15 minute read

Signals are green for new investment in renewables transition

SIGNALS ARE GREEN

FOR NEW INVESTMENT IN RENEWABLES TRANSITION

Advertisement

By Katie Barnett, Partner, Energy Transition - Deals, PwC Australia

Australia's energy challenges are getting a lot of airtime.

With so much happening, there is no shortage of commentary and unprecedented attention on power markets. And, for those with patience and tenacity, there will also be plenty of commercial opportunities.

There are operational challenges with an aging thermal fleet (coal and gas), global gas shortages sparked by the war in Ukraine, the rising cost of power bills, the decreasing reliability and impending retirements of coal generation, and the pressing need for firming/ storage solutions.

The energy sector was firmly in the spotlight in the lead-up to Australia’s May federal election, with power prices and cost of living, along with grid stability and commitment to renewables, key policy battlegrounds. The Federal Government’s energy platform included the $20 billion ‘Rewiring the Nation’ program, a national electric vehicle strategy, amendments to the safeguard mechanism to incentivise emissions reductions, commitments to community battery storage systems and solar banks, as well as enthusiasm for green hydrogen and green metals.

Having received public endorsement for these policies, the challenge now is to ensure they are swiftly and successfully implemented, so Australia can realise its net zero ambitions – because there is no time to waste.

NATIONAL ELECTRICITY MARKET DISRUPTIONS

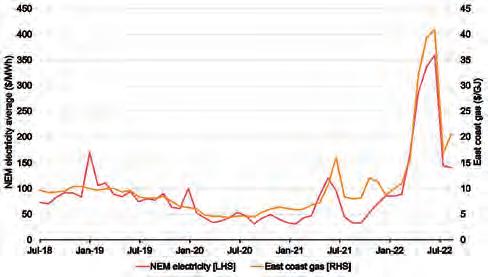

In June, there was a profound disruption in the National Electricity Market (NEM) due to the Russian-Ukrainian War, outages in a third of the NEM’s coal capacity and floodrelated impacts on coal logistics. Additionally, cold weather and soaring gas prices led power prices to spike to three to five times higher than they stood in Q1 of 2022 (gas-fired plants being the marginal generator).

On 15 June, the Australian Energy Market Operator (AEMO) took the unprecedented step of suspending electricity wholesale trading and activating the $300/MWh administered price cap (APC) (which exists to protect consumers from surging electricity costs), throwing the urgent need for more transmission, storage and renewables into sharp relief.

Whilst under the APC, some participants withdrew their supply sparking claims of anti-competitive behaviour. In response to these, in late June the ACCC led an inquiry into electricity market trading, investigating whether participants were participating in market misconduct and manipulating the spot market.

FIGURE 1: NEM AVERAGE MONTHLY WHOLESALE ELECTRICITY SPOT PRICES AND EAST COAST WHOLESALE GAS PRICES TO SEPTEMBER 22. SOURCE: AEMO QUARTERLY ENERGY DYNAMICS Q3 2022.

Discordance in the energy market continued into July, with a rule change request submitted to the market rule-maker the Australian Energy Markets Commission (AEMC), seeking to double the NEM's APC to $600/MWh to better reflect thermal fleet input costs. The request followed claims by coal and gas generators that the current APC (set in the

1990s) inadequately reflects their input costs and should be increased to prevent the supply withdrawal events in June from reoccurring.

In mid-November, in its final rule change determination, the AEMC accepted the APC be raised to $600/MWh from 1 December 2022 onwards, in a transitional arrangement applying until 30 June 2025 – after which date changes may be made following recommendations from the Reliability Panel (and any others who request a rule change). The $300/ MWh increase was deemed necessary to improve NEM reliability and cost outcomes for consumers as the revised APC is likely to reduce the compensation costs payable to directed generators in future administered price periods.

While the June 22 'coal (not gas) crisis' is over, demonstrable pressure will remain in the Australian power market while the war in Ukraine continues, global gas prices remain elevated, and the aging coal and gas fleet continues to be marred by operational issues.

Between January and July 2022, east coast gas prices and NEM power prices rose more than 400 per cent, while by the end of September, demand for domestic gas in New South Wales was over three times recent levels (notwithstanding a fall in energy prices from their June highs as coal plants came back online). The 25 October Federal Budget forecast energy price increases will continue in the next 20 months with electricity prices to rise 56 per cent and gas prices 44 per cent. The Federal Government is currently considering a range of options for tackling rising energy prices, without stoking inflation.

