LOUISIANAAGENT

N O V E M B E R 2 0 2 2

A M O N T H L Y P U B L I C A T I O N O F T H E I N D E P E N D E N T I N S U R A N C E A G E N T S & B R O K E R S O F L O U I S I A N A

JEFF ALBRIGHT

Chief Executive Officer jalbright@iiabl.com (225) 236 1366

BENJAMIN ALBRIGHT

Vice President of Strategic Initiatives balbright@iiabl.com (225) 236 1357

KAREN KUYLEN

Director of Accounting & Finance kkuylen@iiabl com (225) 236 1353

Director of Insurance Programs jnewchurch@iiabl.com (225) 236 1350

KATHLEEN O'REGAN

Director of Communications & Events koregan@iiabl.com (225) 236 1360

BRANDI

Insurance Programs Administrator bvanpelt@iiabl.com (225) 236 1358

DUSTIN WAMBSGANS

Agency Consultant dwambsgans@iiabl.com (225) 236-1361

Director of Member Relations lyoung@iiabl.com (225) 236 1351

Jeff Albright November 2022

Jeff Albright November 2022

The IIABL Board of Directors met at the Capitol Hilton in Baton Rouge on November 11, 2022.

IIABL Secretary-Treasurer, Bret Hughes, reviewed the 2021-2022 annual CPA Financial Audit. The auditor issued a clean audit with no recommendations IIABL suffered a financial loss for the year as a result of strategic investments in association technology, agency technology through Catalyit, and hiring Dustin Wambsgans to provide agency consulting services to IIABL member agencies. The board approved the audit without objection

Jeff & Ben Albright discussed preliminary planning for the 2023 Session of the Louisiana Legislature. In the past two years, the Louisiana Legislature has been critical of the insurance industry’s handling of hurricane claims and have been focused on making sure that insurers pay policyholder claims promptly and fairly. In recent months, the legislature has turned their attention to the severe insurance market crisis of both availability and affordability of property insurance.

Insurers do not find the Louisiana insurance market attractive because it provides relatively small opportunity with high risks of hurricane losses, a dysfunctional tort liability system, hostile legislative environment, and a difficult regulatory environment. It was the consensus of the IIABL Board that in order to attract new insurance market capacity to Louisiana, improvements must be made to the legislative and regulatory environments. IIABL plans to lead efforts for legislative and regulatory reforms. IIABL has surveyed insurance companies and have identified the following possible legislative and regulatory reforms:

1) Reform the “satisfactory proof of loss” trigger in the bad faith penalty statute to reduce excessive litigation on property claims

Continued from page 6

2) Eliminate the “LDI 12 month rule” which prohibits insurer from filing for a rate increase more often than once every 12 months

3) Deregulate rate filings from the current prior approval (1/3 of states) to file and use or use and file (2/3 of states)

4) Modify or repeal the “ more than 3 year rule” prohibiting insurers from nonrenewing or cancelling Homeowners policies (IIABL does not support)

5) License, permit and regulate roofers to reduce roofing abuses

6) Require policyholders to notify their insurer 15 days before demolition to allow insurers to inspect in order to reduce remediation abuses

IIABL will continue to work with the insurance industry to identify and support reasonable reforms to encourage new insurance market capacity.

Jeff & Ben Albright led a discussion by the board on next year’s election for Insurance Commissioner. There are two announced candidates, current Commissioner Jim Donelon and Tim Temple who ran against Donelon in 2019.

IIABL President, Mike Scriber, presented a plan to the board on the transition of IIABL CEO from Jeff Albright to Benjamin Albright. The Executive Committee recommends that the IIABL Board name Benjamin Albright to CEO role effective January 1, 2024. Jeff Albright will remain as full time employee until December 31, 2024, as a consultant. The plan to transition Ben Albright to CEO, effective January 1, 2024, was approved by the board without objection

IIABL National Director, Johnny Beckmann, reported that IIABA President & CEO, Bob Rusbuldt will retire August 31, 2023, and Senior Vice President, Charles Symington has been named to replace Rusbuldt

The IIABL Board also did extensive strategic planning which is reported in a separate newsletter article.

The IIABL Board of Directors went through a strategic planning process at the November board meeting in Baton Rouge to update the strategic goals of IIABL. These strategic goals are the most important things that the association can do for our member agents.

In perhaps the least surprising news you’ll hear this year, the board’s number one priority is markets.No one reading this will be shocked to learn that every agent writing in Louisiana is struggling with our current market environment. Not enough insurance companies want to write business in the state, especially in the coastal areas, though our North Louisiana agents are feeling the squeeze too.We need to increase competition in the state and drive down the astronomical cost of insurance for our clients.If we can develop strong market access programs and provide a channel for our members to access new capacity through the association, that would be perfect. But, even if they don’t use the association

as a distribution channel, attracting companies into the Louisiana marketplace’s independent agency system is the single most important thing that we can do for members.

Given the loss experience that companies have faced in Louisiana, it has been an uphill climb to convince new capacity to come into the state. In addition to the frequency and severity of storm losses over the past few years, our tort, legislative, and regulatory environments have compounded the problems that insurance companies face in our state. Social inflation leads to unpredictable losses, so carriers cannot price their products effectively. The board therefore tasked the association with addressing the broader market conditions which make Louisiana an unattractive state for insurers to deploy capital. If we can lessen the legislative, regulatory, and litigation hurdles for insurance companies, we will be better able to attract competition into the marketplace and ease the burden for our agents.

