Detached Single Family Housing – Continued development of detached, single-family housing.

Missing Middle Housing – Varied housing forms with 2-16 attached units, either rental or condo, addressing affordability, senior accessibility, and neighborhood compatibility.

Housing for Seniors – Independent and assisted living units for the growing senior population. Some of these units should be targeted downtown, within walking distance of services and opportunities for socialization.

How to Use this Report

This findings of this report should be taken into consideration when reviewing residential development proposals, plans, and other decisions affecting housing in the City of Menasha. However, it is important to note that the findings of this report are a snapshot in time and reflect the existing conditions of the Menasha housing market circa 2024. Locally, regionally, and nationally, the underlying factors affecting the housing market continues to be in a state of flux.As a result, the findings of the report may need to be reevaluated overtime to stay consistent with up-to-date trends and community conditions.

Housing Gaps and Opportunities

The 517-707 owner-occupied units that are projected to be needed in the local housing market by 2040 should be in the following categories:

• 135-184 subsidized/low-income units

• 87-118 workforce units

• 222-303 market rate units

• 74-101 luxury units

The 510-619 rental units that are projected to be needed in the local housing market by 2040 should be in the following categories:

• 110-133 subsidized/low-income units

• 115-139 workforce units

• 142-172 market rate units

• 144-175 luxury units

An additional 10 assisted living units are needed for seniors by 2040.

A total of 33 subsidized and 51 market rate senior units are needed by 2030.

STUDY PROCESS

Introduction

This study was commissioned by the City Council to inventory the existing housing stock in the city and assess where gaps exist in the housing market. The purpose of the study is to help the city better understand its housing market and to craft targeted strategies to improve options within the community.The study process began in January 2024 and was completed in June 2024. Project oversight was provided by City of Menasha staff.

Primary Data Sources

• US Bureau of Labor Statistics and American Community Survey (ACS) 2018-2022 Estimates

• Wisconsin Department of Administration Population Projections (2025-2040)*

• CoStar

• Job Center of Wisconsin (2024)

• Zillow

• Wisconsin Balance of State Continuum of Care

• United for ALICE Wisconsin

• US Department of Housing and Urban Development Comprehensive Housing Affordability Strategy Data (2020)*

• Menasha Comprehensive Plan/Water St Corridor Plan/Downtown Vision Plan

• Menasha Municipal Code

• City Building/Zoning Data

• Outagamie County Housing Study (2022)

Interviews and Focus Groups

• NAIP

• REALTORS Association of Northeast Wisconsin

• Menasha Joint School District

• Fox Cities Chamber of Commerce

• Greater Fox Cities Are Habitat for Humanity

• Dura Fibre

• FORE

• Atkins Family Builders

• REMAX

• River City Realtors

• Martenson & Eisele

DEFINITIONS

Included here are definitions of housing terminology that is used throughout this report. Please consult this page to give greater context to the analysis and recommendations provided.

• Affordable Housing – Housing and associated costs (i.e., property taxes, utilities, etc.) that total less than 30% of a household’s income.

• Housing Cost Burden – A household is considered cost burdened when spending over 30% of total household income on housing and associated costs.

• Area Median Income (AMI) – The median household income of a given area (in Menasha this is $62, 514).

• Subsidized Housing – Housing affordable to households earning typically below 60 percent of area median income that require subsidy in order to be considered affordable. Units are typically funded, owned and operated by mission-driven organizations including local governments, nonprofits and more.

• Workforce Housing – Housing affordable to households earning between 60 and 120 percent of area median income.

• Market Rate Housing – Housing affordable to households earning 100 percent or above of area median income.

• Luxury Housing – Housing affordable to households earning120 percent or above of area median income.

ENGAGEMENT METHODS

Stakeholders and organizations with interest and knowledge of the Menasha and Fox Cities housing market were consulted to inform this study. From January to March, 3 individual interviews and 3 focus groups were conducted.The stakeholders interviewed are displayed here.

ABOUT MENASHA

COMMUNITY BASICS

The City of Menasha is in both Winnebago and Calumet Counties, bordering the Fox River, Little Lake Butte Des Morts, and the northwestern portion of Lake Winnebago. US Hwy 10 and State Hwys 114 and 47 intersect the City with easy access to Interstate 41.

The City is located within the larger Fox Cities metropolitan area and is neighbored by Appleton, Neenah, Harrison, Fox Crossing, and Oshkosh.

This purpose of this study is to assist the City of Menasha in better understanding its housing market needs and demands currently and over the next 5 to 15 years, as well as recommend strategies for boosting housing production and affordability.

City of Menasha

REGIONAL OVERVIEW

While this report is focused on housing conditions and needs within the confinements of City borders, it does reference regional projections and conditions. The City exists in the larger Fox Cities region and makes up 7% of the total population falling under the Fox Cities metropolitan planning organization (MPO) area. This region and the surrounding municipalities are noted within the report for comparison. For county comparison,Winnebago County is used most frequently as it is where a majority of City area is located in. However, Calumet county also encompasses are portion of the City to the west.

Fox Cities Metropolitan Planning Area

There are key differences in comparing Calumet County versus Winnebago County. Calumet County is generally higher in income, has a greater share of owner households, larger household size, higher valued homes and rental units, and is slightly older in its population.While much larger in population, Winnebago has seen significantly lower growth in population over that last decade.These distinctions should be in mind when considering community development goals.

Source: Wisconsin Department of Transportation, US Census Bureau ACS

POPULATION CHANGE AND FUTURE PROJECTIONS

Menasha saw higher population growth from 2010-2020 (5.3%) in comparison to Winnebago County and the State (2.7% and 2.0%, respectively).The City added 296 people between 2020 and 2023.

The Wisconsin DOA population projections, adjusted to reflect the results of the 2020 U.S. Census count, estimate the Menasha will grow about 10% between 2020-2040 (1,828 people).

Continued growth in the Fox Cities Metro combined with the City’s constrained borders will likely cause additional growth pressure in years to come. Market shifts or significant development changes within the Fox Cities region will impact the projections provided.

HOUSEHOLD CHANGE AND FUTURE PROJECTIONS

The total number of households in Menasha increased over 13% since 2010 and is projected to increase at a slightly lower rate over the next 20 years (8%).The number of Winnebago County households is expected to increase by 14.7%, while the State is anticipated to see a 12% increase by 2040.

While the total number of households increased over the last 10 year, the average household size in Menasha decreased. In 2013, the average household size was 2.36; as of 2022 it fell to 2.25. Household size is projected to continue decreasing through 2040, attributed to smaller families and more people living alone.This is a trend seen across Wisconsin and the U.S.

The falling household size trend indicates additional demand for smaller sized housing units (1-2 bedrooms at 700-1,600 sqft) in both rental and ownership markets, such as attached single family townhomes and duplexes housing products that interviewees noted were in high demand.

2.25

Source: Wisconsin Department of Administration, US Census Bureau ACS

Menasha (left axis) Winnebago County (right axis)

AGE COHORTS AND FUTURE PROJECTIONS

35-54Yrs Old

Housing preferences change with age:

• The youngest independent households (2034) tend to demand smaller, more affordable housing units, especially before they have children or while those children are young.

20-34Yrs Old

65-84Yrs Old

Source: Wisconsin Department of Administration, US Census Bureau ACS

10-19Yrs Old

0-9Yrs Old

55-64Yrs Old

• The 35-54 age group has the strongest demand for larger housing units, given they are most likely to have growing families.

• Beyond age 55, and especially beyond 65, households may prefer to downsize for easier upkeep and accessibility.

In recent years, the fastest growing age cohort of Winnebago County was 65 and older. From 20152020, the 65-84 age bracket rose 16%. By 2040, this group will grow another 41%.

85+Yrs Old

The 85+ age cohort is projected to increase 117% between 2020-2040.This age group is the fastest growing statewide. Cohorts aged 0–9 and 10–19 are also projected to increase between 2020-2040 (18% and 21%, respectively). All remaining age cohorts are projected to remain stable over this same period.

