08 PIA debt restructuring: a surprisingly balanced deal

15 US farmers want to sell cheap oilseeds to Pakistani companies. Why won’t the government let them buy it?

21 Why do Pakistani businesses fail at innovation? Asif Saad

24 Did paint manufacturers shoot themselves in the foot going to the CCP?

26 From incubation to acceleration, are Pakistani ESOs really serving the startup ecosystem?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

PIA debt restructuring: a surprisingly balanced deal

By Mariam Umar

In the most literal sense of the word, PIA is worthless.

In fact, it is worse than worthless because even if it is given away for a price of Rs0, the buyer would become poorer, not richer, because they would now own the responsibility to pay back the airline’s debts, which far exceed its ability to pay them.

So how do you find a buyer for something that is worse than worthless? It is a long and complicated process, but you start by accepting the fact that the transaction is going to lose you money.

And when it is a private sector company, you then begin a process of distributing the pain among the owners (shareholders) and the lenders into the company, a process where the amount of pain you will feel is directly proportional to how much risk you accepted when you gave the company money. The lenders, who accepted a fixed, lower return generally expect the lowest losses and expect to be paid back first. Shareholders, who had accepted higher risk, expect the highest losses, and in the event of bankruptcy generally do not get paid back at all.

But when an entity is a state-owned company – and an economically important one such as the national airline – the rules are not strictly what is dictated by corporate and bankruptcy law. The government is a more powerful borrower than just about any other borrower, but its powers are also not limitless. Who comes out on top in a negotiation between the government and a consortium of virtually every single bank in the country is a question without an obvious answer.

The deal struck between the government and the banks on restructuring the debt of the state-owned Pakistan International Airlines, offers us some clues as to what the answer might be. Somewhat surprisingly, given the general incompetence of the government of Pakistan on all matters of economic policy, the government ended up with an agreement where it neither strongarmed the banks into accepting heavy losses, nor did it completely cave and let them have everything and absorbed all the losses.

It achieved, in other words, what one would expect from a negotiation between relatively evenly matched parties: a balanced deal.

How did that happen? To answer that, it helps to understand the context of what the government is trying to achieve, what it offered the banks, and why it got the best of what was not an obviously strong negotiating position.

The disaster of PIA’s management

PIA, the nation’s flag carrier, has been a financial burden for decades, accumulating billions in debt and persistent losses. Now, under pressure from the International Monetary Fund (IMF) to reduce its fiscal deficit, the Pakistani government is accelerating plans to privatise this struggling airline along with numerous other state-owned enterprises (SOEs).

This push for privatisation coincides with Pakistan’s negotiations for a new longterm Extended Fund Facility (EFF) with the IMF. Reports indicate that 84 institutions across various ministries are earmarked for privatisation, with decisions finalised for 24 and another 41 awaiting cabinet approval.

While several entities, including the House Building Finance Company Limited, and First Women Bank Limited, are slated for privatisation this year, the Privatization Commission (PC) has prioritised PIA. Initially aiming to conclude the process by August 2024, the final bidding has now been postponed to October 2024.

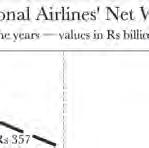

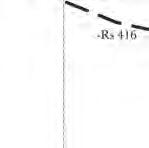

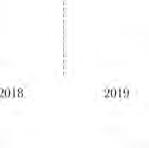

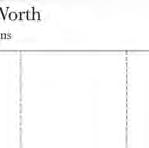

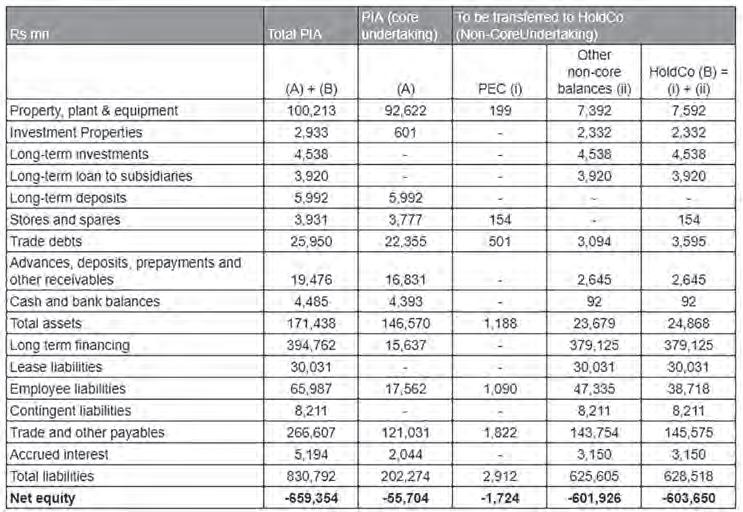

At some level, it makes sense. Among all of the financial basket cases owned by the government of Pakistan, PIA is among the very worst. The company has approximately Rs892 billion in debt and liabilities and only Rs390 billion in assets. It tends to lose tens of billions of rupees every single year, and in the most recent year for which financial statements are available (the 12 months ending June 30, 2023), its losses exceed Rs100 billion.

Why PIA is as much of a sinkhole for money is something that has been documented ad nauseum, including by this newspaper. But briefly: “Frequent management changes, the undue influence exerted by unions and associations, political interventions, wasteful spending, unchecked borrowing, and a lack of internal accountability mechanisms have further contributed to the decline of the national flag carrier,” wrote Ayesha Rahman, Research Assistant at Pakistan Institute of Development Economics (PIDE), in an article published in Business Recorder in May 2024.

More recently, in 2020, the European Union Aviation Safety Agency (EASA) suspended PIA operations in Europe after a flight crash and the fake pilot license scandal. The ban was extended. As of June 2024, EASA has postponed its decision to lift the ban on PIA flights as the airline failed to implement safety measures required by the EU Commission. All of these issues, along with rising fuel prices, have resulted in accumulated financial losses of up to Rs724 billion by

end of 2023.

This is a business that simply does not generate enough cash to sustain itself, and the only way it even has the money to keep the lights on is because the banks have been willing to lend it money under the assumption that the government of Pakistan will ultimately ensure that they get paid back.

That assumption is now being tested.

The privatisation (and restructuring) begins

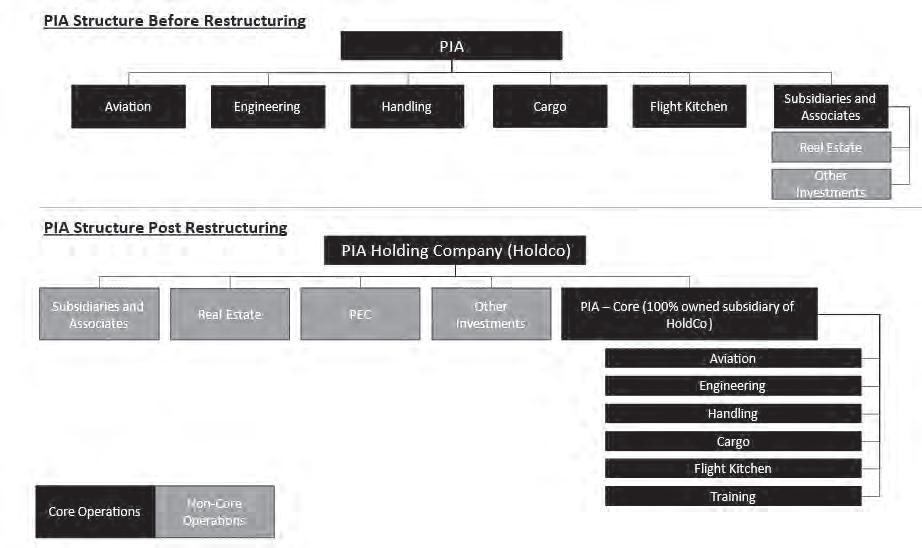

When a company is this far gone and needs to be privatised, there is generally an accepted formula for to make it happen: create two separate companies, one of which will include all of the economically viable operating assets, and a far smaller share of the liabilities, and then a second entity that will contain all non-core assets and the bulk of the liabilities.

This approach is an amalgamation of two approaches: the GoodCo / BadCo model, and the OpCo / PropCo model.

