08 How the PIA privatisation became a train wreck inside a dumpster fire

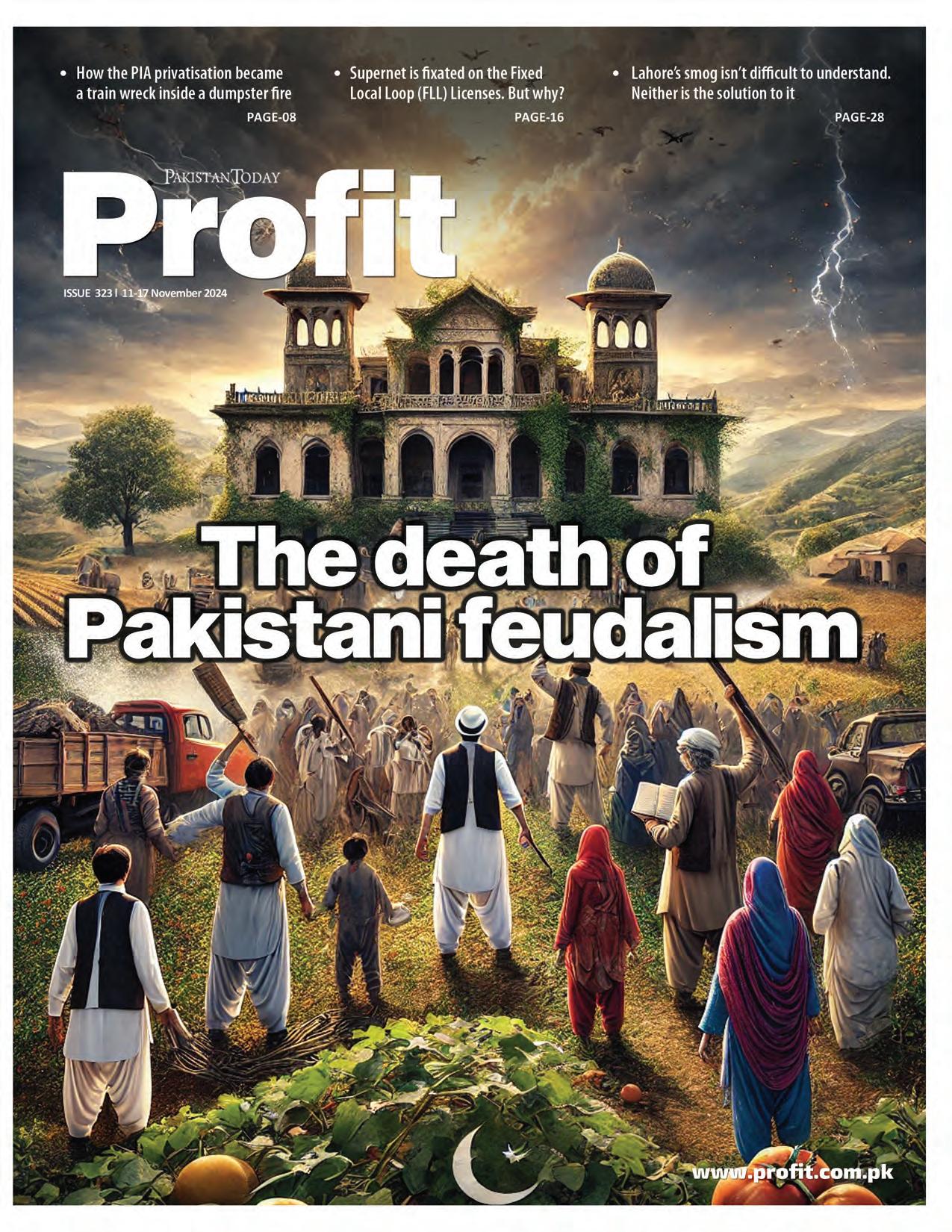

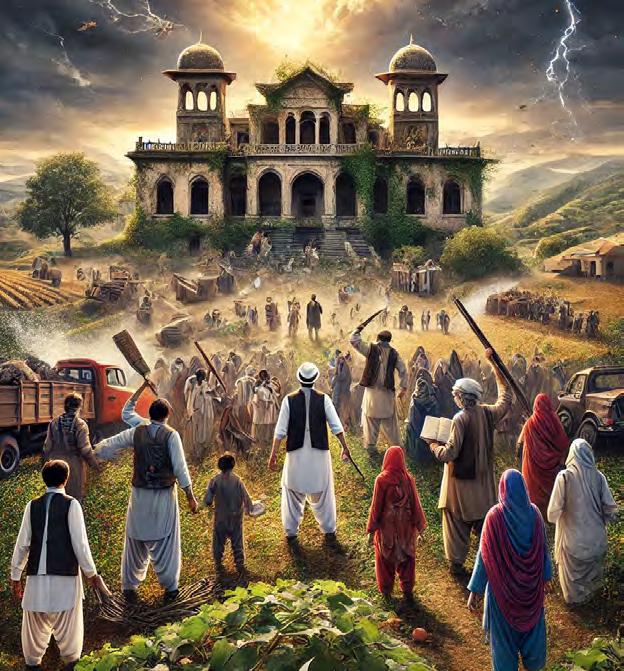

10 The death of Pakistani feudalism

16 Supernet is fixated on the Fixed Local Loop (FLL) Licenses. But why?

24 Since the 2022 floods, farmers have been enjoying higher yields. This Kharif season might buck the trend

26 A year after going public very quietly, Big Bird Foods has made a profit. Here’s what happened

28 Lahore’s smog isn’t difficult to understand. Neither is the solution to it

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

How the PIA privatisation became a train wreck inside a dumpster fire

PIA will go up for bidding once again depending on what cabinet makes of it. In the meantime, everybody is trying to make bank

Profit Report

It started off strange enough. Nearly two weeks ago, a consortium led by Blue World City, the controversial housing society on the outskirts of Rawalpindi, has become the first and only entity to qualify for bidding in the sale of Pakistan International Airlines (PIA).

Of the six consortiums that were in the running, this was the unlikeliest to emerge as the only contender. Of these six different consortiums pre-approved to bid for PIA, four different airlines were involved including FlyJinnah, AirSial, AirBlue, and Serene Air. However, all five of the consortiums other than the one led by Blue World City have stayed away from the process.

The Blue World consortium was the least experienced when it comes to the aviation business, although it does include Blue World Aviation, owned by the same family, as well as IRIS Communications Limited.

Immediately it became clear something was off. Profit reached out to representatives from FlyJinnah, AirSial, and Arif Habib for an answer. All of the individuals contacted declined to answer on the record. One significant bidder did say they weren’t speaking now because even though Blue World had seemingly become the only contender, the competition

was far from over. This became clear in only a few days. The Blue World consortium made a Rs 10 billion bid for a 65% share in PIA, only for the government to demand Rs 85 billion in comparison. Since then, the matter has gone back to cabinet which will deliberate on whether to accept the over or go back to the drawing board. So what happens now?

