A PensionBee and MoneyMagpie collaboration What Do I Do? Help, I Have No Retirement Savings

Contents 1. Intro 2. Why the earlier you save into your pension, the better 3. Retirement investing in your 20s 4. Retirement investing in your 30s 5. Retirement investing in your 40s 6. Retirement investing in your 50s 7. Self employed pensions 8. Don't panic! How to top up your pension even if you're only a few years from retirement 9. Investing in line with your beliefs 10. Savvy pension choices when it's time to draw down - shopping around, annuity vs flexible drawdown vs income

1. Introduction

Paying into a pension can be easy to put off. You’ll do it later. Next year. When you’re older.

And then, suddenly, you’re older - and you have no pension savings!

The first thing to do is not panic. It’s OK – there are still plenty of things you can do to build up your pension pot. Whether you’ve got decades to go or just a few years until retirement, taking action now could help lift your retirement from the bare necessities to enjoying luxuries like holidays (or, at least, an extra treat here and there).

This guide will help you understand why pensions are essential – and what action to take each decade of your life to make sure you’re not left in the financial lurch when it’s time to retire.

SAYS:

For many workers, a happy retirement holds the promise of spending more time doing the things they enjoy - whether that’s seeing friends and family, pursuing a new adventure, or simply relaxing. Our new guide will help you understand why pensions are essential – and what action to take each decade of your life to ensure you’re on track to achieve a happy retirement.

Pension consolidation can offer significant benefits for any saver with multiple pension pots from old employers. Combining numerous pensions into a single plan not only helps to reduce the stacks of paperwork associated with scattered savings, but can also provide a clearer picture of how investments are performing. Having full visibility can help savers achieve their goals faster and ultimately get the retirement they want.

For younger savers in particular, there’s something very motivating about having a holistic view of your finances and seeing your savings grow over time, whether that's thanks to a combination of compound interest, personal and employer contributions and perhaps even investment growth. However, as this guide explains, it’s never too late to start saving whatever your age!

2. The Earlier You Save, The Better

The State Pension isn’t a reliable income. The age at which you receive it could go up in future – for example, now it is the age of 66, but goes up to 67 in 2028. This is likely to increase again in the future – and there is no guarantee of the rate of State Pension, either.

If you have 35 years of National Insurance contributions by the time you reach State Pension age, your weekly allowance is (currently in 2021/22) £179.60 a week – that’s £9,339 a year. Most people will also have paid into a workplace pension during their career, too. That boosts retirement income on top of the State Pension income.

Free money!

Auto-enrolment comes with free money! Yes, really. The regulations mean that employers must contribute a certain percentage of an employee’s qualifying earnings every month, and, on top of that, the Government pays tax relief too (in other words they put into your pension the tax you would have paid on the money you contributed). The employer contributions cannot come out of your salary package – it’s paid on top. So, you’re only gaining by remaining opted-in to your workplace pension.

At the moment, the legal minimum is a 5% employee contribution (4% from you and 1% from the Government in tax relief), and 3% from your employer. So, someone earning £25,000 a year would pay £83.34 a month, their employer pays £62.50, and the Government adds £20.83. For £83.34, the individual gets a total of £166.67 paid into their pension! You can use the Government’s MoneyHelper calculator to see how much you could gain from opting in to your workplace pension.

Compound returns are your friend!

It’s tempting to see the money going out of your pay cheque each month for your pension as ‘lost cash’, especially if things are a bit tight at the moment.

However, unless you’re REALLY hard up, try to stay enrolled in your workplace pension. Or, if you don’t have one (we’re looking at you, freelancers), set aside whatever you can each month to pay into a private pension. More on this later!

Even the tiniest amounts add up over time. And time is the important factor for getting a headstart on your pension pot. Compound interest over many years, even decades, helps your pension pot to grow.

It means that £100 put in now is likely to have grown exponentially compared to £100 put in closer to your retirement.

But don’t panic!

This all sounds like we’re saying the future is doom

gloom for anyone already approaching retirement. It’s not!

However, if you can afford to shift a larger amount of your savings into your pension right now (particularly if you’re within five to ten years of retirement), there’s time for your money to grow.

*Inevitable caveat: all pensions are investments. That means you could get back less than you put in and your capital is at risk.

How much do I need in my pension pot?

Decide how much you’ll need each year to live off – comfortably – and add a little for inflation (let’s say 2% to err on the side of caution). Not sure how much that really is? A pension calculator can help you set a retirement goal and show you how much you’ll need to save in order to achieve it.

