2. TunisianEconomy:TrendsandDevelopments

TheTunisianeconomyisfacingmajorsocioeconomicdifficulties.Growingtwindeficits,slowingeconomicgrowth,depreciationoftheTunisiandinarandpersistentlyhighunemployment andinflationrateshavecharacterisedtheeconomyoverthepastdecades(Nuciforaetal., 2014).Thesestructuralweaknessesarelikelytolimitthecountry’sadaptivecapacityand increaseitseconomicvulnerabilitytoclimatechangeinthemediumandlongterm.

Sincethe2011revolution,Tunisiahasexperiencedparticularlyfragileeconomicconditions duetopoliticalandsocialinstability,whichhasledtoanunfavourablebusinessclimate forinvestmentandhamperedeconomicgrowth.RealGDPgrowthhasslowedsignificantly overthisperiodcomparedwiththepreviousdecade,fromanaverageannualrateof4.6% between2001and2010to1.4%between2011and2019,mainlyduetotheslowdownindomestic andforeignprivateinvestmentandthedeclineinexportdynamism.

Thedeteriorationininternationalfinancialconditions,combinedwiththestructuralweaknessesoftheeconomy,haslargelycontributedtotheworseningofthecountry’sinternaland externalmacroeconomicimbalances.Thetradeandbudgetdeficitshaverisentohistorically highlevels,leadingtogrowingimbalancesinthecurrentaccount,publicfinances,andthe foreignexchangemarket.

Table1:Macroeconomicindicators,source:NationalInstituteofStatistics,CentralBankof Tunisia,andauthors’computations.

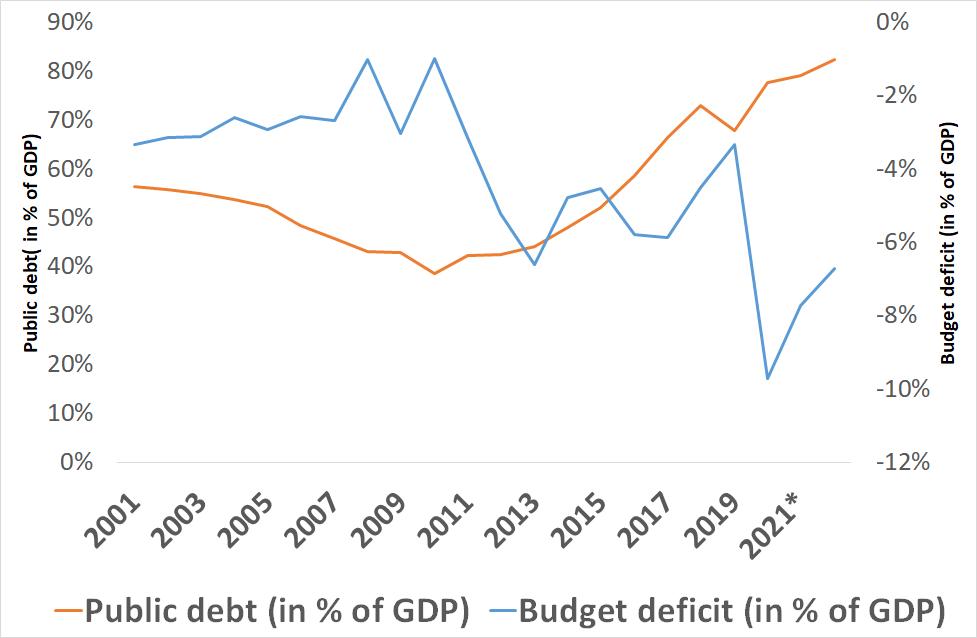

Whileweakeconomicgrowthhasallowedonlymarginalgrowthingeneralgovernment resources,publicexpenditurehasrisensharplyduetoincreasesinthepublicwagebilland highersubsidiestokeepfoodandenergypricesincheckinanenvironmentofhighglobal inflationofimportedcommoditiessuchasoilandcereals.Thebudgetdeficithaswidened

Averageannualgrowthrate GDP 4.61.6 8.64.3 Agriculturesector 1 94 60 2 2 5 ProcessedFoodsector 2 72 40 7 3 5 Sector’scontributiontoGDP Agriculturesector 8 78 89 410 3 ProcessedFoodsector 3 53 33 43 7 TradeBalance(%ofGDP) 10 915 616 911 5 FoodBalance(%ofTradeBalance) 7 57 312 912 Investment(%ofGDP) 24 121 119 415 8 TotalExternalDebt(%ofGDP) 39 546 261 956 3 FXreserves(monthsofimports) 6 23 75 44 4 Inflationrate(%) 4 155 65 7 Foodinflation(%) 45 64 37 6 Unemploymentrate(%) 1315 11817 9 Budgetdeficit(%ofGDP) 2 55 19 76 6 PublicDebt(%ofGDP) 49 156 278 079 5 NIIP(%ofGDP) 93 6 153 2 163 9 160 6

Indicator2001-20102011-201920202021

4

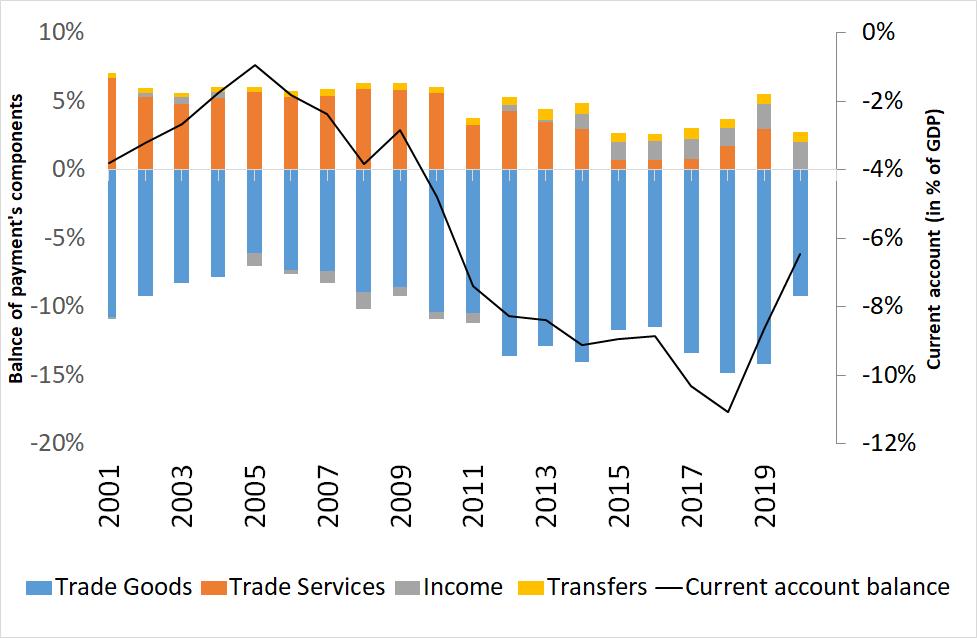

rapidlyrisingfrom3.6%in2011to9.7%in2020duringtheCovid19pandemic,seefigure1a.Asa result,publicdebtincreasedsignificantly,reachingover80%ofGDPin2020,mainlydrivenby asharpriseinpublicexternaldebt,whichexceeded50%ofGDPin2020.

Inaddition,thesharpriseinthetradedeficit,mainlyduetothelargedeficitinenergytrade, persistentfooddeficits,andthedeclineintheservicessurplusduetoasharpfallintourism activity,hasledtoawideningofthecurrentaccountdeficit,whichincreasedasapercentage ofGDPfrom-4.8%in2010to-11%in2018,seefigure1b.Before2010,thecountryreliedmainly onFDIinflowstofinanceitscurrentaccountdeficit.Aftertherevolution,FDIdeclinedfrom3.5% ofGDPin2009to1.9%ofGDPin2019.Thus,thelargeandpersistentcurrentaccountdeficit wasonlypartiallycoveredbyFDIandthegovernmentresortedtoexternalborrowing,leading toanaccumulationofexternaldebtandaworseningofcountryrisk(IMF,2019).

Indeed,astheoverallfinancingneedsoftheeconomyhavesteadilyincreased,andthe contributionofthebankingsystemandhouseholdsavingstothisfinancinghasremained limited,externalborrowinghasenabledthefinancingofprivateandpublicdeficitsoverthe lastdecade.Despitelargeinflowsofremittances,whichhaveaveraged4%ofGDPoverthe lastdecade,externaldebtservicingandlargedividendpaymentsbythecorporateand bankingsectorstotherestoftheworldhaveabsorbedallexternalfinancing.Asaresult, netinternationalreserveshavedeclinedsignificantly,fallingtoonly84daysofimportsin 2018.

Duetolowhouseholdincomeandhencelowsavings,depositgrowth,themainsourceofbank financing,didnotfollowloangrowthandthebankingsectorhadtoresorttolargeamounts ofcentralbankfinancing.Liquidityinthesectorremainedbelowinternationalstandards,with liquidassetsnotexceeding20%oftotalassets.Profitabilitywasalsolow,withthereturnon equityaveraging10%between2008and2018,andthenon-performingloanratiowasvery high,averagingat13.3%in2018.(CentralBankofTunisia,2019).

(a)Budgetdeficitandpublicdebt,source:Ministryof Financesandauthors’computations.

(b)Balanceofpayment,source:CentralBankofTunisia andauthors’computations.

Figure1:FiscalBalancesandBalanceofPayments;Source:INS

(a)Budgetdeficitandpublicdebt,source:Ministryof Financesandauthors’computations.

(b)Balanceofpayment,source:CentralBankofTunisia andauthors’computations.

Figure1:FiscalBalancesandBalanceofPayments;Source:INS

5

3. ClimatechangeinTunisia

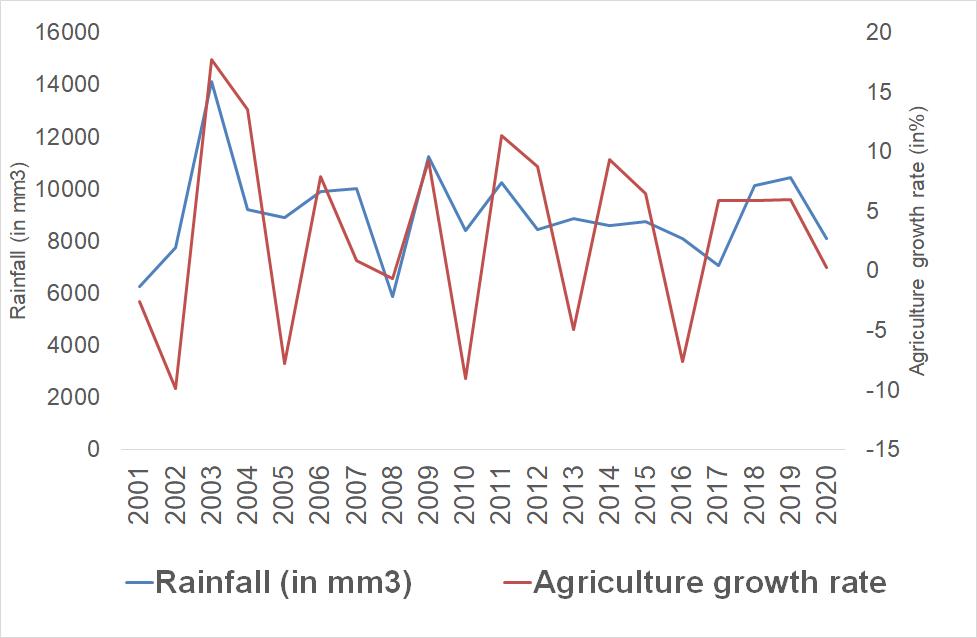

Characterisedbyanaridtosemi-aridclimateover80%ofitsterritory,Tunisiahasapermanent waterdeficitandremainsthe30thmostwater-stressedcountryintheworld(WRI, 2020). Overthepastdecade,thecountryhasexperiencedtwoperiodsofseveredroughtin2013 and2015-2017,withasignificantriseintemperature,followedbyperiodsofrecurrentheat waves,aswellasfiresandfloods,whichhavemultipliedinrecentyears.Theagricultural sectorisessentiallybasedonrain-fedproduction,whichaccountsformorethan90%of thecultivatedareaand65%ofagriculturalvalueadded.Itisthereforehighlydependent onclimaticvariations(Chebbietal.,2019),asshownbythestrongcorrelationbetweenthe growthrateofagriculturalvalueaddedandrainfallinFigure2b

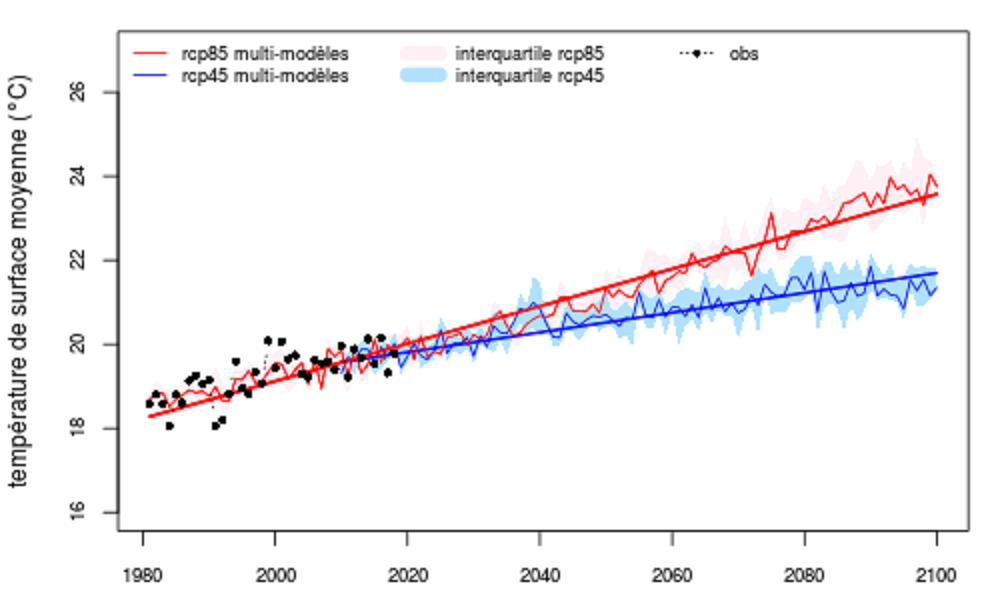

(a)AveragetemperatureunderRCP4.5andRCP8.5scenarios.Source:NationalInstituteofMeteorology(Climat-c, 2020)

(b)AgricultureValueAddedandrainfall.

Figure2:RecentclimaticconditionsinTunisia;Source:TunisiaNationalInstituteofMeteorology, NationalInstituteofStatisticsandauthor’scomputations.

