08 Bad practices and over-reliance on govt has made Pakistani agriculture volatile and uncompetitive. It doesn’t have to be.

14 The bull case for Pakistan

24 Pakistan has a serious taxation problem. Its answer is in the constitution

28 Getting to the root of the subsidy addiction

34 A major multinational has been fined Rs 6 crore for deceptive marketing of their soap. They aren’t the only ones

38 Pakistan is in the midst of an investment winter. Could Patient Capital be the way out?

44 It’s been a great year for the stock market. Was it for real?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Bad practices and over-reliance on govt has made Pakistani agriculture volatile and uncompetitive. It doesn’t have to be.

It is a very simple equation. Pakistan has a set amount of land (possibly shrinking) and a growing population. That means we need to grow more food on less land

By Abdullah Niazi

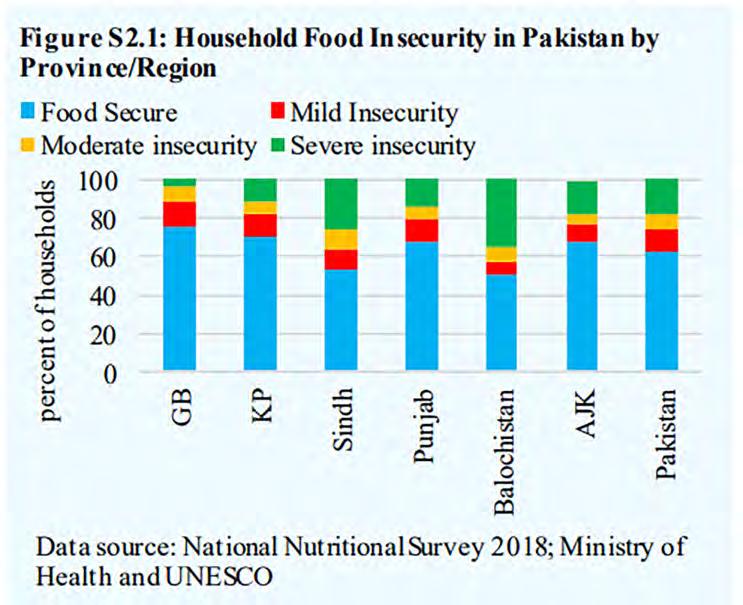

Pakistan is food insecure. This means that people can’t access the food they need to live their fullest lives. Even though a lot of households might have access to food, there is a severe lack in the quality and quantity which leads to issues of malnutrition and a population that is growing weak, unhealthy, and inefficient.

This is despite the fact that Pakistan is ranked 8th in producing wheat, 10th in rice, 5th in sugarcane, and 4th in milk production. Even these figures are there thanks to Pakistan’s land being arable, its farmers being seasoned experts in staple crops, and there being enough room and fertility in the land to grow these crops despite the lack of farm mechanisation.

It is a sad state of affairs, but there is an opportunity to be found in this. Pakistan has the basic building blocks to let agriculture thrive. But to get to this point, we need to begin by understanding the scale of the problem, identifying the key factors that hold this country’s agriculture back, and mapping a clear path of action that does not involve the government.

Food insecurity is killing us

In 2019, the State Bank of Pakistan (SBP) released a report with alarming data on food insecurity in the country. The report claims that nearly 37%

of households in Pakistan are food insecure. In the five years since the SBP’s report, matters have only worsened. Food price inflation in Pakistan has been in double digits since August 2019. The cost of food has been 10.4-19.5% higher than the previous year in urban areas and 12.6-23.8% in rural areas, according to figures published by the Pakistan Bureau of Statistics.

So how does a country with one of the largest agrarian economies in the world find itself unable to sufficiently provide food for nearly 40% of its population? For decades, agriculture has been neglected and people’s earnings have been hit by one economic crisis after another. On top of this, particularly in the past decade or so, climate change related disasters and changes in the environment have resulted in our already neglected agriculture becoming less competitive.

It sounds baffling that a country with the capability of producing food sufficient not just for itself but also to export would be facing food security issues. Despite the fact that Pakistan produces vast quantities of major staple and nonstaple food crops, the state of food security in the country is inadequate.

According to the UN’s Food and Agriculture Organization (FAO), the concept of food security is flexible, but is widely believed to “exist when all people, at all times, have physical, social and economic access to sufficient, safe and nutritious food which meets their dietary needs and food preferences for an active and healthy life.”

In short, for a country to be considered food

sufficient it does not just have to produce a sufficient amount of food, but that food should be easily available, affordable, and of a quality that meets basic nutritional requirements. For a reliable level of food security, it is vital that the access and affordability of food is not affected by shock events such as floods and economic crises that result in inflation. The concept is not difficult to grasp, but it is so simple that it often gets lost in the cracks. Food is the most basic building block of human life. The quality and quantity of caloric intake of a population affects its overall productivity, standard of living, and most importantly happiness and satisfaction.

While access to food is a basic, fundamental human right there is a way to put an economic cost on food insecurity. The lack of food security has strong economic implications. According to a special section of the SBP’s annual report from 2019-20, the state of food security has strong linkages with the state of human capital in the country. The Food and Agriculture Organisation of the United Nations has also estimated that a high rate of malnutrition can cost an economy around 3-4% of GDP. In the case of Pakistan, estimates suggest that malnutrition and its outcomes cost the economy 3% of GDP (US$ 7.6 billion) every year.

To put this in very mathematical terms, malnutrition and food insecurity manifests in the shape of high child mortality rates, prevalence of zinc and iodine deficiencies, stunting, and anaemia, which lead to deficits in physical and mental development that weakens labour productivity and loss of future labour force in the country.

On a much more human level, however, the lack of food security means a whole lot of misery, hunger, and anguish. According to the State of Food Security and Nutrition in the World report for 2023, nearly 10.5 million people (29 percent of the population analysed) are experiencing high levels of acute food insecurity between April to October 2023. The last detailed report on the issue came out in 2021, and that indicated the prevalence of undernourishment in Pakistan is 12.3% and an estimated 26 million people in Pakistan are undernourished or food-insecure. Pakistan’s children have suffered and are continuing to suffer. Malnutrition from an early age results in consequences that last entire lifetimes. Add on top of that a high population growth and unfavourable water and climatic conditions and you have a scenario that threatens to spill over and cause mayhem. Pakistan is barely maintaining its current food security level of just over 60%. According to the SBP report mentioned earlier, “of the 36.9 percent of the households in Pakistan labelled as “food insecure”, 18.3 percent face “severe” food insecurity.”

Imports, R&D, and climate change

So what exactly is holding our agriculture back? There is of course the reality of government interference and incompetence that we will not get into at this stage. But if Pakistan was an open field and a large corporation was coming in to farm on it, what would be the issues they would have to tackle?

Imports

This is the first one and a big one. Despite being a large producer of food, Pakistan will need to import certain foods no matter what because they simply cannot be grown in Pakistan. akistan produces a lot of its food on its own. When it comes to vital crops like sugarcane, wheat, and rice farmers are regularly backed by support prices and manage to produce enough to export as well. However, some of our most basic caloric inputs are imported with very little attention being paid to growing them domestically. And there is no example more pertinent than oilseeds.

Oilseeds is a term used to describe any kind of seeds or plant product that can be compressed to extract and produce oil for cooking – basically the raw product for edible oil. Oilseeds have two purposes. The first is to produce edible oil for cooking purposes. The other is to produce ‘meals’ using the mulch and byproducts of the compression process that

are then fed to livestock including poultry and cattle.

In Pakistan, nearly 90% of the import of oilseeds is constituted by palm and soybean oilseeds. In its recently released report for the first quarter of the FY 2021-22, the SBP included a special section on rising palm and soybean imports. According to the report, Pakistan’s palm and soybean-related imports stood at US$ 4 billion in FY21, rising by 47% year-onyear, compared to compound average growth of 12.3% in the last 20 years. Pakistan’s reliance on these two oilseeds is not out of sync with global trends, and some of the largest producers of canola and sunflower – which are the third and fourth most consumed vegetable oils in the world – still rely heavily on palm and soybean.

Now, these seeds cannot be grown locally. Canola, sunflower, cotton and mustard seeds are indigenous to Pakistan and easily grown, but soy and palm still make up an important chunk particularly for the poultry industry. The issue here is less about finding alternatives and more about being able to trade, which means Pakistan needs crops that they can produce in massive numbers and export to the world and get whatever we need in exchange. This requires dedicated efforts and a huge focus on research and development, which brings us to our next issue.

Research and development

R&D. It is a buzz-term that you will find everywhere in organisations, think tanks, and

government departments. But in the field of agriculture, it is an oft touted but rarely implemented mantra. One of the most important things to understand is that as the world’s population has grown, more land has had to be brought under cultivation to meet humanity’s caloric needs.

And as the world has progressed, this has required a serious scientific approach. Research in the field of agriculture has led to mechanisation of farms, the development of seeds that give higher yields and are more resistant to different weather conditions, and areas before thought uncultivable have been turned into rich sources of food. The primary role of agricultural research is to heighten knowledge and improve technology. It heightens understanding of the interactions and interdependence between production systems and farming communities. This requires a holistic and interdisciplinary approach to problem identification, analysis and solution-finding.

This has been entirely missing in Pakistan. A major reason for the food price inflation in recent times are increasing input costs for agriculture over the past two years. Higher fuel prices and the devaluation of the rupee have led to a rise in costs in both fertiliser and seeds. Prices increase more in rural areas because commodities are diverted to cities due to higher profit margins, and because of the higher cost of imported items such as pulses and cooking oil.

Some of these situations are largely out of the control of farmers and provincial agricultural departments. However, low yields and production losses due to climatic changes have also had a detrimental impact on commodity prices. These factors could have been avoided if Pakistan had robust agricultural research organisations focused on producing better quality seeds, providing farmers with better techniques, and tailoring solutions for different regions. While organisations such as the Pakistan Agricultural Research Council (PARC) do exist, their role is vastly underplayed. Until a scientific approach can be taken to try and resolve the issue, there is very little that can actually be done.

As things stand, Pakistan may face an issue of even self-sufficiency in the coming years. And even if we manage to stay sufficient, that does not guarantee food security. A country is considered food secure if food is not only available, but is also accessible, nutritious, and stable, regardless of its origin. Pakistan provides support to its farmers on various levels, particularly when it comes to crucial crops such as wheat. However, even this may become difficult.