According to Which?, individuals wanting a comfortable or luxury retirement will need a pension income of £19,000 or £31,000 per year, respectively. A basic pension of £13,000 will cover the essentials. If you’re in a couple, you’ll find you won’t need exactly double these amounts, as many bills are shared – so a joint pension income of £18,000 to cover essential costs, £26,000 to live comfortably, and £41,000 to afford a luxurious lifestyle.

If this sounds like a LOT of cash, don’t fret! Even if you’re ten years away from retiring and have no cash set aside, you can find ways to top up your pension.

We’re going to take a look at the steps you can take in every decade of your life to make sure your pension pot is a comfortable nest egg – including if you’re coming up to retirement and need a last-minute boost!

and

One way to make sure you have enough set aside for your retirement is to work backwards from your retirement plans.

3. Retirement investing in your 20s

Your 20s are the first moments of real adult freedom and it’s understandable you want to have fun! However, sacrificing a little of your pay each month into a workplace pension now can have SERIOUS benefits to your pension income in later life.

Let’s say that, in one year, you have £5,000 paid into your workplace pension (including employer contributions and Govt tax relief). Assuming you’re aged 25 in the year this happens, and you’re retiring at 60, that means your cash has 35 years to grow.

Compound returns – means this £5,000 will be worth more than someone who is aged 59 and pays in £5,000 in the same year. That’s because the older person won’t be able to benefit from compound interest or investing gains.

Let’s break it down like this…

Age 25, you pay £5,000 into your pension. 35 years of an assumed compound interest rate of 2% means that becomes £9999.45*.

Without you doing anything else to it. The first year, you’ll earn around £100 in interest. That’s reinvested the following year, so your interest earns interest!

Now, if you pay in £5,000 every year for 35 years, it’s easy to see how that quickly grows your pot!

On the other hand, if you put in £,5000 when you’re aged 59, you have one year of interest. So, your pot might have grown by £100 instead of doubling, thanks to time.

And this bit of maths means one important thing: you don’t have to sacrifice a lot of your salary in your 20s to build a good pension pot. A little goes a long way! Of course, the more you can tuck away now, the less you’ll need to put away in the future for the same returns. (If you want more examples of how small amounts add up over time, check out Turn £25 a Month Into Thousands for Retirement).

How to Start Building Your Pension in Your 20s

The first thing to do is find out if you’re eligible for your workplace pension scheme. You may not qualify if you’re earning under £10,000 (in 2021) – but even then, you may be able to apply to opt in to the pension scheme (and your employer can’t refuse). Check if you’re eligible here.

1. Ask for a pay rise

Yes, really! Many employers undervalue the experience of younger employees. If you’ve been with your current employer for more than a year on the same pay, talk to them and request a pay rise.

Even a small increase in your overall pay will add to the amount you – and your employer (free money!) – have to pay into your pension. The amount may be small, but remember – time is on your side.

2. Keep a spending diary

Do you know how much you spend on takeaways each month? How about those coffees with your mates? Do you get taxis when you could walk?

Keep a running total of every single penny you spend for a month – ideally three months, if you can – and then take a long, hard look at it. If you’re feeling broke all the time, and a pension isn’t on your mind, look at where you might be able to make some changes. Paying off your biggest debts now will leave you with good saving habits that you can turn to your pension when you feel more financially secure.

Yes: Salaries don’t match inflation, new graduates are currently down on their luck when it comes to the employment market, and everything – including basic food and utilities – just seems to cost so much more than even a few years ago.

We’re not placing blame here by suggesting you keep a spending diary! We know how hard it is to have any spare cash at the end of the month. But, keeping a spending diary will help you see where you might be able to make small changes now that add up in the future. For example, if you like taking an exercise class with your friends at £8 a week, could you go for a hike together instead?

It’s not about missing out – it’s about savvy spending.

Lifetime ISAs

We’ll cover Lifetime ISAs in more detail in the next chapter (and PensionBee have a great article on LISAs here).

Pay in up to £4,000 a year and the Government tops up by 25% with a tax-free bonus. You can open one between the ages of 18-39, pay into it until you’re 50, and not access it until you’re 60. The exception here is you can also access it for a deposit for your first home, before you turn 60.

Let’s assume you pay in the full £4,000 every year from the age of 18. Before compound returns, you’ll save £128,000 of your own cash. Add to that a £32,000 Government top-up, and your pot sits at a healthy £160,000. Not being able to touch that £160,000 for a further decade means you’re looking at a very healthy potential pot when you turn 60! The cash is tax-free, too.

HOWEVER – if you need to apply for means-tested benefits at any point, the amount in a LISA is taken into consideration as capital (whereas money in a pension scheme is not). You can’t draw your cash until either you turn 60 or you buy your first home – unless you want to pay a fine and receive less money than you paid in. That’s why it’s not ideal for everyone – but it IS worth considering (especially if buying a house is on your long-term list, too).

