LOUISIANAAGENT

M A R C H 2 0 2 3 A M O N T H L Y P U B L I C A T I O N O F T H E I N D E P E N D E N T I N S U R A N C E A G E N T S & B R O K E R S O F L O U I S I A N A Read more aboutIIABL'sLegislativeAgenda on page#

IIABL STAFF

JEFF ALBRIGHT

Chief Executive Officer

jalbright@iiabl.com

(225) 236-1366

BENJAMIN ALBRIGHT

Vice-President of Strategic Initiatives balbright@iiabl.com

(225) 236-1357

KAREN KUYLEN

Director of Accounting & Finance

kkuylen@iiabl com

(225) 236-1353

JAMIE NEWCHURCH

Director of Insurance Programs

jnewchurch@iiabl.com

(225) 236-1350

KATHLEEN O'REGAN

Director of Communications & Events

koregan@iiabl.com

(225) 236-1360

BRANDI VAN PELT

Insurance Programs Administrator

bvanpelt@iiabl.com

(225) 236-1358

DUSTIN WAMBSGANS

Agency Consultant

dwambsgans@iiabl.com

(225) 236-1361

LISA YOUNG-CROOKS

Director of Member Relations

lyoung@iiabl.com

(225) 236-1351

LOUISIANAAGENT PAGE 3

OF CONTENTS & FEATURED STORIES

Surety Bonds: Are Independent Agents Leaving Money on the Table?

Top 5 Reasons Agents Love Selling PUPs

Annual Convention

How Taverns Can Avoid Slippery Floors

Catastrophe Claims Process

Disclosure Form-Guide

Traditional Underwriting Won't Cut It In "Chaotic" Cyber Market - Corvus

6 Underrated Marketing Tactics to Give Your Insurance Agency an Edge

The Office is Back, But It's Not the Same

How to Cultivate a Flexible Culture at Work

What are Claim-It Referrals?

Expand Your IMS Offerings

Upcoming Events

Continuing Education Offerings

Advertiser Index

2023 Industry Partners

IIABL Officers & Board of Directors

CONTENTS LOUISIANAAGENT 2023 IIABL LEGISLATIVE AGENDA 06

11 14 18153 E Petroleum Drive Baton Rouge, LA 70809 Ph: (225) 819-8007 www.iiabl.com WHYLOUISIANA HASAPROPERTY INSURANCECRISIS PAGE 4 CONTROVERSIAL BILLS TO LOOK OUT FOR DURING SESSION 16 18 20 21 22 25 27 30 34 36 40 42 43 44 46 47 48

9% of Homeowners Adjusted Limits for Inflation, Supply Costs

TABLE

Only

2023 IIABL Legislative Agenda

The 2021 and 2022 Regular Sessions of the Louisiana Legislature were a fight for survival of the insurance industry. Hurricanes Laura, Delta, Zeta, and Ida left policyholders and legislators frustrated and angry about the slow and difficult claims processes with 800,000 claims and $25 billion in paid losses. Legislators introduced a tremendous number of bills to hold insurers accountable for paying storm claims. In the end, the legislature passed reasonable insurance reforms but did not pass the truly punitive legislation.

As we approach the 2023 Legislative Session, the mood around the Capitol is quite different. Legislators have heard loud and clear from their constituents that the property insurance crisis is real. Insurance is unavailable and unaffordable. Some people can’t afford to own their home. Businesses have a hard time operating with massive premium increases. Builders can’t build, realtors can’t sell and bankers can’t loan. Something has to be done. Legislators have stopped looking for ways to punish insurers and are looking for ways to bring more insurers back to Louisiana.

Jeff Albright

March 2023

LEGISLATIVEAGENDA

At an elemental level, two things have caused the Louisiana property insurance crisis. First is a bad run of hurricanes with historic losses. There is nothing we can do about that except pray for better weather. Second, for many years Louisiana has over legislated, over regulated, and over litigated against insurance companies. If we want more insurance companies to do business here… this must change.

IIABL has a plan to change this insurance market environment by reducing the legislative and regulatory burdens on insurers.

For the past six months, IIABL has worked to develop consensus among insurers as to which reasonable reforms would attract new insurance market capacity to our state without hurting consumers. Following are the reforms we will pursue during the 2023 Legislature.

Continued from page 7

1) Reform bad faith penalty statutes R.S. 22:1892 & R.S. 22:1973

a. Maintains 50% bad faith penalty and attorney’s fees

b. Establish claim processes with time limits to promote timely payment of claims

c. Provide a clear trigger for 30-day payment requirement

d. Protects policyholder rights to supplemental payments

2) Deregulate admitted insurer rate filing process

a. Maintain commissioner’s ability to disapprove rate filings that are unfairly discriminatory or otherwise violate LA law

b. Remove discretion to disapprove rate filings based on price

c. Modeled after the Arizona “use-and-file” statutes

d. Allow multiple filings per year (eliminate LDI “12-month rule”)

PAGE 8

LOUISIANAAGENT

LEGISLATIVEAGENDA

3) Build stronger to reduce losses

a. Strengthen building code

b. Fund the Louisiana Fortify Homes Program

4) Strengthen statutory prohibition of assignment of benefits

a. Prohibition of assignment of benefits based on Florida law

b. Prohibits policyholder abuses similar to Apex Roofing & McClenny, Moseley & Associates

In addition to the legislation outlined above, IIABL is negotiating with insurance companies over legislation they want to bring to modify or repeal the “ more than 3-year rule” R.S. 22:1265.D. & 22:1333.C. The IIABL Board of Directors voted to oppose legislation that repeals the “ more than 3year rule” or exempts the surplus lines industry. However, the Board remains open to possible amendments to the law which would allow insurers some ability to manage their wind risk on legacy books of business, without undue hardship on policyholders and agents.

IIABL also recognizes that tort reform is critical to improving our insurance market environment, but it is not politically feasible until 2024 when we have a new governor.

Your grassroots support is essential to passing these insurance reforms. Please email your legislators when you receive IIABL Grassroots Alerts.

PAGE 9

BEYOND INSURANCE ISSUES... CONTROVERSIAL BILLS TO LOOK OUT FOR DURING SESSION

The 2023 Regular Session of the Louisiana Legislature begins on April 10, 2023. In odd numbered years, Regular Sessions are what we refer to as a “fiscal” session with there being a limit to the number of bills of general jurisdiction and a much shorter time frame. Each Legislators is allowed to pre-file 5 bills of general jurisdiction and as many fiscal bills as they want. Once the pre-filing period has ended on March 31, 2023, Legislators are allowed to file up to five additional fiscal bills during the first ten days of the session. Fiscal Sessions are also shorter. The Legislature convenes on the second Monday in April and can meet for no more than 60 calendar days and not more than 45 legislative days. And must end on June 8, 2023.