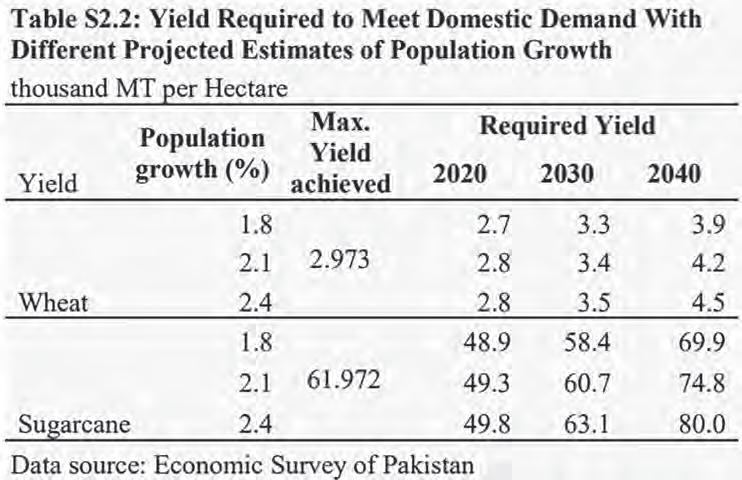

According to the SBP special report, land extension is not an option anymore

for Pakistan, and in the presence of current cropping practices, water shortages and expected climatic changes, it will be challenging to improve yields substantially. This means Pakistan’s best bet is to invest heavily in research and development in the hopes that we can produce research that allows us to grow high-yield crops with a tolerance for rapidly changing climate conditions. And that is what brings us to our next time-bomb, and perhaps the biggest one there is — climate change.

Climate change

This one is the Big Kahuna, and we need not look beyond the events of the 2022 floods. Climate change in Pakistan is a ticking time bomb that has already gone boom. If there was need for any other proof, then all you have to do is look at the disastrous flooding we saw less than two years ago. The water ravaged millions, destroyed crops, levelled entire villages, displaced 33 million people, and caused an estimated $40 billion in damages all over the country.

Climate change has resulted in a gargantuan increase in the amount of monsoon rainfall that Sindh and Balochistan have seen this year. The two provinces saw the highest amount of water fall from the skies in living memory, recording 522% and 469% more than the normal downpour this year according to the met department.

The effects are devastatingly clear. Pakistan was hit with a major wave of climate-change related activity that resulted in death, destruction and total annihilation in some areas. And this will by far not be the only time the issue strikes us. According to UNESCAP, Pakistan could lose more than 9% of its annual GDP due to climate change. Severe heat waves and untimely rains have also severely impacted Pakistan’s agricultural production. The Intergovernmental Panel on Climate Change has warned that the frequency of such extreme weather conditions will increase in the future, causing a severe risk to Pakistan’s food security. The Asian Development Bank projects sharp declines in key food and cash crops (such as wheat, sugarcane, rice, maize, and cotton) in the coming years due to rising cultivating costs and climate change. And the problem is all encompassing. On the one hand, there is increased rainfall and erratic weather patterns that our farmers are unable to keep up with because they do not have the resources to do so. On the other hand, there is a much more critical hold that changing weather patterns have on the jugular vein of Pakistan’s agriculture.

In addition to the many historic reasons for the state of the Indus River, climate change is causing direct consequences already, adding another layer of complexity to an already troublesome issue. What is clear is that the early effects are already visible. In an arti-

cle published in the journal for Global and Planetary Change, a report on the state of the Tibetan Plateau published a few years ago reads that the region has faced “evident climate changes, which have changed atmospheric and hydrological cycles and thus reshaped the local environment.”

To put that into perspective, more than 1.4 billion people depend on water from the Indus, Ganges, Brahmaputra, Yangtze, and Yellow rivers which are fed by these water towers. Without an effective policy on how to manage and handle this crisis, Pakistan does not stand a chance on the food security front.

Jo Banain Gai, Khain Gai

This is what it all comes down to. Allow us the liberty here to divert from agriculture for just a moment.

For a very long time, Pakistan has been in a bad relationship with debt. And like all toxic relationships, it is a boom-and-bust cycle of taking a loan at a bad time, getting into bad habits, having a falling out, pretending to go through a period of change (symptoms may include political instability, jingoism, and reliance on religious symbolism), before finally becoming desperate enough to once again go back to the debt equation.

Pakistan faces severe external financing challenges with rampant domestic political instability and higher rates in developed markets hitting capital inflows on the one side, while on the other rising commodity prices pump-up the import bill to unsustainable levels at a time when the country’s largest export markets in advanced economies are facing recession.

What that means, essentially, is that as prices rise on the global market Pakistan is left vulnerable. Since we rely majorly on exports, we need more dollars at home to buy commodities. And since the American federal reserve is in Washington and not Karachi, the only way to get those dollars is to earn them by selling our products on the international market.

This is what it boils down to. The simple fact is that in the absence of borrowing all we are left with is what we as a nation can produce. This means that all the accountants, journalists, marketing professionals, video editors, HR managers and other members of the services industry are useless to what we can call the very basic core of what we as a nation must produce. So what

does that leave us with? This is a very basic economic equation but at the end of the day, what we produce we consume ourselves and then send the excess of our production to the world to earn dollars and trade with other countries and get products we can’t produce as imports. Our manufacturing sector and our agricultural sector produce the goods that we can consume. And that is our little segue back into agriculture. Jo Banai Gai, Khain Gai. What better thing for an agrarian food insecure country with a reliance on certain imported foods to make than more food?

Pakistan’s manufacturing industry has a long way to go to be competitive on the international market. But perhaps one of the fields in which Pakistan has the potential, the raw materials, the space, and the natural inclination to succeed is the agriculture sector. And more importantly than that, for a food insecure country like Pakistan, focusing on agriculture gives us the added advantage of regaining our food security and self-sufficiency.

Pkistan’s agriculture has suffered from a lack of attention for decades. The country’s natural resources, soil fertility, and robust rivers have kept Pakistan in the running as a solid agrarian economy for almost its entire existence. However, shortsightedness has meant that successive governments have been very comfortable allowing things to run as is without investing in the future. As the population has increased, climate change has dug in its claws, and water scarcity has started hitting farmers, it is quickly becoming apparent that we have fallen behind. Immediate attention is needed, but only time will tell whether decision makers realise the urgency before it is too late. After all, this is not a question of just our agriculture. It is a question of what we are willing to do to thrive. n

The bull case for Pakistan

WHY, DESPITE ALL THE NEGATIVITY, THE FUNDAMENTALS OF THE COUNTRY’S ECONOMY ARE ABOUT TO HIT A POSITIVE TIPPING POINT, FOLLOWED MOST LIKELY BY A MULTI-DECADE BOOM

By Farooq Tirmizi

If you read about Pakistan’s economy, you have probably – at some point – felt some optimism about Pakistan’s prospects as a country. Just as equally likely, you have probably felt that optimism fading away some time over the past 2-3 years, if not even earlier. It is our contention that you were not wrong to feel that optimism. You saw something real. And it is still there.

This article is not a pie-in-the-sky optimistic view of Pakistan that believes in stupid things like “if the government were to solve these problems, we would be prosperous.” No, our view of Pakistan’s economy is that for it to be successful, the ingredients that make it successful need to be idiot-proof. Because the only logical assumption is that Pakistan will continue to be run by idiots for decades to come.

What we describe below, therefore, is a view of Pakistan’s economy that does not expect the government of Pakistan to do anything to help the economy at all. Indeed, we go so far as to assume that the government of Pakistan will continue its destructive ways and that the growth we describe will simply have to make room for that destructive behaviour.

Luxuries like “political stability” and “a conducive environment for foreign investors” are not factors we will be listing in our bull case for the Pakistani economy.

We do not, however, have a completely cynical view of the government. It is not as though the government of Pakistan does nothing right. It is just that it tends to find the most inefficient ways of doing the right thing, starts doing them decades after other countries, and makes slower progress. We do not anticipate any of that changing any time soon.

This article is the fourth in a four-part series we have been publishing over the past few weeks. It tackles the fourth in what we think will likely be the four key ingredients of Pakistan’s ability to capitalize on its demographic dividend. The four ingredients are:

1. Electricity generation, which needs to be above 500 kilowatt-hours per person per year in order for the country to have enough electricity to begin the industrialisation process;

2. Stabilising fertility, which means having a fertility rate below 3.0 in order to have the right balance of dependents and working age adults in the population to work, save, and grow the economy;

3. Sufficient literacy, specifically meaning adult literacy above 70% in order to have a workforce that can do basic skilled tasks in industrial settings, and educate their children to move even further up the value-chain

4. Sufficient domestic savings, specifically a domestic banking sector large enough to result in relatively lower costs of capital.

Every country that has industrialised over the past 75 years has had all three of the first of these characteristics come together at the same time (the fourth one is an almost inevitable byproduct of the second two). Many countries that did not have these characteristics come together are very likely to have missed the boat on industrialization – and therefore creating a mass middle class – entirely.

You would think that Pakistan will be in that second category of countries, because that is how our luck seems to run. Call it Murphy’s Law of Pakistan’s political economy: any bad thing that can happen to a country usually does happen to Pakistan.

Except, you would be wrong. Pakistan has already achieved the first milestone, and is on track to achieve the second two by some time early next decade, and possibly as early as 2030. And it will do so in a manner that is almost immune to government actions, meaning Pakistan’s politics can continue to be the dumpster fire that it is and we will still hit each of those three milestones at the same time, meaning we will – just barely – be able to make it to becoming one of the lucky countries that is able to capitalise on its demographic dividend.

What follows is a summary of how the first three ingredients were put in place (we already covered them in three previous editions), as well as how the fourth one will answer the question: “but how will we achieve economic progress without political stability?”

We will, because there is no set pattern to political stability and economic progress. Some nations achieve political stability, and then economic progress. Some attain economic progress first, then political stability. Clearly, we are the second type of country.

But first, a recap of the previous three stories, told through the lens of how they put in place each of the necessary pillars of economic progress.