In the ‘good company/bad company’ model, the aviation business consisting of profitable routes, the operations yielding revenue, the skilled workforce, and all other profit centres, would be amalgamated into a single entity (good company) while remaining liabilities, surplus staff, and all other loss centres are then relegated to a separate entity (bad company).

The fate of these two entities? The ‘good company’, now streamlined and profitable, is primed for privatisation, while the ‘bad company’ remains under governmental purview for future strategising. The government stands to gain through taxation and reduced losses from the ‘good company’, while simultaneously devising debt management strategies and severance packages for redundant staff. A similar

strategy was successfully employed during K-Electric’s privatisation.

The good PIA could create value and future cash flows from the huge liabilities that have been incurred and have to be owned by the government. The idea is to reduce the burn rate and generate some cash flows from good assets that can be used to pay the liabilities (the bad PIA part).

On the other hand, in the OpCo/PropCo model, the government would carve out and separate the core airline operations and ancillary businesses such as properties, hotels, etc. The reason for the specific split is that PIA owns a lot of properties globally, these properties are consolidated into the PropCo, whilst its core operations are kept as part of the OpCo.

The real estate can be leased out separately at a later stage to ensure maximisation of proceeds to the Government. Whether or not these in particular are made private is up to the government. PIA’s core business, the OpCo is then the one that is privatised.

In either case, however, the debt of the company has to be divided up, and – critical-

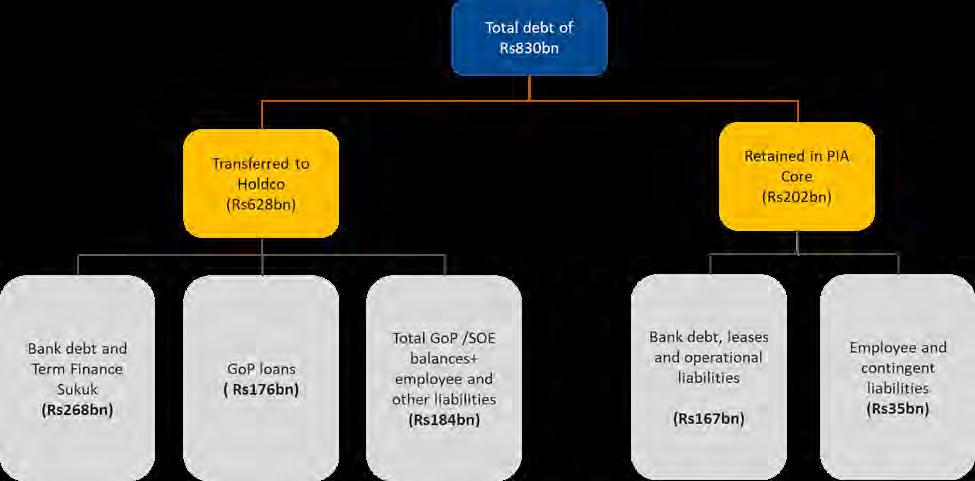

ly – the lenders have to agree to refinance and restructure the debt of the BadCo / PropCo. For PIA, the government has decided to put Rs202 billion of the Rs831 billion in debt and other liabilities in the GoodCo / OpCo, and the remaining Rs629 billion in the BadCo / PropCo.

How a restructuring can work

This is not the first time the government of Pakistan has used this kind of approach. The bank privatisations in the early 1990s under the first Nawaz Administration and then later in the late 1990s and early 2000s under the Musharraf Administration took place with a very similar GoodCo / BadCo formula. Those bank privatizations worked out well for the government, and the debt on the BadCo balance sheets simply became part of general government liabilities.

More recently, in 2009, the government created Power Holding Ltd with the aim of better managing the debt of publicly owned power companies. The intention was to transfer this debt to the new company, thereby alleviating financial pressures on individual entities and the power sector as a whole. The hope was that doing so would allow the power companies to start becoming more efficient, and for government to slowly pay down that debt over time. That, however, is not how it worked out and Power Holding’s debt has since ballooned to unsustainable levels, now exceeding Rs800 billion.

Analysts, however, believe that nightmare scenario is unlikely in the case of PIA. “With PIA, we’re witnessing a strategic separation of core and non-core assets, a move that diverges significantly from what transpired with Power Holding Limited. The latter was essentially a vehicle to house debt with no substantial assets, relying on rollovers and restructuring to manage liabilities,” said Nadia

Ishtiaq, head of investment banking at Pak Oman Investment Company.

By contrast, PIA owns a fair amount of valuable real estate that would not be part of the OpCo, such as the Scribe Hotel in Paris, and the Roosevelt Hotel in New York. “These are revenue-generating assets,” Ishtiaq stated, adding further “the proceeds from their eventual sale are intended to help settle PIA’s liabilities. Importantly, the non-core operating assets themselves are expected to generate enough revenue to service the holding company’s debt through a structured repayment solution, creating a more sustainable pathway forward.”

The government’s track record on the matter, therefore, is somewhat mixed. In some cases it did work out, but in others, it has been a colossal failure. It is this context in which the government went into negotiations with the banks to try to get them to agree to the split.

A case of competing leverage

How this negotiation could have worked out is best illustrated with the case of the extremes: what would have happened if the banks had all the power, and what would have happened if the government had all the power?

Let us start with the case of the government having maximum leverage. It could have come in and said to the banks: “Look, this is a large and unsustainable debt level on PIA and you know it. You will never get paid back 100% of your money, so your best case is to accept that you will get paid back maybe 70%, 60% or even as low as 50% of the money PIA owes you. We are the government, and we can make your life miserable. Accept this deal, or else we will use our power as your regulator to completely cripple your business.”

Why did that not happen? Because the banks have a response to that. “Ok, you can win this round and make us accept those massive losses on our loans to PIA. However, we have also been lending money to all of these other state-owned companies that do not have the ability to pay under the assumption that the government will honour their debts. If you are now telling us that you will not honour those debts, then we have to start looking at those state-owned companies as the functionally bankrupt companies they are, and stop giving them more money.”

“If we stop lending to the state-owned electricity, oil, and natural gas companies, the entire country’s energy supply chain will come to a halt, and you will be blamed. Your only way out will be to print massive amounts of money and use the state-owned banks to pump it into these companies, but you will cause so much inflation if you do that that you will almost certainly be thrown out of power.”

The government, in other words, does

not have maximum leverage. But neither do the banks.

The banks are currently earning a hefty interest rate on the loans they have outstanding to PIA, and could simply say to the government: “You can reorganize this company however you like, but we like the 23%+ interest rates we are earning on our loans, and we will not refinance them to a lower interest rate. We find that this interest rate adequately compensates us for the risks we are taking with these loans and do not believe your plans that the restructured companies will collectively have lower risk that would justify giving them a lower interest rate.”

The government, however, could respond to that in a predictable way: “If you do not do this, you will suddenly find that every single issue on which you need a favourable ruling from either the State Bank of Pakistan or any other regulatory body will start going against your interests. Your sponsors will find themselves losing bids for any government contracts for any of their other businesses. We are the government. We can make your life uncomfortable.”

Both parties, in short, are evenly matched, and neither can force the other to accept a one-sided solution. Given this fact, what was the deal that got struck?