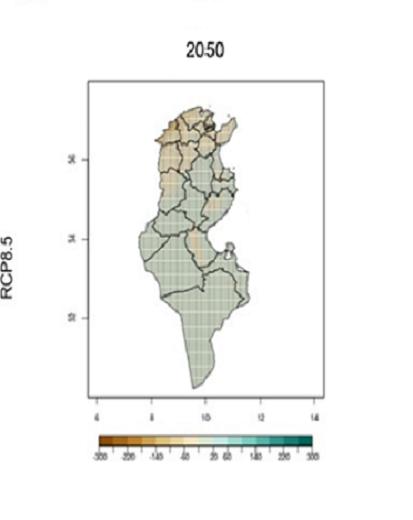

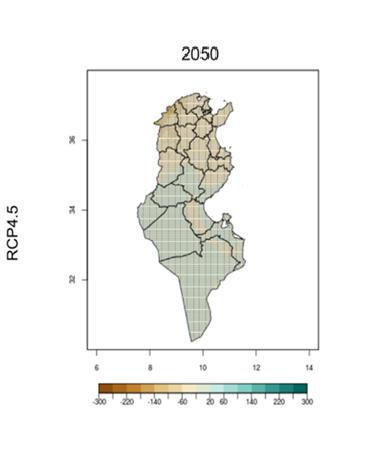

TheupdatedprojectionsoftheNationalInstituteofMeteorologyin20201 indicateatemperatureincreaseofupto1.8°Cby2050forRCP4.52 andupto3°Cby2100.Tunisia’sinlandregions willexperienceatemperatureincreasecomparedtothecoastalregions.ForRCP8.5,this temperatureincreasewillbeevenmoreacute,reachingthevaluesof2.3°Cand5.2°Cforthe 2050and2100horizons,respectively.Underthusclimateforcing,thearidinlandregionswill experiencemajorheatwaves,threateningalreadyfragileagro-systems.

Withregardtoprecipitation,theclimateprojectionsoftheNationalInstituteofMeteorology showasignificantdecreaseinprecipitationunderthetwoscenarios,withadecreaseof between14and22mmin2050undertheRCP8.5andRCP4.5scenariosrespectively,i.e. alossof-6%and-9%comparedtotheaverageprecipitationobservedovertheperiod 1981-2010.

1Onthebasisof14regionalclimatemodelswithaspatialresolutionofupto12.5km,theNationalInstituteof Meteorologyisassessingtheimpactoffutureclimatechangeontemperatureandprecipitationfortwohorizons, 2050and2100,comparedtothe1961-1990averageunderRCP8.5andRCP4.5,presentedinFigures3aand3b 2InitsFifthAssessmentReport,theIntergovernmentalPanelonClimateChange(IPCC)presentedthemodelling ofgreenhousegasesthroughRepresentativeConcentrationPathway(RCP)scenariosthatincludeapessimistic scenarioRCP8.5,twointermediatescenarios(RCP4.5withastabilizationofemissionsbefore2100atalowleveland RCP6.0withastabilizationofemissionsbefore2100atamediumlevel),andanoptimisticscenarioRCP2.6(IPCC, 2014).

6

Theclimatescenariosalsopredictasignificantincreaseinclimateextremes,indicatinga longerdurationofheatwavesandahighfrequencyofdroughtsandfloods.Indeed,Tunisia wouldexperienceanincreaseinthenumberofconsecutivemaximumdrydaysonaverage of9.3daysperyearaccordingtoRCP4.5and17.1daysperyearaccordingtoRCP8.5scenario, i.e.anincreaseof11%and19%respectivelycomparedtotheaveragerecordedovertheperiod 1981-2010.

4. Agriculturalproductionandclimatechange

Withthepredictedincreaseintemperatureanddecreaseinrainfall,thelossofagricultural productioninTunisiaislikelytoworseninthecomingdecades.Tunisianagriculturehas alreadyexperiencedtheseverenegativeimpactsofclimatechangeincertainpartsofthe country.Risingsealevelsduetoclimatechangehaveincreasedcoastalerosionandsalinity contaminationofcoastalaquifers(Brahmietal., 2018).Thesecoastalaquifersareused byfarmersforirrigation,whichhasledtothesalinisationofseveralirrigationperimetersin Tunisiaandtheirpermanentloss.Forexample,accordingtoIssametal.(2022),theaquifer ofthecoastaltownofDyiar-Al-HujjejinCapbonhasexperiencedseawaterintrusion.The salinisationoftheaquiferreachedaveryhighelectricalconductivityof15dS/minthe1990s, causingmanylocalfarmerstoabandontheirplotsandwells.Inaddition,salinityhasreduced plantgrowthandwaterquality,resultinginlowercropyieldsandreducedwaterreservesin

(a)PrecipitationsunderRCP4.5scenario (b)PrecipitationsunderRCP8.5scenario

ofMeteorology

Figure3:PrecipitationProjectionsUnderRCP4.5andRCP8.5;Source:TunisiaNationalInstitute

7

livestock.

Asincoastalareas,thevulnerabilityoflandintheinteriorofthecountry,whichisclassifiedas semi-arid/arid,iscompoundedbyadverseclimaticconditionsandunsustainableagricultural practices.InTozeur,wherethelargestoasisfarmingsystemislocated,datecropsareatrisk, sufferingthefullimpactofclimatevariabilityandpoorsurfaceirrigation(Dhaouadietal., 2017).Muchofthelandoccupiedbysmallholdersisonlow-fertilityland,whereinappropriate agriculturalpracticeshaveledtosoilerosionandlossofbiodiversity.Irrigationwithhighly salinewaterhasledtothedegradationoreventotalsterilisationofasignificantproportionof Tunisiansoils(KhawlaandMohamed,2020).Indeed,inTunisia,irrigationwateristhemain sourceofsalinisationinirrigatedareas(Louatietal.,2018).

FutureclimatechangeisexpectedtoraisesealevelsalongtheTunisiancoastlineby30to 50cm,leadingtolossofarablelandandacceleratedsalinisationofgroundwaterincoastal areas.Inaddition,soildegradation,increasedheatwavesanddroughts,andreducedrainfall willleadtoageneraldeclineinyieldsandcultivatedareas,resultinginlossesinagricultural production.

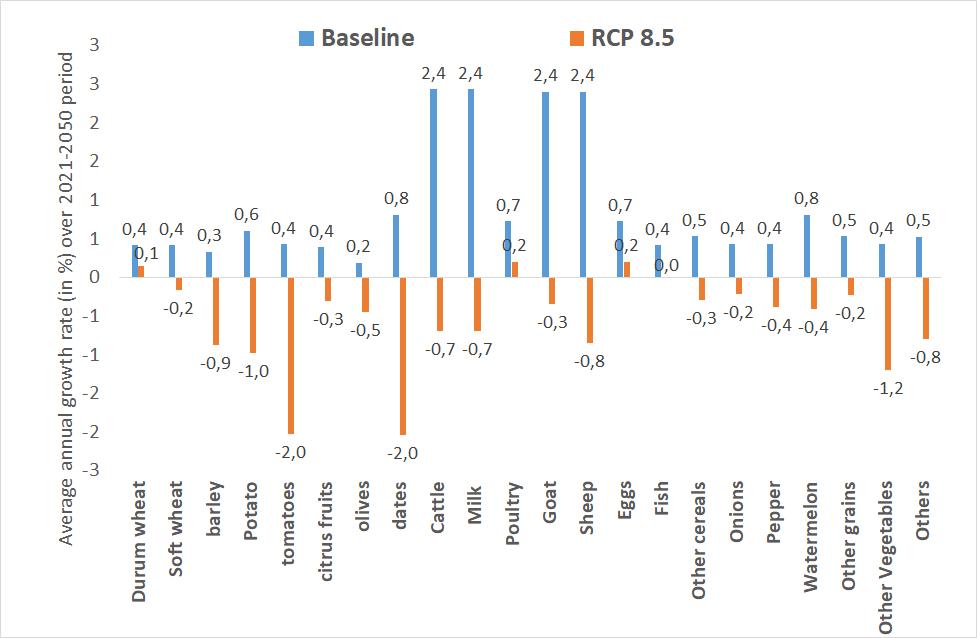

InordertoanalysetheimpactofdecliningagriculturalproductionontheTunisianeconomy, wefirstconstructproductionprojectionsintonnesfortwenty-twodifferentagriculturalcrops underBusinessAsUsual(BAU)andtheRCP8.5scenarioforthe2022-2050timehorizon. Ourcropbasketcoversallagriculturalproduction.InourBAUscenario,weuseprojections fromtheFAO’sGlobalAgro-ecologicalZones(GAZ)model(Fischeretal., 2021)toproject productionlevels.3 Forthemaincerealcrops(durumwheat,softwheatandbarley)andolives, wequantifytheimpactofclimatechangeonharvestedareasandcorrespondingyieldsunder theRCP8.5scenariothroughprojectionsdevelopedundertheAdapt’Actionproject,with theparticipationoftheTunisianMinistryofAgricultureandtheFrenchDevelopmentAgency (Deandreisetal., 2021).FortheremainingcropsnotcoveredbytheAdapt’Actionproject (dates,citrusfruits,tomatoes,potatoes,onions,peppers,livestock,milk,eggs,watermelon, othercerealsandothervegetables&fruits),weuseprojectionsbythe Foodandofthe UnitedNations(2018)undertheStratifiedSocietiesScenario(SSS).

Figure4ashowstheaveragesmoothedgrowthratesofyields(intonnes)ofourcropbasket fortheBAUandRCP8.5scenarios.Asexpected,projectionsundertheRCP8.5scenarioshow significantlossesforthemaincropsgrowninTunisia.Amongcereals,barleyandsoftwheat productionin2050areprojectedtodecreasebyrespectively0.9%and0.2%peryear,while durumwheatisprojectedtoincreasebyonly0.1%over2022-2050period.

Themainexportcommodities,i.e.datesandolives,willalsobeseverelyaffectedbyfurther increasesingroundwatersalinityindeepaquifersinsouthernregions,fordates,andbyloss ofrainfallandincreasedtemperaturesforolives.Accordingtoprojections,datesproduction willdeclineby2%peryearuntil2050,whileoliveproductionwilldeclineby0.5%.Livestock production(cattle,goat,sheep)willalsofallasfeedlossesincrease,leadingalsotolowermilk productionby2050.Thegrowthrateofpoultryproductionwillslowdowntoonly0.2%,which willalsobetherateofgrowthofeggproduction.AccordingtoMedECC(2021),astructural shiftinfisheryresourcesisexpected,withanincreaseinthermophilic,exoticspeciesanda

3Morespecifically,forourBAUscenario,weuseagriculturalproductionprojectionsreportedinthe’ClimateShifter’ socio-economicpathwayprovidedbyFAO,whichcorrespondstotheRCP6.0climatescenario

8

(a)Cropsaverageannualgrowthrateover2021-2050 forBAUandRCP8.5scenarios.Source: Deandreisetal. (2021);FoodandAgricultureOrganizationoftheUnited Nations(2018)andauthors’computations

(b)Demandcomponentsofdomesticagricultureproduction(involume)underBAUandRCP8.5scenarios.Source: Deandreisetal.(2021);FoodandAgricultureOrganization oftheUnitedNations(2018)andauthors’computations

Figure4:AgriculturalProductionProjections.Source:Author’scalculations

simultaneousdecreaseincurrent,coldaffinityspecies.Soweassumethatfishproduction remainsstableandfixtoits2021value.Insummary,thetotalagriculturalproduction(in addedtonnes)sectorwilldeclinebyanaverageof0.5%peryear.

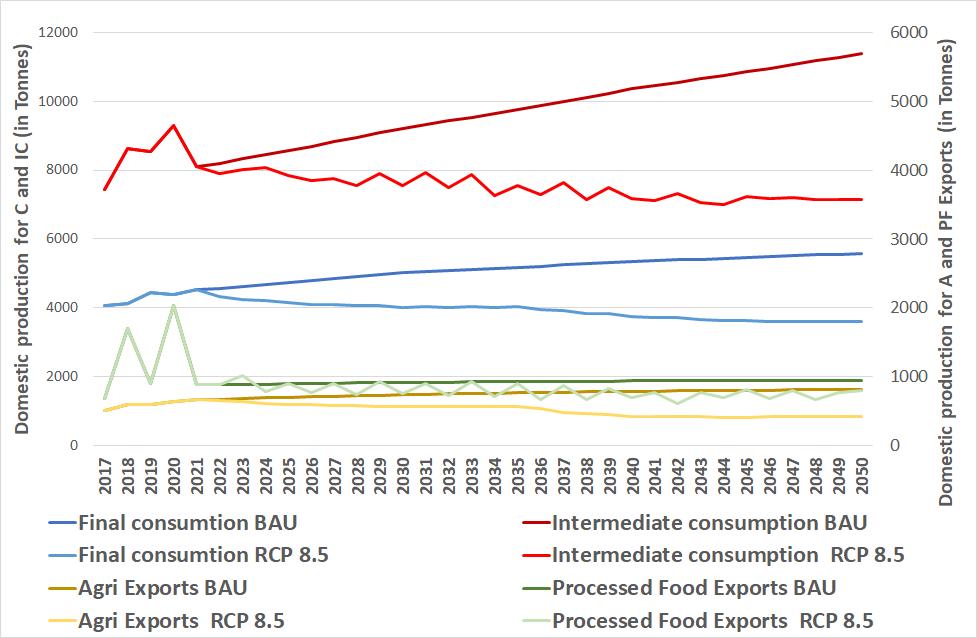

Inordertousethesevolumeprojectionsinoureconomicmodel,weclassifycropsaccordingto theiruse,usinginformationfromthe2015product-levelsupply-usetable(SUT)foragricultural commodities.Morespecifically,weallocatethesupplyofeachcropintonnestosatisfy threecategoriesofdemand:householdconsumption,intermediateconsumptionbyagroindustry/othersectors,andexports.Wethenuse2017pricesforeachcroptocalculate thevalueofoutputforconsumption,intermediateconsumptionandexportsinconstant prices.

Figure4bshowstheevolutionoftheproductionofagriculturalconsumergoods,intermediate consumptiongoods,andagriculturalandprocessedfoodexportsinconstantpricesunder theBAUandRCP8.5scenarios.5 Allfourproductioncategoriesshowcontinuousandsustained declinesuntil2050.Withagrowingpopulationandincreasingdemandforfood,thisdecline inproductionwillleadtoincreasedfoodimportstomeetdomesticdemand,increased ruralunemploymentandpossiblymigrationtourbanareas.Combinedwiththedecline inagriculturalandagro-industrialexports,Tunisiafacesasignificantlossofvitalforeign exchange,especiallyifglobalfoodpriceinflationishighinthecomingdecades.Inthenext section,wediscussthemainaspectsofalarge-scale,empiricalstock-flow-consistentsystem dynamicsmodeloftheTunisianeconomytocapturetheimplicationsofthesedevelopments forTunisia’smacrodynamicperformance.

4Asdiscussedinthenextsection,exportsofagro-industrialgoodsdependsolelyonprojectedoliveandfish production.Fromtheseprojectionsanexogenousexportpathfortheprocessedfoodisconstructed.

5Notethatthefigureusesactualproductiondatauntil2021andprojectionsfrom2022onwards.Theincreasein theproductionofintermediateagriculturalgoodsbetween2018and2020ismainlyduetohigholiveproductionin 2018and2020andhighdurumwheatproductionin2019.However,thesetrendsarenotmaintainedin2021and2022, whendroughtandheatwaveshaveastrongnegativeimpactonyields

4 .