Electricity availability

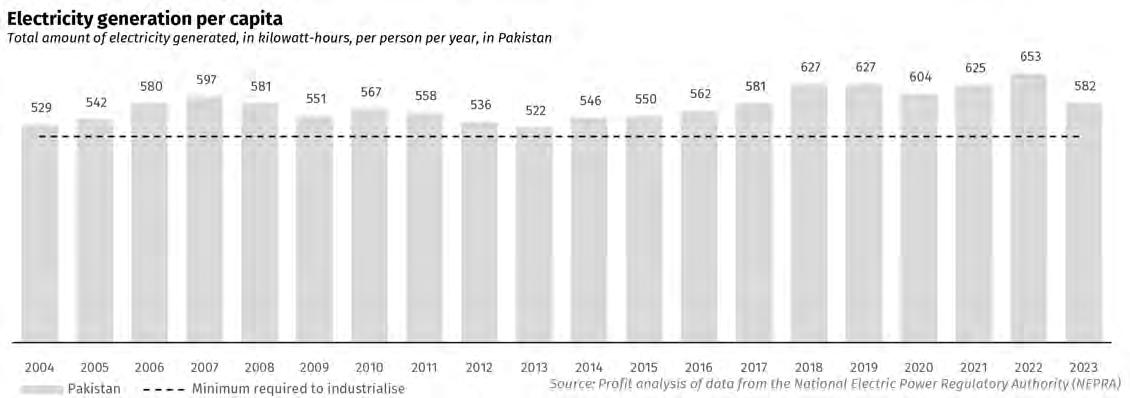

This is the one area where the government of Pakistan has taken meaningful action, though perhaps in the most inefficient way imaginable. Here is the punchline: for any country to industrialise, it needs to have electricity generation (not just capacity, but actual generation) of above 500 kilowatt-hours per person per year, according to research by Charles Robertson, an economist at FIM Partners, a London-based investment firm, and author of the book The Time Traveling Economist.

Pakistan has been at that level since at least 1999, though it helped that in the third Nawaz Administration from 2013 to 2018, Pakistan expanded its power generation capacity by a lot – actually, by too much.

The debt and capacity payments from that building spree are an issue, to be sure, but most crucially, if we are going to take on debt like we always do, at least this time it was for an investment in the future productivity of the country. In purchasing power terms, this is the most expensive electricity will likely ever be in Pakistan, and costs are likely to decline as more and more consumption means less and less of your bill needs to go to pay for capacity payments. That will – eventually – reduce the per unit cost, at least in inflation-adjusted terms, over time.

You cannot build prosperity in a country without a mass middle class, and you cannot build a mass middle class without industrialization, which in turn is impossible without sufficient electricity. On that front, at least, Pakistan appears to have what it will take.

Stabilising fertility

This factor is perhaps the most under-appreciated: family size in Pakistan is getting smaller, because more and more women are choosing

to have fewer children. So long as we do not overcorrect and start having too few children, this factor alone is an important driver of economic growth even if nothing else happens.

This fact is best illustrated with an example: suppose you have a family with a husband and wife and six children, the oldest of whom is 10 years old. The husband works for a minimum wage job bringing in Rs25,000 a month and the wife works as a domestic worker, bringing in maybe another Rs15,000 per month. That’s a Rs40,000 per month income spread over an 8-person household, or Rs5,000 per person per month. Now suppose they had just three children instead of six: that same income gets spread over five people, meaning Rs8,000 per person per month.

Where is that extra Rs3,000 per person per month going? More food, so probably less malnutrition. And more education, so the children will have a higher income than the parents.

Note that we did not add education or higher earning ability of any kind to either parent in that household. Just by reducing the number of children, their economic situation improved, thereby improving the economic wellbeing of the country as a whole.

The scene we describe above has been happening across Pakistan since 1990. Right now, the average Pakistani woman has 3.3 chil-

dren, down from 6.0 as recently as 1992. This has the effect of increasing the proportion of the population that is part of the labour force, which improves household economic conditions. And in Pakistan, at least, it has been a precursor to rising human capital levels.

As state above, countries that are able to go below 3.0 in fertility begin to have the kind of rising domestic savings and rising literacy to attempt industrialisation. There is no such thing as an industrialised country with 6-children families as the norm.

Rising literacy

Talk about the advantages of a larger population and most Pakistanis’ first objection will be pointing out that most of that population is illiterate, or at least badly educated. We would like to point out two things: firstly, the majority of the population in Pakistan is now literate, and every successive generation is better educated than the previous one. And secondly, while it would have been better had they had a good education, this is Pakistan’s first majority-literate generation, and basic literacy may be sufficient for now (emphasis on “now”; it will not be enough in the long run).

In urban areas in Pakistan, particularly in Punjab, we now have near-universal youth

literacy, and the gender gap has almost completely closed. This has been made possible almost entirely due to the previous factor we just described: smaller family sizes means that each household has more money to spend per child, and a majority of Pakistani households are choosing to use those extra resources to educate their children.

Overall, adult literacy rates in Pakistan are just above 60%, which is below the 70% that economists like Robertson believe is the minimum required level to start industrialising, but in urban Pakistan, where that industrialisation is likely to begin, adult literacy is above 70% and youth literacy is above 90% in most major cities. Perhaps most promisingly, the youth literacy rate for boys in urban Punjab, where over half the population lives, is only 1% higher than that for girls.

While part of this progress is certainly driven by improvements to the government’s own infrastructure, measured purely by proportion of the increase in student enrollment, the private sector has contributed just under 75% of the total growth in enrollment between 2009 and 2022, according to enrollment estimates published in the Pakistan Education Statistics reports published by the Pakistan Institute of Education. The public sector accounts for the remaining 25%.

In other words, Pakistanis are not

waiting around for the government to fix the schools (even though the government is making some progress on that front). They are simply going ahead and paying for private schools themselves as soon as they have the ability to pay. And they have that ability to pay just because the earlier, illiterate generation had fewer children.

As we have argued before, education in Pakistan is not good. But it might finally be good enough for us to get started on the path to prosperity.

Put these three ingredients together, and you get the fourth one, the one that will make this all immune to government stupidity: rising domestic savings.

Rising domestic savings

It bears repeating: any model of economic growth and prosperity for Pakistan cannot rely on some magical reforms undertaken by the government because the absolute fecklessness of Pakistan’s ruling elite simply cannot be counted upon to change in any predictable time frame. But Pakistan’s upward march towards industrialisation will happen because the government’s failures will be neutralised.

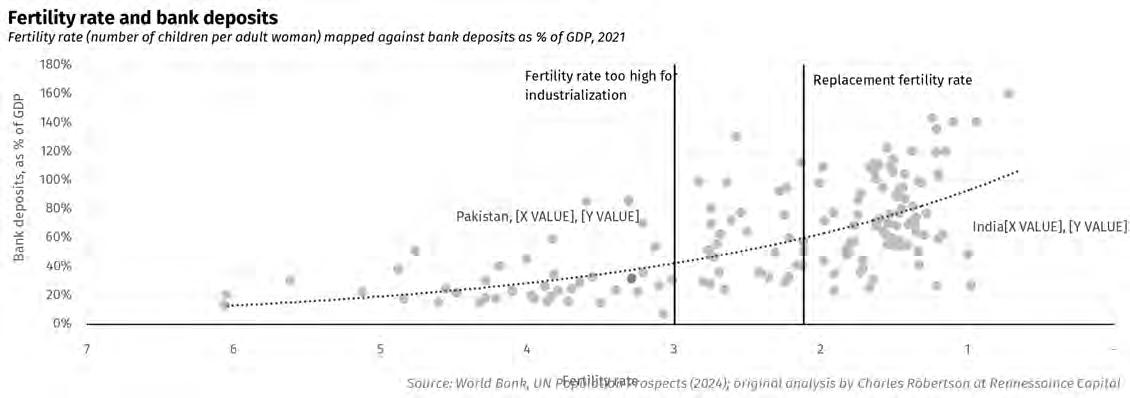

That will happen when Pakistan’s bank

deposits rise from the roughly 32% of gross domestic product (GDP) they are right now to the roughly 50-60% of GDP they will be by around 2035. Why will bank deposits rise that fast? Because when a country crosses the tipping point of 3 children per adult woman, it sees what is typically the sharpest increase in its bank deposits as a percentage of GDP.

According to research by Robertson, an economy that has between 3-4 children per woman has deposits equal to an average of about 30% of GDP, which is very close to the number Pakistan is at right now. When it goes below 3 children per woman, it sees a rapid increase in its household ability to save, and bank deposits as a percentage of GDP effectively double to about 60% of the total size of the economy.

Pakistan will hit that tipping point sometime around 2030, at which point the rise in deposits is likely to be quite rapid. Crucially, this is the kind of change that is already baked in and the government can do almost nothing to mess it up.

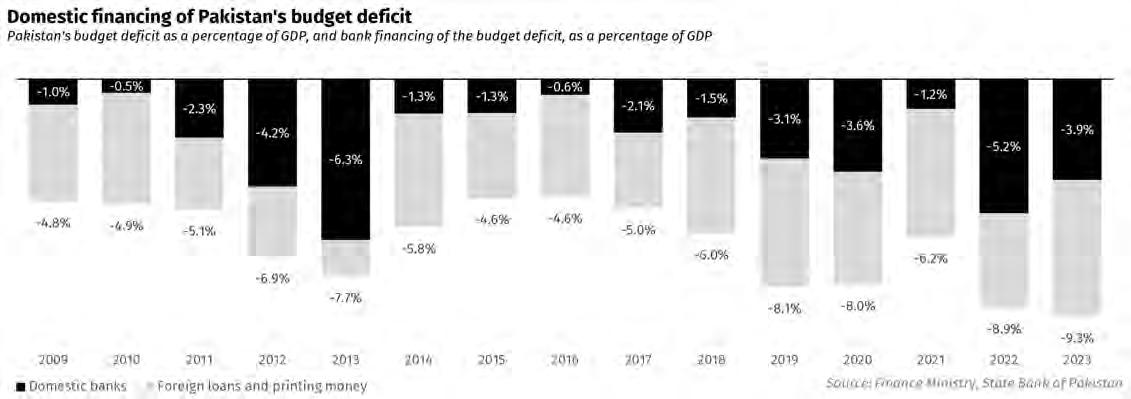

This matters because, while there are many ways the government of Pakistan is dysfunctional, the one that harms the economy the most is the fact that it persistently runs very large fiscal deficits relative to the total size of the economy, or GDP. The government does this because Pakistani politicians are a notoriously bad at determining what is a good or bad use of government money.

Over the course of a business cycle, Pakistan’s budget deficit tends to clock in at about 6% of GDP per year. Financing that from domestic savings with bank deposits equaling just 32% of GDP is effectively impossible, which is why the government does two things that are both inflationary:

1. It borrows from outside the country, which causes the currency to weaken whenever repayments are due, which causes inflation.

