24 minute read

NARFE 2020 Financial Statements

from August 2021 NARFE Magazine

by NARFE

REPORT OF THE NATIONAL SECRETARY/TREASURER

Advertisement

The annual financial audit was performed by the firm selected by NARFE’S Audit Committee. NARFE’s annual financial reporting is shown as a Consolidated Statement of Accounts in accordance with AICPA standards. All accounts—investment accounts, general operating and capital accounts, and NARFE-PAC funds are consolidated for one summary report.

NARFE has ended fiscal year 2020 with a surplus in general operating funds. NARFE policy on investments only in equities and bonds remains very conservative. The NARFE investment portfolio is well managed by Morgan Stanley with oversight by NARFE’s secretary/treasurer and final decisions by the National Executive Board (NEB). We ended 2020 with an increase in investment earnings. Fiscal year 2020 was a different year. Like every other business, our financial operations were affected by the pandemic. Many normal costly events handled in the past were curtailed, resulting in overall savings. From oversight by the Budget and Finance Committee to more emphasis on accountability by the NEB, we are adjusting to a new normal. The Configuration Advisory Board (CAB) charter was updated, and they instituted a new tracking system for improved monitoring of our new data management system (AMS). AMS should be fully implemented in 2021 as we deal with some quirks that affect not only Headquarters accounting but also the verification of reports for the field organizations.

As we determine further improvements to the accountability of NARFE operations, we are aware of the human elements—our staff and our members—to whom we owe our gratitude for their dedication and assistance. A special thank you to Region VII Vice President Rodney Adelman for his persistence as he urged for better controls and documentation in his extra roles as the NEB’s chair of the Audit Committee and compliance officer for the past five years. He has provided outstanding service to NARFE. —Kathryn E. Hensley

The National Executive Board (NEB) Audit Committee held a videoconference on April 5 with our auditors, Marcum LLP, first with the NARFE National Officers and staff and then privately, to review the draft audit of NARFE’s financial statements for the year ended December 31, 2020. National Audit Committee members participating were Region VII Vice President Rodney Adelman (Chair), Region II Vice President Gary Roundtree Sr., and Region IX Vice President Linda Silverio.