Your Risk Appetite in Your 20s: High

When we invest in a pension, the majority of that money usually goes into shares on the stock market. So, it can go up and down over time, and you could get back less than you put in (like any type of investment).

You can choose something that is in line with what is called your ‘risk appetite’. In your 20s, you can afford to go for a highrisk fund portfolio. These funds tend to be more volatile by nature and could experience pronounced highs – or lows –over time.

That sounds scary, but wait! The higher risk comes with potentially higher reward. The returns on ‘riskier’ funds CAN be significantly higher than ‘safer’ funds.

And, as we’ve shown you earlier, time is on your side. That means you can afford to take more risks with your pension at this point in time. Your investments have time to ride out dips in the market – and take advantage of the highs they may see, too.

High-risk funds are better suited for those decades away from retirement, for this very reason of volatility. Even if you opt for them in your 20s, we have to remind you that your capital is at risk.

4. Retirement investing in your 30s

This is the time we’re supposed to be having families, buying houses, and moving up in our careers… but let’s be honest for a moment. All of that ‘supposed to’ is a mountain many of us struggle to climb these days.

The cost of renting in the UK, for example, plus house price rises, mean it’s very hard to get a deposit together for a mortgage on a house. As for children, well: the cost of childcare very often outweighs earnings, so many people face difficult decisions about their career and family choices.

It’s not all doom and gloom, though! This is the time of life when we’re more personally confident and know more about our aims and goals for the future. We know that we want to buy a house (or not), have children (or not), or set up our own business (or not). It’s a decade of choice!

In the flurry of exciting life decisions, it’s easy to put pensions to one side. But, it’s more important now than ever before in your life to consider what you want from your future.

For example, you may need to think about passing your pension to your children as part of their inheritance. A pension is, in most cases, excluded from Inheritance Tax calculations as part of the estate. You can nominate a beneficiary to receive your pension when you die, either as a lump sum or as a continued income, depending on a number of factors such as if you have already started to draw on your pension.

Set Your Financial Goals

We’re ‘supposed to’ know what we’re doing with ourselves by the time we reach our 30s. First thing’s first: it’s entirely OK to NOT know what you want to do with your life! Especially lately, with the pandemic shaking the world up onto its head. Many of us are reassessing what’s important to us – and that has an impact on our financial decisions, too.

Were you made redundant in the pandemic? Perhaps you took on extra work while on furlough and received more income overall than before. Or maybe you’ve had to eat into your nest egg earmarked for a house deposit to get through tough financial times. First: take a breath.

Don’t worry about where you’re ‘supposed to’ be. Think about what’s important to you, right now and in your future, and start planning small things that can be done with ease to prepare for your retirement whatever comes your way in this decade.

1. Sweep your savings

Even if you’re not sure what your big goals are yet, starting a savings fund is the first step to a comfortable retirement. Set up a money-saving app, or within your banking app (as many main banks have this option) to ‘sweep’ your spends.

This is when everything you spend is rounded up to the nearest pound. For example, if you buy something that costs £4.50, you’ll be charged £5.00 – with 50p going into the savings pot. It’s an easy way to start saving without noticing.

After a couple of months, you’ll know what your minimum ‘sweep’ total comes to. Set up a Direct Debit to your pension pot each month to further shift your sweep savings into your pension.

2. Consider other saving options

Shop around to see where you can boost your savings – sometimes with free money. If, for example, you’re saving for a house deposit, look into opening a Lifetime ISA. This allows you to save up to £4,000 a year – and your partner can have one too (if they are also a first-time buyer), bringing the allowance up to £8,000.

The Government tops up your balance by a huge 25% - so each year you save the full £4,000, you get an EXTRA £1,000 from the Government towards your house deposit.

A couple saving the full amount can raise £30,000 in just three years thanks to this bonus top-up.

And why are we telling you this?

The more you can boost your savings elsewhere, the more spare cash you’ll have to sweep into your pension. See – we told you there was logic.

3. Make sure you’re getting everything you’re entitled to

If you’ve taken time off to take care of children or a family member, you could be entitled to extra tax credits.

This ensures your contributions to your State Pension remain in place, even when you’re not earning. Find out more about National Insurance credit eligibility here.

Recently married? You could be entitled to a tax rebate – including for the previous tax year. In fact, Marriage Allowance rebates can go back to April 2017 if you were married then (or since). If one of you has an income of £12,750 or less, and the other earns between £12,501 and £50,270 (£43,662 in Scotland), the higher earner can transfer some of their tax allowance to the lower earner.