2. It simply prints the money.

But what would happen if you needed to finance a 6% of GDP budget deficit with a bank deposit base that was equal to 60% of GDP? You would have a much easier time being able to do so.

Over the past 15 years, the government of Pakistan has run a fiscal deficit equal to an average of about 6.4% of GDP per year. It has financed just under 41% of that deficit from bank borrowing, with the bulk of the remainder coming from foreign borrowing or printing money. This borrowing represents an average of about 8.2% of the banking sector’s deposits in any given year.

Sure, the government could try to reduce its frivolous expenses like the bailouts of loss-making state-owned companies, and it could tax the untaxed sectors of the economy. But that would involve an improvement in the quality of our government and we at Profit simply do not believe in that. So instead, we assume this level of borrowing will remain the same over the course of any business cycle.

Now imagine what happens if Pakistan’s banking sector is larger, at around 60% of GDP. Apply that same 8.2% of banking sector deposits as being a sustainable path towards deficit financing, and you get the banking sector being able to comfortably finance a budget deficit of about an average of 5% of GDP, leaving an average of about a 1.4% of GDP deficit per year over the course of a business cycle that needs to be financed by foreign borrowing or printing money. That is a much more manageable number.

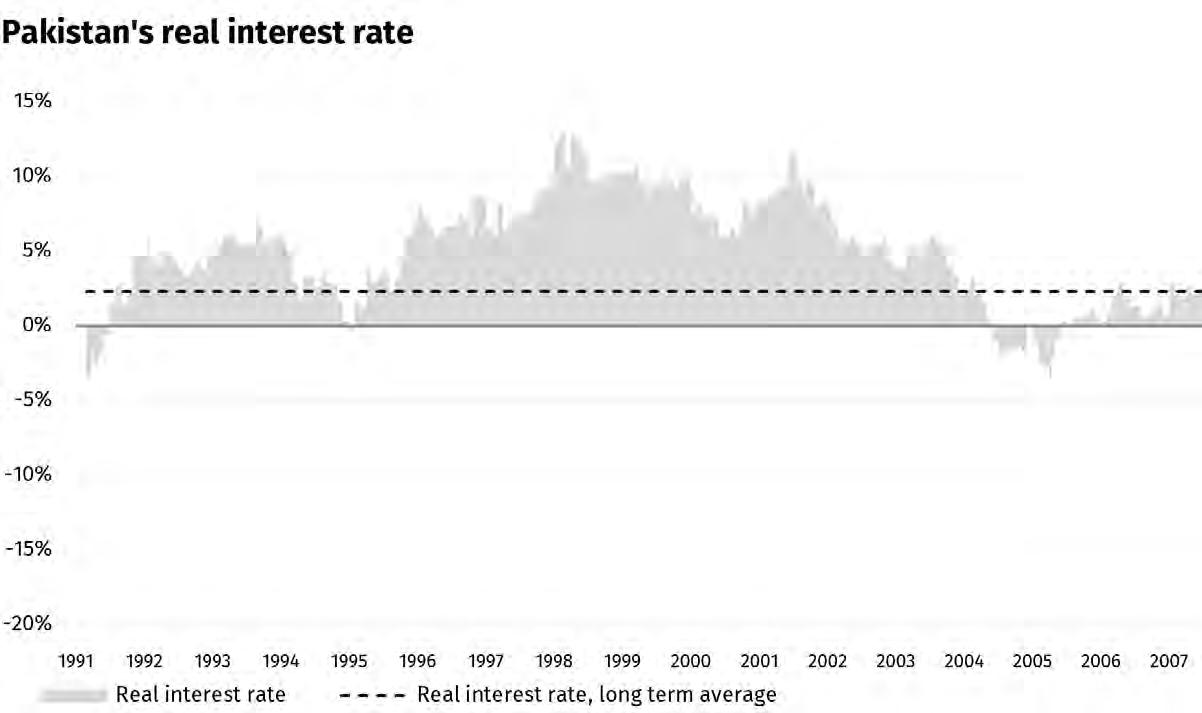

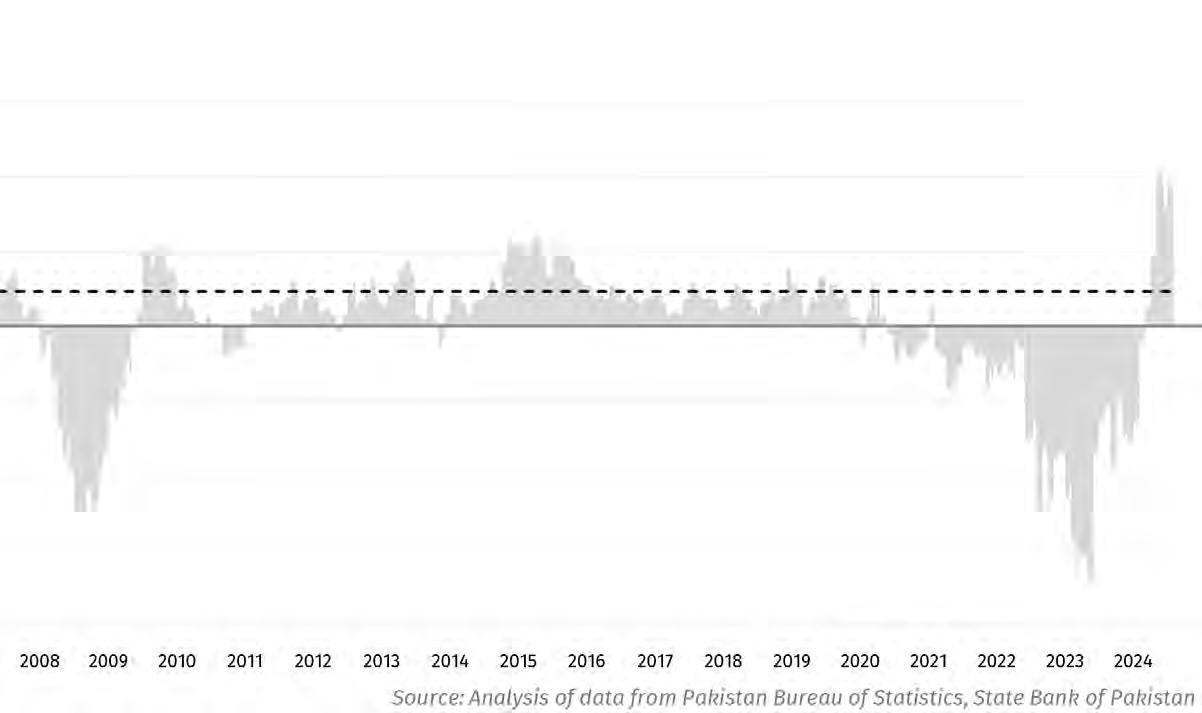

But, see, the progress does not simply end there. Because once the government can finance the bulk of its deficit from domestic bank deposits, it will not need to print as much money, which in turn will cause a long-term reduction in the inflation in the economy, which currently averages 8% per year. A reduction in the interest rate will spark a reduction in the government’s own cost of

borrowing, which currently averages over 10% per year for its long-term bonds, implying an average 2% real interest rate.

Two things are likely to happen once the government starts financing the bulk of its deficit domestically: the inflation rate is likely to start coming down, and is likely to vary a lot less than it does (that 8% average is hiding the fact that inflation swings from as low as 4% to as high as 35% over the course of a business cycle). Inflation will be both lower, and will likely swing more narrowly than it currently does. That will reduce the government’s cost of borrowing, which will reduce its need to borrow in the first place, reducing further its need to print money, further reducing the fiscal drag on inflation.

And since the fiscal deficits will be lower, the government’s need to borrow from foreign lenders – which creates this artificial cycle of currency stability followed by crashes in the exchange rate – will also decrease both in intensity and frequency. We might – just maybe – be able to say good bye to the International Monetary Fund (IMF).

Pakistan’s current account deficit tends to be around 1% of GDP in years when the government leaves the exchange rate alone and stops trying to artificially prop it up. That level of current account deficit will probably still cause the Pakistani rupee to continue depreciating – but probably much more slowly than the current average of over 7.5% per year.

Notice that all of this positive shift is likely to happen with absolutely no improvement in the behaviour of the government with respect to its fiscal prudence.

Other countries – with governments that are capable of getting their house in order – would use the increased domestic capital to allow businesses to finance their growth, and further increase the economic growth potential of their economies. That will likely not happen in Pakistan.

But what will happen is that the people will have collectively developed more capacity to absorb the pain that comes from the government’s refusal to fix itself, and we will be able to get on with our lives.

Once the country’s economy has a lower (not low in absolute terms, but low relative to current levels) and more predictable level of inflation, the cost of borrowing for businesses is lower, and they have a literate workforce and a reasonably plentiful supply of electricity, they can begin the work of industrialising the economy in earnest.

Yes, the government will continue to harass legitimate businesses, will continue to tax what it can and not what it should, and will continue to be capricious in its rulemaking activities. But all of those are much more manageable problems to deal with. Aggravating, to be sure, and the country’s economic growth would increase if the government were to improve its delivery of services to its citizens, but at least it would no longer be as regularly debilitating as it is now.

Here is the truly important part: once

this boom starts, it will likely continue almost uninterrupted for at least three to four decades. Meaning for anyone who was born in the 1990s or later, they will experience nearly the entirety of their careers in a booming Pakistani economy.

Conclusion

The point of this article is not to suggest that politics is not important or that we as a country should not try to have more political stability. It is to establish that the baseline of economic progress we can expect without succeeding in changing our political stability is still high enough that it may get us to become at least a solidly middle income country within the next three decades. If we achieve political stability before then, that will serve as an accelerant to growth. But not achieving that stability will probably not slow us down much more than the scenario laid out here.

Based on just the reduction in the gyrations caused by the fiscal deficit alone,

the Pakistani economy is likely to increase its growth rate back towards its historical average of about 5% per year in inflation-adjusted terms, which would put the country on track to become a solidly middle income country over the course of the next 30 years.

More importantly, it would do so while remaining a young, vibrant society at a time when the vast majority of the world consists of societies getting older and slowly dying off. As many of Pakistan’s best qualified professionals search for the exits, these longer-term trendlines may be worth keeping in mind.