9

5. Themodel

TheGEMMES-Tunisia6 modeldescribestheevolutionoftheTunisianmacroeconomyunder differentclimatechangeandclimateadaptationscenarios.Thetechnicaldescriptionofthe modelwithdetailedequations,informationonthedata,calibrationandsimulationstrategies canbefoundintheAppendix.ThestructureofthemodeliscapturedbytheTransactionFlow Matrix(TFM,Table2)andtheBalanceSheetMatrix(Table3),whichshowthebalancesheet structureofeachsector,andthetransactionsthattakeplaceintheeconomybetweenthe institutionalsectorsrespectively.NotethattheTFMalsorecordsthenetsavingpositionsand thecorrespondingchangesinthefinancialandrealstocksofthemodel.Assetsandinflows areindicatedbya(+)andliabilitiesandoutflowsbya(-).

Themodelhassixinstitutionalsectors:Firms,Households,Banks,Government,CentralBank andtheRestoftheWorld.Thefirmssectorisfurthersubdividedintotheagriculturalsector andthenon-financialcorporations(NFC)sector.Therearefivetypesofcommodities.Three differentagriculturalproductsforhouseholdconsumption,intermediateconsumptionand exportsrespectively,producedbytheagriculturalsector;aprocessedfoodproductproduced bytheNFCsector,whichisusedforintermediateandfinalconsumption,andanon-food productalsoproducedbytheNFCsector,whichisusedforinvestment,intermediateandfinal consumption.Inthiscontext,particularattentionispaidtothemacro-financialconditions affectingproductionandthedevelopmentofinternalandexternalimbalances,including foodandconsumerinflation,unemployment,theaccumulationofprivateandpublicdebt, thedeteriorationofcountryrisk,externaldeficitsandtheaccumulationofforeigndebt,and theassociatedfinancialacceleratoreffectsthatfeedbackintospendingdecisionsinall sectors.

5.1. Firms

5.1.1. Output,ExpensesandResources

Domesticagriculturalproductionforfinalconsumptiondemand,intermediateconsumption andexportsisgivenbytheprojectedclimateconditionsasdescribedintheprevioussection, andisexogenoustothemodel.Aggregatedomesticdemandforagricultureiscomposedof finalconsumptionandintermediateconsumption.Anyexcessdomesticdemandiscovered byimportstoclearthemarket.Theagriculturalsectorconsumesasintermediateinputs agriculturalgoods,processedfoodgoodsandNFCgoods,infixedproportionsofitstotal production.Similarly,thesectoruseslabourandcapitalinfixedproportions.Employment isdeterminedbytotalproductionandtheconstanttrendinlabourproductivity.The agriculturalsectorismostlyhousehold-ownedandthereforeitgeneratesmixedincomefrom itsproductionactivities,afteraccountingforallthetaxesinproduction,socialcontributions andsubsidies.Giventheexogenousgrowthofproduction,itisassumedthatthesector operatesatafixedcapitaltooutputratio,andinvestmentisalwayscarriedouttoensure thatthecapitalstockissufficientforthegivenproductionpath.Netprofitsaredefinedbythe 6

GEMMESstandsforGeneralMonetaryandMultisectorialMacrodynamicsfortheEcologicalShift.

10

mixedincomeofthesectorfromwhichinterestpaymentsonserviceableloans,insuranceand commissionspaidtothebankingsectorandincometaxestothegovernmentarededucted. Aproportionofnetprofitisretainedtofinanceinvestmentandremainingfinancingneeds arecoveredbynewborrowingfromthebankingsectorindomesticcurrency.

TheNFCsectorproducestwogoods,processedfoodandannon-foodgood,withtwodistinct productionprocesses.Domesticproductionoftheprocessed-foodgoodisdemandedfor finalandintermediateconsumption,andexports.Thenon-foodgoodisfurtherdemanded forinvestmentbyfirmsandhouseholds.Aswithagriculturalproduction,intermediate consumptionfunctionsaregivenbythetechnicalcoefficientsandthelevelofproduction forbothgoods.Thesectoruseslabourandcapitalinfixedproportions,andemploymentis determinedbytotaloutputandlabourproductivity.Duetothedependenceoftheprocessed foodproductiontoagriculturalintermediateinputs,wefurtherassumethatprocessedfood exportsdependonclimaticconditionsandareexogenoustothemodel.Importsofprocessed fooddependontimevaryingimportpropensitiesoutofreallevelsoffinalandintermediate consumption.Theimportpropensitiesgraduallyadjusttotheirtargetlevels,whichdependon relativeprices(takingintoaccountimporttaxes)andrelativeproductivitybetweenTunisia andtherestoftheworld,withdifferentelasticities.

Domesticproductionofthenon-foodgoodissoldforfinalandintermediateconsumption, investmentandexports.Asintheothersectors,fixedproportionsofintermediateinputs,labour andcapitalisassumed.Importsofnon-foodgoodsaredeterminedbydomesticdemand forprivatefinalconsumption,intermediateconsumptionandinvestment,withendogenous importpropensities.Aswithprocessedfoodgoods,importpropensitiesareslow-movingand dependonrelativepricesandrelativeproductivitylevels.Exportsofnon-foodgoodsdepend onforeignGDPwithanendogenouspropensitytoexportthatdependsonrelativepricesand relativeproductivitylevels.

Theprocessedfoodanddurablegoodmarketsarecharacterisedbydisequilibria.Ateach pointintimeandforeachgood,totaldemandisnotnecessarilyequaltototalproduction. NFCfirmsformadaptiveexpectationsonrealexpecteddemandaroundthetrendgrowth ofprocessedfoodandthedurablegoodsales.Thistrendfollowspopulationgrowthrate forprocessedfoodandcapitalaccumulationfornon-foodgood.Excessdemandorsupply isclearedbyinventoryadjustmentsinbothmarkets.NFCfirmshaveadesiredinventory toexpectedsalesratiosforprocessedfoodandnon-foodgoods,whichdeterminedesired inventories.Therefore,totalproductionisbasednotonlyonexpecteddemand,butalsoto attaindesiredinventorylevels.

11

AgricultureNon-AgriculturalNFCHouseholdsBanksC.BankGovernmentRoW Σ CurrentCapitalCurrentCapital AgriculturalConsumption C A nom C A nom 0 ProcessedfoodCons. C PF nom C PF nom 0 NFCConsumption C NF nom C NF nom 0 AgriculturalMarginsMRG A + MRG A 0 Investment I NF A,nom + I NF nom I NF F,nom I NF H,nom I NF G,nom 0 Imports IM A N IM PF N IM NF N + IM nom 0 Exports + X A nom + X NF nom + X PF nom X nom 0 AgriculturalIntermediateConsumption + IC A PF,NF,G,nom IC A PF,NF,nom IC A G,nom 0 ProcessedFoodIntermediateConsumption IC PF A,nom + IC PF A,G,nom IC PF G,nom 0 NFCIntermediateConsumption IC NF A,nom + IC NF A,B,G,nom IC NF B,nom IC NF G,nom 0 Wages WB A WB F + WB WB B WB G 0 Employers’SocialContributions ESC A ESC F ESC B + ESC ESC G 0 ValueAddedTaxes VAT A VAT F + VAT 0 OtherTaxes Otaxes A Otaxes F + Otaxes 0 ImportTaxes TIM A TIM F + TIM 0 Subsidies + sub A + sub F sub 0 Taxesonproduction Tpr A Tpr F Tpr B + Tpr 0 GrossOperatingSurplusDistribution MI A GOS F H + MI A + GOS F H [0] InterestonDeposits + IntD F + IntD H IntD 0 InterestonDomesticLoans IntL A D IntL F D IntL H D + IntL D 0 InterestonNFCFXLoans IntL F B,FX + IntL F B,FX 0 InterestonDirectFXLoans IntL B D,FX IntL G D,FX + IntL D,FX 0 InterestonBonds + IntB H + IntB B + IntB CB IntB 0 Comissions Com A Com F Com H + Com 0 Insurance Ins A Ins F Ins H + Ins 0 InterestonAdvances IntA + IntA 0 Remittances + Rem Rem 0 CentralBankProfits F CB + F CB 0 TaxesonIncomeandProfits T A T F T H T B + T 0 SocialContributions WSC + WSC 0 SocialBenefits + GE GE 0 Transfers Transf F G + Transf G H Transf B G Transf CB G + Transf G Transf W G 0 BankDividends + Div B H Div B + Div B G + Div B W 0 NFCDividends Div F + Div F H + Div F G + Div F W 0 RetainedEarnings + RE A + RE F + RE B 0[ RE ] [Capital] [ K A ] [ K F ] [ K H ] [ K G ] [ K ] [Inventories] [ V F ] [ V F ] DomesticCurrencyDeposits + Dep F D + Dep H D Dep D + Dep W D 0 FXDeposits + Dep F FX e N + Dep H FX e N Dep FX e N + Dep W FX e N 0 GovDepositsattheCB Dep G,cur + Dep G,Cur 0 DomesticCurrencyLoans L A D L F D L H + L D 0 Bonds + B G H + B B G + B G CB B G 0 Advances Ad + Ad 0 ForeignDirectInvestment FDI F e N FDI B e N + FDI W e N 0 DomesticCurrencyReserves + R D R D 0 BanksFXReserves + R B FX e N R B FX e N 0 FXReserves + R FX e N R FX e N 0 IntermediateFXLoans L F FX e N + L F FX e N 0 RoWFXLoans L B FX e N L G,Tot FX e N + L FX e N 0 Σ0000000000 Table2:TransactionFlowMatrix 12

5.1.2. Pricedetermination

Theproductivesectorchargesarangeofdifferentprices.Themodeldistinguishesbetween producerpricesandusageprices,i.e.intermediateconsumption,finalconsumptionand investment,bythetypeofgood,i.e.agricultural,processed-foodandnon-foodgood.Itfurther distinguishescommodityspecificinternationalimportandexportprices.Firmssettarget producerpricesbasedonamarkupoverhistoricalunitcostsandgraduallyadjusttothese targets,witharelaxationspeedinverselyproportionaltonominalrigidity,capturingprice inertia.Then,thedifferentcompositeusagepricesfollowproducerprices,afterconsidering alltherelevanttaxes,subsidiesandmargins,andaccountingfortheimportsharesof intermediateandfinalconsumption,andthecorrespondingeffectsofworldpricesand thenominalexchangerate.Theagriculturalmarkupisfixed.Themarkupsonprocessedfood andnon-foodgoodsdependnegativelyonthedivergencebetweentheactualandadesired inventorytooutputratios.Thus,asunwantedinventoriesaccumulate,producersreducethe mark-ups(andviceversa).Notethatbyseparatelytrackingdownthedifferentprices,the modelcomputesfoodinflationandalsohouseholdCPIinflationthroughaCPIindex,which dependsontheconsumerpricesofeachproductandtheircorresponding,time-varying relativesharesintheconsumptionbundleofhouseholds.

5.1.3. FinancingInvestment

Asstatedabove,theagriculturalsector’sinvestmentisdeterminedbytheconstantcapital tooutputratioandtheexogenous,climatedependent,productiontrajectory.NFCfirms’ investmentdecisionsdependonsectoralprofitability,whichiscapturedbytherealrate ofprofit.Themodeltracksdownexplicitlytheformationofgrossoperatingsurplusfrom bothprocessedfoodandnon-foodgoodproductionprocesses,includingthegood-specific margins,subsidiesandtaxesonproduction7.Grossprofitsaredefinedafterconsideringthe interestreceivedontheirdeposits,interestpaidontheirserviceabledomesticandforeign currencyloans,insuranceandcommissionsthatfirmspaytothebankingsector.Netprofits istheresidualafterfirmspaycorporatetaxes.Netofinflation,netprofitsformtheprofitability ofthesector.Then,firmsdistributepartoftheprofittodomesticandforeigninvestorsas dividends.

7Inreality,partofproductiontakesplaceinhouseholdsandthereforehouseholdproducersalsogenerategross operatingsurplus.Themodelassumesthatallproductiontakesplaceinfirms.Inorderthentomatchempirically thenationalaccountsandespeciallythesectoralsavingpositions,aproportionofthegrossoperatingsurplusthatis generatedbyfirmsisdistributedtohouseholds,whichisthentaxedbythegovernmentalongsidetheirothersources ofincome.

VariableAgriNFCHouseholdsBanksCBGovernmentRoW + Capitalstock +KA +KF +KH +KG K Inventories +V F V F [Non-FinancialAssets] +NFAA +NFAF +NFAH +NFAB +NFACB +NFAG +NFAW NFA DomesticCurrencyDeposits +DepFD +DepH D DepD +DepW D 0 FXDeposits +DepFFX e N +DepHFX e N DepFX e N +DepWFX e N 0 GovernmentDepositsattheCB DepG,cur D +DepG,cur D 0 DomesticCurrencyLoans LA D LFD LH +LD 0 Bonds +BG H +BB G +BGCB BG 0 Advances Ad +Ad 0 ForeignEquity EQW F EQW B +EQW 0 DomesticCurrencyReserves RD RD 0 BanksFXReservesatCB +RBFX e N RBFX e N 0 FXReserves +RFX e N RFX e N 0 IntermediateFXLoans LFFX e N +LFFX e N 0 RoWFXLoans LBFX e N LG,Tot FX e N +LFX 0 Other OtherB +OtherB 0 [FinancialAssets] +FAF +FAH +FAB +FACB +FAG +FAW 0

Table3:BalanceSheetoftheTunisianEconomy.

13

Firmsfinanceinvestmentthroughretainedearningsandexternalfinance.Theyfurtherrequire fundingtokeepdepositsinbothdomesticandforeigncurrenciesforworkingcapital.Firms desiretofinanceaconstantproportionoftheirtotalfinancingneedsthroughFXdenominated loans.Themodelassumesthatcreditprovisioninforeigncurrencyisrationed,andonlya fractionofthedesiredcreditisprovidedbythebankingsectorinFX.Theremainingfinancing needsaresatisfiedthroughcreditprovisioninginthedomesticcurrency.

5.2. BankingSector

5.2.1. CreditRationingandInterestRates

Asmentionedabove,banksholdsavingandcurrentaccountdeposits,provideforeignand domesticcurrencyloans,provideinsurancetocompaniesandreceivecommissionsfortheir services.Theyalsoholdgovernmentbondsascollateral.Akeyvariabledeterminingthe availabilityofcreditandtheliquidityoftheFXloanmarketiscountryrisk.Indeed,boththe rationingofcreditvolumeandtheinterestrateschargedonFXloansdependoncountryrisk. Inturn,thecountryriskisaconvexfunctionofthecountry’sinternationalinvestmentposition (ignoringforeign-ownedequityofdomesticfirms),highlightingthesensitivityofsmallopen economiessuchasTunisiatotheperceivedsustainabilityoftheexternaldebtbyinternational investors.