The deal

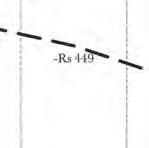

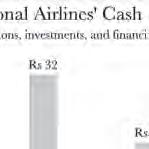

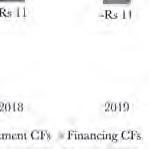

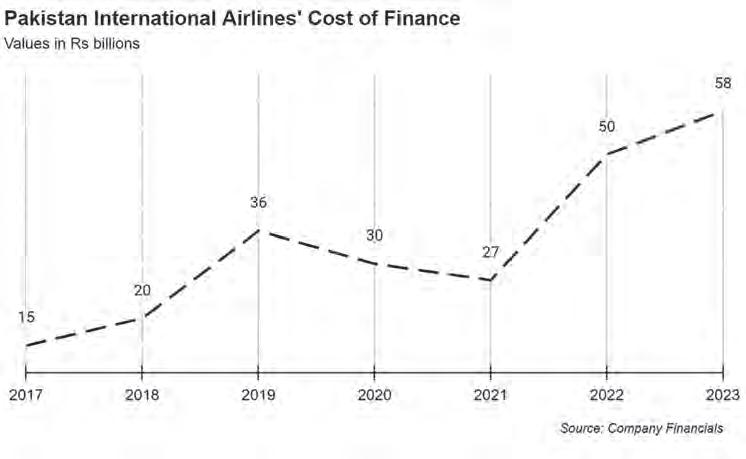

The government and the banks struck an agreement over this debt restructuring. According to the agreement, the government will allocate proceeds from PIA’s sale to cover principal payments, resorting to the budget if necessary, essentially converting an implicit sovereign guarantee into an explicit sovereign guarantee. In return, the banks consented to a 10-year debt rollover at a 12% annual interest rate, leading to Rs 32.2 billion in annual interest

payments on Rs268 billion in underlying debt. They agreed to extend their debt for ten years and reduce interest rates from the existing approximately 23.5% to a maximum of 12%. This has been done exclusively to appeal to potential buyers, and as part of the restructuring, a clause has been added to the restructuring in which banks will have the right to reopen the deal and demand an interest rate equal to prevailing rates in 2027 in case the government is unable to privatise PIA in three years.

“The arrangement represented an opportunity for both the banks and the government to resolve a long-standing issue for which all other options had already been extensively explored with little success,” stated a banking industry source familiar with the negotiations who wished to remain anonymous.

Both sides gave up something. The government gave up an explicit sovereign guarantee and abandoned the pretense that they could have negotiated a haircut on the amount of debt outstanding. And the bank agreed to a significant lowering of the interest rate they are earning on a large volume of loans, effectively accepting a cut to their revenue exceeding Rs25 billion for this year.

Both sides also gained something. The government gained a deal that will make it much easier to find a buyer, given the fact that they can now promise a much lower debt burden on the OpCo and that the interest burden on that will remain fixed for the next 10 years. And the banks gained a large volume of longterm loans that may be lower than the current high interest rate they are earning, but is still higher than the 10.5% average interest rate on the 10-year government bond that is the norm over the course of a full 10-year business cycle.

What this deal represents

Restructuring deals are a complicated business, where it is very easy to misconstrue each side’s intentions and what either party is getting out of the transaction. It is the perfect place that would lend itself to a massive problem since it requires both attention to detail and an ability to ensure that a complex matter is publicly explained simply and in a manner that does not generate negative public opinion. Both of those are capabilities that the government of Pakistan completely lacks.

That this part of the deal got handled relatively well is a positive indicator that the government is not just serious about the PIA privatization, but also has the capacity to

execute on its stated policy goal.

Despite the current travails of the airline, there is considerable interest in buying it from the government. Six parties have thrown their hat in the ring, including Fly Jinnah, Air Blue, Arif Habib Corporation, Y.B. Holdings, Pak Ethanol, and Blue World City.

And this desire is not without merit. Any buyer would be gaining access to the largest airline in the country and one that is serving an increasingly large desire on the part of Pakistanis to travel, both domestically and abroad.

That travel abroad, in particular, is a potentially lucrative business with revenues that are effectively dollar-linked. In 2023, Pakistanis spent $2.2 billion on foreign travel, and the bulk of that spending went to airlines to purchase tickets. While the Gulf airlines like Emirates, Etihad, and Qatar have a significant share in that spending, PIA remains the single largest player in that lucrative market segment and, with new ownership, could even start gaining market share.

Beyond just the success of this particular transaction, though, there is a broader significance to this debt negotiation and what it may represent for the country’s economy. The privatization agenda is a core part of the reforms needed to reorient the government from trying to run commercial enterprises and spending money in wasteful subsidies toward more necessary expenditure like education, healthcare, etc.

For the past decade and a half, largescale privatisation has been stalled for a variety of reasons, mostly to do with the government’s incompetence in dealing with predictable issues. That this predictable issue was handled well suggests a seriousness of purpose, and increase technical capability that could well yield meaningful dividends for the country’s economy. n

US farmers want to sell cheap oilseeds to Pakistani companies. Why won’t governmentthelet them buy it?

Prices for US soybeans, an import input in the edible oil and poultry feed industries of Pakistan, are at an all time low. The government is not letting them capitalise on the opportunity because of an unfounded fear of GMOs

By Abdullah Niazi

Normally, you would expect news out of San Francisco would have to do with the city’s gigantic tech scene and the many major companies like Google and Meta that call Silicon Valley their home. But at the end of last month, the Tech Capital of the world was uncharacteristically at the centre of a tense moment in the international trade of agricultural commodities.

In the third week of August, soybean farmers from all over the United States and potential buyers from all over the world descended on The City by the Bay to engage in negotiations to buy and sell soybeans.

The occasion was an annual conference on the topic of Soy, and the pulse of the event was easy to gauge. The United States is seeing perhaps the best soybean crop in its history this year, and farmers there are looking left, right and centre for buyers. The United States Department of Agriculture (USDA) has estimated US soybean production will reach a re-

cord 124.9 million tonnes in 2024-25. This has pushed prices 18% below the average estimated cost of production in that country, making it a nervous time for farmers looking to push their product and a lucrative chance for buyers. Why is this relevant to us? Because among the more than 700 people attending the conference at a downtown hotel, there was a small delegation of Pakistanis as well. Soybeans are not grown in the country, but they are an important caloric component in the average Pakistani diet. Not only are they used as a component in cooking oil, often mixed with

GMOs for processing are regulated commodities but the legal framework for its import approval was incomplete as Pakistan Biosafety Rules 2005 lacked provisions for imports of GMO grains under the Food or Feed or Processing (FFP) category, and addressed requirements for cultivation only which are understandably much more complex

Shakil Ashfaq, CEO of Shujabad Agro Industries

other oilseeds such as canola and sunflower, they are a big part of poultry feed.

But unlike their colleagues from Sri Lanka, Bangladesh, and other regional neighbours, the Pakistani buyers present at the event were saddled with baggage. You see the majority of the soybeans grown in the United States are Genetically Modified Organisms (GMOs). Even though the law allows the import of GMOs oilseeds into Pakistan, which are for crushing not planting, since last year the government has effectively barred the import of these GM beans. Which is why while other countries were trying to get the best deal, Pakistani buyers were desperately looking for farmers willing to sell them non-GMO soybeans which cost significantly more. This increased cost ends up having an inflationary effect on the prices of cooking oil and chicken, making two staple basket goods costlier and contributing to rising food inflation.

For all intents and purposes, you have a

situation where the United States has cheap soybean to offer, Pakistani buyers want to buy them, but the government is intervening because it does not understand its own laws and the international protocols it is party to. But why does the government of Pakistan not allow the import of genetically modified soybeans from the United States? What exactly makes them so much cheaper, and the entire matter really as simple as it seems? To answer these questions, we must go through the dramatic highs and lows of the past few years.

Pakistan’s needs

It all starts with a basic question: Why does Pakistan need soybeans in the first place? The crop is not indigenous to the subcontinent, and the people of this region went for centuries without it. But over the decades, global preferences for caloric con-

sumption have changed, including in Pakistan. Our story begins in the 1930s – when a Dutch company called Dada in association with Lever Brothers in London (the forebearer of today’s Unilever) planned to import cheap vanaspati ghee to the Indian subcontinent. Ghee had long been an ancient staple of the rich in the Indian subcontinent. The cooking substance made of clarified cow milk was used sparingly to make delicacies on festive occasions. Ghee, as a signifier of wealth, has even been codified into the Urdu language, with the idiom ‘paancho ungliyan ghee mein’ entrenched as a mainstream saying.

Because most Indians could not afford the product regularly, inventors in Europe had discovered a method to hydrogenate vegetable oil and turn it into a substance that convincingly mimicked the taste and function of ghee. That was the product that Dada and Lever brothers were now bringing to the Indian market. There is a long story as to how Dada and Lever Brothers came to an agreement to launch Vanaspati Ghee under the brand name ‘Dalda’ Ghee — and you can read more about it here. But when the first tins of this product hit the market, they made an impression because of the bright green palm tree logo on yellow that they used. The vegetable oil being used to make Vanaspati Ghee came from the seeds of the palm tree. That is a legacy that we have inherited to this day. In Pakistan, the most commonly used edible oil is Vanaspati Ghee. To produce this, we are dependent entirely on palm oil that is imported from Malaysia and Indonesia.