The options include introducing a wholesale market price cap on natural gas, enacting Petroleum Resource Rent Tax reforms, introducing a temporary windfall tax on gas exports or subsidising gas users. Importantly, (temporary) price relief for trade-exposed industries is critical. The chosen mechanism is expected to be announced by Federal Treasurer Jim Chalmers before the end of 2022.

THE CLIMATE CHANGE BILL, NATIONAL ELECTRICITY OBJECTIVE REFORMS, SAFEGUARD MECHANISM AND COP27

In early September 2022, the passing of the Federal Climate Change Bill through the Senate enshrined in law national commitments to achieve net zero by 2050 and a 43 per cent emissions reduction (on 2005 levels) by 2030, marking the first successful passage in a decade of Australian climate change legislation.

In mid-August 2022, we saw Federal and State Energy ministers meet at the Energy Ministers Meeting (EMM)1 and agree on re-incorporating environmental and emissions reduction considerations into the National Electricity Objective (NEO), critical to the National Electricity Law. Once enacted, this landmark change will see electricity regulatory decisions, investments and rule-making decisions appraise climate impacts when the AEMC considers electricity rule changes and power infrastructure investments. This will remove the sometimes perverse outcomes under the current NEO and enable further decarbonisation momentum for power markets.

A week later, the Federal Government released an industry consultation paper2 for its proposed reforms to the ‘safeguard mechanism’ (SM). The Abbott government introduced the SM in 2016, requiring Australia’s 215 largest greenhouse gas emitters (who accounted for 28 per cent of Australia’s total emissions in 2020-21), to keep their net emissions below an emissions limit or ‘baseline’. The paper is the first step in another momentous reform process. It reflects the Federal Government’s commitment to strengthen the SM and ensure Australia meets its 2030 43 per cent emissions reduction target and net zero commitments.

The consultation paper outlines a suite of proposed reforms to change how emissions baselines are set and how to lower baselines over time. Indicative emission reduction rates for big emitters are expected to be between three and a half and six per cent, per year to 2030. The consultation paper also considers introducing tradeable credits for facilities that emit below their baseline and providing support to emissions-intensive, trade-exposed businesses (such as steelmakers and alumina refiners), including financial assistance and differentiated baseline ratchets.

The economy-wide consultation works to a tight deadline; submissions were due by the end of September, (a response from Climate Change and Energy Minister, Chris Bowen, is expected early December 2022) with a more detailed design released for feedback in late December. The current aim is for the reforms to be legislated by March 2023 and come into effect from 1 July. This timeline exemplifies a real urgency by the Federal Government to transform the SM into an effective and credible emissions reduction tool, balanced to support big emitters to transition and decarbonise in an orderly yet demonstrative and prompt way. Of course, there are and will be a plethora of stakeholders in this consultation process, and many opinions and good ideas will be articulated before the final design is legislated. Watch this space.

The Federal Government has also announced a $1 billion ‘Powering Australia Technology Fund’ will be established to support the commercialisation of clean energy technologies. The fund, which rebadges a previous fund proposed to be administered by the Clean Energy Finance Corporation (CEFC), will comprise $500 million in Federal Government funding and $500 million in private sector support. In line with CEFC eligibility rules, carbon capture and storage, nuclear technology and nuclear power projects will no longer be eligible for funding.

COP27, which ran from early to mid-November 2022, highlighted how crucial system-wide changes are (such as those occurring in Australia to support the energy transition) if net zero targets are to be achieved. Despite COP27 reaffirming commitments to keeping global warming below 1.5°C, 2021’s global decarbonisation rate was the lowest it’s been in a decade at just over 0.5 per cent. Decarbonisation efforts need to accelerate rapidly if the 1.5°C target is to be maintained, and COP27 was marked by renewed calls for

more ambitious national targets and stronger implementation measures. Australia used COP27 to advocate for greater global ambition and officially launch its bid to co-host CO31 in 2026 with Pacific nations.