Thecostofforeigncurrencydenominatedprivatedebtdependsonapremiumovertheworld interestrateandisaconvexfunctionofthecountryrisk.Thetargetinterestratethatbanks payondepositsisdeterminedbyamarkdownfromthepolicyratesetbythecentralbank. Themarkdown,inturn,dependsontheliquidityneedsofthebankingsector,andincreases asthebankingsector’sassetsideofthebalancesheetexpandsrelativetoliquidityneeds, capturedbythethebank’sassets-to-advancesratio.Inaddition,thedomestictargetlending ratedependsonthedomesticpremiumovertheaveragecostoffundingforbanks.The domesticpremiuminturndependsontheratioofdebttogrossoperatingsurplusofthe NFCsector.Iftheprivatedebtburdenishighrelativetotheprofitabilityofthesector’smain economicactivity,bankswillraisetheinterestratetocompensateforahigherperceivedrisk ofdefault.Forsimplicity,itisassumedthatthelendinginterestratechargedtohouseholdsis aconstantmarkupoverthelendingratechargedtofirms.Actualeffectiveratesgradually adjusttotargetswithrelaxationspeedsthatdependontheinverseoftheaveragematurity ofloans/deposits.

5.2.2. Banksprofits,nonperformingloansandleverage

Banksmakeprofitsfromtheinteresttheyreceiveonserviceableloansfromtheprivatesector, couponpaymentsongovernmentbonds,commissionsandinsurance,afterdeducting theirfundingcosts,i.e.interestpaidonsavingdepositsandadvances,wagesandsalaries ofpersonsemployedinthebankingsector,employers’socialcontributions,intermediate consumptionandothertransferstothegovernment.Wealsoassumethatinsuranceservices totheproductivesectorsoftheeconomyareconstantproportionsofthenominalvalueofthe capitalstockineachsector.Itisalsoassumedthatcommissionsareproportionaltothetotal debtoftheprivatesector,includinghouseholds.Asinothersectors,grossprofitsaretaxed bythegovernment.Partofnetprofitsisdistributedtodomesticandforeignshareholders throughdividends,andtheretainedearningsincreasebanks’ownfundstosatisfyariskweightedtargetcapitalratio(BankforInternationalSettlements,2017).Notethatafraction ofagriculturalloans,mortgagesandcorporateloansisnon-performing(NPLs).Thelower thelevelofeconomicactivity,asmeasuredbyunemploymentandrealGDPgrowth,the higheristheproportionofNPLs.InflationtendstoreducetheamountofNPLs,ashigher nominalincomesmakeiteasiertomeetpaymentobligations.Finally,ahigherreturnon equityallowsbankstofinancelessriskyinvestmentprojects,therebyreducingthelikelihoodof

14

non-performingloans(MessaiandJouini,2013;Abidetal.,2014;RomdhaneandKenzari,2020). Notethatemploymentinthebankingsectorisaconstantfractionofactivepopulation.

Inreality,banksreceiveinterestonserviceableloansandpayinterestonsavingsdeposits, asrecordedintheTFM 2.Notehowever,thatinthenationalaccounts,theoutputofthe financialsectorincludesfinancialintermediationservicesindirectlymeasured(FISIM).FISIMis anaccountingconventionthataimstocapturefinancialintermediationanddividesinterest paymentsasfollows.Anamountthatcorrespondstotheinterestchargedbybanksfor providingloanablefundstoinvestors,calculatedastheinterestpaymentsresultingfroma ratespreadbetweenthelendingrateandthereference(policy)rate,plusanamountthat correspondstotheinterestbankspaytosavers,calculatedastheinterestpaymentsfroma ratespreadbetweenthedepositrateandthereferencerate.Putsimply,ifcreditoperated throughaloanablefundsmarketandifsavingsandinvestmentequilibratedthroughthe naturalrate,FISIMwouldcorrespondtowhatbankswouldcharge(markup)toinvestors pluswhatbankswouldretainfromsavers(markdown),overthenaturalrateofinterest. NationalaccountsthenproceedbydistributingFISIMasfinalandintermediateconsumption offinancialservicesbynon-financialcorporationsandhouseholdsandtreatitasgrossvalue addedfromfinancialintermediation.TheremaininginterestpaymentsnotrecordedasFISIM, i.e.interestpaidondepositsandreceivedonloans,calculatedusingthereferencerate,is thenrecordedundertheprimarydistributionofincomeaccounts8 .

However,itiswellestablishedthatbanksdonotactasintermediariesinaloanablefunds marketwhenprovidingdomesticcurrencyloans(McLeayetal.,2014).Indeed,becauseofthe model’sendogenousmoneyframework,thereisnoreasontotreatbanksasintermediaries. WethereforeconsideralltheFISIMrecordedinthenationalaccountsasamarginoninterest ratesandshiftittointerestpayments.Consequently,thegrossoperatingsurplusandthe valueaddedgeneratedbythebankingsectordifferfromthenationalaccountsandtherefore arenotreported,andnominalGDPismeasuredonlythroughfinalexpenditure.Sincewetreat thebankingsectorasanon-productivesector,weunderestimatenominalGDPbyanamount equaltoFISIMpaidtohouseholdspluscommissionsandinsurancecostsofhouseholds 9.In orderthentomatchempiricallythenominalGDP,weaddtofinalexpendituresthemissing financialconsumption,i.e.insuranceservicesandcommissionspaidbyhouseholdsand householdFISIM(seeequation267and268intheAppendix).

5.3. GovernmentandtheCentralBank 5.3.1. Governmentexpenditureandfinancing

Thegovernmentprovidespublicservicesbyemployingaconstantproportionofthetotal populationaspublicservants.Italsoinvestsinpubliccapitalataconstantrate,andinadaptation(irrigationmainlyaswewilldiscussbelow)dependingontheclimatechangescenario simulated.Totalgovernmentoutputisthereforecomposedofthelabourcostsofgovernment employees,totalpublicintermediateconsumption,employer’ssocialcontributionspaidby thegovernmentanddepreciationofpubliccapital,asinSystemofNationalAccounts(SNA). Governmentalsoprovidessocialbenefitsandwelfareprogrammes,whichareassumedto bepro-cyclical,dependingontheunemploymentlevelandtheaverageprivatewagelevel. Totalpublicexpenditureisgivenbythesumofpublicemployees’wagesandemployer’s socialcontributions,intermediateconsumptioninputs,socialbenefits,investmentinpublic capitalandadaptation,andinterestpaidonoutstandingpublicdebt.

Governmentrevenueisdeterminedbythesumofemployers’socialcontributions,workers’

8See(ZezzaandZezza,2019)forasimilardiscussion.

9TheFISIMthataccruestoNFCsandthecommissionandinsuranceservicesconsumedbyNFCsincreasethe grossvalueaddedofbanksbythesameamountthattheyreducethegrossvalueoffirmssotheydonotneedtobe addedtothenominalGDPcalculationsfromthedemandside.

15

socialcontributions,VATinthethreegoodsoftheeconomy,importtaxes,taxesonproduction andothertaxesonproducts,dividendsfrompublicenterprises,centralbankprofits,and incometaxes.Thepublicdeficitisfinancedbyborrowing.First,thegovernmentborrows partofitstotalfinancingneedsasforeigncurrency(FX)denominatedloansataconstant proportionofthetradedeficit10,andtheremainingneedsarefinancedbydomesticcurrency bonds.Itisassumedthattheinterestrateonforeigncurrencypublicbondsdependsonthe countryrisk,whiletheinterestrateonthedomesticcurrencybondsdependsontheratioof publicdebttoGDPandCPIinflation.

Aswiththebankingsector,wetreatthepublicsectorasanon-productivesector.This meansthatproduction,andhencefinalandintermediateconsumptionofpublicservices asmeasuredbytheNSAframework,isnotexplicitlytrackedintheTFM.Therefore,inorder totracknominalGDP,weaddtofinalexpenditurethenominaldepreciationofthepublic capitalstock,theemployer’ssocialcontributionspaidbygovernment,publicwagesand government’sintermediateconsumptiontoaccountfortheproductionandthereforefinal consumptionofpublicservices.

5.3.2. CentralBank

Thecentralbankfollowsapureinflation-ratgetingTaylorrulewhensettingthepolicyrate andactsaslenderoflastresorttothebanks,providingliquiditytothebankingsectoron demandthroughcentralbankadvances.Italsobuysafixedfractionofpublicbondsateach pointintime.Anyprofitsmadebythecentralbankaredistributedtothegovernment.

5.4. Households 5.4.1. LabourMarketandWageBargaining

Employmentinthemodelisdemanddrivenbymarketconditions,andpartlysupplyconstrained,byclimatechange.Asexplainedabove,employmentintheagriculturalsectoris drivenbyclimatechange,andacomponentofdemandforprocessedfood,i.e.exports,is alsodirectlyaffectedbyclimatechange.Fortherestoftheproductiveactivities,expected salesdetermineproductionandthereforeemployment.

Themodeldoesnotidentifydistinctsocialclasseswithinthehouseholdsector.However, tocapturethedifferentpositionsinthesystemofproduction,wedistinguishbetweentwo sourcesofincome.First,householdsearnnetdisposablewageandproductionincomefrom theemployedpersonsintheprivateandpublicsectors,afterconsideringtheincometaxes, socialbenefitsandworkers’socialcontributions.Second,householdsearnnetfinancial incomeintheformofdividendsandprofitsfromtheproductiveandbankingsectors,interest incomeonsavingsandcurrentdepositsandremittancesfromtherestoftheworld.Non-wage incomeisnetofinterestpaidonserviceablehouseholddebt,commissionsandinsurance paidtobanks.

Inallthesectors,i.e.agriculture,NFCs,banksandgovernment,nominalwagesarefully indexedtoinflationandproductivitygrowth,keepingrealwagesconstant.

5.4.2. ConsumptionandSavings

Householdshaveatargetlevelofnominalconsumption,whichdependsonatime-varying marginalpropensitytoconsumeoutofnominalincome;thepropensityisanegativefunction oftherealdepositrateashouseholdshaveanincentivetosavemorewhenthedeposit

10Thedecisiononwhatproportionofnewdebtwillbeinforeigncurrencydependsonanumberoffactorsand considerations,suchasarbitrageopportunities,riskmanagementandotherpolicyobjectives.Wedisregardthese considerationsinthislong-runmodelanduseafixedratioforpublicFXborrowingtothetradedeficit

16

rateishigher.Actualconsumptionadjustsgraduallytoitstarget,witharelaxationspeed thatcaptureshabitformation.Oncetotalconsumptionisdetermined,householdsallocate theirincomebetweenagriculture,processedfoodandthenon-foodgoodthroughalinear expendituresystem(LES)asinLluch(1973).However,withfixedmarginalbudgetshares,LES violatesEngel’slawthatmarginalincomeelasticitiesoffoodmustdecreasewithgrowing income(seeHoetal.(2020)).We,therefore,assumethatthemarginalbudgetsharesof agriculturalandprocessedfoodarenegativefunctionsofrealconsumption.Householdsalso haveatargetinvestmentinhousing,definedasafractionoftheirtotalnetdisposableincome, andactualhouseholdinvestmentgraduallyadjuststothistarget.Aconstantproportionis financedthroughbankinglendingandtherestthroughthenetdisposableincome.

Householdsdistributetheirsavingsinforeigncurrencydeposits,savingandcurrentaccount depositsindomesticcurrencyandgovernmentbonds.Foreigncurrencydepositsarea shareoftotalremittancesreceivedfromabroadandcurrentaccountdepositsareashare ofconsumptionfortransactionpurposes.Aconstantshareoftheremainingsavingsis investedingovernmentbondsandtheresidualsavingsareheldassavingaccountdeposits indomesticcurrency.

5.5. BalanceofPaymentsandExchangeRateDynamics

Theforeignexchangemarketischaracterisedbyadisequilibriumbetweentheflowofforeign exchangedemandandsupply,asinCharpeetal.(2011).Therefore,thenominalexchange rate,measuredasdomesticcurrencyperunitofforeigncurrency,increases(decreases)with excessdemand(supply).Totaldemandforforeignexchangeisgivenbythesumofimports, theincomeaccount,i.e.theinterestpaymentsonforeignexchangedebtanddividendspaid totherestoftheworld,andtheflowdemandofthebankingsector,whichisdeterminedby the’no-FX-openposition’requirement.Totalforeignexchangesupplyisgivenbythesum ofexports,FDIflows,remittancesandothertransfersfromabroad,cross-bordercreditand foreignexchangedepositinflowstotheprivateandgovernmentsectorsand,dependingon thesimulatedscenario,concessionalloanstothegovernmentthatfinancepublicadaptation investment.

Thestock-flowconsistentstructureofthemodelisparticularlysuitableforstudyingexternal imbalances,thevulnerabilityofcountriestofinancialcrisesandthemacro-environmental channelsthatcanpropagatetheenvironmentaldamages,sincethemodeltracksnotonly theevolutionofcurrentaccountimbalancesandthefirst-roundnegativeeffectsofclimate damagesonthetradebalance,butalsothegrossexposuretoexternalfinancialrisks,which isusuallyneglectedwhenassessingexternalimbalances(BorioandDisyatat,2011,2015).The latterisexplicitlytrackedbytheendogenousinternationalinvestmentposition,aswellasby thedynamicsofavailableforeignexchangereserves.Furthermore,themultisectoralstructure allowsforadetailedexaminationofhowsuchfinancialrisksaredistributedwithinthecountry throughtheaccumulationofexternaldebtinthebalancesheetsofallinstitutionalsectors, andallowsfordetailedfeedbackeffectssuchaspriceeffects,throughtheevolutionofthe interestrates,andquantityeffects,suchasthequantityrationingintheforeignexchange market,theevolutionofdomesticnon-performingloansandtheoverallindebtednessofthe Tunisianeconomy.

6. Calibration

Inordertocalibratetheparametersofourmodelweutilizeawidevarietyofeconomic data,listedinTable 4.TheCovarianceMatrixAdaptationEvolutionStrategy(CMA-ES) (HansenandAuger,2011)isusedtoempiricallyfitthemodeltoTunisianmacroeconomicand financialdataforvariablesforwhichwehaveasatisfactorilylargedataset.TheCMA-ESis

17

astochastic,evolutionaryoptimisationalgorithmthatisappropriateforthecalibrationof complex,nonlinearsystemsofdifferentialequationsasitallowsforanefficientexplorationof theparameterspace.Usingablockapproachandtakingintoaccounttheavailabledata,the calibrationoftheparameterswascarriedoutforfiveblocksrelatingtoproductionandpricing inprocessedfoodandnon-foodgoodsectors,consumption,imports,exports,andnonperformingloans.Theiterativeprocedurethatwasutilisedinthecalibrationprocessesisthe following.Anobjectivefunctionisdefined,whichmeasuresthedifferencebetweenthemodel’s predictionandactualdata.Then,theparameterspaceisdefinedthrougharangeofplausible parametervalues.Avectorofparametervaluesisrandomlyinitialisedandthesystemis simulatedthrougha4thorderRunge-Kuttamethod.Thecandidatesolutionsareevaluated andbasedontheirfit,themeanandcovariancematricesoftheparameterdistributionare updated.Then,anewparametervectorissampledfromtheupdateddistribution.Thelast twostepsareiterateduntilthealgorithmconvergestoasatisfactorysolution.Weprovidea completelistofparametersintheAppendix,withtheirvalues,definitionsandhowtheywere obtained.Forparametersforwhichanestimationwasnotpossibleduetothelackofalarge enoughsample,weusedthedataattheinitialpointofsimulationsforcalibrationtoensure thatthemodelreplicatestheeconomicdataaspreciselyaspossible.