But there is another side to this. Palm is brought into Pakistan in the form of oil. There is on the sidelines another entire thriving industry that is growing and will at some point surpass palm for other oilseeds, the chief among which is soy. These oilseeds (a word used to describe a kind of agricultural product that is pressed to extract oil from it) are then used to produce edible oil.

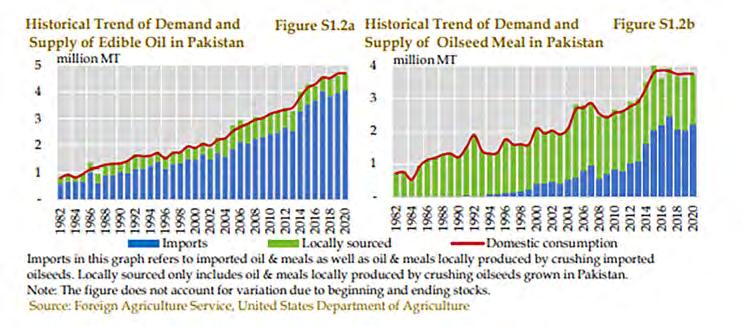

In Pakistan, nearly 90% of the import of oilseeds is constituted by palm and soybean

oilseeds. In a special report for the financial year 2022, the State Bank of Pakistan included a special section on rising palm and soybean imports. According to the report, Pakistan’s palm and soybean-related imports stood at $4 billion, rising by 47 percent year-on-year, compared to compound average growth of 12.3% in the last 20 years.

The share of soy and other oilseeds in this has been growing. There is a clear indication that as people climb social and financial brackets, their preferences change towards cooking oil over Vanaspati Ghee. Edible oil consumption in Pakistan has increased significantly over the last few decades: from 0.7 to 4.7 million tonnes between 1981 and 2020. The main demand drivers are rising population, dietary preferences and increase in per capita income. According to the recent SBP report: Pakistan’s per capita edible oil consumption is already higher compared to economies with similar income levels.

In addition, increasing income levels may also translate in increased per capita consumption of edible oil, as will population growth. According to the UN’s World Population Prospect 2019, at constant-fertility, the country’s population in 2025 is set to reach 245 million, and 328 million by 2040. This implies that demand for edible oil will continue to increase noticeably. According to estimates by the Pakistan Oilseed Department, total demand for edible oil in the country is conservatively expected to grow to 5.9 million tonnes in the fiscal year ending June 30, 2026, from 4.7 million tons in fiscal year 2021.

And that is not all. There is another major advantage to oilseeds such as soy. In the solvent extraction process in which these seeds are pressed, the remaining material that is left after the oil is extracted is highly nutritious. This material is then used to create “meals” which are fed to poultry. In the three decades since 1990, the consumption of oilseed meals as feed for livestock has tripled in the country – a big reason for which is the growth of the poultry industry. Just think about it. If you remember a time before the 1990s, chicken

Hundreds of millions of genetic experiments involving every type of organism on earth and people eating billions of meals without a problem

Robert Goldberg, plant molecular biologist at UCLA

was not the cheapest protein available and the poultry boom only came later.

Soybean meals are apparently especially good for the poultry industry. Since it is rich in nutrition, its meals offer better digestibility, quality mix of amino acids and have the highest protein content (around 44-50%) compared to all other oilseed meals. These qualities make it a better feed ingredient for chicken in comparison to cottonseed – which was the traditional oilseed used in Pakistan.

(Note: Remember that cotton seeds were a major component in poultry feed before soybean meals became more common. This will become relevant later in the story.)

Cheap soybeans for sale!

So we have got a simple equation here. Pakistan has, over time, become reliant on imported oilseeds for its edible oil and poultry feed needs. The total import bill for this is over $4 billion, which is a significant drain on foreign exchange reserves.

There are certain alternatives such as canola and sunflower seeds that have been successfully grown in Pakistan, but experiments to grow soy and palm have largely failed. This means for better or for worse Pakistan is reliant on imports for this basic caloric import, and it is in Pakistan’s best interest to import the cheapest soybeans

possible.

This is where the United States comes in. This year is likely to see a massive yield of soybeans in the US. But even before this year’s abundant crop, the US has engineered their supply chains to ensure they have incredibly cheap agricultural products to offer.

Just consider the soybean supply chain. This correspondent had the opportunity to visit a number of farms growing soybeans across Middle America last month. From Missouri to Kansas, Illinois, and Iowa, there is an impressive process that backs soybean farming in the United States. To start off, one must realise agriculture is pretty huge in the US and it is done very differently from what we know in Pakistan.

These farms are often massive, spanning over hundreds and sometimes thousands of acres. Some are run as corporate farms, which means they are backed by money from corporations. There are also a large number of farms that are family run. Because of the massive and high-tech machinery they have on their hands, from large scale factors to seed planters and harvesters that are guided by GPS trackers and drone operated pesticide dispersal, these huge tracts of land are often farmed by a handful of people which keeps labour costs down.

The seed and input research available to these farmers is the best in the world. Each state has its own association for soybeans, and there are national level associations and lobbying groups that help them at every stage from research and development to connecting them to buyers.

These soybeans are transported from states in the middle of the US all the way to the Gulf of Mexico through engineering marvels. Along the Mississippi river, soybeans are one of many commodities (coal and corn are significant examples) that are loaded onto barges directly from the elevator containers and pushed along the river. In areas where the water level of the river is low and boats drag across the riverbank, a system of locks and dams has been created. Using these dams controlled by the United States Army’s Corp of

Engineers, water levels are increased at will in these spots on the river and these boats float through with ease and make it to the gulf at a much cheaper transport cost than they would if the products were transported on trucks through the road system.

The farmers also use GMO seeds, which give bigger yields and are easier and cheaper to grow. As a result the US ends up having cheap soy that is in demand globally. China in particular relies on US Soy for their swine feed as well as their edible oil consumption. This is what gives soybeans such an edge, and this year the US crop of soybeans is set to be more bountiful than ever. But as we know, it is this exact benefit that is a problem for Pakistani buyers.

The GMO issue in Pakistan

Let us take a step back here. You have a scenario in which Pakistan is a significant importer of oilseeds, but is unable to purchase it from the US because of regulatory issues. The regulatory issue in question has to do with the GMO status of the soybeans produced in the US.

This issue began in December 2022 in a dramatic episode that has been covered by Profit before.

To cut a very long story short, It all started with a technicality — but a technicality that was being ignored for a few years. On October 20, 2022, two shipments were stopped at Port Qasim in Karachi. The shipments contained GMO oilseeds worth some $100 million on board. And despite the very vocal protestations of the importers that had paid for the consignments, they stayed stuck at the port pending a single certification from the ministry of climate change. The climate ministry was concerned that the oilseeds were GMOs. In the months that followed, more vessels joined the two stuck at Karachi and the value of the oilseeds piling up at the port grew over $300 million.

Now, it is worth pointing out here why the shipments of GMO oilseeds were stopped. There is a general fear of GMOs in many places across the globe, fears that are completely unfounded and not based in any scientific research.

The reality is that farmers and agricultural scientists have been involved in genetically modifying the food we eat for a very long time. “For many decades, in addition to traditional crossbreeding, agricultural scientists have used radiation and chemicals to induce gene mutations in edible crops in attempts to achieve desired characteristics,” reads an article by Jane Brody published in The New York Times back in 2018.

This is where there is a parting of ways,

and one that is very important to understand. Everyone is agreed that genetic modification has been in place for centuries now. Farmers have used cross-breeding or both livestock and crops to achieve better yields and resistance to weather. What is new, however, is that there are now possibilities of extracting genes from other organisms and including them in different organisms. For example, to make a certain maize crop more resistant to cold, scientists might extract a gene from a fish that swims in icy waters and inject it in the maize. It really is a scientific marvel, and at the same time it makes sense that eyebrows would be raised over this level of interference in nature. But by and large, the scientific community has upheld that GMOs are safe.

