17 minute read

The dynamics of the development of the wood industry Poland

in comparison with the rest of Europe and the world

Vice-president of the Polish Pellet Council ENplus®, DINplus/SURE-UE/DDS Systems Lead Auditor

A graduate of the Faculty of Commodity Science with specialisation in Commodity Science and Quality Management at the Gdynia Maritime University and postgraduate studies in Energy and Renewable Resources at the University of Warmia and Mazury in Olsztyn.

For 10 years associated with the certification of product quality systems and product management systems. Long-term third party auditor in the field of factory production control, due diligence systems for biomass used for energy purposes, quality of wood pellets and sustainability criteria for solid biofuels, in respective certifiers, viz. Polish Center for Research and Certification, SGS Polska sp. z o.o., Control Union Poland sp. z o.o., DQS Polska sp. z o.o., DINcertco GmbH and Bureau Veritas Polska sp. z o.o. Co-author of standards for the due diligence system for solid biomass, e.g. the SWP-SNS:2015 standard “System for verifying the origin of solid biomass for energy purposes”.

A member of Technical Committees operating at Bioenergy Europe. Member of technical committees at the Polish Committee for Standardization (PKN) and of the Forestry and Wood Commission at the General Directorate of State Forests. Currently also Vice-President of the Polish Pellet Council. Gained her experience in over 50 full implementation projects preparing plants to meet the requirements of ENplus®/DINplus certification schemes.

Wood is an important resource for the Polish economy. In 2020 production sectors based on the processing of this raw material, i.e. woodworking, furniture manufacture and paper production, made 9.5% sales in the whole industry. Every year, approximately 40 million m³ of wood, including around 35 million m³ of usable timber, is supplied to the Polish market; this is the total amount that Polish producers have at their disposal. At the same time, the constantly growing demand for timber and wood products makes this raw material more and more valuable and it becomes necessary to optimize its use. A possible reduced supply of wood on the market will issue a number of challenges for producers. Adaptation of the timber industry to the new supply conditions may require, for instance, an increase in imports and a decrease in exports of raw material from Poland, as well as an increase in production efficiency and in the share of recycled wood (see Scheme 1).

Types of biomass produced in Poland

Analyzing biomass fuels produced by domestic producers available in Poland, one must consider wood pellets and agripellets (made of straw and agricultural production residues) as the most important ones. Taking into account the logistic aspects as well as the accessibility and possibility of contracting supplies of this type of fuel, it should be assumed that:

Industrial wood pellet is characterized by high availability and relatively stable price. However, it should be noted that industrial pellets (usable in combustion processes carried out in large installations) often happen to be produced with the use of waste wood from woodworking and furniture manufacture, which in practice means that not pure wood biomass is used as a raw material but one contaminated with adhesives, resins and varnishes. Unfortunately, the method of market surveillance carried out by governmental services – Voivodeship Environmental Protection Inspectorate (Pl. WIOŚ), Office of Competition and Consumer Protection (Pl. UOKIK) – is ineffective, which results in the presence of large amount of adulterated form of the fuel on the market.

Agripellet, similarly to the wood pellet described above, is produced within the country, mainly for the needs of the electric utility in Poland. However, considering the possible use of this type of fuel, two factors that have a significant impact on the choice should be noticed. The first one, comes down to physical and chemical parameters, i.e. particularly low calorific value (approx. 13 GJ/Mg) and high chlorine content of pellet (especially in the case of pellets made of fresh straw), which may negatively affect technical installations by accelerating corrosion. The second and equally important one, consists in the lack of an effective system of quality control upon this type of fuel and the lack of supervision against possible fuel adulteration by using admixtures of various types of non-biomass waste.

Wood pellets

Poland, like any other pellet-producing country, is struggling with the availability of raw material, which is concurrently used for the production of wood-based plates and the like, or burned by electric utilities. It should also be added that the occurrence of smog, which is a common problem of Polish cities, makes more and more Poles change their minds about the use of solid fuels, and the obligatory replacement of old boilers with ecological ones (meeting Ecodesign) increases the demand for pellets on the local market. However, we are one of the leaders in the production of the ecological biofuel, which pellet indeed is.

Taking into account the growing demand for wood pellets in Europe and all over the world, it can be predicted that in the next few years its production in Poland will be constantly increasing. The effect of this will not only be an even greater public demand and awareness, but primarily the growth of the wood pellet and briquette market.

