Features:

WORKING FOR THE FUTURE Workers Compensation Insurance

WHILE M&A ACTIVITY SLOWS, BROKER OPPORTUNITIES QUICKEN Mergers & Acquisitions

SEPTEMBER 2023

YOUR VOICE

LEADING INTO THE FUTURE with the 2023 Broker of the Year Award state winners WE ARE

Also inside: 2023 NIBA CONVENTION A snapshot of the program

qbe.com.au/goodbusiness Remote Piloted Aircraft Policy is issued by QBE Insurance (Australia) Limited (AFSL 239545). To decide if this product is right for you, please read the policy available online at www.qbe.com.au. Policy QM8051 can inspire the next generation.

ACN 006 093 849

ABN 94 006 093 849

Insurance Adviser magazine is the monthly magazine of the National Insurance Brokers Association (NIBA).

Insurance Adviser magazine is published by NIBA

Publisher Philip Kewin, CEO, NIBA

T: (02) 9459 4305

E: pkewin@niba.com.au

W: niba.com.au

Communications Manager

Wendy Martin

NIBA Editor Virat Nehru

Editorial enquiries

E: editor@niba.com.au

National Sales Manager

Tony May

E: tmay@niba.com.au

Design Citrus Media www.citrusmedia.com.au

NIBA gives no warranty and makes no representation that the information contained in this magazine is, and will remain, suitable for any purpose or free from error.

To the extent permitted by law, NIBA excludes responsibility and liability in respect of any loss arising in any way (including by way of negligence) from reliance on the information contained in this magazine or otherwise in connection with it.

CONTENTS

September 2023

A SNAPSHOT OF THE 2023 NIBA CONVENTION PROGRAM

Gain insights about burning issues shaping the industry’s future

The contents of Insurance Adviser are protected by copyright and NIBA reserves its rights in this regard. 24

With the 2023 Broker of the Year Award state winners

NIBA.COM.AU / 3

FEATURES

LEADING

INTO THE FUTURE

18

REGISTER NOW

CONTENTS September 2023 4 / INSURANCE ADVISER SEPTEMBER 2023 IN EVERY ISSUE NIBA CEO Welcome 6 Member Benefits 8 EVENTS Forthcoming Events 10 NIBA MEMBER PORTAL A deep dive into your subscription list 12 NEWS Industry Bulletin 16 REFERENCE Community Hub ......................................... 52 Insurer Strength Ratings 58 FEATURES DISPLAY ADVERTISING INDEX – SEPTEMBER 2023 QBE IFC Vero 5 Allianz 7 Insurance Advisernet ............................ 9 Simfuni 11 UAC 15 NIBA Convention 23 Zurich 39 Hunter Premium Funding 41 Code of Practice ................................... 43 Community Broker Network 47 Ebix 49 ASR 51 NIBA Advertising 57 CGU OBC If you’d like to advertise your products and services through NIBA, please contact Tony May today on (02) 9459 4303 36 WORKING FOR THE FUTURE Evolving challenges in the workers compensation space 44 WHILE M&A ACTIVITY SLOWS, BROKER OPPORTUNITIES QUICKEN Importance of brokers in an increasingly regulated environment

It takes insight to future-proof a property portfolio

A property investment business with a large commercial portfolio wanted to know how vulnerable its assets might be to natural disasters.

Together with the broker, Vero’s Risk Engineering team reviewed the exposures and identified a range of risk mitigation strategies. They created a bespoke acquisition solution to help the business analyse their risk before investing in new property.

That’s insurance with insight. For help tailoring insightful solutions that suit your clients’ needs, speak to Vero’s Risk Engineering and Underwriting teams today.

Be the broker who sees the solution at vero.com.au

Insurance issued by AAI Limited ABN 48 005 297 807 trading as Vero Insurance. Read the Product Disclosure Statement before buying insurance. The TMD is also available. Go to vero.com.au for a copy.

A COLLABORATIVE CULTURE

This month, the Insurance Brokers Code Compliance Committee (the IBCCC) released its full Annual Report. The report highlights the IBCCC’s efforts in monitoring compliance with the Insurance Brokers Code of Practice (the Code), promoting good practices among insurance brokers that subscribe to the Code, and improving outcomes for their clients. The IBCCC welcomed the fact that more subscribers were reporting breaches, and this continues the trend of improvement, which is a positive and indicates more and more subscribers are improving their reporting standards. NIBA has been working more closely with the IBCCC to ensure the smooth implementation of the 2022 Insurance brokers Code of Practice, and to improve self-reporting that is so valuable in building upon the procedural framework and culture of code subscribers.

The IBCCC, however, did note the need for more improvement from subscribers who had not reported any breaches, and this is something we want to continue to work on. The independence of the IBCCC is paramount to being an effective code monitoring body, and cooperation and collaboration are important to ensure the right outcomes are being achieved in this regard. NIBA has been engaging with its members (code subscribers) and the IBCCC, and will commence a Working Group to ensure that the reporting processes are continually improved. We acknowledge the improvements made, and feedback from members is that we can further improve the way information is collected, which may have a positive impact on improving reporting. Working on information gathering may also help to remove any potential hurdles stopping subscribers from reporting appropriately.

Keeping in touch with our members is incredibly important. Not only do we want you to know about important compliance issues such as the IBCCC Annual Report, but also share our advocacy efforts, changes in legislation, as well as all of the upcoming events to keep you connected with the NIBA insurance broker community.

In July, we launched our new website and updated Member Portal. Since then, many members have made the most of the opportunity to update their subscription preferences. Now, you have greater flexibility to choose the types of communications you receive from NIBA. In this edition, we profile those options and how you can tailor your

6 / INSURANCE ADVISER SEPTEMBER 2023

CEO / Welcome

Get ready to elevate your expertise

2023 Allianz Broker Training Series, 12-14 September

Get ready to elevate your expertise to the next level at the 2023 Allianz Broker Training Series, offered exclusively to Allianz Broker Partners. Hear from our keynote speakers on mental health, resilience, wellbeing, sustainability and climate change, and the future of work. You’ll walk away inspired, and ready to go further, together. All while earning essential CIP/CPD accreditation points.

Don’t wait, register today for your chance to get ahead of the competition.

For more information on how to register, contact your Allianz representative today.

Insurance issued by Allianz Australia Insurance Limited ABN 15 000 122 850, AFS Licence No. 234708. This information is general advice only and does not take into account your objectives, financial situation or needs. Consider the relevant PDS in deciding whether to buy or continue to hold any insurance products. Target Market Determinations (TMD) are available on our website.

GET TO KNOW THE NIBA TEAM

What’s the last book that you read?

VIRAT NEHRU NIBA Editor and Content Writer

How long have you worked at NIBA?

Six months.

What does a typical day in your role look like?

I create the weekly newsletter Broker Buzz and this wonderful magazine that you’re holding in your hands right now called Insurance Adviser. As a news junkie, it’s really rewarding to be reporting on the many things that impact NIBA members and our profession more broadly, be it updates from ASIC and APRA or stories that reflect the amazing achievements of NIBA members and the broking community. I’m also excited for the NIBA Convention in October, as it will be my very first Convention and I cannot wait to experience the energy that such an event brings with it.

ABOUT NIBA

OUR MISSION

NIBA is the one voice for insurance brokers in Australia, representing their interests and promoting high standards of professionalism and competence.

OUR OBJECTIVES Representation

We represent the interests of members and their clients to governments, regulators, industry stakeholders, the media and the community in a manner that is respected and relevant. We have forged strong relationships at a state and national level to ensure that your interests are represented.

I read a lot of fiction. For some reason, I’ve always gravitated towards fiction over non-fiction. In recent times, I’ve become fascinated with climate fiction; stories that are tackling the climate crisis that we’re all living through right now. One of my favourite authors is Richard Powers. I cannot recommend his 2019 Pulitzer Prize winning novel, The Overstory, highly enough. It’s this beautifully sad epic of how nine American lives and their relationship with trees brings them together and changes them forever. If you want to understand how writers today are commenting on urgent issues of our time like climate change, this is a great place to start.

NIBA SAYS CONGRATULATIONS

NIBA CONGRATULATES THE FOLLOWING MEMBERS FOR RECEIVING THEIR QPIB DESIGNATIONS

Adam Luppino, Guardian Insurance Brokers Pty Ltd

Dominic Maratos, Westralian Insurance

Eric Richardson, Regional Insurance Brokers t/a QIB Group Pty Ltd

Pearl Gutierrez, Aon Risk Services Australia Ltd

If

you had to recommend a film, what would that be?