“Although about 90% of scientists believe GMOs are safe — a view endorsed by the American Medical Association, the National Academy of Sciences, the American Association for the Advancement of Science and the World Health Organization — only slightly more than a third of consumers share this belief,” states a report from the United States Food and Drug Administration (FDA).

And that is the crux of the problem. Even though the scientific evidence is overwhelmingly in the favour of GMOs, the public perception of GMOs is unfavourable. This is mostly coming from the same brand of pseudo-science that promotes homoeopathic remedies over actual, tested, medicine that works and peddles crystal therapy and all manners of snake-oil.

Robert Goldberg, a plant molecular biologist at the University of California, Los Angeles, says that such fears have not yet been quelled despite “hundreds of millions of genetic experiments involving every type of organism on earth and people eating billions of meals without a problem.”

The main problem is that science rarely uses definitive language when a sample size is small or relatively new. In the case of GMOs, for example, scientists maintain a regular

level of human error and make statements like “foods have not shown any harmful effect,” rather than saying categorically that a certain food does not have harmful effects.

“You never know for sure, because you can’t prove a [universal] negative. After more than a quarter century of growing GMO crops in North America, no detrimental impacts have been detected in North America compared to Europe, where people have been exposed very little to GMOs,” says Goldberg. Meanwhile, the benefits from GMOs have been authoritative.

“By engineering resistance to insect damage, farmers have been able to use fewer pesticides while increasing yields, which enhances safety for farmers and the environment while lowering the cost of food and increasing its availability. Yields of corn, cotton and soybeans are said to have risen by 20% to 30% through the use of genetic engineering,” writes Brody.

“Can you, in fact, feed the 9 billion peo-

ple we’ll have by 2050 … and how do you do that with minimal ecological impact? “I think the way to do that is through food science,” says Dr Goldberg. “I see no difference between manipulating a gene the classical way, through breeding, or by adding a gene.”

All of this is to establish that GMOs are safe by all accounts and nothing to be feared. Despite this, their acceptance in Pakistan is low. When the oilseed shipments in Pakistan were stopped in 2022, it was followed by a huge ruckus raised by then food minister Tariq Bashir Cheema, who announced he would suggest people stop eating chicken because it was “toxic”. These unfounded fears have caused more harm and confusion than anything else.

What could be …

In the middle of all this, Pakistan’s soybean extractors are caught in an unenviable position. They have seen firsthand the benefits of soy and the effect it has on pricing, but because of the fear mongering regarding GMOs they are unable to purchase the cheap soy available. That does not stop the appetite for soy in Pakistan, and instead for expensive oil and soybeans have to be imported from other parts of the world. There is also the issue that US soy is some of the highest quality in the world when it comes to nutrition and results for the poultry industry.

The reason given for blocking the shipments was that Pakistan is party to the Cartagena Protocol Biosafety to the Convention on Biological Diversity, signed in 2001 and rectified in 2009. The Cartagena Protocol is an international treaty governing the movements of living modified organisms (LMOs) resulting from modern biotechnology from one country to another.

Its purpose is simple. One of the observations scientists had after genetically modifying different crops was that when certain modified plant varieties are introduced to new environments, the results can be disastrous for the local ecology. As a result, to make sure there is no unchecked introduction of GMOs to new environments, the Cartagena Protocol monitors this. And as part of the Pakistan Biosafety Rules of 2005, the ministry of climate change needs to give approval to any new GMO shipments coming into the country.

Before 2022, soybean extractors had been importing GMO soybean oilseeds mostly from the United States. However, they had been getting away with it since the climate change ministry had not been paying attention to the issue. In 2022 the ministry refused to grant the required approval triggering the crisis.

The GMOs that are being talked about here are not for sowing. The oilseeds being imported are simply pressed and their oil extracted. The mulch that is left behind is used

to create ‘cakes’ that are then fed to poultry. So the Cartagena Protocol really does not have any involvement here. Then there is the other claim: that since Pakistan’s poultry has been eating meals made from oilseeds that are GMOs, the harmful traits on those GMOs are transferred to the chickens and from there to the people that eat them.

The issue is succinctly explained by Shakil Ashfaq, the CEO of Shujabad Agro Industries. “GMOs for processing are regulated commodities but the legal framework for its import approval was incomplete as Pakistan Biosafety Rules 2005 lacked provisions for imports of GMO grains under the Food or Feed or Processing (FFP) category, and addressed requirements for cultivation only which are understandably much more complex,” he says.

The categorisation of FFP is for foods such as soybeans which are not being planted but are instead only an input either in processing of food or in the feed of animals that eventually become food.

“PSEA has been pushing the relevant authorities in EPA and MNFSR to complete the framework since 2018 but to no avail. All relevant authorities were fully aware that the oilseeds were GMOs. In October 2022, some vested interest groups raised the issue which resulted in imports being abruptly halted at a huge risk and cost for importers. Impact: Starting in around 2000, the local poultry industry had made remarkable investments in its value chain. This was followed, in 2015, by a change in the feed formulation to a corn-soybean diet which resulted in significant gains in the Feed Conversion Ratios (FCR, the ratio of feed consumed and bird weight achieved). The net impact of these remarkable initiatives was a significant decline in poultry products’ prices in real terms, making chicken meat and eggs the cheapest protein sources in the country. For comparison, a kilo of chicken meat which cost more than a kilo of beef prior to 2000, hovered at less than 40% of the cost of beef over the last decade. The poultry industry was devastated

by the unavailability of soybeans resulting in steep rise in poultry prices. The local corn crop has also been affected by this crisis as poultry was the main market for it.”

The inability to get these GMO oilseeds has serious business implications for soybean extractors. The average premium for nonGMO soybeans is around $150 per ton. So if the market is 2 million tons, the total yearly impact is around $300 million. Furthermore, higher cost of poultry resulting from 30% higher soybean meal cost kills demand which further affects the feasibility of poultry farming. Only 12% of Pakistan’s edible oil demand is met through indigenous sources. In the absence of soybeans, we end up importing more soybean oil and lose the opportunity to have value addition in the country by importing raw material instead of finished products.

“GMOs have been widely misunderstood across the globe. Two to three decades ago, they faced significant opposition—a common reaction to new scientific developments. However, as scientific evidence has become clearer, the world has gradually accepted GMOs. Historically, we have been slow to fully understand new technologies. Politicians and bureaucrats often lack the willingness to take responsibility, finding avoidance a safer strategy. In the absence of a scientific and knowledge-based environment (and undue reliance on myths rather than science), the public is more prone to misconceptions, often viewing new developments as schemes driven by “mafias” seeking to profit,” explains Mr Ahsfaq.

And that is really what it comes down to. Pakistan is not in an ideal position when it comes to oilseeds. The country is reliant on imports which are a drain on national resources as it is. At the same time there is increasing reliance on soybeans and other oilseeds within Pakistan. What is the answer? We can say with quite some certainty that it is not to block local companies from buying the soy they want because of some unfounded fear. n

OPINION

Asif Saad

Why do Pakistani businesses fail at innovation?

As a society, our culture wants us to conform and follow a laid-down path in life. Innovation requires breaking out of this which means facing our worries about failure, criticism, and the potential adverse impact on our careers

When was the last time we heard of a Pakistani business doing something different?

Something which has not been done before?

My memory fails me, perhaps for my age, and I would happily stand corrected. But in over 30 years of partaking in and observing our businesses and companies, I can’t recall any time we had provided the world with a new idea, a business model, a strategy, or anything. Perhaps, as individuals, we feel it is enough of a risk to be living and working in Pakistan and therefore why do something different in work or business? The modus operandi is to survive.

However, I contend that Innovation needs to be at the centre of our businesses, the driving force, so to speak. If your organiza-

The writer is a strategy consultant who has previously worked at various C-level positions for national and multinational corporations

tion cannot continuously reinvent itself, it will gradually become extinct. I understand that this subject deals mostly with ambiguity whereas, as leaders, we are always trying to create more certainty in our business. This creates tension and anxiety in our decisions. But then, this is exactly the kind of uncertainty our leaders should be trained to deal with. We should be able to place bold bets in the face of uncertain outcomes and should be able to persevere with our decisions.

