19 minute read

The Rise

The Adani group companies have seen a significant rise in their market capitalizations to the extent that, on an average, the listed firms have seen a growth of nearly 819% in the past three years This has been the biggest contributor not only to the rise of Gautam Adani's wealth but also to the firms being able to pledge these shares against huge loans from institutions for their capex

One of the major claims that the report makes is that the firms are not eligible to be listed on the market as the promoters, through various channels, own more than 75% of the shares in most of the listed firms of the group.

Advertisement

As per Securities Contract Regulation rule by SEBI 2010 promoters of listed Indian companies (other than PSU companies) can hold a maximum 75% of shares of the listed firm

This has been done through various shell entities across Mauritius, UAE, Cyprus, and similar tax havens

The Fall?

On the 24th of January, Hindenburg Research, a short seller, released a 100-page report The report's timing makes it more interesting as Adani was meant to open their 20,000 Cr FPO, making it the biggest FPO in Indian History.

These shells have been identified as owned by Vinod Adani and closed associates through which they have parked their shares in these entities and used them for stock manipulation , revenue and earnings manipulation, per the Hindenburg report.

Many of these firms, which are reported as public/Non-promoter shareholders Adani's listed firms, are funds established in these regions Some of these also have more than 95% of their portfolio in Adani companies

This is underscoring the fact that the Adani group's listed firms are not eligible to be listed as these are not to be considered as public, but promoter's ownership, therefore crossing the 75% limit in these firms set by SEBI.

% of Assets of these funds in Adani

These funds have already been under investigation by SEBI, and SEBI has said that they would add the details mentioned by Hindenburg in their ongoing investigation regarding the offshore funds and foreign portfolio investors of the group's listed companies The claims that make these funds non-public are such that Monterosa's chairman has served alongside a diamond fugitive merchant who is Vinod Adani's daughter's father-in-law, underlining that these are related parties and not public shareholders.

Similarly, a former trader of Elara told Hindenburg that the fund is structured so that the ultimate beneficiary of the shares is hidden, but Adani does control these shares These offshore entities have not only been used to manipulate prices through high volume trading to increase prices but also for revenue manipulation through fake export/import invoices and to launder money into the listed companies of Adani.

Suspected Flow of Funds

Funds from these offshore entities are given as loans to private firms of Adani, and are not reported Further these are sent to the listed firms and reported as loans from other group firms

This report not only invited more regulatory scrutiny into Adani group's companies but also led to turmoil in their share prices. In one week's time, the group lost nearly 108$ million in their Market capitalization.

This drastic fall was expected to affect its subscription, yet public offering was fully subscribed at the time When the issue was announced, the price set was at a discount compared to the market price , but due to the report and the turmoil their stocks witnessed, the stock closed half of the price they were to be issued in the FPO on the 2nd of February.

Subsequent to this, Gautam Adani announced that the firm would be withdrawing the FPO in the interest of their investors and would revisit their capital market strategy after a certain stabilization in the market

This also raised questions on the auditors of the group, which were the firm for the , Shah Dhandaria which has four partners and eleven employees and no working website

Over Leveraged

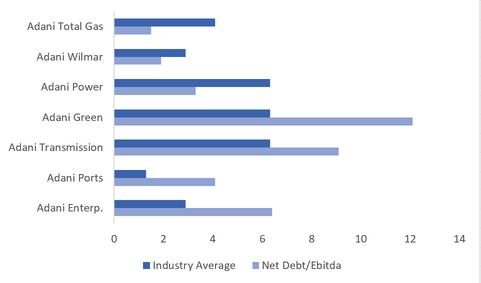

The report also claimed that even if the allegations posed are ignored, the stocks are highly overvalued, and these firms are over-leveraged alongside the promoter's shares being pledged for the same Such fundamentals pose an expected 85% downside risk to the stocks.

The Justification

The fact that these firms are overleveraged posed not only a risk to the group companies but led to a fall in the stocks of Banking stocks as these firms accounted for nearly 40% of the total group borrowings as per CLSA. This led to a fall in their stock prices even after excellent quarterly results and raised a lot of concern amongst investors regarding their exposure to Adani firms

On the 29th, the Adani group released a 413-page response to Hindenburg, stating, "This is not merely an unwarranted attack on any specific company but a calculated attack on India". They also stated that they were not contacted regarding any legal document for the same, and the allegations were baseless and devoid of facts. Furthermore it stated, "There are more than 27 statutory audit firms which audit various entities within Adani Enterprises These include a mix of big-four statutory auditors as well as statutory auditors who are highly reputed in their respective jurisdictions " They answered nearly 65 of the 88 questions from the report SBI had also announced that the bank's exposure to the group stands at 0.9% of their total loan book and is well below the exposure standards set by RBI for large Exposures. They also stated that these are backed by secure cash-generating assets. LIC, on the other hand, stated that they are sitting on significant gains from their investments in the Adani group and not looking to reduce their exposure to the group firms These assets account for 0 975% of their AUM, although they will be meeting to the top management of the group soon.