Winnebago County Age Cohort Projections

EMPLOYMENT INDICATORS

Employment is often a significant factor in a person's decision for where to live. As of 2021, there were about 8,000 employed people living in Menasha, but employed outside the City. On the contrary, 7,000 people were employed in Menasha but lived outside of the City. Only 676 people lived and were employed within Menasha.

There is a high degree of employment mobility within the Fox Cities metro area. Most people who work in Menasha are commuting in from nearby communities (Appleton, Neenah, etc.) and most Menasha residents are traveling for work outside of the City. For those who travel for work, the majority of driving commute times are relatively short (under 24 minutes), indicating they are staying in the region.The “other locations” category in the middle chart above represents workers living in the surrounding townships within the Fox Cities region.

Menasha Inflow Outflow Job Counts Where Workers in Menasha Live

Average Daily Commute for Menasha Residents

Source: US Census Bureau On The Map

Source: US Census Bureau ACS

Source: US Census Bureau ACS

INCOME TRENDS

Median household income in Menasha remains lower as compared to Winnebago County ($62,514 vs. $70,041). Since 2019, the City has seen a significant increase in number of lowest income households (< $50K) and greatest decrease in highest income households (> $100K).The County overall observed the opposite trend during this period.

While wage growth has increased 15.2% since 2019, median rents and home sales have increased 36% and 53%, respectively. Since housing costs are typically the largest share of a household's living expenses, this indicates that wages are largely not keeping up with the rising cost of living.

City of Menasha

County

City of Menasha Winnebago County

EMPLOYMENT INDICATORS

Generally, the median salary of the major occupations in Menasha are below the level needed to comfortably purchase a home.The median household income for the City in 2022 was $62,514 which correlates to an affordable monthly rent of $1,563 and affordable home price of $221,700. In 2024, the median single-family home value was $300,000.

Source: US Census Bureau ACS, Job Center of Wisconsin, Zillow

Top Employers Located in Menasha (2020)

Top Occupations in Menasha (2022)

ACCESS TO BROADBAND

Access to broadband is often linked to household income. For Menasha households making less than $20,000 annually, nearly 40% do not have internet access.This is the highest level amongst the communities surrounding Menasha.

As the economy becomes more reliant on the internet, access to broadband service is key to unlocking economic opportunity. One of the trends observed in the post-pandemic digital economy is the greater shift towards working from home. In 2022, nearly10% of Menasha residents worked from home full time (3.8% in 2015), and even more presumably work in a hybrid work environment.

Programs to grow broadband access will be important to bridge the “digital divide” and increase options for those

Winnebago County Menasha

Percent of Households without Broadband

Source: HUD CHAS

STUDENT POPULATION

Like many other communities, Menasha has been dealing with declining school enrollment in their K-12 school district. From 2019 to 2023, Menasha Joint School District lost 171 students or a 5% decrease in student population. Statewide, enrollment has dropped 3.8% during that same time period. K-12 student population peaked in Wisconsin in 1997-1998 when a majority of Millennials were school age. Since then, enrollment has declined annually and more rapidly since the pandemic. Enrollment is projected to decrease 1-2% each year through 2033.

Declining enrollment translates to less money to spend on existing students, facilities, and faculty. Many communities, including Menasha, are having to make difficult choices about the future of their school infrastructure leading to many schools closing in recent years.

At the higher ed level, there are 4 universities within a 30-minute drive from Menasha.These include UW-Oshkosh at Fox Cities (1,367 students), Lawrence University (1,426 students), Lakeland University (~600 students), and UW-Oshkosh (7,949 students). It will be important to monitor the changes in higher ed including closures and shift towards online degree program when considering housing need.

Jefferson Elementary School is slated to close after the 2024 school year; however, it may find new life as a districtwide Wraparound 4K program.

Other schools, like Nicolet Elementary School which closed in 2022, can be converted into housing or other uses.

Flexibility in school space will be key in planning for changes in student population.

Menasha Joint School District Neenah Joint School District Appleton Area School District

Enrollment in K-12 School Districts

Source: Wisconsin DPI

TRANSPORTATION

Of the roughly 9,000 employed people in Menasha, 80% of them drive alone to work and 10% work from home full-time. 8% of workers carpool, while the remaining commute by public transportation, bike or foot, or use a taxi or motorcycle.

This aligns with statewide commuter trends in 2022. Notably, biking and walking to work is more common statewide with 3.3% of workers using these modes. Pedestrian and bicycle-oriented development is important for connecting residents to employment centers, schools, shops and restaurants, and public spaces like parks. Given the lack of developable land within Menasha, the City should prioritize development patterns that emphasize pedestrian and bicycle connectivity and create infill within existing development areas.

I-41 Expansion

Starting in 2024, the WisDOT is working on Interstate-41 to reconstruct and expand 23 miles of the highway. I-41 runs northwest of City limits but is a main mode of travel for Menasha residents.The expansion will increase the number of lanes from 4 to 6 reducing commute time and lead to greater capacity. City officials should monitor impacts of the I-41 expansion on business and community growth in the years ahead.

City of Menasha Commuting to WorkTrends

Worked from Home

GENERAL HOUSING CHARACTERISTICS

HOUSEHOLDS BY TENURE

City of Menasha and Surrounding Community Housing Tenure

Renter households represent 36% of total households in Menasha.This is similar to the housing tenure split across the region and in Winnebago County. Statewide, renters represent roughly 32% of total households. Notably, Calumet County household tenure is composed of considerably more owneroccupied units representing 81% of total households.

In 2019, renters represented 39% of total households in Menasha.The decrease in renter households aligns with the City’s goal of increasing its share of owner-occupied units, specifically in the downtown core. At the same time, interviewees have cited that there is strong demand for rental units as the ownership market remains relatively more unaffordable for potential buyers. Source: US Census Bureau ACS

HOUSING TYPE BY UNIT

The most common structure type in Menasha,Winnebago County, and statewide is detached, single-unit homes.

The second most common structure type in the City and County is 5-19 unit buildings. Statewide the second most common housing type is 20+ unit multi-family buildings.

Providing a variety of unit types is essential to allow residents choice within a housing market.

City of Menasha Housing UnitType

Winnebago County Housing UnitType

Source: US Census Bureau ACS

YEAR STRUCTURE BUILT

Nearly 50% of all housing units in Menasha were built before 1970. Compared to the County, Menasha has a relatively older housing stock. Older homes can lack amenities that current buyers are interested in, often require rehabilitation, and tend to have higher maintenance costs.

The peak of residential construction in the City was prior to 1969, with a secondary boom between 1990-2009, followed by a slow down due to the Great Recession. Since 2010, owner-occupied homes have still outpaced renter-occupied development (418 units versus 211 units, respectively).

City of Menasha Winnebago County

CONSTRUCTION ACTIVITY

Building permit data shows a real time trend of new construction in Menasha. Single family home construction has fallen significantly since its high in 2003. Meanwhile, two-family home construction has not contributed meaningful unit production in the last two decades.

Multi-unit building construction has extremely low coming out of the Great Recession which has been typical of many communities. However, there has been a significant uptick with several projects completed between 2023 and 2024, mirroring national trends in multi-family development.

Notably, included in the multi-family permit data are several commercial to residential property conversions, such as the Harbor Lofts and BantaVillage.

Single Family and Two-Family Home Construction Permits

RENTAL MARKET

RENTER OCCUPIED PROPERTIES – EXAMPLE

AFFORDABILITY

The table below shows the general monthly rent a household could afford, by household size, at various income levels as a percentage of the Area Median Income (AMI). Using HUD methodology, the median household income of $62,514 is used to calculate the maximum amount a median household could spend on monthly rent for it to be considered affordable is $1,563. In comparison, the median monthly rent in 2024 was $1,017 in Menasha, meaning households earning over 80% AMI can generally afford rent, but households falling below that income may be cost burdened.

A household that spends more than 30% of its income on housing is considered cost burdened. A household that spends more than 50% is considered severely cost burdened. In Menasha nearly 40% of renters are cost burdened, which is high in comparison to surrounding communities.The percentage of renters who are cost burdened in Menasha is much higher than homeowners.This is typical in most communities given that renters tend to have lower incomes than homeowners and face more barriers in securing the financing required for homeownership.