Take any of the global giants today and you will find this to be the common factor in their success. Could Tesla, Apple, Google, Amazon and many other businesses exist without their leaders making a high-risk bet on a new technology, a different business model or creating a new market?

Given innovation’s critical importance in driving growth, it is a subject worth spending time over. When we imagine Pakistani businesses, think of the largest sectors such as textiles, banking, chemicals, or even information technology. Where do we see evidence of bold moves? On the contrary, we continue to do the same things in the same ways that our forefathers did. Or we borrow ideas from somewhere else and copy the same, in droves.

“Bher Chaal” – doing the same things which others do, is the innovation strategy for most Pakistani companies.

What do we fear?

In the business world, the fear of financial loss or its impact on our careers is the biggest fear and if such worries continue to exist for long periods at the topmost levels, we can imagine risk aversion leading to mostly continuation of status quo. If people are insecure that they will lose their wealth or their income for taking risks, it is likely for the business to decline over time.

Another barrier to innovation is dealing with uncertainty and its accompanying loss of control. Such fears trigger the pursuit of more certainty in outcomes and hence the desire for guaranteed returns! Sounds familiar? In most Pakistani companies, leaders seeking more control over outcomes end up prioritizing incremental steps that they perceive as less risky but are also much less ambitious.

We also fear criticism, much more so than other societies. This is another big hurdle to innovation as people don’t wish to be seen doing something out of the ordinary. Group conformity leads to a lack of innovation and therefore, sadly, to mediocre outcomes.

Such fears have caused value destruction in many sectors. For example, in the Automobile industry in Pakistan, the traditional players, despite having access to the latest technology, continued to play safe and sell obsolete engines in this market to protect their existing profitability.

Until recently, when new producers entered the market and started hurting their sales by offering new hybrid and EV engines packed with superior options!

Or take the case of a commodity chemical business which allowed new entrants to enter the market by its decision to grow incrementally instead of catering to the entire market demand. This eventually led to it losing market share and pricing power.

The retail apparel industry in Pakistan is a classic case of everyone selling the same products with negligible differentiation. When you take off the label, it is impossible to tell the brand. This group think has sadly led industry leaders to follow the crowd, much to their own detriment.

There are scores of similar examples of missed opportunities and value destruction which has impeded profitable growth across many sectors.

How can this be solved?

Businesses wishing to build a thriving culture of innovation need to embed it within their organisations. First, they need to build processes which

allow disagreements with leaders/owners to take place. And this needs to be cascaded to the lowest level of employees. Pakistani businesses wishing to innovate must get out of the God syndrome attributed to owners and bosses. It is so prevalent in our businesses, bordering on the scale of a rampant sickness.

Second, companies looking to innovate need to have people who are willing to challenge the status quo. Stop hiring yes men. So many of the people in leadership positions in Pakistan are born bureaucrats who practice the “cover my backside” management style. They will need to be replaced whenever the business looks to innovate. And once the right leaders are on board, it is up to the leadership teams to build optimism and consistently encourage risk-taking by framing innovation as fundamental to the organization’s success.

Third, establishing rituals is important to make innovation the norm rather than an occasional endeavour. Leaders in Pakistani organizations don’t invest enough in establishing routines such as innovation days, hackathons, and meeting-free days that senior management lead or at least participate in to signal innovation’s central role. Add to these rituals, the conferring of recognition

and rewards on innovators which will enable the organization to provide incentives for innovation.

In my opinion, it is this cultural piece which has been missing in Pakistan for the longest time. Businesses cannot innovate via innovation departments or when leaders try to become the biggest innovators themselves. It has to come from everyone, from the lowest to the highest rungs of the hierarchy, or it will not happen. The Owners and leaders role is only to create the right environment for this to happen.

By building a sense of belonging and safety through a shared commitment to innovation, companies can assure employees that it’s ok to experiment, ask questions, and provide feedback.

By having a sense of psychological safety, an innovation-centric purpose, and explicit encouragement and rewards, leaders can help employees at all levels find the courage to risk failure in pursuit of new and different solutions.

One of the best known innovators of yesteryears thought about innovation in a very different way. Thomas Edison famously said about his experiments, “I have not failed. I’ve just found 10,000 ways that won’t work”. n

Did paint manufacturers shoot themselves in the foot going to the CCP?

The CCP’s decision to fine Diamond Paint opens a can of worms that will implicate all paint manufacturers in a malpractice that might not make all that much sense

Profit report

We must begin this story by commending the Competition Commission of Pakistan (CCP). It seems that the regulatory law enforcement authority has finally woken from its slumber after more than a year and a half in which it did not issue a single order.

The CCP normally ends up issuing at least a handful of orders every year. In the years preceding the interlude, the body issued between 8-11 orders annually. So it was strange when the CCP went missing in action from January 2023 to the 31st of July 2024.

The month of August, however, has marked a bit of a resurgence. In the span of the month of August, the CCP issued three different orders finally breaking its dry spell. However, the CCP might be a little over eager getting back on the horse.

One of the three recently passed orders has to do with the paint industry. The complaint was originally filed by Nippon Paints against Diamond Paints. In their complaint, Nippon claimed that Diamond was using deceptive marketing tactics. What misrepre-

sentation was Nippon claiming? According to them, Diamond Paints was being deceptive by not disclosing that their paint contains ‘tokens’. Now, if you’ve lived through the early 2000s and the campaign by Master Paints that followed, you’ll know tokens are a pretty contentious issue in the paint industry. But why would Nippon claim Diamond is engaging in deceptive marketing techniques by not disclosing in their television ads that their paint has tokens?

Because the CCP is of that opinion. In fact, the CCP had demanded these declarations in an earlier order some years ago. It just so happened that the entire paint industry decided to not really implement it and nobody seems to have followed up. Until Nippon decided to one-up Diamond in this way. Now, the dynamics in the entire paint industry’s marketing departments are changing, and tokens seem to be on everybody’s mind. So let’s start there.

The token story

It all started in the mid-1990s, when a small boom in construction, combined with a large number of new entrants in the paint manufacturing market, led to

a serious increase in the level of competition in the paint market in Pakistan. Companies were desperate for market share and willing to offer massive discounts in order to be able to get it. According to market research conducted by Nippon Paint Pakistan, 60% of paint buying in Pakistan is conducted by the labourer doing the actual painting. Another study found that 70% of consumers and painters stated that the advice of the painter was critical to the decision of which paint was purchased for a paint job.

Under these circumstances, while offering a discount on the wholesale or retail price of the paint would help somewhat, the companies looking to entice more buyers of their paints had to find a way to make sure that it was the labourer who got the discount, even though he was not the one paying for it.

The token was an innovative practice invented in the mid-1990s, and it was meant to solve the decision-maker/purchaser dichotomy. Before the anti-token campaign by Master paints, which was followed by litigation in Competition Commission of Pakistan, tokens were strictly speaking not illegal and soon every company realized the sheer genius of the scheme. Paint manufacturers started placing

tags or stickers on each paint box with an amount of money written on it. That tag or sticker came to be known as the token, and could be redeemed at any paint retailer or wholesaler for cash. In order to ensure that it is the painter and not the homeowner who gets the cash from the token, paint companies place the token inside the paint bucket at the bottom, in a concealed packet underneath the actual paint. This is designed to ensure that the person doing the painting would be the first person to be able to access the token. With the introduction of the token, the labourer all of a sudden saw their incentives flipped. Prior to the advent of the token, the labourer would either buy the cheapest paint or the one with the highest quality, or else a good combination of price and quality, depending on the needs and ability to pay off the person getting their house painted. Now, however, the labourer did not care about price or quality, but instead about which paint company was offering the highest redemption value for the tokens on their paint boxes. In other words, the painter was being offered a bribe. Naturally, the paint industry did not want to advertise this. Ideally, the concept of tokens would have gone unmentioned. Sort of secret only known by painters and not by those buying the paint. But there was one company that was not using tokens in their products: Master Paints. As a result, painters started recommending people don’t buy it, and their business suffered. What they decided to do was launch a marketing campaign that pointed out the presence of tokens in other brands. This was the origin of the iconic “Token se Zara Bach Ke” tagline from one of the most recognisable ad campaigns of that time period. And that is when the CCP first got involved.