BOB, SBI and LIC were the leading decliners post the report was released Subsequently, RBI had asked all these lenders to provide a report with detailed statements regarding their exposure to the Adani group, along with SEBI increasing their surveillance of these stocks. 27,000

The worst is not over

Post the report was released, MSCI stated that they no longer consider a certain amount of stocks as free-float Hence the weightage assigned to the group companies could be reduced in the quarterly rejig of the index

This could lead to a further fall in the stock prices of the group companies as many Institutional investors like Blackrock and have nearly $1.6 Billion worth of shares in Adani firms based on the index as these firms invest in India based on these indeces. A further sell-off of these shares would be detrimental to the firm and its existing investors.

Along with these, leading rating firms such as S&P and Moody's changed their outlook on Adani to "negative" from "stable "

Along with this, the yields on the group's bonds have reached 30%, forcing it to cancel its plan to raise ₹1000 Cr through issue of public bonds.

As a consequence of this fall, Credit Suisse, Citibank are no longer accepting Adani bonds as collateral

Similarly, the pledged shares of Adani have fallen largely in their values and has applied more pressure on finances of the group in the form of a margin call to the extent of $500 Million This forced the Adanis to pay the whole loan altogether to avoid further downfall in the values of these stocks and not to trigger even larger margin calls.

The Way Ahead

Adani, claimed that the withdrawal of the FPO would not have an impact on the existing operations of the group, and they would continue to focus on timely execution and delivery of the projects He also stated that the fundamentals and assets of the firm are robust and will focus on long-term value creation and growth

Aswath Damodaran gave Adani Enterprises a fair value of ₹947 with very favorable assumptions for the firm ignoring the allegations made by Hindenburg in their report. He also supported the group's high leverage, stating that such infrastructural firms are known to be high on debt

The report and controversy have sparked a lot of interest in the markets The Adani group can navigate through this mess with solid documentation and proof But what is certain is that this will be a long-winded affair, and much remains to be explored.

Mr. Siddharth Borkar

India M&A lead

Orkla and MTR Group

Could you please share how your decade-plus journey across various finance functions and work cultures has been? Please share your experiences on numerous challenges you might have faced, which young aspirants like us can imbibe and learn from.

My decade-plus journey across various finance functions has covered audit tax valuation and M&A in various-sized organisations, and it has been extremely enriching. In my journey, I had the privilege of working with startups and MSMEs to large MNCs, each of which has only helped sharpen the experience Work culture varies not only from country to country but also from company to company I was fortunate enough to develop some very strong relationships across the spectrum that helped me progress, which I deeply cherish. Consulting and M&A jobs are very high-pressure jobs because a top-quality output is expected from us in the shortest possible time. This is where one should learn to remain calm under pressure, enjoy what one is doing, at the same time, not ignore health at any cost. While it is important to pay attention to details, but it is also important that one doesn't forget the big picture All jobs involve challenges, especially when one is new. And that is when one should pay even more attention to details, build relationships, and be extremely receptive to ideas, opinions, and views without bias Given the pace of change and the world we're living in, I think it's important to learn and update our knowledge constantly

With retail inflation hitting a 3month high, projections about rural demand revival have come into question. How do you think the FMCG sector will perform in FY24?

Inflation continues to be a weak spot in India's consumption story, with volume growth remaining a challenge, especially in the first half of FY 24. Volume growth has been subdued because of rising inflation and sluggish rural demand. Rural demand accounts for almost 40% of overall FMCG demand. Looking at the brighter side, I think, as far as the inflationary scenario is concerned, the worst is past us. We should see a gradual consumption improvement in the second half of this year. In my view, high MSP, normal monsoon and good harvest should push rural demand Brands that stay relevant to the consumer and deliver products that add value will always have an edge In addition to top-line growth, balancing the margin will be critical for FMCG companies Packaged foods and ready-to-eat segments will drive both in FY 24, given the shift from unorganised to organised segments, coupled with digitization initiatives. All in all, I think in FY 24, we are headed for some strong urban growth though sluggish rural growth will remain a concern

The Auto sector saw a tepid performance in December due to the base effect, weak export demand, and overall low growth in PV, 2-wheelers except for heavy commercial vehicles. What is your outlook for the Auto Sector in 2023?