Source: US Census Bureau ACS

HOUSING STRESS

Cost Burden - Renters

Amongst cost burdened renters, nearly 19% (580 households) are severely cost burdened (spending more than 50% of their income on housing costs).

Cost burden amongst Menasha residents exists primarily with renter households at or below 50% of the area median income—those considered very low or extremely low income.

According to the Comprehensive Housing Affordability Statistics (CHAS) from HUD, there is an under supply of rental units affordable to those earning the lowest incomes and highest incomes, suggesting a need for both subsidized and higher-rent,“luxury” units in the market.

Rental Unit Mismatch

RENTAL UNIT CONSUMPTION

The figure on the upper right shows 56% of rental units affordable to those earning 30% or less of AMI (under $18,750 annually) are being rented by households at that income level. 44% of these units are rented by households earning more than 30% AMI. Meanwhile, 58% of the units affordable to households earning more than 80% AMI (over $50,000 annually) are rented by households earning less than that. This indicates that higher income households are “renting down”, which tightens the market of units affordable to lower income households.

While this data shows that most households are spending below their means (less than 30% of their income), it also indicates that many lowest-income households are spending above their means to secure housing.

Adding more choices at appropriate price points will draw households toward housing that fits their needs and budget and can decrease cost burden among renters across the market.

Median Income (AMI) in 2022: $62,514

Households by Income and Tenure

Rental Unit Consumption by Income

UNIT TYPES

Historically, medium-sized apartment buildings have been built in Menasha and in the region. Nearly 1/3 of the current rental housing stock in Menasha are 5-19 unit structures. This type is a desired building size, as it's more cohesive within the traditional neighborhood setting.As seen on the Rental Properties by Size map following page), many of these buildings are clustered within the downtown.

Recently, both across Wisconsin and nationally, multi-unit residential developments have been favoring larger buildings (20+ units).This can be attributed in part to increasing housing costs, meaning larger builds are more economical. However, these larger structures can have negative impacts on existing neighborhoods. It is important to have a diversity of housing options and that includes a variety of development sizes that fit into new and existing neighborhoods.

RENTAL PROPERTIES BY SIZE

Source: CoStar

RENTAL COST

Among peer communities, Menasha generally sees lower rents for units of all sizes.The majority of rental units in the City are priced between $500 to $999 per month according to American Community Survey 5-year estimates. These estimates are likely low as they do not reflect the 100+ new rental units constructed in the past several years. Recent new rentals that could affect rising rent prices in the city are the Brin, BantaVillage, Discovery Point, Lakeshore Ridge Apartments, and Harbor Lofts. Median rent as of 2024 ($1,017) in the City still sit below the state and national average of $1,160 and $1,517, respectively.

Median Rent by Bedroom (2022)

# of Bedrooms

Unit Rents (2022)

(2024)

City of Menasha City of Neenah City of Appleton Village of Fox Crossing

RENTAL VACANCY

Vacancy rates are an important measure of balance between housing demand and supply.

Menasha’s vacancy rate is estimated at 4%, well below the State rental vacancy rate of 5.1%. A typically healthy rental vacancy rate is between 5-7%. This indicates there is more demand than supply, making it harder for renters to find units and easier for landlords to raise rents.This also indicates there is opportunity for more rental unit development in the City.

The short supply of rental units was confirmed in interviews with local housing experts.These experts noted that 1- and 2-bedroom units were in highest demand.This is also expected given shrinking average household size.

Vacancy Rate of Menasha and Surrounding Communities (2024)

Source: CoStar

City of Menasha City of Neenah City of Appleton Village of Fox Crossing

AGE OF RENTAL STOCK

54% of the rental units in Menasha were built prior to 1990, indicating an aging rental housing stock. However, older units generally translate into more affordable rental prices and are often referred to as “naturally occurring affordable housing” (NOAH).The median rent for units produced prior to 1990 is $863 per month, according to CoStar.

On the other hand, new rental units provide greater housing choice for residents—especially those at 80-100% of AMI. Since 2010, only 211 units have been built, roughly 7% of total rental stock.The median rent for units produced after 2010 is $1,384 per month, according to CoStar.

Source: US Census Bureau ACS, CoStar

Rental Housing byYear Built

NEW/RECENT RENTAL STOCK

The following rental projects were completed within the last 10 years:

• Harbor Lofts (Built 2023, 14 units)

• BantaVillage (Built 2023, 34 units)

• Lakeshore Ridge (Built 2023,120 units)

• The Brin (Built 2024, 43 units)

Potential Projects

• Shopko Redevelopment (Mixed Use Residential)

BantaVillage

Lakeshore Ridge

Harbor Lofts

Source: City of Menasha

DEVELOPMENT SCENARIO

There is a need for new rental construction in the City that serves both low- and high-income earners.

High income earning households can often afford rents associated with higher cost of new-construction and developers can market increased costs through increased amenities; however, lower income households largely cannot afford new construction and settle for older, less amenity rich units.

The table at the right displays an example scenario of the cost to construct a 1-bedroom new construction and the monthly rent needed for the developer to breakeven.At a breakeven rent of approximately $1,600/month, this matches the current leasing rates of new construction rental units in Menasha. Meanwhile, the maximum affordable rent the median household can spend without being cost burdened is $1,563.

It is clear, to ensure expanded opportunities and units that meet the needs of all residents, subsidies are likely needed to offset construction costs to make units more affordable.

OWNERSHIP MARKET

AFFORDABILITY

The table above shows the general purchase price a household could afford at various income levels and household sizes, without being cost burdened (paying more than 30% of gross income paid towards housing). Most of these price points are a challenge for developers to build at due to increasing costs of labor and supplies.

57% of the City’s owner-occupied households earn an income that is 100% or more of the area median income indicating most owner households are capable of purchasing a home at or above $220,000 which is also the current median value of a starter home in the City.

Income Levels for Homeowners in Menasha

HOUSING STRESS

When a housing market is “tight” or competitive, this drives up costs for consumers and makes it harder for households without down payment savings.

While the rental market shows higher levels of cost burden, the ownership housing market experiences cost burden less frequently. Homeownership has barriers to entry, so people must qualify to buy by meeting underwriting standards.These standards serve to reduce risk to borrowers and lenders by ensuring adequate income, increased access to credit, etc.

OWNER STRESS BY INCOME

In Menasha, the vast majority of homeowners are not cost burdened.The greatest cost burden is seen for households earning less 30% of the area median income.

Ownership unit mismatch shows homes available in the market are generally oversupplied in the lower cost market, likely a reflection of a sizeable number of aging homes in the City.

The unit mismatch table shows that there is a very low supply of housing that is affordable only to higher income level households.This is important to note as the population projections show high growth in the area and more owner-occupied housing will be needed.

Ownership Unit Mismatch

Cost Burden by Household Income for Homeowners

HOMEOWNERSHIP UNIT CONSUMPTION

In Menasha, many homeowners own houses considered affordable relative to their incomes.

The graph on the bottom left illustrates the consumption of affordable ownership units at various household income levels. Almost 2/3 of homes affordable to households earning 50% of the median income are owned by households making 80% or more than the area median income.This can be a challenge for lower income families to purchase a home, as higher-income families can offer more money, better terms, and use standard mortgage types (not FHA).There is a very low percentage (about 12%) of homeowners in the City that are 0-50% AMI, even though most of the ownership units are affordable at that income level (see the prior page). This reflects the barriers to entry into the ownership market for lower-income households. Because of these barriers, many households are forced to keep renting, putting further strain on the rental market.

HOUSING COST

The median home value in Menasha has seen persistent growth in the postpandemic era.The current estimate for median home value is $300,000, up from $197,000 in March 2019. The median home price has risen by 53% in the past 5 years in Menasha, which tracks state and national trends. From 2017 to 2022, the median home sale price in Wisconsin increased by more than 50%, while median household incomes in the state increased by only 19.7%, according to the Wisconsin Policy Forum.

Many of the new homes being added to the market are priced at $400K or higher. The employer focus group emphasized there is a great need for new homes, or existing homes to enter the market, in the $250-300K range.