Token disclosures

In 2011, the Competition Commission of Pakistan, then chaired by activist chairman Khalid Mirza, decided to take action against the practice of placing tokens that were clearly designed to benefit the labourer at the expense of the end consumer. Over a period of seven months, beginning in June 2011, almost all of the major paint manufacturers in Pakistan submitted public documents explaining their marketing practices of using tokens for the very first time. The hearings were a fascinating insight into the corporate culture of the companies involved in the paint industry.

The most forthright was Nippon Paints Pakistan, which admitted that it started the practice in 2009, two years after entering the Pakistani market and discovering that tokens were standard market practice. They admitted that the target of the token is the

painter, and not the end consumer and that the purpose is to persuade the painter to buy their paint, or recommend to the homeowner to buy their paint.

That’s right, this is the same Nippon Paints which has now used the CCP’s 2011 judgement to go after Master Paints. Remember, Master was the only paint brand not using tokens, which means Nippon too relies on them.

After three hearings over a period of seven months, the Commission issued an order on January 13, 2012, and found that the use of tokens without proper disclosure constituted deceptive marketing practices, and was a violation of Section 10 of the Competition Act of 2010. The commission ordered paint manufacturers to begin prominently disclosing both the existence and the redemption value of tokens on the paint buckets. The order read as:

“The disclosure with respect to the token on the paint pack as mentioned at (i) above should be made with the use of bright/ conspicuous colours distinct from the colour of the packaging of the paint pack and should be printed in clear, bold and legible size.”

The decision was made. One can argue over whether or not it was a good one or not. After all, what exactly is the point of these disclosures? They don’t really determine or have anything to do with the quality of the paint. On top of this there is an advertising angle here. The CCP usually gets involved when there is deceptive marketing involved. What is deceptive about not disclosing the presence of tokens? These were all questions that some paint makers still had on their minds. Even though the decision was made, the CCP’s order was very quietly ignored. However, multinationals like AkzoNobel (formerly ICI), Nippon and a few local companies in the interest of best practice decided to follow this. That is where the CCP’s latest order comes in.

Nippon has a bone to pick

The paint industry in Pakistan has many players and they aren’t always the nicest to each other. Nippon decided it would go for Diamond and filed a complaint with the CCP. The subject of a complaint was a regular television advert for its product ‘Durasilk’ run on various television channels. There is a back and forth between Diamond and Nippon whereby Nippon made this complaint, and Diamond responded by saying Nippon’s use of the term “Asia’s Number 1 Paint” is also deceptive marketing.

But the CCP was quick to make a decision on Nippon’s complaint because there was already a decision from them with precedent. It is, however, interesting to see the

defence that Diamond Paints put up because it has some good points to make. Diamond’s lawyers pointed out first that the complaint fails to explain how the TVC misled consumers regarding the product. Then there is the other problem. Every TVC is limited in its time and other print ads are limited in their space. Are paint manufacturers now expected to use longer ads and spend money on ad space to run disclosures not regarding their products but the presence of what is an industry-wide practice?

It was the sort of case that could have gone in either direction. However, the CCP ruled in the favour of Nippon. The CCP bench emphasised that proper disclosure of tokens is critical for customers. Marketing techniques that include redeemable coupons have a substantial impact on customer purchasing decisions. They also slapped Master Paints with a fine of Rs 50 lakhs. But in the aftermath of this decision, the effects will be felt beyond just Diamond Paints.

Could it come back to bite everyone?

What this means is that all paint ads are now fair game. Master Paints, for example, could have a field day finding TVCs without appropriate disclosures and complaining about them to the CCP to have their competitors fined and give them negative press. Even Nippon Paints, which filed the case, admits that they might possibly have to rethink their marketing strategy in the wake of this decision.

A company representative tells Profit, “It might affect Nippon too. But as far as the disclaimers are concerned, Nippon has never participated in deception marketing knowingly. All the content and products (that contain tokens) have always been disclosed - on cans and in campaigns so we don’t see a reason why the competitors shouldn’t do it too. It definitely affects business as it discourages people to buy products with in-can incentives but customers have the right to know. For customers who want products without tokens, we have a separate product range to accommodate them too.”

“Our hope is ideally every brand should start to include disclaimers in their campaigns at least on wider mediums. This change will help customers understand the market and little more and make an informed decision.”

The decision of CCP essentially makes life difficult across the board for manufacturers in the paint industry. In the days to come, it will be interesting to see if matters go back to a quiet agreement between all parties to ignore the decision, or whether they will now have to take the decision more seriously. n

From incubation to acceleration,

are Pakistani ESOs really serving the startup ecosystem?

The mushroom growth of these programs in the country raises questions about their efficacy

By Hamza Aurangzeb

As we enter 2024, Pakistan’s once-promising startup scene finds itself in the midst of an investment winter. Venture capital and private investors, once eager to tap into the potential of this emerging market, have largely retreated. The funding slowdown that began in 2023 has now ground to a halt, with the first two quarters of 2024 passing without any substantial funding rounds.

For Pakistani startups, this drought presents a formidable challenge. Limited dry powder, erratic macroeconomic indicators, and unpredictable government policies have created a perfect storm of adversity. Yet, in this tumultuous landscape, a beacon of hope emerges: the country’s network of incubators and accelerators.

The Lifeline: Incubators and Accelerators

In these trying times, incubators and accelerators can play a crucial role in sustaining the country’s entrepreneurial spirit. These entities serve as the nurturing grounds for innovation, providing vital support to fledgling startups.

Incubators focus on early-stage startups, offering a cocoon of support where ideas can germinate and grow. They provide mentorship from seasoned entrepreneurs, initial capital funding, logistical support, and invaluable networking opportunities. Their programs, often lasting from six months to several years, aim to transform raw ideas into investable businesses, usually without taking equity.

On the other hand, accelerators work with startups that have already found their footing. These intensive, short-term programs lasting three to six months are designed to catapult startups to the next level. With a rigorous curriculum, expert mentorship, capital funding, and direct access to potential investors, accelerators prepare startups for rapid growth. The culmination of these programs is often a “demo day,” where startups pitch to a room full of eager investors, hoping to secure the funding needed to scale their operations.

While the modern incubators and accel-

erators may seem like a recent phenomenon in Pakistan, its roots trace back to the early 2010s. This period marked the beginning of a transformative era, as the country witnessed the emergence of pioneering incubators and accelerators that would lay the foundation for today’s vibrant startup landscape.

Among the trailblazers was Plan9, launched in 2012 by the Punjab Information Technology Board. Named after the cult science fiction novel “Plan 9 from Outer Space,” this tech incubator aimed to defy expectations and nurture groundbreaking ideas. Situated in Lahore, Plan9 quickly became a beacon for aspiring entrepreneurs across the country.

Around the same time, Invest2Innovate (i2i) entered the scene, bringing a fresh perspective to startup acceleration. Founded by Kalsoom Lakhani, a Pakistani-American entrepreneur, i2i sought to bridge the gap between Pakistani startups and global investors. Its four-month acceleration program didn’t just focus on business fundamentals; it aimed to create a new generation of ethical, impactful entrepreneurs.

The National Incubation Centre (NIC)

More recently, the National Incubation Centre (NIC), a public-private partnership that has emerged as the backbone of the country’s startup support system. Established by the Ministry of Technology and Telecommunication in collaboration with the Ignite Technology Fund, the NIC has cast a wide net across Pakistan.

From the bustling metropolis of Karachi to the historic city of Lahore, and from the capital, Islamabad to the valley of Quetta, NIC has established centers in eight cities. Each center operates independently of the other, but collectively they are capable of nurturing 245 startups annually. But there is more to it. The government claims that these centers have supported over 1,480 startups, of which more than 710 have successfully completed the incubation program.

Further, as per official claims, NIC-supported startups have created over 128,000 jobs, raised a staggering Rs. 23 billion in investments, and reported revenues of Rs. 16 billion.

Perhaps most encouragingly, the initiative has provided support to more than 2,800 female entrepreneurs, fostering a more inclusive startup ecosystem.

As Pakistan’s startup landscape matures, so too does the NIC’s approach. Recognizing the need for specialized support, the authorities are now focusing on industry-specific incubators. In Faisalabad, an agri-tech incubator is nurturing startups at the intersection of agriculture and technology. Meanwhile, in Rawalpindi, an aerospace-focused incubator is helping startups reach for the stars.