Controversial standing

The emergence of Blue World should have been the first sign. Blue World City rose to fame as a mega project in Chakri on the outskirts of Islamabad. Owned by Chaudhry Saad Nazir, it was launched as one of many real estate contenders in the Chakri area in 2018. Having presumably collected a decent amount from initial sales of files, they went on a massive marketing campaign that used classic real estate techniques. They even roped in Engin Altan, the Turkish actor that plays the lead role in the Ertugrul Resurrection drama series that has become a phenomenon in Pakistan, to be their brand ambassador.

However, the Blue World City has maintained a controversial reputation. It has never been approved by the Rawalpindi Development Authority (RDA) and continues to be labelled illegal by the development authority. The land authority says it is not planning to give its ap-

proval any time soon. In fact, on recommendation of the RDA, Blue City is being investigated by the National Accountability Bureau (NAB), and has not bought a fraction of the land they claim to already be in possession of.

The land in Chakri is a quagmire of legal cases, feuds, and disputed ownership that now has multiple parties involved. Many different housing projects operate in this area, and very few are actually ratified by the RDA. All of these different players have turned Chakri into a hotbed of armed violence, gang wars, and land grabbing.

The fighting came to a head in the summer of 2021, when an armed conflict between Blue World City and a rival housing society, Abdullah City, broke out. The police sent the owners of the both illegal housing societies to Adiala Jail on a court order. Chaudhry Naeem of Blue World City and Tahir Aziz of Abdullah City were summoned by the police for inquiry into the land dispute. During the inquiry, both parties started threatening each other with dire consequences in the presence of Rawalpindi police officers and district administration officers and there were quarrels between them.

Later on, in the midst of these challenges, Blue World also launched a television channel by the name of Suno TV. The channel has been used by them in the past to report news related to Blue World City. Acquiring a media outlet has been a regular tactic by different real estate

developers in Pakistan to buy some sort of influence in the media.

The other bidders

Of course, it now seems Blue World may not get PIA as some were expecting. According to sources, the other bidders backed out over a number of key issues. The main one was the government’s insistence that they have directors on the board with decision making input and power. Essentially, the government wanted a new owner to put in the money and inject equity but also let them have a hand in running the show. On top of that, buyers were also seriously concerned about the airline’s ability to return their planes. Historically, the PIA has never been able to return planes to the companies they lease them from. Airlines normally operate by leasing planes but they need to return them in the same condition they get them in. This means refurbishing them at the end of the lease. However, PIA fails to do this, resulting in rising debts.

Remember, Blue World City was one among six initial consortiums that were interested in acquiring PIA. At least four different Pakistani airlines including Fly Jinnah, AirSial, Serene Air, and Air Blue were all part of these consortiums. For these airlines, it was natural to be interested in PIA because it is a matter of survival.

PIA currently has the largest fleet and the largest domestic and international network in Pakistan. The national flag carrier is the market leader in Pakistan’s airline industry, and control of it means having a significant advantage over other airlines. If a consortium with an airline involved in it acquired PIA, it would automatically become the market leader. However, if a consortium without an airline like the Blue World consortium acquires PIA, it will mean a new entity is born and PIA’s position stays the same. In either case, the changes will shake up Pakistani aviation.

Possibly the consortium best poised to acquire PIA was Fly Jinnah and Air Arabia. Fly Jinnah took its maiden flight in Pakistan in October 2022, and has quickly positioned itself as a high-quality low-budget airline.

Fly Jinnah was the brainchild of the Lakson Group, one of the largest and oldest conglomerates in Pakistan. Founded in 1954 by the Lakhani family, the group first made its money in the tobacco business before selling it to Phillip Morris, which runs the business to date. The company is also the owner of McDonalds in Pakistan and also has interests in FMCG in the shape of Colgate-Palmolive, as well as in tech in the form of companies such as Stormfiber. They are also in the media business, running and operating the Express Group which has a news channel, an entertainment channel, as well as

an Urdu and an English daily to boot.

The other partner in this partnership is Air Arabia, the UAE based low-cost airline. During the pandemic, Air Arabia was lobbying heavily with the UAE government to be allowed additional international flights to Pakistan but failed to do so. So what did they do instead? They decided to enter an alliance with the Lakson Group to form Fly Jinnah. And the response from within Pakistan’s aviation industry was not particularly welcoming. In fact, it was PIA that was most up in arms and worried about FlyJinnah giving them competition.

So much so that the then Chief Executive of PIA, Air Marshal (R) Arshad Malik, penned a missive to the government, imploring them to prohibit Fly Jinnah from taking flight. The letter contended that green-lighting Fly Jinnah would enable Air Arabia to monopolise the local market and circumvent the country’s aviation policy, under which Air Arabia was barred from further rights to operate in Pakistan. Moreover, the letter revealed that Serene Air and Airsial had approached PIA to address the issue as well. The matter was also a topic of heated debate in the Senate’s Standing Committee on Aviation.

The fear amongst these airlines is that Fly Jinnah would serve as a conduit for Air Arabia, who would then whisk them off to other destinations. And the fear might be able to materialise. In 2023, after completing one year of domestic flights, Fly Jinnah can now operate internationally as well and launched their first flight to Sharjah in February this year.

Now, it seems Air Arabia is in the mood for complete dominance. You see, the consortium bidding for PIA is between Fly Jinnah and Air Arabia. This gives Air Arabia a lot of control since they already have a 45% stake in Fly Jinnah and completely own their UAE airline. Ownership of PIA would give them access to a lot more international flights and routes that they can coordinate with Air Arabia and Fly Jinnah.

There were others of course. Another consortium included AirSial and Serene Air, although this particular group was led by Pak-Ethanol. There was also a bid by Younus Brother Holding, which has amongst its subsidiaries Lucky Cement.

The Privatisation Commission also pre-qualified Airblue Limited; a Pakistani low-cost airline, Arif Habib Corporation Limited; a leading financial services firm, and Blue World City.

The challenge that faces the buyer

The challenge facing the eventual owner of PIA is massive. PIA’s losses are so staggering that it is hard to wrap one’s mind around them. PIA’s cash flows are in a state of chaos.

A retrospective glance at PIA’s cash flows from 2017 to June 2023 paints a grim picture. PIA only managed to keep its head above water for a fleeting one and a half years. The remaining five years saw PIA grappling with negative cash flows from its operating activities. In layman’s terms, PIA was bleeding money from its core airline operations. So, how has it managed to stay afloat? The lifeline has been debt.

During the aforementioned period, it was only in the first six months of 2023 that PIA managed to repay more loans than it borrowed. That’s not to say it didn’t borrow. It did. This borrowing spree has been the lifeblood of its operations for the past six and a half years. Is this a sustainable model? Far from it. PIA’s finance costs for 2022 alone amounted to a staggering Rs 50 billion — a record high over the past six years. Yet, barely halfway into 2023, PIA has already incurred an alarming 74% of this cost. It is this escalating cost of finance that prompted PIA to engage the government in a dialogue for financial aid to alleviate its debt burden. PIA is a negative equity company. Negative shareholder equity is a chilling scenario where a company’s liabilities to its investors eclipse the worth of its assets. In layman’s terms, when a company’s mountain of debt towers over the aggregate value of its assets, even after a complete liquidation, it is branded with the ominous label of negative equity. The fiscal abyss that PIA finds itself in has only yawned wider with time. The negative equity has mushroomed from Rs 291 billion in 2017 to an astronomical Rs 649 billion in June 2023. This gargantuan sum also symbolises the debt albatross that any prospective buyer would be saddled with upon acquiring PIA.