The domestic auto industry saw a healthy revival in FY 23, which was aided by recovery in economic activity and increased mobility The demand sentiment for most automotive segments has remained healthy despite the lingering effects of semiconductor shortage and supply chain bottlenecks. However, the twowheeler industry continues to struggle with industry volume still below the pre-COVID levels. Even as improved demand in the recent festive months has provided some optimism, a sustained recovery in demand is yet to be seen

The adoption of electric vehicles has started and will only accelerate in 2023. Now, besides rising interest rates, the impact of a not-so-bright global economic situation are the factors that will keep the industry cautious And from a potential passenger vehicle buyer standpoint, I think in 2023, they may have to brace for some increase in vehicle prices from April 23, given that a lot of the OEMs will comply with stricter emission standards, thereby increasing the cost.

Given the challenges, such as FPI outflows, crude oil imports, and the fiscal deficit, do you expect the rupee-dollar rate to stabilize in the near future?

I think the Indian rupee emerged as Asia's worst-performing currency in 2022 against the US dollar due to outflows by foreign investors. Let's not forget that the dollar is a safe-haven asset, and global investors have flocked to it at times of uncertainty. The dollar has appreciated because of various reasons, given the RussiaUkraine conflict and the global slowdown in global inflation, leading to a surge in US bond yields. If the commodity prices remain in check, we may see some narrowing in the ballooning deficits, which are the current account deficit and the trade deficit I expect the rupee to trade in the range of 80 to 85 per dollar, with further weakness possible in the first half of the year, given the global inflation and economic concerns. But the green shot is that since India is expected to grow at a fast pace, possibly in the second half of 2023, there may be some positives for the rupee

What is so fast about the FMCG Sector?

FMCG is the 4th largest sector in the Indian economy. These companies are characterized by low cost and a low shelf life Since, by definition, they are highly perishable, they have a high inventory turnover and hence are “fast” off the shelf The range of FMCG varies from food items to toiletries to even over the counter drugs There must also be an understanding that since these items are for the average consumers, profits depend on volumes for firms. Apart from production distribution, and marketing, one of the main functions for FMCG firms is packaging. They try to innovate to make their products to make them attractive to the consumers, but not only that, packaging is important for shelf life and product integrity.

The Rural Angle

Currently the urban segment accounts for 66% of the FMCG sales in India Yet the rural segment forms one of the most importance piece of the revenue puzzle Rural disposable income is sensitive to harvests, retail and commodity inflation, government stimulus etc. These have a direct effect of volumes of sales So,in this segment, the firms tend to offer smaller packs in their portfolio to help bolster sales

Nielsen has predicted that the FMCG sector will touch $100 billion by 2025, and the rural segment is expected to drive this growth This resilience is evident as in the later quarters of 2021, firms, even after covid shocks, reported that sales had already surpassed pre-covid levels.So, firms maintain a bullish stance on this segment

E-commerce channels and Technology:

E-commerce channels have significantly boosted the FMCG sector as channels such as Flipkart and Amazon have offered customers convenience Combined with the fact that there has been technological advancements which has helped in sales and operational efficiency, the consumption economy is being effectively catered for Mergers & Acquisitions:The FMCG sector has received interest from domestic and foreign financial investors The primary reason is the race to cater to the growing consumption demand M&A deals hence are the backbone of this industry, with many players partnering up. Most recently, Reliance retail,HUL,Tata consumers group have been quite active in acquiring stakes in D2C brands, packaging companies and much more.

Government Push :The government has allowed up to 100% FDI investment in the single brand detail and up to 51% in the multi brand. Also the government’s PLI support in the food processing industry will help in creation of further production expansion will help cater the need to an expanding customer base.

Key Drivers Challenges

Retail and Commodity Inflation:

The FMCG sector receives much support from other industries, such as food, beverages, personal care items, oil, etc. The point is that due to inflation ,a price increase in the these commodities leads to the increase in input costs.Also, the consumer ’ s buying gets reduced, leading to low sales and volume growth This has been the main reason for pessimism in FMCG stocks in 2021 and 2022, resulting in a strong sell sentiment.

Direct to Consumers(D2C) models

competition: In Comparision to the traditional multi-layered FMCG models, the D2C model merges production, packaging distribution and marketing into a single entity Over the years, due to meteoric growth of home-grown D2C brands such as MamaEarth, and Sugar has forced a fundamental shift. This has led even giants such as Tata Consumers and HUL to launch their own D2C brands. However, D2C brands pose a credible threat to this sector

Key Metrics

Royalty Payments to Turnover: As a part of domesticating the brands, firms borrow creative licenses from parent companies to operate In turn, the firms pay royalty fees to these companies as a percent of turnover

ROCE is defined as EBIT divided by net capital employed (Debt + Equity), which signifies how efficiently the firm utilizes capital to generate profits.