Corporations as Catalysts

While government initiatives like the NIC play a crucial role, private corporations are also increasing their footprint in Pakistan’s startup ecosystem.

NetSol Technologies, a stalwart in Pakistan’s tech industry, operates Nspire, an incubator that doubles as an impact investor. Nspire, as per its mission statement, goes beyond mere profit; it seeks to create an environment where startups can flourish and create meaningful societal impact. With a particular focus on fintech ventures, Nspire is NetSol’s attempt to diversify its portfolio of offerings.

In the telecommunications sector, giants like Telenor and Jazz are not content with being mere spectators. They’ve launched their own accelerators, Velocity and Xlr8 respectively, as part of their strategic shift towards becoming full-service digital companies. These accelerators were conceptualized to serve as laboratories of innovation, where startups can leverage the telcos’ vast technical expertise, digital infrastructure, and customer base to develop and scale new products and services.

As per Jazz, Xlr8-backed startups have raised Rs. 1.4 billion and generated a revenue of Rs. 543 million, with 25 startups graduating from the program. Telenor claims that Velocity has helped 42 startups raise an impressive $6.8 million. These accelerators claim to not just be launching pads for startups; but are building bridges between Pakistan’s corporate giants and its next generation of entrepreneurs.

“Jazz xlr8 has laid the foundation for a sustainable technology ecosystem, and provides the resources and expertise to help

Plan 9 Incubator 2012 Government-led Lahore Incubator set up by Punjab Information Technology Board (PITB)

WomenX Incubator 2014 Private Islamabad A program initiated by the World Bank for women-led businesses

WECREATE Incubator 2014 Private Islamabad Coworking and incubation space by TiE Islamabad, funded by the US State Dept.

Social Innovation Lab Incubator 2013 Private Lahore Incubator for social enterprises housed initially at LUMS

LUMS Center for Incubator 2014 University Lahore University’s incubator which later Entreprenuership became NIC Lahore

The Nest I/O Incubator 2015 Private Karachi Established by the Pakistan Software Houses Association (P@SHA)

Founder’s Institute Incubator 2016 Private Islamabad, Karachi Global incubator with chapters in two cities in Pakistan

Revolt Incubator 2016 Private Peshawar An initiative of Peshawar 2.0, an entrepreneur support orgranization

TechValley Abbottabad Incubator 2015 Private Abbottabad Coworking space and incubation center which later became part of KIPTB’s Durshal network

Seed Ventures Incubator 2009 Private Karachi Seed Ventures operates a diverse set of incubation centres across Pakistan

NSPIRE Incubator 2016 Private Lahore Set up by Netsol Technologies.

NUST Technology Incubator 2005 University Islamabad One of the earliest incubation centers in Incubation Center Pakistan focused on tech startups, now the National Science and Technology Park (NSTP)

IBA Center for Incubator 2011 University Karachi University incubator open to all types Entreprenuerial Development of entrepreneurs

Ignite’s National Incubation Incubator 2017 Private, Islamabad The first NIC which started operations in early Government funded 2017

Invest2Innovate Accelerator 2012 Private Islamabad An accelerator which assists impact entrepreneurs over four months each year

Plan X Accelerator 2014 Government-led Lahore PITB established an accelerator as the next step for startups graduating from the incubation program, Plan 9

10XC Accelerator 2016 Private Karachi The accelerator offered equity-based funding, advice, and shared ser vices to startups

Source: Ignite

Jazz xlr8 has laid the foundation for a sustainable technology ecosystem, and provides the resources and expertise to help entrepreneurs fulfil their potential, and scale their businesses. It is a first-of-its-kind technology hub, launched as a digital accelerator. Jazz Xlr8 provides in-kind support for startup growth and does not take any equity. Jazz Xlr8 does not directly invest in any startup

Salman Iqbal, Manager, Usability and Design at Jazz

entrepreneurs fulfil their potential, and scale their businesses. It is a first-of-its-kind technology hub, launched as a digital accelerator. Jazz Xlr8 provides in-kind support for startup growth and does not take any equity. Jazz Xlr8 does not directly invest in any startup,” remarked Salman Iqbal, Manager, Usability and Design at Jazz.

But does it work?

Amidst the challenges, success stories are emerging that highlight the potential of Pakistan’s startup ecosystem. One such story is that of Y-pay Financial Services, a graduate of NIC Karachi’s Cohort 5.

Founded by computer science graduates Furqan Karim and Sarfaraz Shahid, Y-pay is a wealth management company targeting Pakistan’s youth. Their app makes investing in mutual funds accessible and understandable for first-time investors, democratizing access to capital markets. The startup is backed by international investors like On Deck, and its co-founder, Furqan Karim, has been a part of Antler’s Entrepreneur in Residence program. Reflecting on his journey with NIC, Furqan Karim stated, “NIC is like a home to many Founders like me. It’s not just a physical space but a strongly bonded community of budding entrepreneurs where we go through thick & thin together.” This sense of community, of shared struggle and success, is perhaps the most valuable asset that incubators and accelerators provide to Pakistan’s startups.

A pipe dream?

Despite these success stories, Pakistan’s startup ecosystem faces significant challenges. Many incubators and accelerators struggle with sustainable funding models, often relying heavily on government or corporate partnerships. This can limit their financial resources and, consequently, their impact. The

ecosystem also grapples with a shortage of experienced mentors, particularly in advanced domains, which can hinder the growth of more specialized startups.

Infrastructure remains a challenge, with many incubators and accelerators concentrated in major cities like Karachi, Lahore, and Islamabad. This urban-centric approach leaves entrepreneurs in more remote regions underserved. Moreover, the limited network of investors and partnerships with universities and research institutions can constrain the flow of knowledge and expertise crucial for startup growth.

Yet, these challenges also present opportunities. The current funding squeeze, while difficult, is coercing startups to focus on fundamentals and develop more robust business models. Incubators and accelerators are adapting, with some exploring specialization to better serve niche markets. There’s also a growing recognition of the need to expand beyond major cities, with initiatives like NIC’s plans to establish centers in tier 2 cities like Sialkot.

Lessons to be learned

As Pakistan’s startup ecosystem evolves, there are valuable lessons to be learned from more mature markets. In the United States, for instance, Y Combinator (YC) has set the gold standard for startup accelerators. Having funded over 5,000 startups with a combined value of $600 billion, YC’s impact dwarfs the entire GDP of Pakistan.

What sets YC apart is not just its financial clout, but its comprehensive approach to startup support. From dedicated mentors to an extensive investor network, from a private social network connecting founders to a vast talent pool for hiring, YC provides a holistic ecosystem for startup growth. Its investment model, which includes both upfront funding and potential follow-on investments,

aligns the accelerator’s interests closely with those of its startups.

While Pakistan’s ecosystem may not yet match the scale of Silicon Valley, it can certainly draw inspiration from these models. The focus on building strong networks, providing comprehensive support beyond just funding, and fostering a global outlook from day one are lessons that Pakistani incubators and accelerators are increasingly taking to heart.

What lies ahead?

As we look to the future, there’s cause for cautious optimism. The $1 billion raised by Pakistani startups over the past decade is a testament to the ecosystem’s potential. While the current investment winter poses challenges, it also presents an opportunity for consolidation and refinement.

Incubators and accelerators are at the forefront of this evolution. They’re not just weathering the storm; they’re helping startups navigate through it. By focusing on fundamentals, fostering innovation, and building resilient business models, these institutions are laying the groundwork for the next wave of Pakistani startups.

The road ahead will not be easy. Pakistan’s startup ecosystem will need to overcome significant hurdles, from macroeconomic instability to regulatory challenges. But with the continued support of incubators, accelerators, and a growing network of mentors and investors, Pakistani startups are poised to not just survive, but thrive.

In the grand tapestry of global innovation, the country’s startup ecosystem may still be a small patch. But it’s a patch that’s growing, evolving, and increasingly catching the eye of the world. As incubators and accelerators continue to nurture the seeds of innovation, Pakistan’s entrepreneurial landscape is set to bloom, one startup at a time. n