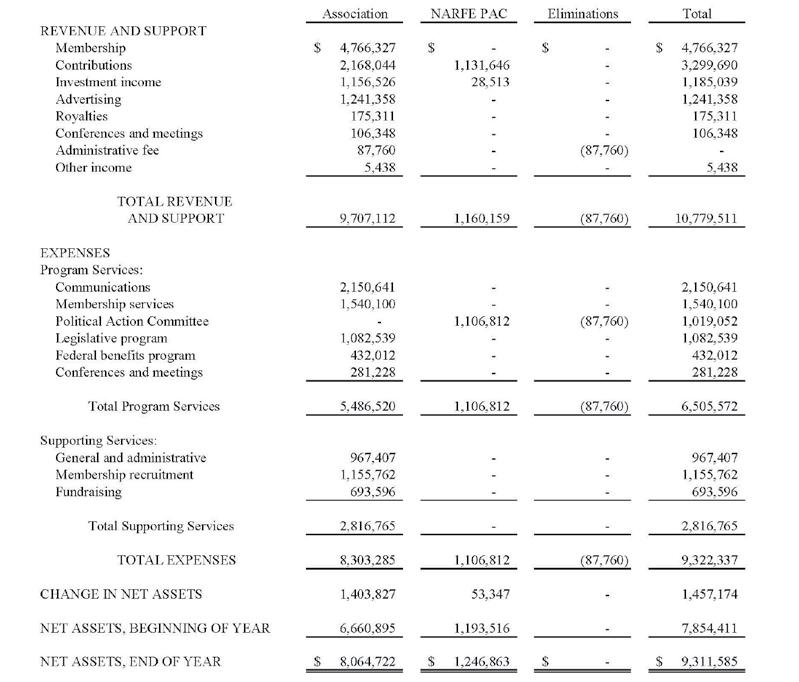

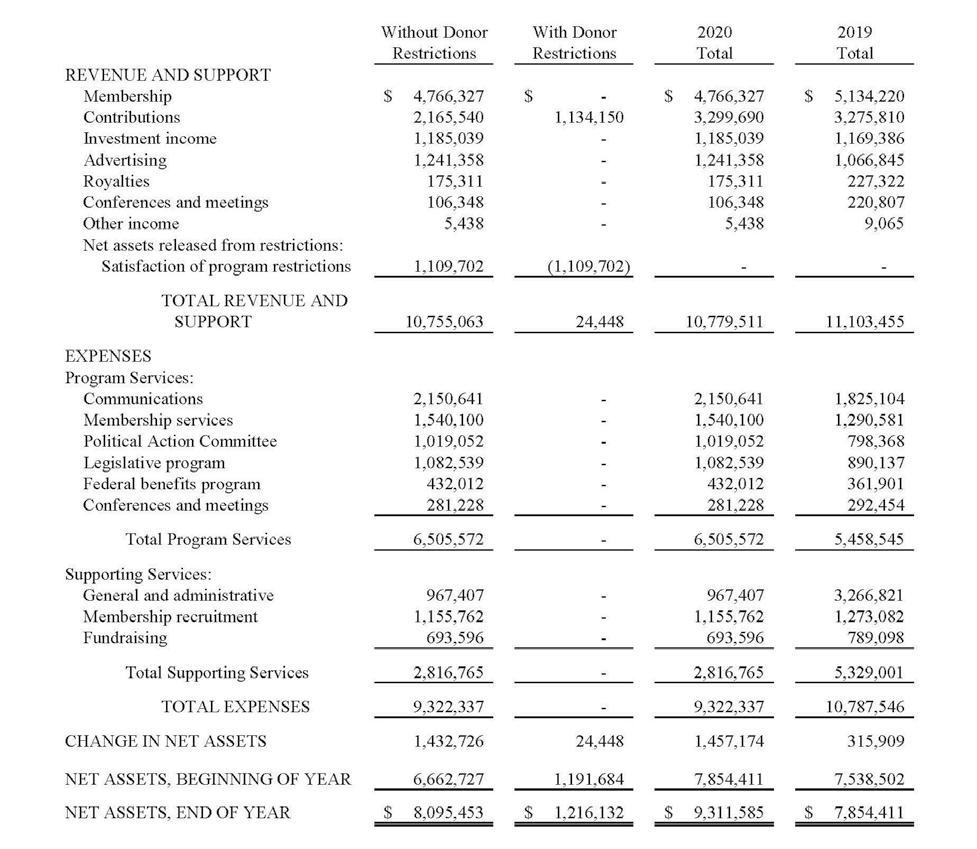

The auditors provided a comprehensive review of NARFE’s Consolidated Financial Statements and their Governance Letter. The auditors reported finding no material weaknesses in internal controls and have provided an unqualified opinion on our financial statements, a “clean” audit. Of note, the 2020 audit was done entirely remotely due to Covid-19 precautions. The audit confirmed a $1,432,726 gain in net assets, primarily due to investment income of $1,185,039 and a reduction in expenses of $1,465,209. However, membership loss continues to be a concern.

Pursuant to the Audit Committee’s recommendation, the NEB unanimously voted on April 23 to accept the audit. Based on the results of the audit, the Committee commends NARFE senior management and staff for their contributions to qualitative financial reporting.

After having served as the National Audit Committee Chair for the last five audit cycles and as the NARFE Compliance Officer since the position’s inception in late 2016, I have decided to step down from these positions. It is time for some “new blood” and a different perspective. It has been a pleasure to serve. —Rodney L. Adelman, Chair

To the National Executive Board of National Active and Retired Federal Employees Association and Affiliate

Report on the Financial Statements

We have audited the accompanying consolidated financial statements of National Active and Retired Federal Employees Association and Affiliate (collectively referred to as the Association), which comprise the consolidated statement of financial position as of December 31, 2020, and the related consolidated statements of activities, functional expenses and cash flows for the year then ended, and the related notes to the consolidated financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the 2020 consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of National Active and Retired Federal Employees Association and Affiliate as of December 31, 2020, and the changes in its net assets and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Other Matters Report on Summarized Comparative Information

We have previously audited the Association’s 2019 consolidated financial statements, and in our report dated March 20, 2020, we expressed an unmodified opinion on those statements. In our opinion, the summarized comparative information presented herein as of and for the year ended December 31, 2019, is consistent, in all material respects, with the audited consolidated financial statements from which it has been derived.

