4. One in three new affordable homes were delivered in Birmingham last year, although the city accounts for over 50% of the total dwelling stock in the city region. Solihull delivered 21% of new affordable homes but accounts for just 11% of the total dwelling stock.

Housing delivery and affordability (GBSLEP)

Barriers to housing, which includes unaffordability, is one of the main drivers of deprivation across the city region (see Chapter 3). The Levelling Up White Paper sets out ambitions and aims to improve homeownership and improve the standard of housing significantly by 2030.

27

Source:MHCLG,Livetablesondwellingstock;ONS,Housepricetoresidencebasedearnings ratio.

Affordabilityratioisbasedonmedianhousepricetomediangrossannualresidencebased earnings.

Glenn Harris, Chief Executive Officer, Midland Heart

As I write this, we stand on the edge of having a new Prime Minister, a new government, and very likely a new Secretary of State for Levelling Up, Housing and Communities. But what can we do to level up Birmingham and the wider West Midlands, and address the housing crisis the city, the region, and the country faces?

Housing in the city and the wider region presents a particular challenge. According to official figures, over 12,000 households live in temporary accommodation in the city, and there are over 14,000 households on Birmingham City Council’s housing waiting list.

Affordability doesn’t fare much better, according to the Halifax building society you need an income at least seven times the local median wage to buy an average priced house in the city.

Private renting is no more affordable, according to the most recent ONS data, the median monthly private rent in the city is £695, this outstrips local housing allowance for all but 4+ bedroomed homes, meaning that many private renters will be paying towards rent from their other income. Birmingham has also become the epicentre of poor quality ‘exempt accommodation’ where unscrupulous landlords have been taking advantage of housing benefit rules to claim enhanced rent levels designed to fund support for vulnerable people, but not delivering that support, and worse, providing them extremely substandard accommodation. This cannot go on. On top of all that, we know that twenty per cent of all UK carbon emissions come from the ways we power and heart our homes, so we need to address that too if we are to reach the government target of net zero carbon by 2050.

We do have solutions though. But we need some help from national and local government to make them possible. As one of the main developers of social housing in the region, these are our asks that could unleash our ability to develop new, and retrofit existing, homes:

1. There is a challenge with the proportion of land set aside for residential buildings compared to businesses in the city curtilage, in our view this needs to be reappraised with greater land allocated for residential development

2. The main issue that prevents us from retrofitting our homes to make them greener is planning permission we’d like to see greater resources for local planning departments and, as already happens in some areas, a default presumption of approval for retrofit

3. There are more than enough flats in the city, whilst we need accommodation for single people and couples, they are not the answer to the housing crisis we need a better mix of new homes being developed

4. One of the solutions proposed is the conversion of offices to residential units safety and building regulations mean this is unlikely to be viable and we need better ways of raising the number of homes in the city

5. There is demand for new homes and no shortage of social housing providers with grant programmes to deliver. Like Midland Heart, most have a broad geography and will develop where it’s easier to do business and more welcoming local authorities must work with us to set realistic standards and build the homes we need

6. Low carbon homes are now a given in cities, but local authorities need to be careful that pursuing excessive standards doesn’t drive developers away, to build in other areas.

On this last point, I’m extremely proud to say Midland Heart have recently completed building the first homes in the country that meet the Future Homes Standards, some three years ahead of the government target. This means we’ve reduced the carbon use in building and living these homes by some 80 per cent. The three blocks of homes on the site, on Eco Drive, Handsworth, use different combinations of technology to heat and ventilate them, this means we can gauge what works well and what doesn’t. Because these homes use this new, innovative technology, we’ve partnered with Birmingham City University (BCU) to provide training and online resources for tenants, so they can maximise the benefits of their homes. BCU are also supporting the

28

project by researching not only the carbon and cash savings these homes make, but also the experiences of the families living in them. This research will be shared with other housing providers across the country, so that others can learn from Birmingham’s innovative new homes.