To Barbie or not to Barbie, that is the question! If there’s one thing I love more than reading fiction, it’s watching movies. I’ve volunteered for the Sydney Film Festival and the Melbourne International Film Festival for a decade now and I cannot imagine what my life would be without films. We recently screened the 1983 sci-fi cult classic Twilight Zone: The Movie on the occasion of its 40th anniversary, and it struck me that this film from 40 years ago is still more exciting than anything mainstream Hollywood is making today. So, if you’ve got a dusty old copy handy, plan a movie night-in on a Friday night. I promise, you will not be disappointed.

NIBA CONGRATULATES THE FOLLOWING MEMBER FOR BECOMING AN ASSOCIATE MEMBER

Adam Luppino, Guardian Insurance Brokers Pty Ltd

NIBA CONGRATULATES THE FOLLOWING MEMBER FOR RECEIVING THEIR QFSR DESIGNATION

Louisa Jammal, Convergence Wealth Management Pty Ltd

Professionalism

We set and promote high standards of professional practice for insurance brokers for the benefit of their clients and the community through the development of professional standards, QPIB, CPD accreditation and the Insurance Brokers Code of Practice.

Community

We provide members with opportunities to meet, share, grow and prosper, and build professional networks with the wider intermediated insurance community that will last throughout whole careers.

GET IN TOUCH!

Whatever your age, or level of experience, NIBA has brokers’ best interests at the core of everything we do. Find out what we can do to help benefit your business and your team at niba.com.au/membership

8 / INSURANCE ADVISER SEPTEMBER 2023 NIBA / Member Benefits

high quality ADVICE BEGINS WITH A

high quality NETWORK

Insurance Advisernet is looking for you to join the most awarded Authorised Representative network in Australia.

As a network that prides itself on its positive and supportive culture, you’ll never feel more at home. Our emphasis on expert advice means that you will have access to all the support systems you need to perform at your very best, including referral leads, IA Foundation initiatives to support your local community, marketing support and BOT technology for product comparison, providing more efficiency for you and your team.

NIBA EVENTS

NIBA stages a variety of educational and social events across Australia for the whole intermediated insurance community.

UPCOMING EVENTS

2023 NIBA VIC R U OK? DAY SEMINAR

WHERE: Marsh, Level 15, 727 Collins Street, Melbourne

WHEN: Thursday 14 September 2023

In recognition of R U OK? Day, the NIBA Vic Committee is proud to host a seminar by mental health charity, ‘It’s okay, not to be okay’.

‘It’s okay, not to be okay’ was developed in 2016 by three sisters following the tragic loss of their brother to suicide.

The charity’s mission is to advocate and create change in mental health, grief support and suicide prevention by increasing mental health literacy and raising awareness about available support services.

2023

NIBA QLD THE IMPACT OF UNDERINSURANCE SEMINAR

WHERE: UQ Brisbane City

WHEN: Wednesday 20 September 2023

Join us for an enlightening seminar on the significant topic of underinsurance.

In an ever-changing economic landscape, the impact of underinsurance has become a pressing concern for individuals and businesses alike.

This seminar aims to provide you with invaluable insights into the world of valuations and their pivotal role in mitigating risks associated with underinsurance.

In an increasingly interconnected world, the threat of cyber attacks is a critical concern for individuals and businesses alike. This seminar aims to equip you with essential knowledge to navigate the evolving cyber landscape, so you can best assist your clients in this space.

WHERE: The Star, Gold Coast

WHEN: Sunday 8 October to Tuesday 10 October 2023

2023

NIBA VIC YP BUSINESS INTERRUPTION SEMINAR SERIES

WHERE: QBE, Level 18, 839 Collins St, Docklands

WHEN: Wednesday 4 October 2023

UAC EXPO – SAVE THE DATES

14 SEPTEMBER 2023

UAC Adelaide Underwriting Expo

18 OCTOBER 2023

UAC Wollongong Underwriting Expo

2023

NIBA YP QLD YP CYBER SEMINAR

WHERE: UQ Brisbane City

WHEN: Tuesday 26 September 2023

Join us for a breakfast seminar on the compelling topic of cybersecurity.

Join us for an insightful seminar series on business interruption, presented by Colin Chinner.

Aimed at intermediate level brokers, the series will offer interactive sessions where you will learn about the importance of getting business interruption insurance right – and how to do it.

15 NOVEMBER 2023

NIBA UAC WA Underwriting Expo

More information is available on the UAC website, www.uac.org.au/events/

10 / INSURANCE ADVISER SEPTEMBER 2023 NIBA / Events

STAY UPDATED! Check out what’s happening close to you and register via the events calendar at niba.com.au/ events

2023 NIBA CONVENTION

NIBA.COM.AU / 11 Events / NIBA

A DEEP DIVE INTO YOUR SUBSCRIPTION LISTS

Within your NIBA Member Portal, you now have the ability to select which communications you would like to receive from NIBA. Here is a summary of all the options.

NIBA ESSENTIAL COMMUNICATIONS

Essential updates for Members on NIBA governance, including notification of upcoming member meetings, Code of Practice updates and NIBA Membership requirements.

POLICY & REPRESENTATION

Updates on policy changes, government regulations and advocacy efforts undertaken by NIBA to protect and promote the interests of insurance brokers.

BROKER BUZZ

Our weekly newsletter includes updates and insights on the latest trends, news and developments impacting insurance brokers.

NIBA EVENTS

Gain access to exclusive updates and announcements regarding upcoming events, conferences, workshops and seminars organised by NIBA.

NIBA INITIATIVES

Receive all the latest news and information about NIBA member services, benefits and initiatives, including NIBA Awards and the Broker Market Survey.

NIBA SPONSORS & PARTNERS

Sponsored content from partners and sponsors affiliated with NIBA. Receive information about products, services and offerings that may be of interest to insurance brokers.

12 / INSURANCE ADVISER SEPTEMBER 2023 NIBA / Member Portal

QPIB – A STATEMENT OF PROFESSIONALISM

Apply online at niba.com.au or email Scott Raymond, NIBA’s Membership Engagement Manager at sraymond@niba.com.au

• QUALIFIED PRACTISIN G INSURANCE BROKERQPIB

“QPIB represents competence and the will to strive for excellence.”

– CAITLIN CARSON, 2019 YOUNG PROFESSIONAL BROKER OF THE YEAR

WE ARE YOUR VOICE!

The following is an overview of some of the things NIBA has been examining on behalf of members.

NIBA SEEKS FEEDBACK ON INSURERS’ RESPONSES TO FLOOD CLAIMS

Ahead of the Parliamentary Inquiry into insurers’ responses to the 2022 floods, NIBA is seeking feedback from members whose clients and/or communities were impacted by these devastating events.

The comprehensive review will consider a range of aspects aimed at improving outcomes for Australian consumers including insurance availability, claims handling, land-use planning and mitigation. Specifically, the review will encompass the following areas:

• the experiences of policyholders before, during and after making claims;

• the different types of insurance contracts offered by insurers and held by policyholders;

• timeframes for resolving claims;

• obstacles to resolving claims, including factors internal to insurers and external, such as access to disaster hit regions, temporary accommodation, labour market conditions and supply chains;

• insurer communication with policyholders;

• accessibility and affordability of hydrology reports and assessments to policyholders;

• affordability of insurance coverage to policyholders;

• claimants’ and insurers’ experience of internal dispute resolution processes; and

• the impact of land use planning decisions and disaster mitigation efforts on the availability and affordability of insurance.

NIBA is seeking feedback from members who specialise in this area and wish to provide feedback to inform Treasury’s approach to implementation. Members can

provide feedback in writing to info@niba. com.au. You can also share your experience with flood insurance in Australia in 2022 and inform the public debate via the online survey at the Australian Parliament website.

The full report post the Parliamentary Inquiry by the House of Representatives Standing Committee on Economics is due by 30 September 2024.

To complete the online survey, go here: https://www.aph.gov.au/Parliamentary_ Business/Committees/House/Economics/ FloodInsuranceInquiry CONTACT

As always, brokers who have questions about these or any other government or regulatory matters should feel free

14 / INSURANCE ADVISER SEPTEMBER 2023 NIBA / Representation

NIBA

contact

Kewin at:

THE QR CODE TO COMPLETE THE ONLINE SURVEY

to

NIBA CEO Philip

pkewin@niba.com.au SCAN

RECORD NUMBER OF COMPLAINTS TAKEN TO AFCA IN 2022-23

Over the past 12 months, 6,987 complaints were lodged with the Australian Financial Complaints Authority (AFCA), making this a record increase of 34% when comparing complaints from the previous financial year.

AFCA’s Chief Ombudsman and Chief Executive Officer, David Locke, said the rise reflected growing financial stress in the community, the continued scourge of scams, and issues with insurer claims handling.