Report on Supplementary Information

Our audit was conducted for the purpose of forming an opinion on the consolidated financial statements as a whole. The consolidating supplementary information is presented for purposes of additional analysis of the consolidated financial statements, and is not a required part of the consolidated financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the consolidated financial statements. The consolidating information has been subjected to the auditing procedures applied in the audit of the consolidated financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the consolidated financial statements or to the consolidated financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the consolidating information is fairly stated, in all material respects, in relation to the consolidated financial statements as a whole.

Marcum LLP Washington, DC April 21, 2021

National Active and Retired Federal Employees Association and Affiliate Consolidated Statement of Financial Position December 31, 2020 (With Summarized Financial Information for the Year Ended December 31, 2019)

National Active and Retired Federal Employees Association and Affiliate Consolidated Statement of Financial Position December 31, 2017 (With Comparative Totals as of December 31, 2016 and 2015)

Additional NARFE Financial Data

The salaries of the National Executive Board, as of December 31, 2020, are as follows (rounded): President: $128,067 Secretary/Treasurer: $114,544 Regional Vice Presidents: $27,750 In 2020, NARFE’s investments were held with these firms: • Operating Fund: Morgan Stanley and The Vanguard Group • Life Membership Trust Fund: Morgan Stanley • Contingency Fund: Morgan Stanley • PAC Fund: Raymond James

The accompanying notes are an integral part of these consolidated financial statements.

NATIONAL ACTIVE AND RETIRED FEDERAL EMPLOYEES ASSOCIATION AND AFFILIATE

CONSOLIDATED STATEMENT OF FUNCTIONAL EXPENSES For the Year Ended December 31, 2019 (With Summarized Financial Information for the Year Ended December 31, 2018)

Program Services

Political Federal Total Membership Action Legislative benefits Conferences Program Communications Services Committee program program and meetings Services

Salaries and benefits $ 444,239 $ 704,102 $ - $ 699,634 $ 228,046 $ 108,282 $ 2,184,303

Printing and postage 1,112,571 10,044 103,515 46,491 9 1,001 1,273,631

Contract services Political contributions Advertising 244,320 561,193 8,454 616,000 26,528 9,997 850,492 - 616,000NATIONAL ACTIVE AND RETIRED FEDERAL

EMPLOYEES ASSOCIATION AND AFFILIATE

- - - - - -

Office expenses 7,958 15,242 22,147 20,976 6,487 15,484 88,294 Meetings and conferences 4,226 - 17,702 9,732 4,302 155,502 191,464 CONSOLIDATED STATEMENT OF FUNCTIONAL EXPENSES Professional fees 11,790 - 674 113,304 96,529 2,188 224,485For the Year Ended December 31, 2019 Bank fees and taxes - - 29,876 - - - 29,876 (With Summarized Financial Information for the Year Ended December 31, 2018) Depreciation - - - - - _______________ -

TOTAL EXPENSES $ 1,825,104 $ 1,290,581 $ 798,368 890,137$ Program Services $ 361,901 $ 292,454 $ 5,458,545

Political Federal Total Membership Action Legislative benefits Conferences Program Communications Services Committee program program and meetings Services

Salaries and benefits $ 444,239 $ 704,102 $ - $ 699,634 $ 228,046 $ 108,282 $ 2,184,303

Printing and postage 1,112,571 10,044 103,515 46,491 9 1,001 1,273,631

Contract services 244,320 561,193 8,454 - 26,528 9,997 850,492

Political contributions - - 616,000 - - - 616,000

Advertising - - - - - -

Office expenses 7,958 15,242 22,147 20,976 6,487 15,484 88,294 Meetings and conferences 4,226 - 17,702 9,732 4,302 155,502 191,464 Professional fees 11,790 - 674 113,304 96,529 2,188 224,485 Bank fees and taxes - - 29,876 - - - 29,876 Depreciation - - - - - - -