Midland Heart has also kept a sharp focus on making our existing homes as energy efficient as possible with well advanced ‘retrofit’ programme to fit new boilers, insulation, and heating. Following a successful pilot scheme in Coventry, we are partnering with British Gas to retrofit more homes to improve all their EPC ratings to at least a ‘C’ by 2030. Although 2050 may seem a long time in the future, we are working together with the region’s businesses to adapt existing homes and develop the homes of the future.

29

Digital Connectivity

Digital connectivity has become even more important during the past few years as services and work have increasingly moved online. It is vital to economic recovery, resilience and growth across all sectors from manufacturing to healthcare and entertainment to public services. Digital is key to realising opportunities in key markets such as future mobility, data driven healthcare and life sciences, creative content and modern services.

The WMCA’s Digital Roadmap for 2021 2026 aims to improve access to digital opportunities, especially for those in poverty, realise the economic potential of digital, increase usage of digital public services and for the region to become the UK’s best connected.26

30

26 WMCA, 2021, West

Midlands Digital Roadmap

Kasam Hussain, Regional Director Midlands, Openreach

Whether it's employees working from home, businesses interacting with customers or students learning online connecting to the internet is more important than ever.

Openreach the UK’s largest phone and broadband network is at the heart of this digital transformation, with our new full fibre network already providing consistent, fast, and reliable broadband, which is future proof for decades to come.

More than 700,000 homes and businesses across the West Midlands can already use the new technology an investment in excess of £200 million and we’re constantly announcing new locations, including Castle Bromwich and Selly Oak recently.

Full fibre offers download speeds of 1 Gbps, which is up to 10 times faster than the average home broadband connection. This means faster game downloads, better quality video calls and higher resolution movie streaming.

You can also use multiple devices at once without experiencing slowdown so more people in your household can get online at once. Even if the rest of your family are making video calls, streaming box sets or gaming online, all at the same time you won’t experience stuttering, buffering or dropouts.

Full fibre is also less affected by peak time congestion so you can enjoy your Saturday night blockbuster in 4K without the dreaded buffering screen.

Bringing communities together

Hundreds of service providers (the companies that sell phone and broadband packages) use our superfast and full fibre networks, connecting their customers to the outside world.

Our engineers build, maintain, and manage more than 197 million kilometres of fibre and copper wires. In fact, if you laid it out end to end, the Openreach network could stretch around the world a huge 4,825 times.

We’re proud of our team

Around 3,200 of our people live and work in the West Midlands and most of them are busy working on the broadband network every day, tackling complicated engineering problems, coordinating works with councils, highways agencies, energy suppliers and landowners.

They also install and maintain the complex kit that provides ultrafast and gigabit capable broadband services

And we’re always on the lookout for new talent. Earlier this year, Openreach announced record recruitment with 300 more engineers set to join our ranks across the region.

As part of this recruitment, we’re doing our best to make huge strides in becoming an even more diverse workforce, after last year doubling the number of female engineering recruits in what’s been a historically very male dominated industry.

This progress is thanks partly to employing language experts to transform job adverts and descriptions, making them more gender neutral sometimes through just a simple change to some of the language used or the way we phrase things.

Get onboard if you’re not already

As full fibre becomes available to more communities every week, you’re urged to check if you can sign up to the fastest speeds available to you.

31

A quick check at openreach.com, where you can put your postcode into our fibre checker, will tell you what broadband services are available to your address and how you can go about comparing packages.

32

Broadband

Ofcom’s Connected Nations data shows that broadband performance and coverage vary across Greater Birmingham. Birmingham has relatively low coverage (95.5% of all premises) of superfast broadband (30mbits/second and above) but relatively high levels of coverage for connections capable of 100mbits/second and above (90% of all premises) and full fibre availability (40.6% of all premises). In contrast, Tamworth has very high levels of superfast broadband coverage (99.2% of all premises) but lower levels of ultrafast broadband (86% can achieve 100mbit/second and above) and full fibre availability (5.5%).