Menasha Appleton Neenah Kimberly

Median Sales Price for All Homes

Source: Zillow

STARTER HOME COST

Lower-Income Households that own their housing commonly occupy what is referred to as the “starter home” market. For purposes of this study, this is tracked as the “Bottom Tier Home Value” and is the median of the 5th to 35th percentile of all home values within the City.

Starter homes followed the same general trend going into and coming out of the recession: consistently steady cost increases over the past decade. Menasha tracks higher than its peers in affordable starter homes at $217,000.

The median household of 4 would just be able to afford the median starter home in the City ($217,000 entry cost vs $221,000 purchase limit). For Menasha households earning under the median income, homeownership remains out of reach.

$217,071

Menasha Appleton Neenah Kimberly

Source: Zillow

Starter Home Value

UNIT TYPES

Single-unit detached (single-family) is the most prevalent owner-occupied unit type in the City (88% of the housing stock).

Mobile Home is the second most common unit type in the City. Five Oaks Park mobile home park encompasses 300 home sites offering an affordable entry point to those looking for a smaller size home.

Owner occupied 1-unit attached (twin homes) and multi-unit condo buildings are not as prevalent. Condos offer an opportunity for denser redevelopment in areas of the downtown and can provide a more affordable option for home ownership but can price can vary based on building footprint and age. Additional condo developments are proposed in the City though they are not approved or under construction at the time of this report and not reflected in the data.

Owner Unit Types

OWNERSHIP UNIT SIZE

Over 78% of owner-occupied housing has three or more bedrooms. Meanwhile, household size continues to decrease within the City, indicating decreasing need for larger homes. Larger home often have a more difficult time finding buyers according to the builder focus group.

Homes with fewer bedrooms are generally more affordable both within existing and new-construction markets. Ownership units with one and two bedrooms can fill a niche in the market, accommodating households who wish to downsize as they age and households who may be first-time homebuyers. This is consistent with responses from interviewees observing growing demand for smaller size homes that are more affordable.

Number of Bedrooms

Source: US Census Bureau ACS

HOUSING AGE OF OWNER-OCCUPIED HOUSING

Approximately 51% of owner-occupied homes were built prior to 1970.While older housing units tend to be more affordable and offer opportunity for households with lower incomes and entry-level homebuyers, there is also significant cost and work involved with remodeling these homes as noted in our interviews with local housing experts.

Owner-occupied housing produced since 2010 has been extremely low compared to previous periods and represents only 7% of total owner-occupied units. The ownership housing that has been produced since 2010 has a sale price starting at $380,000 with many homes well above $500,000.

Source: US Census Bureau ACS, CoStar

Ownership Housing byYear Built

NEW/RECENT OWNER OCCUPIED PROJECTS

The following ownership projects were completed in recent years:

• Lake Park (Townhomes and SF Detached Homes)

• Woodland Lake Cottages (SF Detached Homes)

• Grassymeadow Ln/Brie Ct (SF Detached Homes)

• Lake Cottage Ct (SF Detached Homes)

• Lake Park Heights (SF Detached Homes)

• Woodland Heights (SF Detached)

Potential Projects

• 477 Ahnaip St (6 SF Attached Homes)

• 449 Ahnaip St (~12 SF Attached Homes)

• 1109/1101 Province Terrace and 2027 Manitowoc Rd (16-22 SF Attached Homes)

• Creekside Estates (SF Attached and Detached Homes)

Woodland Lake Cottages

Lake Park Community

Grassymeadow Ln

1109 ProvinceTerrace

Source: City of Menasha

DEVELOPMENT SCENARIO

There is a need for more owner-occupied housing units, for both detached and attached homes.The figure to the right illustrates the approximate cost of home production by square footage.Within the Fox Cities area, building costs can range from $120-250/sqft according to Fixr, a national cost estimator. A mid-range cost of $200/sqft is assumed for the City of Menasha. Land and infrastructure costs included are assumed at $3.50/sqft.

Scenarios are displayed for home sizes of

• 1,200 sqft (small SF attached/detached)

• 1,500 sqft (medium SF detached)

• 1,800 sqft (large SF detached)

Builders typically include for a 20% mark up on homes. Including this calculation, new home prices are likely to range from $320,000 to $490,000 based on the square footages to the right.This tracks with recent 1,500 sqft homes selling for roughly $400,000.

Builders are increasingly looking to build smaller homes at a greater density in response to market demands for more affordable housing.Attached townhomes are one way to achieve this.A 1,200 sqft townhome may be sold close to below $300,000 which is achievable for Menasha households making roughly $90,000.

HOUSING FOR SPECIAL POPULATIONS

ALICE HOUSEHOLDS

ALICE is an acronym for Asset Limited, Income Constrained, Employed households that earn more than the Federal Poverty Level, but less than the basic cost of living for the county (the ALICE Threshold).While conditions have improved for some households, many continue to struggle, especially as wages fail to keep pace with the cost of household essentials including but not limited to housing.

33% of households in Winnebago County were considered ALICE or below the Federal Poverty Level in 2021. The City of Menasha was well above the County average with 40% of households considered ALICE or below the Federal Poverty Level. The number of ALICE households has increased from 2010, while the number of households at a household income at or below the federal poverty line has generally stayed the same.

Winnebago County ALICE and Poverty Households Change OverTime

Winnebago County Financial Status by Household Type

HOMELESSNESS

The Winnebagoland Housing Coalition (WHC) and Fox Cities CoC are groups that work to address homelessness in the Winnebago County region. Both participate in the statewide Wisconsin Balance of State Continuum of Care (CoC) program that supports agencies, coalitions, and non-profits around Wisconsin to end homelessness. Support includes funding assistance, optimizing delivery of homelessness services, providing education to the public and advocating for those in need, and promoting the CoC mission.

Point in Time count data from the local CoCs indicate that there is approximately 450 individuals in the Fox Cities and Winnebago County region receiving homeless services as of 2023, up from 375 in 2019.

The Winnebagoland 2021 Homeless Continuum Report cites that the impact of the COVID19 pandemic has exacerbated the homelessness crisis in the region, as well as key indicators such as housing cost burden and poverty.The report recommends greater collaboration among staff, development of new shelters and housing services, and establishing a task force to address youth homelessness.

Menasha does not have a formal homeless shelter within the City; however, with 7% of the Fox Cities MPO population, existing services for youth and families experiencing hardship can be found in the City through the headquarters for United Way Fox Cities, Leaven, Habitat for Humanity, Salvation Army, Goodwill, FoxValley Workforce Development Board, St. Joesph Food Pantry, Hope Homes, Neenah-Menasha Emergency Society, Advocap, Samaritan Counseling, the Boys and Girls Club of Menasha, and a number of other local charities or social services organizations. The City should continue to support dialogue with these groups and provide resources on the City website.

Point inTime Homeless Population Count byYear

Winnebagoland

Source: Wisconsin Balance of State Continuum of

AGING POPULATION

Senior households are anticipated to have the largest percentage of growth through 2040.As seen in the lower right figure, the majority of seniors are homeowners. Some senior will continue to live in their own home with virtually no support services, while some will look to townhomes and apartments that offer the ability to “downsize”, specialized housing with limited services, and different types of assisted living facilities. Often senior households will pay up to 50% of their income for market rate senior housing and up to 90% for specialized living.

City of Menasha Senior Household Income

City of Menasha Household by Age andTenure

DISABLED POPULATIONS AND ACCESSIBILITY

Those with an ambulatory, self-care, or independent living difficulty are most likely to require specialized forms of housing.

Most housing units are not traditionally constructed to accommodate aging or disabled populations (e.g. wider doorways, lower counter tops, etc.)

City of Menasha Households with a Member with a Disability by Income and Type

New market rate and workforce housing should contain set-aside units that meet universal design standards.

Current trends show that there are residents across all income levels that have a disability, but many would qualify for subsidized housing (<80% AMI).

As the population continues to age, ensuring accessibility of new and existing homes should be a priority.

City of Menasha Persons with a Disability by Age and Type

STAKEHOLDER ENGAGEMENT SUMMARY

ENGAGEMENT METHODS

Stakeholders and organizations with interest and knowledge of the Menasha and Fox Cities housing market were consulted to inform this study. From January to March, 3 individual interviews and 3 focus groups were conducted.The stakeholders interviewed are displayed here.