“We are deeply concerned by the volume of complaints consumers are having to escalate to AFCA,” Mr Locke said. “It’s not fair on consumers and is not good for business. We need to see a significant improvement from firms.”

IMPACT OF FINANCIAL STRESS A VISIBLE MARKER

The impact of financial stress due to rising interest rates and the increase in the cost of living are clear markers in complaints received in the final quarter of the financial year.

Overall, banking and finance complaints rose 27% to 53,638 in 2022-23. However, this figure rises to 31% when we look at the June quarter of this year as compared to the same period last year.

“We want to see banks and other finance providers continue to take active steps to

identify and support customers who are experiencing financial difficulty,” Mr Locke said.

RISE IN SCAM-RELATED COMPLAINTS AND THE NEED TO REGULATE BNPL

Scam-related complaints rose by a staggering 46%, with complaints totalling 6,048.

“We witness first-hand the human cost of this serious and sophisticated financial crime,” Mr Locke said.

“It’s pleasing to see initiatives by individual banks to combat scams, but we would welcome a more consistent approach across the sector.”

Mr Locke welcomed the government proposal for codes of practice addressing scams. “AFCA believes there is a need for enforceable standards, to lift the bar on scam prevention and remediation. This will also aid the work we do as an ombudsman service.”

Mr Locke would also like to see buy now pay later (BNPL) forms of credit to be regulated and supports the Federal Government’s intention to introduce regulation in this area.

Mr Locke noted that people were turning to other forms of credit to manage tight budgets.

“This underlines the importance of the Federal Government’s plan to regulate

BNPL under the National Consumer Credit Act, and recent reforms addressing what’s known as ‘payday’ lending,” he said.

BNPL complaints rose 57% in the past 12 months.

INSURANCE CLAIM HANDLING IS A MAJOR ISSUE

The top issue in complaints to AFCA in 2022-23 was delay in insurance claim handling, up 76%. Overall, general insurance complaints rose 50% to 27,924.

“We have been raising our concerns about claim delays with insurers for over 12 months now,” Mr Locke said.

“It is disappointing that this continues to be a concern. While we acknowledge the challenges insurers have faced, the bulk of complaints in the past year were not about natural disasters but about regular claims. We would like to see insurers take the necessary steps to ensure fewer policyholders have to take a complaint to AFCA.”

Delay in insurance claim handling was also a significant issue in superannuation. Super complaints rose 32% overall, but within this was a 136% rise in complaints about claim delays, including the payment of death benefits.

In 2022-23, consumers secured $253.8 million in compensation and refunds after coming to AFCA.

16 / INSURANCE ADVISER SEPTEMBER 2023 PROFESSIONALISM / Industry Bulletin

ASIC REVIEW FINDS INSURERS NEED TO IMPROVE CLAIMS HANDLING

ASIC is calling on general insurers to improve their claims handling practices and resourcing after a review of home insurance claims found weaknesses across five key areas.

ASIC’s Report 768, Navigating the storm: ASIC’s review of home insurance claims, assessed claims handling practices to coincide with the commencement of general insurers’ obligation to manage claims efficiently, honestly and fairly from January 2022. The review looked at data from more than 218,000 claims lodged between January and March 2022 from six insurers that cover 63% of the Australian home insurance market.

The insurers that participated in the review are:

• AAI Limited (Suncorp) (including AAMI, APIA, GIO, Shannons, Suncorp and Vero)

• Allianz Australia Insurance Limited (including Allianz and TIO)

• Auto & General Insurance Company Ltd (including Budget Direct, ING and Virgin)

• Insurance Australia Group, which includes Insurance Australia Limited and Insurance Manufacturers of Australia Pty Limited (including CGU, Coles, NRMA, SGIC, SGIO, WFI and RACV)

• QBE Insurance (Australia) Limited (including QBE, ANZ and Elders), and

• Youi Pty Ltd.

This review is part of ASIC’s ongoing work in relation to insurance claims handling. Insurers need to ensure their claims handling and dispute resolution functions are adequately resourced and sufficiently trained in order to meet their regulatory obligations as well as the standards in their voluntary General Insurance Code of Practice.

Deputy Chair Karen Chester said, “An insurance claim doesn’t have to be handled perfectly, but it must be handled well. Our claims handling review found good practices and poor practices across all six insurers. We identified five areas where insurers can and should make immediate claims handling improvements – consumer communications, project management, identifying vulnerable consumers and complaints, resourcing of claims and complaints handling”.

“Importantly, all five areas we’ve identified for improvement are within the insurers’ control. Improving claims handling practices and resourcing will make an immediate and positive difference to consumers when it matters most –

making a claim on their home insurance,” added Ms Chester.

REP 768 identified five areas for improvement:

• better communication with consumers about decisions, delays and complications

• better project management and oversight of third parties

• better recognition and management of expressions of dissatisfaction and complaints

• better identification and treatment of vulnerable consumers, and

• better resourcing of claims handling and dispute resolution functions.

ASIC examined all home insurance claims lodged with the six participating insurers between January and March 2022, and followed those claims through the claim handling life cycle for a further six months. The claims reviewed show that the insurers were unsurprisingly facing pressures due to severe weather events during and prior to this period.

ASIC also calls on insurers to further analyse the resourcing of claims handling and immediately address under-resourcing of their complaints handling (dispute resolution) functions.

NIBA.COM.AU / 17 PROFESSIONALISM / Industry Bulletin

A SNAPSHOT OF THE 2023

NIBA CONVENTION PROGRAM

The 2023 NIBA Convention program offers an exciting opportunity for attendees to hear from industry leaders on burning issues that are currently impacting the industry.

Over the course of two-and-a-half days, the program balances social events and networking opportunities such as the NIBA CGU Night Market Welcome Function and the NIBA Marketplace, with thought-provoking sessions about the breadth and diversity of the broking profession.

Sunday 8 October NIBA CGU Night Market – Welcome Function

Monday 9 October

NIBA MARKETPLACE

SESSION KEY SPEAKER(S)

Opening Keynote Dr Jordan Nguyen

Planning and Resilience: Where to From Here? Panel session with Brendan Moon, National Emergency Management Agency; Andrew Hall, Insurance Council of Australia; Drew MacRae, Insurance Brokers Code Compliance Committee and Financial Rights Legal Centre; Gary Okely, NIBA President

Future Risks – Propert Insurance Done Differently

Brian Maruncic, AXA AL

Unlocking Purpose, Performance and Power Dr Bronwyn King AO

Tradition to Transformation: Attracting Talent to the Industry

Cameron Sheild, Lockton Australia; Tom Wheeler, Lockton Australia; William Thompson, Thompson Insurance

Sharing Risk to Create a Braver World

Patrick Tiernan, Lloyds

NIBA MArketplace Happy Hour

TUESday 10 October

NIBA MARKETPLACE

SESSION

Reimagining Key Alliances: 5 Keys to Building Meaningful Business Relationships

Leading Change in a Changing World

KEY SPEAKER(S)

Nikki Heald, Corptraining

Jenny Haddad, Spring Business Consulting; Noel Kelly, AEI Insurance Group

The Exec Chat, Panel Session

Dianne Phelan, NIBA Past President; Rebecca Wilson, NIBA Director; Lynette Walsh, NIBA Director; Steven Hill, NIBA Director

The Importance of Technology in the Insurance Industry

Dale Smith, JAVLYN; Pieter Versluis, Transwest Insurance Brokers (NSW) Pty Ltd

Supporting Vulnerable Clients: Insights from Banking’s Best Practices

The Strategic Direction of NIBA

Prue Monument, AFCA

Gary Okely, NIBA President; Dianne Phelan, NIBA Past President; Nicholas Cook, NIBA Vice-President

Promoting Insurance Broking as a Career Choice

Closing Keynote

Philip Kewin, NIBA CEO and Cameron Sheild, Lockton Australia

Gus Balbontin

NIBA GALA DINNER AND AWARDS CEREMONY

18 / INSURANCE ADVISER SEPTEMBER 2023 COMMUNITY / 2023 NIBA Convention

HONOURING BROKER EXCELLENCE AT THE NIBA GALA DINNER AND AWARDS CEREMONY

Join us for a night of celebration, as we honour excellence in broking, insurance and underwriting and announce the winners for the following awards

TUESDAY 10 OCTOBER, 7:00PM-11PM THE GOLD COAST CONVENTION AND EXHIBITION CENTRE

2023 BROKER OF THE YEAR AWARD

THE FINALISTS FOR THE 2023 BROKER OF THE YEAR AWARD ARE:

2023 YOUNG BROKER OF THE YEAR AWARD

THE FINALISTS FOR THE 2023 YOUNG BROKER OF THE YEAR AWARD ARE:

2023 LEX MCKEOWN TROPHY

THE TROPHY CELEBRATES A BROKER’S LIFETIME OF ACHIEVEMENTS AND SERVICE TO THE INDUSTRY.