Technology continues to be one of the most important issues for future success of independent agents. However, agents rarely have time to devote to improving the technology deployed in their business. With the market going crazy, the constant need to sell, service, and assist in claims, agents need to keep their head in their business. That’s where the association can help. The board reaffirmed their commitment to Catalyit, our agency technology consulting company. Catalyit is your one stop resource for technology in your agency. Catalyit does your homework for you, so that you can implement new technologies useful technologies that bring a real ROI to your business, not just shiny new toys in your agency with minimal effort. The Catalyit Success Journey makes it easy for you to improve your agency technology by providing a step by step process.

The Catalyit Success Journey - Part 1: Introduction

The Catalyit Success Journey - Part 2: Baseline Milestone

The Catalyit Success Journey - Part 3: Better Milestone

The Catalyit Success Journey - Part 4: Best Milestone

The Catalyit Success Journey - Part 5: Beyond Milestone

The Catalyit Success Journey - Part 6: So What?

The third strategic goal that the board identified was helping agents learn to run more sophisticated, efficient agencies In addition to identifying educational opportunities for events and webinars, the board affirmed the development of IIABL Agency Consulting. IIABL has hired Dustin Wambsgans to be a full time consultant on staff at the association. Dustin will be rolling out consulting services for members in the following

areas: Sales Transformation, E&O Loss Control & Operational Improvement Reviews (may be eligible for discounts on your E&O written through the association), Website Audits, Agency Workflows & Automation and more. Dustin will bring best practices from across the industry to your agency, improving the efficiency of your staff, freeing up their time to provide best in class customer service and expertise in sales. All of this is designed with member satisfaction in mind: our consulting will be offered at a reasonable price, allowing all members, large and small, to access best practices operations in their businesses.

ICYMI: Watch the entire Catalyit Success Journey series now!

Having difficulty finding coverage for your non standard property risk? Big "I" Markets is here help.

We’ve partnered with an A rated excess & surplus lines carrier offering homeowners insurance for risks other carriers decline or are unable to write, and a second market offering vacant personal lines coverage.

Sample eligible risk exposures include earthquake, coastal, unprotected locations, rentals, short term rentals, vacant homes, loss frequency/severity, and multi location property blankets. Some California wildfire exposures may be considered on a case by case basis.

Coverage highlights include:

Non-standard Homeowner/Rental Dwelling/Vacant Dwelling/Unsupported Secondary Dwelling:

Industry accepted ISO HO3 special form modified to tailor coverage for unique exposures.

Vacant Dwelling uses DP3 coverage form.

Minimum premium $1,000 Many standard ISO endorsements and customized endorsements available Flexible deductible options

Condominium Unit Owner / Renters:

ISO HO 4 (Tenant)

Minimum Premium $500

Optional standard ISO endorsements available to allow customized coverage Coverage Contents, Loss of Use, Liability and Med Pay

Flexible deductible options

These products are available for Big “I” members to access in all states except AR, HI, NE and WV.

Not yet registered for Big “I” Markets, the online market access program available exclusively to Big “I” members featuring no fees, no minimums and ownership of expirations? Complete a simple and free registration online at www.bigimarkets.com.

This article is intended for general informational purposes only. IIABA and its subsidiaries and affiliates shall not be held responsible in any way for, and specifically disclaim, any liability in any way relating or connected to any reliance on or use of this article. The information contained or referenced herein is not intended to constitute and should not be considered legal, accounting or other professional advice, nor shall it serve as a substitute for obtaining such advice. If specific legal or other expert advice is required or desired, the services of an appropriate, competent professional, such as an attorney or accountant, should be sought.

Copyright © 2020, Big I Advantage, Inc. All rights reserved. No part of this material may be used or reproduced in any manner without the prior written permission from Big I Advantage. For permission or further information, contact Big “I” Markets, 127 South Peyton Street, Alexandria, VA 22314 or email at bigimarkets@iiaba.net.

As an insurance agent or broker, you’ve honed your craft as a personal lines agent, developing relationships with your clients over the years. But did you know that many of your clients are likely to run a home based business or side gig? Without insurance to cover their commercial forays, some of your clients are likely not fully protected from the unexpected.

Adding business insurance services to your repertoire may sound intimidating but these days there is a wide variety of tools available, including Coterie, that make the process much simpler.

You know your clients and have spent time building deep relationships. Take your services to the next level by branching out to small commercial insurance.

There are 31.7 million small businesses in the U.S. according to the SBA. Furthermore, the number of new businesses continues to increase. The opportunity for agents and brokers to step into writing commercial insurance is massive. The demand for business insurance services is likely to continue to grow so opening up your agency to commercial insurance will increase your ability to not only better serve your clients, but allow you to tap into this huge market. In addition, independent agents write 83% of commercial lines premiums compared to one third of personal lines according to the IIABA.

2)Build deeper relationships.