TOTAL EXPENSES $ 1,825,104 $ 1,290,581 $ 798,368 $ 890,137 $ 361,901 $ 292,454 $ 5,458,545

National Active and Retired Federal Employees Association and Affiliate Notes to Consolidated Financial Statements December 31, 2020

NOTE 1: NATURE OF ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization: National Active and Retired Federal Employees Association (NARFE) was established in 1921 to advance the general welfare of its 160,000-plus members and to aid them in securing their rights under federal retirement laws. NARFE is incorporated under the laws of District of Columbia. Its programs include legislative, federal benefits, communications and conferences. These activities are primarily funded by membership dues and contributions and revenue derived from advertising.

There are fifty-four (54) federations, located in the United States, District of Columbia, Panama, Puerto Rico, and the Philippines, that are affiliated with NARFE and conduct local independent programs. Ten percent of all eligible member national dues collected are passed- through to these federations to facilitate local activities. In addition, there are 872 chapters affiliated with NARFE that are located in the United States and some international locations. The chapters are established by members to increase the scope and effectiveness of NARFE. Chapter dues are established by the chapters and are billed and collected by NARFE with the national dues. NARFE rebates to the chapters one-third of the national fee charged for all new members joining chapters.

The federations and chapters are independent and autonomous organizations. As NARFE has no economic interest in or control of federations and chapters affiliates, their financial activities are not included in the accompanying consolidated financial statements of NARFE. The federations’ bylaws must adhere to NARFE’s bylaws.

NARFE has created a political action committee called NARFE PAC. Basis of Accounting: These consolidated financial statements have been prepared on the accrual basis of accounting in accordance with accounting principles generally accepted in the United States of America (GAAP). Consequently, revenue is recognized when earned and expenses are recognized when incurred. Principles of Consolidation: The consolidated financial statements of the Association have been prepared on the accrual basis of accounting and include the accounts of NARFE and its affiliate, NARFE PAC (collectively referred to as the Association). All material intercompany balances and transactions have been eliminated in consolidation. Cash and Cash Equivalents: Cash and cash equivalents are composed of demand deposits and money market funds. Accounts Receivables: The Association uses the allowance method to record accounts receivable at their estimated net realizable value. The allowance for doubtful accounts is based on various factors, including management’s analysis of the collectibility of the accounts, historical write-off of expenses and current economic conditions. A provision for doubtful accounts is made when collection of the full amount is no longer probable. Investments: Investments consist of mutual funds, corporate bonds and certificate of deposit. Investments are recorded in the accompanying consolidated financial statements at their fair value. Fair value is the price that would be received to sell an asset or paid to transfer a liability through an orderly transaction between market participants at the measurement date. Purchases and sales are reflected on a trade-date basis. Interest, dividends and realized gains or losses are recorded when earned. Changes in the fair value of the portfolio are recorded as unrealized gains or losses.

Fair Value of Financial

Instruments: In accordance with the accounting standards for fair value measurement for those assets and liabilities that are measured at fair value on a recurring basis, the Association has categorized its applicable assets and liabilities measured at fair value into a required fair value hierarchy. The fair value hierarchy gives the highest priority to quoted prices in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). If the inputs used to measure the financial instruments fall within different levels of the hierarchy, the categorization is based on the lowest level-input that is significant to the fair value measurement of the instrument.

Applicable financial assets and liabilities are categorized on the basis of the inputs to the valuation techniques as follows:

Level 1 – Financial assets and liabilities whose values are based on unadjusted quoted prices for identical assets or liabilities in an active market that the client has the ability to access.

Level 2 – Financial assets and liabilities whose values are based on quoted prices in markets that are not active or model inputs that are observable, either directly or indirectly, for substantially the full term of the asset or liability.