This means you can claim £252 for each tax year that you’ve been married (and eligible). If you were married before 2017, that’s over £1,000 back to you! A nice chunk to tuck away into your pension.

Check your pension contributions

Now is a good time to see if you can add a 1% or 2% increase to your workplace pension contribution. It won’t feel like a lot extra out of your pay packet each month, but will make all the difference when you retire.

Your Pension Risk Appetite in Your 30s

You’re still THIRTY YEARS away from retiring. You may feel like you can take more of a risk with your investing at this age.

It might be time to check exactly WHERE your money is invested, though. Some funds might invest in tobacco, oil, or energy companies that you don’t want to support. Looking at responsible or green funds is one way to make sure your money supports the causes that matter to you. These funds are often a little more costly, as there is additional administrative cost to ensure they maintain strict requirements to be considered ethical funds – but it could future-proof your investment choices, as the world moves towards more ethical and sustainable business practice. (Reminder: any investment is not guaranteed).

Your 30s is a good time to check where your funds are invested – higher-risk funds are an option for those who want to take them, as there is still plenty of time to ride out market dips and troughs. Remember: if you’re not sure about investing your money (including in your pension), talk to a financial advisor.

5. Retirement investing in your 40s

Your children (if you have them) are older, you’re more established in your career – now’s the time to start taking retirement planning into account with your annual financial health check.

Take a look at your expenditure – mortgage or rent, living costs, treats – and work out how much it costs you in a year. This is a big figure – especially if you have a family. The good news is this is the most you’ll spend on living throughout your life.

Yes, really.

Think about it: in your 50s, your children will be older and family holidays, school uniforms, the grocery bill of hungry adolescent teenagers, still paying your mortgage – these are costs you won’t face in the future, assuming you don’t get divorced and start a second family by then! (If you’re renting, even that cost will reduce in future if you downsize to a smaller home).

If you’re stretched to your income limit right now, don’t panic. As your costs recede (such as teenage children not wanting to join you on holiday!), sweep those extra savings across into your pension.

There are other ways you could free up some more of your money to boost your income, too:

1. Consider remortgaging your home

Remortgaging means you find a new mortgage that essentially ‘buys out’ your old mortgage. It can give you more favourable interest rates and lower your payments. Remortgaging is not for everybody. However, if you are out of your fixed term period on your mortgage, speak to an independent mortgage broker.

A broker will be able to help you shop around to find the right deal. They will also tell you if remortgaging is not ideal for you – so you won’t risk making a costly decision.

Remortgaging helps your finances in a couple of ways:

• It can either reduce your interest rate to slash repayments, and some can lock you into a low rate to protect against rises.

• Or, you could opt to pay your mortgage off quicker than your original loan term. For example, if your original mortgage was for 25 years, ten years ago, (with 15 years left to repay), you might find a new mortgage deal that will have you repaid in ten or 12 years instead. Shortening the term also reduces the lifetime cost of the mortgage – leaving you mortgage-free (and therefore with more spare capital) sooner.

2. Ask for a greater pension contribution from your employer

We mentioned asking for a pay rise back in the 20s section. Of course, you should still DEFINITELY keep asking for regular promotions and pay increases throughout your career.

However, one way to get a pay rise without really getting a pay rise is to ask for your employer to match, or even pay more than, your pension contributions. This can be a smaller risk and cost to the employer than a full pay rise, so may be easier to negotiate than you think.

Ask your employer to match your workplace pension contributions, whatever they are. This is also a time to consider bumping up your contributions to a higher proportion if you can - 7%, 8%, or even 10% if you can tuck that away each month. Your employer isn’t legally obliged to match your contributions beyond 3% – but asking them for an increase will effectively bump up your free earnings into the pension pot!

3. Look at alternative income avenues

The advantage of living in such a technological age is that it’s now easier than ever to build a passive income stream. In your 40s, you’ll have a wealth of experience in a range of different things – so put them to good use!

We have literally hundreds of ways that anyone can make money on the side at MoneyMagpie.com. Check out our Make Money section for all sorts of ideas, including some truly weird and wonderful ones!

Consider teaching a weekly art class in your local community, or offer GCSE students extra help to prepare for exams. Perhaps you want to help others keep fit, so run a class or, even better, turn to online!

Online courses, live webinars, and one-to-one support had a boom (or should we say, Zoom) time in the 2020 pandemic. With lives turned online, it became clear that there’s an audience for online courses, classes, and groups.

While you can make money from live online sessions, you can also build a passive income from creating online courses or video courses to sell. Or, turn your crafty hands into a side business to sell your creations online. Find out lots of ways to make money online here.

What we’re saying is: find a way to make a little extra cash doing the things you love.