2023 LARGE GENERAL INSURER OF THE YEAR

VOTED BY BROKERS IN THE ANNUAL BROKER MARKET SURVEY, THE AWARD RECOGNISES THE BEST INSURER IN THE PAST 12 MONTHS.

2023 UNDERWRITING AGENCY OF THE YEAR

VOTED BY BROKERS IN THE ANNUAL BROKER MARKET SURVEY, THE AWARD RECOGNISES THE BEST UNDERWRITING AGENCY IN THE PAST 12 MONTHS.

2023 SPECIALTY INSURER OF THE YEAR

VOTED BY BROKERS IN THE ANNUAL BROKER MARKET SURVEY, THE AWARD RECOGNISES THE BEST SPECIALTY INSURER IN THE PAST 12 MONTHS.

NIBA.COM.AU / 19

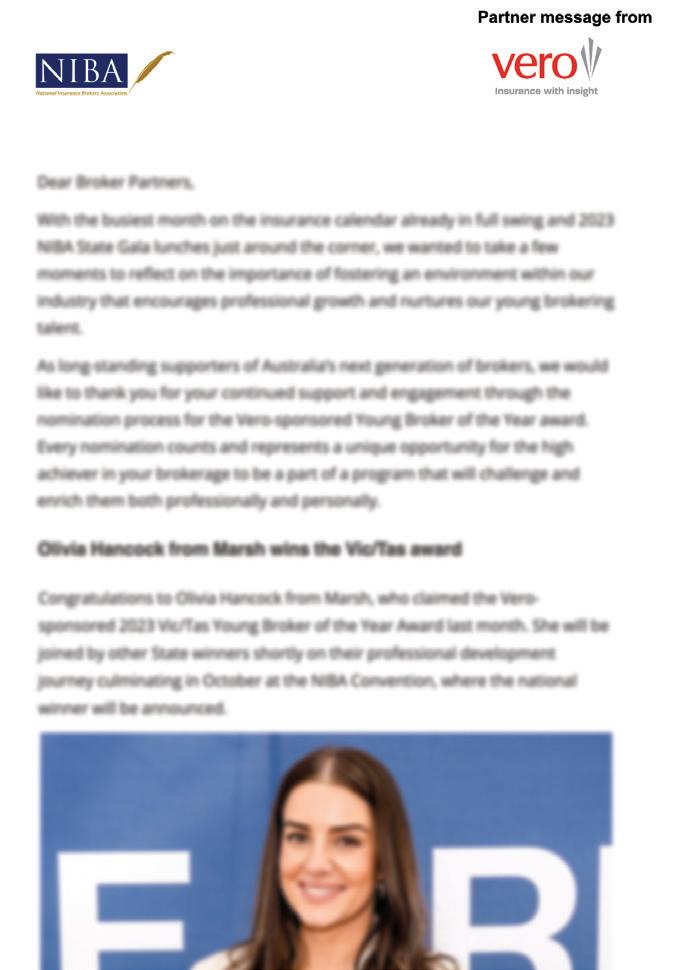

Olivia Hancock VIC/TAS winner

Joel Morrell NSW/ACT winner

Adam Luppino SA/NT winner

Taylor Burstow QLD winner

Justin Purslowe WA winner

Nick Hodges VIC/TAS winner

Barry Sonter NSW/ACT winner

Gary Thomas SA/NT winner

Lisa Shanta QLD winner Frans du Plessis WA winner

PROGRAM HIGHLIGHTS

Monday 9 October

Australia has been through an unprecedented period of natural disasters and a sustained hard insurance market. However, the lessons of the past have not translated into a cohesive and coordinated approach to planning and resilience. How can we collectively take a strategic approach to future planning and resilience that will better position Australian communities to protect against and deal with natural disasters?

In this session, join key industry stakeholders as they discuss these issues with a view to determining a better future path.

PLANNING AND RESILIENCE: WHERE TO FROM HERE THE EXEC CHAT, PANEL SESSION

Tuesday 10 October

In celebration of the remarkable contributions made by women in the insurance industry, this panel discussion aims to showcase their expertise, leadership and achievements. We believe in the power of diversity and inclusion, and this panel discussion will shed light on the unique perspectives and experiences of women in insurance.

Gain valuable insights from successful female leaders who have shattered glass ceilings, overcome challenges, and made a significant impact in the field. This is an incredible opportunity to connect with like-minded individuals, network with industry professionals, and be inspired by the remarkable journeys of women in insurance.

20 / INSURANCE ADVISER SEPTEMBER 2023 COMMUNITY / 2023 NIBA Convention

GARY OKELY

ANDREW HALL

BRENDAN MOON

DREW MACRAE

REBECCA WILSON

LYNETTE WALSH

DIANNE PHELAN

STEVEN HILL (MODERATOR)

REIMAGINING KEY ALLIANCES: 5 KEYS TO BUILDING MEANINGFUL BUSINESS RELATIONSHIPS

Tuesday 10 October

Developing key connections in business involves more than just a transactional approach. In today’s competitive market, understanding how to develop lasting partnerships with clients and key stakeholders, is crucial to increasing referrals and ongoing success. In this interactive presentation, led by Nikki Heald, Managing Director of Corptraining, attendees will learn the five keys they can use to sustain positive alliances and stand out in a cluttered market.

SUPPORTING VULNERABLE CLIENTS: INSIGHTS FROM BANKING’S BEST PRACTICES

Tuesday 10 October

Join Prue Monument, General Manager of Code Compliance and Monitoring, and Chief Executive Officer of the Banking Code Compliance Committee at the Australian Financial Complaints Authority (AFCA), as she delves into the important role brokers play in identifying and supporting vulnerable clients.

Drawing insights from the banking sector as well as other industry codes, brokers can gain practical insights to enhance client relationships, strengthen ethical practices, and contribute to a more inclusive financial future for all.

NIBA.COM.AU / 21

NIKKI HEALD PRUE MONUMENT

Exhibitors

principal partners

22 / INSURANCE ADVISER SEPTEMBER 2023 COMMUNITY / 2023 NIBA Convention

THANK YOU TO OUR SPONSORS AND EXHIBITORS

Convention 2023 'Banking Sponsor' Marketplace Happy Hour Sponsor Name Badge and Lanyard Sponsor Relax and Recharge Lounge Sponsor Espresso Bar Sponsor Closing Keynote Speaker Sponsor Gelato Bar Sponsor Writing Pads and Pens Sponsor NIBA Gala Dinner & Awards Cocktail Bar Sponsor Destination Supporter CONCURRENT SESSION SPONSOR PLENARY SESSION SPONSOR Commercial Safety Australia

REGISTER NOW!

Be quick to secure your full NIBA Member Convention registration ticket. A discount applied to group tickets of eight or more delegates. Conditions apply.

Reimagine: Think Differently 8-10

2023 THE STAR, GOLD COAST

Proudly sponsored by Register at: www.2023nibaconvention.com.au/registration EARN UP TO 10 CPD POINTS

OCTOBER

LEADING INTO THE FUTURE with the 2023 Bro ker Year Award state

COVER STORY / 2023 Broker of the Year

Award State Winners

24 / INSURANCE ADVISER SEPTEMBER 2023

ker of the winners

What will be the role of an insurance broker in the future?

From technological advancements to emerging risks such as cyber security and climate change, there are many new challenges on the horizon that brokers and the insurance industry have to contend with.

In the lead up to the 2023 NIBA Convention, where we will celebrate the shining beacons who are leading the way in the broking profession, Insurance Adviser caught up with the 2023 Broker of the Year Award state winners to get their insights on some of the most pressing issues that are impacting the industry right now, and what being a broking leader might look like in the future.

LEFT TO RIGHT: Gary Thomas, Nick Hodges, Frans du Plessis, Lisa Shanta, Barry Sonter

NIBA.COM.AU / 25

The Broker of the Year Awards are proudly sponsored by QBE

Nick Hodges on the evolution of a broker

and

giving back to the community

EVOLVING ROLE OF A BROKER

As brokers, we need to be evolving and transitioning from insurance brokers to risk advisors. This change has been happening for the past twenty years, but it is becoming increasingly important for the future as the world becomes more complex and new threats emerge. The world is constantly changing and more than ever, new and emerging risks have to be considered.

For example, we have new considerations like cyber risks, ESG (which is now on the radar of insurers and Australia’s middle market), global supply chain issues, political environments of Russia/Ukraine, China and Taiwan, the war for talent, and the list goes on.