Dry and uncontaminated sawdust from coniferous trees, which is the remnant of the main sawmill production, is most often used for the production of wood pellets. The most frequently purchased raw material is dry wood dust (with moisture content of about 15%), which comes from highly specialised timber-processing plants able to facilitate collection and storage proper for maintaining low humidity and ensuring that the material is not contaminated.

However, due to the high demand and low supply of this raw material, pellet producers are often forced to collect sawdust of worse parameters, or even wood raw material in the form of woodchips or edgings, and grind this type of raw material on their own. There are also cases where large sawmills invest in a granulation line and thus use practically all of the purchased round wood (main product + post-production residue). Although the wood pellet industry in Poland is developing very well, it suffers from a shortage of raw material. The production potential of many Polish plants is very small and they are mainly suppliers to the local market (as solid fuel for households). Larger production plants, due to the high investments made to improve the quality of the finished product, are mainly interested in the production of pellets for export. Therefore, they mainly cooperate directly with foreign customers or with distributors specialised in exporting pellets to the Austrian, French, German, Italian and Nordic markets. According to the EPC

Wood pellet price statistics in Lithuania

Development of the wood pellet industry in Poland

Survey for 2021, Poland produced around 1.2 million tons of wood pellets, of which some 500,000 tons were sold domestically and about 700,000 tons were exported. The results of Poland in this industry compared to other EU countries are shown in Figures 1 and 2 (see p. 35).

According to the figures collected by the Polish Pellet Council, five companies with the production volume of around 0.5 million tons per year make 30% of the annual production of wood pellets in Poland. There are also about 100 smaller companies operating mainly on the local market, half of which produce yearly up to 10,000 tones, whereas the remaining ones have a total production capacity of 15−20,000 tons. It should be noted that about 50% of wood pellets produced in Poland are sold to the West as ENplus®/ DINplus certified products.

Analyzing the current data published by the Lithuanian biomass marketplace BALTPOOL International Biomass Exchange on its website (https://www.baltpool.eu/; Figure 3), which brings together producers, traders and buyers of biomass in the Baltic States, it can be seen that pellet prices in the short period from the second quarter of 2021 to February 2022 more than doubled – rising from below EUR 25/MWh to above EUR 45/MWh.

Reports published by the European Pellet Council (EPC) list Poland among the leading producers of wood pellets – next to Belgium, Finland and Hungary. In 2017−2018, for instance, an 18% increase in pellet production was recorded in Poland. At the same time, Europe witnessed an increase of over 10% in pellet production, reaching 20.3 million tones. Importantly, Poland also follows Europe closely in the number of new production plants and trading companies certified in quality systems according to the ENplus®/ DINplus schemes. From December 2017 to January 2021 there were as many as 60 new ones, and at the beginning of March 2021, we recorded the 100th certificate issued in the ENplus® system in Poland. This is a huge success of the industry, which brought an increase in the overall domestic production!

Growing popularity of biomass fuels results not only from the greater care for the environment, but also from growing thriftiness. Still, even today the majority of the production is exported to countries such as Sweden or Denmark, which started producing green energy on an industrial scale as early as in the 1980s and began reducing CO₂ emission and liquid fuel consumption earlier than Poland.

The year 2019 in Polish wood pellet industry was similar to 2018. It was characterized by a growing demand for pellets, mainly to be exported to Italy and Denmark. Already in 2018 some producers had problems with obtaining raw material, and the situation recurred in 2019. Warm winter of 2019/2020 forced entrepreneurs to suspend production despite putting some new production units into operation. Nevertheless, Polish wood pellet industry kept pace with European leaders – we observed a constant production increase affected primarily by new medium-sized units producing up to 10,000 tons of pellet per year. Most of them decided to obtain a certificate confirming the repeatability of pellet parameters in A1 or A2 quality class, i.e. ENplus®/DINplus certificates. From January 2020 to the end of February 2021, several new entities were recorded on the list of certified producers and trading companies. Currently, in Poland there are 60 producers and 45 trading companies that have already obtained the ENplus® certificate.