So why does anyone want to buy it in the first place? Perhaps the biggest factor in this which will be a boon for potential buyers of the airline is the decision to restructure PIA’s debt. In March this year, The Pakistan International Airline Holding Company approved the restructuring of the airline’s Rs 268 billion commercial debt, incorporating it into the public debt. The term sheet was finalised by the Ministry of Finance with commercial banks. The government’s decision to merge the airline’s debt into public debt means that taxpayers will bear the cost of PIA’s historic inefficiency and mismanagement.

And as Profit has pointed out before, even though the government of Pakistan is generally terrible at negotiating complex transactions, but in the PIA debt restructuring, may have gotten itself an as-good-as-possible agreement that spreads the pain among the banks and the government relatively evenly. n

The death of Pakistani feudalism

What was once the dominant force in Pakistan’s political economy is on its last legs. What comes next is not yet known.

By Farooq Tirmizi

Sometime during the Musharraf Administration a very important economic milestone was crossed in Pakistan. Agricultural land ceased to be the largest asset class in Pakistan, a title that it had likely held for millennia before then. With that change died the economic basis of what had hitherto been one of the defining features of Pakistan’s political economy: feudalism.

It rarely gets mentioned now, but there was a time not very long ago when a discussion of Pakistani politics was almost impossible without mention of the word “feudalism”. It was to pre-2008 opinion journalism what “civ-mil” is today: the topic everyone discusses ad nauseum and talks about as the permanent feature of the country’s political firmament.

But contrary to one of the most fervently held of Pakistani beliefs, things do change in Pakistan, and they change rather dramatically at times, albeit not always at the pace the population would hope they would. No doubt some will consider the title of this article to be provocative, but once we are done laying out the evidence, we suspect hardly anyone will disagree with the conclusion that feudalism as an economic force is dead, and as a political force is well on its way out.

More important than describing just something that has happened in the past, it will help explain why the Pakistan Army has faced an increasingly uphill task in creating a political arrangement that works to its liking, and why outright military coups are no longer possible not just because of perceived American pressure.

This magazine likes to consider itself strictly focused on business and the economy, and we have historically shied away from talking about politics for the simple reason that there are plenty of people with astute analysis about Pakistani politics, but far fewer who can talk about Pakistani business and its economy. We would rather stick to what we know.

But at times, talking about politics becomes unavoidable. We are not naïve enough to think that politics is downstream of economics, or vice versa. The relationship between the two is far more complex. And while we will never become a publication with regular content about politics, when the economic half of political economy deserves to be highlighted, we will offer our analysis for consideration.

In this story, we will talk about the origins of Pakistani feudalism and its most recent iteration, how its economic and political strength manifested itself, and what were the secular economic trends that have sapped it of its power.

Origins: or how modern Pakistan was built in the 1880s

Let us start first by defining feudalism, especially as it exists in Pakistan: the combining of land ownership and political power in a single person, usually the patriarch of a family. In Pakistan, since we do not formally have aristocratic titles, this meant a person who was seen as the de facto ruler of a region, even though he may hold no formal titles from the government.

Who these families are and how they acquired this power is a subject that we are not experts in, and cannot comment upon. What we can say, however, is that while the system of political power and ownership of agricultural land being tied

together is quite old – likely even preceding the Mughal Empire – the manifestation of it that Pakistanis are familiar with acquired its current shape in the 1880s.

It was during that decade that much of what became Pakistan acquired its base level of economic infrastructure. Why that decade? Because that is when the British were able to complete a project 40 years in the making.

The British vision for the economy of what is now Pakistan was simple: grow food in the river plains of Punjab and Sindh (and to a lesser extent, Balochistan and Khyber-Pakhtunkhwa), and then sell it to the world through the port in Karachi.

The British conquered Sindh in 1847, and in 1855 began construction on the railways. The infrastructure they began building would fall into place by the 1880s. In 1881, they created the Karachi Port Trust, to manage what would go on to become the largest grain port in the British Empire. In 1883, the Attock Bridge created the first permanent road to allow travel between Peshawar and Lahore. In 1886, they began construction of the Punjab Canal Colonies to farm more of the land between the rivers of Punjab. In 1889, the last piece of the railway connection – the Lansdowne Bridge in Sukkur – was completed.

What does this all have to do with feudalism? It created the economic landscape that allowed many more families to gain feudal power. Much of the agricultural land in Punjab was not farmable before the 1880s, and so a landowner ruling that region would not be possible because, hard as it may be to believe now, many of these regions were sparsely populated in the 1870s and prior. And once the colonies were built, owning the land would still

not have been meaningful without the railways that allowed for the surplus crop to be exported around the world.

The Mughals may have had the mansabdari system that feels like it was the origin of Pakistani feudalism, but the infrastructure that gave most of the erstwhile feudal families their wealth – which formed the basis of their political power – was the canal colonies and the railway.

And for almost a century, this system was almost the only source of wealth in the country which meant that, if you were a rural landowner, you owned effectively the entire avenues of wealth generation in your region, and were so completely dominant, that you were effectively the absolute ruler of that region. Feudals used to have (and some still do) small private armies, courts, and prisons.

This kind of political power in the hands of a small, discrete number of families meant that the political and economic elite of the country were effectively the same, and a very clearly well defined class. It is also, by the way, why Aitchison College was set up around the time this elite was being formed, and its original name was Punjab Chiefs College.

No sense in having an aristocracy unless you will make their future patriarchs bond together through shared experiences of hazing rituals at an all-boys boarding school.

It also means that anyone who wants to rule Pakistan simply needs to court this small number of families. And since it was the British that gave these families the means of becoming rulers, it means that while they exercised near-absolute control within their regions, they are used to interacting with a party outside of their kind to hold ultimate political power of

the polity of which they hold citizenship, and see themselves as subsidiary partners of the central government.

They are the “electables”.

The power of the electables

In a sense, Pakistan’s power structure never really changed from about 1886 until about 2008. The British, civilian control, military rule… these are all just the central government veneer on the core of the superstructure of the feudal aristocracy that has historically ruled Pakistan. In the symbiotic relationship between the state and the aristocracy, the aristocracy gets access to state resources for themselves and the people they rule, and the state gets to borrow their local political legitimacy.

Of course, the aristocracy is not a unified bloc, and the various entities that want to control the state take advantage of the divisions within the aristocracy to form ruling coalitions. This is the “electables” strategy of taking power in Pakistan, and contrary to common perception, both civilian prime ministers and military dictators use it to gain power.

Indeed, the first person to use this strategy was Muhammad Ali Jinnah in the 1946 elections when the Muslim League effectively absorbed the membership of the Punjab Unionist Party and got them to support his agenda of the creation of Pakistan. Why did Punjab’s aristocrats move to support Jinnah? Because they guessed, correctly, that Pakistan would be safer for their interests as a landed aristocratic class than India.