Right now, the difference in economic opportunity between Pakistan and richer economies is quite high. But that difference is likely to narrow over time, and the social and family aspects of life become much more salient as one ages. To the future emigrant from Pakistan, we would suggest considering having a plan to come back home even if you do decide to leave.

Pakistan is about 5-7 years away from economic lift off. And you will not want to miss it. n

Mr. Muhammad Hassaan Pardesi INTRODUCING

Mr. Muhammad Hassaan Pardesi is a distinguished and influential figure in the business community. After attaining a Bachelor’s degree in Business Administration from the American University of Dubai, Muhammad Hassaan Pardesi joined his family business in Ajman to manage a real estate project comprising of 10 towers

Director at HMR GroupGoldcrest Mall and FunationNascent Innovations

He is a Director at HMR Group, a business conglomerate headquartered in Karachi. HMR Group is renowned for its leading role in real estate development in Pakistan and the UAE, as well as its significant presence in the textile market in Tanzania. The group is a family-owned enterprise led by Haji Muhammad Rafiq Pardesi.

HMR is proud to introduce HMR Waterfront. A luxurious gated community that encloses fourteen high-rise residential towers, facilitated with modern amenities and efficient security to enjoy a peaceful, entertaining, and contemporary lifestyle.

Hassaan Pardesi serves as the CEO of Goldcrest Mall and Funation, a Family Entertainment Center (FEC). The premier indoor Largest Entertainment center in Lahore DHA, Phase 4. From thrilling rides to interactive attractions for all ages.

Goldcrest Mall, located in DHA Lahore, Phase 4, has become a premier destination where visitors can find their favorite stores and restaurants all under one roof. With over 100 shops and eateries

He also runs and owns an IT company named as Nascent Innovations which is a leading software house in Pakistan specializing in software applications, website designing, and custom software development

Mr.M.Hassaan Pardesi diverse portfolio showcases his exceptional versatility and expertise in managing enterprises across various industries, from construction, retail, and facility management to information technology. His strategic vision and innovative approach have been instrumental in driving the growth and success of his businesses. Through his dynamic leadership, Pardesi has solidified his reputation as a notable entrepreneur and leader, consistently delivering excellence and fostering growth in all his ventures.

Its answer is in the constitution Pakistan has a serious taxation problem.

A little thing called the 18th Amendment has set out a three tiered democracy in which taxation is a local government subject

By Abdullah Niazi

It was the kind of news one can really only laugh and shake their head at.

Early in the month, a report emerged indicating that salaried individuals had overtaken the country’s powerful textile industry when it came to income tax payments.

And the salaried class beat the textile sector by a pretty big margin. In the year 2023-24, income tax from the textile industry amounted to Rs 111.23 billion. In comparison, the salaried class pitched in with Rs 367.8 billion in income tax payments. That is more than three-times more than what the country’s largest sector paid.

This isn’t some coincidence of course. The burden on the salaried classes has increased at an alarming rate in recent times. The Rs 367.8 billion that were paid in income tax by salaried individuals was already up by nearly 40% from Rs 263.8 billion in the 202223 financial year. This contribution exceeds that of wealthy textile exporters by Rs 276.57 billion, even though they exported $16.655 billion worth of goods last year.

Put the contribution of the salaried classes to Pakistan’s tax net in context and it becomes clear just how massive it is. Out of the biggest contributors in the country, only commercial banks and petroleum products produced more tax income for the government

than salaried individuals.

The banking sector contributed Rs 946.08 billion to income tax collection in FY24, a significant 66 per cent increase, from Rs 568.68 billion in FY23.

Petroleum Products were the next big contributor. And even within this, salaried individuals pay a chunk of the sales tax that is generated from these products. Petroleum products remained a significant contributor to federal taxes, generating a total revenue of Rs 1.195 trillion in the financial year that just closed, up 5% from Rs 1.138tr in the previous year. Within this sector, income tax collections rose 6% to Rs 413.48 billion, from Rs 388.75 billion in the previous year. The sales tax revenue generated from petroleum items was Rs 457.88 billion. Customs revenue from

POL also rose, reaching Rs 310.62 billion from Rs 289.89 billion in the previous year. In addition to the taxes on petroleum products, the government also collects a petroleum development levy on them.

All of this is bound to get worse.

The budget for the upcoming year has already increased the burden of taxation on the salaried classes further, it has also increased the petroleum levy and the general increase in indirect taxation has meant the proportion of income that salaried individuals spend on taxes has increased at a breakneck pace.

This is one example of how badly structured taxation is in Pakistan. Why is this the case? To put it quite simply, the wrong people are responsible for taxation in this country, they in turn focus on the wrong people to

squeeze more and more out of, and they do it on behalf of the wrong people.

What we mean by this is that the federal government is in charge of taxation. They tax those already documented because that is easier for them than casting a wider net. They do so on behalf of the provinces, which receive large portions of this taxation revenue through the NFC Award. Of course, the provinces themselves are actually supposed to collect these taxes. Our entire contention is that there is an answer for these woes within the constitution in the form of the 18th Amendment which enshrines a three tiered democracy and demands the devolution of powers, including taxation, to local governments.

It’s bad

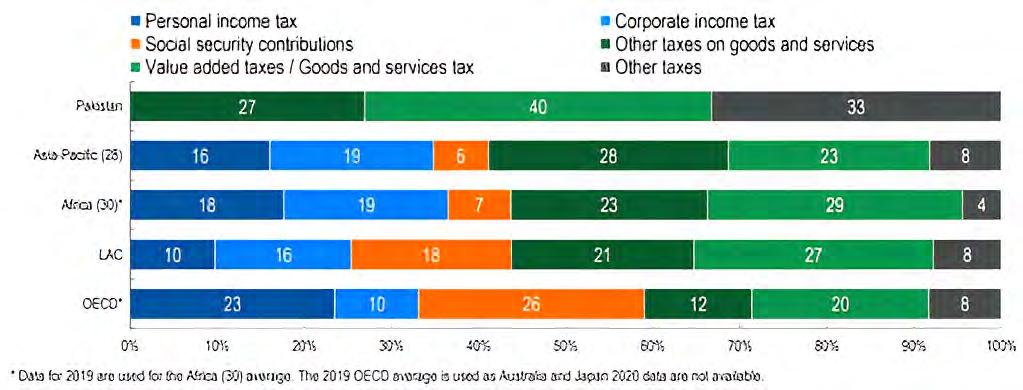

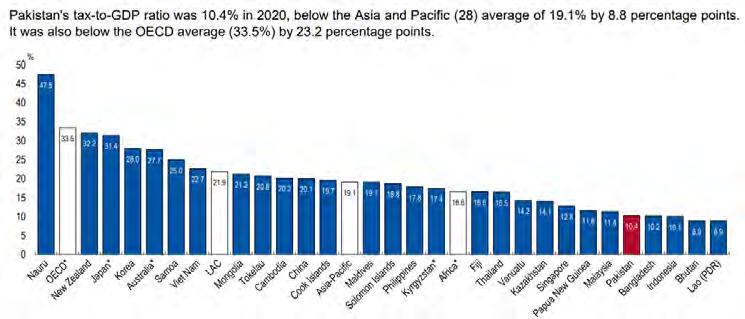

The situation is quite bleak. The real problem is that Pakistanis are taxed unfairly and those that should be paying the lion’s share end up paying nothing. Just take a look at Pakistan’s tax structure. Tax structure refers to the share of each tax in total tax revenues. The highest share of tax revenues in Pakistan in 2020 was derived from value added taxes / goods and services tax (39.8%). The second-highest share of tax revenues in 2020 was derived from other taxes (33.3%).

In comparison to Pakistan, countries in the Asia-Pacific region only collect about 23% of their taxation from goods and services taxes — meaning Pakistan’s average is almost double. Why is this the case? The biggest reason of course is that taxation in the country is centralised. The FBR collects almost all taxes (even the ones that should be collected by provinces under the 18th amendment) and then those collections are then given to the provinces in the form of the NFC award leaving the federal government with very little spending money. In an earlier interview former Finance Minister Dr. Hafiz Pasha, while talking to Profit, lamented that, “We as a country have failed to implement the beautiful 18th amendment. The implementation has been slow and weak.”

Since the share of the provincial governments, under the NFC awards, over the last few years has been increased from 40% to around 57%, it has provided the provinces with very little incentive to develop their own revenue sources. Despite having access to the two biggest cash cows, services and agriculture, the share of provincial tax revenue is close to 1% of the GDP.

The solution of course is right in front of us: devolution. More than just being a third tier of democracy, having a local bodies system means having a new economic process. In essence, it is not just a new administrative stratification, but also involves the dispensa-

We as a country have failed to implement the beautiful 18th amendment. The implementation has been slow and weak

Dr Hafiz Pasha, former finance minister

tion and spending of money. Things such as education and health that people automatically look towards the provincial government for would now be handled by local representatives. Perhaps most crucially, the ability of local governments to collect taxes and release their own schedule of taxation allows them to make their own money and spend it on themselves rather than waiting for the benevolence of the provincial or federal government.

Local governments are the answer

The answer is clearly right in front of us. And there have been attempts to make it work. Before we begin with the examples, it is important to note that local governments make sense. We are not speaking here specifically of any local government acts that have been passed in Pakistan, but generally of a third tier of democracy as a concept. It is a more efficient administrative system and adds another tier to the democratic process, making accountability and access to said administrators a less arduous process than it currently is. It also allows communities to look out for and administer themselves in accordance with their own best interests, and leave legislators in the assemblies to the more important task of actually legislating instead of being caught up in gali mohalla riff raff.

But more than just being a third tier of

democracy, having a local bodies system means having a new economic process. In essence, it is not just a new administrative stratification, but also involves the dispensation and spending of money. Things such as education and health that people automatically look towards the provincial government for would now be handled by local representatives. Perhaps most crucially, the ability of local governments to collect taxes and release their own schedule of taxation allows them to make their own money and spend it on themselves rather than waiting for the benevolence of the provincial or federal government.

Currently in Pakistan, the system that operates rather than local body governments is a bloated, vain, and self-contradictory bureaucracy where rather than elected representatives controlling local issues, the district is in essence the fief of a government appointed district commissioner (DC). This not just centralises authority, but means locals with a better understanding of the area’s politics and requirements are not in charge of decision making. On the matter of taxation, since DCs do not collect this, it is all left up to the Federal Board of Revenue (FBR).