Half of all small businesses begin at home, according to the SBA. If you already insure your clients’ home and auto policies, having the conversation about how to best insure their small business which very well might be home based is a natural progression of your relationship. Take time to ask if your clients have developed a side hustle or gig. They may not realize what their personal lines policies will not cover, leaving them at risk.

Through raters where agents like you can get quotes from several companies at once, to networks or aggregators where you can get access to several insurance companies writing small commercial, there are more solutions now than

Continued from page 16

ever before. Small commercial insurance is no longer a long, unprofitable process.

4) Your clients need you and you can start with your current clients.

You likely already have clients who either have a side hustle or have opted to start a business full time. Deepen your current relationships by discussing what business activities your clients might be currently conducting. Business owners are busy, they need a trusted advisor to help them sort through the complexity of small commercial insurance.

5)

From home-based businesses to start-ups, build a niche and develop a reputation for handling small commercial business that many agents don’t want

to handle. By targeting, marketing, and prospecting small commercial, you’ll build trust and bring in referrals. Act now while small businesses are still underserved by the insurance market, and build your reputation, expertise and book of business with business insurance services.

Seize the opportunity now around you and start writing small commercial insurance today. Coterie Insurance provides agents and brokers with a fast and easy solution to writing small commercial insurance.

View an online version of this blog on Coterie’s website.

...

Continued from page 17

I came across an interesting report from Reuters recently that, among other things, found that today’s talent pool is approaching work from an entirely different perspective than in the past. Namely, today’s job seekers do not have the “job for life” mentality that previous generations embraced, while at the same time they are much more interested in pursuing roles at organizations that offer growth opportunities and opportunities for work and projects that might be outside of their specific job descriptions but are tied to their unique skill sets.

While this presents a challenge for recruiting, keeping and motivating talent in the industry, it nevertheless aligns with the way business is going in general: embracing a skills based approach to work.

We’ve talked previously about the transition to thinking of work in terms of the skills needed to achieve business goals, versus work as defined by traditional job roles. Companies that adopt this approach have been dubbed “skills based organizations” and according to Harvard Business Review, they’re the way of the future. “Evaluating employees and new hires based on their skill sets instead of their work history can help level the playing field and help companies realize the talent they already have. It also makes talent pools more diverse and often makes hiring more effective. This is the future of hiring and development.”

As we all know, the insurance industry does not have enough talent to fill the many open positions. By focusing on skills, including cross over skills from different insurance sectors or industries, companies can increase their talent pool.

So while talent today may be more selective when it comes to their jobs, expect more in terms of flexibility, and seek additional work opportunities and career growth more quickly than in the past, the most forward looking organizations have already been adapting to focusing on skill sets casting a wider net to find the right talent and to keep employees.It’s much easier to offer people internal growth opportunities and out of the box projects when you are focused on skills rather than on job descriptions, for example. And when you’re prioritizing skills, you’re also prioritizing exactly the type of innovative and creative mindset in your workers that experts say will be crucial for success going forward.

Sharon Emek, PhD, CIC CEO and President, Work At Home Vintage Experts WAHVE.com

The holiday season is a time to reflect on and honor the things we are most thankful for, and at the top of the list are our members! This Thanksgiving, we want to let our members know how much you are valued and how grateful we are for your patronage and participation.

Everything we do is done with the goal of serving agents, insurance consumers, and the industry at large. As part of that mission, we continue to provide Independent Market Solutions (IMS), a market access program that offers agents flexible appointment terms and a robust selection of competitive insurance products. Both our products and member participation continue to grow, creating scale and efficiency that will allow even greater success in the future.

As we work to expand and improve IMS in the coming year, we take this time of Thanksgiving to express appreciation to our members for the progress we have made thus far!

To learn more about IMS and the carriers we can help you get connected with, click here.

IMS partners with Synchronosure in FL, NC, NY, NJ, CT, AL, and CA to create bindable quotes for your agency’s customers within minutes Additional states coming soon! Underwriting response time is typically less than 10 minutes, simplifying the underwriting process so you can get more done in less time

“We are thrilled to extend our partnership with IMS and bring our products and solutions to the IMS marketplace. Our technology and experienced underwriters position us to respond very quickly to member agency ’ s business opportunities, typically giving you quotations in seconds and minutes rather than the 2 to 3 days common in the industry. We have a broad range of appetites within each product, and we are working on introducing additional product to

our distribution partners over the next few months which will include BOP, Property, expanded GL appetite, and other types of business insurance specifically focused on meeting the needs of small business We have a simple process to get producers appointed, and can have your team set up, trained, and doing business within a few days ”

“We are pleased to announce the addition of our newest Independent Market Solutions partner, Synchronosure. With the addition of the Synchronosure products and solutions offerings we, once again, have found a proven partner that will assist our members and their clients.”

The primary areas of focus for this partnership are:

Workers Compensation: Over 900 available governing class codes representing most of the classes associated with hazard grades A F, and 15 classes within hazard G. Maximum unmodified manual premium is $35,000. The maximum experience mod is 1.35. The insurer is Sutton National, rated A VIII by AM Best.

Agricultural Risks (no trees or animals bigger than we are).