Most, if not all of these issues weren’t on the agenda twenty years ago. We are now having conversations about these issues with many of our clients and helping them develop solutions. More and more of our conversations are now risk-lead rather than insuranceled discussions, so we must think more broadly than just insurance, and bring our knowledge and ‘risk thinking’ to the table to help our clients.

RELATIONSHIPS BETWEEN BROKERS AND CLIENTS

First and foremost, I’m big on adding value. We don’t want insurance and risk transfer to just simply be transactional and about price. Anyone can do that. I’d much rather have a conversation about a client’s business, what’s happening in their world, key challenges and opportunities, understand their environment and look at ways in which I can help.

To me, understanding the client underpins everything I do. Demonstrating to a client that you do understand, and that you have listened is critical. Quite often, we can assume we know what a client needs or wants without asking, or we fail to listen to what a client is telling us.

Bringing additional services and value to a client is something I always focus on. It can be a fine balance between ‘selling’ as opposed to identifying a need for a particular client and bringing them potential solutions. It’s critical that we strike that balance.

In the end, it’s about the small things such as keeping promises, managing expectations, responding to emails, phone calls, and managing timelines. This sounds so simple and in many ways it is – but quite often, these things are overlooked. My view is, if you

do these little things, you will build trust and credibility with your clients.

ON THE NEXT GENERATION OF BROKING TALENT

I think a big part of attracting top talent to our industry is about not just looking at broking in isolation, but insurance as a whole.

Brokers play a critical role in society and business and provide professional services. We should be seen as a destination industry for school and university graduates in the same way as legal, banking, engineering industries and the like are.

Education is key in bringing about this change and spreading the word about the benefits and opportunities of the industry. In many ways, our industry is a best kept secret – but we have to change that. I think, if more people were truly aware of where the industry can take them, knew about the opportunities and the type of work we do on a day-today basis, we would definitely see an uptick in interest.

I think all brokers and insurers should include school leavers and university graduates in their recruitment and succession planning. Getting people into our industry early, learning from senior people and learning on the job is paramount. There is no substitution for sitting with a more experienced or senior colleague and learning from them. The more young people we bring into the industry now, the better placed we will be for the future.

ON GIVING BACK TO THE COMMUNITY

I really enjoy giving back and using the fortunate position that I am in to do something.

When I was interviewed for the VIC/TAS Broker of the Year nomination, I spoke about some charity fundraising I had done in the past and how it had been a little while since I did something on a larger scale. I committed to the panel that if I did win, I would use that as a platform and challenge myself to do something on this front.

When I was awarded the Graham “Bear” Stevens trophy for winning the VIC/TAS Broker of the Year, I saw this as a good opportunity to do something charitable and use my profile for that. I also think giving back to the community through a charitable initiative is a great way to honour the award and Graham’s legacy.

26 / INSURANCE ADVISER AUGUST 2023 COVER STORY / 2023 Broker of the Year Award State Winners

NIBA.COM.AU / 27

The Broker of the Year Awards are proudly sponsored by QBE

WINNER OF THE VIC/TAS BROKER OF THE YEAR AWARD Corporate and Commercial Leader, Marsh

28 / INSURANCE ADVISER SEPTEMBER 2023 COVER STORY / 2023 Broker of the Year Award State Winners

WINNER OF THE NSW/ACT BROKER OF THE YEAR AWARD

Senior Account Manager, Finsura Insurance Broking

Barry Sonter on

why good

broking

is a team effort

BROKING IS NOT AN INDIVIDUAL PURSUIT

As a broker, you’re like a conductor in an orchestra. Providing quality broking advice to clients is a team process; if any part of the team lets you down, you can’t deliver for your client. In my role as a broker, even though I am ultimately responsible to the client for all aspects of their account management, I rely on my support team such as the claims managers, administrators, assessors and underwriters to play their part.

That’s why, I have always focused on building relationships with underwriters, claims teams and assessors, as I consider these relationships to be imperative in meeting my client’s expectations. I have learnt that you need to work with them to source a solution. Experience suggests that you need to be respectful and understand that they have limitations, procedures and protocols which they must undertake, and that sometimes means that we may not get the response we seek.

LISTENING TO YOUR CLIENT’S STORY

Everyone’s got a story to tell, you just need to be patient and build relationships. Clients tell me things face-to-face that they wouldn’t do over the phone. Client visits, in my opinion, are absolutely essential. By taking time to visit your clients, you receive an insight into their business, their risk management protocols and their future plans. Every client has a story to tell, and they are very proud of their achievements and what they have created. When you pay a visit, it demonstrates to a client that you are interested in their business.

Time is very important. You need to take time to understand your client’s problems. Because if something goes wrong, you, as the broker, are their best friend.

IMPORTANCE OF A BROKER

I believe that an insurance broker’s role is far more important than sourcing competitive premiums. Our role is to understand our clients’ business and exposures, and structure coverage placements that will provide them with the indemnity they need should something go wrong.

Clients develop trust with their broking partner when they have peace of mind that in the event of a crisis, their broker will come through for them. Clients rely on us to structure their cover such that it will protect them in a

crisis and in times of need. We are essential to our clients, especially in these critical moments.

POINT OF DIFFERENCE AS A BROKER

Anyone can sit in front of a screen, compare policies and quotes, and say which one is cheaper. Adopting a personal approach to our clients, that’s our point of difference as brokers. Professional brokers sell more than just price. We sell credibility, we sell experience, and we sell knowledge that we can tailor an insurance program which will respond to those contingencies which would have serious implications for our clients. That’s our point of difference.

I have always maintained that brokers are essential and are considered to be a ‘trusted business partner’. I see this relationship becoming even more crucial in the future, as placements become more difficult with emerging risks such as climate change and other global influences.

With new risks on the horizon, clients will engage with brokers who understand their business and can source the required coverage. The relationships you build will continue to be important, because no matter the risk, as a broker you will need to work with underwriters and specialist agencies in order to secure placements for your clients.

KEEPING PACE WITH THE CHANGES

Broking is becoming more complex and has more challenges than ever before.

Going forward, the general insurance broker is going to need the support of a team with specialist product knowledge, especially as new covers evolve, and new contingencies arise. Cyber risk, for example, is going to be a major factor, and as technology changes, so will the need for improvements and understanding of covers.

Property placements have also become increasingly difficult. With underwriters providing reduced capacities, brokers need to understand how to negotiate terms using various underwriting partners and understanding parametric insurance for risks with specific and/or difficult exposures.

Having said that, despite all these changes that may create uncertainty, I believe that our industry has an incredible future. Clients will need the support of quality brokers to navigate them through continual changes in exposures and availability of covers.

NIBA.COM.AU / 29

The Broker of the Year Awards are proudly sponsored by QBE

Gary Thomas on the value of tertiary education and continuous learning

ADAPTING TO THE FAST-PACED NATURE OF SOCIETY

We live in such a busy society that people just don’t have that much time to spend anymore.

We’re all a bit time poor. People are happy communicating via email. They don’t necessarily even want to talk as much on the phone, which to me feels like a real shame. It’s when you have conversations over the phone or face-to-face with people that you get to understand their personalities, and as a broker, that’s when you really get the opportunity to be persuasive about what you’re trying to achieve – whether it’s about placing a risk or getting a claim over the line. You don’t get that emotion or inflection from the other end in an email or a text message.

It’s the nature of society. We want a fast fix to everything. But, when it comes to making important decisions such as your insurance policy, taking the time to reflect and consider rather than rushing into a decision can be incredibly useful.

IT’S ALL ABOUT THE PERSONAL TOUCH

Trying to advise on cover and not on price, that’s the main thing.

That’s the value that brokers can provide. We build meaningful relationships with our clients so that we can help them in times of crisis, such as at a time when they need assistance for a claim. It’s this personal touch which clients may not get if they opt for a policy that’s direct with an insurer. When it’s claim time, brokers provide a massive value add. Clients may not even realise this when they first come to us for a quote for their policy.

Good brokers also take the initiative and are proactive in their communication with their clients, being in touch with them at regular intervals, which can help give peace of mind to a client; knowing that someone is there looking out for them and their needs. A broker may not have an answer immediately, but they will do the research that’s needed and get back to their client with a balanced response. That’s part of the due diligence that’s required for this job.

THE VALUE OF TERTIARY STUDY

The knowledge that you gather and the learning that you need to do for this job cannot be underestimated.

I only went up to Year 11 in High School, I didn’t do Year 12. So, my success as a broker has really been through tertiary studies via TAFE and other avenues. When I started my career, it was expected as a young broker finding his feet that you would undergo tertiary education to complement on the job training.

I’m adopting this approach with one of the younger brokers in my office. They are currently doing their diploma.

If they pass their subjects, I will pay their diploma fees. Everything that you learn, you may not put into practice next week or next month. But say, in six months’ time, the information you’ve gathered through your studies will come in handy. You will remember having studied a case that you can draw from in dealing with your client.