Broadband coverage and performance across Greater Birmingham

Performance

Median download speed (Mbit/s)

Coverage (all premises)

SFBB availability (>30Mbit/s)

UFBB availability (>100Mbit/s)

UFBB availability (>300Mbit/s)

Full Fibre availability

Birmingham 78.1 95.5 90.1 89.4 40.6

Bromsgrove 54.8 97.4 75 75 54.9

Cannock Chase 50.3 98.1 49.6 49.6 28.5

East Staffordshire 51 95.3 40.6 36.9 32.8

Lichfield 60.9 96.2 72.7 69.7 30.8 Redditch 69.4 98.5 82.2 82.2 8.1 Solihull 75.7 97.7 89.7 88.9 43.8 Tamworth 73.5 99.2 86 82.8 5.5 Wyre Forest 53.5 97.2 48.8 48.8 3.1

Source:Ofcom,ConnectedNationsdata.

PerformancedataistakenfromConnectedNations2021.Coveragedataistakenfromthe2022 interimupdate.

Redsdenotelowerthanthemedianvalueforthegivenindicatorandgreenshigherthanthe median.

Improving broadband connectivity across the whole city region is imperative to unlock the potential of the digital economy and improve the reachability of digital services.

5G

According to umlaut, the WMCA area ranks highest in terms of 5G coverage when compared against other UK cities and combined authorities. Geographical coverage was 15.4% in 2021. In terms of cities, Birmingham ranks 3rd at 22.9% behind only Manchester (25.8%) and London (25.6%) and has the highest downlink speed and the second highest uplink speed.27

Between 2019 and March 2022 the West Midlands was host to the UK’s first region wide 5G testbed, WM5G, led in collaboration between WMCA and the Department for Digital, Culture, Media and Sport. The trial has set the region up as a leader in 5G and provided case studies on how enhanced connectivity can improve productivity and services across the region, including on the road and Metro systems and in the manufacturing and logistics sectors 28

Sustainability

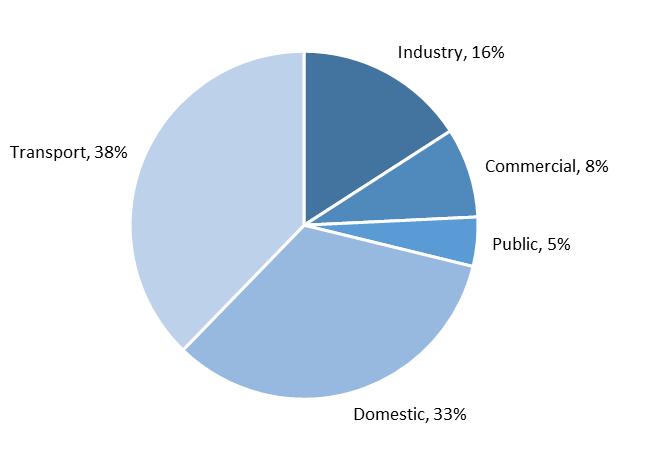

Connectivity and place are hugely important in the effort to decarbonise the UK. The largest share of regional emissions derives from the transport sector, which accounted for 38% of the total in 2020. The domestic sector, which includes residential heating and cooking as a primary driver, accounted for another third. A shift to cleaner and zero carbon forms of transport and heating, along with more energy efficiency buildings, are a necessity for reaching net zero by 2050 as enshrined in UK law.

Umlaut, 2021, 5G coverage

WM5G, Use case / case study and video library

UK

33

27

and performance assessment in

top cities and Combined Authorities 28

Greenhouse gas emissions by sector GBSLEP (2020)

Source:BEIS,UKlocalauthorityandregionalgreenhousegasemissions,20052020.