Level 3 – Financial assets and liabilities whose values are based on prices or valuation techniques that require inputs that are both unobservable and significant to the overall fair value measurement.

As of and for the year ended December 31, 2020, only the Association’s investments, as described in Note 2 to these consolidated financial statements, were measured at fair value on a recurring basis. Property and Equipment: All acquisitions of property and equipment greater than $1,500 and an economic life in excess of one year are capitalized at cost. Depreciation and amortization is computed by using the straight-line method based upon the estimated useful lives of the assets. Building and improvements are recorded at cost and depreciated using the straight-line method over their estimated useful lives of 20 to 40 years. Furniture, equipment and software are recorded at cost and depreciated using the straight-line method over their estimated useful lives of three to eight years. Expenditures for major repairs and improvements that extend the useful life of an asset are capitalized, whereas expenditures for minor repairs and maintenance costs are expensed when incurred. The cost of property and equipment retired or disposed of is removed from the accounts along with the related accumulated depreciation, and any gain or loss is reflected in revenue and support or expenses in the accompanying consolidated statement of activities.

Classification of Net Assets:

NARFE’s net assets are reported as follows: • Net assets without donor restrictions represent the portion of expendable funds that are available for any purpose in performing the primary objectives of the Association at the discretion of the Association’s management and the National Executive Board (the Board). From time to time, the Board designates a portion of these net assets for specific purposes, which makes them unavailable for use at management’s discretion. The Board has designated $2,000,000 of net assets without donor restrictions to serve as a working capital reserve to secure the Association’s long-term financial viability. Also included in board-designated net assets is the life membership fund in the amount of $1,375,761. • Net assets with donor restrictions represent funds that are specifically restricted by donors for use in various programs and/or for specific periods of time. These donor restrictions can be temporary in nature in that they will be met by actions of the Association or by the passage of time. Other donor restrictions are perpetual in nature, whereby the donor has stipulated that the funds be maintained in perpetuity. As of December 31, 2020, the Association had no net assets with donor restrictions that are required to be maintained in perpetuity.

Revenue Recognition

Membership Dues: Membership dues are on an anniversary-date basis and are recognized ratably over the membership period since there are no distinct performance obligations and the general member benefits are considered a bundled group of performance obligations that are delivered to members throughout the membership period.

Life membership dues are recognized as revenue over the duration of the life membership based on the collective average life expectancy for life members, according to life expectancy tables. Accordingly, dues paid by members in advance of the reporting period to which the dues pertain are reported as deferred revenue in the accompanying consolidated statement of financial position. Contributions: Unconditional contributions received are recorded as revenue with or without donor restrictions, depending on the existence and/or nature of any donor stipulations. Donor restricted contributions are reported as an increase in net assets with donor restrictions, depending on the nature of the stipulation. When a restriction expires (that is, when a stipulated time restriction ends or purpose of a restriction is accomplished), net assets with donor restrictions are reclassified to net assets without donor restrictions and reported in the accompanying statements of activities as net assets released from restrictions. Investment Income: Realized and unrealized gains and losses and investment income (loss) derived from investment transactions are included as income in the year earned. Advertising: Advertising revenue is recognized based upon when the advertisements are published, which is consistent with when the performance obligation is satisfied. Revenue from these activities received in advance of the period to which the revenue pertains is reported as deferred revenue in the accompanying consolidated statement of financial position. Royalties: The Association receives various royalties from other organizations. These royalties are primarily from membership benefits offered to members of the Association. The revenue is recognized when earned according to contractual agreements with each organization.

Conferences and meetings:

Conferences and meetings revenue consists of registrations, event sales and sponsorship fees and is recognized in the year in which the conference takes place. Revenue from these activities received in advance of the meeting is reported as deferred revenue in the accompanying consolidated statement of financial position.

Impairment of Long-Lived Assets:

In accordance with the provisions of Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 360, Property, Plant and Equipment, the Association reviews its property for impairment whenever events or changes in circumstances indicate that the carrying value of an asset may not be recoverable. If the fair value is less than the carrying amount of the asset, an impairment loss is recognized for the difference. As of December 31, 2020, the Association has not recognized an impairment loss.