INTERVIEWS

The 3 interviews conducted between February and March 2024 highlight the mismatch between housing inventory and demand seen throughout the region, state, and country.The interviewees had backgrounds in real estate, residential development and building, and housing advocacy.The key themes from the interviews are outlined below.

OverarchingThemes

1. Extremely Low Inventory – Low number of builds and lot creation has been prevalent in the region since the Great Recession.A recent uptick in construction has alleviated some of the inventory stress; however, there is still significant need for housing at all income levels, notably entry level single-family homes.

2. Strong Demand for all Housing Types – All housing types are in demand. Low interest rates during the pandemic, shifts in demographics and housing preferences—specifically for Baby Boomers and Millennials—and Gen Z looking for workforce housing has caused immense change in housing demand in recent years.Workforce and income-restricted housing are lacking as well as entry level homes priced between $250-300K. Senior housing needs to be addressed to absorb the incoming “Silver Tsunami.”

3. Costs are Up – Cost of construction, driven by materials and labor, skyrocketed coming out of the pandemic and have remained high.This has also contributed to higher home and rent prices. High interest rates have contributed to low turnover and greater risk for developers to take on a new development.

4. Opportunity for Infill – There’s been a recent push for City staff to revitalize the downtown. Constrained municipal borders have put the focus on infill opportunities. Redevelopment has occurred in the downtown in the form of office, retail, and multi-family uses. Consideration of funding programs should be taken in downtown development opportunities.

5. Challenges and Barriers – Developers are fewer, and risk is higher since the Great Recession and pandemic, reducing ability to keep up with demand. Regulations, including zoning code barriers, and development fees have made the development process slower and more cost prohibitive. Zoning code recommendations included reducing the number of residential districts, expanding allowed uses, and reducing minimum lot sizes.

6. Future Outlook – Interviewees are concerned about changing demographics, change in commuting patterns due to I-41 expansion, and high construction costs and interest rates. If communities would like to see more housing development, they need to be proactive in their housing policies and work to attract developers to potential sites.

FOCUS GROUPS

Focus group conversations with developers, builders, and local employers revealed additional insight into what the current condition of Menasha’s housing market, as well as identified barriers to housing development and potential solutions.

Developers

• High demand for affordable housing. Preference towards one and two-bedroom rental units and smaller single-family homes.

• Land availability, inability to receive financing and funding, resident pushback, and high costs have been major barriers to development.

• Potential solutions include reducing development fees and zoning code barriers, partnerships with land trusts, and municipal financing assistance such as TIF and interest free loans.

• Developers are monitoring the market uncertainty surrounding interest rates and demand shifts.

Builders

• Recent development projects have favored multi-family buildings, though builders have been involved in single-family, duplex, townhome, and mixed-use development types as well.

• Demand has been high for workforce housing and small single-family and duplex homes. Luxury apartment demand is slowing.

• Construction costs have been biggest barrier along with unclear permitting/development review processes, NIMBY-ism, and lack of buildable land zoned for residential.This has made it difficult to build affordable entry-level homes.

• Solutions focused on training/education for City leaders and the public, reducing zoning regulations, and allowing for greater density.

Local Employers

• Largest employment industries include manufacturing, education, and transportation. Entry-level jobs range from $20-25/hr.

• High rent and home prices are causing longer commutes for employees, difficulties recruiting employees, and employees with families to move to other school districts.

• Lack of available land and housing stock is hindering growth opportunities for Menasha.

• Education, updating the zoning code for more density, programs to help create workforce housing, and redevelopment of large sites into housing initiated by the City are seen as potential solutions.

• Proposed redevelopments include the quarry, old Shopko, and Lakeside Book site.

FUTURE COLLABORATION WITH COMMUNITY PARTNERS

Community Partners

• City and County Housing Authorities

• Menasha Joint School District/UW-Oshkosh at Fox Cities

• Nearby Jurisdictions

• Developers/Builders/Realtors

• Local Employers

• Community Members

• Housing Now Coalition

• Fox Cities Chamber of Commerce

• Greater Fox Cities Habitat for Humanity

• Strong Neighborhoods Program Stakeholders

• Fox Cities and Winnebagoland CoCs

Opportunities for Collaboration

1. Education & Advocacy – Shared education and advocacy materials both internally and externally ensures there is a common understanding of housing challenges and can create an opportunity to broaden a community’s collective knowledge.This includes engaging the public at community events to discuss housing issues and needs as well as educating elected officials and commission members.

2. Zoning Code Updates – Establish dialogue with stakeholders to discuss changes they would like to see to the zoning code to address barriers to housing development. Existing requested changes include allowing for more density and unity types by right, reducing minimum lot sizes, and reducing parking requirements.

3. Resources & Programs – Aggregate resources and programs available to partners and the public on the City website and other media modes to ensure access.

4. Share Information & Data – Community partner data combined with data from the City, including property information, tax delinquencies, code violations, building permits, and a series of other key indicators from national and institutional data sources should be available to all partners and the public.

5. Roundtables & Workshops – Hosted round tables and workshops give awareness to the housing crisis and provide a space to address it.

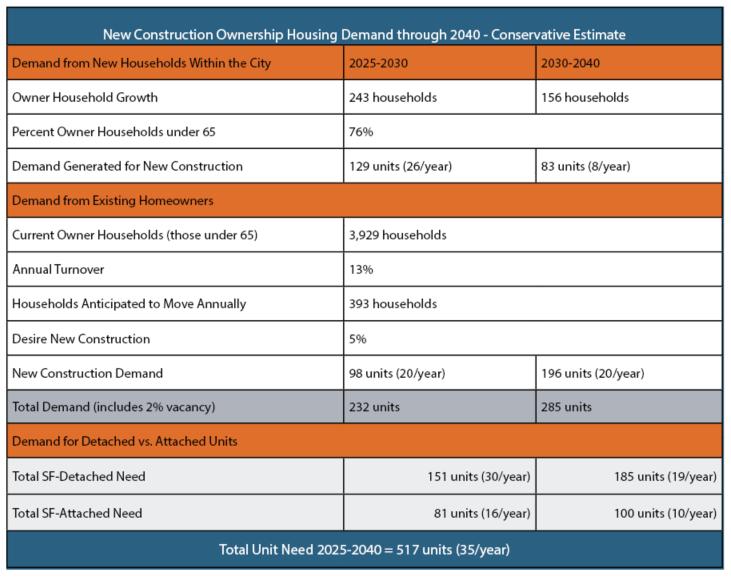

HOUSING NEEDS AND PRIORITIZATION

OWNER

OCCUPIED HOUSING UNITS NEEDED - CONSERVATIVE

The conservative household growth estimate uses the adjusted DOA’s projected growth rate for the City through 2040 (11%).

Under this scenario, there is a need for approximately 517 owner-occupied units over the next 15 years. Based on the current income distribution in Menasha, these units would ideally be priced in the following sale ranges (in 2024 dollars). However, this breakdown is subject to change as the income distribution in Menasha changes over the next 15 years:

• 135 subsidized/low-income units

• 87 workforce units

• 222 market rate units

• 74 luxury units

Regionally, the Outagamie Housing Study (2022) projects 10,910-17,738 new units needed between 2020-2030 in the Fox Cities and Greater Outagamie County.

OWNER OCCUPIED HOUSING UNITS NEEDED

- HIGH

The high household growth assumes a 16% growth in households in the City through 2040.This is consistent with the growth the County is anticipated to see through 2040.

Under this scenario, there is a need for approximately 707 owner-occupied units over the next 15 years. Based on the current income distribution in Menasha, these units would ideally be priced in the following sale ranges (in 2024 dollars). However, this breakdown is subject to change as the income distribution in Menasha changes over the next 15 years:

• 184 subsidized/low-income units

• 118 workforce units

• 303 market rate units

• 101 luxury units

Regionally, the Outagamie Housing Study (2022) projects 10,910-17,738 new units needed between 2020-2030 in the Fox Cities and Greater Outagamie County.