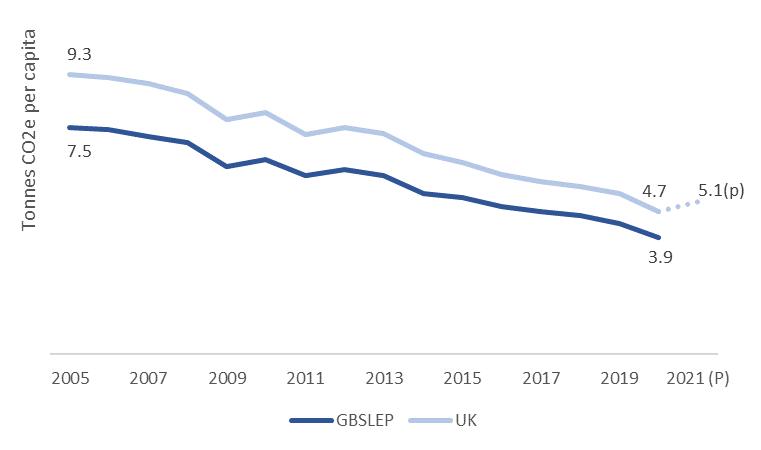

Population adjusted greenhouse gas emissions have been falling since at least 2005 across the city region, reaching 3.9 tonnes of CO2 equivalents (CO2e) per resident in 2020 down from 4.4 tonnes in 2019. Provisional data from the Department of Business, Energy and Industrial Strategy suggests that UK emissions increased in 2021 primarily due to increased road traffic, however, emissions remain lower than in 2019 maintaining the downward trend.29 Greenhouse gas emissions per capita

Source:BEIS,UKlocalauthorityandregionalgreenhousegasemissions,20052020. Basedonterritorialemissionsforcarbondioxide,methaneandnitrousoxide.Excludes emissionsfromlandusechanges,agricultureandwastemanagement.

34

29 Reuters article, available here

Dr. Annum Rafique, Research Fellow, City REDI, University of Birmingham.

The UN Climate Change Conference (COP26) was held in November 2021 in Glasgow, UK. The conference was attended by 120 world leaders and over 40,000 participants. The conference's main goal was to review the implementation of the UN Framework Convention on Climate change, Kyoto Protocol and Paris Agreement and to develop them further.

The conference's outcome was that all the countries needed to reaffirm the Paris Agreement goals and accelerate their climate change actions. Some important pledges were made, such as to stop deforestation by 2030, for India to become net zero by 2070 and for all countries to sell zero emission vehicles globally by 2040 and in leading nations by 2035. In 2019, ahead of COP 25, the UK became the first major economy to pass the law to reach net zero emissions by 2050. Similarly, local authorities have set their own climate goals and targets. The West Midlands Combined Authority (WMCA) pledged to be the home to the green industrial revolution and be carbon neutral by 2041. Birmingham City Council has developed their own goals through Route to Zero (R20) to be net carbon zero by 2030. Actions are already underway to achieve these goals, and decarbonisation is being promoted in the housing, transportation, energy, and waste sector.

Housing: Priority has been given to new builds and retrofitting existing housing stock to address the net zero goals. Around 7,000 social houses would be constructed in Birmingham by Birmingham Municipal Housing Trust (BMHT) under the agreed environmental standards. These houses would be better insulted and use 80% less energy than the traditional houses. Improving housing energy efficiency would have multiple benefits, including a reduction in energy bills, reduction in fuel poverty and improved health, especially in fuel poor and low income homes.

Transport: The Birmingham Transport Plan was introduced in 2021, which sets out Birmingham's vision for a sustainable, green, and inclusive transportation network. Decarbonisation in the transportation sector in Birmingham is prioritised through transitioning to electric vehicles, supporting active travel (walking and cycling), promoting public transportation, and managing cars in the city through parking measures. Birmingham City Council has already purchased 20 new hydrogen double decker buses as part of their Clean Air Hydrogen Bus Pilot. Over £1 billion is being invested in Birmingham's infrastructure to help people use more sustainable forms of transportation such as public transportation, cycling or walking rather than using their private cars. Plans are underway to install 3,600 EV charging points by 2032 to make switching from petrol and diesel fuelled vehicles easier.

