3 minute read

How investing tax free can boost long-term returns

PIETER KOEKEMOER Head: Personal Investments, Coronation

The start of the new tax is an opportune time to look at your options to invest tax efficiently. Three products can help investors to maximise their tax benefits over the next 12 months:

• Retirement annuities (RAs)

• Endowments (for high-income earning individuals)

• Tax-free investments (TFIs)

Each product has a different function in an investment portfolio, so it is not a case of one being preferable to the other. But whether investors are saving for retirement through a workplace retirement fund or an RA, they can also consider a TFI for its long-term benefits of tax-free compound growth. And the earlier investors start investing in a TFI each new tax year, the more they can make of the potential growth benefits over the full 12 months.

As of 2 March, investors can invest between R250 and R3 000 in a TFI via a monthly debit order, or a lump sum of up to R36 000 per tax year, and up to a maximum of R500 000 over their lifetime. The amount they save on tax remains invested, which can make a significant difference to the growth of their money over the long term. But how much of a difference?

The benefits of investing tax free are compounding every day

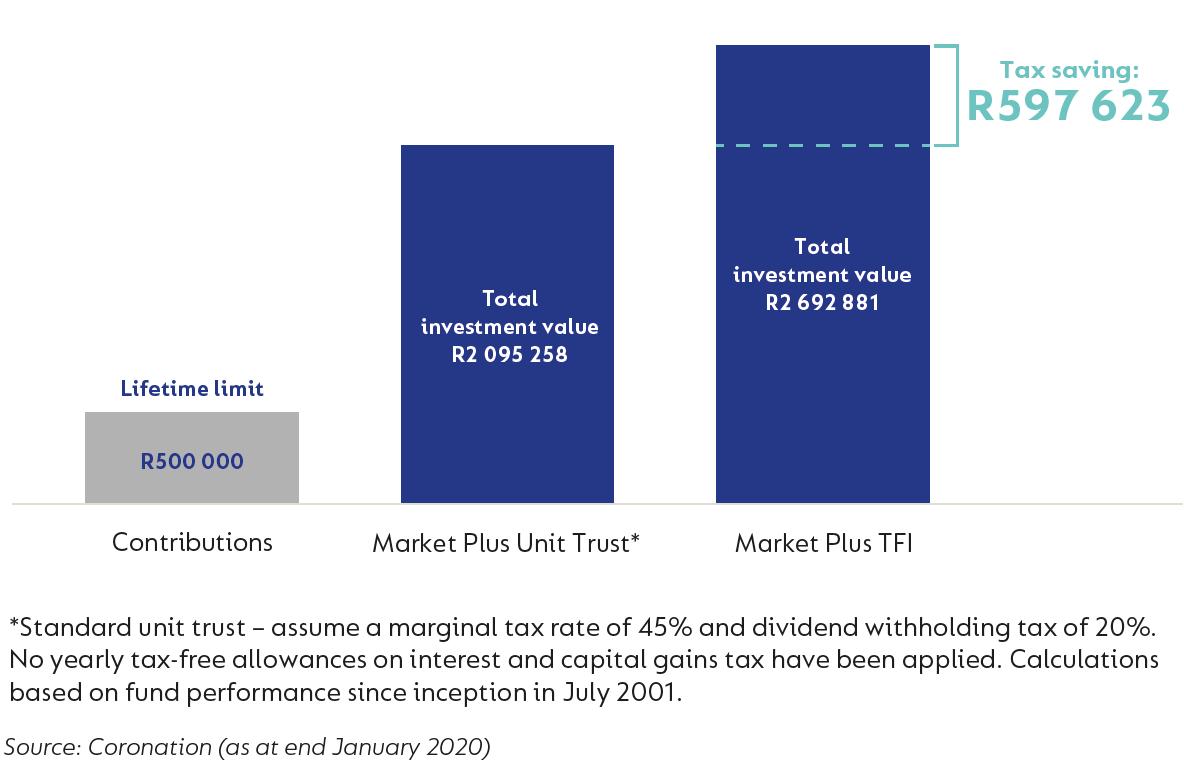

The graph below shows very clearly the benefits of investing in a TFI over the long term. It compares the same investment in the taxable Coronation Market Plus Fund versus the tax-free Coronation Market Plus Fund over the same time period.

MARKET PLUS TFI VS. TAXABLE MARKET PLUS UNIT TRUST

Let’s assume that from the fund’s inception in July 2001, an investor was able to contribute the R36 000 annual limit until the lifetime limit of R500 000 was reached. And then, assume this investment was left to compound until the end of January 2020. Simply by investing tax-efficiently, the investor would have R597 623 more capital in the TFI fund than the taxable fund. It’s a significant difference over time and could make the world of difference to an individual’s life at retirement or a child or grandchild’s education.

The sooner investors invest their lifetime allowance, the more they will reap the rewards of long-term investing and the power of compounding, as long as they remain invested.

While investors don’t get a tax break when contributing to a TFI, no tax is accrued while they are investing and all proceeds withdrawn from the investment are tax free. Investors have complete tax certainty and do not have to worry about facing a larger-than-expected tax rate when they withdraw funds from their investment in future.

No switching costs

Investors can switch between funds, or withdraw money, without incurring any costs or penalties. Just be mindful that all amounts invested will count towards their annual and lifetime limits, regardless of any withdrawals they make – investors cannot ‘replace’ the money they withdraw with a new investment. So it’s best to consider a TFI as a longterm investment in order to take full advantage of the tax-free returns and proceeds.

For investors who already hold a tax-free savings account with a bank, it makes sense to consider moving their money to a unit trust-based TFI, which offers greater access to growth assets (such as equities and listed property stocks) and offshore diversification. And switching doesn’t cost a cent.

No additional product fees

Also, when investing in a TFI, investors don’t pay any additional fees for the tax-efficient product structure. They only pay for the administration and investment management of the underlying unit trusts (which you would have paid regardless).

For full details about the Coronation Market Plus Fund, download its comprehensive fact sheet from www.coronation.com