From then until about the end of the Musharraf era, if you were a civilian prime minister, you needed the aristocrats to vote with

you in the assembly to keep your seat. If you were a military dictator, you needed enough of them acquiescing to your coup to even consider one. And therefore, to keep them on your side, you needed to consider their interests more than any other class of people.

It is not a coincidence that Zulfikar Ali Bhutto, the founder of Pakistani democracy, was an aristocrat himself. He was of the class he knew needed to back him, and he was able to get them on his side by essentially conceding that their interests would largely go unperturbed by the government. It is not a coincidence that the federal and provincial cabinets in his era had heavy overrepresentation from the aristocracy.

The combination of state power and land ownership was potent back when there was no other source of wealth in Pakistan.

That is no longer true, and the consequences of that change are what Pakistan is now living through.

Growth: why change is happening

It is important to recognise that the aristocracy is losing power not because the value of their land is going down. Far from it: agricultural land grows in value during most years. The reason they are losing power is because other assets in the economy are becoming more valuable, which reduces their relative power. That reduction in relative power has been going on for decades, and it is the reason why non-aristocratic segments of Pakistan’s political elite have continued to emerge.

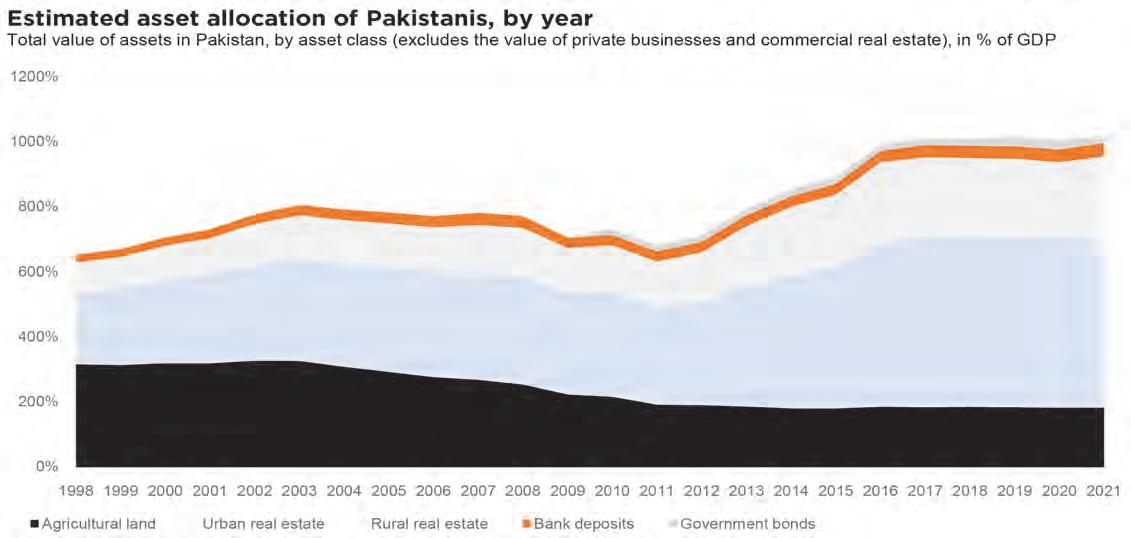

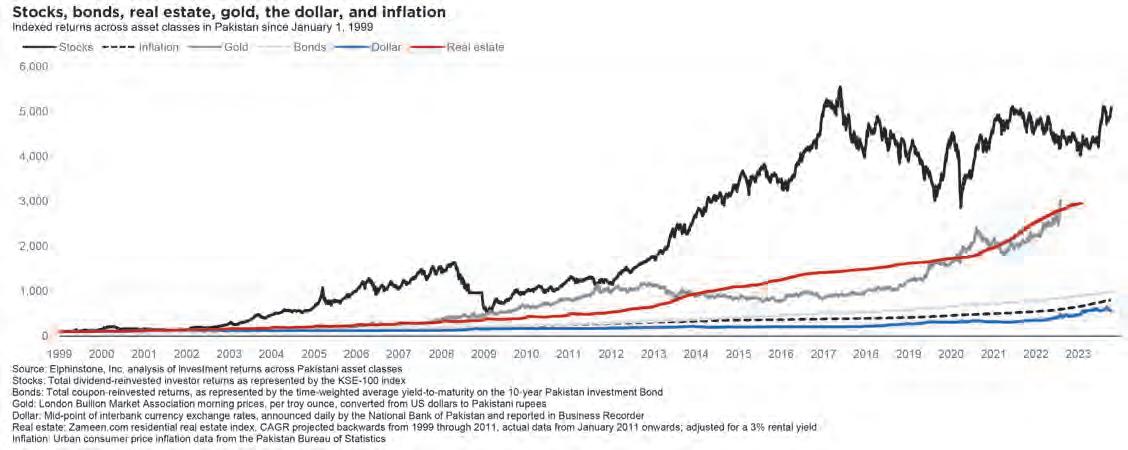

For this analysis, Profit relied on data analysis from Elphinstone, an investment advisory company (of which I am the founder and CEO), to understand just how significant the shift has been. And it has been marked.

While our data analysis only extends

between 1998 and 2021, and relies on some extrapolations and interpolations of values for real estate in particular, we are reasonably confident that the analysis is at least directionally correct, and reveals a fascinating look into the sources of wealth in Pakistan.

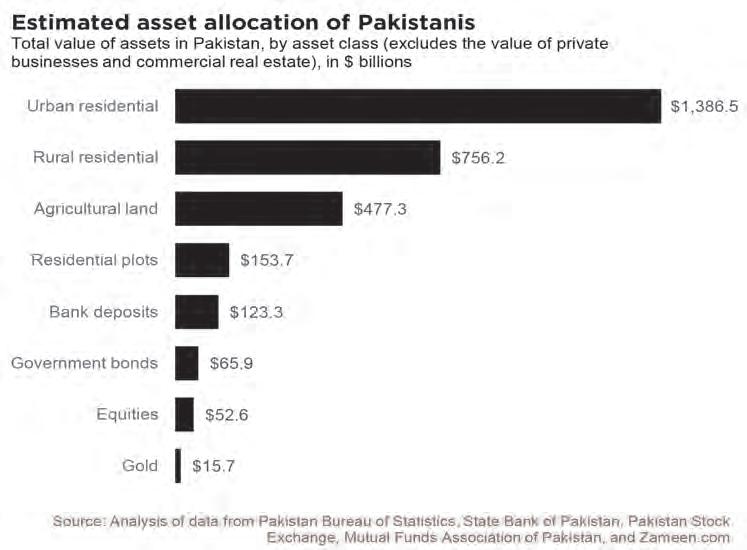

Based on Elphinstone’s analysis, agricultural land was the most valuable asset in Pakistan until approximately 2005, after which urban real estate became the most valuable, a position it holds until present day.