GIGBOP: A package insurance coverage includes Business Personal Property, Business Liability, and Miscellaneous Professional Liability, uniquely crafted to meet the needs of modern small businesses. Minimum policy premium is $350 for $100,000 liability limit and $500 for $1 million policy limit. Currently active nationwide on an E&S basis. The carrier for this product is Sutton Specialty, rated A- VIII by AM Best. Segments include:

Continued from page 24

Gig Workers, Independent Contractors, Freelancers, including Home Based Businesses and Businesses Operating Out of Shared Workspace (e.g., Regus, WeWork)

General Liability: Live in December 2022. General Liability with more than 150 available class codes with a particular focus on small business. Limits to $1 million per occurrence / $2 million general aggregate / $2 million products completed operations aggregate. ISO based policy language. Minimum premium is $1,000. Currently active nationwide on an E&S basis. Maximum premium of $35,000.

Follow Form Excess Liability: This liability coverage provides protection for premises and operations liability, and products/completed operations liability. Coverage is offered on a follow form excess liability basis, and we sit over GL and Auto liability, but will not do auto by itself.We have more than 550 available class codes, and have up to $5 million in capacity to attach in the lead $11 million from ground up, and a second $5 million of

capacity that can attach at $11 million from ground up. Currently active nationwide on an E&S basis. Maximum layer premium is $35,000. Segments include but are not limited to:

Contractors

Hospitality Habitational

Get Appointed Today! Agency Agreement

https://synchronosure.com/wp content/uploads/2022/09/SynchronoSure IMS Pr oducer Agreement Watermark 02162022 2.pdf

The SynchronoSure® agency agreement is between the individual signing agency or brokerage firm and SynchronoSure®. When you agree to and e sign the agreement during this application process, you also agree to the instructions, guidelines, policies, and procedures contained in the agency agreement.

from page 25

Please Read If Considering SynchronoSure: Producer Sign up for SynchronoSure must be completed by clicking this link https://synchronosure.com/producer registration/ Website synchronosure.com

Explore the new and improved Social Media Suitcase® site from Foremost® Insurance! It offers free marketing resources to help build your agency’s online presence and connect with consumers.

Foremost designed the Social Media Suitcase to make marketing more effective and easier for agents like you! The tools you’ll find include:

You’ll also find our brand new digital marketing guide: The Social Media Carry On! It’s packed with tips and strategies to help your agency excel. Whether you’re new to social media or already a confident user, there’s something valuable for everyone.

Get started at SocialMediaSuitcase.com and reach out to your Foremost marketing rep with any questions!

February17,2021

It is no secret that over half of the agency owners today are at or nearing retirement age. Current agency owners are facing a transition in their agency within the next 5-10 years. Their agency transition is not a question of if it is a question of when. Many carriers and agency staff want to know that the agencies they are partnered with or a part of have a solid perpetuation plan in place, but what exactly does that mean? To some agency owners it means that they have a rough idea of what they plan to do when they decide to retire In many cases they have a handshake agreement with another agency owner, or member of their team and have talked about what they will do someday, but no details have been decided and there is nothing in writing. While that is a good step in the right direction, that is not a plan that's just an idea.

To have a strong plan for your agency you need a written document that addresses what will happen to the ownership of your agency if the you are no longer able or willing to run the agency. This can occur due to a planned event or an unplanned event, and the agreement needs to address both types of situations. In short, you need to define the who, what, when and how for your agency. Here is an overview of the basic areas that need to be addressed in your agency’s perpetuation plan:

Define who is eligible to become an owner of the agency.

The order that will be followed if there are multiple people eligible to purchase shares. Definition of triggering events that will cause a change in ownership.

Define how the price of the agency will be determined.

The way in which the purchase will be funded and the related tax implications.

Outline of how the agreement can be amended, changed, or terminated.

As you can imagine, agencies that have a single owner are at the most risk when they do not have a perpetuation plan in place. By an agency owner taking the time to think through and document their wishes in advance, they take the pressure off their loved ones at a time that is in many cases the most difficult situation they may ever face. Having a document that addresses all these factors in advance provides all the people involved in that agency with a roadmap and peace of mind that the agency will continue to operate seamlessly if something unfortunate happens to the owner. Both the experience and financial impact will be significantly different for an agency, their family, staff, customers, and carrier partners when a clear plan has been pre defined than it is for an agency that is put in the position to decide on the spot because there is no plan in place.

In almost every organization their people are their most valuable asset. Inside an independent insurance agency, this is 100% the case. We operate in an industry that relies heavily on relationships, and your people are the ones that build, maintain, and grow those relationships in every facet of your agency. Whether it be with customers, partners, carriers, vendors and with members of your staff they are key to your success. In addition to the relationships they build, many people inside organizations hold key roles that are critical to the organization.

This becomes even more pronounced in organizations that are small and have limited abilities to have multiple people in similar roles. The average independent agency has a staff size of 7 employees, which does not leave a lot of opportunity for cross-over in key roles. As a result, the people that hold key roles become an area of risk for the organization. We talk a lot about

succession planning for the owner of an agency, but not a lot of focus is placed on creating a plan to cover key roles within the agency should one of your employees chose to leave, become ill or retire. Here are some ways you can reduce the key role risk inside your agency.