RENTER OCCUPIED HOUSING UNITS NEEDED - CONSERVATIVE

The conservative household growth estimate uses the adjusted DOA’s projected growth rate for the City through 2040 (11%).

Under this scenario, there is a need for approximately 510 rental units over the next 15 years. Based on the current income distribution in Menasha, these units would ideally be priced in the following sale ranges (in 2024 dollars). However, this breakdown is subject to change as the income distribution in Menasha changes over the next 15 years:

• 110 subsidized/low-income units

• 115 workforce units

• 142 market rate units

• 144 luxury units

Regionally, the Outagamie Housing Study (2022) projects 10,910-17,738 new units needed between 2020-2030 in the Fox Cities and Greater Outagamie County.

RENTER

OCCUPIED HOUSING UNITS NEEDED - HIGH

The high household growth assumes a 16% growth in households in the City through 2040.This is consistent with the growth the County is anticipated to see through 2040.

Under this scenario, there is a need for approximately 619 rental units over the next 15 years. Based on the current income distribution in Menasha, these units would ideally be priced in the following sale ranges (in 2024 dollars). However, this breakdown is subject to change as the income distribution in Menasha changes over the next 15 years:

• 133 subsidized/low-income units

• 139 workforce units

• 172 market rate units

• 175 luxury units

Regionally, the Outagamie Housing Study (2022) projects 10,910-17,738 new units needed between 2020-2030 in the Fox Cities and Greater Outagamie County.

SENIOR UNITS NEEDED-ASSISTED LIVING

The number of senior households is projected to increase by 23% in Menasha by 2040, up from 1,690 senior households currently. Planning for aging populations is essential to the success of the housing market in Menasha.

As seniors age some will need assistance with daily living (ADL) and need to move out of their current homes.

Menasha already has a significant network of assisted living facilities to meet these needs. Current estimates indicate demand for assisted living units may be satisfied through 2030, although with continued growth in aging households, additional units may be required. Projections for 2040 indicate need for 10 additional assisted living units in the City.

SENIOR UNITS NEEDED-INDEPENDENT LIVING

The number of senior households is projected to increase by 23% in Menasha by 2040, up from 1,690 senior households currently. Planning for aging populations is essential to the success of the housing market in Menasha.

Some seniors will not need assistance with daily living but will still desire to move and look for housing dedicated to seniors.

Many independent living units currently exist for seniors or 55+.These units vary by amenities provided and development type including luxury cottage-style homes and subsidized apartments. Projections for 2040 indicate need for 33 subsidized and 51 market rate independent living units in the City.

TYPES OF HOUSING NEEDED

UNDERLAYING FACTORS INFLUENCING AFFORDABILITY

Some of the most significant factors contributing to housing affordability, or the lack thereof, today are:

• Lagging Production: In both the rental and ownership markets, housing production since the 2008 housing market crash has not kept up with household growth. Nationally, experts estimate that there is a shortage of 4 to 7 million homes.* This low supply increases prices and competition across the market.

• Rising Interest Rates: In the decade after the 2008 recession, mortgage interest rates were relatively low (under 5%) and dropped even lower between 2020 and 2021 in the initial wake of the COVID19 pandemic. Since 2022 however, interest rates have increased substantially and are now at a 30-year high; the average 30-year mortgage interest rate is 7% as of April 2024.The combination of high housing prices due to limited inventory and high interest rates has pushed homeownership out of reach for many families.

• Zoning and Land Use Regulations: Zoning and subdivision ordinances govern what, where and how housing is developed. Overly restrictive or exclusionary zoning practices can contribute to housing un-affordability by slowing down (therefore increasing the cost) of the development process and by limiting the types housing allowed to be built. In both Menasha and communities across the U.S., most residential land is devoted exclusively to detached single family homes.

*Housing experts say there just aren't enough homes in the U.S. : NPR

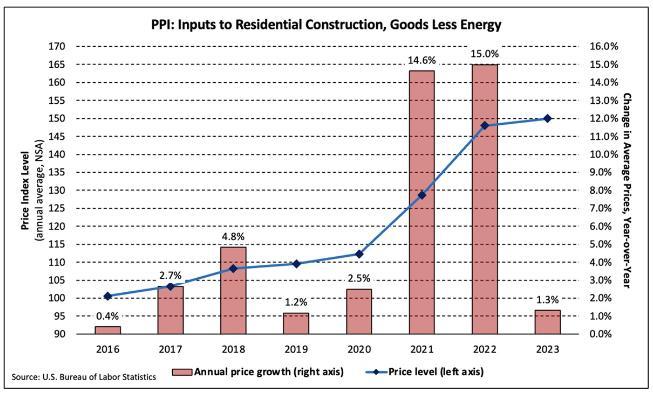

Another factor impacting affordability is the increasing cost of construction, particularly since the onset of the COVID-19 pandemic. Nationally, the overall cost of construction rose 37.7% between February 2020 and December 2022.* This rise was the result of several interacting factors, including global supply chain disruptions, inflation and interest rate hikes, rising insurance premiums, and labor shortages.

Thankfully, the average price increase for residential building materials fell dramatically between 2022 and 2023, according to the National Home Builders Association. However, building material prices and interest rates remain high relative to the pre-pandemic era. This is likely to inhibit housing production, making it more difficult to close the inventory shortage that is a primary contributor to high prices for both renters and owners.

While it is difficult to predict with precision how much a community will grow in the decades a head, it is true that population change influences the housing market—and vis versa. For instance, as Menasha’s senior population continues to expand as a percent of the total population, the demand for senior housing will increase in tandem. On the other hand, if the City invests in building more 1- and 2-bedroom rentals and attached single family homes/townhomes at affordable entry points, young people and families from the broader Fox Cities region will be more likely to move into the community.

The location and type of housing the City chooses to invest in will impact the City’s ability to grow—or stagnate—in the years ahead. Investing in denser, mixed-use developments with good pedestrian and biking connections are likely to attract Millennials and Gen Z. Redeveloping the City’s downtown riverfront (as noted in the future land use map and DowntownVision Plan) is a great opportunity over the next 15 years to attract these generations to Menasha and encourage them to set roots down in the community.

Screenshot from the 2018 City of Menasha Downtown Vision Plan

BARRIERS TO HOUSING

THE IMPACT OF “BY RIGHT” DEVELOPMENT

When zoning codes are overly restrictive, the development process can be severely inhibited. Amending zoning to broaden permitted land uses, design standards, and other regulations therefore is one way to reduce barriers to housing development.

In the absence of zoning that allows for a broader range building types by right, developers must obtain special use permits or rezonings that can add time, uncertainty, and cost to the process.This process can also invite community opposition to building types, like mixed-use and multi-family developments, that are otherwise consistent with the City’s Comprehensive Plan. This can in turn push developers to communities where the development process is more streamlined and certain.

RESIDENTIAL ZONING

The City’s ordinance has eight zones that allow for various types of residential development. Each zone is evaluated for dwelling types permitted by right (P) and what requires a special use permit (SU).

Townhomes and multi-family dwellings are allowed in R-2A, R-4, and TND.

Traditional Neighborhood Development allows for greatest housing diversity, but currently no City parcels are zoned for this district.

Interviews and focus group indicated that greater allowed densities and housing type diversities are favored to help improve the development process. It was also recommended that the City proactively zone properties to allow for more density.

According to the Land Use Chapter of the City’s Comprehensive Plan (updated in 2021), 43% of the City’s land area is comprised of single-family homes—the largest of any category. Multi-family housing makes up only 4% of the City’s total land area.

OTHER REGULATORY BARRIERS

Parking Minimums

Parking minimum requirements are another potential barrier to housing development, as it can ultimately limit how many housing units can be built on a property. The City’s current standards includes minimum and in some cases maximum for residential uses (as shown below). Generally, the City's minimums are on the low side; however, the multiple family requirement could be limiting in cases where efficiencies and 1-bedroom units are the primary unit mix.The City’s current standards for:

• Single Family Dwellings- At least 1 parking space, but no more than a total of 4 parking spaces for each single-family dwelling

• Two-Family and Multiple-Family Dwellings- At least 1.5 spaces for each dwelling unit. For two family dwellings, no more than a total of 4 parking spaces.

