2 minute read

Introduction

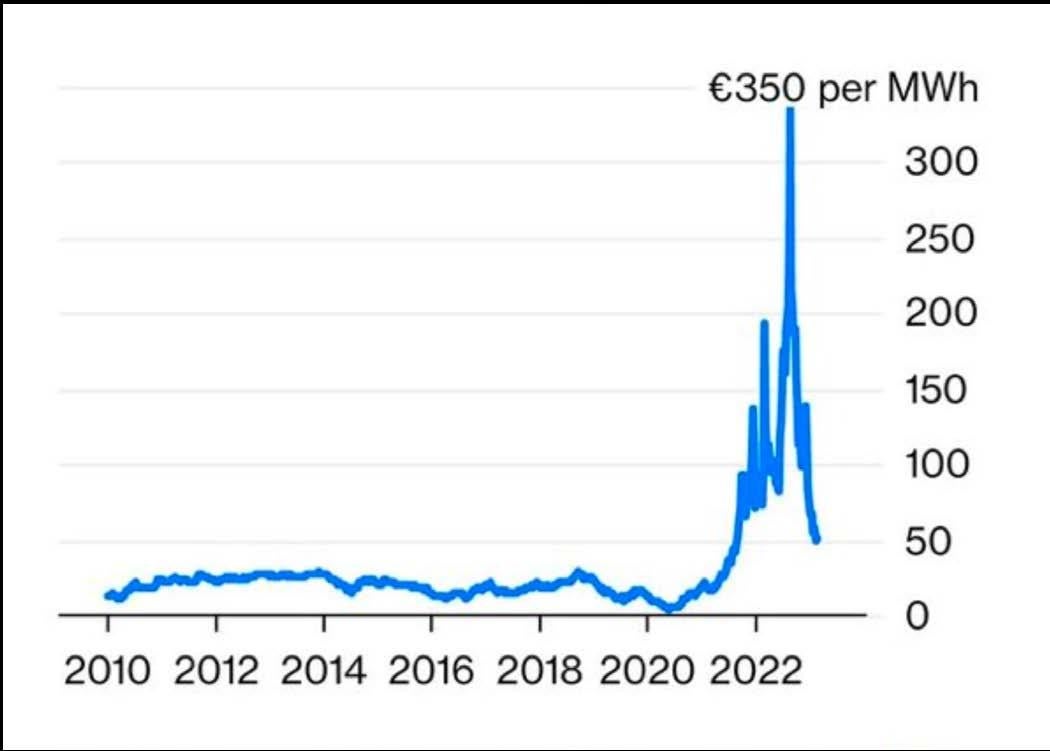

The unprecedented energy crisis the world is facing has been analysed through many different lenses. Geopolitical shifts, market shifts, social crisis, record corporate profits, industry lobbying, regulatory changes and forecasts. In all these reports and briefings, one crucial group of industry actors continues to stay under the radar: fossil gas infrastructure operators. These middle men of the gas industry are often considered to be mere executors: they build pipelines and terminals, to be used by other - key - actors of the fossil industry. Pascal De Buck, the CEO of Fluxys - one of the largest gas operating companies in Europe - states it clearly: they have little responsibility, they are not the ones deciding, controlling, or pushing for gas contracts.38 If anything, gas operators have been praised for their role in tackling the current energy crisis, serving the common good by developing the infrastructure that will keep us warm throughout the coming winters.

Our analysis will debunk these misconceptions. We will show that gas operators are driving the expansion of the gas industry and risking increased catastrophic climate impacts. We will also inspect the plans they put on the desks of decision-makers, showing these are not based on a rigorous assessment of the current situation, but constitute irrational proposals which, if fully implemented by our representatives, would lead us to miss our climate targets while shifting the bill onto citizens.

LNG: an introduction

We will focus on the biggest geopolitical shift in the fossil landscape: Europe’s detachment from Russia and its new reliance on the United States of America. We will analyse gas flows, contracts, finances, infrastructure expansions, emissions, regulatory changes, political agreements, and industry lobbying. We will confront all of this with the data that should have been the basis for the steps and decisions taken in 2022-23. We will also give a platform to the communities fighting against this fossil fuel invasion of their lands and, through their battles, defending a sustainable future for us all. We will illustrate global trends and figures with concrete examples on both sides of the Atlantic.

In the US, we will highlight the export terminals delivering the most gas to Europe: especially Sabine Pass LNG, owned by Cheniere, which is the biggest export terminal in the US.39 The petrochemical and fossil fuel industry continues to sacrifice the health and safety of communities on the US Gulf Coast by ramping up the build-out of fossil fuel infrastructure. In Europe, we will focus on Dunkirk LNG, owned by Fluxys, which is the second-largest LNG terminal in continental Europe and the prime entry-point of US gas to Europe. We will uncover the plans of Fluxys and show that, far from being follow-up plans, they are both executive and inconsiderate.

Liquefied Natural Gas (LNG) is fossil gas, mostly methane, that has been cooled down to its liquid state for ease of transportation and storage. Unlike pipeline gas, LNG is usually transported over long distances using highly specialised tankers. The liquefaction process reduces the volume of fossil gas by a factor of around 600, by keeping it at extremely low temperatures. However, LNG liquefaction, transportation and regasification require a significant amount of energy, resulting in a higher carbon footprint compared to pipeline gas. LNG can be up to 4 times more CO2 intensive than pipeline gas in the EU.40 LNG sourced from fracked gas in parts of the US is among the most environmentally destructive sources of fossil energy in the world.41