9 minute read

Tomorrow Never Dies

What a year! We could have started the last Newsec Property Outlook with the same sentence, however, for 2022 “what a year” reflects perhaps one of the most turbulent years in the history of Nordic & Baltic real estate. The year started with guns blazing, and deal after deal was closed at record levels – the happy 10’s were becoming the happy 20’s, despite the pandemic. Early on in 2022, market sentiment however changed. By summer investors had grown cautious, and after the autumn the market had completely cooled off, with fewer deals noted and lower valuations – the annual doomsday predictor had finally hit right. Thus, we decided to dedicate this Newsec Property Outlook to investigate statements that have arisen from the downturn and assess which are true and which are urban legends. Before we dive in, remember – doomsday predictors are generally wrong in the long-term and thus in practice, tomorrow never dies.

Statement 1 & 2.

“Buy low, sell high”

& “Cash is king”

To have impeccable timing is nearly impossible, yet many real estate investors strive to do so. However, in the pursuit of perfect timing investors become blind to opportunity and instead fall into the “wait and see” trap. The “wait and see” trap is common in environments which are difficult to forecast. Instead of acting on opportunities, outsmarting the market and timing the bottom becomes the strategy. In practice, however, outsmarting the market and timing the bottom is difficult even for the most skilled investors. Thus, most investors wait too long and miss the window of opportunity. Looking back at the previous crisis in 2009, when the real estate market in the Nordics & Baltics essentially stopped, and the transaction volume dropped by more than 50%, one type of investor remained a strong buyer –institutions. Institutions are by nature real longterm investors and buy throughout the cycle. Institutions are also highly liquid and as it has become both more difficult and expensive to get capital through debt, cash is again king.

In exhibit 1, the share of institutions of the total transaction volume in the Nordics & Baltics can be seen. It is apparent that the institutions’ share of the total transaction volume increased dramatically in the crisis year of 2009. Although the total transaction volume was lower than in 2008, it is evident that long term and cash strong investors such as institutions buy relatively more than other investors in downturns and relatively less than other investors in upswings. As can be noted in the graph, the monthly share of institutions has dramatically increased in

Definitions

Inter-Nordic investor: investor from a Nordic country investing in another Nordic country

Non-Nordic investor: investor from outside of the Nordics

Domestic investor: investor investing in their home country the autumn of 2022 and is expected to remain at a high level this year.

In 2023, all investors will not be able to be net buyers, but the ones who can, should seize this opportunity by buying throughout the cycle, instead of shying away from investments while trying to catch a falling knife. Cash strong funds and institutions are forecast to be net buyers, while listed property companies will be significant net sellers. It is however, likely that listed property companies, strapped for cash, will try to both service debt and acquire new properties through large new issuances. Whether they will succeed or not, time will tell. Nevertheless, Newsec assesses that this type of investor will be a net seller in 2023. Thus, statement no. 1 is in fact an urban legend (at least in practice for most investors) and statement 2 is in fact true.

Statement 1 – “Buy low, sell high” – Urban legend

Statement 2 – “Cash is king” – True

Statement 3.

“Non-Nordic investors to save the day”

The above statement is perhaps one of the most spoken in the last months – claiming that international presence will increase and drive the market in 2023. Many claim that weakening currencies (NOK and SEK, and to some extent EUR) will lead to an increase in non-Nordic investors, in turn indirectly implying that real estate acquisitions will not be currency hedged and will include currency risk. It is probable that non-Nordic investors will continue to be noted on the market, as they often are on the buyside of mega-deals. However, it is very unlikely that this investor type will drive the transaction market to any meaningful degree in the coming year. This is especially the case since assets in many of the largest non-Nordic investors' home markets have fallen sharply, thus allowing for many domestic opportunities and perhaps less capital allocation towards foreign markets such as the Nordics. In exhibit 2, the share of non-Nordic investors over time as part of the total transaction volume is displayed. The graph shows that on average, nonNordic investors account for approximately the same share as inter-Nordic investors – a relatively low 15% each (with the rest being domestic investors). It can also be noted that during the great financial crisis in 2009, non-Nordic investors dramatically decreased their share of the transaction volume. The same could be noted during the pandemic in 2020, where non-Nordic investors again dramatically decreased their presence due to instability and uncertainty. This time, however, inter-Nordic investors remained solid. Non-Nordic investors thus seem keener to stick around in good times. The graph also implies that the Nordic market is self-sufficient (at least since after the great financial crisis) and non-Nordic investors are nonessential to achieve liquidity – even in uncertain times. In 2023, Newsec expects nonNordic investors to have a presence on the market, however not to an extraordinary high extent. Contrary to popular belief, non-Nordic investors have not to an apparent degree increased nor decreased their share of the transaction volume since the great financial crisis and their presence can to some extent be interpreted as white noise. Newsec assesses that domestic investors will continue to drive the market in 2023. Also, Newsec assesses it is more likely that inter-Nordic investors grab a higher share of the transaction volume in 2023 than non-Nordic. Thus, non-Nordic investors will not save the day and statement no. 3 is concluded to be an urban legend.