SourceData-set

NationalInstituteofStatistics(INS)

CentralBankofTunisia

MinistryofAgriculture/NationalObservatoryofAgriculture

MinistryofFinances

UNCOMTRADE,WorldInternationalTradeSolution (WITS)

IntegratedEconomicAccounts(IEA),MacroeconomicAggregates,Supply-UseTable,FlowofFunds(FoF),Populationand LabourMarketStatistics

BalanceofPayments(BoP),InternationalInvestmentPosition (IIP),NetBankingProducts,ExchangeRates,ExternalDebt, Loansbysector,BondsandInterestRatesStatistics

DomesticproductionbycommodityinAgricultureSectorin quantity(Tonnes)andValue(TunisianDinar),Commodity prices

PublicDebt,Publicfinancialindicators,Taxesonprofitsand income

Imports/Exportscommodityinquantityandvalue(HS-6digits,Imports/ExportsCommoditypricesinDollar,Importsshare forconsumption,intermediateconsumptionandinvestment bysector(A,PFandF)

LaborproductivityinTunisiaandtheRestoftheWorld InternationalMonetary Fund FinancialSoundnessIndicators(FSI),IntegratedMonetary Statistics;BanksandCentralBank’sBalancesheet

PennWorldTable(PWT)

Table4:MaindatasetsusedtodeveloptheSFCempiricalmodel

7. Simulations

InordertosimulatetheeffectsoflossesinagriculturaloutputontheTunisianeconomy,we makecertainassumptionsonthefutureevolutionoftheexogenousvariablesinthemodel. ThesevariablesandthedifferentscenariosontheirdynamicsarelistedinTable5below.

Forourinitialanalysis,weconstructthreedifferentscenarios:Thebusinessasusualscenario (BAU)definedabovewithnochangeincurrentmacroeconomicpolicies;anoptimistic scenarioinwhichwetakeintoaccountthelossesinagriculturalproductionundertheRCP 8.5projectionsbutassumethatfoodpricesriseinlinewithgeneralworldinflation(scenario RCPLI);andapessimisticscenarioinwhichweassumethatfoodpriceinflationexceeds

18

generalworldCPIinflationoverthenextthreedecades(scenarioRCPHI).11 Table5displays thesmoothedannualgrowthratesassociatedwithFigure4bofagriculturalproductionfor consumption(grypac),forintermediateconsumption(grypaic),forexports(grypaw)andgrowth rateofprocessedfoodexports(grPF X ).Forallscenarios,wesettheworldinflationrateof non-foodgoods(Inf NF,w)atthreepercent,whichistheaverageofthelasttwodecades. Throughoutthesimulations,weassumethatthetermsoftradeforallgoodsremainthesame, sothatinflationinimportsofnon-food(inf NF,w),processedfood((inf PF,w))andagricultural goodsforconsumption(Inf A,w C )andintermediateconsumption(Inf A,w IC )areequaltoinflation inthepricesofexportsofthesegoods(Inf NF X , Inf PF X and Inf A X respectively).Wecalibratethe labourproductivitygrowthfunction(seeAppendix,equations248-249)tosetitsvalue(gra) equaltoitsaveragevalueoverthelasttwodecadesinTunisiaat1.5%.Wealsoassumeno catching-uporlaggingintermsoflabourproductivitygrowthbetweenTunisiaandtherest oftheworldandthuswealsosetthegrowthrateoflabourproductivityintherestoftheworld ( graw)at1.5%.Thegrowthratefortheworldeconomy(grw)isfixedarounditsaveragevalue inthelasttwodecadesatthreepercentinallthescenarios.ForTunisia’spopulationgrowth rate(αpop),weuseUN’s’highvariant’scenarioprojectionswithanadditionalassumptionthat labourforceparticipationrateincreasesby4%overthenextthreedecadesandwesmooth thegrowthrateto0.7%peryear.

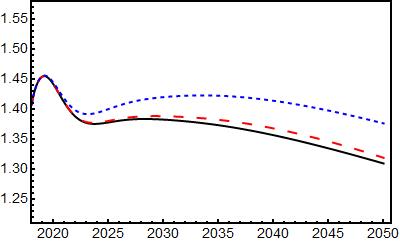

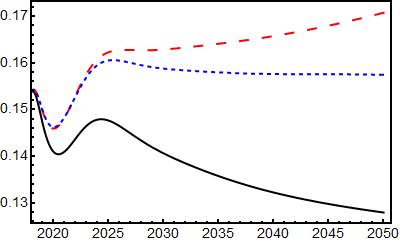

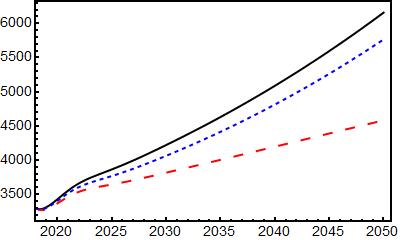

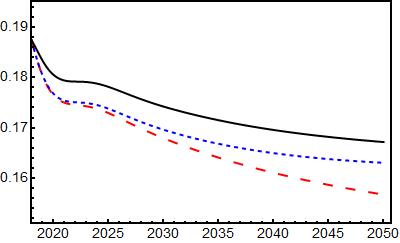

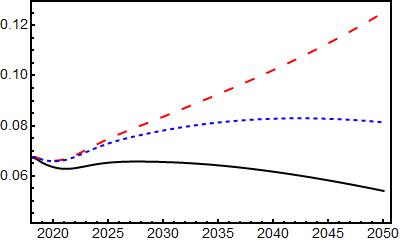

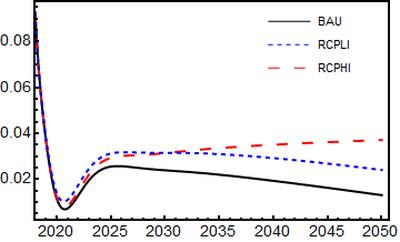

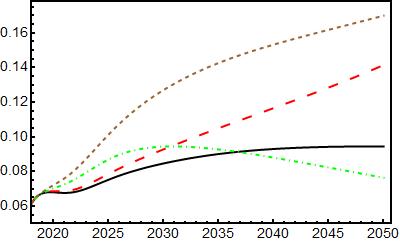

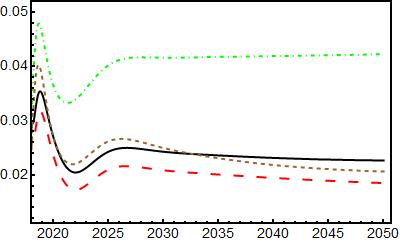

Thegraphsoffigure6showtheresultsofthesimulationsfortheBAUandthetwoRCP8.5 scenarios(RCPLIandRCPHI)describedabove.12 OurBAUscenariograduallystabilisesjust below13%unemploymentrateandgeneralinflationfallsbelow5%.Bothagriculturaland processed-foodinflationremainclosetothegeneralinflationrate.Similarly,economicgrowth isabove2%inthelongrun,inlinewithpopulationandgeneralproductivitygrowth.Inthe longrun,thepublicdeficitisaround5%ofGDPandthepublicdebtstabilisesat90%ofGDP. Startingfromover13%ofGDPinearly2018,thetradedeficitsettlesaround9%inthelong

11Thisisessentiallythedisturbingobservationofthelastdecade,asdocumentedbyBogmansetal.(2021).

12Wedonotbringtheeconomytoasteadystate,butsimulatethemodelstartingfromtheactualvaluesofthe Tunisianeconomyattheendof2017.Therefore,thedisequilibriumadjustmentprocessesleadtofluctuationsinthe modelbeforestabilising.Infact,withoutlaggingproductivitygrowthrelativetotherestoftheworldandduetothe largedepreciationofthenominalexchangeraterelativetodomesticinflation,therealexchangeratedepreciatesat thestartofallsimulations,leadingtoanexport-ledgrowthspurtthatstabilisesasthemacro-financialfeedback loopstakeeffect.

VariableBAU RCP8.5LowInf (RCPLI) RCP8.5HighInf (RCPHI) grypac 0.97%-0.36%-0.36% grypaic 1.3%-0.13%-0.13% grypaw 1.45%-0.53%-0.53% grPF X 1%-0.37%-0.37% Inf NF,w 3%3%3% Inf A,w C 3%3%5.5% Inf A,w IC 3%3%5.5% inf PF,w 3%3%5.5% Inf NF X 3%3%3% Inf PF X 3%3%5.5% Inf A X 3%3%5.5% gra 1.5%1.5%1.5% graw 1.5%1.5%1.5% grw 3%3%3% αpop 0.7%0.7%0.7%

Table5:ExogenousVariablesforallscenarios.

19

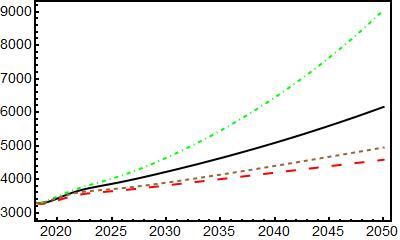

run,leadingtoacurrentaccountdeficitofroughly7%ofGDP.Astheexternaldeficitsettles downtoitslong-runvalue,thecountryslowlyaccumulatesforeignexchangereserves,which reachjustoverfourmonthsofimportsinthelongrun.Finally,foodimportsasashareofGDP stabilisecloseto4%ofGDPintheBAUscenarioandpercapitaincome,measuredin2017 Euros,risessteadilyto6000Euros.

Figure 5 summarisesthemainpropagationmechanismsfollowingacontinuousdecline inagriculturalproductionduetoclimatechange.Becauseweassumeaconstantrate ofproductivitygrowthintheagriculturalsector,inlinewiththerestoftheeconomy,falling agriculturalproductionleadstoandecreaseinemploymentintheagriculturalandprocessed foodsector,whichreduceshouseholdincome.Thisfallinhouseholdincomeleadstoafallin overallrealconsumption.However,thedynamicsofrealconsumptionoffood,processed foodandnon-foodgoodsisambiguousduetothelinearexpenditurespecificationofthe consumptionallocationdecision.Ontheonehand,lowerrealconsumptionlevelsunder RCP8.5leadtohighermarginalbudgetsharesoffoodandprocessedfoodandalower marginalshareofnon-foodgoodsinconsumption.Ontheotherhand,realconsumption offoodandprocessedfoodfallsbecausepriceinflationforthesegoodsishigherthanfor non-foodgoodsunderRCP8.5duetothehighcostofimportedfood.Asaresult,theoverall impactonrealconsumptionofnon-foodgoodsdependsonthemagnitudeoftheseeffects. Inoursimulations,thismechanismhasanoverallpositiveimpactontherealconsumption demandfornon-foodgoodsundertheRCPHIscenario(butnotRCPLI),mitigatingthenegative impactoflowerhouseholdincomes.However,withhigherfoodprices,theoverallshareof agro/processedfoodproductsinthehouseholdconsumptionbasketishigherunderboth RCPLIandRCPHIscenarios,despitelowerrealconsumptiondemandforthesegoods.In otherwords,householdsconsumelessfoodandspendahigherproportionoftheirtotal consumptionexpenditureduetoclimatechange.

Loweragriculturalproductionandthegrowingdemandforagriculturalandprocessedfood commoditiesalsopushagriculturalimportsaboveBAUlevels,whicharemuchhigherin

Figure5:TransmissionofLossofAgriculturalProduction

Figure5:TransmissionofLossofAgriculturalProduction

20

nominaltermsinRCPHIwithelevatedglobalfoodpriceinflation.Demandforforeignexchange isalsohigherwithahighertradedeficitdrivenbyfoodimports,andgivenourassumptionthat thegovernmentborrowsafixedproportionofthetradedeficitinforeignexchange,partofthis additionaldemandforforeignexchangeismetbypublicsectorforeignexchangeborrowing. However,thenominalexchangeratestilldepreciatesfasterthanintheBAU,pushingup inflation.

