GFSC Discussion paper on Sustainable Finance: a response Improving climate risk assessments through public disclosures.

International Sustainability Institute, October 2024

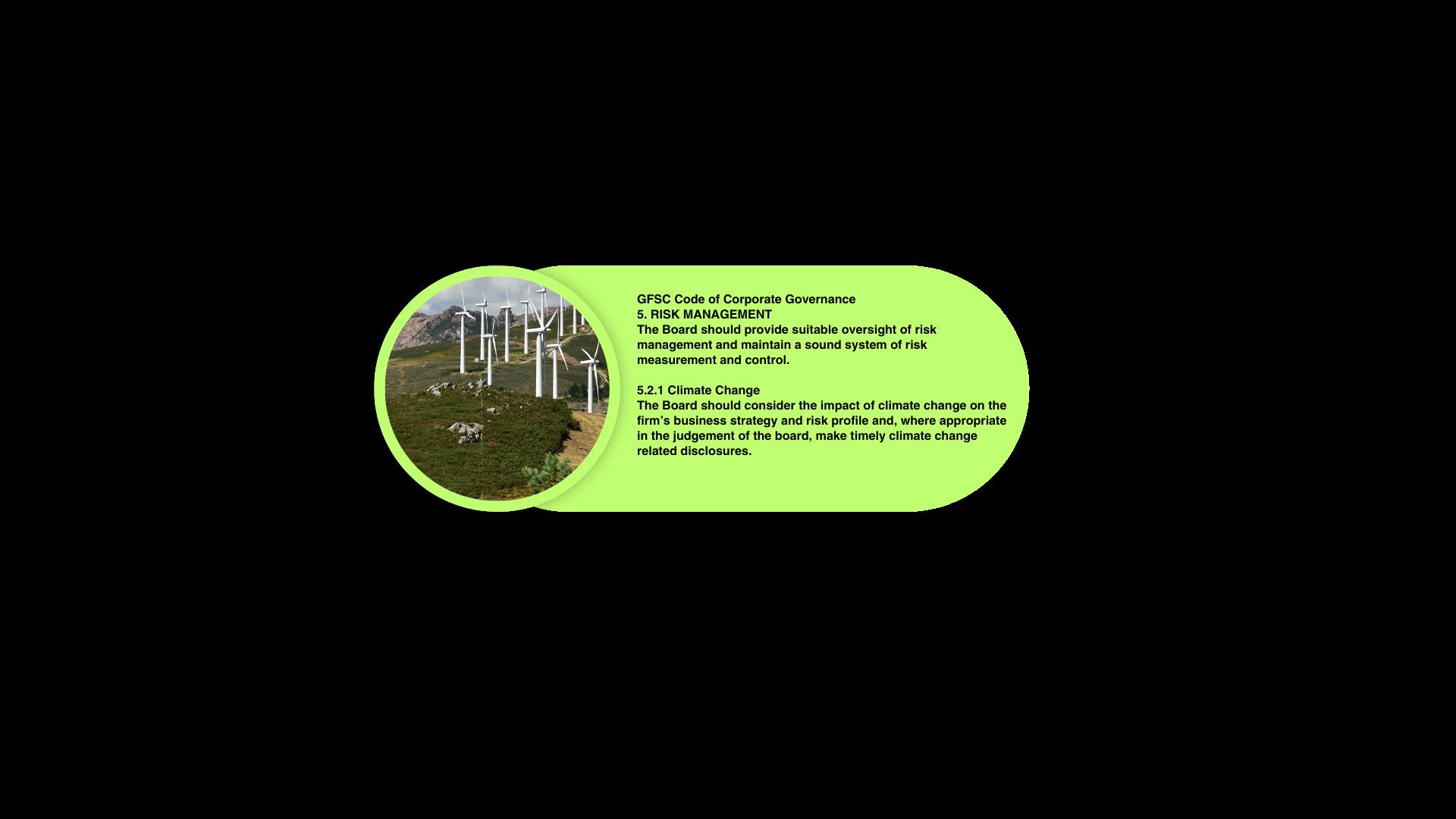

GFSC Code of Corporate Governance

5. RISK MANAGEMENT

The Board should provide suitable oversight of risk management and maintain a sound system of risk measurement and control.

5.2.1

Climate Change

The Board should consider the impact of climate change on the firm’s business strategy and risk profile and, where appropriate in the judgement of the board, make timely climate change related disclosures.