Energy and Waste: Reducing emissions through energy use is routed in two steps: reducing energy demand and adopting low carbon technologies to replace fossil fuel powered ones. Emphasis has been placed on generating renewable energy through district heating, solar PV and local community projects. The Waste Strategy highlights the importance of maximising recycling, re using, and minimising waste production. The strategy also shows that Birmingham is currently on its way to becoming a zero waste city by eliminating waste going to landfills by 2040. The city council has committed to a £44.2 million investment to generate energy from waste at the Tyseley Energy Park (TEP) waste management facility.

Birmingham City Council, WMCA, and the UK government have taken steps to tackle the issue of climate change. Still, they all agree that there is much to be done, and everyone needs to make a collective effort to reduce their environmental impact.

35

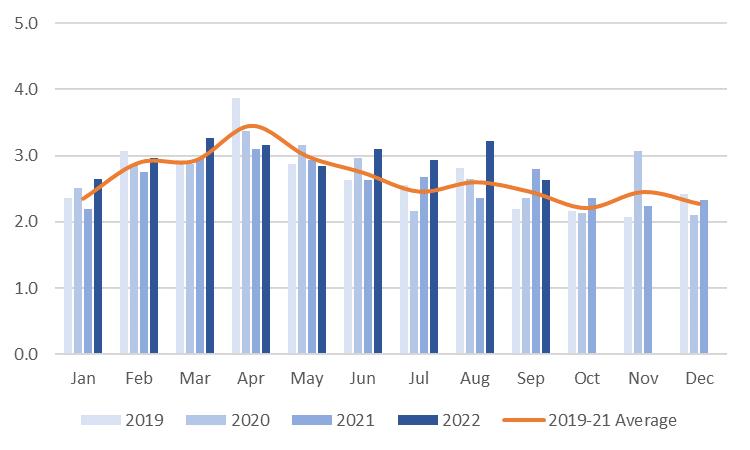

Air pollution

Data from the Department for Environment, Food and Rural Affairs’ Daily Air Quality Index shows that by the end of September 2022, 88% of days had been scored as having a low level pollution and 12% as having a moderate level. This compares unfavourably to prior years. By the same point in 2021, 94% of days scored for low levels of pollution and 6% for moderate. The cause is unclear with various factors potentially contributing to the apparent worsening, including atmospheric conditions and travel patterns. Analysis by the University of Birmingham suggests the Commonwealth Games had a negligible impact. Positively, there has not been a day of high of very high pollution since November 2020.

Average daily air pollution index by month West Midlands Urban Area

Source:Defra,DailyAirQualityIndex(DAQI)regionaldata WestMidlandsUrbanArea. Thedailyindexisdeterminedbythehighestconcentrationoffivepollutants. Adailyscoreof13=low;46=moderate;79=high;10=veryhigh.

Birmingham City Council introduced a Clean Air Zone (CAZ) to the city centre in June 2021. The CAZ appears to be having a positive impact based on a six month interim assessment which found early indications of a reduction in pollution and discouragement of non compliant vehicles from entering the Zone. It does not appear that polluting traffic has been displaced to the ring road. It should be noted that the results are difficult to interpret due to ongoing disruption caused by the pandemic and related restrictions.30

36

30 Birmingham

City Council, 2022, Interim report on the impact of the Clean Air Zone [accessed August 2022]

Councillor Liz Clements, Cabinet Member for Transport, Birmingham City Council

Birmingham City Council’s Transport Plan represents our vision for a zero carbon, resilient transport system that will help to ‘level up’ the city and remove the barriers that sustain inequality.

Our plan is working towards the delivery of safe and attractive environments for active travel, and a high quality, sustainable public transport system fit for all users.