Risinginflationhasseveraleffectsontheeconomy.Ontheonehand,higherinflationpushes

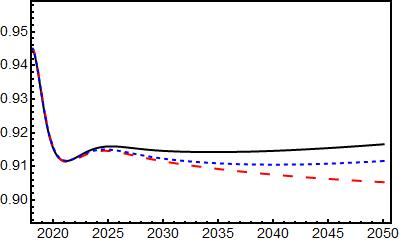

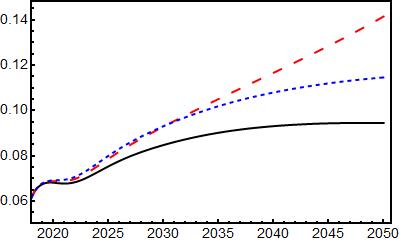

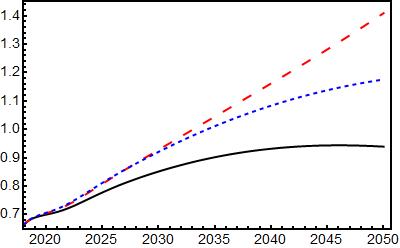

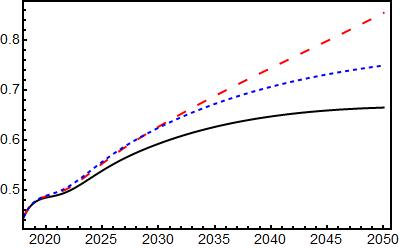

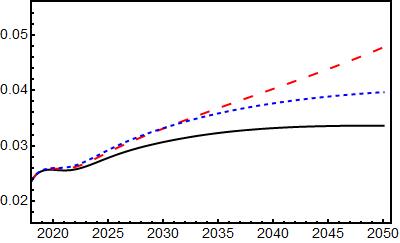

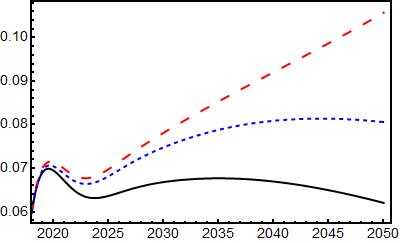

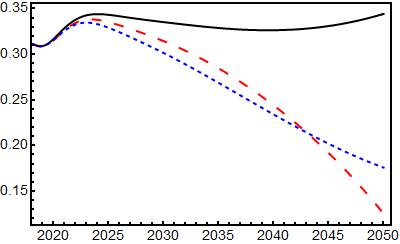

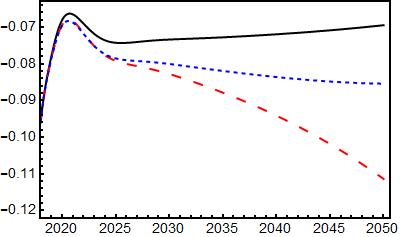

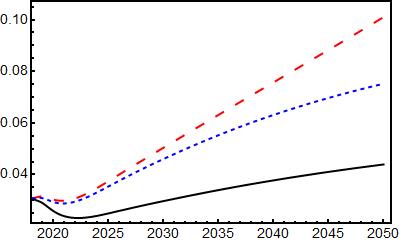

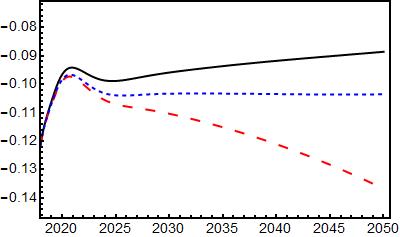

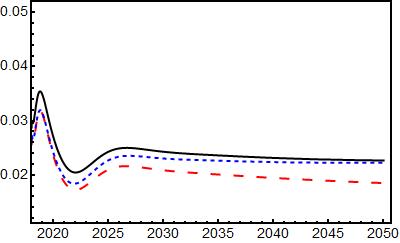

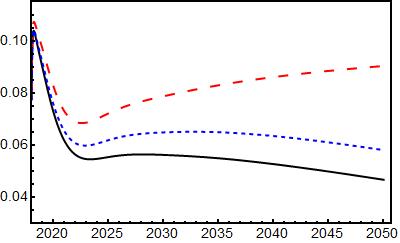

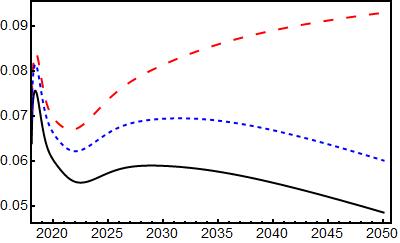

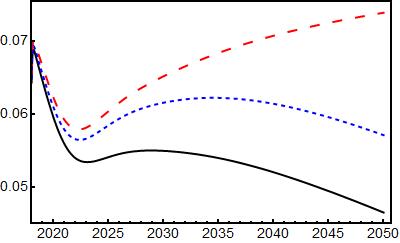

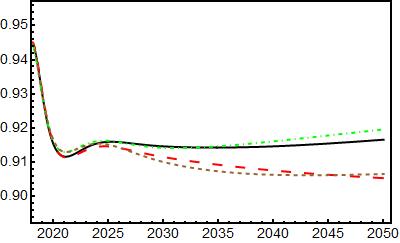

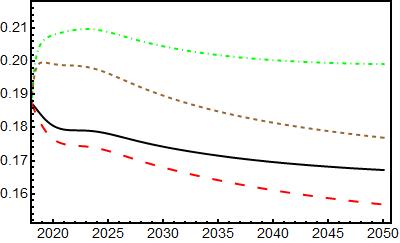

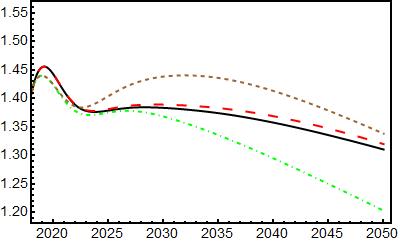

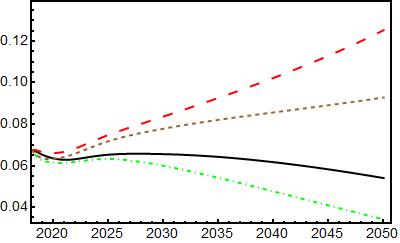

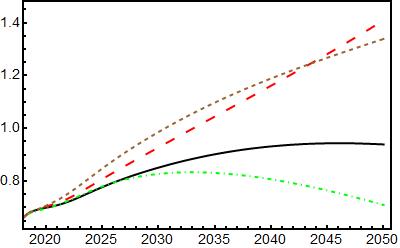

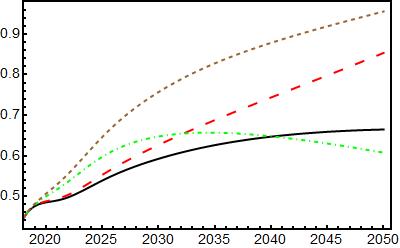

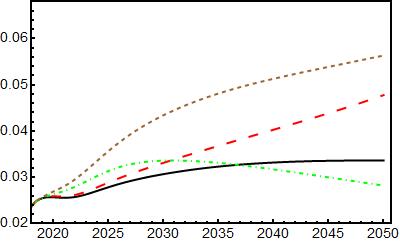

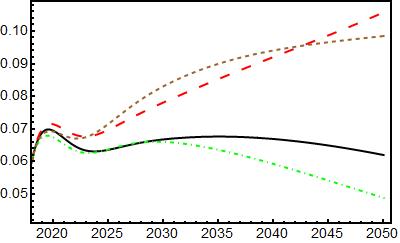

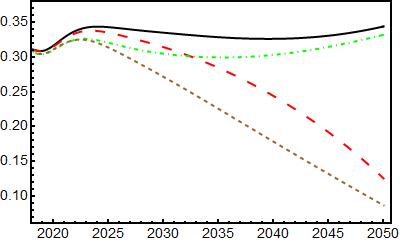

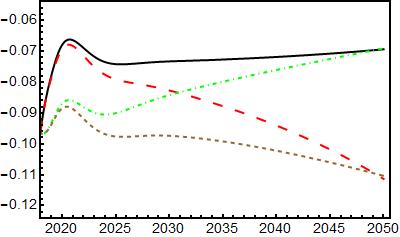

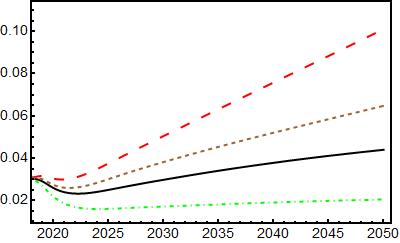

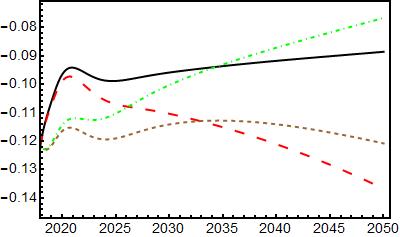

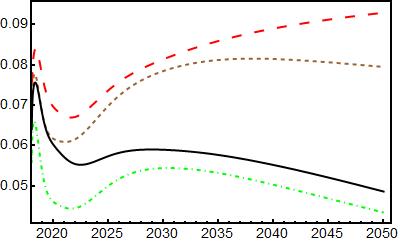

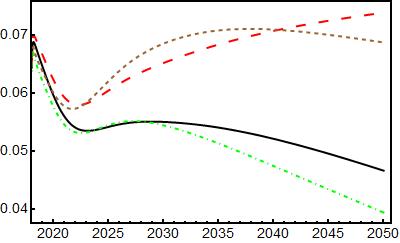

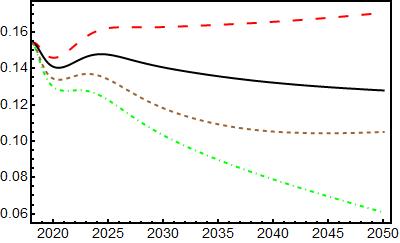

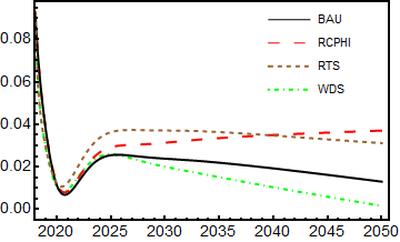

(a)NominalDepreciation (b)Unemployment (c)Inflation (d)Foodinflation (e)ProcessedFoodInflation (f)RealGrowthRate (g)TradeBalance(%GDP) (h)FoodImports(%GDP) (i)CurrentAccount(%GDP) (j)FXReserves/Imports (k)DomesticBondRate (l)FXBondRate (m)PublicFXDebt/GDP (n)PublicTotalDebt/GDP (o)PublicDeficit (p)RealExchangeRate (q)Investment/GDP (r)CountryRisk (s)PropensitytoConsume (t)PercapitaIncome Figure6:Simulationresultsforselectedvariables.Source:authors’computations.

21

uppolicyrates,pushinguprealdepositratesandlendingratesindomesticcurrency.While higherrealdepositratesreducethemarginalpropensitytoconsume,leadingtoafurther declineinconsumptiondemand,higherdebtfinancingcostsreducetherateofprofit,leading tolowerinvestment.Ontheotherhand,duetotheimperfectpass-throughofnominal exchangeratestodomesticinflation,therealexchangeratedepreciatesmorerelativeto BAU,reducingthepropensitytoimportnon-foodgoodsandtriggeringhigherexportdemand fornon-foodgoods.Theoverallimpactondemandfornon-foodgoodsisthusdetermined bythemagnitudeoftheseeffectsonconsumption,investmentandexports.Althoughinour simulationsthepositiveeffectofhigherexportdemandoutweighsthenegativeeffectson consumptionandinvestmentunderRCPLIandnon-foodproducersemployaslightlyhigher percentageofthelabourforcethanintheBAU,thisadditionalemploymentinthenon-food sectorisfarfromcompensatingforthedeclineinemploymentinagricultureandprocessed food,andtheoverallunemploymentraterisessignificantly 13 .

Whilerealdepreciation-inducedexportgrowthmitigateshigherunemploymentasmentioned above,rapidnominalexchangeratedepreciationhasevenmoreseriousconsequencesfor theexternalpositionandfiscalbalancesbothbypushingupthealreadyhighexternaldebt-toGDPratioandbyincreasingcountryriskandthustheassociatedfinancialacceleratoreffects. Highercountryriskraisesforeignexchangeborrowingratesforboththegovernmentand firms,whileatthesametimeleadingtogreaterrationingofNFCsbyinternationalmarketsand reducingthesupplyofforeignexchange.Theincomeaccountdeterioratesasaresult,putting furtherpressureonanacceleratingcurrentaccountdeficitanderodingforeignexchange reserves.14 Combinedwithhigheroverallunemployment,lowergrowth,lowertaxrevenues andhigherborrowingrates,thegovernment’soverallfinancingneedssoar,pushinguppublic debtfurther.

ThedynamicsoftheeconomyunderfallingagriculturaloutputareshowninFigure6,together withtheBAU,toillustratethemagnitudeoftheseeffects.Clearly,theeffectsoflossof agriculturaloutputareverysevereontheTunisianeconomy,whetherglobalfoodinflation remainslowornot.However,asexpected,theconsequencesaremuchdirerifglobalfood pricesincreaserapidlyinthenextthreedecades.UndertheRCPHIscenario,unemployment exceeds17%inthelongrun,withbothfoodandprocessedfoodimportsmovingtowards two-digitlevelsinthelong-run.Tradedeficitexplodesabove13%,drivenbyhighlevelof foodimports.Similarly,currentaccountdeficitsetsonanunsustainablepath,asthecountry runstheriskofaloomingcurrencycrisiswithadepletionofFXreserves.Publicdeficitand publicdebtlevelsindicaterisingpossibilityofadefaultonpublicdebt,asdebttoGDPratio exceeds140%inthelong-run,withnosignofstabilizing 15.Percapitaincome,measuredin 2017Euros,barelygrowsuntil2050.Inshort,allelseequal,no-actionagainstclimatechange pavesthewayforanalmostcertaineconomiccrisisforTunisiaunderrapidlyrisingglobal foodprices.

8. AdaptationPolicy

Next,wesimulatetwodifferentadaptationpolicyscenariosenvisagedbytheTunisian governmentandoutlinedinthe’Water2050Plan’(Jeffetal.,2020).Whilethisplanincludes severaldifferentadaptationscenarios,wechosetosimulatetwoofthem,namelythe ReinforcedTendencyScenario(RTS)andtheWaterandDevelopmentScenarios(WDS). Table6summarisesthemainassumptionsbehindthesescenarios.IntheRTS,economic growthremainsaroundits2018valueat2.5%.Similarly,thewaterelasticitiesofproductionin

13UndertheRCPHIScenario,employmentinthenon-foodsectoralsofallsbelowtheBAUlevels.

14NotethatwehavenotimposedanyrationingofgovernmentFXborrowing,andthehigherFXdemandcausedby highertradedeficitsispartlymetbygovernmentFXborrowing,asthegovernmentborrowsafixedproportionofthe tradedeficitinFX.

15NotethatwehavenotassumedanyrationingonpublicFXborrowingtoshowtheimplicationsofclimatechange onpublicfinancesclearly.Withsuchelevateddebtlevels,thepublicsectormayfacehighrationinginFX-borrowing, causingacurrencycrash

22

manufacturingandservicesremainattheirobservedvaluesin2020,whilewaterelasticity ofagriculturalproductionisassumedtofallto0.2.Insuchacase,agriculturalproduction canonlygrowby1%peryear,despiteastrongadaptationinvestmentplantoincreasewater resources,astheavailablewatersupplyismainlyconsumedbytheindustrialandservice sectorsandthuscannotsupportahigheragriculturalgrowthrate.IntheWDSscenario,onthe otherhand,amuchmoreefficientwaterusestrategyinthesesectorssignificantlyreduces thewaterelasticitiesofproductioninallsectors,allowingagriculturalproductiontogrowby 3.5%peryear,alongsideanoveralleconomicgrowthrateof4.3%peryear 16 .

InlinewiththeWater2050plan,weassumethatpublicandprivateadaptationinvestments areboth1.1%ofGDP,andthatpublicinvestmenthasaveryhighimportpropensityof60%,as itinvolvestheconstructionofdesalinationandwastewatermanagementplants,someof whichwillbesolar-powered.Itisalsoassumedthatthepublicadaptationinvestmentwillbe financedbyforeignexchangeloansatafixedrateof1.7%,whichistheinterestrateontheloan fortheSfaxdesalinationplantcurrentlyunderconstruction(JapanInternationalCooperation Agency,2017).Inourmodel,themedium-andlong-termgrowthrateoftheeconomydepends strictlyonthegrowthrateoflabourproductivity.Thus,toachievethehighgrowthrate envisagedintheWDS,weassumethatpublicinvestmentgrowsatamuchhigherratethan inpreviousscenarios,at4.5%,andthatefficientinvestmentinareassuchasinfrastructure, health,R&Dandeducationgraduallyraisesthegrowthrateoflabourproductivitytoover threepercentperyearby2050.Thisisinlinewiththeendogenousgrowthliterature,as detailedinAgenorandYilmaz(2012,2016),andobservedbytheIMF(XiaoandLe,2019).

Figure7showstheresultsofthesimulationsforBAU,RCPHI,RTSandWDS.17 Thegradualincreaseinlabourproductivity,drivenbypublicinvestment,andtherapidgrowthinagricultural productionhavesignificantpositiveeffectsonmacroeconomicdynamics,despitethehigh levelofadaptationinvestmentandthehighimportpropensityundertheWDS.Unemployment

16Theadaptationplandoesnotspecifythegrowthofagriculturalgoodsforconsumption,intermediateconsumption orexports.Thus,inoursimulations,wesetthegrowthrateoftheseequaltothegeneralgrowthrateofagricultural productionundereachadaptationscenario.

17InordertoensurethattheshareofagriculturalemploymentremainswithinreasonablelimitsundertheWDS scenario,weassumethatlabourproductivitygrowthintheagriculturalsectorisequaltothegrowthrateofagricultural outputat3.5%.