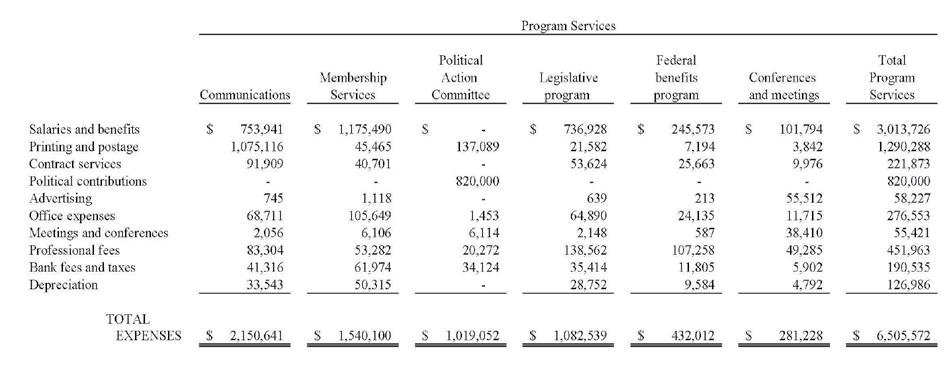

Functional Allocation of

Expenses: The costs of providing the various programs and other activities have been summarized on a functional basis in the accompanying statement of functional expenses. Expenses directly attributed to a specific functional area of the Association are reported as expenses of those functional areas and are charged directly to the programs those items support. Shared costs such as office expenses are allocated to the functional area and the programs pro rata based on estimated time and efforts by employees. Estimates: The preparation of consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect certain reported amounts and disclosures. Accordingly, actual results could differ from those estimates.

NOTE 2: INVESTMENTS AND FAIR VALUE MEASUREMENTS

The following table summarizes the Association’s assets measured at fair value on a recurring basis, aggregated by type and fair value hierarchy level within which those measurements were made:

For the year ended December 31, 2020, the Association used the following methods and significant assumptions to estimate fair value for investments recorded at fair value:

Mutual funds and exchange-traded funds – Value of these funds is based on quoted market prices in active markets.

Certificate of deposit and corporate bonds – Valued at fair value by discounting the related cash flows based on current yields of similar instruments with comparable characteristics.

Depreciation and amortization expense was $191,677 for the year ended December 31, 2020.

NOTE 4: NET ASSETS

Net Assets Without Donor Restrictions

As of December 31, 2020, the Association’s net assets without donor restrictions were composed of the following:

Net Assets With Donor Restrictions

As of December 31, 2020, net assets with donor restrictions were available for the following purposes:

NOTE 5: REVENUE FROM CONTRACTS WITH CUSTOMERS

The following table provides information about significant changes in the Association’s deferred membership revenue for the year ended December 31, 2020:

NOTE 6: CONCENTRATION OF CREDIT RISK

The Association maintains its cash and cash equivalents with a certain commercial financial institution, which aggregate balance, at times, may exceed the Federal Deposit Insurance Corporation (FDIC) insured limit of $250,000 per depositor per institution. As of December 31, 2020, the amount in excess of the maximum limit insured by the FDIC was approximately $794,000. The Association monitors the creditworthiness of this institution and has not experienced any credit losses on its cash and cash equivalents.

NOTE 7: LINE OF CREDIT

In June 2019, the Association obtained a line of credit with available borrowings of up to $500,000. The interest rate was 3.75% as of December 31, 2020. The interest rate is based on the Bank prime rate plus 0.5%. The line of credit is secured by investments and will mature in June 2021. The outstanding balance at December 31, 2020 was $300,000.