The consumption of pellets in Poland has been growing steadily since 2014. Government and local government subsidies for the replacement of old heating systems resulted in an increasing number of new, ecological heating units, which translated into a growing consumption of pellets. It is expected that the impact of these grant programs (including the „Clean Air” program) will be felt for many years to come. In terms of retail sales in Poland, the capacity of the market is growing. However, due to the high VAT rate (23%) for pellet, it will be rather a long-term process. For comparison, in the countries of Western Europe, it is reduced to the level of 10%, which encourages buying this kind of fuel. Still, the price of pellets remains competitive in relation to, for example, eco-pea coal. It is also important that producers pay constantly more attention to products’ quality and thus certify them, which does not come unnoticed by the increasingly aware fuel consumers.

The growth in retail sales of pellets is also influenced by the manufacturers of boilers, which are modern, easy-to-use and, above all, affordable. All of these factors are of great importance for the development of the industry, which should become even more apparent in the coming years. Thus, in a long-term perspective, the choice of RES may contribute to the economic growth of the entire country.

Non-wood pellet

In the group of renewable resources, the major role is played by biomass, the source of which are both timber-processing companies and farms with a surpluses of straw, hay and other agricultural products. These are the main raw materials of which the so-called agripellets, i.e. pellets of agricultural origin, are made in Poland. However, it is a product that is relatively hard to find on the local market. The low supply results from the specificity of its production and use. In order to produce it one must compress large volumes of raw material, which should be stored for a sufficiently long period so that its chemical properties, in particular the chlorine content and moisture, were at pelletizing-appropriate levels. Agripellet is characterized by physical and chemical parameters of exceptional variability conditioned by the given batch of delivered input material. The fluctuations of these parameters depend not only on the type of agricultural biomass used, but also on harvesting techniques, seasoning time and storage methods. Due to the properties of the finished product, it is mainly used as animal bedding or as fuel in biomass burning installations.

Woodchips and sawdust by-produced by timber industry

Research shows that currently the largest part of wood biomass intended for the production of green energy is obtained from timber-processing plants, specifically from sawmills. Sawmill activity leads to the production of solid biofuels in a natural way – these are by-produced during the main technological process in the form of sawdust, edgings and woodchips. Polish Pellet Council has been conducting research on the wood biomass market in Poland since 2015. This market has been analyzed by conducting audits of production sites and telephone surveys. Active economic agents supplying wood biomass mainly to RES production units or to intermediaries have participated in the research. Most sawmills and timber processing plants purchase timber mainly from the State Forests, whose forest districts have valid FSC and/or PEFC certificates. These plants possess from a few to a dozen or so contracts with local Forest Inspectorates, which guarantee them the yearly contracted amounts of roundwood. Some of the sawmills also purchase timber from private forests, and those located near the southern border of Poland occasionally buy wood imported from the Czech Republic or Slovakia. Following is a description of biomass production in a sawmill.

Roundwood is transported to the timber yard, where it is sorted and pre-cut into the appropriate length. It is then forwarded to the sawmill and a series of saws shape the timber to the size requested by buyers. During the mechanical processing of timber, waste is produced in the form of sawdust and edgings, which constitute biomass. It should be noted that a large number of sawmills do not remove the bark before sawing the wood, so the outer edgings will contain it. Sawdust is often collected mechanically from the place of production and directed to the appropriate storage locations. The edgings are directed to a chipper or to an edging storehouse. Sawmills do not use any chemical substances at any stage of timber processing that leads to the production of biomass. The product is therefore a clean biomass that meets the requirements of RES. This biomass is most often produced on the spot (in the sawmill) and freighted by road transport to the recipient. Some sawmills are not equipped with chippers, so they sell edgings to their customers, who chip wood material on their own yards before delivering it to the power industry. The sawmill companies included in this study are active biomass supply companies, but they are not direct suppliers. Sawmills usually offer products from both deciduous and coniferous trees. It should be noted that these two types of timber are not separated at any stage of biomass extraction. The exceptions are highly specialized plants that produce only specific types of wood products. Looking at Figure 4, it is easy to see that Polish forest stands are dominated by conifer trees.