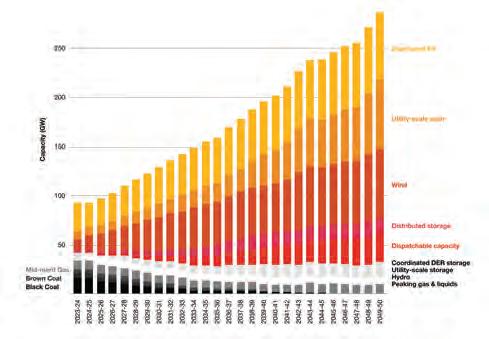

There's little doubt of an increased national appetite for a rapid transmission, storage and renewables roll-out and a cleaner, greener energy future. But there's still a massive task ahead. To achieve the widely accepted 'step change' scenario outlined in the AEMO’s most recent Integrated System Plan (ISP)3, the pace of new renewables, storage, and transmission developments will need to dial up to maximum – as will the level of investment.

FIGURE 2: FORECAST NEM CAPACITY TO 2050, STEP CHANGE SCENARIO. SOURCE: AEMO, 2022 ISP.

There's plenty of cause for energy infrastructure investors and developers to be optimistic in this opportunity-rich time and place. But can we be confident that energy markets are changing in the right way and at the right pace and scale? Given the interrelatedness of all energy system components, it's easy to solve one problem and find another has been created.

In our view, change is never simple, but it must happen. The success of the energy transition will rest on three critical components: 1. More transmission build-out 2. More storage build-out 3. More renewable energy build-out

And, all three builds need to happen quickly.

To move at pace, the sector will need to: • Remove lengthy transmission approval processes • Streamline generator grid connection processes • Resolve current (and likely future) supply issues across the energy value chain (personnel, materials, equipment, shipping, critical minerals) • Build trust with communities and improve environment, social and governance performance • Obtain the all-important revenue offtake arrangements needed to make projects bankable

All of these factors are needed for successful projects in the renewable energy revolution. As the new energy picture takes shape, it will also remain important to keep a watching-brief on the implementation of new energy policies and programs and the progress of long-awaited energy market reforms.

RENEWABLE ENERGY ZONES ARE UNDERWAY

In New South Wales, Victoria and Queensland (and soon Tasmania), there is solid progress advancing Renewable Energy Zones (REZ), the transmission 'highways' connecting areas of good solar, wind and pumped hydro resources to the NEM. Tenders are underway to build the transmission infrastructure, and auctions will soon commence for generator access rights to connect and dispatch. The first tender to build the transmission infrastructure for the Central West Orana REZ in New South Wales closed at the end of November 2022, with the tender process currently expected to conclude mid-2023.

Under New South Wale’s Long Term Energy Service Agreement (LTESA) scheme, projects deploying renewable generation over 30MW, firming/storage and long duration storage are eligible for option contracts which offer stable long-term revenue (20 years for generators, 40 years for pumped hydro and 14 years for chemical batteries) and “zero price floors”, protecting proponents from low or negative wholesale prices. The first stage of non-financial bidding in the first competitive tender process for LTESAs, indicatively 2500GWh pa (approximately 1,000MW) for generation and 600MW for long duration storage, closed 28 October 2022. AEMO Services is now assessing the non-financial elements of Proponents’ bids, with a shortlist expected by the end of 2022 for stage two financial bidding likely to close in March 2023 with LTESA awards currently expected to be announced by April 2023.

State governments have also announced a suite of new energy targets and investments in recent months to support the required renewables build out. In September, the Victorian Government announced a target of 2.6GW new energy storage capacity by 2030, and 6.3GW by 2030, alongside $157 million in funding to support renewables build out. The targets are aimed at supporting both short and long duration storage systems, including chemical batteries, pumped hydro and hydrogen technologies.

Also in September 2022, the Queensland Government released the Queensland Energy and Jobs Plan, which outlined plans for $62 billion of investment in the energy system to 2035 and a target of 70 per cent of Queensland’s capacity to be from renewable sources by 2032. The plan includes commitments for 25GW of large-scale wind and solar to be online by 2035 (over eight times the current 3GW) and over $270 million in funding to projects capable of delivering 7GW of 24 hour pumped hydro.

Australian governments are also mobilising around offshore wind (OffSW) with a spate of recent announcements following the formative Offshore Electricity Infrastructure Act 2021 and the Offshore Electricity Infrastructure (Regulatory Levies) Act 2021 (collectively, the OEI) enacted in June

2022. The relevant OEI regulations and guidelines are being released in stages – the first, which covers the licensing schemes, fees and treatment of existing infrastructure, was released in final in early November 2022. The draft second tranche is expected in early 2023 and will cover management plans, financial security, protection zones and work health and safety.