Statement 3 – “Non-Nordic investors to save the day”

– Urban legend

Statement 4.

“The residential asset class has become unattractive”

The residential segment has been one of the most popular among investors in the past few years, averaging an astonishing 27 % share of the total transaction volume annually in the Nordics & Baltics since 2016 (exhibit 3), making it the largest investment segment in the Nordics & Baltics. The segment has also noted substantial yield compression in the past five years, and e.g. between 2017 and 2021, the prime yield shrunk by 25% on average in the Nordics. This has made the segment one of the most lucrative investments in the last few years, having among the highest total return across all segments in Sweden, Finland, and Denmark. The playing field has however changed with the new macroeconomic climate. Rising financing costs and higher inflation without, in many cases, CPI adjusted rents have made this investment class look less attractive. The segment is also subject to regulations across the Nordics*, which in some cases has resulted in unfavorable rulings or political decisions – in several cases related to rental growth. However, let us revisit why the segment was an attractive investment from the get-go. The primary reason for the attractiveness of the segment is the strong underlying long-term fundamentals which outperform the rest of Europe. In exhibit 4, the demographic outlook in the Nordics vs the rest of Europe is shown. The outlook is clearly superior in the Nordics with three out of four Nordic countries displaying the highest growth among the countries in the graph. Thus, the demand for residential is high and is forecast to remain on a high level, given the stronger demographic outlook than the rest of Europe.