P/E ratio: It is the ratio of Market Price per share to Earnings per share of the stock.

Introduction

“You can learn a lot, you know, just by going out and using some shoe leather.”

Scuttlebutt investing is an innovative and increasingly popular form that relies on informal conversations, or "grapevines," to identify investment opportunities Unlike traditional forms of investing, which rely on publicly available information, scuttlebutt investing relies on private, often hard-tofind information which is often not available to the general public. Scuttlebutt investing, also known as "gossip investing," is a method of making investment decisions based on information that is not widely known to the public, such as rumors or insider information The term "scuttlebutt" comes from the nautical term for a water cooler or gathering spot where sailors would exchange information and gossip The practice of scuttlebutt investing is controversial, as it can be illegal to make investment decisions based on insider information. The Securities and Exchange Commission (SEC) has strict rules in place to prevent insider trading, which is defined as buying or selling securities based on material, nonpublic information. Insider trading is illegal because it gives an unfair advantage to those who have access to this information and can harm other investors who do not have access to the same information One example of scuttlebutt investing might be a venture capitalist who hears about a promising startup from a friend in the industry, and decides to invest in the company before it becomes publicly known. Another example might be a hedge fund manager who receives inside information about a company through a personal connection, and uses that information to make a profitable trade

Benefits of Scuttlebutt Investing

Scuttlebutt investing offers several benefits over traditional methods of investing. The first is that it can provide access to information that may not otherwise be available. By talking to people close to the company being considered for investment, investors can gain insights that they may not be able to find through typical research methods.

Additionally, scuttlebutt investing can offer investors a way to get a better understanding of a company ’ s culture and how it is managed This can be incredibly helpful in determining whether or not an investment is a good choice Finally, scuttlebutt investing can also provide investors with early access to news about a particular company or industry before it is released to the public. This can give investors a competitive edge in making informed investment decisions However, there are some situations where scuttlebutt information can be used legally

For example, investors can use publicly available information, such as news articles or social media posts, to gather information about a company. Additionally, investors can also use their own personal connections and relationships to gather information about a company, as long as the information is not considered nonpublic. One of the main advantages of scuttlebutt investing is that it can provide investors with valuable information that is not widely known to the public This can give investors an edge over others relying solely on publicly available information Additionally, scuttlebutt information can also be used to confirm or refute information that is already available to the public. Unlike other forms of investing, scuttlebutt investing does not require a large amount of money to get started. It is the perfect choice for those who are just beginning to learn about investments or those who may not have the resources to invest large amounts of money. Additionally, scuttlebutt investing can be done without relying on any outside advice. This allows investors to make decisions based on their own research and knowledge

Another advantage of scuttlebutt investing is that it can help investors identify potential investments undervalued by the market. For example, suppose an investor hears a rumor that a company is about to release a new product or secure a significant contract In that case, they may invest before the news becomes public, allowing them to buy shares at a lower price.

Drawbacks of Scuttlebutt Investing

However, scuttlebutt investing also has its drawbacks One major disadvantage is that scuttlebutt information can be unreliable or inaccurate It's essential to verify the information before making an investment decision. Additionally, scuttlebutt information can be biased or influenced by personal interests, leading to poor investment decisions Moreover, using scuttlebutt information can be illegal, leading to penalties and fines. Another disadvantage of scuttlebutt investing is that gathering information can be timeconsuming and challenging. Investors need to be willing to invest time and resources into researching and verifying scuttlebutt information

Furthermore, scuttlebutt information is not widely available to everyone, which can create an uneven playing field for investors.

Incorporating Scuttlebutt Investing into your investment strategy

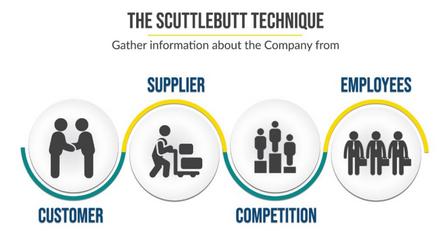

Identify valuable sources - The first step in scuttlebutt investing is identifying reliable sources. This can include feedback from customers and industry experts, as well as rumors from family and friends It’s essential to be aware of the sources you ’ re using and ensure the information is reliable. Analyze the data - After gathering the data, it’s essential to look for patterns and trends. Analyzing the data can help you decide which stocks to invest in and when Be aware of the risk - Scuttlebutt investing can be risky because it’s difficult to verify the accuracy of the information you receive. Before investing, make sure you do your research and understand the potential risks involved.