• Central Business- At least 1.5 spaces for each dwelling unit in a multi-family residential building.

Development Fees

Development fees are another potential barrier to housing as they increase a developer’s costs.At the same time, these fees provide revenue to the City to cover the cost of necessary services like safety inspections.

According to the 2022 Housing Fee Report, Menasha currently collects:

• Building Permit Fees

• Park Fees

• Plat Approval Fees

• Water of Sewer Hook-up Fees

• Stormwater Management Fees

In 2022, Menasha collected over $78,000 in fees, equating to $656.13 in fees per approved residential dwelling unit.The City also does not charge any impact fees or fees in lieu of land dedication. For comparison, in 2022 the City of Neenah charged $2,395.70 per new construction residential unit and the City of Appleton charged $626.56 per new approved residential dwelling unit. In 2020, the City of Oshkosh charged $1,403 per approved residential dwelling unit.These rates are subject to fluctuate year over year based on the number of new residential dwelling units approved.

LESSONS LEARNED FROM OTHER COMMUNITIES

The American Planning Association (APA), in collaboration with the National League of Cities, recently released the Housing Supply Accelerator Playbook.This report features a wealth of recommendations for removing barriers to housing development, as well as case studies from across the country. Below are three case studies from the handbook with relevance to Menasha.

Grand Rapids, MI

After several years of study and engagement, the City of Grand Rapids adopted a new zoning ordinance.The reconfiguration collapsed zone districts from multiple residential and commercial zone districts to a combination of three “Neighborhood Classifications” and a simplified list of “Zone Districts.” Residential zone districts, for example, shrank from seven to two but still offered a wide variety of housing types.The Zoning Code also provides incentive-based policies, such as minimum lot area reductions in exchange for meeting housing goals like accessible units and mixed-income housing. A review for uses listed as permitted and meeting all applicable standards (e.g., building design standards) is a counter review or director review process. A use listed as a special land use requires a public hearing with the Planning Commission so notified neighbors can provide input.

Lexington, KY

In 2018, Lexington adopted a series of reforms to promote infill and mixed-use development.The key updates included minimum parking requirements and allowing retail and multifamily by right in specific commercial areas. Lexington also converted to B6-P zoning, also called a “Planned Shopping Center.” This change allowed aging retail along commercial corridors to shed excess parking and transform into new retail and residential development. Planners could allow by-right residential development with no height limit, with virtually none of the opposition that happens when upzoning within existing residential areas

Portland, MN

Since 2014, average rents in Portland have increased by more than 80 percent as the city faces a serious housing problem.After careful planning and analysis, Portland opted to improve upon state mandates by approving a reform package allowing multifamily housing of up to four units on all residential lots by designating the entire city as a growth area (with sensible modifications for the Casco Bay islands) and allowing ADUs by right.The city also eliminated any parking requirements for these new units and increased flexibility in dimensional limitations, including lot size.These updates were approved within the broader context of previous local initiatives aimed at housing supply, including inclusionary zoning, special financing programs and a surplus land program

RECOMMENDATIONS

RECOMMENDATIONS

Zoning Amendments

Permit Cottage Clusters

Cottage Court style development is an affordable ownership option.This style of development includes small groupings of housing around a shared public space and may be particularly attractive to seniors looking to downsize. Cottage Courts can be implemented through PUD (Planning unit development) and TND zoning.Alternatively, Cottage Courts could be allowed by right under a Specific Requirements of Certain Land Uses section of the zoning code.

Parking Requirements

Parking requirements can impact density and make some developments less viable. Parking minimums should consider space requirements based on the unit type. Efficiencies and 1-bedroom units, and senior housing could potentially require only 1 space per unit. Rehabilitations of existing buildings could not require any parking.

Example Cottage Court

RECOMMENDATIONS

Zoning Amendments

Proactively Zone Properties for Housing

The City should identify and consider proactively rezoning properties to allow maximum diversity of housing types. The recommended redevelopment sites later in this chapter are all good candidates for rezoning for residential.

Add an Urban Residential Zoning District

An Urban Residential Zoning District would allow for greater density and traditional housing types.This zoning district follows the guidance of the Comprehensive Plan Land Use Chapter which recommends the creation of a separate residential zoning district with reduced lot sizes, reduced lot widths and setbacks to make older residential areas of the City conforming, single family attached units allowed by right, and allows for duplexes and multi-family buildings through a special use permit. Much of the downtown area is identified as Urban Residential in the future land use map.

Example of Urban Residential Development

RECOMMENDATIONS

Capacity Building & Communication

Provide Housing Education Programming

Many interviewees and focus groups cited a need for educational materials about housing issues and barriers that the community is facing.The results of this study can be utilized to provide housing education programming to public, practitioners, elected officials, landlords/tenants, and employers.The programming should address affordable housing need, resources and assistance programs available, benefits of diverse housing types, and supporting housing projects that meet needs of residents.

Engage with Community Partners

The City should continue to engage with community partners to forge a path forward in addressing housing affordability and need. Opportunities identified for collaboration include dialogue around zoning code updates, keeping an inventory of housing programs and resources, sharing data and information, and hosting frequent roundtables and workshops.

Housing Education Materials from Housing Now Coalition

Development processes require collaboration with multiple City departments and committees. Getting feedback and sign-off from each department in an efficient manner is a challenge in many communities.A strategy to improve the process would be to find ways to coordinate so everyone is looking at the application at the same time and explore opportunities to hold joint approval meetings.Any processes that can be consolidated or expedited would lower time (costs) to developers, which ultimately lowers costs to owners and renters.

• As of the time of the production of this report, the City is seeking quotes for permitting software that would improve the review process.Third party commercial plan review and delegation are also being considered.

Harbor Lofts

RECOMMENDATIONS

Initiatives

Assist in Development of Community LandTrust

Community land trusts acquire land and maintain ownership of it permanently, to ensure long-term housing affordability.

With prospective homeowners, land trusts enter into a longterm renewable lease.When the homeowner sells, the family earns only a portion of the increased property value.The remainder is held in trust, preserving affordability for future low- to moderate-income families.The City should contact the Madison Area Community Land Trust for best practices in developing this type of organization.

Prioritize Business Attraction

Continue to prioritize business attraction to provide retail, dining, and other commercial amenities residents are seeking. Form partnerships with local development corporations to execute projects consistent with community objectives

City-Owned Properties

The City should continue to identify and purchase properties that would be prime for redevelopment, in particular downtown, as well as locations in existing neighborhoods where smaller development projects (three-, four-plex, or small multi-family) serve as a means to increase affordability. The Redevelopment Development Authority is the recommended lead for this effort.

Downtown Menasha

RECOMMENDATIONS

Initiatives

Identify Areas Suitable for Mixed Unit Types

Small-lot and large-lot new development is needed, so are unit type mixes within new subdivision development. Integrating a mix of housing types (attached/detached, 3-9 unit rental) within subdivisions creates more choices and options in the housing market – ensuring households of all incomes can find suitable housing in most neighborhoods.This enables more people to stay in a neighborhood over time as their housing needs change.

For this initiative the city should identify:

• Sites that transition to higher intensity areas

• Sites large enough to place higher density with intensity of use transitioning down to single family density with existing neighborhoods

• Potentially mixed-use corridors

• Predesignated sites in new subdivisions

Example Townhomes

RECOMMENDATIONS

Initiatives

Provide Housing Options for Aging Seniors

The large share of senior households projected through 2040 is a major component of the local housing market.The City should develop accessibility programs to retrofit homes to age-in-place (potentially funded through the Strong Neighborhoods Initiative) and identify locations for senior apartments or condos. Providing attractive, affordable options for seniors who wish to move has the added benefit of putting those often older, more affordable homes seniors are currently living in back on the housing market.

Identify Areas Appropriate for “Luxury” Housing

There are households that could afford luxury unit rents, many of which are currently renting down into more affordable units. Development of additional luxury units is recommended to diversify the market and attract some of those households that are competing with lower-income households for housing, both renter- and owner-occupied units.Work with developers to identify areas that are appropriate for luxury housing.