Indeed, agricultural land has decreased in value relative to the total size of the economy, from about 314% of gross domestic product (GDP) in 1998 to just 181% in 2021. The monopoly of landowning aristocrats on wealth generation has considerably receded.

Think about what this means: if you were a farmer in rural Pakistan about 50 years ago, you were either reliant on work or a tenant farming position on the estate of the local aristocrat, or a government job, as the means of creating economic security for yourself and your family. And even that government jobs was only accessible through the intercession of that aristocrat on your behalf.

Now, however, while Pakistan is far from being an economically prosperous country, there are plenty of options, and the land or government job options seem far less appealing than they used to be. As a result, the aristocrat gets far less deference from the residents of the villages that their family owns, and the demands and needs that the villagers have are far more complex and beyond the ability of these aristrocrats to give.

In other words, we did not dismantle feudalism. We outgrew it.

How did that happen? The Pakistani economy grew more complex, and the government not only let a private sector economy grow but engaged in some privatization transactions that allowed even some state-owned

commercial enterprises to be operated by private businesses. Industry and services grew as a percentage of GDP relative to agriculture, and cities grew at the expense of rural areas, making the rural electable no longer a monopoly for the source of political power.

The breakdown of the electable strategy

What all of this means is that the electables are no longer the only path to political power.

To some extent, we have already seen political parties build both a cadre of workers and a level of leadership who are not aristocrats themselves. The ruling Pakistan Muslim League Nawaz, while a partial user of the electables strategy, has always had a core leadership team that was not of the traditional aristocracy.

But the aristocracy remained large enough and important enough well into the Musharraf era for it to be possible for the Musharraf administration to cobble together a ruling coalition using those electables. And the PPP and PML-N were able to rely on at least some of them to cast deciding votes in Parliament after their 2008 and 2013 elections as well.

But the Pakistani elite is getting bigger and bigger, and there is more competition both for the aristocrats and among them as well. As a result, if you want to gain power in Islamabad, having a few “electables” by your side is simply not enough. They cover a much smaller geographic footprint than they used to, and command a lot less deference than in decades past.

To build a ruling coalition now requires sources of legitimacy far more complex than simply having all of Pakistan’s largest landowners by one’s side. This is a large part of why the Pakistan Peoples Party (PPP) has been struggling, since they – more than any other single party – has

been one that has relied on rural aristocrats to form the core of their electoral strategy.

Pakistan’s economy has shifted from being one where the only path to economic security involved the largesse of the aristocrat or the government to being one where there is a very rough correlation between an individual’s own efforts and the level of economic security they can achieve.

This previous sentence is particularly hard to appreciate right now, given how many young and talented people want to leave Pakistan right now, but it is true. Relative to our past, Pakistan

is far more meritocratic than it was. That it is not a good enough meritocracy is precisely the frustration felt by the population.

But this is the change: we have gone from “please give me a land tenancy or a government job so that I have some measure of security and I will recognize your authority over me in return” to “I have the ability to make my own way in the world, but the infrastructure I need to make things happen – education, healthcare, etc. – are not being delivered to me and so I want the person who is best positioned to deliver that to become the ruler whom I will find to be most

worthy of political power.”

That latter sentiment involves much more complex standards of judging who gets power. It lends itself well to a functioning democracy, but not at all to an authoritarian regime, which is why the attempts to run the country as an authoritarian regime are requiring a lot more force than has historically been needed. People expect more, and unless their local electable is used to competing for their vote using more modern criteria, they are unlikely to acquiesce.

What comes next

We are not political analysts and not well positioned to offer insights into what is likely to be Pakistan’s political structure in the coming decades. But, to return to our earlier point, there is an economic context that influences any country’s political institutions, and understanding how that context is changing is important.

Our view is that, too often, those who examine Pakistan’s politics tend to not study the economic changes taking place in the country and we hope to be able to provide at least some of the data to help shape the discussion.

What is abundantly clear, however, is that Pakistan is not a static country, that progress does happen, and that it happens even in the realm of politics, where we are most likely to view developments as being simply a viciously repeating cycle of history.

You can choose to be a pessimist about Pakistan if you wish. But you cannot ignore the manner in which the country is changing if you wish your analysis to be accurate. n

Supernet is fixated on the Fixed Local Loop (FLL) Licenses. But why?

Supernet Limited’s Fixed Local Loop (FLL) licenses will replace its Customer Value Added Services License, but why does the company want to go down that path?

By Hamza Aurangzeb

The dawn of the information age in the early 1990s ushered in a transformative era for the Information and Communication Technology (ICT) sector in developed markets. This period saw the foundations of the modern digital economy being established through the rise of the internet, personal computing, and advanced telecommunications infrastructure. These elements paved the way for the exponential expansion of several ICT companies, many of which have since become the tech giants we know and admire today.

However, while the ICT industry was booming in the developed world, Pakistan’s digital landscape remained in its infancy during this time. Limited telecom infrastructure, outdated equipment, and slow, high-cost internet access meant that the benefits of the information age were largely restricted to large businesses, academic institutions, and government entities. It was not until 1995, with the introduction of dial-up services by private internet service providers like Supernet Limited, that Pakistan began its journey towards a more connected future.

In the decades since, Pakistan’s internet landscape has evolved significantly, with the widespread adoption of mobile broadband outpacing even fixed broadband technology.

This raises an intriguing question: Why then did Supernet Limited, a pioneer of the dial-up era, decide to acquire Fixed Local Loop (FLL) licenses? To understand Supernet’s strategic move, Profit delves into the company’s story, shedding light on its operations and the factors

shaping its evolution within Pakistan’s rapidly transforming ICT landscape.

Supernet and its vision of “Beyond Connectivity”

Supernet Limited, a subsidiary of Telecard Limited, is a pioneer of dial-up internet services in Pakistan, which commenced operations in 1995. The company quickly gained traction as it captured the growing demand for internet usage in the country. Over time, Supernet expanded its offerings, introducing advanced connectivity solutions like VSAT and alternative wireless services, allowing it to differentiate itself from competitors and provide LAN/WAN services to enterprises.

While Supernet’s customer base was primarily restricted to corporate clients due to limited infrastructure and high internet rates, the company focused on customized connectivity solutions and related services. However, in 2018, the company broadened its horizons, introducing a “Beyond Connectivity” vision. This strategic shift saw Supernet venture into new domains like IT infrastructure, solar power, cybersecurity, and software/applications, anticipating rapid demand for ICT services from enterprises and government institutions driven by the growth of connectivity and digital networks.

While speaking to Profit, Mr. Jamal Nasir Khan, CEO of Supernet, explained, “Since the inception of Supernet Limited, connectivity services have remained its core business. However, in 2018, we decided to expand our solutions and

services from ‘connectivity’ to ‘beyond connectivity’ domain to cover IT & infrastructure, solar power, cyber security, and software & applications. This decision was taken in anticipation of an increase in demand for ICT infrastructure and services from corporations and government departments due to rapid digitization. In order to cater for this demand we established two dedicated new subsidiaries with the brand name of SuperSecure a dedicated managed cybersecurity service provider and SuperInfra for IT infrastructure and renewable energy solutions.”

Today, it has evolved into a large technology group, which offers a full spectrum of ICT solutions. It is one the leading telecommunications services providers and systems integrators in the country, which has extensive experience in providing ICT services to corporate clients. Supernet’s engineering resources can be found at 200+ locations in the country. It has developed an expertise in both connectivity and non-connectivity services for businesses.

Supernet Limited serves a diverse customer base, including enterprises in banking, oil & gas, telecom, distribution, and manufacturing, as well as various government departments and defense forces. The company has four subsidiaries - Supernet Secure Solutions, Supernet Infrastructure Solutions, Supernet E-Solutions, and Phoenix Global FZE - that collectively offer a range of services, encompassing connectivity, cybersecurity, power management, IT infrastructure, and software solutions.

The company has extensive experience in establishing and managing advanced connectivity networks, enabling it to provide robust data services, dedicated internet, and voice

solutions. Supernet Secure Solutions operates as a managed security service provider, offering threat protection, compliance management, and security operations. Supernet Infrastructure Solutions provides power solutions, data center infrastructure, LAN/WAN management, and cloud/surveillance services. Supernet E-Solutions develops vertically integrated, affordable ICT software solutions tailored to customer needs. Lastly, Phoenix Global in the UAE delivers IT and communication solutions to international clients.

Listing of Supernet on the GEM Board

Telecard, the parent company of Supernet Limited, decided to list Supernet on the Pakistan Stock Exchange (PSX) in September 2021, making it the first IT company and the third overall to be listed on the GEM board. Telecard’s decision to publicly list Supernet was driven by three key reasons. Firstly, the company wanted to access capital markets and unlock the true value of Supernet.

Secondly, Telecard had anticipated that Supernet’s revenues would double in the next two to three years due to the burgeoning demand for ICT solutions and rampant digitization, and the company required capital to expand its new business segments.

Thirdly, Telecard wanted to establish Supernet’s presence in the capital markets to enhance its credit history, creating a conducive environment for raising debt in the future for further expansion. The capital raised through the public listing was utilized to fuel Supernet’s growth ambitions, including the procurement of fixed assets, investments in subsidiaries, and gathering working capital. Additionally, Telecard offered its own stakes to raise further working capital for the group.

The capital was raised entirely through

the book-building method. The total issue size was 21,111,121 ordinary shares, where 8,888,889 shares were offered by Telecard Limited, while 12,222,232 fresh shares were issued. The floor price for the entire issue was set at Rs 22.50 per share. Supernet planned to raise 475 million, where 200 million were to be raised through selling shares of Telecard while the rest of 275 million were to be injected as fresh equity. The book building for the IPO took place on April 12 and April 13, 2022, where Supernet’s issue was oversubscribed by 1.35x at the floor price of 22.50 per share. This showcased the faith and conviction of both individual and institutional investors in the long-term success of Supernet. A sum of 106 investors participated in the process of book building and 88 investors were successful in acquiring the shares of the company. These investors included high-net-worth individuals, insurance companies, modarabas, and foreign institutional investors.

Supernet’s transition from CVAS to FLL

Since Supernet’s forte was data, it acquired the Customer Value Added Service License for Data on October 23, 2009, to provide internet and data services along with other value-added services to its corporate clients for 15 years until October 22, 2024. Initially, the company opted for a Customer Value Added Service to provide top-notch data and internet services along with customer care but without the hassle of establishing and managing its own infrastructure, as it is capital intensive. However, now the company believes that it is witnessing robust growth and has expanded its network to a great extent by delivering services in major cities across Pakistan. It has also become a publicly listed company and diversified its portfolio which has bolstered its position. Moreover, the market size of Fixed Local Loop stands at Rs103.9 billion approximately, while Customer Value Added Services offers a shallow market of only Rs28.3 billion. Thus, it wants to expand its footprint across all telecommunication regions of Pakistan and develop its own fiber optic infrastructure that will allow it to reach all regions including remote and far-flung ones that lack coverage but require connectivity solutions. It has acquired new licenses for Fixed Local Loop for 14 regions across the country, which will allow it to offer data and internet services and deploy its own fibre infrastructure, independent of other third-party operators. This was not the case with the CVAS license, where the company was dependent upon the infrastructure of third parties. Moreover, PTA has terminated the issuance of CVAS, so there is no other option for the company.

The company has also embarked on this endeavor to develop a reliable and resilient fibre infrastructure to capitalize on the growing demand for fixed broadband services in Pakistan.

Although the company does not offer data and internet services to households and retail customers directly, it could offer other internet service providers that serve households and retail customers to utilize its infrastructure in accordance with their needs.

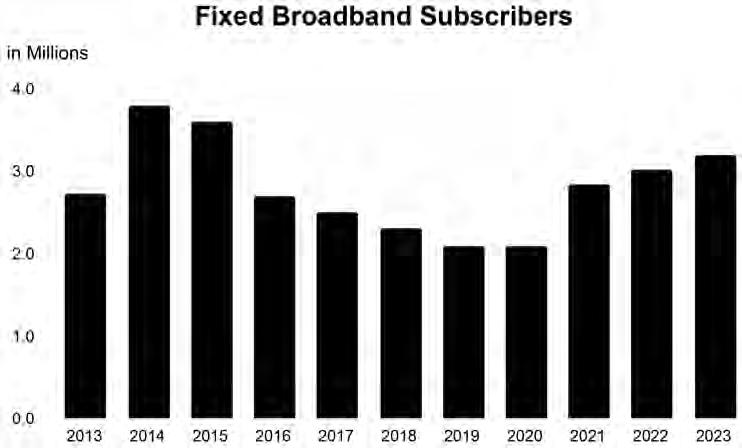

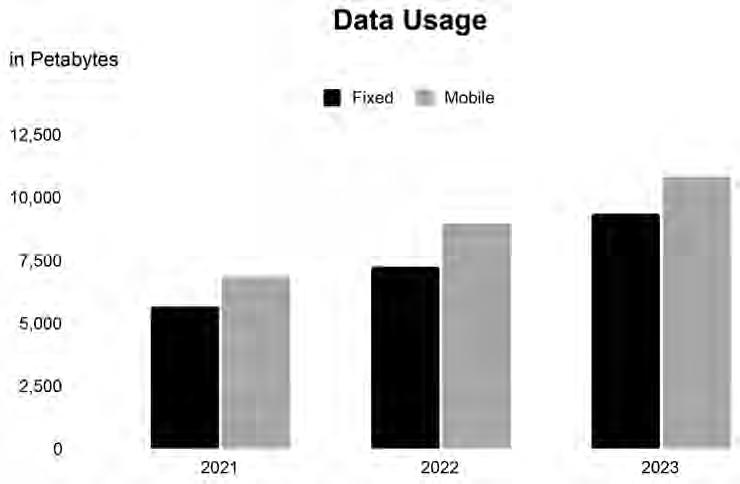

We are witnessing a resurgence in the popularity of fixed broadband, which is primarily driven by households. The fixed broadband penetration in the country was consistently declining from 2014 to 2020 until the pandemic engulfed the entire globe including Pakistan. The pandemic expedited technology adoption and introduced a culture of work-from-home, both of which increased data consumption in households. People started completing professional tasks from their households more frequently, while at the same time, advanced appliances like smart TVs with 4K and HD quality became popular across various segments of the population, leading to increased watch time on TVs. Moreover, the frequent disruption of the mobile broadband service due to power outages and national security concerns also played a pivotal role in the redemption of fixed broadband services. The revival of the fixed broadband services could be corroborated by the number of subscribers, along with its data usage which is not far behind the data usage of mobile broadband.

“Supernet has obtained FLL licenses to expand its network in all telecommunication regions and build its own fiber optic infrastructure, which will improve its availability in all areas of Pakistan and improve its margins in the long run. The company is positioning itself to serve as a carrier for large volumes of data for telcos and internet service providers that cater to households and retail customers and also improve the availability of connectivity for enterprises across Pakistan. Thus, this initiative holds great potential for the company’s growth. Supernet is also planning to start operations in the MENA region as well,” Khan reiterated.

Supernet’s Vision for Innovation and Expansion

The company has an ambitious plan to develop its own infrastructure by erecting a fibre network, which will assist telecom companies in the transmission of data. The company believes that there will be a transformational rise in the data volume of telcos due to increased data consumption as soon as 5G technology is launched in the country. The telcos will require a gigantic capacity to transport their mammoth data volumes. This is where Supernet will come in, it will serve as a carrier for telcos and provide high-quality service through its resilient and robust infrastructure.

The Fixed Local Loop licenses will also assist the company in cost optimization. Currently, the company utilizes the infrastructure of third parties, the price they charge is the sum of the cost of establishing and maintaining infrastruc-

ture; and their margin. However, if the company establishes its own infrastructure, it will be able to eliminate the margin of the third party, which in turn will improve its margins in the long term.

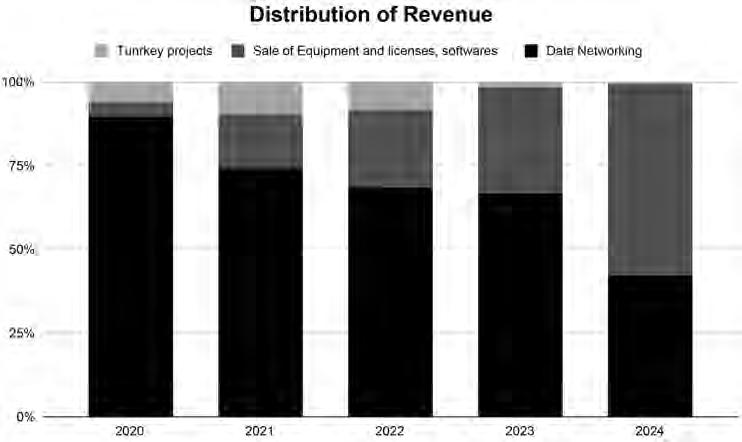

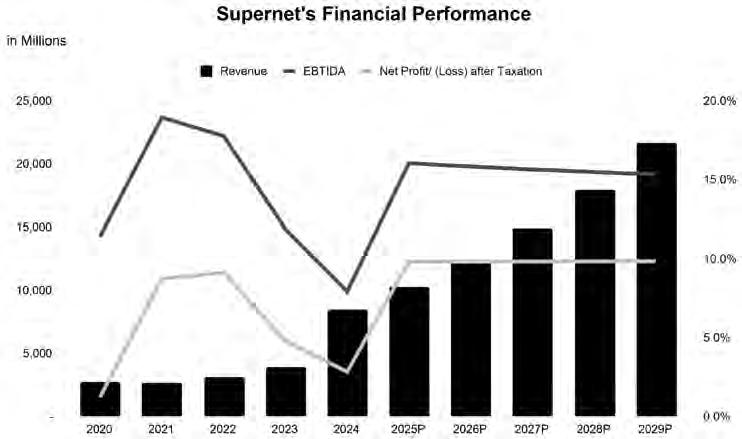

Analyzing the historical performance of the Supernet group reveals that it is a company which has witnessed tremendous growth over the past five years. On a consolidated basis, its topline has grown from Rs 2.7 billion to Rs 8.5 billion at a rate of 32.8% per annum. This growth is primarily driven by its offering of a comprehensive suite of ICT services under one roof to a diverse range of customers, including corporations, government agencies, and defence forces.

The company’s revenue could be divided into three main segments, data networking, turnkey projects, and the sale of equipment, software, and licenses, where the data networking segment has expanded at a rate of 10% per annum and turnkey projects segment has plummeted at a rate of 31.0% annually. However, the segment which focuses on the sale of equipment, software, and licenses has witnessed an unprecedented growth of 158.0% per annum to become the leading segment. If we discuss the company’s profitability, its net income has seen an impressive growth of 63.2% per annum, where it stood at only Rs 34 million in 2020 but now it has increased to Rs 241 million in 2024, while its EBITDA has enlarged by 21.2% per annum, it has gone from Rs 312 in 2020 to Rs 674 in 2024. Supernet’s acquisition of Fixed Loop Licenses certainly reflects its visionary approach, where it not only aspires to expand its data and internet services across distant regions in the country but also wants to explore the possibility of serving as a carrier for telcos and internet service providers for retail customers. Supernet has proved its potential in the past by successfully implementing its vision of “Beyond Connectivity” but will it be able to achieve its objectives this time around? That is a question only time can answer. n

A Rs 2.4 trillion question haunts Pakistan’s power puzzle.

As the government unveils its latest debt management plan, can the power sector escape its deepening financial spiral?

By Ahtasam Ahmad

Constantly pointing out the flaws in Pakistan’s power sector may seem repetitive, but the magnitude of its challenges keeps it in the headlines. In early November, the Government of Pakistan announced its Circular Debt Management Plan (CDMP) for the power sector. While the projected growth in debt liability is a modest 1.5%, the outstanding liability has already reached Rs2.4 trillion, and these projections rest on some generous assumptions that warrant closer examination. The question remains: are we headed for doom, or does hope still flicker in Pakistan’s power corridor?

Making of the crisis

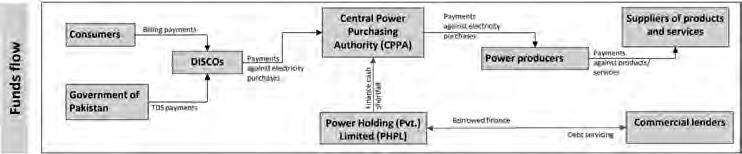

Pakistan’s power sector struggles with a persistent circular debt problem rooted in a complex web of unpaid obligations that has grown increasingly intricate over the years. At its core lies the unfunded outstanding liability of power distribution companies (DISCOs) and K-Electric (KE) to the Central Power Purchasing Authority-Guarantee (CPPA-G), a situation that has become more precarious with each passing year.

When DISCOs fail to clear their dues to CPPA-G, it creates a cash shortfall, prompting Power Holding Private Limited (PHPL) to borrow funds to cover CPPA-G’s liabilities. This cycle of delayed payments represents the accumulated circular debt in the country.