David Tatman, The Tatman Group

David Tatman, The Tatman Group

March 2023

The 2023 Regular Session will not be without controversy. As many of you already know, we have a property insurance crisis in Louisiana. Your team at the IIABL is heavily involved in that conversations. There will also be several other bills that will draw crowds to the Louisiana State Capitol. Here are just a few:

Guest Contributor

CONTROVERSIALBILLS

Fish or Cut Bait

You have heard the saying before, but that will be the basis around the bill to limit menhaden off of Louisiana’s coast. The menhaden (Pogey) industry in Louisiana is the largest industrial fishery in Louisiana.

Oil and Gas

Carbon Capture will stir up some controversy from environmental groups as the oil and gas industry pushes for Louisiana to lead the way in what could turn out to be a new resource for the state.

To Pay or not to Pay

There will be a stout discussion on legislative pay raises. The legislature will debate tripling the current salary $60,000 per year. Teachers will also be in line for another pay raise. Odds are that they will get a raise, the question will be, how much!

Smoke em’ if you got em’

Or maybe chew them? Hemp, Kratom, Delta 8 & 9 will all be discussed during the legislative session. There has been an explosion of products on the market that get you stoned and are sold over the counter. Emotions will be “high” during this debate!

Rolling in dough

The State of Louisiana is flush with cash. So much so that legislative leaders will likely have to pass a resolution to exceed the current spending cap. The Senate is more likely to pass that resolution which needs a two-thirds vote (27 Senators). The House is a much different story. There will be plenty of politics surrounding this issue.

It's important to keep in mind that the entire legislature and all statewide elected officials will be up for election or re-election this fall. The potential political overtones of the session may and likely will become campaign issues. There will be less turnover than in previous years in the legislature since there are fewer open seats this term. Most of the action is going to occur at the

Continued from page 11

statewide level. We will have a new Governor, Attorney General, Treasurer and Insurance Commissioner. With those changes, we will likely see new faces in most state agencies. The learning curve will be steep. There will also be a new Speaker of the House and President of the Senate as both leaders are at the end of their term limits. Expect election year posturing to work its way into the legislative process.

Stay informed on all legislative activity, it will be important. Louisiana has one of the best legislative web portals in the country www.legis.la.gov. It will be particularly important to keep up on all of your Big I news. As a new feature this year, our firm is hosting a podcast which focuses on legislative and elections activity. You can follow us on Social Media @thepelicanbrief225. We are all the major podcasting platforms and on YouTube. Tune in for regular updates.

LOUISIANAAGENT PAGE 12

WHY LOUISIANA HAS A PROPERTY INSURANCE CRISIS

There are four reasons Louisiana has a property insurance crisis.

Historic hurricane losses which has caused insurers to be very unprofitable.

Historic reinsurance losses worldwide which has reduced reinsurance capacity.

The size and structure of our economy presents high risk and low opportunity.

Years of Louisiana legislation, regulation, and litigation hostile to insurers.

We cannot manage hurricanes, reinsurance markets, or the economy of our state.

But we can manage legislation, regulation, and litigation.

Louisiana has a separate committee in the Legislature dedicated to insurance, which passes many bills every year, and has resulted in a massive Insurance Code that mandates how insurers manage every aspect of their business. In the interest of “protecting policyholders” legislators restrict how insurers manage their business and control the prices admitted insurers can charge. The result is that many insurers who operate in other coastal states do not offer coverage in Louisiana.

Insurers find the Louisiana Department of Insurance (LDI) difficult to deal with. Rather than acting as a resource to help insurers do business in Louisiana, they tightly regulate industry practices and try to control premium costs. Insurers that cannot operate the same way they do in other states and cannot charge the premiums they think are necessary to pay their claims and make a profit don’t do business in Louisiana.

Our litigation problems showed up first in automobile insurance where we claim to be hurt in auto accidents twice as much as the national average. The TV and billboard lawyers have convinced most people that if you “ are in a wreck, get a check.” After Hurricanes Laura, Delta, Zeta and Ida, the amount of litigation on property insurance claims soared to historic levels. Excessive litigation is a problem in all lines of insurance.

The bottom line is that Louisiana is a difficult and frequently unprofitable place to sell insurance, and we have made it more difficult by trying to legislate, regulate and litigate insurers into submission. The result is that we do not have enough insurers doing business in Louisiana. This crisis in availability has caused a crisis in affordability.

J e f f A l b r i g h t 2 8 M a

c h 2 0 2 3

r

1.

2. 3. 4.

PROPERTYINSURANCE

The solution to our insurance crisis is to reform our legislation, regulation, and litigation to make Louisiana an attractive place for insurers to write business. Only a healthy, competitive insurance market can make insurance available and affordable.

We need insurers more than they need us

It is up to us to make Louisiana a place they want to insure.

Continued from page 14

PAGE 15

LOUISIANAAGENT

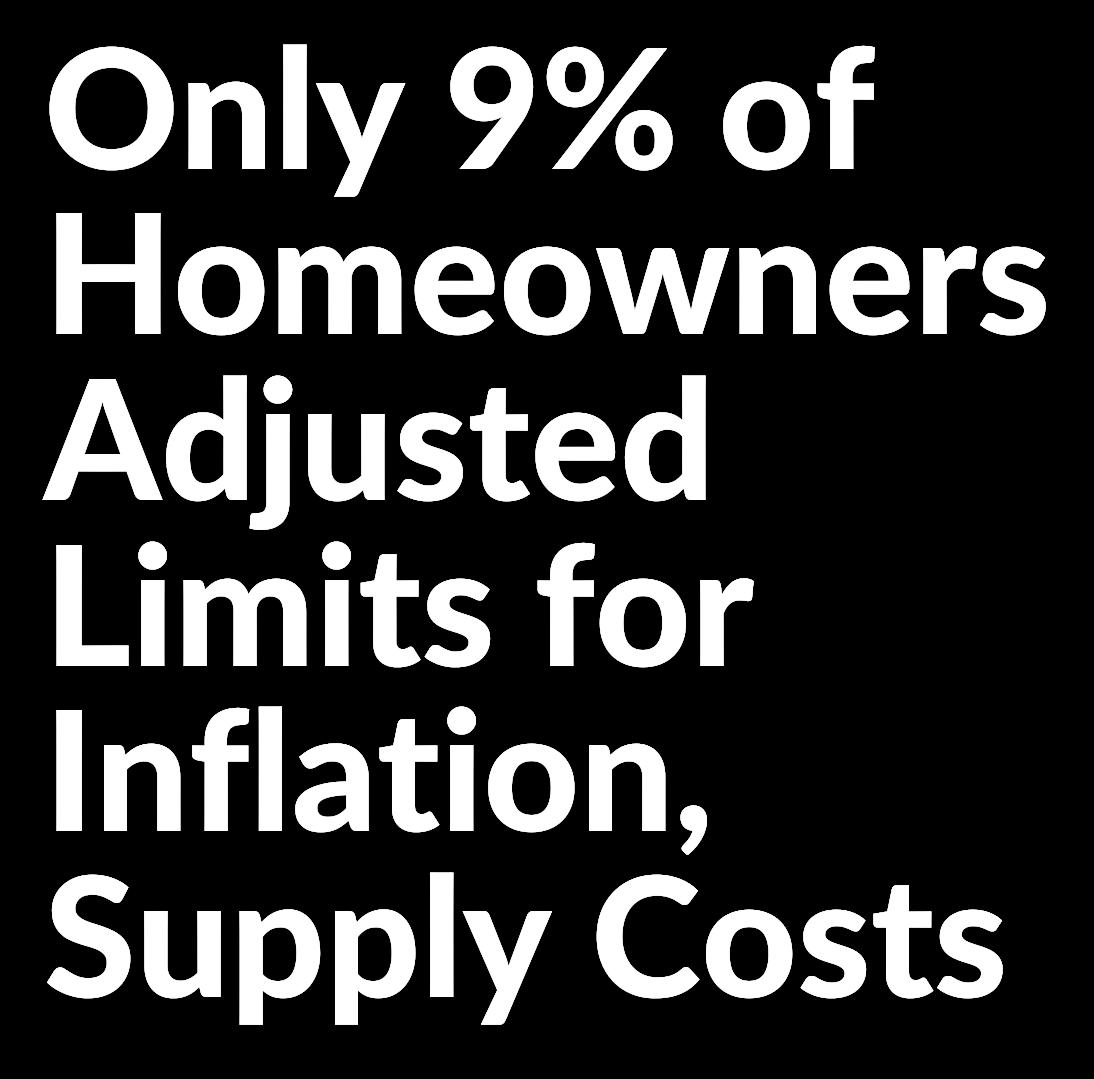

Despite 40-year-high inflation rates and record home construction costs in 2022, more than half of U.S. homeowners haven't even checked whether their insurance coverage is keeping up, according to Policygenius' “Home Insurance & Inflation Shopping Survey."

While construction costs on single-family homes were up nearly 17% in 2022, according to the U.S. Census Bureau, 56% of homeowners have not reviewed their homeowners policy in the last year to see how much coverage they had, Policygenius reported. And only 9% of surveyed homeowners increased their home's coverage limit in the last year to account for rising construction costs and inflation.

Most homeowners are a bit shaky about whether they have enough insurance to cover their home. Only 1 in 3 homeowners claimed to be “ very sure" their homeowners coverage limit is high enough to cover their home's entire rebuild cost. Additionally, 83% of homeowners either don't have or aren't sure if they have inflation guard coverage to automatically increase their coverage each year to keep up with inflation.

This may come as a shock, but homeowners who proactively checked their policies last year were more certain of where they stand. Forty-five percent of homeowners who reviewed their policy were very sure their house was fully insured, compared to only 24% of those who didn't check.

And 2 in 3 homeowners who reviewed their policy knew they had either guaranteed replacement cost coverage or extended replacement cost coverage, with 20% still unsure whether they had either coverage and 12% not having either. But among homeowners who hadn't checked their insurance in the last year, 42% did not have either guaranteed or extended replacement cost coverage, with 44% being unsure and 15% not having either.

Those who reviewed their coverage were much more likely to increase their limits or have at least one coverage feature in their policy that accounts for high rebuild costs. Of homeowners who did check their coverage, 22% either increased their coverage limits or added a new coverage feature.

LOUISIANAAGENT PAGE 16

Annemarie Mchperson Spears

IA News Editor

ADJUSTINGLIMITS

However, those who checked were also more likely to take action to lower their insurance costs. They were more likely to get rid of coverage features they no longer felt they needed (7% versus 3%), increase their homeowners deductible (5% versus 2%) and bundle their home and auto policies (14% versus 10%).

Cost-saving actions were the most common among homeowners ages 18 to 34, who were also nearly twice as likely as other age groups to switch insurers for cheaper rates, at 31% compared to 13% for 35-to-54-year-olds and 7% for those over the age of 55. Additionally, 14% of 18-to-34-yearold respondents said they got rid of extra coverage features they didn't need to lower their costs, compared to only 3% of homeowners ages 35-54 and 3% of those over 55.

Continued from page 16

LOUISIANAAGENT PAGE 17

The insurance and surety markets both provide for an assumption of risk and protection in exchange for payment. And while they both provide a risk transfer mechanism, surety bonds are defined as “providing financial protection to businesses, families, and consumers by guaranteeing contractual obligations are met through the securement of a bond," according to the Surety and Fidelity Association of America.

However, while “most agents have some familiarity with bid bonds, performance and payment bonds, and license and permit bonds, unfortunately, there are many types of bonds that people are not aware of," says Jack Anderson, president, Goldleaf Surety Services LLC.

S U R E T Y B O N D S : A R E I N D E P E N D E N T A G E N T S L E A V I N G M O N E Y O N T H E T A B L E ?

Each type of bond can be tailored to the specific needs of either the issuer or investors, creating an opportunity for agents to offer more protection to their clients.

According to Anderson, here are five types of bonds that agents can write but many don't, which means agents are leaving money on the table:

1) Supply bonds.

Guarantees that the material equipment ordered by the owner will be delivered within the time specified and meets the requirements of the purchase order.

O l i v i a O v e r m a n

SURETYBONDS

2) Financial guaranty bonds.

Guarantees that the company fulfills its payment obligations under the agreement.

3) Advance payment bonds.

Guarantees that the owner receives the equipment or materials paid for via the advance payment.

4) Fidelity bonds.

Indemnifies an employer against a financial loss due to the dishonesty of an employee

5) Court bonds.

Guarantees that an individual or organization will fulfill their responsibility ordered by a court.

The world of bonds is vast. Other examples of bonds that agents could offer include any bonds required for contractor clients. “A lot of states and cities or local municipalities require contractor license bonds," says Jeff Cose, senior vice

Continued from page 18

president, head of national bond center, Nationwide.

Also, when it comes to business services bonds, “ a lot of agents just don't know they exist, but if their clients have employees on a premises, this coverage is required to can help protect against any financial liability or from loss of money or property while their employees are on site," Cose says.

But when is the right time for an agent to offer a client surety bond coverage? “Agents already have the main element to sell bonds in place, which is the insurance relationship," Anderson says. “With the existing relationship in place, it is easy to discuss the handling of their surety bonds."

LOUISIANAAGENT PAGE 19

T O P 5 R E A S O N S

A G E N T S L O V E S E L L I N G P U P S

When it comes to a personal umbrella policy from RLI, there's a lot to love. Not only are your clients getting an extra layer of protection over auto, homeowners and other personal insurance policies, they can enjoy peace of mind when the unexpected occurs.

Here are the top five reasons agents love selling RLI PUPs:

Stability in the personal umbrella market. RLI's standalone personal umbrella product was first introduced in 1983 and is written on RLI Insurance Company paper, rated A+ by AM Best.

Competitive pricing. Coverage limits start at $1 million and the average premiums are less than $1,000. In today's litigious society, it's an inexpensive way to for your clients to cover their assets.

Expert, in-house claims handling. RLI's dedicated team has decades of experience in auto and casualty claims handling.

Ease of use. A self-underwriting application and full automation with electronic signature and payment options means you spend less time quoting and more time selling.

Low maintenance. No need to gather declarations pages, exposure schedules or babysit the policy throughout the term. RLI processes limited endorsements and handle the entire renewal process with your clients directly.

Show your clients you care with a personal umbrella policy from RLI. Learn more on the Big “I" Umbrella page.

April Pitz

Big I Personal Umbrella

K E Y N O T E S P E A K E R

JAY

LA Commissioner of Administration

Don't miss his renowned presentation

B

Room Block Deadline: May 16, 2023

(or until the room block is full) DARDENNE

O O K Y O U R H O T E L R E S E R V A T I O N S ! Q U E S T I O N S ? Contact Kathleen O'Regan, IIABL Director of Communications & Events, at 225-236-1360 or

"Why Louisiana Ain't Mississippi"

koregan@iiabl.com

How Taverns Can Avoid Slippery Floors

RMS Hospitality Group

February 15, 2023

Taverns can get slippery, especially when there are many customers and plenty of food and drink involved. Even though bars, pubs & taverns program insurance protects an establishment from general liability, a customer who falls on a slippery floor can still sue the owner for pain and suffering, lost wages, medical bills, and more. Your company might pay for a large claim if a judge decides in the customer’s favor.

TIPS FOR TAVERNS TO FOLLOW

Here are some tips to keep this situation from happening to your clients.

Explain the Bars, Pubs & Taverns Program Insurance Policy to Your Clients

As an insurance agent, you know all about the liabilities of slippery floors in taverns, but your clients may not. Start the conversation by explaining how their insurance depends on making sure their floors are a safe place to walk. If the establishment advertises a karaoke night, paint a vivid picture of the traumatic aftermath of a client slipping and suffering a severe injury while singing on stage.

N O M A D I C | 2 4

TIPSFORTAVERNS

Advise Clients To Choose Cleaning Products Wisely

There are commercial cleaners on the market. Thus, some purchase a brand based on unimportant qualities such as its fragrance or ease of dispensing. The characteristics they need, however, depend on their flooring type. For example, it is acceptable to clean hardwood floors with an oil-based soap, but tile and concrete require a stronger degreasing detergent that won’t leave an oily residue.

Tell Owners To Take Care of Their Mops

The number one weapon to wield against slippery floors is a mop. Once owners choose the most appropriate model for their flooring type, recommend these tips to take care of it:

Clean after every use

Use a mechanical wringer instead of your hands to remove excess water

Launder regularly with a non-beach detergent

Continued from page 22

Allow to air dry or put in the dryer without fabric softener

Store with the mop head in the air, not on the ground or in a bucket

Encourage Safety Training for Employees

Pub owners should instill in workers the importance of customer safety. They should teach all new hires to monitor floors throughout the night and instruct managers to provide constructive feedback on employee performance. Suggest periodic safety refresher classes as a form of professional development. Businesses could also offer money or other incentives to those who spot and clean up spills the fastest.

Alert Clients to Any Changes in Their Bars, Pubs & Taverns Program Insurance Policies

Be sure to review your client’s taverns program insurance policy regularly. Terms can change

LOUISIANAAGENT PAGE 23

TIPSFORTAVE

periodically, so it is cruc on current requirement until someone slips on a learn that they don’t hav thought they did.

Bars, pubs & taverns pro safety net to protect peo only works if they do the environment. While it is accidents from occurrin keep your clients from f claims. By maintaining c will decrease the chance their policies.

About RMS Hospita

At RMS Hospitality Gro policies are written spec industry. We offer custo meet any venue’s specif information, contact our today at (888) 359-8390

If you would like to read an online version of this blog, click here.

PAGE 24

CATASTROPHE CLAIMS PROCESS DISCLOSURE FORM-GUIDE

Louisiana Department of Insurance Regulation 124

The Louisiana Department of Insurance (LDI) promulgated Regulation 124 to implement the provisions of Acts 2022, No. 80 of the Regular Session of the Louisiana Legislature, which mandates that the Department promulgate rules and regulations for a catastrophe claims process disclosure form-guide.

Regulation 124 applies to all property and casualty insurers settling a property insurance claim arising out of a state of emergency declared by the governor.

Whenever a state of emergency is declared by the governor, an insurer must provide a disclosure form-guide to all policyholders asserting a claim for damages caused by the disaster or catastrophic event made the subject of the governor’s emergency declaration.

The disclosure form-guide was created by the department and issued to all property and casualty insurers licensed in this state.

The disclosure form-guide has been uploaded to the department’s website HERE, at www.ldi.la.gov, and insurers are authorized to access and download it as needed to comply with Regulation 124 and with the statutory requirements set forth in R S 22:1897

The insurer shall send the disclosure form-guide to the policyholder on the date that they adjuster begins and initial investigation of the claim. The insurer may deliver the disclosure form-guide to the policyholder and appropriate proof of timely delivery must be maintained by the insurer:

FORMGUIDE

United States mail: proof of such mailing shall be sufficient evidence to establish delivery of the disclosure form-guide, provided it reflects the date of the mailing and the policyholder.

Electronic delivery: email delivery receipt or, if none, a copy of the as-sent email, shall be sufficient evidence.

Hand-delivery: the insurer must complete and sign a Certificate of Hand-Delivery, verifying pertinent details related to the delivery of the disclosure form-guide, including the date and location of the delivery, and the name of the policy holder.(see Certificate of Hand-Delivery from LDI HERE)

Regulation 124 shall become effective immediately upon publication (March 20, 2023).

View Regulation 124 here.

Continued from page 25

Although Regulation 124 applies to insurers not insurance agents, agents can use the disclosure guide as educational materials to help their customers deal with catastrophe claims.

LOUISIANAAGENT PAGE 26

1.

2.

3.

GiaSnape 24Feb2023

Cyber risks are evolving beyond the confines of traditional underwriting techniques, and the industry must embrace a new approach that involves proactive, ongoing risk assessment.

“When cyber [risk] started to grow 10 years ago, it was underwritten like a traditional specialty insurance coverage application,” said Brian Alva (pictured), SVP of cyber underwriting at Corvus Insurance, a Boston-based commercial insurance platform with footprints in the UK, Canada, Australia, and the Middle East

“At the time, that was probably sufficient, but as exposure started to grow and we saw an explosion of ransomware and additional cybercrime techniques, people realized that ‘snapshot-in-time’ approach doesn't work for cyber ”

The old application-based practices of commercial insurance – where companies tick off “yes” or “no”

boxes to questions – is no longer an adequate way to get a holistic view of a company’s cybersecurity posture, Alva argued.

“In theory, that's great. But in practice those questions shouldn't always have a yes or no answer. But there's always going to be a lot of gray areas,” he told Insurance Business.

“You’re answering questions that might be true today but might not be true tomorrow as you as your network and change security controls ”

How is cyber underwriting evolving?

Data, artificial intelligence, and machine learning have had a profound impact on cyber underwriting in recent years, according to Alva.

“As we've been able to collect and analyze various forms of data, using different AI and machine

CHAOTICCYBER

learning models helps us start to build profiles of clients as well to predict the probability of claims,” he said.

“Using new forms of data using these new models, we're able to get a much better picture of a company's exposure profile than we were a couple of years ago.”

The most significant change that data has brought is to enable underwriters to quickly adapt as an insured’s cyber exposure shifts within a policy period. Data can deliver ongoing insights so that at renewal time, carriers don’t need to ask as many questions as they did in the policy year before.

Claims data are also becoming less relevant to the cyber underwriting approach. While such data can help inform future decision-making, the biggest threats last year or a few months ago may not be the same today, Alva emphasized.

“One of the interesting things about cyber is that it has evolved so quickly that the trends we see today are different from the trends we saw we saw five or six years ago,” the SVP said.

“While the additional claims data is certainly helpful and something that we build into our modeling, we have to be careful not to let past claims bias determine too much of what we're looking at in the future.”

For example, eight years ago, the most significant concern in cyber insurance was data breaches around credit cards. But this threat has ebbed with the adoption of better chip technology and encrypted payment information in the retail space.

“The tide instead turned to ransomware and cybercrime,” Alva said. “While we do pay attention to past claims data, we also want to be mindful that the exposures of tomorrow are not necessarily going to be the exposure as yesterday.”

Finally, underwriters are working more closely with cyber experts to look at and price risk from the inside-out.

PAGE 28

CHAOTICCYBER

“At Corvus, we have a handful of staff who are threat intel specialists who can monitor the dark web to spot emerging trends. We then use that information to inform our underwriting,” said Alva.

What can we expect from cyber market in 2023?

The past few years saw the cyber insurance market hardening significantly amid heightening ransomware and cyberattacks on organizations. While rates have stabilized in recent months, Alva said the market has diverged some aspects.

“I think [the cyber market] is a bit chaotic, if I'm being honest,” Alva told Insurance Business. “We’re seeing a lot of divergence among insurers. Some are moving to soft market tendencies, while others are trying to get more rate. There seems to be a different view of exposure within the market itself.”

The lack of consensus also reflects other threats in the market, such as evolving exposures in the regulatory landscape and several class-action lawsuits around data privacy, according to Alva.

“I think we'll continue to see different reactions from various markets on these newer trends,” he said.

PAGE 29

6 UNDERRATED MARKETING TACTICS TO GIVE YOUR INSURANCE AGENCY AN EDGE

As an independent insurance agent, you've had to adopt a handful of general digital marketing strategies to grow your business and stay competitive in this digital era. From creating a professional website that acts as the foundation of your digital presence to building an email list for a targeted newsletter and promotional emails, it's become more of a task than a strategy

Other marketing tactics can include running paid advertising on Google Ads and Facebook (Meta) Ads Manager, while also generating blog posts for some search engine optimization juice as part of your content marketing strategy

However, there are many other, less common digital marketing strategies that you can utilize to reach new prospects and grow your independent agency. Here are six examples:

1) Quora marketing.

Quora is a popular, free question-and-answer website where people can ask and answer questions on a wide range of topics. As an independent agent, you can use Quora to establish yourself as an expert in your field by answering questions related to personal or commercial lines insurance.

By providing helpful and insightful answers, you can build trust with prospective customers and drive direct traffic to your website via referral and search visits. It takes less than five minutes to get started and begin answering questions immediately related to insurance.

You can also search for questions related to your niche and provide helpful answers. Be sure to include a link to your agency website in your

Sachin Rustagi

AGENCYEDGE

profile and answers to drive relevant traffic and generate leads.

2) Referral marketing 2.0.

Referral marketing is one of the oldest sales channels and predates the digital economy. Just adding a few simple tweaks to your existing “always-on" referral program can provide a significant sales boost.

Encouraging satisfied customers to refer their friends and family by offering rewards or discounts is definitely a first step. As a second step, you can create partnerships with cross-industry experts from non-competing verticals and horizontal industries, such as life insurance or financial wealth brokers, where you can exchange leads.

A third step would be to customize your program. For your most loyal insureds that refer their family members, offer them a double referral bonus. This will ensure you get trusted and serious leads from a channel that usually has the highest conversion rate among other marketing channels.

3) Influencer marketing.

Influencer marketing is often overlooked in the insurance industry and involves partnering with social media influencers who have large followings and can promote your products to their audience. As agents, you can partner with influencers who have a strong presence in your target market, such as experts in the home buying and investment space or partner with a popular home design influencer to promote your homeowner's insurance products

Getting started is pretty straightforward for big deals you can work through fee-based social media influencer marketplaces, but the easier method is to research social media influencers in your niche For example, target small- or mid-size companies and reach out to them to see if they can promote professional liability insurance.

Continued from page 30

Be sure to choose influencers who have a strong presence in your local geographic market and align with your business values.

4) Podcast advertising.

Podcasts have become increasingly popular in recent years and they can be a great new way to reach potential customers. You can advertise on relevant podcasts by sponsoring episodes or running ads. For example, if you sell auto insurance, you could advertise on a popular automotive podcast.

To get started with podcast advertising, research podcasts in your niche and reach out to them with a sponsorship proposal. A challenge to be cognizant of with podcast advertising is focusing on local prospects against a more global audience. Although geographic targeting can be done, it is sometimes hard to find enough regional volume to make it feasible or sustainable.

PAGE 31 LOUISIANAAGENT

AGENCYEDGE

5) Educational webinars.

After spending thousands of hours on Microsoft teams and Zoom during the coronavirus pandemic for client and work-related meetings, video conferencing has become second nature. So, it's no surprise that webinars could be a natural effort for many agents.

Webinars are online events where you can provide valuable information to potential customers about the insurance & risk services you provide. Your agency could host a webinar on a hot topic, such as how to choose the right errors & omission policy or what directors & officers coverages are a must. By providing valuable information, you can establish yourself as an expert in your field and attract potential customers.

Continued from page 31

6) Localized SEO.

While SEO is a mature and well-known digital marketing strategy, local SEO is often overlooked. Local SEO involves optimizing your website and digital content to rank higher in local search engine results. You can optimize your agency website for local insurance and risk-related keywords and phrases, such as "home and office insurance in [your city]" or "auto insurance near me." This can help you attract potential customers in your local area, especially if your agency is hyper-targeted in one specific region or city.

To get started, research keywords and phrases that are relevant to your insurance markets and products and include them in your website content, meta descriptions and title tags. You can also create location-specific landing pages and

PAGE 32 LOUISIANAAGENT

AGENCYEDGE

include your business name, address, and phone number on your website to improve your local search rankings.

Regularly monitoring and analyzing your digital performance when leveraging these—or any— digital marketing strategies can help you identify what's working and what's not, allowing you to adjust your strategies accordingly. Start by using free web analytics tools like Google Analytics to track your website traffic, social media engagement and advertising performance.

Lastly, it's good to remember digital strategies and marketing tactics are constantly evolving, and it's essential to stay up to date with the latest trends. By investing time and resources into your digital marketing efforts, you can differentiate

Continued from page 32

yourself from competitors, build a strong brand, and ultimately grow your book of business.

LOUISIANAAGENT PAGE 33

Sachin Rustagi is head of digital at Markel International (Canada).

THE OFFICE IS BACK, BUT IT'S NOT THE SAME

I was struck recently by a conversation among several of my friends, all peers in different industries, about work.

“I know this might be an unpopular opinion,” one lawyer was saying, “but I don’t want to work from home all the time.”

“Me neither,” agreed a marketing and public relations executive. “I actually want to put on pants and interact with people in real life.”

“I hear you. Too much Zoom is making me depressed,” said another attorney

“I’ve been trying to up my in-person days from two to three per week!” laughed our friend who works in city government.

Apparently, they’re not alone According to a new article published by Korn Ferry, people are returning to their pre-pandemic work habits and routines in droves.

But there’s a problem. After three years of mostly virtual work and online-only interactions, both

workers and employers are trying to figure out how much should be office time and how much remote work time. They are also out of practice when it comes to many of the in-person things we used to do, from networking to business travel to building corporate culture. In essence, we’re rusty and figuring out the how-to dos in a new hybrid world

“It’s as if we were in jail, and now we’re all free again,” one staffing executive told Korn Ferry.

This is spurring an “intense” rethinking about how to maintain culture and manage a hybrid workforce where a percentage of staff will be in the office full-time, some three or four days a week and some fully remote to meet the needs of employers and their employees. A recent Korn Ferry article notes that we are all collectively struggling with rebuilding our corporate cultures post-pandemic. Roughly 40% of CEOs today say they are dissatisfied with their work environment, according to a survey by Work Forum.

In fact, experts told Korn Ferry that many of the conversations they’re having around jobs and work

Sharon Emek, PhD, CIC CEO & President Work At Home Vintage Experts

WORKHABITS&ROUTINES

hours are now more open and franker about the needs of the business to be successful as well as the quality of life and work success needs of the employees Expect this to continue, as it often results in deeper, more meaningful relationships and better cultural fits between employee and employer.

A major struggle employers now face is how to balance the needs of younger workers that are on a career path to have mentors with the needs of more experienced workers with families who prefer a hybrid work schedule. Having different work arrangements becomes a challenge to maintaining culture and to convincing employees that no matter their work schedule, all are treated with the same care.It shouldn’t matter whether you’re in the office or working remotely: You’re treated the same, with the same opportunities.

Messaging should capture your company values and be consistent across the board, from the initial recruiting efforts through to employment and

Continued from page 34

promotion. And keep in mind that while consistency in the messaging is key—after all, your company values don’t change the mediums through which the values are communicated should adapt to the audience For example, a semiopen floor plan and open-door policy can communicate transparency for those in the office, and daily video Team or Zoom calls with and from remote working colleagues instead of emails can do the same for remote workers.

It then is up to each company’s leadership to model these behaviors, and to “walk the walk,” to solidify and authenticate the corporate culture and to make all employees feel part of the team..

Ultimately, it seems that we are all ready to embrace the hybrid workplace that has been heralded as the way of the future when it comes to work. How, and how well, we do that is up to us.

LOUISIANAAGENT PAGE 35

09 march 2023

In my daily conversations with executives, I hear about their challenges as they confront a rapidly shifting landscape while managing their most important resource: people. Without people, widgets don’t get made, services don’t get delivered and businesses do not run.

Retaining top talent is critical as companies and leaders work through how to achieve commercial goals for the year ahead and beyond. In fact, one result of the tight U.S. labor market is that employees have demanded more empathetic leadership and are getting it. I see in my own coaching work a notable uptick in requests to work on developing more humane leaders and helping them to create workplace cultures that are better at listening and responding to their people.

When leading, it’s important to understand what makes them tick. One size does not fit all when it comes to the individuals who make up your organization. Thus, we must invest the time and attention to develop a deeper understanding of what our employees need most not only to do their jobs well, but to thrive and to drive the business forward.

Mary Olson-Menzel

Mary Olson-Menzel is the founder and CEO of MVP Executive Development and co-founder of Spark Insight Coaching.

Mary Olson-Menzel

Mary Olson-Menzel is the founder and CEO of MVP Executive Development and co-founder of Spark Insight Coaching.

WORKCULTURE

So far this year, three people-related themes have emerged as preoccupations among my corporate clients: the ongoing need for flexibility, reimagining meetings and building more tangible corporate cultures. Here are some suggestions for how to tackle these challenges in your own organizations.

Flex first

Many employees have proven that they can be equally if not more productive working from home. Yet, at the same time, they miss the day-to-day interactions and camaraderie developed when working alongside one another in the same location. As a result, more and more of our clients have designed hybrid work weeks so that employees can enjoy the best of both worlds.

However, to make a hybrid schedule operate seamlessly, parameters and clear expectations need to be set in advance. Best practices from my experience as an executive recruiter, coach and operational consultant include:

Continued from page 36

Involve employees in hybrid work model development so they have a stake in the outcome and are invested in the success of the group as a whole.

Understand that some employees have roles that require them to work onsite. Make sure that the new rules consider their situation and are equitable.

Accept that hybrid work requires more coordination and set clear communication parameters for both management and staff. Provide technology and tech support that helps employees perform efficiently and effectively from wherever they are working.

Meeting mania

The second recurring theme is meetings their frequency, structure, and length. “Too many meetings!” We hear this every day, even among the best-performing hybrid teams. Post-pandemic Zoom marathons are the norm now and there’s no time left to address actual deliverables.

PAGE 37 LOUISIANAAGENT

WORKCULTURE

In a recent study conducted at Microsoft, researchers confirmed exactly what we are talking about: Back-to-back virtual meetings are stressful, and long-term detrimental to brain health. The findings also support our simple remedy: take short breaks. “Our research shows breaks are important, not just to make us less exhausted by the end of the day, but to actually improve our ability to focus and engage while in those meetings,” says Michael Bohan, senior director of Microsoft’s Human Factors Engineering group, who oversaw the project.

So, how do you keep others engaged when you might be catching them preoccupied or at the end of their work day? Step one is to know your audience. As you review your calendar, ask yourself who you are meeting with, what their priorities are, and how they best receive and process information. Second, get creative about the structure and length of your meetings. Do you really need to have a 30-minute meeting or will 15

Continued from page 37

suffice? Have you tried having a standing meeting? They tend to wrap quickly and keep everyone more focused. Meeting agendas, talking points, and templates also help to facilitate and move the conversation along to a productive outcome.

Cultivate culture

Organizational culture is the shared values, beliefs, and practices of an organization. It’s how members of an organization view their work, their colleagues, and themselves. A sense of community and the feeling of belonging are vital in the workplace. Culture is what motivates your people to come to work (to an office or via a screen) and it’s why people will stay at an organization.

Is your internal employee brand as strong as your external brand? Are you, your executives, and your staff living in the core values of the organization? A simple cultural assessment can really shed light on this question.

Culture is ever-changing and shifting and we want to make sure we are creating a culture of acceptance, equality, and performance in order to shift as the workforce needs are shifting. What was considered a great culture in 1990 might not be considered a great culture now. Therefore, we must constantly strive to create a culture of excellence in whatever business we are in.

A suggested group exercise with a few questions that my colleague, Mel Shahbazian, and I ask when creating a leadership signature and creating a culture of excellence starts with alignment of the following:

What is your North Star: Think of this as your top leadership declaration. What is the essence of who you are as a leader and as an organization?

What is your Mission: Your mission should be bigpicture, long-term and meaningful. Something that people can imagine and hold on to.

PAGE 38 LOUISIANAAGENT

WORKCULTURE

What is your Goal: This is more benchmark oriented, less about values, and more about the bottom line Actionable and trackable

What is your Values Proposition: Prioritize the top values that you hold dearest in your role and on your team. What lights you up?

What is your Promise: What is the promise you offer to your employees and your clients/customers?

What is your Mantra: What do you say to yourself and your team every day to ensure that your culture and your words are inspiring?

Continued from page 38

According to Simon Sinek: “A culture is not invented. A culture constantly evolves … which is why it must be nurtured.”

Nurturing a culture is not only from the top down, it can be driven also from all levels of the organization Learning from one another and taking best practices from top-performing employees can be helpful in creating a winning culture.

PAGE 39

LOUISIANAAGENT

WHAT ARE CLAIM-IT REFERRALS?

Claim-it Referrals are high-quality, exclusive, digital insurance referrals from prospects actively seeking an agent. Here's how they work.

The Claim-It Referral program continues to grow at a great rate. In just the past few months we have had more than 13,000 online insurance prospects enter the Claim-It pool. Producer availability continues to be a challenge and many of these leads are going unclaimed In effort to create a better user experience, and create opportunities for your agents, TrustedChoice.com is proactively reaching out to eligible agents to encourage them to sign up to receive Claim-it notifications.

29 Jan 2020

Currently, any agent that has an Advantage Professional subscription is eligible to participate in the program. Many agents are not aware that they have this opportunity!

Claim-it® Referrals included with Advantage Professional are high-intent, appetite-matching, exclusive, inbound opportunities from insurance buyers actively searching for an independent agent to work with. Here’s how you can start claiming the insurance industry’s hottest referrals.

CLAIM-ITREFERRALS

So how does Claim-it work?

When an agent is onboarded for Claim-it, we ensure they are signed up to receive notifications by text or email when a Claim-it Referral matching their unique business appetite in their area rolls in. To help them determine whether a referral is a good match for their appetite, each notification allows agents a glimpse at the Claim-it Referral information. Agents will see a brief rundown on the referral, like:

Continued from page 40

referral or see the referral information. Think of Claim-it like the Uber of the insurance industry. An online insurance prospect in your area.

Why should I become a Claim-it agent?

Our Claim-it program is growing at an exponential rate, and you can get in front of the more than 13,000 online insurance prospects who have entered the Claim-it pool in just the past few months. See the numbers for yourself in the graph below:

By clicking the link in the notification, the agent is redirected to TrustedChoice.com, where they can purchase a Claim-it Referral for a nominal fee. Claim-it Referrals are exclusive. Once a referral is purchased, no other agent can compete for the

Each Claim-it Referral is carefully curated to suit your business appetite and get you connected with interested, real-time prospects who are waiting to speak with an agent. In fact, our current Claim-it producers report a 50%-60% closing rate on average with Claim-it Referrals.

Pricing & Signing Up

ll Advantage Professional subscribers are able to access Claim-it Referrals With our Claim-it feature, you can connect instantly with real people who have real insurance needs

Pricing is as follows:

Life & Annuities – $10

Personal Lines – $17

Commercial Lines – $24

To Sign up to Receive Claim-it Referrals:

With an Advantage Professional subscription, signing up to receive Claim-it Referrals only takes 30 seconds of your time at no additional cost to you. Sign up for Claim-it Referral notifications here.