You don’t have to go all-out business on it either: running a local class once a week might put an extra £100 in your pocket each month. Stick that in your pension pot and it’s easy to see how you can grow your retirement nest egg without dipping into your valuable time too much.

(Remember: if you earn over £1,000 a year from these extra earners you must register with HMRC for tax).

Check Your State Pension Eligibility Now

To qualify for a State Pension when you’re 66 (or older, in the future), you need to have at least 10 years-worth of National Insurance contributions to quality for the basic pension and 35 years-worth to get the full pension. If you don’t have the full amount, you can ‘top up’ with an extra payment. It’s better to identify missing years earlier rather than later – as you can choose to ‘top up’ by a smaller amount and/or work some of the extra years required (you’ve still got around 20 years to go if you check in in your 40s!) to make sure you have the full requirement. If you wait until your 50s, you could be faced with a choice of a large top-up bill or a lower State Pension when you reach State Pension age.

Check your State Pension forecast here.

Your Pension Risk Appetite in Your 40s

This is when you need to start thinking about the future in more detail. The higher-risk funds you’ve been investing in may have performed very well – but it’s time to start mitigating some of that risk. You don’t want to undo years and years of growth with one stock market blip!

Consider moving at least some of your savings to a lower-risk portfolio. A medium-risk fund at this stage of your life will help balance the need for growth with the need for stability.

6. Retirement investment in your 50s

Here we are: the home stretch. But what if you’re already here and haven’t covered the steps listed above in your 20s, 30s, or 40s?

Don’t panic! We’ve got you covered in Chapter 8.

If you have a pension pot, keep reading.

Now is the time to look at your retirement options. Make sure you know how much you have in your pension pot – and how much you’ll need to top it up by before your retirement date.

Consider your plans for your pension: do you want a regular, reliable monthly income from it? Or would you like to use a tax-free lump sum to invest in buy-tolet property or other assets? You can do both – but remember that taking the lump sum will reduce the amount you can draw down as an income from your pension pot. We explain the different types of pension income in Chapter 10.

When will you take your pension?

You can access a private pension from the age of 55 (57 from 2028) if you have enough cash to fund it – but think hard about whether you want to do this. Here’s what you need to weigh up:

1. Accessing early means you can go part-time

If you want a phased retirement, opting to access some of your pension income from the age of 55 means you can reduce your work hours rather than suddenly stopping work in your 60s.

A phased retirement also means you can benefit from ‘semi-retirement’ early –less demand on your time from your career, and more time to do the things you want, while still receiving a salary.

2. Your pension pot could benefit from more time

If you leave your pension pot until you’re 60 or even later, that’ll help you to grow your retirement income further – leaving you with a larger pot for a more comfortable retirement.

Accessing your pension at 55 will mean that cash won’t have time to grow further. Of course, if you’re using a taxfree lump sum to make other investments such as on a buy-to-let property, you may receive an income from that, too.

However, like any investment, those returns aren’t guaranteed – so it’s important to make sure you don’t leave yourself asset-rich but cash-poor in your retirement.

3. Your current health may impact your decision

We don’t want to get morbid here, but it’s part of pension planning: if your health isn’t great, you could benefit from taking your pension earlier than later. In fact, as we’ll see in Chapter 10, some annuities could give you more pension income based on your health conditions –and the earlier you opt for one, the more likely you are to maximise the value of your pension income.

Annuities are worked out based on proportionate risk. So, if you don’t have brilliant health, a pension provider will assume you won’t live as long as your healthy counterpart. Putting off taking your pension – and continuing to work with worsening health conditions – could mean you don’t get to enjoy a very long retirement OR maximise the return on your lifelong investment.

It’s not fun to talk about, but it IS important to think about this. If you continue to work until State Pension age or beyond, without taking your pension, will you realistically be able to make the most of your life savings? Or, would it be better to retire earlier – or take semiretirement, at least?

Your Pension Risk Appetite in Your 50s

Now’s the time to slow down.

As you approach retirement age, consider shifting your pension funds to a lower-risk portfolio. It’s had lots of time to grow already, and you want to protect your fund. Moving to a low-risk option helps to mitigate against any sharp market falls when compared to higher-risk funds.

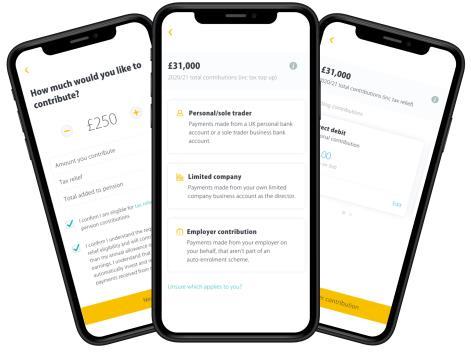

7. Self-Employed Pensions

If you work for yourself, you won’t be able to rely on being auto-enrolled into a workplace pension. Instead, you’ll need to make your own pension arrangements. Thankfully, doing so is simple!