Example Senior Housing

RECOMMENDATIONS

Funding

Continue Funding Strong Neighborhoods Initiative

The City should continue to fund and promote its Strong Neighborhood Initiative that assists homeowners in renovation and curb appeal projects by providing reimbursable grants and forgivable loans.The goals of this program are to increase the quality of Menasha’s housing stock, while also increasing the level of home ownership within the City.

The City could consider prioritizing projects or making an additional program that helps owners modify their homes to accommodate aging/disabilities and accessibility challenges.The program could possibly be amended to provide support for infill construction and redevelopment that improve an existing neighborhood.

Home rehabilitation projects can be funded through the Major Renovations or Curb Appeal program as part of the Strong Neighborhoods Initiative. Interested residents must meet the eligibility requirements outlined on the Strong Neighborhoods webpage and apply through the Community Development Department.

RECOMMENDATIONS

Funding

Amend Strong Neighborhoods Initiative to Provide Affordability Incentives

Federal Low Income Housing Tax Credit (LIHTC)

The City could consider adding additional programs to the Strong Neighborhoods Initiative to provide support for developing affordable units. This can be used for matching funds, land purchase, and new construction. Additional funds could come from TIF Affordable

Housing One-Year

Extensions, general obligation bonds, sale of surplus land, general fund budgeting and private contributions.This funding could be leveraged to make developers more competitive when applying for Low Income Housing Tax Credits (LIHTC) or WHEDA loan programs.

Wisconsin Low Income Housing Tax Credit (LIHTC)

Similar to the federal LIHTC program,Wisconsin offers a 4% noncompetitive state tax credit which can be used as match for the federal 4% program.Again, the City should seek to work with developers familiar with the LIHTC program.

For development of affordable housing in the community, seek out a developer familiar with LIHTC. LIHTC (or Section 42) is a federal program which gives the Wisconsin Housing and Economic Development Authority (WHEDA) the authority to issue tax credits for acquisition, rehabilitation or new construction of rental housing for low-income households.There are two types of tax credits available through this program: 1) Federal 9% Tax Credit (competitive) and 2) Federal 4% Tax Credit (non-competitive).The City should seek developers with LIHTC experience. This program offers the opportunity for new construction at rents that fit within the limits and demands of the community. Statewide and locally, we are hearing from employers that workers need local housing they can afford.

Employer-Assisted Housing

Employer-assisted housing is a type of housing program that involves employer or non-profit contributions into a fund to develop affordable housing or provide direct assistance to employees seeking housing. Sheboygan County Economic Development Corporation recently led efforts to establish a major employer and non-profit funded program called the Forward Fund.This program is being used to help develop affordable entry level homes in Sheboygan County.

RECOMMENDATIONS

Funding Down Payment Assistance

WHEDA and the Federal Home Loan Bank Of Chicago (FHLBC) already have down payment assistance programs which should be promoted.These programs are typically available for households at/below 80% AMI.The FHLBC Downpayment Plus program provides matching funds which could be matched from pools of local employers or from the City.

WHEDA 7/10 Flex Financing

The City should encourage developers to apply for these low interest loans that require developers to set aside at least 20% of units to households at or below 80% AMI.This is a noncompetitive program and applications are accepted at any time. Loan amounts have a maximum of $10 million.

Waive Fees on Housing Rehab for Low-Income Owners

The City should consider waiving fees for housing rehabilitation projects for low-income households (<80% AMI).

Tax Increment Financing

Tax Increment Financing (TIF) districts can include residential property. In areas targeted for new residential growth the City should consider TIF district creation to provide incentives to support new housing development that is affordable, such as infrastructure improvements, land purchase and housing tax credit matching funds. Project plans could also provide incentives to developers prioritizing density in their projects or support infill and redevelopment. Many developers noted that TIF is necessary for nearly all projects they complete.The intent is to ensure that investments in the attraction of businesses and jobs should be coupled with investment in housing affordable to who will work those jobs.

Federal Home Loan Bank Affordable Housing Program

Encourage developers of rental projects to apply, and encourage local banks and single-family home developers to participate in the Federal Home Loan Bank (FHLB) Affordable Housing Program (AHP). Under this program a FHLB member bank can partner with a developer to apply for grant funds for rental projects where at least 20% of the units are affordable for and occupied by those at or below 50% AMI or owner-occupied programs for households at or below 80% AMI.

RECOMMENDATIONS

Funding

WHEDA Loan Programs

Vacancy-to-Vitality - $100 million allocated

This loan programs assists in converting vacant commercial properties to workforce or senior housing. In 2023, 25% of funding was set aside for senior housing, 30% for communities of 10,000 people or less.This loan program is exclusive for private developers. Cannot be combined with TIF.

Restore Main Street - $100 million allocated

Provides loans for converting rental properties on 2nd and 3rd floors of mixed-use properties that are vacant or underutilized. In 2023, 30% for communities of 10,000 people or less.This loan program is exclusive for private developers. Cannot be combined with TIF.

Infrastructure Access - $275 million allocated

Allows a residential housing developer to apply for a loan to cover the costs of installing, replacing, upgrading, or improving public infrastructure related to workforce housing or senior housing.These costs are typically covered by the developer. Local government units may also apply for loans using this program.

Home Repair and Rehab Loan (Home R&R Loan) - $50 million allocated

This loan program makes modifications to the Workforce Housing Rehabilitation Loan Program administered by WHEDA. Qualified Wisconsin homeowners may apply for the Home R&R Loan to repair and/or rehabilitate their single-family residence.This program is still under development.

These loan programs were recently created through the 2023 Wisconsin Bipartisan Housing Legislation Package. In order to be eligible for these programs, municipalities must have:

1. Updated housing element of the comprehensive plan within past 5 years

2. Updated comprehensive plan within past 10 years

3. Changes to ordinances or regulations to decrease cost of housing development

With this housing study, Menasha hopes to update its housing chapter of the comprehensive plan. Upon approval and implementation of strategies of this plan, projects may be eligible for these program as early as October 2024.

REDEVELOPMENT OPPORTUNITIES

Identified in this map are 7 redevelopment sites the City should consider to maximize housing potential. Each site has been reviewed for development potential, future land use, and applicable funding resources. General marketing strategies are included for how the City can best advertise these development opportunities to potential developers.

REDEVELOPMENT SITES

Site #1: Badger Highways Quarry (800 Ninth St)

Former Use:

Quarry site, currently landscape yard

Zoning District:

I2 – General Industrial

Future Land Use:

Industrial

Possible Use:

Neighborhood residential including single family attached and detached

homes with mixed use retail and institutional

Funding Resources:

• WHEDA Infrastructure Access Loan Program

• TIF

• LIHTC

• CDBG

Site #2: Lakeside Book Company Site (800 Midway Rd)

Former Use:

Lakeside Book Company, now vacant

Zoning District:

I1 – Heavy Industrial

Future Land Use:

Industrial

Possible Use:

Medium density residential and mixed-use activity center

Funding Resources:

• WHEDA Infrastructure Access Loan Program

• TIF

• LIHTC

• CDBG

REDEVELOPMENT SITES

Site #3: Nicolet Elementary School (449 Ahnaip St)

Former Use:

Elementary school, now vacant

Zoning District:

C1- General Commercial

Future Land Use:

Institutional & Facilities

Possible Use:

Conversion to residential apartments or single family attached homes

Funding Resources:

• WHEDAVacancy-to-Vitality Loan Program

• TIF

• LIHTC

• CDBG

Site #4: Appleton Pentecostal Assembly Building (1100

Former Use:

Religious facility, for sale

Zoning District:

C1- General Commercial

Future Land Use:

General Commercial

Possible Use:

Conversion to residential or senior living apartments

Funding Resources:

• WHEDAVacancy-to-Vitality Loan Program

• TIF

• LIHTC

• CDBG

London St)

REDEVELOPMENT SITES

Site #5: Appleton RdVacant Lot (1165 Appleton Rd)

Former Use:

Vacant lot

Zoning District:

C1- General Commercial

Future Land Use:

General Commercial

Possible Use: