08 Citi Pharma gets FDA nod to start exporting nutraceuticals to the United States

10 Can fintech help finally unlock financing for small businesses?

17 Fauji’s bid for Agha Steel: is it the right move?

20 Despite a thriving pharma industry, Pakistan does not manufacture any condoms

22 Lahore Gymkhana pays Rs 417 every month in rent. Does the Punjab Govt have what it takes to make them pay their fair share?

27 Abhi partners with TPL to buy out FINCA Microfinance Bank

27 Are Islamic Banks taking their customers for a ride?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

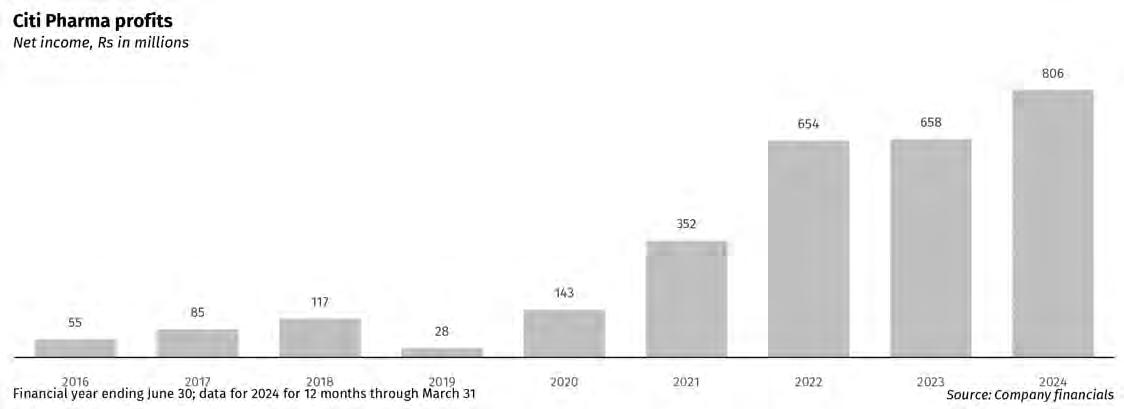

Citi Pharma gets FDA nod to start nutraceuticalsexporting to the United States

The pharmaceutical ingredients manufacturer enters the consumer-facing market in the US with a product the US regulator classifies as food, and not drugs

CBy Profit

iti Pharma, the Lahore-based drug manufacturer and the country’s largest producer of active pharmaceutical ingredients (APIs) is set to begin exporting nutraceutical products to the United States after the US Food and Drug Administration (FDA) allowed its products to gain access to that market.

In a notice sent to the Pakistan Stock Exchange on Friday, the company stated that intended to export products in fertility, weight management, stress and mood boosters, hair and skin care, and joint and muscle pain.

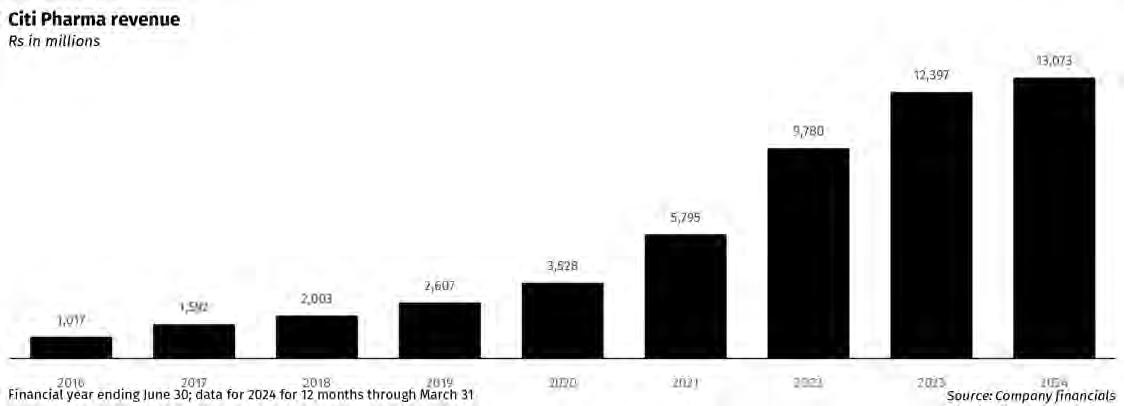

The company expects to generate $3 million (Rs832 million) in export revenue from these products, and expects profit margins in the 2530% range, though it did not specify whether those would be gross profit margins or net profit margins.

The revenue number would amount to a 6.4% increase in the company’s revenue, based on the revenue data for the 12 months ending March 31, 2024, the latest period for which financial statements are available.

While the company consistently used the phrase “FDA approval” in its announcement, that phrase has a meaning in this context that is different from what “FDA approval” normally means. Specifically, neutraceuticals are governed under a distinct regulatory cate-

gory for dietary supplements, treating them as a subset of foods rather than drugs.

Nutraceuticals, as with all other dietary supplements, face a far less rigorous regulatory process. Under the Dietary Supplement Health and Education Act of 1994, manufacturers can produce and sell these products without FDA pre-market approval. The onus falls on the companies to ensure product safety and proper labeling before hitting store shelves.

In contrast, pharmaceutical drugs must run a gauntlet of clinical trials and FDA scrutiny before reaching consumers. This process often takes years and costs millions of dollars, with no guarantee of approval.

The FDA does maintain some oversight of nutraceuticals post-market. The agency can

take action against unsafe or misbranded products and requires manufacturers to comply with Current Good Manufacturing Practices. However, this reactive approach differs significantly from the proactive stance taken with pharmaceuticals.

Critics argue this disparity leaves consumers vulnerable to potentially ineffective or harmful supplements. Proponents counter that it allows for greater consumer choice and access to natural health products.

Nonetheless, the nutraceutical market is massive, with global sales projected to reach $722.49 billion by 2027, and the bulk of that market being concentrated in the United States. And the ability to export into that large and growing market represents a coup for Citi Pharma, one of the fastest growing pharmaceutical companies in the country.

The company was founded in 1990 as a project of the Army Welfare Trust and was originally named Askari Pharmaceuticals, a company that manufactured pharmaceutical products, medical chemicals and botanical

products. It owned a factory in Kasur, which started production in 1996. In 2003, Askari Pharmaceuticals set up a second manufacturing unit in the same location for pharmaceutical formulation.

In March 2013, a group of five Lahore-based brothers acquired the company for Rs429 million ($4.4 million) and moved the company more towards the manufacture of active pharmaceutical ingredients (APIs). In the process of developing consumable medicines, APIs are mixed with other salts (inactive ingredients) to produce formulation.

Citi Pharma’s biggest customer, accounting for over 50% of revenue is GlaxoSmithKline (GSK) Pakistan, the local subsidiary of the British pharmaceutical giant. By far, the single biggest product in their portfolio is the active ingredient for Paracetamol (acetaminophen), the common pain medication. The company is the largest API manufacturer for Paracetamol, accounting for between 40-45% of the drug’s total volume in Pakistan, according to Citi Pharma’s CEO in a June 2021 interview with

Business Recorder.

Within the Pakistani API market, Citi is one of the two biggest companies. Its meteoric growth over the past decade resulted in the firm being able to list publicly on the Pakistan Stock Exchange in June 2021, raising Rs2 billion in what was only the second pharmaceutical IPO in over 30 years.

Somewhat unusually for such a company, the majority of the proceeds from the IPO went towards the construction of a new hospital in Lahore, and only a minority of those proceeds went towards the expansion of its manufacturing capacity.

This may stand to reason, given the background of the founding brothers. Amjad Nadeem, the eldest of the five brothers, and the one who owned 40% of the company prior to the IPO, appears to have made much of his money buying and sell real estate in Hong Kong, and even set up a real estate development company in Islamabad. It is possible they viewed a hospital as a healthcare-focused real estate investment. n

Despite all the State Bank and SECP’s attempts to help small businesses attract more financing, SME lending remains in the doldrums. Fintech could be part of the solution, but first everyone needs to admit that the problem is the FBR

IBy Hamza Aurangzeb

t is a dream that the State Bank of Pakistan (SBP) and the Securities and Exchange Commission of Pakistan (SECP) have been dreaming for a long time: getting more credit flowing to small and medium-sized businesses, the backbone of any economy, including that of Pakistan. And with the rise of fintech platforms, the dream feels tantalizingly close to reality.

The problem is that while technology can and does supply solutions to at least some of the bottlenecks that constrict the flow of credit to small and medium-sized businesses (SMEs), there would still be one that would trump them all: the Federal Board of Revenue (FBR), or more specifically, the approach of the federal government to setting tax policy.

Getting credit policy for SMEs – whether it be for a financial institution or a regulatory body – in any country not named the United States is incredibly difficult. And the State Bank in particular has been trying to balance the need to encourage this important avenue of credit while at the same time trying to manage the level of risk it would introduce to the banks’ balance sheets.

So what does it take to make it work? And is fintech really the key to helping unlock credit to SMEs in Pakistan? Possibly, but before diving into all of that, let us take a look at where things stand now.

The state of play

According to the World Bank, SMEs constitute around 90% of businesses globally, generating 40% of GDP and providing 50% of employment opportunities. Pakistan’s figures mirror these global trends, with 90% of business enterprises falling under the SME category, mostly operating in the informal economy. As of 2020, the country’s informal economy was estimated to account for 35%-56% of the official GDP.

The Small and Medium Enterprises Development Authority (SMEDA), using proxies like electricity connections for industrial, commercial, and agricultural sectors, estimates that there are currently 5.2 million SMEs operating in Pakistan. These SMEs contribute approximately 40% of Pakistan’s GDP, 30% of its exports, and employ around 78% of the non-agricultural labor force.

Despite the global consensus on SMEs forming the majority of private sector businesses, there is no universal definition for SMEs. Each country defines the segment using its own parameters such as number of employees, net revenue, output, investment, and value of total assets. The absence of a standardized definition has created dissonance among

various government factions in Pakistan, with each department following its own definition, undermining the efficacy of initiatives launched for SMEs.

While departments like SECP, SMEDA, and SBP have agreed on a single definition (a company with a revenue of up to Rs800 million), there are dissenting voices. The Federal Board of Revenue (FBR), as per the Finance Act 2021, defines SMEs as companies with revenue of up to Rs250 million. They argue that extending the revenue limit to include a broader category of companies for preferential tax treatment would deteriorate the tax base and incentivize companies to underreport sales.

SME financing has been a major bottleneck in Pakistan for decades. Traditional banks have historically been apprehensive of lending to the private sector, preferring to invest in government-issued treasury bills. This inclination is fueled by multiple factors, primarily the high-risk profile of the private sector, particularly SMEs, further exacerbated by the high interest rates that have dominated since the beginning of fiscal year 2020.

Loans to private businesses have grown at a mere 7% annually, while banks’ investments in government securities have ballooned by 17.6% per annum. Consequently, loans to private sector businesses stand at only Rs7.1 trillion, while banks’ portfolio of government securities has exceeded Rs. 35.8 trillion.

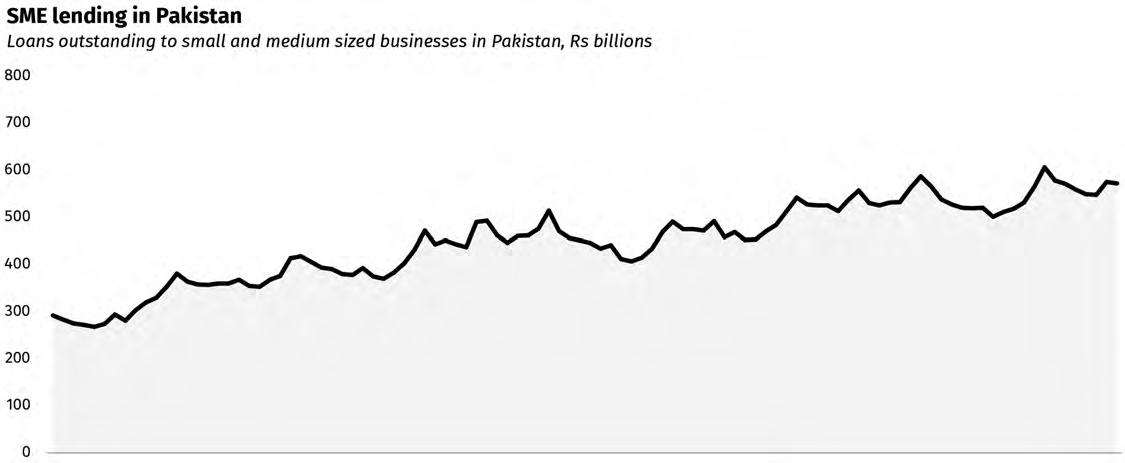

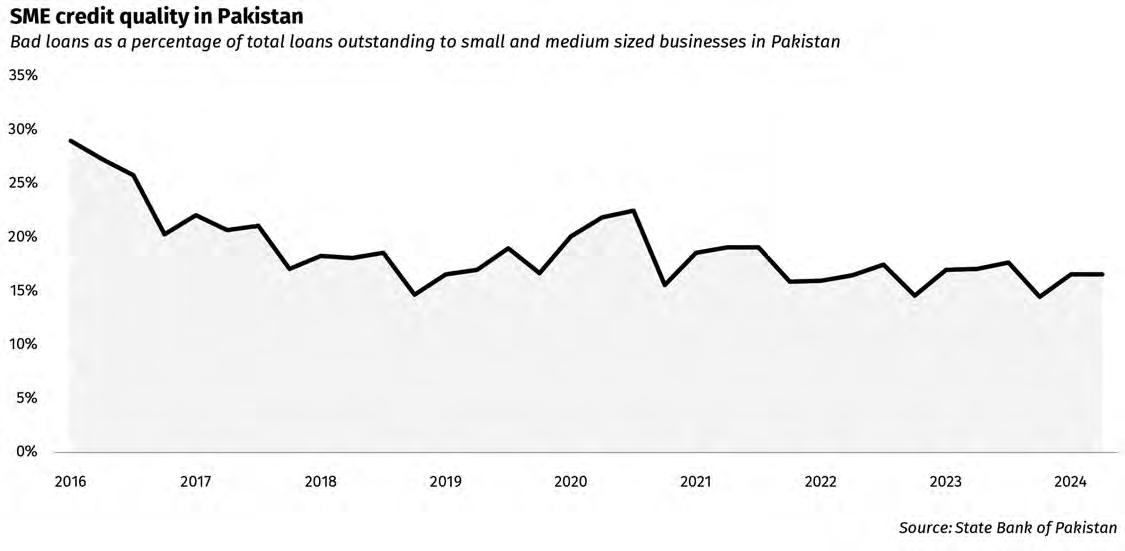

A closer look reveals an even more concerning picture: outstanding loans advanced by banks to SMEs stand at a paltry Rs572 billion, just 8.0% of total loans extended to private businesses, which itself is only 16.6% of the total credit. This means that SME lending constitutes only 1.3% of the total credit extended by banks in Pakistan.

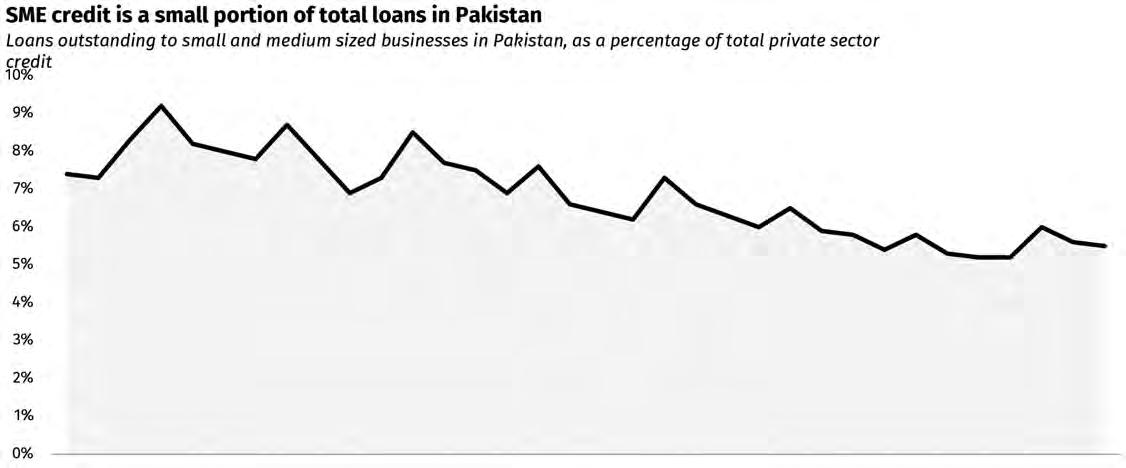

The growth in SME lending has been sluggish, with outstanding loans to SMEs increasing from Rs292 billion in December 2015 to Rs572 billion as of July 2024, representing an annual growth rate of just 8.1%. Moreover, the share of SME financing as a percentage of private credit has declined from 7.3% in June 2015 to 5.5% in June 2024, despite the Non-Performing Loans (NPL) ratio of the sector improving from 31.4% to 16.6% during the same period.

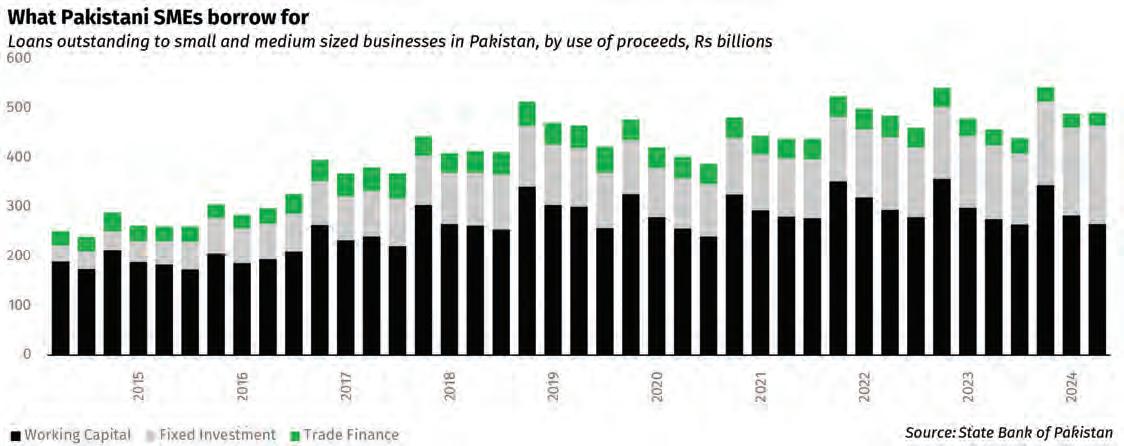

Analyzing the composition of credit extended to SMEs reveals that most of it (54.0%) is utilized for working capital requirements, while, 40.5% and 5.5% are used for trade finance and fixed investment, respectively, as of June 2024. These statistics underscore the significance of credit for working capital in the SME sector.

So why is the situation so bad? Because it is very, very hard to make SME lending work.

What it takes to make SME credit work

There are three main ingredients to helping make SME credit work:

1. Low-cost deposits

2. Low intermediation cost

3. Visibility and predictability of SME cash flows

The low cost of deposits is necessary because it is very costly to deploy capital into small business lending, and so the cost of capital needs to be low in order to accommodate that high cost (both of disbursing the loan, and of the higher loan losses).

This point is worth explaining a bit: it costs a bank a lot more money to disburse smaller loans than it does to disburse a large loan. Consider the following, very simplified scenario.

Suppose Engro Corporation comes to Habib Bank and asks for a Rs10 billion loan. The bank’s average cost of deposits is around 10%, but it can lend to Engro at, for example, just 0.5% above the State Bank’s benchmark interest rate of 17.5% so it makes 18% interest on that loan. That represents an 8% per year net interest margin, or about Rs800 million per year.

To disburse the loan probably took about 20 highly paid corporate bankers and treasury staff the equivalent of perhaps one week of their time (averaged across all individuals), meaning even if one assumes an average salary of Rs1 million per employee per month, the operating cost of disbursing this loan to HBL, in terms of employee costs, was around Rs5 million (rounding a week to be one-quarter of a month). Let us be generous and add on another Rs5 million in overhead costs, and it still only cost about Rs10 million to disburse a loan that generates Rs800 million in net interest revenue.

Now let us add the the operating costs of the branches that HBL needs to maintain in order to even have that Rs10 billion to lend. In 2023, HBL spent about Rs29.6 million in operating costs on its branches per Rs1 billion in deposits, meaning the Rs10 billion in deposits came in at an operating cost of Rs296 million.

Let us add in all of these and you still get Just Rs306 million in costs for Rs800 million in revenue. The math is straightforward: relative to the size of the revenue from a large corporate loan, the cost of actual disbursement of that loan is not very high at all. And there is, of course, a near-certainty that Engro will pay that loan back.

Now consider the example of SME lending. What would it take to disburse Rs10 billion worth of loans to small businesses, assuming an average loan size of Rs10 million?

Well, for one thing, that means giving out 1,000 loans. Let us assume you can charge significantly more interest – let’s say 25%. That would make the net interest margin on these loans about 15%, or Rs1.5 million per year.

Now subtract out the cost of the branch network, and you are left with Rs1.2 million in room to work with. Could you make a small business loan in that much? Maybe, but certainly not with the same caliber and compensation level of employees as the corporate bankers who made that loan to Engro.

So what would you need? You would need to essentially create an algorithm that decides who gets how much in loans so that even lower capacity employees are able to make decisions on whether or not to give the loan. But for that, you would have to assume that the financial statements being provided to you by the small businesses seeking the loans were reliable. And that they are likely

to pay the loan back and that you will not have to spend yet more money chasing after them.

None of those assumptions, of course, is true.’

And herein we arrive at the problem of small business lending. It is not the margins that are the problem. It is the information asymmetry: banks have no reliable way of knowing who is a reliable credit risk and has both the capacity and intention of paying them back. If that is not possible, then the margins simply do not matter.

Could technology help?

The SBP has launched numerous initiatives over the years to boost SME financing, but their impact has been minimal.

Most SMEs in Pakistan transact in cash and resist adopting modern technology to evade government scrutiny. A common practice is the maintenance of dual books, one for official purposes and another for under-the-table transactions.

While this helps SMEs minimize their tax obligations, it also presents a misleading picture to banks, making it difficult for them to assess the true financial health of these businesses.

Commercial banks, aware of these dubious practices, often disregard the account receivables and cash flow projections of SMEs, treating them as mere formalities. Instead, they resort to collateral-based lending, providing financing in exchange for valuables. However, SMEs frequently fail to present noteworthy collaterals, leaving them underfinanced for working capital.

The transition to clean lending, where

no collateral is required and credit risk is evaluated based on cash flows, could potentially ameliorate the bleak situation of SME financing in Pakistan. While microfinance banks have had some success with clean lending, it is typically capped at low amounts, with larger loans still requiring collateral.

Some success stories in the microfinance sector offer hope. For instance, Mobilink Microfinance Bank (MMBL) has partnered with B2B marketplace startups to gain valuable data on retail merchants, enhancing its credit assessment models. Moreover, MMBL leverages various sources, such as Jazz GSM data, JazzCash account data, customer electronic credit information bureau details, and recharge on Jazz sims to further augment its credit assessment models.

Similarly, Telenor Microfinance Bank has launched initiatives like Easypaisa Karobar in collaboration with e-commerce infrastructure providers. Shahzad Khan, Head of Channels and Corporate Business at Telenor Microfinance Bank states, “Easypaisa Karobar is an innovative platform designed to help SMEs and MSMEs streamline their business operations and unlock new growth opportunities. By offering flexible stock financing and digital payment solutions, it addresses key cash flow challenges faced by businesses.”

And then there is potentially the most important one of all: the partnership of Haball – the B2B payments fintech – with Meezan Bank to help enable Digital Supply Chain Finance (DSCF).

By establishing a holistic digital ecosystem involving ERP systems and banking portals, banks can track transactions and goods exchanged throughout supply chain networks.

This would enable them to amass

historical data, making verification of identity, assigning credit scores, and estimating cash flows of SMEs more straightforward.

A representative from Meezan Bank Ltd. explains, “Digital Supply Chain Finance improves SMEs’ access to finance by streamlining the submission of onboarding and transaction requests through their ERP systems or other digital platforms. This seamless integration facilitates faster approval and disbursement of funds. Consequently, it lowers the costs associated with borrowing and simplifies the customer onboarding process, making financing more accessible and efficient for SMEs.”

DSCF could allow banks to intervene instantaneously in supply chain transactions, paying upfront to companies while allowing distributors to pay the bank at a later date, or paying vendors immediately while companies repay the bank later.

Initially, banks are likely to follow an anchor-driven strategy, using large established companies as anchors and extending credit to associated SMEs based on verifiable transaction data.

Think about what each of the above examples are trying to do: use some means other than self-declared financial statements by small business owners to determine the actual financial health of those businesses, most specifically the volume and timing of their cash flows.

Why supply chain financing is attractive

It is an intriguing idea, and certainly one that might help reduce the intermediation cost and reliability of creditworthiness assessments for small business

borrowers. If everyone connects their revenue and expenses to software tracking systems and those systems are accessible to banks, then the banks can make determinations about who to lend to and how much to lend to them almost automatically, with very little cost involved.

Add in the supply chain component, and it becomes even more attractive. To understand why, consider the following example.

We established earlier that the banks already have much more trust in larger Pakistani companies than smaller ones. What supply chain financing does is allow that trust to be leveraged for a much larger loan book than just the bigger company itself.

Consider, for example, a company like Atlas Honda, the motorcycle manufacturer. Atlas Honda is easily regarded as a low credit risk company by most banks. Now, imagine Atlas Honda wants to finance Rs10 billion worth of its cost of goods sold. It will borrow that money, and buy Rs10 billion worth of goods from its first level of suppliers. But that group of suppliers, in turn, has other suppliers that they rely on, and so on.

For simplicity’s sake, let us assume that there are four layers of suppliers, and that each layer operates on an identical 20% gross profit margin, meaning that their cost of goods sold is equal to 80% of their sales. Let us also assume that a bank – let’s say Bank Alfalah – lends not just to Atlas Honda, but all four layers of suppliers in that supply chain.

They lend Rs10 billion to Atlas Honda, Rs8 billion to the first layer of suppliers, Rs6.4 billion to the second layer, and Rs5.1 billion to the third layer. That is nearly Rs30

billion worth of loans. Atlas Honda’s loan paid off the first layer of suppliers’ loans, which then paid off the second layer, which then paid off the third layer. All Rs30 billion of loans got paid off a chain of the same sales made by Atlas Honda.

Even assuming a constant net interest margin (in reality, it would be different for each layer of suppliers) of approximately 8%, that means that the bank would earn Rs2.4 billion in revenue for a loan that functionally relied on Rs10 billion being paid back.

You can see why the banks and the SBP are excited about this prospect. This does not even require the suppliers to have formal accounts or even incorporation. All it needs to work is for them to agree to use a Bank Alfalah portal to track payments and a Bank Alfalah account to receive their payments so that the bank can deduct the loan amount from their revenues directly without having to rely on them to pay the bank back. One would have used technology to reduce the informational asymmetry without in any way changing the level of governance of the small business in question.

The problem, of course, is that this works great on paper but is much harder to implement in practice. Because in reality, each layer of suppliers gets divided up into progressively more and more companies, each of which has less and less formal documentation available to them at each stage, and not all of whom will even want to participate, even if the requirement for formal documentation is removed.

Why? Because small businesses in Paki -

stan are absolutely paranoid about becoming visible to the FBR.

The taxman problem

In other words, it is not enough to understand how to reduce the cost and reliability of information about the creditworthiness of small businesses. You have to go one level deeper and understand why the information is unreliable to begin with. And that reason is the FBR.

Nobody likes paying taxes, and Pakistanis are no more and no less inclined to pay them than any other country. What is true, however, is that taxation in Pakistan is unusually coercive in its nature, and it has to do with the incentive structure given to FBR officials.

The State Bank and the SECP have mandates for policy that go beyond governance. They are required to police bad behaviour, yes, but they are also required to promote growth in the industries that they regulate, which means that one can make the case for a policy by arguing that it will enable the industry to grow and that argument then at least gets taken seriously by both the SBP and the SECP. That does not work with the FBR.

The FBR is given only one goal: maximise revenue this year. Not even maximise revenue in general. Very specifically this year. If you are the chairman of the FBR, that is the only question the Finance Minister will ever put to you. He will accept any answer, even one that involves less revenue next year. Because next year is next year’s problem, and

the politicians who run the country are concerned about surviving on a day-to-day basis.

And so the way the FBR goes about their job is trying to find out if the taxpayers about whom they already have a lot of information can be made to pay more. This means that registering a business with the FBR and being honest about how much money you make means attracting their attention when they get desperate about meeting their revenue goal.

This not just about inconvenience. The FBR’s policies sometimes amount to outright theft: they will collect “advance” taxes that are supposedly adjustable and refundable if you pay extra, but the refunds are never paid, so once you lose the money, it is gone forever, even if you were not legally obligated to pay that much in taxes.

Even if one company wants to become compliant with tax law and document everything, they will operate in a market where all, or nearly all, of their competitors are not doing so, and so this will put them at a massive competitive disadvantage.

So no small business ever wants to document itself and would rather accept the slower growth that comes from not having access to capital than to have their earnings stolen from them by the FBR and then lose their competitive advantage to rivals who continue to evade taxes. It would, quite simply, be irrational for them to start documenting themselves.

So the State Bank and SECP and all the fintechs can continue to develop all sorts of nifty products and regulations they want. n

Fauji’s bid for Agha Steel: is it the right move?

Not the most attractive asset in the industry, but that may represent an opportunity for the conglomerate best known for its stewardship of industrial assets

By Zain Naeem

Fauji Foundation, the military-owned diversified industrial and financial conglomerate, is now eyeing a new frontier—the steel industry. Known for its presence in fertilizers, food, energy, banking, and more, Fauji is looking to acquire Agha Steel. But is this move a shrewd step into a growth market, or a plunge into troubled waters?

There are three key variables are key to answering that question. The first is Fauji’s own ability to manage ventures in its ever-expanding and diversifying empire. The second is whether Agha Steel is the best acquisition target in the space, or at least is it one through which Fauji can have a realistic expectation of making a reasonable return. And then the third is the economics of the steel industry itself, and whether or not it is a good industry for Fauji to expand into.

Fauji’s conglomerate

The Fauji Foundation was set up in 1954 as a welfare organization originally meant to support veterans of World War II from the area that is now Pakistan. Its initial capital came from the recently-departed British government. The foundation set up a textile mill, a sugar mill, and a cereal mill from those funds to create a flow of ever-growing dividends that would support the foundation’s grants to the veterans and the families of deceased soldiers.

Over the decades, the foundation expanded its activities, and most notably, in 1978,

entered the fertilizer manufacturing business. Fauji Fertilizer Company was set up as a joint venture with the Danish company Haldor Topsoe. he first urea complex was commissioned in 1982 in Sadiqabad, Punjab. To keep up with the urea demand in the country, a second plant was built at the same location in 1993.

Fertiliser are now the core business of the conglomerate. In 1993, a second fertilizer company – Fauji Fertilizer Bin Qasim – was incorporated and began production of phosphate-based fertilisers in the country.

Both Fauji Fertilizer Company and Fauji Fertilizer Bin Qasim are among the most consistent dividend-paying companies in the country, in part because they sell a product for which there is almost consistently growing demand every year and the country does not produce enough of it. Fauji Cement is somewhat less consistent in terms of paying dividends, but is nonetheless also a major piece of the conglomerate.

As was stated in a recent analysis of Fauji’s business, part of what makes Fauji unique is the insistence on hiring retired soldiers at the top levels of the company. This has certain consequences which lean into some stereotypes about military men: they do well when the product is industrial and requires disciplined adherence to a strict production process, and much less well when they try to sell consumer goods that require creativity in creating brands that appeal to a mass audience.

So, for instance, Fauji Foods struggled even after acquiring well-known Pakistani brands from Noon Pakistan, which owned the Nurpur brand of butter. It required civilian

management to come in and steer the ship, which appears to be struggling again now that it is back under military control.

By that logic, Agha Steel – an industrial entity – is absolutely consistent with the conglomerate’s strategy: it represents the kind of business that Fauji has a strong track record of managing. But there is at least one wrinkle in this decision: it seems to be going against what appears to be a move to simplify the complexity of the conglomerate.

Fauji has been on a simplification kick of late. It is in the final stages of merging Fauji Fertilizer Company and Fauji Fertilizer Bin Qasim into a single entity – a move many market observers believe was long overdue. In 2022, it merged Fauji Cement and Askari Cement to become one of the largest cement manufacturers in the country. And it has folded its investment banking and securities brokerage arm – Foundation Securities – under the umbrella of its bank: Askari Bank.

All of these moves were completely logical and certainly reflect a healthy instinct: cleaning up the governance structure of a complex conglomerate that had grown unwieldy over time. It is also reflective of a reality that is at the heart of every business question around diversification: there is only so much attention that senior management came give to any business line, which means it is entirely possible for a conglomerate to overdiversify.

But is it even right to think of the Fuaji Foundation as a conglomerate? Or it is really more similar to a strategic investor that just happens to prefer a strategy of majority ownership in all its portfolio interests, but otherwise

leaves day-to-day management of the companies to the managers it appoints?

If it is the latter, then an investment in Agha Steel is merely deployment of surplus capital to generate returns in a business that is similar in nature to ones that the portfolio manager already owns. And perhaps the acquisition decision is more logical.

Which then leads us into a discussion of whether or not Agha Steel itself is the right play in the steel sector.

The steel contender: Agha Steel

Founded in 2012, Agha Steel has carved a niche for itself in producing rebar and billets with an annual capacity of 450,000 and 250,000 tons, re-

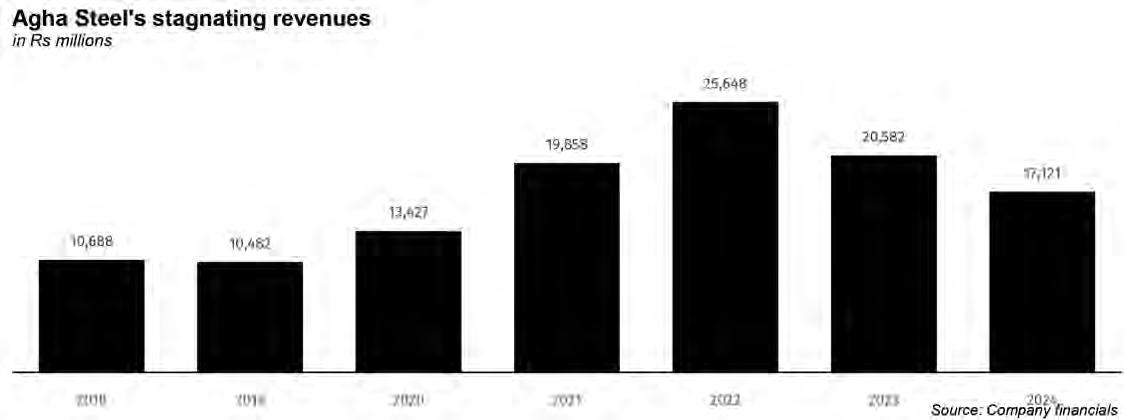

spectively. The company posted impressive revenue figures, clocking in at Rs20.6 billion for the year ending June 2023, along with a net profit of Rs905 million. On the surface, these figures suggest financial strength, but a deeper dive into industry comparisons raises some eyebrows.

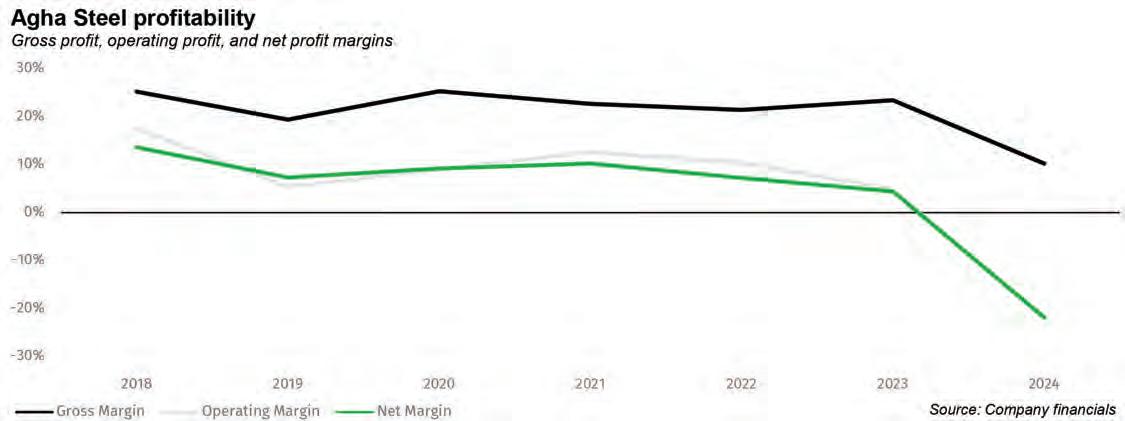

Over the past six years, Agha has managed gross profit margins ranging between 2025%, significantly outperforming the industry average of 7-15%. However, recent downturns paint a different picture. Gross margins slid to 10%, and net profits turned negative at -22% in 2024. In contrast, its competitors saw more stability, with industry gross margins of 14% and net profits holding at 4.6%.

So what went wrong? In a word: leverage.

Agha Steel has way more debt on its bal-

ance sheet than its competitors, and it shows up in terms of how much more it has to spend on interest expenses compared to its rivals.

Agha’s financial struggles seem tied to its ballooning interest expenses. Borrowing is routine in the steel sector, but Agha’s debt servicing has spiraled out of control, with interest expenses surging from 3.92% of sales in 2018 to a staggering 28% in 2024. The reason? Sky-high interest rates imposed by Pakistan’s central bank, peaking at 22%. While the whole industry has felt the pinch, Agha’s borrowing practices have exposed its vulnerability more than most.

Its competitors? They saw their interest costs rise, but nowhere near as dramatically, maxing out at around 6.6% of revenue. Agha’s inability to renegotiate better credit terms is clearly costing it dearly.

Agha’s liquidity is another issue. Its current ratio—a measure of how well it can cover short-term liabilities with short-term assets—has deteriorated from a healthy 1.28 in 2021 to just 1.02 recently. Even worse, its quick ratio, which strips out inventory, has hovered at dangerously low levels, recovering only slightly to 0.55 in 2024. By comparison, industry players have seen stable ratios, giving them more breathing room amid economic turbulence.

Agha’s heavy reliance on short-term borrowing to fund operations has left it highly leveraged. While its debt relative to its property and equipment has fallen from 108% to 74%, the industry average remains higher, with competitors reducing their own debt loads more slowly. Yet, despite borrowing less, Agha’s inefficiency in managing this debt is undermining its profitability.

So what exactly is the problem? Why does the company carry so much debt? Because it seems to carry over eight months of inventory on its balance sheet at all times, and finances that inventory through debt. That only happens when a company is producing far more than it can actually sell, or it is exceptionally bad at planning out how much it expects demand to be.

Agha Steel, perhaps in the hopes of growing its revenue faster than it actually has the capacity to, keeps on producing a lot of steel, but then does not actually sell it at the same pace as it produces, and somehow has not thought to just stop production for a while so as to run down its inventories.

If the company did that, it would be able to sell its inventory, and use the cash received from the sales to pay down its short term debts. That, in turn, would dramatically reduce its interest burden.

That might be seen as bad, but if you are a potential acquirer, having a company’s man-

agement making such elementary mistakes is good: it means there is a clear path to fixing the asset quickly and boosting profitability without having to do a lengthy and time-consuming examination of what would be the right strategy to make the company grow.

The market’s view

Investors do not seem too optimistic about Agha Steel. For every rupee of equity, the market is willing to pay just Rs0.59, compared to its competitors Aisha Steel (Rs0.42) and Amreli Steel (Rs0.56). On the other hand, better-performing companies like International Industries and Mughal Iron & Steel command a premium, with price-to-book ratios above 1.0.

Similarly, Agha’s price-to-earnings ratio sits at 9.42, while the broader industry averages 12.4. Investors are clearly more willing to bet on companies they see as having stronger earnings potential. In other words, the market is clearly less optimistic about its sales potential than Agha Steel’s own management, and judging by the mess on the company’s balance sheet, the market is probably right.

That lower price, again, represents an opportunity for the acquirer: if the market is pricing the asset low, but a change in management and a few simple changes in strategy can result in a higher profitability for the company, that lower price is a good thing from Fauji’s perspective.

Steel’s macro risks

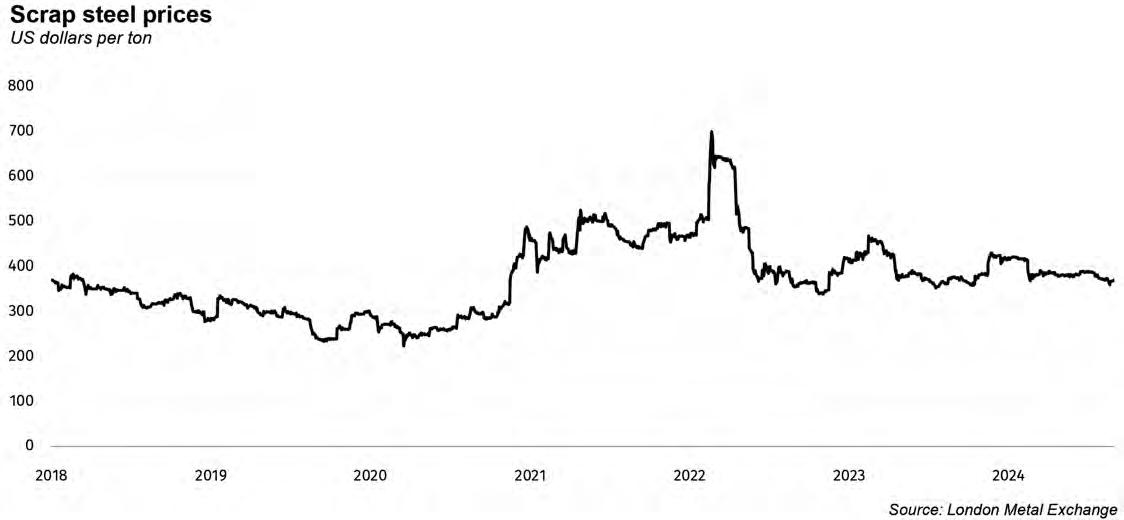

Zooming out, the steel industry faces its own set of macroeconomic challenges. Steelmaking in Pakistan relies heavily on imported raw materials, with iron ore and scrap metal comprising 60-70% of production costs. Between 2018 and 2024, scrap metal prices doubled, only to fall

back to earlier levels. Yet, the rupee’s sharp depreciation has eroded the cost advantage this drop should have provided. Steelmakers are now grappling with a dollar that trades at Rs 280—up from Rs 100 just a few years ago. The industry’s fortunes are tightly bound to exchange rates and raw material prices. Any fluctuation in either could make or break Agha Steel’s recovery.

Despite these headwinds, there’s a silver lining: Pakistan’s steel consumption per capita stands at a mere 36 kilograms, far below the global average of 200 kg. There’s room to grow. Recent government commitments to infrastructure projects, including a Rs 1.4 trillion Public Sector Development Program, could spur demand for local steel.

Additionally, with the central bank’s recent decision to slash interest rates from 22% to 17.5%, the cost of financing is expected to fall. For Agha, which has struggled under the weight of expensive short-term loans, this could be a much-needed break.

The verdict: is Fauji’s gamble worth it?

Agha Steel is undoubtedly a company with potential but one that’s currently bogged down by debt, inefficient capital use, and market skepticism. Fauji Foundation’s planned acquisition could breathe new life into the struggling steelmaker—but only if it tackles the internal financial woes plaguing the company. Meanwhile, the steel sector itself remains a mixed bag. Macroeconomic volatility and competition from cheaper imports, particularly from China, Russia, and Ukraine, will continue to cast shadows over the industry. Yet, with rising domestic demand and easing borrowing costs, Fauji’s gamble could just pay off—if it plays its cards right. n

Despite a thriving pharma industry, Pakistan does not manufacture any condoms

The market for contraceptives is massive in Pakistan. Despite this, nearly all of the options available to people are imported.

By Abdullah Niazi

If you were anywhere near the internet or a television set in 2013 Pakistan, you will remember a time when the entire country was in an uproar over an advertisement for condoms. In the course of 50 seconds, the ad for Josh condoms infuriated enough individuals that PEMRA was inundated with complaints.

The outrage was shared by the esteemed experts over at PEMRA, with the authority’s spokesman telling reporters that airing content like this during the holy month of Ramadan was something that “warrants serious action.” He added that, not only did the advertisement breach Pakistan’s broadcasting standards, its flagrant disregard for Islamic morals also rendered it “unconstitutional.”

Putting aside the ridiculous claim of constitutional conflict, especially considering

the Islamic Holy Book discusses sex during Ramzan very openly, the ruffled feathers point towards a worrying trend. Despite being the fifth largest country in the world by population, Pakistan’s market for contraceptives is in abysmal shape. This includes pills and IUDs, but most importantly condoms, which are the most common form of contraception in the world.

Just how underdeveloped?

The pharmaceutical sector in the country is a sizable industry with an annual turnover of more than Rs 336 billion ($3.2 billion) and a double-digit annual growth rate of 15%.

Currently, the industry has approximately 759 pharmaceutical manufacturing units including those operated by 25 multinational organisations. According to Pakistan Pharmaceutical Manufacturers’ Association, their industry meets around 70% of the country’s demand18 of medicines.

Despite this, only a few pharmaceutical

industries including ZAFA Pharmaceutical, Karachi and HENSEL Pharmaceutical, Lahore are producing 3-month injectable (Depot Medroxyprogesterone Acetate), combined oral pill (COC), and emergency contraceptive pill (ECP). And what makes this worse is out of

this no o industry is producing condoms, intrauterine devices (IUDs), and implants (single rod and two rod), which are being imported to meet the contraceptive requirements.

Condoms are actually a really interesting FMCG product in Pakistan. Since no local pharma companies manufacture this very cheap product in Pakistan, a lot of the market requires the intervention of NGOs and governments looking to encourage family planning. Currently there are two companies involved in the import and sale of condoms in Pakistan. The first is Greenstar Marketing, which has the brands Sathi, Touch, and DO under its umbrella. Sathi is a cheap condom with a single one costing around Rs 32, even though this is a price that has gone up from Rs 18 just two years ago. Touch, in comparison, is a more high-end brand that isn’t marketed in Urdu and was supposed to be for an urban clientele, although this fell flat because of continued consumer preference for Durex brand imported prophylactic.

This group controls around 70% of the entire market mostly through its Sathi brand. However, since around 2013-14, another competitor by the name of DKT Pakistan has also come in with its Josh brand that has found a clientele. DKT International is a charitable non-profit organisation that promotes family planning and HIV prevention through social marketing. The Washington, D.C.-based DKT was founded in 1989

It came to Pakistan in 2012, and has since become a significant player in the market. Because of the nature of the product, both of these companies are involved in a lot of lobbying and advocacy for family planning and are led by doctors. A big reason for this is that

most FMCG companies in the country as well as pharmaceuticals worry about their brand image if they begin to invest in, import, or manufacture the product directly in Pakistan.

The result of this, however, is that Pakistan has abysmal numbers when it comes to contraceptive usage. And now, the rising population is not the only problem that comes from this. The use of condoms in particular is very important in stopping the spread of sexually transmitted diseases (STDs).

Pakistan is experiencing the second fastest rate of HIV increase in the Asia-Pacific region. The Global Fund (GF) has designated Pakistan as a sub-recipient of its $72 million aid for HIV, with the funds now being channelled through the United Nations Development Programme (UNDP) and the private sector instead of the federal government.

According to The Lancet, HIV prevalence among the general population in Pakistan is estimated to be less than 0.1 per cent, with around 165,000 people living with HIV. Last year alone HIV/Aids killed over 12,000 people in the country.

the appropriate information about their use, these unwanted pregnancies would not have occurred in the first place.

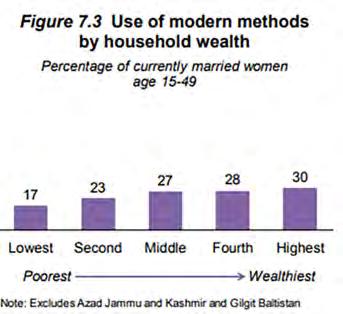

According to data that is a little more dated but from the most recent Health and Family Planning Survey conducted by the Pakistani government, modern contraceptive use by currently married women has stagnated over the last 5 years, with 26% of women using a modern method in 2012-13 and 25% in 2017-18. The most popular modern methods among women are female sterilisation and male condoms.

Because of this, a lot of the work being done towards promoting the use of contraceptives in the country is done through NGOs and foreign aid organisations. But there is also another interesting statistic in the midst of all of this. According to the same report, women choose almost equally the public (44%) and private (43%) sectors in their use of sources of modern contraception, which are mainly condoms.

Pakistan actually has some of the lowest contraceptive prevalence in the entire world. Contraceptive Prevalence Rate (CPR) is defined as the proportion of women of reproductive age who are using or whose partners are using a contraceptive method at a given point in time. Pakistan’s CPR is extremely low at 34.5%. To put this in perspective, Iran has a CPR of 77.4%, Turkey’s is 73.5% and even Bangladesh’s CPR has climbed to 62.4%. Pakistan’s CPR of 34.5% means that 65.5% of women of reproductive age or their husbands are not using any contraceptive method. And this is why Pakistan needs contraception. The Population Council estimates that there are around 9m pregnancies in Pakistan annually. Half of these are unintentional. And around 2.25 million end up in abortion — which is mostly unsafe. Had these couples had access to contraceptive methods and

It is clear that there is a willingness among the population to purchase condoms and there is definitely a market. According to the 2017-18 numbers, the private sector has always been in front as a source provider of this method. An enhanced role from 2012-2018 saw an increased usage of condoms from 35% to 49%. Overall, from the latest data available, 159 million units of contraceptives were sold in Pakistan last year. This included what the industry calls male contraceptives; i.e. condoms (approximately 147 million units or 93% of sales) and female contraceptives, i.e. oral pills, internal uterine devices and injectables (10 million units or seven percent).

Already the prevalence of contraceptives in Pakistan is dangerously low. Within this, condoms are the cheapest, most effective, safest, and most well known method and already enjoy a 90% share of the market. Their manufacturing would be easy in Pakistan, and demand would depend entirely on how manufacturers are allowed to advertise their product. As of now, it is only companies like Greenstar and DKT that have a stated healthcare mission importing and selling contraceptives in Pakistan. If any local company has the guts to take on this task, they will find they have a very good opportunity on their hands. n

Lahore Gymkhana pays Rs 417 every month in rent.

Does the Punjab Govt have what it takes to make them pay their fair share?

Over the past 111 years, Gymkhana has paid a meagre Rs 2.68 lakh in total to the Punjab government as rent. The Punjab Assembly has taken offence to this

By Abdullah Niazi

For the first time in more than a century, the management of the Lahore Gymkhana Club might actually have to pay rent for the 117 acres that the colonial era golf club is housed on.

It is not exactly a secret that Gymkhana basically pays nothing even though it operates on land owned by the Punjab government and given to them through a lease. The

understanding has always been that since Gymkhana is a grand old institution, the free use of public land is essentially a privilege that comes with the legacy.

But this opinion seems to have waned over time, especially since over the years the club has become increasingly more exclusive. New memberships are rarely given out and even old political families have had a hard time getting second-sons, grandsons and son-in-laws trouble getting in. Perhaps that is why in recent times the club has seen some of its influence falter. Nothing is more

evident of that than a new committee of the Punjab Assembly that has been constituted to rethink the relationship between the provincial government and the club. The only question is, will they be able to do anything about it?

Freebies

Here’s a number for you to put things into perspective. In the 111 years since 1913, the Punjab Government has billed Lahore Gymkhana Club

for a total amount of Rs 2 lakh, 60 thousand, and 800 rupees. And the club has not paid all of this either according to the government.

So what gives? The club was founded in 1878 in the Lawrence Gardens opposite the sprawling estate of the Governor House, the imperial symbol of power and authority of the Raj. The first organisational golf tournament played there was the Champion Medal (Roe Medal) which was held in January 1895. The building of the Institute comprised mainly the Lawrence and Montgomery Halls. These were used for social and intellectual recreation for the residents of Lahore. The Lawrence Hall, the building facing the Mall, was built in 1861-62 in memory of Sir John Laird Lawrence, the first Chief Commissioner (1853-57) and Viceroy of India (1863-69), while the Montgomery Hall facing the central avenue of the Bagh-e-Jinnah was built in 1866 to commemorate Robert Montgomery, second Lt Governor of the Punjab (1859-65).

The club was built soon after the annexation of Punjab. Ranjit Singh died in 1839, the Sikh empire fell apart within 10 years of this and the British were ruling Punjab by 1850. In these initial days, creating spaces like Gymkhana was an important part of the colonising process. But by the early 1900s, the colonial government managed by District Commissioners wanted a formal relationship with the government and the private Gymkhana Club.

In 1913, an agreement was signed between Lahore’s DC and the Club management, agreeing that the club land would be leased out to them by the government for the next 8 years at a cost of Rs 1600 per year. This agreement was renewed in 1921 for 40 years to 1960. This meant that at the time when Pakistan was created, the rich and wealthy of the city took control of the club and continued to pay the meagre rent. In 1960 when the lease was up, it was a pretty simple process to have it leased out for another 40 years until the year 2000.

For some reason, in the year 2000 the government decided that instead of maintaining the rent at the historic Rs 1600 per year, they would increase it to Rs 500 per year, meaning Gymkhana now had to pay them a monthly rent of Rs 417.

But there was a difference here. You see the last agreement had been running since 1960, but a big change had occurred in 1972. In this year, the government of Punjab took over the original building of the club and turned it into the Quaid e Azam Public Library. The elite club was moved to its present location at The Upper Mall, which was previously the Golf Club of Lahore Gymkhana and spread over an area of 117 acres of land leased from the Punjab government. The foundation stone of the present building was laid on 5 March 1968

by the then Chairman of Lahore Gymkhana Nawab Muzaffar Ali Qizilbash. The building was completed and occupied on 16 January 1972, the cost of which was borne by the members.

The club’s historic cricket ground, arguably the most beautiful in the country and the second-oldest in the subcontinent, is still housed inside Lawrence Gardens. So when the lease agreement was up for negotiation again in 2000, it was this new 117 acre spread on The Upper Mall that was being given out at Rs 417 a month.

The problem

This is where things stand. The club has stood for decades now at its current location on The Mall. The cost of developing it has been paid by its members, but the government owns the land it is on. The meagre amount they charge in rent is a bit shocking to read, but it is not unprecedented. The government often allows the use of its land at token rates for uses that are in the public good.

It is actually a pretty good idea. Say someone wants to open a sports ground for underprivileged kids or wants to build a charitable hospital or university. These are all endeavours that would fall within the good of the public. The government obviously wants the welfare of its citizens, if not for moral reasons then simply to keep the electorate happy. When you have someone willing to invest in such a project, one thing the government can easily do is give that individual or organisation the land for it. It is a rare win-win situation. Buying land would otherwise have been very expensive for the person wanting to pursue the project, and the government has it just laying around not being used. It is how grants of land have also been made for institutes like Shaukat Khanum Memorial Hospital and the Sindh Institute for Urology and Transplantation.

The only issue here is that Lahore Gymkhana does not make any sense as an institution that promotes public good. No matter what anyone tells you about history, heritage, or anything else the club is simply a relic of the past where people with too much time, money, and privilege on their hands go for afternoon tea so they can feel good looking at their high walls and tell themselves they are members of an exclusive club.

It is the cost of this exclusivity that the people of Punjab pay. And the club in Lahore is not the only such facility. There is Chenab Club in Faisalabad, Punjab Club, and institutions like the Sindh Club in Karachi. The issue is simple. Is there any reason for the government to be subsidising the rent for an institution that represents nothing but the worst of elitism in the country?

What might happen

Well, some members of the Punjab Assembly felt that this was not appropriate in any way and moved for a debate in the assembly on this issue. The members claimed that according to market analysis they had commissioned, the rent of the entire 117 acre area of the Gymkhana could commercially fetch an annual rent of Rs 360 crores, or around Rs 30 crores a month. Of course, this estimate is a liberal one and takes into account the possible commercialisation of the entire area. Ideally, the land should be used in public interest rather than having it handed over to real estate developers. But this does put a cost on the matter. It means if the club does want to use the land in such a guarded and private way, they should be willing to pay at least a fraction of this.

This debate took place in May this year. After the Speaker asked for some facts to be verified, the latest development has come in the form of a special committee. In a detailed explanation, Speaker Malik Muhammad Ahmad Khan has listed the matters on which they wil deliberate.

The committee will determine the legality, appropriateness, and public interest of the current lease agreement between Lahore Gymkhana Club and the Punjab Government. It also has the power to review the 1960 and 1996 lease agreements. It will also take up the issue of public use of this land, and investigate the government’s right, under the Lease Agreements, to resume the land for public purposes, such as converting it into a park, urban forest, or other equitable land uses. What is perhaps most concerning for the club is that as part of this review, the committee will also determine any financial losses due to undervalued rent and recommend recovery measures from responsible parties. The most important sticking point here will be the committee’s findings on the club’s right to have exclusive use of this public land.

Of course, there is a long road to go here and the club will continue on being stuck in time as it is now. If the committee finds the teeth to give a scathing report, it will be a while before a law is passed and the government can take action. Even when that happens, you best believe that the club has more than enough resources to drag this matter to every single court they can find. The point, however, is that this is the first time the Lahore Gymkhana Club is not getting the red carpet treatment from the provincial government. If only a few things go right, they could be facing some trouble. But until we know more, it is hard to imagine this eyesore of a relic going anywhere. n

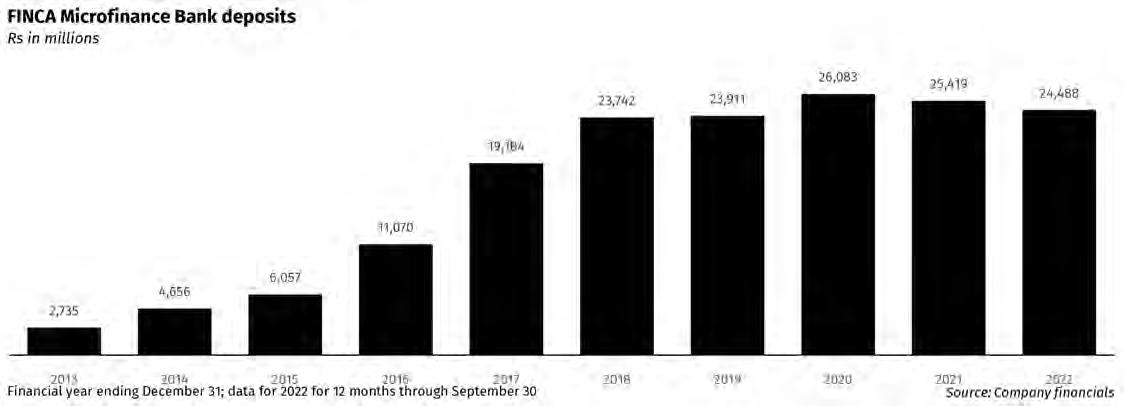

Abhi partners with TPL to buy out FINCA Microfinance Bank

The lending fintech appears to be ready to begin taking on deposits, often seen as a necessary step towards scaling lending operations

ABy Profit

bhi, the lending fintech platform best known for its earned wage access (EWA) product, announced that it has teamed up with TPL Corporation to acquire FINCA Microfinance Bank, in an announcement both companies made on Friday.

While the transaction is still subject to regulatory approvals, it represents a major advance in Abhi’s path towards becoming a fintech powerhouse in Pakistan. The company’s core business lines include various lending products, and while EWA is the one it is most well-known for, it derives the majority of its revenue from small business lending operation.

Abhi has been cash flow positive for over a year now, but being in the lending business, it is likely on the hunt for cheap sources of funding, as is just about any fintech company that is a lender. And there is no better source of cheap funding for a lender than deposits, which is why buying a bank – even a small microfinance bank like FINCA – can make sense.

There are four key reasons why lending fintechs have a tendency to pursue acquisi-

tions of deposit-taking institutions.

First and foremost, cheap deposits provide a low-cost source of funding for loans. Traditional banks have long relied on consumer deposits as a stable and inexpensive way to fund their lending activities. The interest rates paid on savings accounts and checking accounts are typically much lower than what banks can charge for loans, allowing them to profit from the spread. Fintech lenders that can tap into cheap deposits gain a similar advantage, improving their profit margins and ability to offer competitive loan rates.

Secondly, deposits provide greater stability and reduce reliance on more volatile funding sources. Many fintech lenders have historically relied heavily on institutional investors, venture capital, or securitization markets to fund their loan originations. These sources can dry up quickly during economic downturns or periods of market volatility. A base of stable deposits allows fintech lenders to continue operations and lending even when other funding channels tighten.

Additionally, cheap deposits allow fintech lenders to scale their operations more efficiently. As they grow their loan portfolios, they need an expanding pool of capital to fund new loans. Deposits that grow organically

with the business provide a more sustainable funding model than constantly having to raise new rounds of capital.

Access to deposits also gives fintech lenders more control over their costs of funds. Rather than being at the mercy of capital markets or investor sentiment, they can adjust deposit rates as needed to attract the right level of funding. This flexibility is valuable for managing growth and profitability.

Finally, having a deposit base can enhance credibility and open up new strategic options for fintech lenders. It moves them closer to the banking model and may make it easier to eventually obtain a bank license. Deposits also provide opportunities to crosssell other financial products and services to customers.

Abhi itself has tried pursuing non-deposit sources of funding, most notably its Rs2 billion sukuk which it issued in May 2023. As the pseudonymous blogger DMKM pointed out on Substack, that deal was quite onerous in how little it actually allowed Abhi to borrow and the outrageously high pricing it charged, especially given the fact that Abhi’s lenders were essentially taking very little credit risk since they were forcing Abhi to place near-cash instruments as collateral.

It is highly likely that Abhi saw the limits of what it was being allowed to do by the traditional banking system as a borrower and decided that the only way around those limitations was to acquire a deposit-taking license.

Among the deposit taking licenses, the most attractive option, of course, is that of a full commercial banking license, though that requires Rs23 billion in paid up capital to acquire. While Abhi is doing well, that amount is likely too high for the firm to invest into a license at this stage in its evolution, though it is likely its final goal.

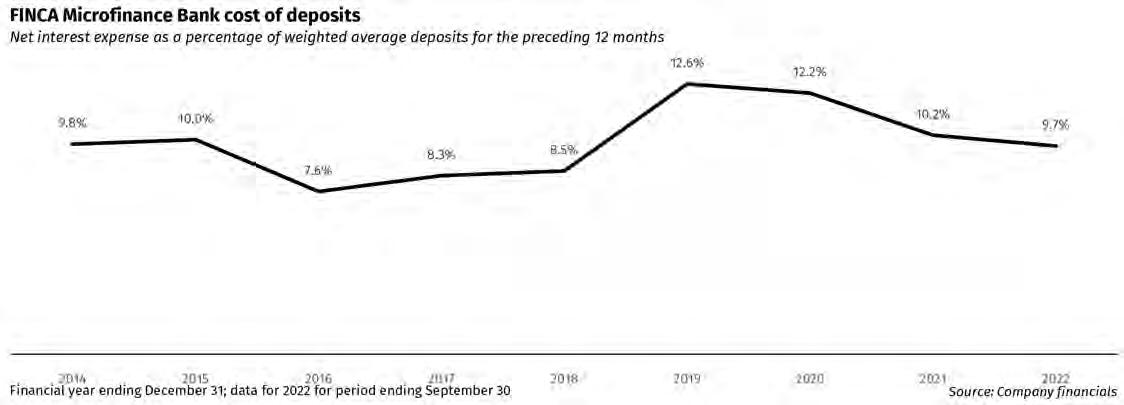

The next easiest option is that of a microfinance banking license, which is a much more manageable number, particularly given the number of microfinance banks in the country that are distressed enough to be on sale. FINCA Microfinance Bank, for example, has not been growing since 2021 and has not issued financial statements since September 2022.

The attraction to Abhi, of course, is likely to be the fact that FINCA has a deposit base of about Rs24 billion on which it pays out interest rates in the 10-12% range at a time

when the benchmark lending rate is 17.5% and Abhi’s clients are likely borrowing at significantly higher rates.

At last disclosure, FINCA’s book value was Rs3 billion, and it is highly likely that the final purchase price will be lower than that number. Abhi appears to have decided to partner with TPL Corporation, which also runs a venture investing arm in addition to its insurance and real estate interests.

Abhi was founded in 2021, and was one of Pakistan’s first companies to have been part of Y Combinator, the prestigious Silicon Valley-based startup incubator. Co-founder and CEO Omair Ansari is a former Morgan Stanley portfolio manager who previously ran two funds focused on consumer goods and fintech.

Ali Ladubhai, also co-founder, is an ex-banker who has held managerial roles in retail banking/ wealth management with HSBC and Samba Bank in Pakistan. Ali co-founded Karlocompare.com.pk, a financial services aggregator helping some of the largest financial institutions (banks and insurance companies) in Pakistan distribute their consumer finance

products digitally. He subsequently moved to Foreepay (Pvt) Ltd, an accounts aggregator & payments company where he was leading the Business Development department.

The company became known for its EWA product. Earned wage access is an emerging financial service that allows employees to access a portion of their earned wages before their scheduled payday. This approach to payroll aims to provide workers with greater financial flexibility and reduce reliance on high-interest payday loans or credit card debt.

Here’s how EWA typically works: Employees use a mobile app or online platform to request access to wages they have already earned but have not yet been paid. The EWA provider calculates the available amount based on hours worked and pay rate, usually capping access at a percentage of net earnings to account for taxes and deductions. Upon approval, funds are quickly transferred to the employee’s bank account or loaded onto a prepaid debit card. On the next regular payday, the accessed amount is deducted from the employee’s paycheck. n

Are Islamic Banks taking their customers for a ride?

Senate Committee grills SBP on Islamic banking practices amid soaring profits and record interest rates

By Mariam Umar

Pakistani banks have been living large over the past few years. As the State Bank of Pakistan (SBP) cranked up policy rates consistently, banks started riding a wave of record profits.vThe banking sector—both conventional and Islamic—has raked in some serious cash.

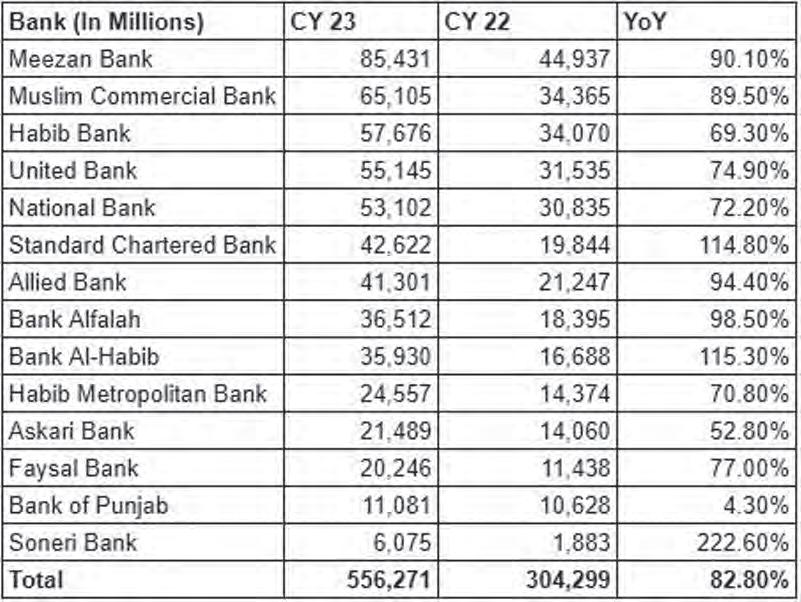

But a closer look shows that Islamic Banks made profits that were a bit larger than what you would expect them to have made in this time. Meezan Bank, for example, made the highest profit after tax in 2023. The bank was able to earn net profits of more than Rs 85 billion while the next best result saw MCB earn Rs. 65 billion. Next in line are the three biggest banks of the country with Habib Bank, UBL and National Bank of Pakistan earning around Rs 57 billion, Rs 55 billion and Rs 53 billion respectively.

This is even more intriguing considering banks like National Bank, Habib Bank and UBL have asset bases which are over Rs. 5 trillion, Rs. 4.6 trillion and Rs. 3 trillion, respectively. On the other hand, Meezan Bank has a smaller asset base of Rs. 2.5 trillion, yet it was able to yield almost double the profits compared to these behemoths.

Perhaps that is why the eye-catching profitability of the Islamic Banking Sector raised some eyebrows at a recent meeting of a Senate Standing Committee, which expressed its doubts about how Islamic Banks managed this. But before we get into that, it is worth revisiting how the banks have done so well in the pat few years.

Sky-High Rates, Soaring Profits

Here’s how it all unfolded. Starting in September 2021, the SBP began aggressively hiking the policy rate. By June 2023, that rate shot up by a staggering 15%, peaking at 22%. The result? Banks posted record profits, with some nearly doubling their earnings. For example, Meezan Bank, the biggest player in Islamic finance in Pakistan, saw its profits after tax soar by 91% in 2023, hitting over Rs 85 billion. Meanwhile, Faysal Bank, another fully Islamic institution, wasn’t far behind, posting a 77% increase in profits.

The root of this windfall? High interest rates. But here’s the twist: instead of lending to businesses and consumers, banks are funneling their capital into government securities—a saf-

er, less risky bet. This has left the private sector scrambling for credit, as borrowing costs have become prohibitively expensive.

It’s no surprise then that the government has started to take notice. On August 28, 2024, the Senate Standing Committee on Finance and Revenue took the SBP to task, calling for a detailed briefing on Islamic banking practices. The committee’s chairman, Saleem Mandviwalla, was quick to point fingers, accusing Islamic banks of exploiting consumers with sky-high rates.

SBP’s Deputy Governor, Dr. Inayat Hussain, pushed back. He contended that Islamic banking in Pakistan adheres to stricter standards than those seen globally, and that the accusations were misplaced. But is the government really just looking for a scapegoat, or is there more beneath the surface?

The Islamic Banking Boom

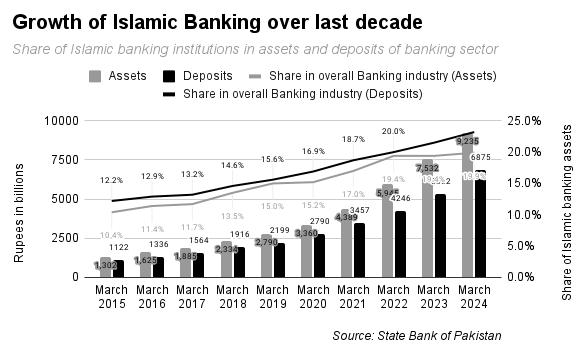

Pakistan’s Islamic banking sector is no small player. It began in 2001 with the goal of offering a Shariah-compliant alternative to conventional banking, and Meezan Bank received the country’s first Islamic banking license in 2002. Fast-forward to today, and Islamic banking has taken off. By the first quarter of 2024, 22 banks were involved in the sector, six of them fully Islamic. Together, they now command a 25% share of the market.

Meezan Bank has been leading the charge. Despite having a smaller asset base than conventional giants like National Bank, Habib Bank, and UBL, Meezan managed to deliver significantly higher profits in 2023. With

Rs 85 billion in profit after tax, it outshined competitors with asset bases more than twice its size.

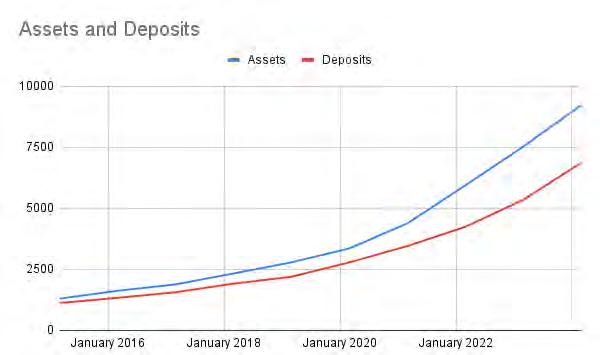

Between March 2015 and March 2024, the assets of Islamic banking institutions have, on average, grown by around 24% annually. Deposits with Islamic banking institutions have grown by around 22% during the same period.

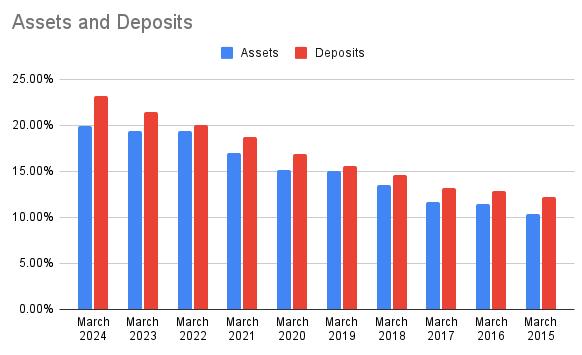

Share of Islamic banking institutions in the overall banking sector has almost doubled. In 2015, the share of Islamic banking assets and deposits in the overall banking sector accounted for only 10% and 12%. This has changed a decade later with the share of assets and deposits doubling to almost 20% and 23% respectively.

Moreover, as mentioned earlier, amongst the banking sector, Meezan Bank made the highest profit after tax in 2023. The bank was able to earn net profits of more than Rs 85 billion while the next best result saw MCB earn Rs. 65 billion. Next in line are the three biggest banks of the country with Habib Bank, UBL and National Bank of Pakistan earning around Rs 57 billion, Rs 55 billion and Rs 53 billion respectively.

This is even more intriguing considering banks like National Bank, Habib Bank and UBL have asset bases which are over Rs. 5 trillion, Rs. 4.6 trillion and Rs. 3 trillion, respectively. On the other hand, Meezan Bank has a smaller asset base of Rs. 2.5 trillion, yet it was able to yield almost double the profits compared to these behemoths.

Perhaps it is this very contrasting profitability that caught the eye of the chairman senate and led to his inquiry into practices of Islamic banking.

Profit has already covered what has led to improved profitability for Meezan Bank and, in general, leads to enhanced profitability for Islamic banks.

So, What’s the Catch?

What’s driving this profitability? A big part of the story is the absence of a minimum deposit rate (MDR) for Islamic banks. Conventional banks, by contrast, are required to pay a minimum rate to depositors—usually 1.5% below the prevailing policy rate. So, with a policy rate of 17.5%, conventional banks are paying 16% interest on savings accounts. Islamic banks, however, aren’t bound by this rule. Instead, they follow a profit-and-loss sharing model, which results

in much lower costs for the banks and fatter margins.

This lack of an MDR has created a larger spread for Islamic banks. While conventional banks saw their net spread (the difference between what they earn and what they pay out) shrink to 30% in 2023, Islamic banks held steady at around 50%.

The Real Difference Between Conventional and Islamic Banking

Islamic finance, by its very nature, works differently. It prohibits the charging of interest (riba) under Shariah law, so Islamic banks don’t engage in interest-based

lending. Instead, they focus on risk-sharing. Depositors, in theory, are more like shareholders—if the bank profits, they profit; if the bank loses, they share in that loss.

On the lending side, Islamic banks often use asset-backed financing. A common structure is ijarah (leasing), where the bank buys a property and leases it to the customer, who makes payments that include a built-in profit margin for the bank.

In Islamic banking, savings and credit function differently from conventional banking. Islamic deposit accounts do not earn interest; instead, depositors receive dividends based on the bank’s overall profitability. If the bank profits, depositors share in the returns, but if the bank incurs losses, depositors may also bear a portion of those losses. This risk-sharing model aligns with the principles of Islamic finance.

In contrast, conventional banks are obligated to pay a minimum deposit rate (MDR) on savings accounts. This interest-based model ensures depositors receive a guaranteed return, irrespective of the bank’s performance, marking a clear distinction from the profitand-loss sharing system in Islamic banking.

On the credit side, Islamic banks often use leasing (ijarah) as a financing tool. For example, the bank might buy a property and lease it to the customer over a fixed period, with payments structured to cover the bank’s costs plus profit. However, these payments are not labeled as interest, maintaining adherence to Shariah principles.

Exorbitant Rates or Fair Play?

So, are Islamic banks charging unreasonably high rates? It’s not a simple yes or no. A look at recent auctions of Shariah-compliant government securities tells a more nuanced story. Take the one-year Ijarah Sukuk, a bond-like instrument issued by the government. In July 2024, it was priced at 17.22%, which was actually 1.02% lower than the comparable one-year Treasury bill, which clocked in at 18.24%. The trend continued in subsequent auctions, with Sukuk consistently priced more competitively than conventional government debt.

For consumer products, too, Islamic banks are holding their own. The average profit rate on Islamic car financing hovers around 21.25%, which is roughly in line with conventional banks’ KIBOR + 4.5% rate. In housing finance, Islamic banks offer diminishing Musharaka (a shared ownership model), with an average profit rate of 20.56%, again aligning closely with market rates.

In some areas, Islamic banks are even leading the charge on competitive pricing. Since 2022, they’ve introduced fixed profit

rates that undercut the current KIBOR regime by almost 3%.

On the consumer front, Islamic banks are increasingly gaining market share. An average Islamic car financing product offers an average profit rate of 21.25%, which aligns closely with the industry standard. Given that conventional banks have an average profit rate of around KIBOR + 4.5%, equivalent to approximately 21.5% with today’s KIBOR rates, Islamic banks are competitively priced. Additionally, Islamic banks have historically set benchmarks, with their lowest profit rate last year being 0.5% below the KIBOR rate, prompting other banks to adjust their rates accordingly.

In the Housing Finance sector, Islamic banks’ Diminishing Musharaka product maintains an average profit rate of 20.56%, consistent with industry rates. Furthermore, since 2022, Islamic banks have offered a unique fixed profit rate with an average of 15.75% across all segments, which is below the current KIBOR regime by nearly 3%. This competitive pricing has influenced other banks to adopt similar strategies.

It is important to note that Islamic banks are subject to rigorous oversight by their Shariah Compliance Departments, ensuring adherence to Islamic principles while maintaining international standards in other financial functions. This commitment to ethical practices and transparent pricing distinguishes Islamic banking and benefits customers by contributing to a more equitable financial landscape.

a sector predominantly managed by conventional banks. Islamic banks offer limited unsecured financing products, which reflects a broader market trend rather than a specific issue with Islamic banking practices.

In contrast, higher rates are often observed in the domain of unsecured financing,

The competitive pricing of Sukuk, the successful participation in government and private sector funding, and the growing consumer confidence all contribute to a more nuanced understanding of Islamic banking

practices. The rise of Islamic finance is driven not merely by religious adherence but also by its practical, asset-based investment model, which offers a competitive and increasingly mainstream alternative to conventional banking.

The Verdict: Ethical or Exploitative?

Islamic banks operate under strict oversight, with Shariah Compliance Departments ensuring that all practices adhere to Islamic principles. This focus on ethics is a big draw for many customers. However, with Islamic banks now competing head-tohead with their conventional counterparts in profitability, questions about fairness and transparency are surfacing.

Is Islamic banking truly a more ethical and consumer-friendly alternative, or are the banks simply cashing in on their unique market position? While their risk-sharing model and asset-backed approach offer some benefits, the absence of minimum deposit rates and government scrutiny are making people think twice. As the government continues its probe, the future of Islamic banking in Pakistan will depend on finding the right balance between profit and principles. n