For each position inside your agency, list the core functions included in each position or role. Once you have the core functions defined, make a list of every person that is trained in each of the core functions across your entire organization. Ask yourself who is the backup for this function inside the agency? In many cases the service and sales focused roles such as CSR, account manager, and producer will have more than one person trained to perform the key functions of these roles. For accounting, administrative, and operational functions you may find that there are several areas where only one person has the access, knowledge, and skillset to perform certain functions. You now have identified your core areas of risks

For each of the core functions identified inside your agency, consider the impact that each function has on your agency and prioritize those functions that will create the most risk should you no longer have the key employee in place to perform that function. Work with your team to document detailed processes to complete each function. Ask them to include all the contact information for the resources they utilize such as technology vendors, carrier contacts, outside accountants or vendors, etc. Consolidate all these processes in one location that will serve as a reference for all of the key functions inside your agency.

Once the processes are documented, identify the right person inside the agency that can serve as a backup to the primary person who is responsible

Continued from page 31

for each function. Some functions will be easier to identify a backup than others as some functions may require access to sensitive information like payroll or financials. Once you have identified the appropriate backup for each function, implement a plan for them to be trained. You may need to create new login to provide the right level of access for the employee that will serve as a backup. The documented process should be used as a guide and be edited as they step through the training process. This will ensure that when they need to perform this function independently, they will have the information they need to be successful. Set goals to have all the key functions documented and cross trained inside your agency by a certain date and set check in meetings with the primary and backup employees to monitor and celebrate the progress.

For each of the critical functions that you have identified, documented, and created a training plan for, it is also important to identify opportunities for the employee who is being trained to practice their skills and test the processes that they have learned. Great opportunities include vacations, setting a periodic interval where they take a turn doing the function. By being intentional about practicing these functions, you will have less down time should something happen to the primary person in your agency that is responsible for these functions.

There are many benefits to cross-training key functions inside your agency besides reducing the risk for the agency. Your entire staff will benefit from having these key functions identified and backed up. There will be less delays when someone is out of the office, and you may find that it has a positive impact on your overall culture. By participating in this process, your staff will gain a greater sense of understanding of some of the different roles within the organization and may even gain a whole new appreciation for their teammates. In many cases, by going through the process of documenting these functions and training others, efficiencies and improvements are naturally identified. A second set of eyes on things that we have always done a certain way, can lead to opportunities for efficiencies. In addition, the employees that are responsible for the key functions will have a greater sense of relief when they take vacations or are away from the office knowing that they have someone there that can cover for them, when needed.

Consumers in the US and Canada are more worried about cyberattacks and data breaches, and they’re taking more action. But some poor cyber security habits are persistent, and not many are aware of the protection that personal cyber insurance affords.

An overwhelming 92% of respondents in Chubb’s annual study on personal cyber risk said they were worried about a cyber breach exposing their personal information or identity, up from 80% in 2019. 81% were concerned that their connected devices pose a threat to their privacy.

GIA SNAPE 11 NOV 2022

Dynata polled more than 1,600 respondents in the US and Canada between August and September this year on their cyber risk attitudes and behaviors.

“One of the biggest takeaways from this report is that it validated what we were thinking around people’s awareness of their cyber risks,” said Carolyn Boris, VP of personal risk services and personal cybersecurity expert.

“During the pandemic, there was a proliferation in the use of internet-connected technologies, and with that increase came a heightened awareness in people,” Boris continued. “But the other thing that was most interesting to us was that people are taking more action as well.”

The Chubb survey found more than half of Americans and Canadians (51%) said they used multi-factor authentication (MFA) to log into their online accounts, twice the level in last year’s report. About half (48%) of respondents cleared their browser history in the past 12 months, compared to under a third (28%) the year before. More

people are also using cybersecurity software (38% this year versus 25% last year) and password protection apps (35% this year versus 19% a year ago).

“Multi factor authentication is one of best things that people can do to protect themselves and to mitigate cyber risks,” Boris said. “Nearly 80% of people said they prefer to use multi factor authentication when logging into their accounts. That's really telling us that people are aware and they're trying to do something about their personal cyber safety.”

Attention to passwords has also increased. Three out of four respondents reported updating their password for their primary bank or financial account in the last 12 months. 70% said they updated a password for a digital account voluntarily without being prompted by the provider.

While good cyber hygiene is taking root among Americans and Canadians, the Chubb survey also found some risky habits were harder to break. Half of people still use their pet’s name or other easily identifiable information as new passwords. This habit was especially sticky in high-net worth Americans and Canadians (about 85%) and Millennials (69%).

“Everyone's trying to save some time, so sometimes it’s just easier to use an old street address when picking a new password because it’s easier to remember,” explained Boris. “Or they might be using public wi-fi in an airport or coffee shop to log into their bank accounts. Those are the types of risks you forget about in the moment when you’re trying to save time.”

Another piece of good news from the survey is that more individuals were taking out personal cyber insurance to protect their data 39% of Chubb respondents said they have a personal policy,

including a majority of mass affluent (63%) and high net worth (83%) consumers.

However, general awareness of personal cyber insurance remains low at 39% across generations. Younger respondents like Gen Z and Millennials were more likely to be aware, while 65% of baby boomers were unfamiliar with the coverage.