According to the data provided by the Industry Monitoring, Sectoral Analysis of PKO BP on the 9th February 2023, the utility wood harvesting in Poland has fluctuated around 39 million m³ over the past few years. From 2018, the average annual export of wood amounted to 4.7 million m³, whereas its import to 2 million m³, which translated into a positive trade balance in this raw material group. Poland is the 7th largest exporter of timber in the world and an important supplier of wood-based panels. The vast majority of unprocessed timber from Poland goes to the EU market and to China (20% of export, though the export of wood to this market is decreasing). The largest foreign suppliers of the raw material are the Czech Republic, Germany and Lithuania. The second half of 2022 brought a slowdown on the wood market, which was white-hot during the pandemic. According to the Large-scale Inventory of the State Forests (pol. acronym: WISL, 2013−2017), coniferous species dominate on 68.4% of Poland’s forest area. Pine occupies 58% of the area, with 60.2% in the State Forests and 54.9% in private stand. Therefore, one should expect to find a similar ratio of softwood to hardwood processed by sawmills.

Research has revealed that the yearly biomass production capacity of the largest sawmill plants producing pure biomass (wood chips and sawdust) often exceeds 12,000 m³

Dominating purchasing profile (inner circus)

deciduous large-size timber coniferous large-size timber medium-size timber small-size timber in total. Among the surveyed companies, the median value of total produced biomass is 2.5, and the average value of 5.3 thousand m³/year. Of which, on average, they produce 3.1 thousand m³/year of chips and 2 thousand m³/year of sawdust. Moreover, the forecasts show (Table 1) that the amount of utility wood available in Polish forests will systematically increase on yearly basis, which means that both, its processing in timber industry plants and the amount of wood biomass they produce, will increase.

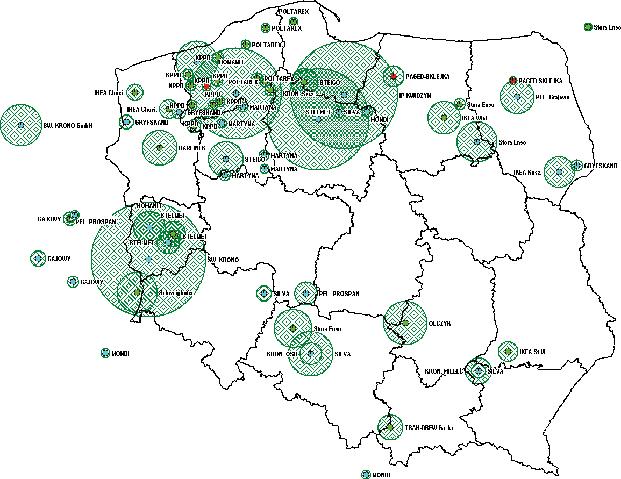

In Poland, at the beginning of the development of RES based on wood biomass, also the furniture industry had its share in supplying biomass. However, after a few years, the leading suppliers of wood biomass resigned from buying it from this type of plants. The main reason for this was the frequent questioning of this wood material as biomass. The doubts were due to the problem with separating clean wood residue from the one contaminated with various types of chemical substances. According to the current legal regulations, this resulted in qualifying the entire wood residue produced as waste, and not as biomass. Similar criteria were adopted for wood material from the industry producing or processing wood panels and other industries where wood used for biomass production could come into contact with chemical substances that contaminate it. Therefore, such plants were not taken into account. As shown in Figure 5, large wood processing plants are located mainly in the northern and north-western part of Poland.

Forest biomass (State Forests and private forests)

According to the report of Industry Monitoring prepared by the PKO BP Sectoral Analysis Team on the 11th of October 2021, forests cover 29.6% of Poland. This is less than the EU-27 average, where the forest cover is approximately 40% (after H. Mauser, Key questions on forests in the EU. Knowledge to Action 4, European Forest Institute, 2021). The countries with the highest forest cover in the EU are Finland (66%), Sweden (64%), Slovenia (58%), Estonia (54%) and Latvia (53%). The majority of forests in the EU-27 are privately owned (58%). In Poland, the share of private woodland is much smaller - less than 20%, of which 94% belongs to natural persons. 76.9% of the total forest area in Poland is under the management of the State Forests. The share of woodland in Poland increased in 2009−2018 by 3.6 pp, while on average in the EU this increase was 2.4 pp (according to Eurostat, data for 2018). A greater relative increase in forest area than in Poland was recorded in Portugal, Greece, Hungary and the Baltic States – Figure 6.