To get started, you’ll need to set up a personal pension. Most pension providers offer personal pension schemes, and they work just like the common workplace pension. Some providers, like PensionBee, allow you to increase and decrease your contributions over time, offering you flexibility depending on your earnings.

The only downside is that you won’t receive an employer contribution, since you work for yourself. However, the government will still top up your personal contributions with 25% tax relief.

To get started, you’ll need to set up a personal pension. Most pension providers offer personal pension schemes, and they work just like the common workplace pension. Some providers, like PensionBee, allow you to increase and decrease your contributions over time, offering you flexibility depending on your earnings.

The only downside is that you won’t receive an employer contribution, since you work for yourself. However, the government will still top up your personal contributions with 25% tax relief.

If you feel confident enough to manage your own investments, you could also consider a Self Invested Personal Pension (SIPP). Unlike the standard personal pension, a SIPP allows you to manage your own pension investment portfolio. Another key benefit is that you won’t be charged an annual management fee. But beware: you could be charged other fees. So it’s important to read all the details to make sure you know what you’re paying.

If you’re a director of a limited company, you may decide to make employer contributions to your pension. In this case, contributions may be considered as an allowable business expense, meaning they could be offset against your company’s corporation tax!

It can be easy to overlook your pension when you’re busy running a business. In fact, research from NEST shows that only 24% of people who are self-employed are actively contributing to a pension.

But it’s arguably even more important to save for your retirement when you’re selfemployed, since you may need to pay in more or for longer to make up for the lack of additional employer contributions.

Are You a Writer or Creative?

A little-known fact if you’re a writer for TV, film, or radio is that you can ask for a percentage of your script fee to be paid into a pension set up by the Writers’ Guild of Great Britain. For self-employed writers, this is a lifeline, as it acts similarly to a workplace pension as a tax-efficient vehicle (as your money goes direct to a pension without being taxed as income on your annual Self Assessment).

You need to have a commissioned script and be a full WGGB member – if you’re not yet a member but have a commissioned script, you can sign up to register. Find out more here.

A similar scheme is available to anyone with an Equity card. Their scheme requires your employer to contribute to the pension, much like a workplace pension. For example, if you’re paid £500 a week, your contribution will be £12.50. The employer then has to pay £25 a week. In one month, you’ve paid £50 but the total contribution to your pension is £203.12 (based on current figures in the advice pack here).

Find Your Professional Union for Pension Help

If you’re self-employed but not in the creative industries, look to your industry union as the first port of call for similar pension schemes. Many, like the WGGB scheme, will ensure that your pension payment goes into the scheme you choose (unlike a specific workplace pension scheme).

If you find an industry-specific scheme like the one Equity runs, remember that you can have more than one pension pot. So, your pension for your contract work can be different to a self-employed pension scheme you also hold of your choice (like PensionBee’s flexible scheme).

You can also transfer between pension pots – so every few years, weigh up the different schemes you have invested in and consider shifting some from the work scheme (like Equity) to your main self-employed pension pot (if the fees, funds, and customer service makes it your preferred choice).

8. Don’t Panic!

How to boost your pension pot close to retirement

If you’ve read all of the above thinking: “If I had a time machine, I’d go back and do these things –but I’m not Doctor Who!”, this chapter is for you.

We realise that many people approaching retirement will not have the full pension pot they need for a comfortable income.

There are lots of reasons for this: a lifetime of high expenses, time off for childcare or caring for family members, working in typically low-paid industries or those with inconsistent incomes (such as self-employment or the arts), and many more.

The good news is that there are things you can do to boost your savings and pension pot before you retire – even if it’s only a few years away.

1. Make sure your pension funds are in a suitable place

Do you have several small pension pots gathered from a range of different workplace schemes over the years? Do you even know where these pots are?!

It sounds like a silly question – but 78% of UK adults don’t know what’s in their pension pot, and over half don’t know how many pension pots they actually have!

As we move homes and jobs over the years, especially before everything was easily done online, it is easy to forget to forward your mail or update your address with old workplace pension schemes.

Track your pension pots using the Government’s free Pension Tracing Service. Make a list of every past employer and look up their pension contact details. Track your old pensions down to make sure you’re not missing any of your hardearned savings.

PensionBee has also developed an online tool that can help you find out whether you have any lost pensions.

Simply answer a few simple questions, and the tool will tell you whether it’s worth getting in touch with your old employers.