Boris said this presents an opportunity for agents and brokers to educate clients. “Individuals and their insurance agents should be thinking about the types of risks that are out there and how they want to mitigate them,” she told Insurance Business. “There are misconceptions around personal cyber insurance and identity theft insurance; the two can be confused.”

Identity theft insurance can protect policyholders when their personal identity information is compromised in the event of a breach. But

personal cyber insurance will go beyond, protecting against ransomware attacks or breaches on household interconnected devices.

“Financial loss was something very important to our respondents, and they want to know that if they suffer some type of loss from their accounts, that that would be reimbursed through a cyber protection policy,” Boris said. “If you experience a breach or disruption to household interconnected devices, you also want insurance to ensure you can correct the damage. Those are some of the things that individuals want to think about when they want cyber protection above and beyond identity theft insurance.”

Ultimately, the best advice that brokers and agents can give their clients is to be constantly vigilant and employing a variety of mitigation actions.

“We talk often about using strong passwords. But it's also about using tools to protect yourself from any cyber threat, like using password managers or multi factor authentication. Not sharing credit card information online and constantly updating software are also important,” Boris said.

“Finally, continually educating yourself about cyber threats and sharing that information with all individuals in your household will help ensure everybody is practicing good cyber behavior.”

Your candy and confection business customers have it pretty sweet their lives revolve around creating, packaging and selling sugary delights to an eager clientele of all ages.

Those customers could hit a sour note, though, if their confection making supplies are stolen from their car, a power outage results in melted merchandise or a candy catastrophe occurs at their booth during a local festival.

Typical homeowners insurance may not cover incidents such as these, which is why a home business insurance policy from RLI is the icing on the cake of coverage related to:

business personal property (equipment, inventory and supplies) and business related liability exposures lost income losses or damage from business activities conducted at the business owner's home or off site at another location business property while in transit liability coverage when performing business related activities at someone else's residence.

With liability limits up to $1 million and business property protection up to $100,000 (with a $250 deductible), an RLI Home Business Insurance policy provides valuable coverage for incidents that could otherwise lead to some bitter results for your customers' candy and confection businesses Make sure they're aware of how sweet it is to be properly protected.

For more information on the RLI Home Business Insurance Policy, contact your state's administrator or visit www iiaba net/homebusiness

from

Whitney Big "I" E&O Guardian

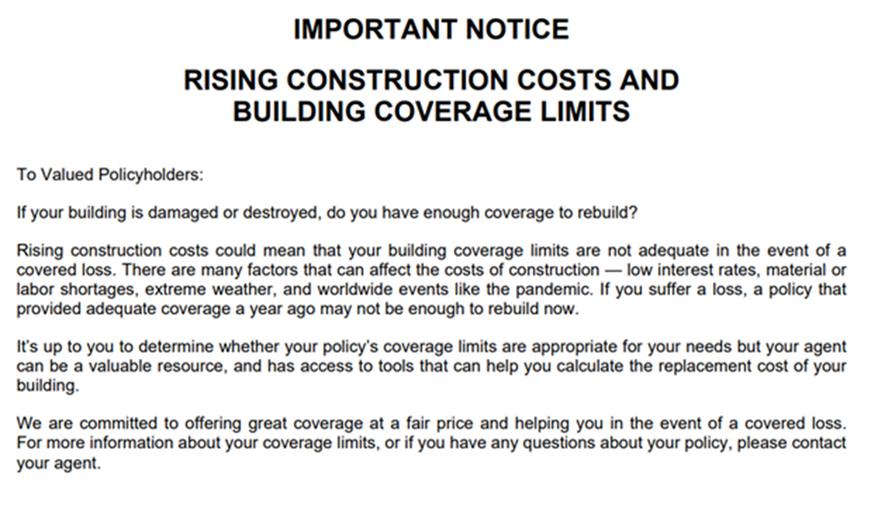

This type of inflation is measured by the consumer price index, which is defined as the price change of a basket of goods or services typically purchased by specific groups. This inflation index rose 7.5% in 2021 and to an annualized rate of 8.3% for April 2022 the highest level in 40 years.

Why does this matter to you? Because it drives up the overall cost of claims. Consumer price increases result in paying more on claims due to rising attorney fees for claims defense and higher actual claim values. For instance, due to inflation, the cost of rebuilding a home that burned down may be 20% more for materials and labor than it was 3 years ago.

This type of inflation is related to strategies used by plaintiff attorneys to inflame juries and increase jury awards. Our defense counsel use strategies to combat these emotionally charged tactics, but it can be an uphill battle.

Inflation can create exposure risks for insurance agency clients. Rising construction costs could mean that a building that was adequately insured a year ago may now be underinsured. Though agencies are not responsible for determining the appropriate limits, you should recommend that your customers reconsider the limits on their policies in light of inflation. Some carriers have sent out notices to policyholders similar to the following.

Elizabeth

If your carriers are not sending a similar message, you may consider encouraging them to do so. You should communicate a similar message to your customers:

Best: After you have had this conversation, follow it up with a letter to your client documenting the conversation.

Finally, when you have offered them higher limits and if they reject them, make sure you have them sign that they are rejecting the higher limits. Otherwise, you may find yourself in a “he said, she said” situation. Even if a partial loss is within your current limit, a substantial coinsurance penalty may be assessed if the property is no longer ‘insured to full value’. Customers should use available resources to reassess the adequacy of their limits and, if needed, ask you to quote higher limits.