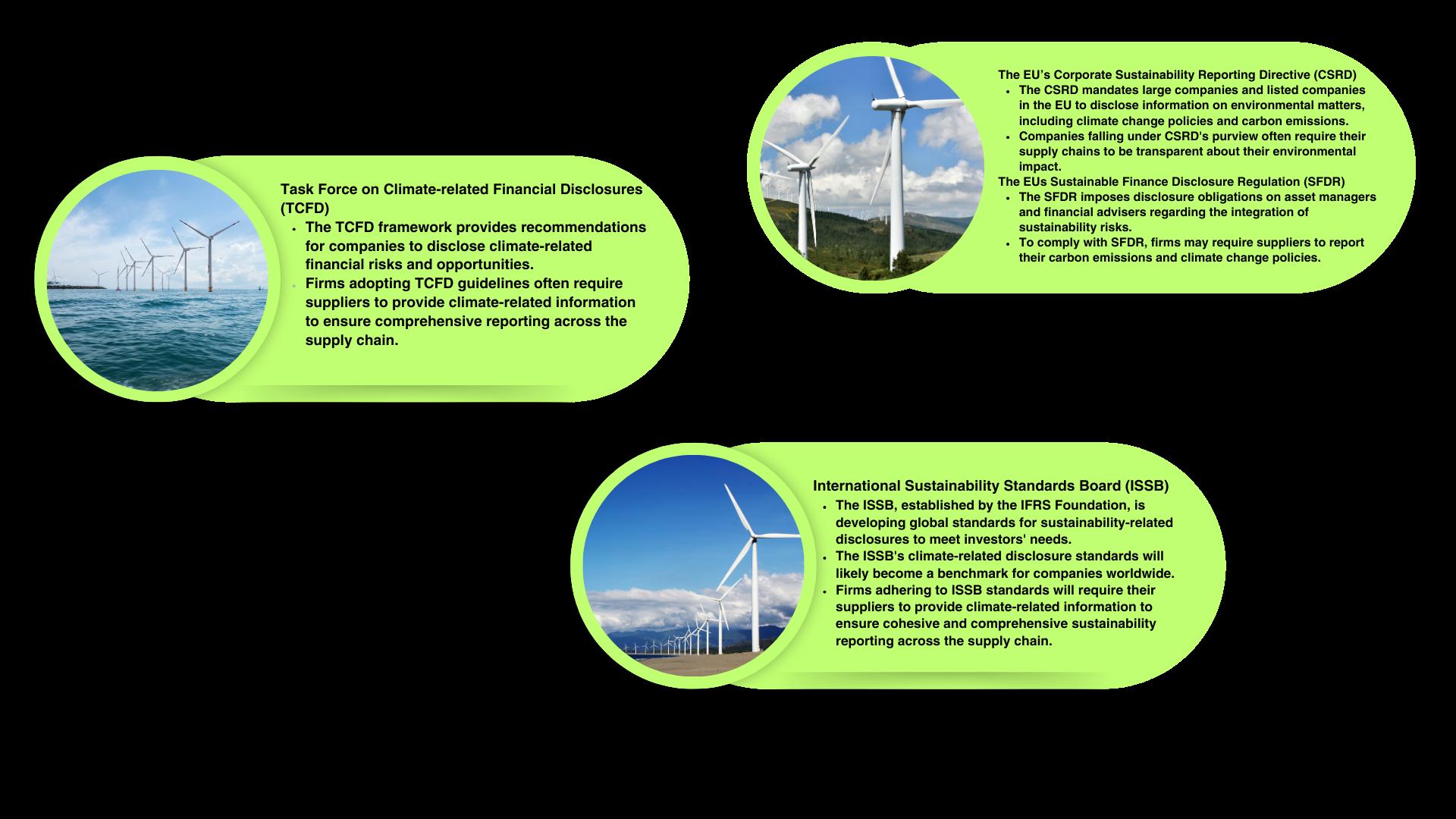

During the summer of 2024, the GFSC invited comments on its discussion paper on sustainability reporting, with the purpose of helping consider what local requirements might be introduced in line with the International Sustainability Standards Board's ('ISSB') reporting standards published in 2023, having introduced a requirement for Boards to consider climate change risk in Guernsey's Code of Corporate Governance ('the Code') three years ago.

The ISSB's sustainability reporting encapsulates more than climate risk but in our view it is climate change that remains the cornerstone of global public policy efforts.

Our analysis is that climate risk reporting in the Channel Islands is still immature and that effort is better directed to improvements in in this area before broadening requirements. For some time, we have been advocating greater levels of public climate disclosures as a route to better climate risk assessments.

Our present experience locally is consistent with the findings of our sustainable finance research of the members of the Group of International Finance Centre Supervisors (GIFCS) last year, when we found a tendency across the offshore centres, for only larger firms to make public climate disclosures and this typically driven by group head offices rather than local management.

We find little evidence of substantive assessment of climate risk amongst local firms and investment boards. One might argue that this matters little for owner managed firms, but where external shareholders or investors are involved, our concern is that too few Directors appreciate the personal liability if assessments of climate risks: physical; transition; liability; financial; regulatory and operational; are not, or are improperly, conducted and such risks materialise.

Transparency is a powerful tool. Public climate disclosures, including emissions disclosures and climate risk assessments, are essential tools for transparency and accountability in achieving net-zero goals. And they are a powerful disciplining mechanism to catalyse and embed thorough risk assessment processes.