The Association regularly monitors liquidity required to meet its annual operating needs and other contractual commitments, while also striving to preserve the principal and return on the investment of its funds. The Association’s financial assets available within one year of the statement of financial position date for general expenditures at December 31, 2020, were as follows:

Cash and Cash Equivalents Accounts Receivable Investments $ 1,619,803 300,672 9,231,256

Total Financial Assets Available within One Year 11,151,731

Less:

Amounts unavailable for general expenditures within one year due to donor’s restriction with purpose restriction (1,216,132)

Financial Assets Available to Meet General Expenditures Within One Year $ 9,935,599 The Association has various sources of liquidity at its disposal, including cash and cash equivalents and investments, which are available for general expenditures, liabilities and other obligations as they come due. Management is focused on sustaining the financial liquidity of the Association throughout the year. This is done through monitoring and reviewing the Association’s cash flow needs on a regular basis. As a result, management is aware of the cyclical nature of the Association’s cash flow related to the Association’s various funding sources and is therefore able to ensure that there is cash available to meet current liquidity needs. As part of its liquidity plan, excess cash is invested in publicly traded investment vehicles, including mutual funds, or to support organizational initiatives. The Association can liquidate its investments anytime, and therefore the investments are available to meet current cash flow needs. To help manage unanticipated liquidity needs, the Association has a committed line of credit of $500,000.

NOTE 9: PENSION PLAN

The Association has a Retirement Savings Plan (the Plan). Employees are eligible to participate in the Plan on the first day of the month coinciding with or next following the employee’s hire date. Employees become eligible for employer matching funds on the first day of the Plan Year (January 1) or the first day of the seventh month of the Plan Year (July 1) coinciding with or next following hire date. Once eligible, an employee is 100% vested. The Association matches 60% of each employee’s voluntary contribution up to 6% of annual compensation. Total contributions made by the Association were approximately $76,000 for the year ended December 31, 2020.

NOTE 10: COVID-19 IMPACT

The COVID-19 outbreak in the United States has caused business disruption through mandated and voluntary closing of business across the country for non-essential services. While the disruption is currently expected to be temporary, there is considerable uncertainty about the duration of closings. The Association has been able to continue its operations in a remote environment and is making plans to adjust activities that cannot, however, at this point, the extent to which COVID-19 may impact the Association’s financial condition or results of operations is uncertain. The Association is exempt from federal income taxes under Section 501(c)(5) of the Internal Revenue Code (IRC). However, income from certain activities not directly related to the Association’s tax-exempt purpose is subject to taxation as unrelated business income. The Association generates unrelated business income from advertising. The Association’s provision for unrelated business income tax expense was approximately $15,000 for the year ended December 31, 2020.

NARFE PAC is subject to federal income taxes under IRC Section 527 with respect to certain investment income. For the years ended December 31, 2020, no provision for federal or state income taxes was made, as there was no significant taxable income.

The Association follows the authoritative guidance relating to accounting for uncertainty in income taxes included in FASB ASC Topic 740, Income Taxes. These provisions provide consistent guidance for the accounting for uncertainty in income taxes recognized in an entity’s financial statements and prescribe a threshold of “more likely than not” for recognition and derecognition of tax positions taken or expected to be taken in a tax return.

The Association performed an evaluation of uncertainty in income taxes for the year ended December 31, 2020, and determined that there were no matters that would require recognition in the consolidated financial statements or that may have an effect on its tax-exempt status. As of December 31, 2020, there are no audits for any tax periods that are currently pending or in progress. It is the Association’s policy to recognize interest and/or penalties related to uncertainty in income taxes, if any, in income tax or interest expense. As of December 31, 2020, the Association had no accruals for interest and/or penalties.

NOTE 12: – PRIOR YEAR SUMMARIZED FINANCIAL INFORMATION

The accompanying financial statements include certain prior year summarized comparative information in total, but not by net asset class. Such information does not include sufficient detail to constitute a presentation in conformity with GAAP. Accordingly, such information should be read in conjunction with the Association’s financial statements for the year ended December 31, 2019, from which the summarized information was derived.

NOTE 13 – SUBSEQUENT EVENTS

The Association’s management has evaluated, for potential recognition or disclosure, events and transactions through April 21, 2021, the date the financial statements were available to be issued. There were no subsequent events identified that require recognition or disclosure in these consolidated financial statements.

Supplementary Information Consolidating Schedule of Financial Position December 31, 2020

Consolidating Schedule of Activities for the Year Ended December 31, 2020