Policy limits that were adequate as recently as a year ago may now be inadequate due to steeply increased construction costs.

There is a “Sample letter for information regarding increased building costs” available on the E&O Guardian Website, which is the exclusive E&O risk management website for IIABA members who are also insured by companies within the Swiss Re Corporate Solutions group. This and other sample letters are there for you to adapt for your agency.

Unfortunately, if your client finds themselves underinsured, they may look to your agency to make them whole To avoid or mitigate an E&O claim we recommend the following best practices

Good: Have a conversation with your clients at renewal and explain that due to inflation they may be underinsured now when they were not in the past.

Better: After you have had this conversation, make a contemporaneous note in your Agency Management System documenting the conversation.

Remember, if you are insured with Swiss Re Corporate Solutions, your deductible will be waived (up to $25,000) if there is a written, contemporaneous documentation of the refusal of any customer to accept any type of coverage or limit offered by you and a subsequent claim alleges the failure to secure that coverage or limit.

While it is impossible to know what the future holds, by looking to our history we can provide advice and tools that will help you better service your clients and hopefully, avoid or mitigate an E&O claim.

*Elizabeth Whitney, J D is the Head of US Agents, Senior Vice President, Senior Vice President, Swiss Re Corporate Solutions Elizabeth is a licensed attorney who has spent the last 24 years focused on various aspects of professional liability including claims, risk management and underwriting.

Insurance products underwritten by Westport Insurance Corporation and Swiss Re Corporate Solutions America Insurance Corporation, Kansas City, Missouri, members of Swiss Re Corporate Solutions

This article is intended to be used for general informational purposes only and is not to be relied upon or used for any particular purpose Swiss Re shall not be held responsible in any way for, and specifically disclaims any liability arising out of or in any way connected to, reliance on or use of any of the information contained or referenced in this article. The information contained or referenced in this article is not intended to constitute and should not be considered legal, accounting or professional advice, nor shall it serve as a substitute for the recipient obtaining such advice The views expressed in this article do not necessarily represent the views of the Swiss Re Group (“Swiss Re”) and/or its subsidiaries and/or management and/or shareholders.

Not too long ago, I was driving home after speaking at a Big “I" state association convention. It was a four-hour drive, and I was mostly in that zone of looking forward to getting home, but I did find my mind mulling over the industry trends that were discussed at the conference—efficiency, direct integration, hiring new talent, diversity, digital models, customer experience.

Then, somewhat prophetically, I noticed a billboard: “Buy a Car in As Little As 11 Minutes."

Interesting. Hmmm … 11 minutes? Who needs to buy a car in 11 minutes? Should we even be able to buy a car in 11 minutes? Is it even responsible to sell someone a car in 11 minutes?

I noodled on that for a few minutes and ultimately acknowledged the billboard was about setting the highest customer expectations and that few people would ever buy a car like that. Of course, the statement is hyperbole, but it does point to ways in which the customer experience could be significantly improved It shouldn't have to take

half a day or longer to purchase a car anymore. In fact, I was driving a vehicle that was bought just a few weeks prior and that experience was ripe for updates.

Those five minutes or so turned into a couple of hours of thinking about how that billboard translates to our industry. And I've been thinking about it ever since, both in my prior role and as I transitioned to my role as executive director of the Big “I" Agents Council for Technology (ACT). Just one billboard prompted thoughts about many similar conversations that we are having in the insurance industry on topics such as:

Speed across seemingly endless transactions

Data collection and utilization

Direct integration

Transparency Marketing accuracy Integrity

Overall efficiency

These topics tend to be very popular with industry podcasts, webinars and conferences. While the day long car buying experience we've all undoubtedly encountered could be finessed, our industry has plenty of room for improvement across a number of fronts. In fact, the number of opportunities for improvement in our industry can feel daunting and, depending on what seat you occupy, the priority of these opportunities can differ sometimes greatly.

This brings us back to speed. We talk about our industry being too slow but too slow to get where? Speed is a function of distance over time. So, by default, you need a destination and a measurement of how long it takes to arrive to calculate speed. We may not be moving as fast as some would like, but let's think about why that is, where we should be going, and then assess our speed.

As an industry, do insurance customers need to buy the proverbial car in 11 minutes? How much better than the half day experience is good enough today, tomorrow or in 10 years? We all agree on the need for improvement, but opinions on how much improvement is needed varies depending on the seat you occupy. Few would argue against the need to evolve, but agreeing on how much is less clear.

So, when an entire industry thinks it shouldn't take all day to buy a car, but disagrees on how much less time it should take, where do we want or need to go? Where do we even start?

If you're a golfer, motorsports aficionado or student of major consulting principals, you've likely heard an expression along the lines of “slow down to speed up." On the surface, there is nothing intuitive about this statement. Even beyond intuition, it doesn't make sense from a physics or math perspective either—until you think about what the statement is implying.

Slowing down allows you to hit your marks, not overswing, control your braking, not roll your wrists, not overdrive a corner, get your hips through, maintain control, apply discipline and manage whatever requisite levels of intention are necessary to reach your goals. And what happens when we do those things well? We hit the ball further and straighter, racers make quicker lap times, and businesses begin to create alignment and hit their targets.