The global economy is undergoing a profound transformation, driven by an essential push toward decarbonization. This shift is poised to dominate growth narratives in the 21st century, with net-zero pled covering 93% of global GDP, 88% of emissions, and 89% of the global population. The decarbonization journey globally is shaped by three driving forces: the push of regulation and reporting requirements, the ESG integration for value creation, and the transition as the global economy undergoes one of its biggest shifts.

Large asset owners are setting ambitious climate targets, with US Firm Mercer reporting that two thirds a incorporate sustainability into investment practices and over half having set transition targets. These actio reflect a growing, unavoidable shift toward climate alignment.

However, this global momentum stands in contrast to the slower, more fragmented efforts in the offshore sector, where regulation is not keeping pace with the urgent need for climate action. Our view is that offsh regulations remain insufficient to compel meaningful climate action. While global leaders are embedding sustainability into strategy, many other organizations view regulation and disclosure as mere compliance requirements rather than th f d ti f t f ti h

A failure to act decisively no alienating it from the broade

Climate risk assessment and reporting is not new. TCFD (the Task Force on Climate Related Disclosures) guidance, published in 2017 by the Financial Stability Board, was a seminal development for climate risk reporting in the finance sector. Based on a four-pillar disclosure framework of governance, strategy, risk management, and metrics, it set out clear guidelines for financial firms on how to consider climate risk and suggested formats for the disclosure of such risks to investors and other stakeholders The International Sustainability Standards Board incorporates this framework as the foundation for its global sustainability standards. For some time now, a variety of rules and regulations at both international and national levels ha required firms to consider climate risk and make public disclosures. Many of these regulations necessitate th firms, particularly those operating in regions with stringent environmental policies, require their suppliers to publish statements on climate change and report their carbon emissions The GFSC Code of Corporate

Public climate reports, such as emissions disclosures and climate risk assessments, are essential tools for transparency and accountability in achieving net-zero goals. These reports allow stakeholders, including investors, regulators, and the public, to assess how effectively organizations are managing their climate impact. By setting clear benchmarks, companies are pressured to reduce greenhouse gas emissions and adopt sustainable practices. Transparent reporting also fosters trust and collaboration, driving innovation an enabling regulatory bodies to monitor progress toward national and global climate targets. Ultimately, these reports help align corporate actions with broader net-zero policies.

The Code of Corporate Governance requires firms to consider climate risk and encourages climate reporting Our assessment of the local landscape is that there are few localised public reports, and similarly there are few local commitments to net-zero*. What reports and committments there are originate from group reporti and it is rare for local performance to be identifiable. When it comes to documenting climate risk assessme to demonstrate compliance with the GFSC Code of Corporate Governance, firms and investment companies should be able to produce detailed, well-structured documentation that shows how climate-related risks are identified, assessed, managed, and integrated into the broader governance framework. Our concern is that this is not widespread. We find little e id f

and investment boards. One might a shareholders or investors are involve assessments of climate risks: physica improperly, conducted and such risks

Covid, the cost of living crisis, and the wars in Ukraine and the Middle East have contributed in recent years to a significantly changed business environment. There are many explanations given for the lack of widespread public climate disclosures. During discussions reasons offered up have included... mor pressing other regulatory priorities, including AML, general business pressures, and a lack of prescriptive clarity from the GFSC on its requirements.

In such times a falling down the agenda of climate risk is understandable, particularly if there are no external shareholders or investors in the picture. But climate risk itself is an existential threat to our wa of life, and an absence of serious consideration of its potential impact on the long term economics of a business or investments is not to be condoned.

The rationale of the International Sustainability Standards Board is that a key benefit of public disclosure is to change c beneficially stimulate clim consistency of climate a

We support the ISSB standards, but we believe that more needs to be done now to move the needle on climate risk assessments and reporting. The lack of localised reporting, some seven years after the publication of the TCFD's global guidance, undermines any claim offshore finance might try to make for leadership in sustainable finance.

In complying with the climate risk requirements of the Code, firms and investment companies should be able to produce detailed, well-structured documentation that shows how climate-related risks are identified, assessed, managed, and integrated into the broader governance framework, alongside risk assessments themselves. We strongly believe that a requirement for public reporting would catalyse a consistent, high standard of risk assessments.

By creating thorough, aligned, and consistent documentation and public reporting, firms and investment companies would show they are not only meeting regulatory expectations but also demonstrate themselves as proactive, forward-looking organizations in the context of climate risk.

About the International Sustainability Institute ('ISI')

ISI specialises in private wealth advisory services for fiduciaries, funds and family offices; our expertise lies in the development of governance, policy and measurement frameworks that facilitate sustainable finance and compliance with evolving regulations. Leveraging the expertise of Dr Andy Sloan, PhD economist, expert reviewer for the IPCC and founder of Guernsey Green Finance in 2018, the ISI also contributes to thinking on global policy by way of published discussion papers and media commentary. www.isici.org/advisoryservices