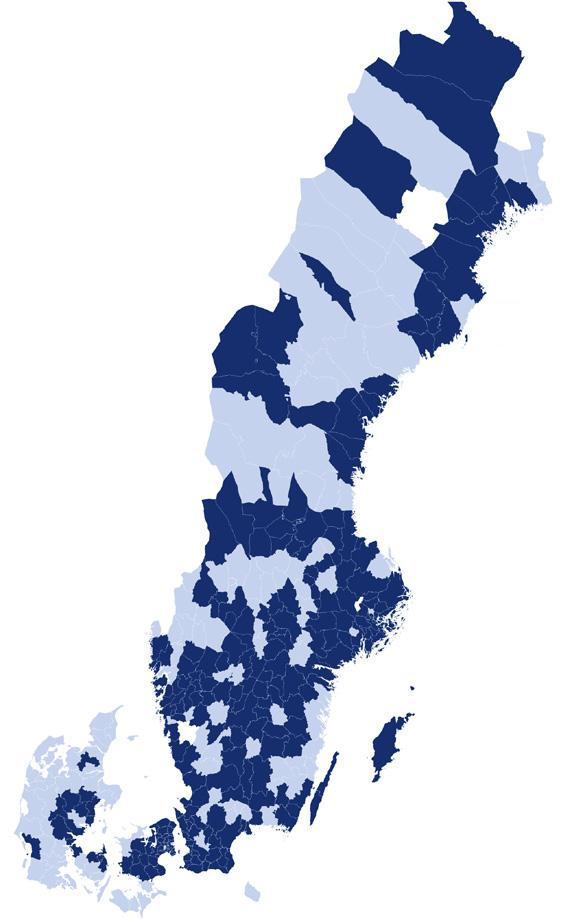

There also exists a structural supply problem resulting in a shortage of housing and thus a low supply. In exhibit 5, the amount of required construction per 1,000 inhabitants in the Nordic capitals is compared to other European cities. As shown in the graph, the amount of housing needed is significantly larger in especially Copenhagen and Stockholm compared to other European cities. The shortage is also fueled by low construction levels, and the number of completions rarely reaches the required levels to meet annual housing needs. New housing is not only needed to meet new demand from demographic growth, but also to dampen the long-term supply shortage in the Nordics. The outlook for construction has also dimmed, with costs rising and thus the structural problem has been prolonged. In most of the Nordic countries the problem is also widespread and not only centered to the capital cities, as can be seen in exhibit 6 which displays municipalities with a housing shortage in Denmark and Sweden. This can in many cases lead to mispricing of assets in smaller cities and in turn create opportunities to acquire high yielding assets which, in fact, carries low risk. Gaining similar exposure to the segment in the rest of Europe is difficult, which makes the segment a healthy option to diversify many portfolios.

All in all, although a temporary downturn in the market can be noted with values falling due to macroeconomic and regulatory factors, the longterm fundamentals behind the segment’s attractiveness remain unchanged. Newsec assesses opportunities will arise within the segment and investors who can see beyond the short-term drivers are in a good position to take advantage of the market sentiment. Thus, the fourth statement is an urban legend.

Statement 4 – “The residential asset class has become unattractive”– Urban legend

The so-called government bond of real estate – the public property – is an investment which remains attractive with strong underlying fundamentals (aging population and lack of modern properties) and credit worthy tenants. Many are turning to the segment because of its predictability and an increasing number of different investors – not only real estate investors but also infrastructure investors – have been entering the market. The segment is characterized by long leases with steady and inflation proof cash flows. However, what happens to the risk when the lease begins to mature? Naturally, the risk increases as you are discounting fewer guaranteed cash flows, but Newsec has studied the probability of a public tenant extending the lease. In the study, Newsec looked at 43 elderly

■

■ care homes and 18 schools with contracts for elderly care homes starting in 1993 and contracts for schools starting in 1980. In the timeline to the right, the study is illustrated. By the end of the timeperiod, 14 out of 18 properties were still schools (78%), and 42 out of 43 properties were still elderly care homes (98%). In terms of extension, 122/126 (96,9%) leases were extended for schools and 209/210 (99,5%) leases were extended for elderly care homes. Compared to a commercial property such as an office, where the same number in an attractive location is assessed to be closer to 75–85% – the risk can be assessed to be low and thus this statement can be concluded to be true.

Conclusion

The long-term perspective for real estate

The common theme throughout almost all of the analyzed statements, to which our title also alludes, is the long-term perspective. The fact remains that in the long-term the outlook for Nordic & Baltic real estate is strong, the market still has potential, and many underlying fundamentals have not changed. In up and downturns, it is easy to forget that the current market sentiment will not last forever. In 2021 and the early months of 2022, the market reached its peak. During this period, people had the belief that interest rates would remain low indefinitely. However, by the end of 2022, people were instead predicting the doomsday for Nordic and Baltic real estate. This goes to show the volatility in market talks and sentiment and why engaging in the current mood is not a winning strategy.

One of the most pressing questions in the market today is how it will adapt to the changed cost of capital. It is worth noting that the Nordic real estate market thrived and remained liquid even during the early 2000s, when the cost of debt was comparable to what it is now. The expected required return in practice for investors has also not been perfectly correlated with changes in the risk free rate and the equity market risk premium is thus likely to note compression in 2023 for some investors. However, for activity to flourish, capital markets will need to become liquid again and price expectations will need to come down so buyers and sellers can meet. In the short term, Newsec forecasts that real long-term investors will stick to their strategy and be active buyers. Newsec also remains hopeful that other investors, with cash on hand, will act on opportunities, as in any other year. As several buyers turn to sellers and many cash strong players are still searching for new acquisitions, Newsec assesses that the year will note significant activity and that the transaction volume for the full year of 2023 will be in line with the historic average of 40 billion euros – despite market uncertainty. The long-term outlook is still positive for the Nordic & Baltic real estate market; however, it is darkest before dawn, and this year is also likely to be characterized by a market that is difficult to navigate. To navigate the market and to distinguish an opportunity from a mirage, contact Newsec, and we will assist you with all your real estate needs, and

Ravi Barot, ravi.barot@newsec.se

Adam Tyrcha, PhD, adam.tyrcha@newsec.se