When you’ve found your pensions, look at what they’re costing you. You may be surprised to find that some funds haven’t grown as much as you expected, because management fees every year have eaten into investments.

It could benefit you to consolidate your pensions into one pension pot to reduce the fees you’re paying and maximise your returns.

Contact PensionBee to consolidate your pensions with them online. It’s free to transfer your pensions to them, and they charge just one simple annual management fee. As with all investments, your capital is at risk.

2. Check you’re getting the benefits you’re entitled to

Many people don’t realise they may be entitled to receive benefits – either meanstested or not means-tested – even if they’re in work. Tax credits, for example, or Personal Independence Payment if you have a disability.

Use the free online Turn2Us benefits calculator.

It takes about ten minutes and will show what benefits and discounts (such as Council Tax reductions) you could be entitled to receive.

The same website also has a grants finder. If you’re in financial need, use the grant finder tool to discover any funds that you could apply to for an income boost – for free.

3. Delay your retirement

If you’ve been looking forward to retiring, this might come as a bit of a blow. However, if you keep working for a few more years, you’ll have time to build up the pot.

Working past State Pension age (currently 66) also means that you won’t pay National Insurance after that age – giving you a little extra to sweep away into your pension. More than that, you can defer your State Pension – you don’t HAVE to take it the moment you become eligible.

Deferring your State Pension could increase the income you receive from it. So, you don’t miss out on the money you’re owed from the age of 66, it just gets paid to you later –increasing your weekly pension amount.

For example, if you defer your State Pension by one year (using today’s figures and assuming you’re entitled to the full amount), your weekly income rises from £179.60 a week to £190.02 per week – an annual increase of £541.84.

4. Boost your savings with a side income

You’re thinking about giving UP work, not working MORE! We know, but for a few years before you retire you could find a dream parttime retirement side hustle that adds to your retirement income AND boosts your savings before you retire.

You have a lifetime of experience to offer people – so use it! Check out our ideas for boosting your savings in your 50s for ways to generate extra cash for your savings and/or pension.

5. Reduce expenditure

This is the tough and boring one, but it’s worth running this exercise to see if you can make easy savings. Make a list of every penny you spend in three months. Then, take a look at where you might cut back.

For example, we’ve all got subscriptions to magazines, online services, gyms and community groups, that we don’t use anymore. Cancelling them could save you a significant chunk of cash each month!

As we’ve said before, too, there are ways to reduce expenditure without missing out on life’s luxuries. Become a coupon lover and you’ll find you can have just as much fun – for less! That includes everything from the grocery shop to going out for dinner or day trip experiences.

You could even save on things like gym and cinema membership if you’re over 50 (or 55 in some cases) – look for discounts wherever you go and the extra pennies will soon pile up!

9. Choosing your pension in line with your beliefs

We mentioned this a little bit earlier in the guide: you have a lot of control over where your money is invested. But, many people don’t know this!

A lot of us pay into a pension, select the risk appetite level we’re happy with, and let it run its own course. We don’t know WHERE our money goes, just that it’s ‘in the pot’ with the funds of thousands of other people.

However, you might feel strongly about some things. Are you passionate about the environment, and green energy? Or perhaps you disagree with the human rights laws of a country where some large corporations are headquartered.

You can square your beliefs with your pension funds with a little bit of research. Do some digging to find out exactly which funds your money is invested in – and if you’re not happy with it, take action.

Environmental, Social & Governance (ESG) investing

Some pension providers offer ‘ESG’ funds. These funds usually only invest in companies that meet a predetermined set of environmental, social and governance criteria. For example, they might not invest in companies that contribute to global warming (such as oil companies). They may exclude companies that contribute to poor health (such as tobacco companies). And they may exclude companies that don’t meet a certain board diversity quota.

Some pension funds operate in the above way, excluding companies outright that don’t align with the fund’s values.

But others may take a more active approach, and use their investing power to influence change. So while they may continue to invest in oil companies, for example, they may pose ambitious carbon reduction deadlines and disinvest if these goals aren’t metputting pressure on the company to speed up its shift from oil to greener energy technologies, for instance.

Sustainable investing

Another variation on this theme is sustainable investing. This type of fund will invest only in companies that operate in a way that considers the long-term impact on people and the environment.

This might involve providing high welfare standards for their employees, reducing greenhouse gas emissions or producing recyclable products. And it might look favourably on companies that operate in certain sectors, such as renewable energy, education or healthcare.

An example of a sustainable investment fund (SRI) would be PensionBee’s Fossil Fuel Free Plan. This plan excludes companies with proven or probable reserves of oil, gas or coal.