Diversify your portfolioScuttlebutt investing should be just one part of your overall investment strategy. Be sure to diversify your portfolio and invest in various stocks to reduce your risk.

By incorporating scuttlebutt investing into your strategy, we can get a leg up on the competition and make informed decisions regarding investing Just remember to be aware of the risk and continuously diversify your portfolio

Real life examples of scuttlebutt investing can be seen in the success stories of investors like

Warren Buffett and Philip Fisher. Warren Buffett is known for his extensive reading of annual reports and competitor analysis. He is a firm believer in the power of scuttlebutt investing and often cites it as a key to his success Similarly, Philip Fisher's investment classic ‘Common Stocks and Uncommon Profits’, which emphasizes the importance of scuttlebutt investing, has been credited with helping him become one of the most successful investors of all time.

Indian Landscape

The Indian landscape is becoming increasingly more investmentfriendly for scuttlebutt investing Scuttlebutt investing is a form of value investing based on information gathered through informal networking This form of investing takes cues from rumors, speculation, and “inside” information, allowing investors to make decisions based on the knowledge they have gathered.

In India, a rapidly expanding stock market, a young population with access to technology, and a competitive business environment have all resulted in a fertile ground for scuttlebutt investing. India’s stock market has been growing steadily since the 1990s, with the Nifty 50 index has risen by nearly 500% in the last ten years This is due to various reforms enacted by the Indian government, such as the liberalization of foreign direct investment and the promotion of efficient markets. In addition, India has a large population of young adults with access to the internet and technology. This allows them to stay informed about the stock market and make decisions based on the information they have gathered Furthermore, India’s competitive business environment and the presence of numerous start-ups have made the stock market even more attractive to investors. The presence of active day traders, frequent merger and acquisition transactions, and abundant liquidity make it easier for scuttlebutt investors to make their decisions

Overall, the Indian landscape has become more conducive for scuttlebutt investing With a large, young population with access to technology, a rapidly growing stock market, and a competitive business environment, investors can make decisions with the knowledge they have gathered through informal networking.

USA landscape

In the United States, scuttlebutt investing is against the law and is considered a form of market manipulation It is illegal for anyone to buy or sell securities based on material, nonpublic information. This type of trading can cause disruptions in the market and distort prices.

The Securities and Exchange Commission (SEC) is responsible for enforcing laws and regulations related to insider trading in the US Insider trading is buying or selling securities while possessing material, non-public information

If a person is found guilty of insider trading, they may be subject to fines, penalties, and even prison time The SEC can investigate and bring enforcement actions against individuals or firms that engage in insider trading It's important to note that scuttlebutt investing is legal as long as it does not rely on nonpublic information. Investors can use personal networks to gather information about companies and industries, but the information must be verified and publicly available to make an investment decision.

In conclusion, scuttlebutt investing can be a valuable tool for investors, but it also has drawbacks It's essential to be aware of the legal and ethical considerations of using scuttlebutt information and verify it before making an investment decision. Additionally, investors need to be willing to invest time and resources into researching and verifying scuttlebutt information. Overall, scuttlebutt investing can be a valuable addition to an investment strategy, but it should be used in conjunction with other forms of research and analysis

Multiplex operators PVR and INOX received approval for their merger from the Mumbai bench of the National Company Law Tribunal (NCLT) on Thursday, 12th January 2023. After this approval, the PVR share closed 2.7% higher. The merged entity is to be called PVRINOX Post the merger, it wi became the largest film exhibition company in India It had 1546 operating screens in 341 properties in 109 cities as on March 2022 After the merger, the combine planned to open 200 new screens every year under the Brand name PVR-INOX rather than refurbishing old properties. A CAPEX of Rs. 500 crore was to be pumped into setting up the new screens.

Details of the merger

Post the merger, the combine will command a 50% market share among the multiplex market and an overall 16%, including the single screens Regarding shareholding in the merged entity, the INOX promotors will hold 16 66%, while the founders of PVR will hold a 10 62% share Mr Pavan

Kumar Jain will act as the NonExecutive Chairman of the merged entity, while PVR Chairman and MD, Mr Ajay Bijli, will be the Managing Director Mr Sanjeev Kumar Bijli will be the Executive Director, and Mr Siddharth Jain will be the Non-Executive, NonIndependent Director in the combined entity The PVR-INOX combine is also expected to enter into film production and ramp up its distribution and food & beverages business as a way to diversify revenue. 17th February 2023 will be the record date that PVR will use to determine the eligibility of shareholders of INOX Leisure to whom equity shares will be allotted INOX shareholders will get three shares of PVR for every ten shares held