We’ve seen glimpses

When the history books are written, one of the turning points in Pakistan will be the 18th amendment. In 2010 after the long years of the Musharraf era, the

Around 26% of General Revenue Receipts (GRR) in the first two years and 28% of GRR from the third year onwards will be transferred directly to local governments (LGs) through the PFC. Approximately PKR 550 billion will be allocated to LGs

Ahmad Iqbal, member Punjab Assembly

country finally seemed to be on a democratic track. And while the 18th amendment will always first and foremost be remembered for limiting the powers of the President and bringing Pakistan into a purely parliamentary form of democracy, it will also be remembered for bringing about the dissolution of certain powers from the centre to the provinces.

The dissolution of powers, however, is not complete yet. Under the 18th amendment, when matters such as health and education were made provincial subjects the understanding was that in due time these powers would be further devolved to a third tier of government – locally elected city, district, and tehsil representatives. Before the 18th amendment, the only serious effort at forming this third tier of government had been made in the Musharraf era. After it, the first time was when the PML-N government in Punjab and the PTI government in KP tried to form local governments in their respective provinces after coming to power in 2013.

The PLGA 2013 enacted by the PML-N left much to be desired. It was a very basic form of local government to begin with, and there was not much control that the local functionaries would have. Under this system, larger issues such as health and education continued to be run by the provincial government through their DCs. More importantly, there was no guaranteed funding that these local governments received.

The PLGA 2019 that followed and

was brought in by the PTI improved on this significantly. Under this Act, a guaranteed 30 percent of the provincial budget would be given to the provinces through the Punjab Finance Commission. The PTI’s Act also introduced directly elected mayors (a measure that has been removed by the new 2022 Act), and gave more control of some subjects to the local governments but still retained major responsibilities such as health and education. Details of how the 2019 Act improved upon the 2013 Act.

Of course, the PLGA 2019 never got a shot at being applied. As Dr Cheema described it, the PTI’s draft was a radical one and never seen before in Pakistan, but it was set aside by the PTI itself in 2021. The details of these acts have been covered by Profit before. The point is that on both occasions the governments were never elected, and there was no chance for a third tier of democracy armed with taxation powers to come through.

Another attempt was made in 2022 by the short-lived Hamza Shehbaz government in Punjab. The structure of governance aside, on the finance side this new bill held that under the Punjab budget, Rs 528 billion is allocated to local governments. Of this, and any future budgets, 10 percent will go directly to the Union Councils through the Punjab Finance Commission – meaning around Rs 55 billion. “Around 26% of General Revenue Receipts (GRR) in the first two years and 28% of GRR from the third year onwards will be trans-

ferred directly to local governments (LGs) through the PFC. Approximately PKR 550 billion will be allocated to LGs,” explains Ahmad Iqbal, who worked on the bill back in 2022 and is currently a member of the Punjab Assembly.

This act was financially progressive. The last time elected local governments were around in 2017 under the 2013 PML-N Act, district councils would have to get funding approval from the local DC on a project to project basis. This time, they will be empowered to make their own budgets with auditing oversight but no oversight from the DC, which would be in the true letter and spirit of the constitution.

How it would work

Even though it makes very obvious sense, there is no shortage of opposition to this act and giving financial control to local governments. Just take a look at the 2022 Act we have just discussed. The last time elected local governments were around in 2017 under the 2013 PML-N Act, district councils would have to get funding approval from the local DC on a project to project basis. This time, they will be empowered to make their own budgets with auditing oversight but no oversight from the DC.

You see, land is one of the most important sources of revenue for local governments. Taxes on land transfers, taxes on immovable property, taxes on unused property, building taxes – all of these are major streams of revenue for local governments. Particularly in large cities where there is real estate development. In most of these cities, all of these streams of revenue are controlled by development authorities, like LDA and Faisalabad Development Authority (FDA) in Faisalabad and even by private housing societies like DHA.

Essentially, local governments would be entities within themselves. What we have described here are simply some examples of flawed legislation that has been passed in the past. With true devolution, there is very much the possibility of local governments making a difference in how our taxation works. n

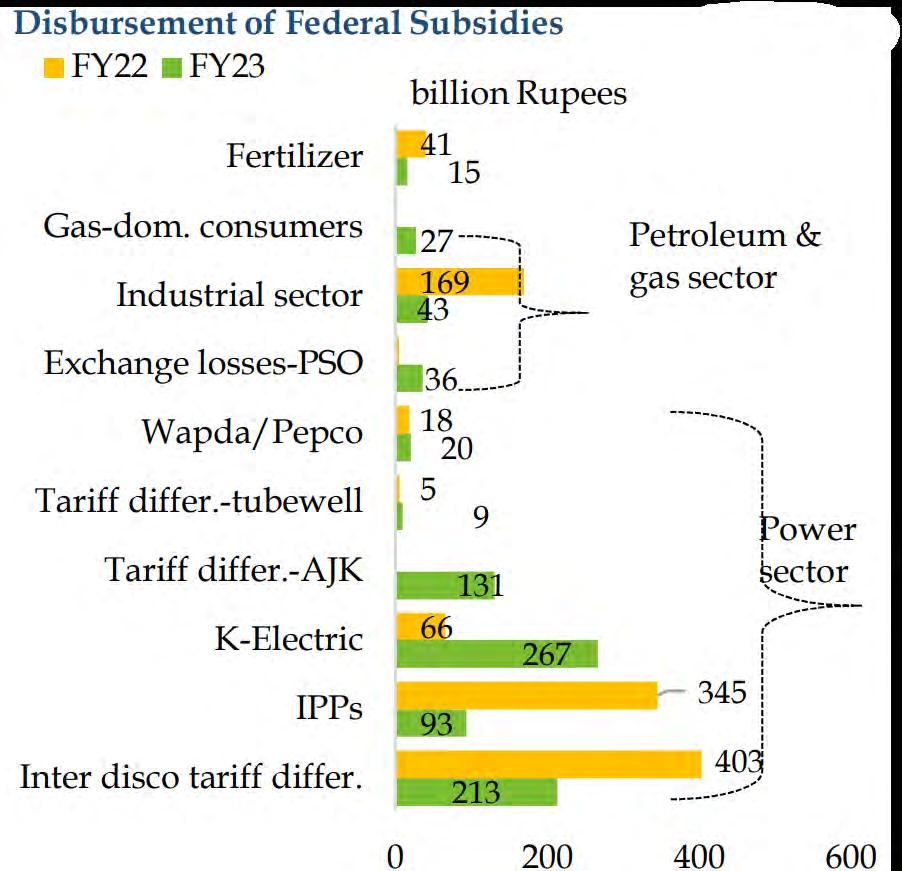

Getting to the root of the subsidy addiction

By Ahtasam Ahmad

A closer look at the Pakistan’s subsidy structure makes it evident where the rot starts

In recent years, the term “subsidies” has become a flashpoint in Pakistani economic discourse, sparking heated debates and policy clashes. A prime example is the 2022 controversy when the outgoing PTI government extended petroleum subsidies against IMF advice, nearly derailing Pakistan’s extended fund facility.

Despite the frequent mentions of subsidies in public discussions, a detailed analysis of their scope and breakdown is often lacking. This article aims to move beyond media simplifications and dig deeper

into Pakistan’s subsidy system. Let’s map subsidy flows, scrutinize allocation methods, and explore more effective alternatives.

The Why and Where of Subsidies

Subsidies are a key mechanism governments employ to provide direct or indirect relief to their populace. In Pakistan, the allocation and distribution of subsidies reveal significant patterns and challenges that merit closer examination.

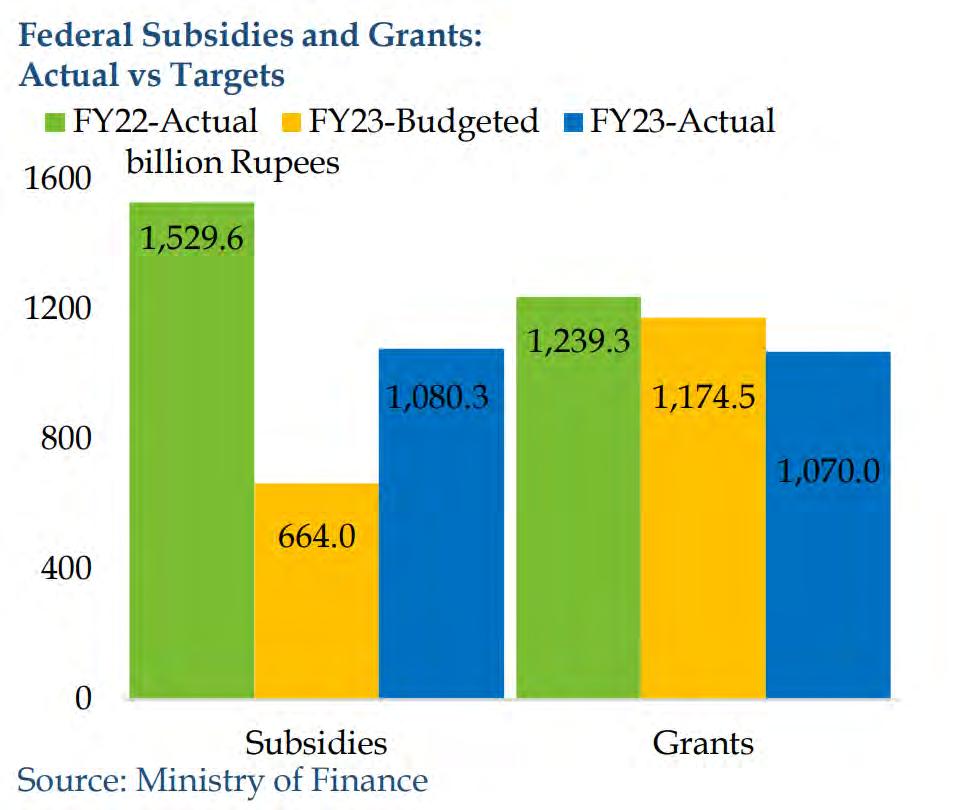

As per the budget for Fiscal Year (FY) 2025, from the total subsidy amount of around Rs. 1.36 trillion, a staggering 87% (Rs. 1.19 trillion) will flow to the power sector, with the remaining 13% divided between food, industries, utility stores, and others.

This is not an anomaly; historically, over 80 percent of recurrent subsidy spending between FY 2013 and FY 2022 benefited the power sector. Further, energy subsidies in FY 2024 are estimated at Rs. 894 billion (1% of GDP), the highest in South Asia, with twothirds allocated for electricity consumption.