Variable Reference (2020) Reinforced Tendency Waterand Development GDPgrowth(2021-2050)2.5%2.5%4.3% Agriculture1.8%1%3.5% Industry1.1%2%4% Tourism3.4%2%4% Services3.2%3%4.5% WaterElasticityofGDP0.520.50.1 Agriculture0.420.20.15 Industry0.60.60.1 Services0.50.50.1 WaterResources(Mm3)498546224594 Conventional492937453968 Non-Conventional66877626 Desalination39752376 WasteWaterManagement 27125250

Table6:AdaptationScenarios

23

fallssteadilyto6%by2050andgeneralconsumerpriceinflationisbroughtdowntobelow theBAUlevels,around4%18.Similarly,processedfoodpriceinflationremainsjustbelowto BAUscenario,slightlyabovegeneralinflationwhileagriculturalgoodsinflationislowertha baselinethroughoutthesimulationperiod.Economicgrowthinitiallyfluctuates(drivenby 18Borio(2014)proposesadistinctionbetweennon-inflationary(potential)outputandsustainableoutput,thelatter dependingonsystemicmacro-financialdevelopmentsandexternalimbalances.Ourmodelsimulationssupport thismodellingfeature.

(a)NominalDepreciation (b)Unemployment (c)Inflation (d)Foodinflation (e)ProcessedFoodInflation (f)RealGrowthRate (g)TradeBalance(%GDP) (h)FoodImports(%GDP) (i)CurrentAccount(%GDP) (j)FXReserves/Imports (k)DomesticBondRate (l)FXBondRate (m)PublicFXDebt/GDP (n)PublicTotalDebt/GDP (o)PublicDeficit (p)RealExchangeRate (q)Investment/GDP (r)CountryRisk (s)PropensitytoConsume (t)PercapitaIncome

Figure7:AdaptationSimulationsforselectedvariables.Source:authors’computations.

24

theexport-ledgrowth,asdiscussedabove)tosettleat4.2%,inlinewiththeWDSprojections. Exportsgrowstronglyduetohighproductivitygrowth,andimportsofintermediateandcapital goodsfallsteadily,improvingthetradebalancetoaround7%ofGDP.Theincomeaccount alsoimprovesslightly,leadingtoacurrentaccountdeficitjustbelow7%inthelongterm.19 Afteraslightdeclineinthefirstdecade,foreignexchangereservesasashareofimportsare setonanincreasingpathtowardssustainablelevelsinthelongterm.20 Despitetheincrease inforeigncurrencyloanstofinanceadaptationinvestment,thetotalforeigncurrencydebtto-GDPratioissetonadecliningpathafterinitiallyrising,fallingbelowBAUlevelstojust under60%inthelongrun,therebyreducingcountryriskandinterestratesonpublicforeign currencyborrowingandeliminatingtheunsustainableaccumulationofforeigndebtinRCPHI. Hightaxrevenuesandlowunemploymentleadtoasustaineddeclineinthepublicsector deficitto3.5%andinthepublicdebt/GDPratioto70%inthelongrun.Percapitaincome, measuredin2017Euros,risesrapidlyto9000Eurosby2050asfoodimportsfallbelowtwoper centofGDP,movingTunisiamuchclosertonear-totalfoodsecurity.

TheRTS,ontheotherhand,paintsaverydifferentpicture.Whilethepositivemultipliereffects ofpublicandprivateadaptationpoliciesreduceunemploymentbelowtheBAUlevel,the currencydepreciatessharplycomparedtoallotherscenarios,keepinggeneral,foodand processedfoodinflationclosetothehighinflationscenario.Despitethepositiveimpactof therealdepreciationonnon-foodtrade,lowoverallproductivitygrowth,highimportcostsof adaptationpoliciesandincreasedfoodimportcostsduetoadepreciatedcurrencyleadtoa tradedeficitoftwelvepercent.Coupledwithanexplodingincomeaccountdeficit,thecurrent accountdeficitreacheselevenpercentofGDPandforeignexchangereservesasashareof importsfallbelowtheRCPHIlevelsinthelongrun.Countryriskalsoexplodestolevelsabove RCPHI,bringingforthamuchhigherprobablityofrationingonpublicFXborrowing.Duetothe sluggishgrowthrateoftheeconomy,publicadaptationinvestmentputsstrongpressureon thebudgetdeficitandpublicdebt,astotaldebtfirstexceedsthehighinflationscenariolevel andstabilizesinthelongrunataroundthesamelevel,withexcessiveexternaldebtdriving theincrease.PercapitaincomegrowthalsoslowsdowntoRCPHIlevels,aggravatedbythe rapiddepreciationofthenominalexchangerate.

9. Conclusion

ClimatechangewillputsignificantpressureonagriculturalproductionlevelsinTunisia, reducingbothproductionfordomesticconsumptionandthetwomainexportcommodities, olivesanddates.Thecostsofnoactionaresevereinmacroeconomicterms,andtheNFC sectorcannotcompensateforthelossesinruralemploymentandproductionifproductivity growthremainssluggishrelativetotherestoftheworld.Theresultisexcessivefiscaland currentaccountdeficits,leadingtounsustainablepublic/externalbalancesandalooming currencycrisis,especiallyifpublicfinancingofexternaldeficitsthroughFXborrowingdriesup inthefaceofelevatedcountryrisk.Theaccumulationofsuchmacroeconomicimbalances

19WehaveassumedthatFDIremainsafixedpercentageofNFCsectorproductionthroughoutthesimulations. Wepartlyunderestimatetheseinflows,asthefavourableeconomicconditionsunderthishigh-growthregimemay triggeranincreaseinFDIinthemediumandlongterm,leadingtoafurtherimprovementinthecurrentaccount.

20Throughthesesimulations,wekepttheratioofpublicFXborrowingtotradedeficitconstant,despiteafalling tradedeficit/GDPratio.Inessence,thereisaconstantneedforcoordinatedmonetaryandfiscalpoliciestoprevent currencyappreciationandensureFXreserveaccumulationandpublicsolvency.Asisthecaseforalldeveloping economies,realcurrencydepreciationinducedbycentralbankinterventioninforeignexchangemarketsmayreduce tradedeficitsatthecostofreducingpercapitaincomeinFX.However,thepositivetradeeffectsofrealdepreciation arelimited,taketimetomaterialiseandareconstrainedbyproductivitygrowthdifferentials,thecomplexityof exportsandthesizeofthetradablesector.Ontheotherhand,depreciationimmediatelyincreasesthedomestic currencyvalueofpublicandprivateFXdebt,increasingcountryriskandthelikelihoodofpublic/privatesector insolvency.WhilepublicFXborrowingmayprovidetheeconomywithmuch-neededFXreserves,increasesinpublic debthaveadestabilisingfinancialacceleratoreffectthroughdomesticandFXbondinterestrates,subsequently worseningtheincomeaccountandleadingtogreaterrationingofcross-borderborrowingbyfirmsorthegovernment. Theseconsiderationscallformuchmoresophisticatedcoordinationbetweenmonetaryandfiscalpolicytoensure sustainabledevelopmentthanthesimpleborrowingrulesweusedinourmodel.

25

willbeexacerbatedifglobalfoodinflationishigherthangeneralglobalinflationorifTunisia’s exportpartnersgrowslowlyinthecomingdecades.

Whilepolicymakershaverecognisedtheseverityoftheproblemandhaveformulatedlongtermadaptationstrategiesthatincludeinvestmentsinwatersupply,reducinglossesin thedistributionprocessandrehabilitatingexistingreservoirs,thesestrategiesarecostly andrequiretheparticipationoftheprivatesectorintheprocessalongsidethepublic sector.Inaddition,increasingwatersupplyrequirestheconstructionofdesalinationand wastewatertreatmentplants,aswellasenergyresourcestopowertheseunits,whichin thecountry’scurrenteconomicstructurerequireimport-intensiveinvestments.Thus,the financingstructureandcostsofadaptationpoliciesplayacentralroleindeterminingtheir overalleconomicimpactandeffectivenessinstabilisingtheeconomyinthelongrun.

Evenwiththeplannedincreasesinwatersupply,thesimultaneousachievementofwater securityandeconomicdevelopmentwillrequiresignificantreductionsinthewaterelasticity ofproductioninagriculture,industryandservicesthroughtheadoptionofwater-efficient productiontechniques.Theseimprovementsshouldalsobeaccompaniedbyrapidgrowth ineconomy-wideproductivitylevels.Efficientpublicinvestmentinalargepusheffortto stimulatethisproductivitygrowthisthereforecrucial.Ourresultsshowthateconomic developmentandwatersecurityarenotorthogonalifsuchproductivity-enhancingpublic policiesareimplementedtogetherwithwater-efficientproductionmethodsandadaptation measures.

26

References

Abid,L.,Quertani,M.,and Zouari-Ghorbel,S.(2014). Macroeconomicandbankspecificdeterminants ofhousehold’snonperformingloansintunisia: Adynamicpaneldata. ProcediaEconomicsand Finance,13:58–68.

Agenor,P.-R.andYilmaz, D. (2012).Aidallocation, growthandwelfarewith productivepublicgoods. InternationalJournalofFinanceandEconomics

Agenor,P.-R.andYilmaz, D. (2016).Thesimpledynamicsofpublicdebtwith productivepublicgoods. MacroeconomicDynamics,pages1–37.

BankforInternationalSettlements(2017).High-level summaryofbaseliiireforms.

Bernanke,B.andGertler, M.(1995).Insidetheblack box:thecreditchannelof monetarypolicytransmission. JournalofEconomic Perspectives,9(4):27–48.

Blecker,R. (2016).The debateover‘thirlwall’slaw’: balance-of-paymentsconstrainedgrowth reconsidered*. European JournalofEconomics andEconomicPolicies: Intervention,133:275–290.

Bogmans,C.,Pescatori, A.,andPrifti,E. (2021).

Fourfactsabout soaringconsumer foodprices. https: //www imf org/en/Blogs/ Articles/2021/06/24/ four-facts-about-soaringconsumer-food-prices. Accessed:2023-04-05.

Borio,C. (2014).Thefi-

nancialcycleandmacroeconomics:Whathavewe learnt? JournalofBanking Finance,45.

Borio,C.andDisyatat,P. (2011).Globalimbalances andthefinancialcrisis:Link ornolink? BISWorking Papers,346.

Borio,C.andDisyatat,P. (2015).Capitalflowsand thecurrentaccount:Takingfinancing(more)seriously. BISWorkingPapers, 525.

Bovari,E.,Giraud,G.,and McIsaac,F. (2018).Copingwithcollapse:Astockflowconsistentmonetary macrodynamicsofglobal warming. EcologicalEconomics,147:383–398.

Brahmi,N.,Dhieb,M.,and Rabia,M.C. (2018).Impactsdel‘élévationdu niveaudelamersurl’évolutionfutured’unecôte basseàlagunedelapéninsuleducapbon(nord-est delatunisie):approche cartographique.In ProceedingsoftheICA,volume1,page14.

CentralBankofTunisia (2019).Annualreporton bankingsupervision.

Charpe,M.,Chiarell,C., Flaschel,P.,andSemmler, W.(2011). FinancialAssets, DebtandLiquidityCrises Springer.

Chebbi,H.E.,Pellissier,J.P.,Khechimi,W.,andRolland,J.-P.(2019). Rapport desynthèsesurl’agricultureenTunisie.PhDthesis, CIHEAM-IAMM.

Chiarella,C.andFlaschel, P. (2006). TheDynamicsofKeynesianMonetaryGrowth:Macrofounda-

tions.CambridgeUniversityPress.

Chiarella,C.,Flaschel,P., andSemmler,W. (2012). ReconstrutingKeynesian MacroeconomicsVolume 1.Springer.

Chiarella,C.,Flaschel,P., andSemmler,W. (2013). ReconstrutingKeynesian MacroeconomicsVolume 2.Springer.

Climat-c (2020).Portailclimatiquedel’institut nationaldelamètèorologie. https://climat-c tn/ INM/web/

Dafermos,Y.,Nikolaidi, M.,andGalanis, G. (2017).Astockflow-fundecological macroeconomicmodel. EcologicalEconomics, 131:191–207.

Dafermos,Y.,Nikolaidi, M.,andGalanis,G.(2018). Climatechange,financial stabilityandmonetary policy. Ecological Economics,152:219–234.

Deandreis,C.,Pommier, D.,Jamila,B.S.,Tounsi, K.,Jouli,M.,Balaghi, R.,Zitouna-Chebbi,R., andSimonet,S. (2021). Impactsdeseffetsdu changementclimatique surlasècuritèalimentaire.

Dhaouadi,L.,Boughdiri, A.,Daghari,I.,Slim,S., BenMaachia,S.,Mkadmic, C.,etal. (2017).Localised irrigationperformancein adatepalmorchardin theoasesofdeguache. JournalofNewSciences, 42:2268–2277.

Fischer,G.,Nachtergaele, F.O.,vanVelthuizen,H., Chiozza,F.,Francheschini, G.,Henry,M.,Muchoney, D.,andTramberend,

27

S. (2021).Globalagroecologicalzones(gaezv4)modeldocumentation.

Flaschel,P. (2008). The MacrodynamicsofCapitalism.Springer.

Flaschel,P.,Groh,G., Proano,C.,andSemmler, W. (2008). Topicsin AppliedMacrodynamic Theory.Springer.

FoodandoftheUnitedNations,A.O. (2018). Future ofFoodandAgriculture 2018:AlternativePathways to2050.FoodandAgricultureOrganisationofthe UnitedNations.

FoodandAgriculture OrganizationoftheUnited Nations (2018).Foodand agricultureprojectionsto 2050. http://www fao org/ global-perspectivesstudies/food-agriculture\projections-to-2050/en/.

Frankel,J. (2010).Monetarypolicyinemerging markets:Asurvey.technicalreport. NationalBureau ofEconomicResearch

Hansen,N.andAuger,A. (2011).Cma-es:evolutionstrategiesandcovariancematrixadaptation.In Proceedingsofthe13th annualconferencecompaniononGeneticand evolutionarycomputation, pages991–1010.

Ho,M.,Britz,W.,Delzeit, R.,Leblanc,F.,Roson, R.,Schuenemann,F., andWeitzel,M. (2020). Modellingconsumption andconstructinglongtermbaselinesinfinal demand. Journalof GlobalEconomicAnalysis, 5(1):63–108.

IMF (2019).Fifthreview undertheextendedfund

facility,andrequestsfor waiversofnonobservance andmodificationofperformancecriteria,andfor rephasingofaccess.

IPCC,A. (2014).Ipcc fifthassessment report—synthesisreport.

Issam,D.,Hedi,D., BenKhalifa,N.,and Mahmoud,M. (2022). Salineirrigation managementinfield conditionsofasemi-arid areaintunisia. Asian JournalofAgriculture,6(2).

Jacques,P.,Delannoy, L.,Andrieu,B.,Yilmaz,D., Jeanmart,H.,andGodin, A. (2023).Assessingthe economicconsequences ofanenergytransition throughabiophysical stock-flowconsistent model. Ecological Economics,209:107832.