PREPARING THE NEXT GENERATION OF BROKERS

A lot of the knowledge and experience that senior brokers have is draining away. Colleagues who are my age or close to my age are nearing retirement or leaving the industry. I’m seeing it happen around me and we [as a community of brokers] do talk about this. We wonder where the next generation of confident young brokers will come from. We need to make sure that the knowledge transition takes place – that all the experience of senior leaders from insurers and brokerages is appropriately transferred to the next crop of younger brokers.

ADVICE FOR YOUNGER BROKERS

When we’re starting out, all of us are a bit naïve in our early days because we think our job is about recommending cover. Of course, that’s partially true. But, it’s not all there is to this job [of being a broker]. When the big claims come, you’ve got to stand shoulder-to-shoulder with your client. The quality of your work is what you’ll be judged upon. There’s nowhere to hide.

Until you’ve got some war stories of your own, it’s easy to think that this job is just about recommending cover. You need to realise that someone’s financial wellbeing is dependent upon the decisions you make as a broker at the time of providing advice. It’s a big responsibility that shouldn’t be taken lightly.

THE VALUE OF TEAM SPORTS

Team sports are great for character building.

I’m heavily involved in team sports. It gets you to interact with people outside your bubble; people who might have different life experiences to you or people with a different socio-economic status. That interaction helps give you a better appreciation of society and the camaraderie that you build with someone with a different lived experience helps build empathy, which is a necessary trait to be a good broker.

I’m still playing hockey myself at sixty years of age. I’ll be playing hockey for the South Australian Over 60s Masters, and then flying straight from that competition up to the NIBA Convention!

30 / INSURANCE ADVISER SEPTEMBER 2023 COVER STORY / 2023 Broker of the Year Award State Winners

The Broker of the Year Awards are proudly sponsored by QBE

OF THE SA/NT BROKER OF THE YEAR AWARD

NIBA.COM.AU / 31

WINNER

Managing Director, Thomas Insurance Brokers

32 / INSURANCE ADVISER SEPTEMBER 2023 COVER STORY / 2023 Broker of the Year Award State Winners

WINNER OF THE QLD BROKER OF THE YEAR AWARD Director, SB Protect Insurance Brokers

Lisa Shanta

on being an advocate for more women leading in the industry

LOOKING TO THE FUTURE

I believe that young brokers of the future will need to be very fluid and aware of changes as they occur.

I believe the insurance broking profession will continue to change and adapt to social, economic, national, and international conditions as it has in the past. There will continue to be changes in compliance, product services and client needs. Because of these changes, younger brokers will need to have great social skills when conversing with their clients so that they’re able to decipher their clients’ complex needs as they evolve and change.

In the new world, I believe that customer service will only become more and more important to ensure customer retention and satisfaction. With continuously rising premiums, clients are looking for a broker who is knowledgeable, approachable and who is genuinely looking out for their best interests.

PERSONAL BROKING PHILOSOPHY

My broking philosophy has always been to put my clients and their needs first.

My goal was always to make a difference in my clients’ lives, and I really believe I am achieving this. I believe I am showing everyone what is possible as I have created a caring and compassionate brokerage that truly has the clients’ best interest at heart. I will always do everything I can and explore every avenue to ensure I find the best outcome for my clients.

PASSING ON KNOWLEDGE AND EXPERIENCE TO THE NEXT GENERATION

I have always seen it as a privilege to pass my knowledge on to young brokers.

I believe the majority of brokers out there would agree with me and would feel the same way. I believe more awareness about the industry needs to be generated to attract young brokers. This could be accomplished perhaps through work experience initiatives and charity days. These initiatives and steps to reach out and connect could help to show young people just how much potential the industry holds for them should they choose to pursue a career in insurance broking.

THE VAST POTENTIAL OF THE INSURANCE INDUSTRY

On my first day of the job, I wish I had known just how much potential the insurance industry has. After so many years, I now understand how many different and varied career paths there are within insurance broking

and how accommodating the industry is for working mothers. Had I realised this potential earlier, I feel that I would have undergone courses and learning earlier, and launched myself into my career sooner.

I feel that it is very important to ensure young brokers know of this potential so that they can make educated decisions as to their future and careers sooner. I also think that making this potential known would further help attract young people to the insurance industry. There are so many avenues and pathways that you can explore in this industry.

SEEING YOUNG WOMEN SUCCEED IN THE INDUSTRY

I am very passionate about helping young women pursue careers within the insurance industry.

I take a lot of pride in being able to facilitate my team in growing within their roles and offering them a caring and compassionate workplace to flourish in. I am very proud of the fact that I have been able to create several roles and job opportunities and feel that my team are continuously learning and growing as brokers. I take training my team very seriously and try to impart as much wisdom and knowledge as I can to them.

My hope for the future is that, as my business grows, I will be able to offer more jobs to young brokers and further help groom the next generation of young women into compassionate brokers who put their clients first.

The top end of the insurance world is still very maledominated. There are not many women who have been in a position to take on the challenge of being a Director, for example. You’ll see many women in junior or middle management roles such as Account Executives or Account Managers, but not many who are able to step up into the C-suite bracket.

That’s where I want to use my position to let women know that you can have a career in insurance from day one. You can even have work life balance – you can have kids, take a career break if you need to, and then transition back into the industry. The industry has that flexibility where it allows you to make these choices and you don’t necessarily have to choose between your family or your career.

There’s plenty of room for all of us; for both men and women, to have successful leadership careers in the industry. If you’ve got that passion, just go for it.

NIBA.COM.AU / 33

The Broker of the Year Awards are proudly sponsored by QBE

Frans du Plessis

on new ways of thinking to address the skills gap in the industry

ROLE OF A BROKER MOVING FORWARD

The role of a broker is likely to evolve significantly due to ongoing technological advancements and shifts in various industries.

Digital transformation: Brokers will likely need to fully embrace digital platforms and tools to stay competitive and may offer some of the best insurance wordings on the market. Online automated systems, and digital communication will become even more prevalent, making it crucial for brokers to have strong digital skills and an online presence.

Data analytics and AI: Brokers may increasingly rely on data analytics and artificial intelligence to provide personalised recommendations to clients. AI algorithms could analyse market trends, client preferences, and risk factors to offer more tailored investment options. As an example, we are currently trialling a telephone AI system to lodge our clients’ claims quicker and more efficiently.

Adopting a consultative approach: As technology automates basic transactions, brokers could focus on providing in-depth risk advice, strategies in minimising risk exposures and managing their insurance program better.

Education and transparency: With information readily available online, brokers should become educators, helping clients understand complex insurance issues, claims and potential exposures. Transparency will be crucial, and brokers will need to communicate clearly about fees, risks and potential additional cost.

ADDRESSING THE KNOWLEDGE AND SKILLS GAP

To keep up with these changes, insurance brokers need to continuously update their knowledge and skills. Clients’ expectations are changing. They expect brokers to offer personalised solutions, transparent advice, and quick responses.

Brokers must develop strong interpersonal and communication skills to meet these expectations. Experienced brokers could play a role in mentoring new entrants to the field. Establishing a culture of knowledge sharing within brokerage firms can help bridge the skills gap.

IMPORTANT LESSONS TO REMEMBER

Communication and time management are key. Learning to manage staff was one of the biggest challenges for me. The insurance work is actually the easy part. Learning to deal with staff is one of the most important skills you can learn and get good at for a long and successful career in insurance.

Technology can streamline processes, but it’s important to find a balance between automation and maintaining the personal touch that clients value. Being accurate and precise is an important skill as an insurance broker. Ensuring that you do not make errors will go a long way in becoming a good broker.

To do this, one should always double-check their work, including policies, documents and other necessary records. Being thorough in record-keeping also comes in handy when it comes to compliance. Having detailed records of your interactions, agreements and policies can help save you from potential disputes.

TAKE ON NEW CHALLENGES

My biggest journey started with a single step. Walt Disney said it best for me: ‘if your dreams do not scare you, dream bigger’. I believe if you can dream it, you can achieve it. Stay focused and work for it. Always remember where you came from and support the up-and-coming brokers. You will be surprised how many will remember you for the kindness you showed them.

Addressing the knowledge and skills gap in insurance broking requires a proactive approach from both individual brokers and the industry as a whole. Continuous learning, embracing technology, and adapting to changing market dynamics will be key factors in overcoming this challenge and ensuring the long-term success of insurance brokers. The insurance industry is undergoing significant changes due to technological advancements, regulatory shifts, and changing customer preferences. The national winner of the Broker of the Year Award will be announced on 10 October 2023, at the NIBA Gala Dinner and Awards following the 2023 NIBA Convention.