The unfortunate reality is that even after allocating such massive amounts for subsidies, additional expenses during a fiscal year in the form of unbudgeted subsidies are still required.

For instance, in FY 2023, while the target for overall subsidies was set at Rs. 664 billion, with Rs. 463 billion allocated for the power sector (including circular debt settlement), the actual disbursement to the power sector reached Rs. 870 billion. This large deviation from the target was mainly due to higher accumulation of circular debt and payments made under a fiscal package.

Powering Through Subsidies

The power sector emerges as the central focus of Pakistan’s subsidy strategy, but it’s crucial to understand what exactly is being subsidized within this sector. A closer examination reveals that a significant portion of power subsidies, approximately 80% in FY 2023, is allocated to tariff differential subsidies (TDS). The concept of TDS stems from a fundamental mismatch between the costbased electricity tariff determined by the

power regulator and the government’s assessment of what the public can afford. To bridge this gap, the government introduces a lower tariff and uses TDS to cover the difference.

At the heart of this issue lies the high cost of power generation relative to the average household income in Pakistan. The total cost of electricity provision, encompassing generation, transmission, and distribution, amounts to around Rs 35.5 per unit.

This breaks down into energy cost (Rs 10.9), capacity cost (Rs 18.4), transmission costs (Rs 1.54), and distribution cost (Rs 4.6 per kWh).

Notably, a substantial portion of this cost is attributed to capacity payments, a topic that has been receiving considerable attention in recent news and policy discussions.

Is It Worth It?

It’s evident that high energy tariffs aren’t affordable for the most vulnerable segments of society. However, the problem with blanket subsidies like TDS is that a significant portion of resources is directed towards paying for inefficiencies or to those who don’t really need subsidizing. Around 60% of residential and all agricultural consumers are subsidized, but not all of them require this support.

A World Bank analysis revealed that in FY 2019, 77% of subsidy spending benefited households in the top 3 income quintiles, while the bottom 40% only received 23%

of total spending, making these subsidies highly regressive. While the situation has improved due to subsequent tariff hikes, significant inefficiencies persist.

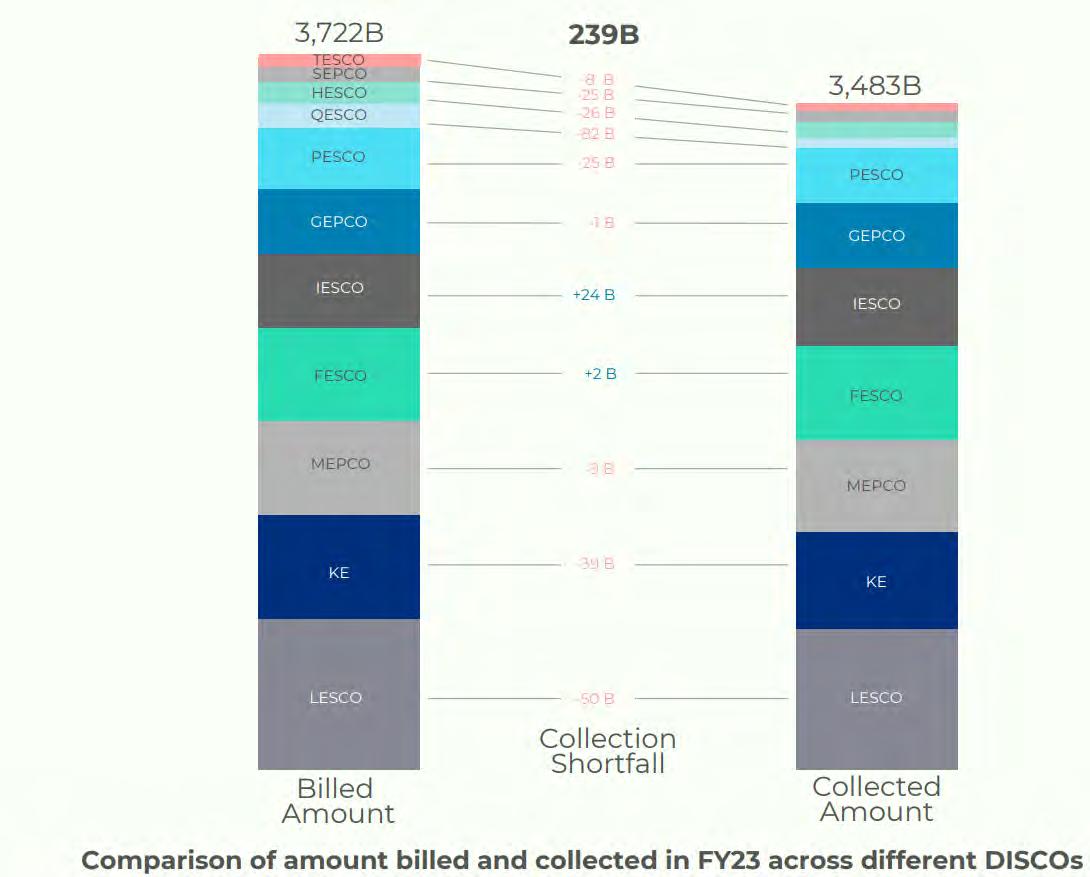

One glaring example is the subsidy to electric tube wells, which continues to be regressive, primarily benefiting large and wealthy farmers. Moreover, inefficiencies in the power sector, such as the collection shortfall of Rs. 239 billion reported in FY 2023, add to the tariff and require additional subsidies to cover the gap.

The irony lies in the financing of these regressive subsidies: they’re primarily funded through indirect taxes, which are themselves regressive. This information can be a bit taxing, we know.

Doing it right

The argument isn’t that vulnerable populations should be left unprotected; rather, it’s that there are more effective ways to provide support. One promising alternative is through direct cash transfers, for which Pakistan has an ideal instrument in the Benazir Income Support Programme (BISP).

In FY 2023, the BISP spending amounted to Rs 408 billion (less than half of subsidies outlay). Under the program, Rs 70 billion were disbursed to 2.72 million flood-affected families (Rs 25,000 each). The program also covers Unconditional Cash Transfer (UCT) and Conditional Cash

Transfer (CCT) schemes. Under Benazir Kafalat (UCT), 7.7 million families initially received Rs 7,000, later increased to Rs 8,750

Source: Renewables First

with 25% inflation adjustment. UCT coverage expanded to 9 million families. The CCT ‘Benazir Taleemi Wazaif’ scheme disbursed Rs 23.4 billion to beneficiaries’ children.

The assistance through programs like BISP can be better targeted and has proven to have positive impacts on people’s lives, including improvements in child nutrition, food consumption, and women’s mobility.

A World Bank analysis found that between 2011-2019, the percentage of BISP beneficiaries below the poverty line fell from 90% to 72%, demonstrating the program’s effectiveness in reducing poverty.

Even globally, multilateral organizations such as the World Bank and IMF have thrown their support behind the policy of deploying assistance through direct cash transfers while phasing out subsidies. This approach isn’t unique to Pakistan but part of a broader international trend.

As the country stands at this economic crossroads, the shift from broad subsidies to targeted cash transfers represents more than a policy change—it’s an opportunity to redefine how the nation supports its most vulnerable citizens. By embracing this approach, Pakistan could not only alleviate immediate financial pressures but also lay the groundwork for a more sustainable and equitable economic future. n

A major multinational has been fined Rs 6 crore for deceptive marketing of their soap. They aren’t the only ones

Unilever Pakistan has been fined for deceptive marketing of its product Lifebuoy. This makes them the third FMCG charged with deceptive marketing in the antibacterial soaps segment

By Shahnawaz Ali

After almost three years of enquiry and legal proceedings, the Competition Commission of Pakistan (CCP) has passed an order imposing a fine of Rs 6 crores on Unilever Pakistan for airing deceptive claims through television commercials for its hygiene and cleansing products, ‘Lifebuoy (Care and Protect) Soap’ and ‘Lifebuoy Hand Wash’.

Based on a complaint submitted by Reckitt Benckiser (RB) a few years ago, about their Lifebuoy Soap and hand wash. The CCP conducted an inquiry into Unilever Pakistan Limited’s absolute claims regarding its products, such as “100% guaranteed protection from germs”, “World’s No. 1 germ protection soap”, and “99.9% germ protection in 10 seconds.”. As per the enquiries, the disclaimers

about these claims were printed in tiny fonts and were hardly noticeable.

While it seems as if Unilever got served for making tall claims about its product, there is more at play here than just marketing. It is to be noted that this is not the first time one of these companies have gone to the regulator against each other for deceptive marketing. Hence it becomes important to understand the dynamics of the anti-bacterial soap industry, the relationship between these companies and how impactful deceptive marketing is in the industry.

“How many germs can a soap kill?”

In recent years, the battle between multinational corporations over market share has escalated beyond product innovation and consumer satisfaction all across the

world. The reason could be market saturation, bad global economic indicators or something more. But there is a feud that predates all these plausible reasons, and that feud is between Pakistan’s anti-bacterial soaps.

According to NielsenIQ as of 2016, the antibacterial soap market of Pakistan comprised 48% market share of the overall soaps market. Which means that nearly half the soaps in the country claimed to be anti-bacterial. However, unlike the beauty soap category, one that has a low barrier to entry, the anti-bacterial soap market had low competition due to the preliminary research and development costs.

By design there are three giants that dominate this specialised soap and handwash market. Unsurprisingly, these giants are Unilever, Proctor and Gamble (P&G) and Reckitt Benckiser.

Over the years, the competition of these

soap makers has increasingly spilled into the regulatory domain, where companies pull each other’s leg for their marketing practices. As a consumer, it is often confusing what is the best antibacterial soap of Pakistan. Is it P&G’s Safeguard? Is it Unilever’s Lifebuoy? Or is it RB’s Dettol?

It doesn’t help that all three of them in their marketing practices claim to kill at least 99.9% of the germs if not the full 100%. It is interesting to note that these jaw dropping figures have been the very reason for regulatory action, yet to this day, these companies continue to use absolute and arbitrary numbers.

It all began when RB lodged a complaint against P&G for deceptive marketing at the CCP, back in January, 2016. The complaint was against the latter’s claim of Safeguard being Pakistan’s number one anti bacterial soap. It was determined that neither by value nor by volume was Safeguard, the number 1 antibacterial soap hence P&G was found in violation of the section 10 of the Competition Act. The CCP set a penalty of Rs 10 million to be paid for this violation. 8 years after P&G’s appeal against the CCP’s decision, the Competition Appellate Tribunal, in 2024, reduced this penalty to Rs 5 million (50 lakhs) due to P&G’s compliance oriented approach.