JapanInternational CooperationAgency (2017).Signingofjapanese odaloanagreementwith tunisia:Contributing toasolutiontothe watershortageina majormetropolitanarea withthesecondlargest cityintunisiathroughthe constructionofseawater desalinationfacilities. https://www2 jica go jp/ yen_loan/pdf/en/6851/ 20170718_01 pdf.Accessed: 2023-04-05.

Jeff,Peter,D.J.,and Williams,R. (2020). Elaborationdelavisionet delastratègiedusecteur delèauàl’horizon2050 pourlatunisie:Réalisation desetudesprospectives multitheèmatiques etetablissementde modeèlespreèvisionnels offre-demande(bilans).

Kaminsky,G.,Lizondo,S., andReinhart,C. (1997). Leadingindicatorsofcurrencycrises. IMFWorking Paper,97/79.

Khawla,K.and Mohamed,H. (2020). Hydrogeochemical assessmentof groundwaterquality ingreenhouseintensive agriculturalareasin coastalzoneoftunisia: Caseofteboulba region. Groundwaterfor sustainabledevelopment, 10:100335.

Lluch,C. (1973).Theextendedlinearexpenditure system. EuropeanEconomicReview,4(1):21–32.

Louati,D.,Majdoub,R., Rigane,H.,andAbida,H. (2018).Effectsofirrigatingwithsalinewateron soilsalinization(eastern tunisia). ArabianJournal forScienceandEngineering,43:3793–3805.

McLeay,M.,Radia,A.,and Thomas,R.(2014).Money creationinthemodern economy. BankofEngland quarterlybulletin,pageQ1. MedECC (2021).Les risqueslièsaux changementsclimatiques etenvironnementauxdans larègionmèditerrannèe.

Messai,A.andJouini, F. (2013).Microand macrodeterminantsof non-performingloans. InternationalJournalof EconomicsandFinancial Issues,3(4):852–860.

MinistryofAgriculture, WaterResourcesand FisheriesofTunisia(2020). Rapportnationalsurle secteurdel’eau.

Nucifora,A.,Rijkers,B.,

28

andFunck,B. (2014).The unfinishedrevolution: bringingopportunity,good jobsandgreaterwealthto alltunisians. Development PolicyReview,Publisher: TheWorldBank

Romdhane,S.andKenzari, K. (2020).Thedeterminantsofthevolatilityof non-performingloansof tunisianbanks:Revolution versuscovid-19. Review ofEconomicsandFinance, 18:92–111.

UnitedNationsClimate Change (2022). Stratègie

dedèveloppementneutre encarbonneetrèsilientau changementclimatique àl’horizon2050-Tunisie. UnitedNationsClimate Change).

WRI (2020).Aqueduct 3.0countryrankings. https://www.wri.org/ applications/aqueduct/ country-rankings/

Xiao,Y.andLe,N.-P. (2019).Estimatingthe stockofpubliccapital in170countries. https: //www.imf.org/external/ np/fad/publicinvestment/

pdf/csupdate_aug19 pdf Accessed:2023-04-05.

Yilmaz,D.andGodin, A. (2020).Modelling smallopendeveloping economiesina financialisedworld:A stock-flowconsistent prototypegrowthmodel. AFDResearchPapers,125.

Zezza,G.andZezza,F. (2019).Onthedesign ofempiricalstock-flowconsistentmodels. Levy EconomicsInstituteof BardColleWorkingPaper, 919.

29

A.1. Themodel

A.1.1. Production

A.1.1.1. Agriculture

Realdomesticagriculturalproduction (Y P,A , 1) issplitinthreecomponents:realagricultural productionfordomestichouseholdconsumption (Y P,A C ),forintermediateinputconsumption byothersectors (Y P,A IC ),andforexports (Y P,A W ).Allthreecomponentsofagriculturalproduction aredeterminedbyclimaticconditionsaswementionedaboveandarethereforeexogenous tothemodel.21

Asexplainedinthemaintext,weuseAdapt’ActionandFAOmodelsinordertoprojectthe productionlevelsofthesegoodsinoursimulationperiod.Wethensmooththeproduction pathsandcalculateconstantgrowthratesforeachcategoryofagriculturalproduction:

Aggregaterealdomesticdemandforagriculturalgoods (Y D,A , 5) iscomposedofreal consumptiondemand (Y D,A C , 6) fromhouseholds (CA) andrealintermediateconsumption demand (Y D,A IC , 7) fromprocessedfood (ICA PF ),NFCsectors (ICA NF ),theagriculturalsector (ICA A ) andthegovernmentsector (ICA G ).Weassumethatthedemandforexportsalways matchessupplyandthusrealexportsofagriculturalgoods (X A , 8) aregivenbytheexogenous supply (Y P,A W )

Inordertoproduce,theagriculturesectorusesintermediateinputsfromitsownproduction (ICA A ) ,fromprocessedfoodsector(ICPF A ) andfromothernon-foodsector (ICNF A ).The demandforthesegoodsinrealtermsaregivenbyfixedinput-outputcoefficients αA A,αPF A and αNF A .

Inwhatfollows,theproducersectorisdenotedwithasuperscriptandthedemandingsectorwithasubscript.

Y P,A = Y P,A C + Y P,A IC + Y P,A W (1)

Y P,A C = grypac Y P,A C (2) Y P,A IC = grypaic Y P,A IC (3) ˙ Y P,A W = grypaw Y P,A W (4)

Y D,A = Y D,A C + Y D,A IC (5) Y D,A C = CA (6) Y D,A IC = ICA A + ICA PF + ICA NF + ICA G (7) X A = Y P,A W (8)

ICi A = α i A · Y P,A,i ∈{A,PF,NF } (9) 21

30

Giventheconsumptiondemandbyhouseholdsandintermediateconsumptiondemand fromallsectors,theexcessdemandinagriculturesectorismetbyimportsfromtherestof theworld.Thus,importsofagriculturalconsumption (IM A C ) andintermediateconsumption (IM A IC ) aregivenby:

A.1.1.2. Non-financialsector

Theremainingnon-financialsectorsaredividedintotwosectors;aprocessedfoodindustry, denotedas PF ,andasectorthatproducesallprivatenon-foodgoodsandnon-financial servicesintheeconomy,denotedas NF .Processedfoodissoldtohouseholdsforconsumption (CPF ),exportedtotherestoftheworld (X PF ) anddemandedasintermediate consumptionbytheagricultural (ICPF A ),processedfood,(ICPF PF ),non-food(ICPF NF )andthe governmentsectors(ICPF G ).Similarly,thehomogeneousgoodproducedbythenon-food secrtorisdemandedforconsumptionbyhouseholds (CNF ),andintermediateconsumption byallsectorsincludingbanks (IC

).Wefurtherassumethatthis isthecapitalgoodoftheeconomy,purchasedforinvestmentbythenon-financialsector itself(processedfoodandnon-foodNFCsector, I NF F ),households(I NF H )andthegovernment (I NF G ),andexportedtotherestoftheworld(X NF ).Thustherealaggregatedemand(net ofimports)fortheoutputoftheprocessedfood(Y D,PF ,15)andtheNFCgood(Y D,NF ,16}) sectorsaregivenby:

,

), j ∈ (PF,NF ) denotetheimportsharesofelementsofaggregate demand,tobedefinedbelowand ICPF and ICNF arerespectivelythetotalintermediate consumptiondemandfortheprocessedfoodandnon-foodsectorgoods,and I NF ( 17) isthetotalcapitalinvestmentintheeconomygivenbythesumofsectoralinvestments ofagriculture(I NF A ),processedfoodandnon-foodNFCs(I NF F ),government(I NF G ),and households(I

H )

.

IM A C = Y D,A C Y P,A C (10) IM A IC = Y D,A IC Y P,A IC (11)

σA M,C and σA M,IC in

σ A M,C = IM A C /CA (12) σ A M,IC = IM A IC /ICA (13)

ICA = ICA i ,i ∈{A,PF,NF,G} (14)

Duetoourmarketclosurebyimportstosatisfydemand,importshares

agriculturearedefinedas:

wheretotalintermediateconsumptiondemandforagriculturalgoods(14)isthesumof demandfromallsectors.

NF A

ICNF PF , ICNF NF , ICNF G , ICNF B

Y D,PF =(1 σ PF M,C ) · CPF +(1 σ PF M,IC ) · ICPF + X PF (15) Y D,NF =(1 σ NF M,C ) CNF +(1 σ NF M,IC ) ICNF +(1 σ NF M,I ) I NF + X NF (16)

σj M,i

i ∈

C,IC,I

NF

31

,

where

(

22

22Wecombinethecapitalinvestmentofprocessedfoodandnon-foodNFCsectorsintoasingleitem I NF F ,aswe willdiscussbelow.

Asintheagriculturalsector,processedfoodandnon-foodsectorsuseintermediateinputs fromagriculture,processedfoodandnon-foodsectors.Intermediateconsumptiondemand functionsaregivenbythetechnicalcoefficientsandthelevelofproductionofthesesectors (Y P,PF and Y P,NF ).

Forthegovernment,realintermediateconsumptiondemandforfoodandprocessedfood dependsonpublicemployment(N G),whereasintermediateconsumptionofnon-foodsector goodsdependsonpubliccapîtalstock(KG):

Thus,totalintermediateconsumptiondemandforprocessedfoodandnon-foodsectorgoods are:

Thegoodsmarketsarecharacterizedbydisequilibriasuchthataggregatedemandlessof imports(Y D,PF or Y D,NF )isnotnecessarilyequaltototalproduction(Y P,PF , Y P,NF ).Firms formadaptiveexpectationsonrealexpecteddemandforprocessedfood(Y e,PF ,25)andthe NFCgood(Y e,NF ,26):

where αpop isthepopulationgrowthrate,

isthegrowthrateofcapitalstockinthe totalNFCsector,and βPF y and βNF y aretheadjustmentspeedsofexpectationstoexcess demand,specifictoeachmarket.Thus,thetrendrateofgrowthintheprocessedfood

I NF = I NF A + I NF F + I NF G + I NF H (17)

ICi PF = α i PF Y P,PF ,i ∈{A,PF,NF } (18) ICi NF = α i NF Y P,NF ,i ∈{A,PF,NF } (19)

ICi G = α i G · N G,i ∈{A,PF } (20) ICNF G = α NF G KG (21) whiletheintermediateconsumptionofbankingsectorofnon-foodNFCgoods(ICNF B )isa functionofsector’semployment(N B ): ICNF B = α NF B N B (22)

ICPF = ICPF A + ICPF PF + ICPF NF + ICPF G (23) ICNF = ICNF A + ICNF PF + ICNF NF + ICNF G + ICNF B (24)

˙ Y e,PF = βPF y (Y D,PF Y e,PF )+ αpop Y e,PF (25) Y e,NF = βNF y (Y D,NF Y e,NF )+( KF KF ) Y e,NF (26)

KF KF

32

sectorfollowspopulationgrowthrateandthatofthenon-foodNFCsectorfollowscapital accumulation.

Bothprocessedfoodandnon-foodmarketsareindisequilibriumsuchthatproduction(Y P,i) doesnotnecessarilyequaldemand(Y D,i).Themarketdisequilibriumateachpointintimeis clearedbyinventory(dis)accumulationinbothmarkets(V i,27).

Theproductivesectornotonlyproducestomeetexpecteddemand,butalsotoensurethatit hasthedesiredlevelofinventoriesdefinedin(28).Thisproductionforinventoryreplacement isgivenbyanadjustmentequationtothedifferencebetweenthedesiredandtheactual inventorylevelforeachmarket(I i V ,29):

Y P,i , 30)ineachsectoristhenequaltothesumofexpectedreal demandandproductionfordesiredinventoryreplacement.

Employmentinthenonfood(N NF , 31)andprocessedfood(N PF ,32)sectorsaredetermined viaaLeontieffproductionfunction,withsectorallabourproductivitylevelsgivenby aPF and aNF respectively.

Realimportsofprocessedfood(IM PF ,33)andthenon-foodgood(IM NF ,34)dependon thedifferenttime-varyingimportpropensities(σi M,j ,i ∈{PF,NF },j ∈{C,IC,I })outofreal levelsofconsumption,intermediateconsumptionandinvestment.Inaccordancewiththe data,weassumethattheprocessedfoodisnotusedforinvestmentandthusnotimported forthispurpose.

Thecorrespondingnominalimportsofprocessedfood(IM PF N ,35)andtheNFCgood(IM

, 36)aredefinedas:

V i = Y P,i Y D,i,i ∈{PF,NF

(27) Weassumethatfirmshaveadesiredinventory(

des,i

αi V . V des,i = α i V .Y e,i,i ∈{PF,NF } (28)

}

V

, 28)toexpectedsalesratiogivenby

I i V =Ωi V · (V des,i V i),i ∈{PF,NF } (29) Totaldomesticoutput(

Y P,i = Y e,i + I i V ,i ∈{PF,NF } (30)

N NF = YpNF /a NF (31) N PF = YpPF /a PF (32)

IM PF = σ PF M,C · CPF + σ PF M,IC · ICPF (33) IM NF = σ NF M,C CNF + σ NF M,IC ICNF + σ NF M,I I NF (34)

NF N

IM PF N = pPF,w e N (σ PF M,C CPF + σ PF M,IC ICPF ) (35) 33

where pPF,w and pNF,w aretheworldimportpricesofprocessedfoodandnon-foodgood respectivelyand eN isthenominalexchangerate.Thepropensitiestoimportmovetowardsthe targetimportpropensities(σi,Tar M,j ,37),whicharenegativefunctionsofsector-specificrelative prices,importtaxes (τ i M,j ) andtheelasticityofsubstitutionbetweenimportedanddomestic goods( j 1,i).Aswellasrelativeprices,thetargetpropensitiesalsodependonrelativelabour productivityofTunisia (takenastheproductivityinthenon-foodsector, aNF ) withrespectto itstradepartners(aW ),whichcapturesnon-pricedeterminantsoftradecompetitiveness. Thespedofadjustmenttothetargetpropensitiesisgivenby βi M,j in(38)23 .

Processedfoodexports(X PF )dependontheabilityoftheagriculturalsectortoprovidethe necessaryintermediateconsumptionandthereforegrowatanexogenousrategivenby theclimateandadaptationscenarios(39).Exportsofthenon-foodgood(X NF ,40)onthe otherhandaredeterminedbytheexogenousworldGDP(GDP W )andatimevaryingexport propensity(σNF X ),whichdependsonrelativepricesandrelativelabourproductivityasabove: Aswithimportshares,theexportpropensityadjuststoitstargetvalueslowly,witharelaxation speedof 1/βNF X

A.1.2. Pricing

Thereareseventeendifferentpricesforgoods,theseareeitherdenominatedindomesticor foreigncurrency:

• Producerprice(pi P )foreachproductindomesticcurrency, i ∈{A,PF,NF }

• Consumerpriceforeachproduct(pi C )indomesticcurrency, i ∈{A,PF,NF }

• Intermediateconsumptionpriceforeachproduct(pi IC )indomesticcurrency, i ∈ {A,PF,NF }.

23Aswementionedabove,processedfoodgoodsarenotusedforinvestmentandthus σPF,Tar M,I =0 and σPF M,I =0 Wethusexcludethisvariablefromourlistofvariablesandoursimulations.