In our industry, most of the fundamentals have held true for decades sound underwriting, adequate pricing, claims handling, compliance, clear appetite, accurate quoting and more. Admittedly, some of those are not overly romantic in a world where nearly all the stakeholders want more, and they want it done faster.

Those fundamentals and conflicting expectations apply to agents, carriers and consumers, as well as many new and existing companies that enable our industry. But, with relatively universal agreement that we can be quicker, more efficient and more effective, it is easy to be distracted by shiny new objects and technology that focuses on more romantic activities and new tools.

To be clear, the industry can and has benefitted from new tools, and it should embrace technology as a means to an end. But, as has been said before, we are not manufacturing and selling widgets. Transferring and assuming others' risk with a promise of financial indemnification in a state by state regulated industry most certainly requires different priorities and approaches than most other industries. Our processes are ripe for improvement, but it is important to keep our industry's unique constraints in mind as we explore, identify and prioritize where we focus resources on getting better, quicker and faster. At the same time, we must consider what steps can be eliminated, what data can be gathered or used as a proxy, how self service tools are implemented and what activities can be fully automated.

To some, this can be construed or even dismissed as an industry's collective reluctance to change. Perhaps that's true for a few outliers, but the vast majority of industry stakeholders are aware of the need to change, intent on learning and evolving, and are open minded about making needed changes to remain viable and add value to our mutual customers. Most insurance professionals are actively on the continuum of change in their organization. However, the challenge and opportunity depend on priority and capacity.

If we all agree that buying a car should not take your entire Saturday, but a small minority believe it should only take 11 minutes, how can we collectively make meaningful strides?

It's important to be really clear on your organization's competitive business strategy. Or, as Simon Sinek wrote, “Start with your why."

Given the overwhelming number of opportunities for change and the seemingly infinite number of approaches to get there, it is very easy to get caught up in what has

been coined as the “shiny object syndrome" or, even worse, analysis paralysis. These decisions are hard, and even deciding to do nothing is a decision with its own outcomes.

In “National Lampoon's Christmas Vacation," Clark sets out to make the biggest and best light display in their town. But if you fill in the blanks, it's clear he bought every shiny object possible, installed them all with no strategy or planning beyond just wanting to be the biggest and brightest, and then plugged them all together in a tangled mess.

Well, we all know what happened when he plugged in the master cord nothing. None of the lights came on. Not one piece of equipment worked as it was intended.

That scene always makes us laugh when we see the movie, but the idea of something similar in our business makes us cringe. It's easy to see how that could happen to a business owner today, because everywhere we turn we are inundated by new tools that promise to make our business the best and brightest on the block.

It can be easy to be influenced by the hype or fear of missing out. While it takes real discipline, it can be easier than you think to mitigate the chances of being Clark and approach integrating technology

with intention and thought, significantly increasing the likelihood of a well designed, executed and functional light display in your neighborhood and your business Of course, it's worth recognizing that there are some amazing opportunities out there that can be leveraged with the right homework, approach and clarity on your competitive business strategy.

We all know this intuitively, but it's easy to lose sight of it because there is no single answer, consultant, tech stack, tool, carrier appointment or key employee hire that is right for all agencies. There are certainly best practices and lessons to learn from one another, though In fact, it is beneficial to do so However, if there are more than 35,000 independent agencies in America, there are arguably just as many points of view on how to run one.

That is not to imply that all are growing, running the same margins, have comparable value, attract the same employee talent or customers, or are evolving with consumer demands in the same way or at the same pace It simply supports the notion that all are independent businesses with unique “whys," each in varied positions on any number of agency technology continuums.

Understanding what's happening in the world is important. Being intentional about your approach is essential. Moving forward is crucial moving faster is only important. The question is: How much faster?

Is there a right answer? If history has proven anything, projections are just that It's easy to get lost in a moment in time and let excitement, fear or complacency govern our decisions. Things also tend to unfold differently and at a different pace than we expect. All of this continues to support the concept: Slow down to speed up.

Slowing down is analogous to taking a breath to ensure you have total clarity on your organization's strategy. To do that, it's critical to have answers to these questions before making significant changes:

What customers do you want to attract and retain?

What geography do you wish to serve?

How do you want to show up and differentiate in the marketplace and your community?

What types of employees do you wish to work with?

It's critical to have thought through these questions to understand how much change is needed. It's critical to

slow down to speed up. It's critical to focus on fundamentals. This process will help you assess where your organization is and where you want to be on the continuum between buying a car in 11 minutes or offering the full Saturday at a dealership experience to your customers.

We all know we need to evolve and change. With a clear vision of our why, intentionality and a focus on delivering the fundamentals in new and meaningful ways, it can be done and is being done. But it cannot be done haphazardly or without focus. Speed for the sake of speed is not sustainable and can be a recipe for bad outcomes, such as hitting the wall, slicing a drive or making less than ideal decisions that will cost you in the long run.

Clearly, there is no proverbial silver bullet, but you can greatly improve your chances for successful decision making, effective change and sustainably improved business results by slowing down to speed up.

Big “I" Agents Council for Technology.

Chris Cline is executive director of the