According to the data of the Central Statistical Office, 39.7 million m³ of wood was harvested in Poland in 2020, including 38.1 m³ of timber. In turn, FAO data for 2020 show that the production was at the level of 40.6 million m³. The timber stock on the market, understood as the volume of domestic production plus imports and minus exports of the raw material, reached the level of 39.1 million m³, of which 88% was utility wood. It can be assumed that this amount of raw material was available to buyers of wood in Poland – Figure 7.

The main recipients of wood are woodwork manufacturers (PKD 16), the furniture industry (PKD 31) and the paper industry (PKD 17). The sold production of these industries reached the level of PLN 103.4 billion in 2020, which corresponded to 9.5% of the sold production of the Polish industry in total. All these sectors of industry use wood for production, but the vast majority of raw material is purchased by sawmills and producers of wood-based panels. It is worth noting that raw material, by-products of the sawmill industry (e.g. shavings, sawdust) as well as recycled wood are used for the production of panels (see Scheme 1). The share of sawmill by-products in satisfying demand of wood panel producers for raw material is estimated at nearly 50%, of which 46% is raw material and 4% is recycled wood. The systematic increase in the share of secondary raw material in production should be considered as a plus; in some plants it currently reaches the level of 25%.

Wood and wood industry products are widely used in construction and in the furniture industry. The links in the supply chain for the furniture industry are strong. Therefore, furniture companies are more and more willing to integrate supply chains, investing, for example, in their own sawmills or panel factories. Wood is also used in the production of joinery or pallets. The demand for the raw material is also reported by producers of the garden joinery (so-called garden program) – Poland is the largest producer of wooden garden architecture in the EU.

Wood-based pulp is supplied to manufacturers of paper and paper products. The COVID-19 pandemic significantly accelerated the development of the e-commerce sector, which in turn increased the demand for packaging (cardboards, paper boxes). Statista estimates that the European paper production market will be 5.5% higher in 2027 as compared to 2019. Wood is also used for energy purposes. In the wood sales offer for 2022 published by the State Forests Directorate, the pool of wood fuel in the total sale offer was nearly 6%.

Countrywide supply of biomass for energy purposes is influenced, on the one hand, by the overall volume of timber harvested (theoretical potential) and, on the other hand, by the actual amount of wood available for these purposes, which principally depend on the legal regulations and related liability to generate energy from renewable resources (Zajączkowski, 2013). The forecast presented by Mr. Zajączkowski shows that the potential base of wood for energy purposes will grow, both regarding state as well as private forests. The estimated theoretical potential of the entire country in 2021 would be 6.28 million m³, and in 2031 7.53 million m³ for the State Forests, and respectively 1.12 and 1.38 million m³ for private woodland. The author, however, includes firewood, small-size wood (including small-size firewood) and logging residues in the energy wood base. Practice shows that only logging residues can be considered as a raw material available for the power industry. This is related to the exclusion of firewood, which is intended only for retail customers and as such subject to a different VAT rate. Similarly, small-size wood together with small-size firewood constitute the so-called brushwood assortment which is made at the expense of the buyer from remains of logging. It consists in extracting thicker pieces from the waste and buying them for heating purposes by the local population. This is a disappearing practice, but statistical numbers include this volume together with small-sized wood coming from thinning and the like, which cannot be used for heating purposes. After correcting the data of Mr. Zajączkowski, a forecasted potential would be 3.76 million m³ in 2021 and 4.21 million m³ in 2031. However, the author of this forecast is aware that this is just a theoretical number, while the actual one must take into account, i.a. ensuring the fuel supply to the local population, leaving part of the residue to protect forest ecosystems, assessing the reasonability of allocating large amounts of wood from the forest to generate energy, or the potential of fast-growing crops cultivated on plantations. He also draws attention to the possibilities of using wood from catastrophic events, which, however, should be considered as a separate category.

Polish Pellet Council (www.polskaradapelletu.org)

Polish Pellet Council is the national contact organization for the pellet industry in Poland and abroad. We focus on improving air quality by promoting pellets as an ecological fuel as well as R&D and educational activities. We readily support producers, trading and service companies applying for the necessary certificates or permits and help them in reaching new markets. We also represent the pellet industry in contacts with public administration and local government authorities.

Polish magazine about fireplaces and stoves

Electric Heater