34 / INSURANCE ADVISER SEPTEMBER 2023 COVER STORY / 2023 Broker of the Year Award State Winners

Support your state’s Broker of the Year Award winner by purchasing your tickets today.

The Broker of the Year Awards are proudly sponsored by QBE

NIBA.COM.AU / 35

WINNER OF THE WA BROKER OF THE YEAR AWARD

Director, Grace Insurance

WORKING FOR THE FUTURE

By MARTIN WANLESS

By MARTIN WANLESS

36 / INSURANCE ADVISER SEPTEMBER 2023 FEATURE / Workers Compensation

Workers compensation challenges are evolving – but a swift and effective return to work is still of paramount importance.

NIBA.COM.AU / 37

FEATURE / Workers Compensation

The latest statistics from Safe Work Australia show that, for every 1,000 employees, 10-and-a-half ‘serious’ workers compensation claims are made. And according to AIHS, work-related injuries and illnesses cost the Australian economy $28.6bn annually.

Those are significant numbers, so it’s no surprise the focus of everyone involved in looking after the safety and wellbeing of workers is to first minimise incidents occurring in the first place – and help those who do suffer injury or illness in the line of work to get back into the workforce as swiftly as possible.

“A holistic approach to worker rehabilitation and wellbeing in the claims management process is important,” says Angela Bertoncin, Head of Workers Compensation, General Insurance, Zurich Australia & New Zealand.

“Key enablers across the industry include the use of emerging technology (such as wearables), workplace rehabilitation interventions focused on holistic wellbeing, mental health support extending beyond usual tools to include practices such as meditation and the utilisation of specialised allied health services.”

That mental health support is particularly important, with an increasing

number of mental health claims being made post-COVID-19.

“One of the significant challenges facing workers compensation schemes around the globe is the rising number of psychological injury claims,” says Mary Maini, Group Executive, Workers Compensation at icare.

“The changing nature of work due to new digital technologies and the impacts of COVID-19 and economic pressures have also posed new challenges for workplaces.”

The increase in mental health claims isn’t a surprise. The stigma of talking about

mental health challenges no longer exists, while people are still processing their COVID-19 experiences, and many are still coming to terms with a new way of working.

Leigh Ebzery, General Manager

Underwritten and Distribution Workers Compensation at Allianz, says there has also been an increase in secondary psychological claims.

“There’s been an increase in the propensity of people that have a physical injury and claim to develop psychological issues as a result of that claim.

38 / INSURANCE ADVISER SEPTEMBER 2023 FEATURE / Workers Compensation

“ANY ISSUES HAVE TO BE IDENTIFIED EARLY, AND AN APPROPRIATE SET OF PLANS, INCLUDING TREATMENT, NEED TO BE PUT IN PLACE. IT’S ESSENTIAL THAT THE RIGHT SUPPORT NETWORK IS IN PLACE AND THE WORKER IS FULLY SUPPORTED THROUGHOUT THEIR TREATMENT PROGRAM.”

– LEIGH EBZERY, GENERAL MANAGER UNDERWRITTEN AND DISTRIBUTION WORKERS COMPENSATION AT ALLIANZ

This information is general advice only and does not take into account your objectives, financial situations or needs. You should obtain and consider the Policy Wording from zurich.com.au before making a decision. The issuer of general insurance products is Zurich Australian Insurance Limited (ZAIL), ABN 13 000 296 640, AFS Licence Number 232507 of 118 Mount Street, North Sydney NSW 2060. ZU24344 V2 09/23 CGAA-021128-2023 Zurich Workers Compensation Zurich’s experience in risk mitigation and proactive claims management along with local technical underwriters, real-time claims reporting and a range of wellbeing resources can help your clients to protect their greatest asset - their people. Workers Compensation for WA & TAS Helping your clients create a safe & protected workplace. For Workers Compensation in WA and TAS, contact us today. zurich.com.au/WC WA 08 9261 1599 TAS 02 5111 5900

FEATURE / Workers Compensation

icare recognises that ongoing training and education of case managers is key to assisting injured workers getting back to work and health. We want to make case management a profession that continues to attract the best and brightest to help in the delivery of treatment so injured workers can recover and return to life and work faster.”

Having a thorough understanding of the situation and making appropriate plans in conjunction with the injured party is essential to achieving an effective return to work, says Ebzery.

“It is, therefore, increasingly important for employers to be able to identify those issues early in a claim to ensure the injured worker isn’t off for any longer period of time, and to also make sure we provide the right support to the injured party, too.”

THE IMPORTANCE OF RETURN TO WORK

Government research shows that if an employee is absent for 20 days, they have

a 70 per cent chance of returning to the workplace; if they’re absent for 70 days, that drops to 35 per cent – illustrating just how important it is to get people back into the workforce quickly.

Strong case management is essential to do this – and requires employers, insurers and brokers to work together to achieve the very best outcomes.

Maini says, “To support employers in improving return-to-work outcomes,

“Any issues have to be identified early, and an appropriate set of plans, including treatment, need to be put in place.

“It’s essential that the right support network is in place and the worker is fully supported throughout their treatment program.

“Ultimately, we are trying to get that person back into full-time employment, and to help them return to work in a healthy and sustainable fashion. When we work closely and together, there are

40 / INSURANCE ADVISER SEPTEMBER 2023

“A HOLISTIC APPROACH TO WORKER REHABILITATION AND WELLBEING IN THE CLAIMS MANAGEMENT PROCESS IS IMPORTANT.”

– ANGELA BERTONCIN, HEAD OF WORKERS COMPENSATION, GENERAL INSURANCE, ZURICH AUSTRALIA & NEW ZEALAND

Help your clients unlock cash flow Proudly industry accredited Today, strong businesses need easy access to cash flow. Hunter Premium Funding, one of Australia and New Zealand’s leading specialist premium funders is here to help your clients when they need it the most. Visit HPF.com.au to find out how Hunter can help your clients today. Ready For Today, Prepared For Tomorrow Hunter Premium Funding Limited ABN 80 085 628 913. A company of Allianz Australia Insurance Limited ABN 15 000 122 850 AFS Licence No. 234708

WORKING IN THE ‘GIG ECONOMY’

The world of work has changed, and an increasing number of people aren’t ‘working’ in the traditional sense, with many on contracts or working on a freelance basis.

While this has business benefits, it also comes with risk, as traditionally, a workers compensation policy wouldn’t respond to an injury or illness suffered by someone who isn’t formally employed by the business.

It is, therefore, essential that businesses understand their responsibilities and are kept up to date with any changes to legislation. Bertoncin says, “It’s important that customers understand the workers compensation legislation within their jurisdiction and continue to upkeep this knowledge as the landscape continues to change. Employers have a duty of care to temporary and freelance workers beyond workers compensation.”

Maini says that new ways of working open up a whole range of risks for employers that need careful consideration – and advises brokers to take a watching brief.

“The changing nature of technology includes the emergence of new ways of working and the development of new business models that engage contractors and freelance workers through digital platforms (like phone apps and web portals). These new work models present new risks and liabilities for employers and businesses to consider.

“Brokers can play a helpful role in reminding employers to consider their workforce’s exposure to safety risks and stay informed about future changes in national and state laws that may redefine their obligations within new business models emerging in their industry.”

Ezbery says this provides another opportunity for brokers to add value.

“With the emergence of the gig economy, where people might be working three or four different jobs, workers compensation doesn’t always necessarily respond because they’re not traditional workers.

“This creates the opportunity for brokers to spot gaps in cover and to provide a solution to fill them.”

better outcomes for the injured worker and the employer.”

PREVENTION BETTER THAN CURE

For brokers, the potential sphere of influence ranges from helping navigate claims and return to work, to helping employers prevent incidents from occurring in the first place.

Maini says, “Brokers play a key role in supporting employers to reduce injury frequency and communicating the importance of earlier return to work and health as quickly and safely as possible, in turn, reducing premium cost for employers.

“They can support their customers to help them understand the range of incentives available for employers to report incidents early, introduce safety initiatives and support injured workers returning to work.

“They can also help employers by explaining the practical support offered

to businesses to deliver safe, healthy workplace environments and the physical and psychosocial risks that unsafe practices can expose an employer to.”

Bertoncin agrees. “Key considerations here include human and organisational performance, continuous improvement strategies, the use of technology to reduce risk, and implementing workplace health and wellbeing initiatives.

“Fostering a proactive and healthy culture around reporting and management of workplace incidents and injuries, including near misses, is also important.”

In terms of offering a serious value-add, helping clients implement a safety-first culture that helps keep incidents to a minimum could be more valuable than anything else.