Federal Climate Change and Energy Minister, Chris Bowen, also recently announced six ‘designated OffSW zones’ spread between New South Wales, Victora, Western Australia and Tasmania in order to commence the regulatory process around the granting of OffSW feasibility licences. Applicants must apply for these seven-year feasibility licences within the declared zones and applications are assessed against new merit criteria. Market sources suggest the first round of applications for feasibility licences is currently expected to commence in December 2022 with a five to six month application period closing May-June 2023, with licences currently expected to be granted in the September quarter 2023.

At the state level, Victoria has been first mover with its March 2022 ‘Offshore Wind Directions Paper’ which set targets including 2GW of OffSW power by 2032 increasing to 9GW by 2040. Victoria subsequently released its ‘Offshore Wind Implementation Statement’ in October 2022, outlining various efforts to enable and facilitate these targets with focus on coordinated transmission, preferred ports, local content, workforce training and the interface between State and Federal legislation. This is likely to be closely followed by NSW, which is currently exploring setting OffSW generation targets, particularly following the significant OffSW representation amongst the Illawarra REZ registrations of interest.

CAPACITY MECHANISMS DIVIDE OPINION

Another policy subject of particular interest and divided opinion is the need for a so-called 'capacity mechanism'4 being assessed by the Energy Security Board (ESB). Currently proposed to be operational by July 2025, State and Federal Energy Ministers also discussed the capacity mechanism at their mid-August EMM. Energy Ministers have agreed to take 'more active control' of the NEM 2025 redesign process from the ESB, focusing more on coal closures and new technologies, however, what this means going forward is yet to be determined.

Wildly unpopular with many in the power market, a capacity mechanism creates a new revenue stream for 'firm' (non-intermittent) generators (coal, gas, hydro and batteries). These entities would be rewarded for having generation capacity/plant available (but not necessarily operating) during certain periods, theoretically ensuring that supply will be adequate to meet demand. Although similar mechanisms exist in other international markets that are transitioning to renewables, there is disagreement over how successful such a mechanism will be at improving supply security (refer to what happened in June with coal plant unreliability) while potentially extending the lives of thermal plants. If a capacity mechanism does prevail, the devil will be in the detail of the design. To achieve net zero goals, while there is a circa ten-year transitional role for more flexible gas plants to play, it will be critical to ensure the lives of thermal generators are not prolonged unnecessarily and the exit of coal (and later gas) is orderly.

Arguably, the mechanism should only be applied to newbuild firm plants and will only be successful for net zero goals if it includes an emissions element, such that generators only receive a ratcheted capacity payment if they are below a certain emissions level.

Given the design difficulties of the capacity mechanism, consideration is also due to alternative options and technologies for providing firming capacity and improving energy security. Perhaps the most promising of these alternatives is what some are calling a Renewable Energy Storage Target (REST) – a target much like the Renewable Energy Target but designed to incentivise storage (and in particular deep/long duration storage) rather than generation.

ADDRESSING ENERGY STORAGE IS KEY

If we are to reach Australia's renewable targets and ensure the energy grid is capable of handling the growth anticipated by the ISP, storage capacity will need to grow by 59GW (20 times the current capacity) by 2050. Although we know storage is a challenge, it is currently the least advanced part of the renewables value chain.

Deep storage chemical batteries (of long-duration 12+ hours) are likely to be the quickest to deploy and easiest to site, but they are currently uneconomic and underdeveloped at this long-duration.

A REST could provide a form of subsidy to storage facilities, helping to overcome some cost-curve issues and incentivising the development of larger and deeper storage systems. The introduction of a REST would provide a subsidy and broader market for storage technologies, incentivise research and development into new storage innovations, and provide certainty around storage demand, supply and development. Contemporaneously, the value chains of the critical minerals which comprise chemical batteries also need to develop and accelerate.

OPPORTUNITY IN COMPLEXITY

Reshaping the energy market to deal with the deeply complex challenges of the rapid shift to renewables will take time, patience and collaboration across all parts of the sector. We eagerly await the outcomes of these and other energy market reforms, which will give investors greater clarity and confidence to make the most of the opportunities to help build a clean, affordable and reliable energy future for a more sustainable Australia.

To learn more about the opportunities inherent in the Australian power market today, or to discuss your utility-scale renewable energy project, please reach out to Energy Transition Partner, Katie Barnett at www.pwc.com.au.