A similar conflict between Unilever and RB began when Unilever Pakistan lodged a formal complaint with the CCP against RB in November 2016. The complaint focused on RB’s flagship product, Dettol Soap, which had been advertised as providing “99.9% germ protection” and offering “24-hour protection against germs, cold, and flu.” These claims, according to Unilever, were misleading and lacked a scientific basis, thereby constituting deceptive marketing under Section 10 of the Competition Act, 2010.

The CCP initiated an inquiry, which concluded that RB’s marketing campaign was indeed deceptive. The claims were found to be unsubstantiated and capable of misleading consumers, as well as harming the business interests of other companies, particularly those competing in the hygiene and personal care sector. As a result, in December 2019, the CCP imposed a fine of PKR 30 million on RB for these violations. Five years later, the appellate tribunal did the same favour for RB, reducing the penalty by half, making it Rs 15 million (1.5 crore) in July 2024.

The most recent complaint against Unilever was lodged in February 2021 by RB. Even though Unilever is found in violation of the same section of the competition act, it was fined at least 4 times more.

According to the CCP, “Unilever’s deceptive practices varied by region, with different wording for the same product in countries such as Saudi Arabia, the UK, and

Bangladesh. The most severe deceptions were found in Pakistan, which the Commission deemed unacceptable.”

The company reserves the right to appeal against the decision just like the other two did.

Why is deceptive marketing dangerous?

Deceptive marketing is not merely a breach of consumer trust; it has far-reaching implications that affect various stakeholders, including consumers, competitors, and the broader market ecosystem. The cases involving Reckitt Benckiser, Procter & Gamble and Unilever serve as important examples of how deceptive marketing practices can actually distort market realities and harm consumer wellbeing.

One of the most direct consequences of deceptive marketing is the spread of misinformation among consumers. When companies make exaggerated or unsubstantiated claims, consumers are led to believe in the efficacy or superiority of a product that may not be as good. In the cases of Unilever and P&G, consumers were misled into believing that their products offered unparalleled protection against germs, which could have serious health implications if the products fail to perform as advertised.

These practices also distort the competition in the market by giving an unfair advantage to companies that engage in such tactics. This not only harms competitors but also undermines the integrity of the market. In both cases filed by RB, RB was placed at a disadvantage because its competitors were making inflated claims that could sway consumer preference. This creates an uneven playing field, where success is not based on product quality or innovation but on who can make the most compelling, albeit misleading, marketing claims. It is also important to acknowledge that while it may seem like it, the personal vendetta and market share politics, come after a brand image. Therefore it becomes mandatory for these companies to report on their competition, if the competition is found in violation.

Another important reason why the CCP cracks down on these practices is because deceptive marketing can also reduce the effectiveness of consumer choice. When consumers are bombarded with misleading claims, their ability to make informed decisions is compromised. This can lead to a situation where inferior products dominate the market simply because they are more aggressively marketed, rather than because they are better or more cost-effective.

Why Does Reckitt Benckiser Benefit from Action Against

Unilever and P&G?

There is of course no denying that these complaints against each other have now become a regular part of the Pakistani antibacterial soap market. Much like Unilever benefitted from the action against RB, Reckitt Benckiser also stands to gain significantly from regulatory action against its competitors.

By holding Unilever and P&G accountable, RB can reinforce its position as a brand that consumers can trust. This is especially important in the health and hygiene sector, where trust in a product’s efficacy is paramount. Regulatory action against deceptive practices also serves as a deterrent to other companies, encouraging a more honest and transparent marketing environment that benefits all players.

Another thing that RB benefits from is the market correction that occurs when deceptive practices are curbed. When competitors are penalised and forced to retract false claims, it opens up market share for RB to capture, particularly if its products are genuinely superior. While this correction has already occurred in the past, there is little to no data to show for it.

Conclusion

Even though there is a lot of gap between the times of the filings of these cases, their resolutions have all come within the last 5 months. This is because the Competition Appellate Tribunal had not been functioning for the last seven years. After the appointment of a full time chairman, the tribunal has made lots of headway into clearing its backlog of more than 200 cases.

These cases are a stark reminder of the importance of maintaining ethical standards in marketing. Deceptive practices can lead to regulatory penalties, reputational harm, and loss of consumer trust. For companies, the pursuit of short-term gains through unethical means often results in long-term consequences that far outweigh any immediate benefits. As consumers become more aware and regulatory bodies more vigilant, the importance of transparency and honesty in marketing cannot be overstated.

The Competition Commission of Pakistan’s actions in this case demonstrate the critical role that regulatory bodies play in safeguarding both consumers and businesses from the harms of deceptive marketing. That is one of the reasons why having a complete regulatory body with all designations performing their functions is important to maintain balance within a market. n

Could Patient Capital be the way out?

Blended finance is proving to be a catalyst of change for the Global South. Does Pakistan have what it takes to capitalize on the opportunity?

By Hamza Aurangzeb

In the world of finance, credit ratings are kind of like a character certificate for individuals, companies, and even entire countries.

Well, when it comes to Pakistan’s rating, we could probably come up with a whole bunch of puns, but as a serious publication, we’re going to hold back on that.

The good news is that Fitch, one of the most widely recognized credit rating agencies, has actually just upgraded Pakistan’s rating to CCC+. But don’t get too excited just yet – this rating still means the country has a substantial risk of defaulting on its debt. And that, in turn, means companies operating here would also be carrying similar levels of risk.

Now, put yourself in the shoes of an investor. How would you feel about that kind of news? Not great, I’m guessing. And that’s exactly what’s been happening – private investors have been apprehensive of wagering their money on Pakistan, especially after the economic crisis that unfolded in 2022.

This lack of investment has led to a scarcity of capital available for important projects, whether it’s building large-scale power plants or financing startups.

But you know what? There might be a solution to this problem, and it’s called “blended finance.” It’s a way to de-risk those kinds of risky investments, making them more attractive to private investors.

In this article, Profit takes a deep dive into the world of blended finance and assesses how it could be relevant for Pakistan.

What is blended finance?

Blended finance refers to the strategic use of development funds to catalyze additional capital towards sustainable development in developing economies through an amalgamation of capital provided at market and concessional rates. It directs private investment to projects aligned with sustainable development in conjunction to value creation

for investors. This ingenious method leverages a wide ranging pool of resources available to developing economies, complementing their domestic funding and Official Dvelopment Assistance (ODA) influx to plug in the financing gap for fulfilliment of Sustainable Development Goals (SDGs) and assisting the implementation of the Paris Agreement. It is essentially a scheme designed to mobilizle private investment in a project through de-risking. A diverse range of institutions are involved, such as development finance institutions etc., who serve as guarantors for these projects by electing the riskiest investment, creating a conducive environment for private investors to contribute towards the development of the project with optimiized risk.

Why is blended finance required?

According to estimates of the United Nations, the development financing gap currently stands at $4.2 trillion annually in comparison to $2.5 trillion before COVID-19. Although ODA is nowhere near capable of filling this gap as it reached only $223.7 billion in 2023, however, it is possible to fill this gap with the help of only 3.9% of global GDP, 14.7% of annual global savings, or 1.8% of the value of global markets,

estimated at $231 trillion.

There is a dearth of private sector investment in areas associated with SDGs, where a handful of worldwide assets of banks, pension funds, insurers, foundations and corporations are deployed in such domains. It is crucial that these assets are directed towards specific sectors related to SDGs, particularly, power, renewable energy, and transport, which have immense potential.

The international development community understands the significance of private capital in eradicating the funding gap for development goals. Hence they are utilizing approaches such as blended finance, where development finance complements private capital rather than serving as a substitute.

Blended finance has catalyzed around $231 billion through 6,800 deals towards achieving sustainable development goals in developing countries thus far.

Types of Instruments

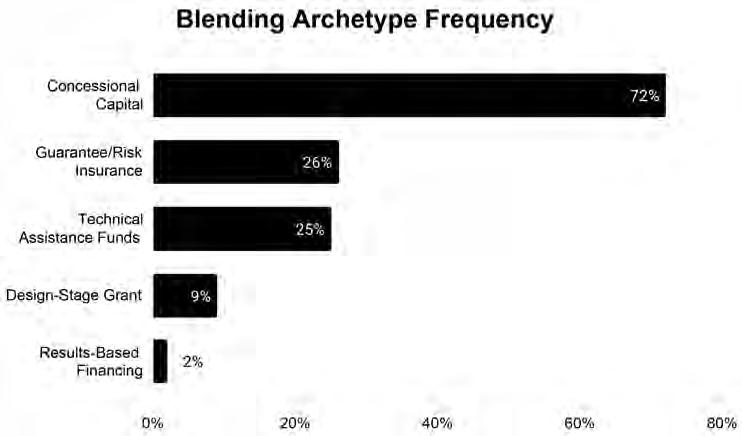

Since now we have developed an adequate understanding of blended finance, let us explore the various kinds of instruments utilized in blended finance, which have been placed into four different clusters depending upon their nature.

Our new fund focuses on blended finance, which aims to turbocharge climate action in Pakistan. We need to source capital from various development institutions like the GCF to achieve this. The GCF is the largest contributor to climate action in Pakistan and has the capacity to tolerate high risks

Rabeel Warraich, Founder Sarmayacar

a. Grants and Technical Assistance

The first cluster encompasses tools like grants and technical assistance, which are usually provided by development and philanthropic institutions. These instruments play a significant role while entering a new market, grants assist in tracing investment opportunities and establishing curated networks, while technical assistance provides domain expertise, crucial for the project’s successful implementation. Institutions like USAID and GIC regularly issue grants and provide technical assistance to local partners for implementing programs effectively.

b. Outcome Funding, Impact Linked Finance, and Impact Bonds

This cluster involving instruments like outcome funding, impact linked finance, and impact bonds has been dubbed as the results-based financing category. The objective of these instruments is to maximize the impact created by a program or project as they interlink impact with financial rewards or funding. All stakeholders involved develop a consensus on predefined targets to be achieved while pursuing a development objective, which in turn unlocks funding or financial rewards. Pakistan Microfinance Investment Company (PMIC) offers instruments like impact bonds which interrelate impact with financing.

c. Market-rate, Subordinated, Concessional Debt & Equity