42 / INSURANCE ADVISER SEPTEMBER 2023 FEATURE / Workers Compensation

“THE CHANGING NATURE OF WORK DUE TO NEW DIGITAL TECHNOLOGIES AND THE IMPACTS OF COVID-19 AND ECONOMIC PRESSURES HAVE ALSO POSED NEW CHALLENGES FOR WORKPLACES.”

– MARY MAINI, GROUP EXECUTIVE, WORKERS COMPENSATION AT ICARE

NIBA launched the 2022 Insurance Brokers Code of Practice on 1 March 2022, and it came into effect on 1 November 2022. It is important that all members have implemented the necessary policies and procedures to comply with their new Code obligations. A number of resources are available on the NIBA website to assist members in implementing the Code.

For a copy of the Code, visit niba.com.au/code INSURANCE BROKERS CODEOF PRACTICE For a copy of the Code, visit niba.com.au/code IA0722p58-60 Events Pictorial.indd 59 25/7/2022 1:40 S&P GLOBAL RATINGS *For the S&P Global Insurer Financial Strength Ratings Definitions visit: https://www.niba.com.au/resource/standardandpoors.pdf Copyright © 2023 S&P. This material is reproduced with the permission of S&P. Reproduction of this the S&P Information in any form is prohibited without S&P’s prior written permission. Neither S&P, its a liates nor any of their third-party licensors: (a) guarantee the accuracy, completeness or availability of the S&P information, or (b) make any warranty, express or implied, as to the results to be obtained by Insurer Financial Strength Ratings or any other person from the use of the S&P information or any other data or information included therein or derived therefrom, or (c) make any express or implied warranties, including any warranty of merchantability or fitness for a particular purpose or use, or (d) shall in any way be liable to Insurer Financial Strength Ratings or any recipient of the S&P information for any inaccuracies, errors, or omissions, regardless of cause, in the S&P information or for any damages, whether direct or indirect or consequential, punitive or exemplary resulting therefrom. Ratings are statements of opinion, not statements of fact or recommendations to buy, hold, or sell any securities. S&P Global (Australia) Pty. Ltd. holds Australian financial services licence number 337565 under the Corporations Act 2001. S&P Global credit ratings and related research are not intended for and must not be distributed to any person in Australia other than a wholesale client (as defined in Chapter 7 of the Corporations Act). Ratings are based on information received by Ratings Services. Other divisions of S&P Global may have information that is not available to Ratings Services.

WHILE M&A ACTIVITY SLOWS, BROKER OPPORTUNITIES QUICKEN

Global

By MARTIN WANLESS

44 / INSURANCE ADVISER SEPTEMBER 2023

M&A activity may have slowed, but increasing regulation means brokers can play an ever more important role.

NIBA.COM.AU / 45 FEATURE / Mergers & Acquisition

The global economic climate has affected many facets of our lives. From mortgage payments to the price of milk, we’ve seen costs go up and up. Of course, that type of economy creates short, medium, and long-term uncertainty. As spending tightens, business performance can be affected. Measures to maximise profit need to be taken, and a business may not have the same value as it did 12 or 18 months ago – certainly not in the eyes of a company looking to acquire.

All of this adds up to a merger and acquisition market that’s seen a domestic and global slowdown.

“Valuation continues to be the key issue affecting transactions, and this is mainly on bridging the gap between seller and buyer expectations on price,” says Sam Thomas, Client Director – M&A and Transaction Solutions at Aon.

“Deal sizes are down, and some deals have financial distress associated with them, so we are seeing insurers being cautious around diligence and financial valuations. We are seeing less auctions as a

process and more bilateral arrangements with parties.”

William Lewis, Head of Liberty Global Transaction Solutions, Asia Pacific, agrees and says that as a consequence, this has created an increasingly competitive insurance landscape.

“The current environment has driven uncertainty in acquisitions,” he says. “Deals are taking longer and often are being agreed at lower values than those from two years ago.

“There has been a slowdown in deal activity and deal values which has occurred at the same time as an influx of new startups bringing insurance capacity online. This has put downward pressure on rates and created a competitive environment and a splitting of the market into established players and new entrants.”

THE CHALLENGE OF REGULATION

The financial services sector has gone through significant change since its failings were spotlighted by the Royal

46 / INSURANCE ADVISER SEPTEMBER 2023 FEATURE / Mergers & Acquisition

“WE NEED TO GET OUR HEADS AROUND FASTPACED CHANGING REGULATORY AND POLITICAL ENVIRONMENTS TO ENSURE THAT WE CAN SPOT EMERGING RISKS AND OPPORTUNITIES.”

– WILLIAM LEWIS, HEAD OF LIBERTY GLOBAL TRANSACTION SOLUTIONS, ASIA PACIFIC

cbnet.com.au/discover-cbn

Commission. And, as such, the increasingly regulatory environment that has subsequently been established has resulted in greater scrutiny when financial sector purchases take place.

“Post-Royal Commission, there’s been a lot of regulatory change in the financial services sector, and some of that is still fairly young,” says Mathew Kaley, who leads the Financial Services practice at McCabes law firm.

“That increases both the burden on the business but also the uncertainty for the purchaser about whether or not the company they’re looking at is compliant or poses a risk.

“In the last 12 months or so, we’ve seen some fairly aggressive activity from ASIC in relation to recent regulatory reforms. After the Royal Commission, ASIC adopted a new catch cry: ‘Where there’s a breach, we asked ourselves, why not litigate?’ While it has since stepped away from that, ASIC remains active.

“For the first two years after the Royal Commission, ASIC was mostly focused

on following up on Royal Commission case studies. But since then, or at least in the last 18 months, they’ve moved from working with industry to implement all of this regulatory change, to providing guidance and prompts and, now, to prosecuting breaches. I expect those actions will continue.”

THE ESG CHALLENGE

ESG is a constant challenge for every business today, and when merging with or acquiring a new company, it’s important to minimise the chances of inheriting any risk.

“ESG provides significant opportunity for our market but also challenges,” says Lewis. “We need to get our heads around fast-paced changing regulatory and political environments to ensure we can spot emerging risks and opportunities.”

Thomas agrees, and highlights that, ultimately, the focus lies on good businesses.

“We are seeing the insurance markets welcome ESG with a focus on

48 / INSURANCE ADVISER SEPTEMBER 2023 FEATURE / Mergers & Acquisition

“A TRUSTED ADVISER CAN OFFER SOLUTIONS THAT CLIENTS MAY NOT BE AWARE OF, AND BROKERS HAVE GOOD RELATIONSHIPS WITH INSURERS TO DISCUSS BESPOKE SOLUTIONS WITH INSURANCE MARKETS APART FROM TRADITIONAL SOLUTIONS.”

– SAM THOMAS, CLIENT DIRECTOR –M&A AND TRANSACTION SOLUTIONS AT AON

The NEXT generation

Cloud software solutions for insurance intermediaries by EBIX, Australia’s #1 InsurTech provider

WinBEAT is Australia’s most popular broking system solution designed specifically for General Insurance Intermediaries.

After 4 years of development, we are happy to introduce WinBEAT NEXT: A browser-based software program designed specifically for General Insurance Intermediaries.

WinBEAT NEXT combines a state-of-the-art software environment with a feature-rich processing environment.

You no longer have to rely on your IT provider to perform upgrades or updates. The Ebix Australia team takes care of everything. Register your interest for WinBEAT NEXT via the link below.

ebix.com.au/winbeatnext2023

Data security and integrity

Available online 24/7

Over 50 new features

FEATURE / Mergers & Acquisition

transactions, which has led to better diligence, but overall, the focus is on well-run businesses with strong earnings,” he says.

Good governance is an important aspect of any purchase, and Kaley says it’s a good indicator when evaluating an opportunity.

“From a governance perspective, if there are decent board minutes, active compliance committees, and the right things are happening each month, these are all great signs that there’s a good proactive culture. There’s not just a policy sitting on a shelf, there’s actually something happening in practice.”

THE ESSENTIAL ROLE OF THE BROKER

As a broker, there’s a significant amount of value that can be added when working with clients on mergers and acquisitions, with that role of trusted adviser seriously coming to the fore.

And, while clients may not immediately think of engaging their broker at the outset, the value-add is something to flag to all clients in order to remain front of mind.

“Brokers should be brought into the transaction as early as possible,” says Thomas.

“A trusted adviser can offer solutions that clients may not be aware of, and brokers have good relationships with insurers to discuss bespoke solutions with insurance markets apart from traditional solutions.”

And, with an increasingly competitive insurance landscape combined with the long-term nature of such projects, Lewis says it’s important to consider the future.

“Given the increased number of transaction liability insurers, brokers will need to select insurers who will be around in years to come and who have the financial strength to support future claims payments,” he says.

TECH CONSIDERATIONS