Line of business Insurance type Location And more

A

PAGE 41 LOUISIANAAGENT

The ability to adapt quickly to change is not only a virtue in life, but also a tenet of any good business. As agents know oh-sowell, the insurance industry is changing rapidly and so are the needs of independent agents. IIABL recognized many of these trends early on and strategically invested in Independent Market Solutions (IMS).IMS provides markets to agencies with the goal of perpetuating the independent agency system, especially for small and rural agencies that can sometimes struggle to keep markets. It also works to solve problems when markets are distressed or the need for new specialty or niche markets arises.

Because IMS takes a broad approach to market access, it means any member agency, whether a start-up or a mid-tolarge sized, can take advantage of the greater efficiencies through scale, enhanced insurance company-agency relationships, and competitive terms the program offers. Thanks to the partnership among several state associations through IMS, the program creates greater volume, leverage, and, ultimately, better terms for IMS sub-producers.

As the industry evolves, the menu of product offerings at IMS continues to expand to provide a robust market access alternative for our members with no strings attached. To get started with IMS, click here.

LOUISIANAAGENT

UPCOMINGEVENTS

Event Date Location Registration IIABL Young Agent Crawfish Boil April 20 Lakeside Daiquiri & Grill Baton Rouge, LA Coming soon! IIAGNO Golf Tournament May 12 Audubon Golf Club New Orleans, LA Coming soon! IIASB May Luncheon May 25 The Shreveport Club Shreveport, LA Coming soon! IIABR TopGolf Charity Event May 18 TopGolf Baton Rouge, LA Coming soon! IIABL Annual Convention June 18-21 Hilton Sandestin Miramar Beach, FL Coming soon! IIAGNO Town Hall Meeting Aug 3 Southern Yacht Club New Orleans, LA Coming soon! IIABL & IIAM Young Agents Conference Aug 24-26 Beau Rivage Biloxi, MS Coming soon!

23 SUN MON TUES WED MAR 26 2 9 16 3 10 17 24 4 11 18 25 5 12 19 26 27 28 29

EDUCATION PAGE 44 3 hrs Ethics 2-5p NeedFloodand/or Ethicsthismonth? Checkoutour calendar. AllCEcoursescan befoundonour websiteHERE. 3 hrs Ethics 12-3p 3 hrs Flood 11a-2p 3 hrs Ethics 2-5p 3 hrs Ethics 8-11a 2 hrs Ethics 9-11a 3 hrs Ethics 11a-2p 3 hrs Ethics 1-4p 3 hrs Flood 1-4p 3 hrs Ethics 10a-1p 3 hrs Ethics 3-6p 3 hrs Ethics 8-11a 3 hrs Ethics 11a-2p 3 hrs Ethics 2-5p

CONTINUING

LOUISIANAAGENT APRIL WEBINAR OFFERINGS THURS FRI SAT 6 13 20 27 7 21 28 8 15 22 29 30 31 1 14 3 hrs Ethics 9a-12p 3 hrs Ethics 11a-2p 3 hrs Ethics 9a-12p 3 hrs Ethics 11a-2p 3 hrs Ethics 11a-2p 3 hrs Ethics 1-4p

Accident Fund Ins Company of America Agile Premium Finance Amerisafe AmTrust North America AmWINS Access Insurance Services, LLC Aspera Insurance Services Berkshire Hathaway GUARD Ins Cos Burns & Wilcox, Ltd. Commercial Sector Insurance Brokers EMC Insurance Companies FCCI Insurance Group Forest Insurance Facilities Homebuilders SIF Imperial PFS Iroquois South, Inc. 41 35 26 8 7 38 29 33 24 12 46 42 24 5 19 LOUISIANAAGENT ADVERTISERINDEX PAGE 46 COMPANY PAGE LA Workers Compensation Corporation Lane & Associates, Inc. LCI Workers' Comp Louisiana Restaurant Association (WC) LUBA Workers' Comp National General, An Allstate Company Progressive RISCOM RLI RPS/Risk Placement Services Safepoint Insurance Company Stonetrust Commercial Insurance Co. Summit Consulting, Inc. The Gray Insurance Company UFG Insurance Wright Flood 2 28 43 9 23 31 13 15 32 29 10 39 9 37 17 28 PAGE COMPANY

IIABL 2022-2023

BOARD OF DIRECTORS & OFFICERS

PRESIDENT, MICHAEL SCRIBER

PRESIDENT-ELECT, ARMOND K. SCHWING

SECRETARY-TREASURER, BRET HUGHES

NATIONAL DIRECTOR, JOHNNY BECKMANN, III

PAST PRESIDENT, DONELSON P. STIEL

YOUNG AGENT REPRESENTATIVE, KRYSTAL GATHE

ANN BODKIN-SMITH

MATTHEW DEBLANC

CHRISTY DESOTO

ROB W. EPPERS

MATT GRAHAM

CHRISTOPHER S. HAIK

STUART HARRIS

ROSS HENRY

CHARLES H. LEBLANC

CRAIG MARTEL

LYDIA MCMORRIS

A. EUGENE MONTGOMERY, III

JOE KING MONTGOMERY

HARTWIG "ROBBY" MOSS, IV

ROBERT LOUIS PALMER, JR.

RANDY PERISE

ROBERT G. RIVIERE

ROBERT STONE

Scriber Insurance - Ruston

Schwing Insurance Agency, Inc. - New Iberia

Hughes Insurance Services, Inc - Gonzales

Assured Partners - Metairie

David H. Stiel, Jr. Agency - Franklin

HUB International Gulf South, Ltd. - Baton Rouge

Thomson Smith & Leach Insurance Group - Lafayette

Continental Insurance Services - Marrero

1st Insurance of Marksville - Marksville

Risk Services of Louisiana - Shreveport

Lincoln Agency - Ruston

Higginbotham Insurance - Lafayette

McClure, Bomar & Harris, LLC - Shreveport

Henry Insurance Service, Inc. - Baton Rouge

Bourg Insurance Agency, Inc. - Donaldsonville

Insurance Unlimited of LA, LLC - Lake Charles

Alliant Insurance Services - Baton Rouge

Community Financial Insurance Center, LLC - Monroe

Thomas & Farr Agency, Inc - Monroe

Hartwig Moss Insurance - New Orleans

Insurance Underwriters, Ltd. - Metairie

Blumberg and Associates - Ponchatoula

Riviere Insurance Agency - Thibodaux

Stone Insurance, Inc. - Metairie

LOUISIANAAGENT PAGE 48