Pension funds that focus their investments on companies that help improve social outcomes may also prove attractive for people wanting to invest in line with their beliefs. Examples of companies that might meet an SRI fund’s criteria might include those with gender-diverse boards and exclude those operating in industries such as gambling or adult entertainment.

Finding ethical and green pension investments can be tough if you don’t know where to start, though. It’s usually best to speak to a pension advisor to get their input on the types of funds you should/shouldn’t invest in based on your beliefs. They’ll help make sure your money is where you want it to be – supporting the causes that matter to you.

10. Savvy pension income considerations

It’s all very well having a comfortable nest egg tucked away in your pension pot – but when the time comes, what are your options to access it?

It used to be the case that you had to buy an annuity from your pension provider. Not anymore! Since 2015, the introduction of ‘pension freedoms’ rules mean you have the right to shop around for a pension product from ANY provider – not just the one that holds your funds.

This means you can find the best deal that maximises your pension income based on your circumstances.

And: it’s not only annuities these days, either. You can opt for a flexible drawdown income, an annuity, a tax-free lump sum – or a combination!

Tax-Free Lump Sum

Whatever way you take your pension, 25% of it is tax-free.

The rest is taxed at your standard income tax rate.

You can opt to take up to 25% of your pension as a lump sum, tax-free, and choose drawdown or an annuity for the rest. If you don’t opt for the lump sum but instead choose regular payments or an annuity, 25% of each payment is tax-free.

So, you don’t lose the tax-free status whichever route you choose. Consider what you want the lump sum for – are you investing in a property? Or a similar large investment for your retirement? If so, it could be worth taking the lump sum. However, any means-tested benefits may be affected by a lump sum payment.

Flexible Drawdown

A flexible drawdown agreement lets you take what you want from your pension, when you want. You can arrange to have it paid monthly as a regular income, or take lumps from your pension pot when you need.

The rest of your money stays invested, so it has more opportunity to grow (but this is never guaranteed).

With drawdown, the main drawback is that the pot is finite. Once you start taking money from it, there is no guaranteed income for the rest of your life. This is fine if you plan carefully – but any unexpected costs in your retirement could leave you short of cash.

Annuity

Annuities provide a regular income to you each month, like a salary. You can buy an annuity for a fixed term or for a lifetime term.

Using your pension funds, you buy an annuity. The annuity provider then sends you a regular payment each month with a guaranteed amount. It’s a good way to secure a regular income that you know will cover your bills.

Annuities had a bad reputation for a long time, because people were unable to shop around for a good deal and the products on offer were less flexible. These days, however, they can work well either on their own or in combination with flexible drawdown and/or lump sums.

For a start, you can now buy a fixed term annuity with some of your pension funds – such as for ten years – which guarantees income for those years. At the end, you can choose whether to buy another annuity or do something else with the rest of your pension funds. However, bear in mind that a fixed term annuity may mean you’re not left with enough in your pension pot for a desirable income when the term comes to an end.

Lifetime annuities can offer good value –especially if you have health conditions or lifestyle choices that, statistically, shorten life (such as smoking). You’ll have a guaranteed income for life, and with health conditions this means you can access a premium rate.

Of course, the challenge here, should you choose to accept it, is to outlive your annuity estimation! For example, if the provider calculates they should pay you a regular income for 25 years (and provide an income based on your pension pot divided by 25 years), and you live for 35 years, you’ll have an extra ten years of ‘free’ money!

Combining Your Options

Many people opt to combine two options when it comes to their pension income. For example, some choose to take a lump sum at the start of their pension, then flexibly draw down an income that helps to pay for regular bills and expenses. Others may opt for an annuity that guarantees an income, leaving a lump sum invested for later on or for an income option after their annuity (if it’s fixed term) comes to an end. Which option you choose depends on your circumstances. Make sure you’re getting the most out of your money for your needs and goals by talking to an independent pensions advisor before making any decisions.

Parting thoughts…

So there you have it - if you weren’t sure where to start with a pension, you should be now! If it feels like a lot to take in, here are some of the key points to consider:

Start your pension as early as possible. The sooner your money’s invested, the longer it will have to grow before you reach retirement.

Get the most out of your pension. Make sure you’re enrolled into your workplace pension so that you receive free employer contributions, and check if you’re entitled to any benefits.

Stay on top of your pension. No matter your age or circumstances, there’s always something you can do to improve your future retirement income. Use a retirement calculator to see how much you should be saving to reach your retirement goal. And consider combining your old pensions to save yourself from paying any unnecessary fees.

This guide is sponsored by PensionBee, a leading online pension provider that’s helped over 500,000 savers be pension confident.

Customers can manage their pension easily, view their live balance, and with the help of a smart calculator to plan their savings, make contributions and withdrawals online.

Capital at risk.