The growth of this circular debt can be

further exacerbated by high transmission and distribution losses, coupled with poor revenue collection by the DISCOs, which have steadily widened the funding gap beyond sustainable levels.

The government’s partial and often delayed payment of tariff differential subsidies has added another layer of complexity to the sector’s financial woes, while high borrowing costs for PHPL and expensive late-payment penalties on CPPA-G’s payables have created an additional burden that seems almost impossible to overcome.

In Pakistan’s power market, consumer-end tariffs are deliberately set below actual electricity supply costs, with government subsidies attempting to bridge the gap. However, as costs persistently exceed revenues, the sector’s financial deficits have averaged an alarming 2.8% of GDP during FY14–FY24.

By June 2024, the total circular debt reached Rs2.4 trillion, equivalent to 2.3% of GDP, representing an almost 50% growth from FY19. This rapid acceleration in debt accumulation began in earnest in 2018 with the signing of “take-or-pay” contracts for imported coal and gas power plants, a decision that increased capacity payments by 50% and exposed the country to the volatile whims of international fuel prices—a vulnerability that became painfully apparent during the global energy crisis of 2022.

The implications of these structural energy sector problems extend far beyond the power industry itself, creating a complex web of challenges that affect Pakistan’s entire economic landscape.

attributed to five fundamental factors that have created a perfect storm in Pakistan’s power sector. High power generation costs have severely undermined DISCOs’ ability to effectively collect revenues and manage their operations, creating a persistent gap between costs and collections.

Compounding this problem are the chronic issues and delays in tariff determination, which have left the sector struggling to maintain financial equilibrium. The situation is

Source: Asian Development Bank

The macro and micro fallout

At the macroeconomic level, the impact is particularly severe in three critical areas. First, the combination of unreliable energy supply and soaring costs has dealt a significant blow to industrial operations and export competitiveness. Consumer tariffs have increased more than sevenfold since 2007, with addi-

tional surcharges for PHPL liabilities and late payment penalties adding to the burden. This situation has become even more challenging under IMF conditions that require increased consumer tariffs to curb circular debt accumulation, creating an almost impossible balance between fiscal sustainability and consumer affordability.

The second major macroeconomic impact stems from the power sector’s massive drain on fiscal resources, which has effectively diverted crucial funds from vital development projects. Power sector subsidies have dominated government subsidy outlays, averaging over 80% during FY13-FY22 and are projected to reach an unprecedented 88% in FY25.

This concentration of subsidies in a single sector has severely limited the government’s ability to invest in other critical areas such as education, healthcare, and infrastructure, creating a development deficit that could take generations to overcome. The government’s guarantee exposure presents an equally concerning picture, with the power sector accounting for 70% of the total Rs3.5 trillion guarantee stock as of March 2024, where PHPL alone represents one-fifth of these guarantees.

At the microeconomic level, the repercussions ripple through the financial sector and corporate landscape with far-reaching consequences. Banks’ high exposure to energy sector loans, second only to textiles and FMCGs, has effectively crowded out private sector borrowing for productive activities, stifling economic growth and innovation.

The accumulation of circular debt particularly strains energy supply chain companies’ financial health, many of which are listed on the stock exchange and have retail investors, affecting their operational efficiency and investment capacity. Pakistan State Oil (PSO) serves as a prime example of this predicament, carrying power sector receivables of Rs180 billion and relying on costly bridge financing to maintain operations. This situation has created a cascade of financial inefficiencies, as companies throughout the supply chain face working capital constraints and increased financing costs.

The circular debt problem has also created significant challenges in financial reporting, forcing regulators to find creative solutions to manage the situation. As PSO’s 2024 financial statements note, “The Company considers this amount to be fully recoverable because the GoP had assumed the responsibility to settle the inter-corporate circular debt in the energy

sector. SECP has deferred the applicability of ECL model till December 31, 2024 on financial assets due directly / ultimately from GoP in consequence of the circular debt.”

The Circular Debt Management Plan

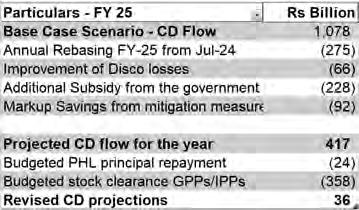

The government’s latest plan assumes a base case that would incur around Rs1 trillion in circular debt during the current fiscal year. However, multiple interventions, including improvement of DISCO losses, additional subsidy, markup savings, PHPL debt repayment, and clearance of a portion of power producers’ stock, aim to reduce the net flow to only Rs36 billion.

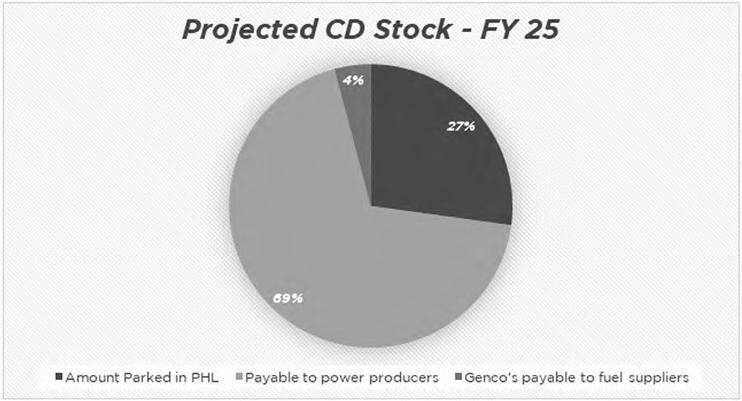

Looking at the projected composition of the circular debt by the end of FY25, with almost Rs1.7 trillion in payables to power producers, the clog in the power sector appears likely to persist. Additionally, the Rs660 billion parked with PHPL, representing significant sovereign-backed borrowing, looms large over the sector’s future.

The government’s response encompasses four key measures, primarily focused on bringing down electricity costs, increasing tariffs, providing additional subsidies, and achieving markup savings.

Currently, approximately 85-90% of end-consumer costs stem from generation expenses. Reducing these costs would require a shift towards least-cost technologies, particularly renewables, strict adherence to economic merit order, and avoiding further investment in excess capacity that could increase capacity

payments, which already account for roughly 60% of generation costs.

While these measures appear promising on paper, the government’s true intentions might be better gauged through the Indicative Capacity Expansion Plan released earlier this year. Unfortunately, the country’s energy planners appear to have overlooked many of these considerations, instead opting for expensive projects likely to increase generation costs.

The rapid pace of solarization also suggests that demand projections may be overestimated, though a revised version of the plan expected in December might address these concerns. Perhaps most tellingly, the CDMP document’s opening disclaimer that “The Plan also assumes that GoP committed subsidies will be budgeted properly and released in a timely manner”, suggests these projections may be optimistic at best.

A critical component of the plan focuses on markup savings, which would be achieved through two primary channels. First, the PHPL debt service would be completely passed on to consumers, resulting in an average surcharge of approximately Rs2.84 in electricity tariffs. Additionally, a projected repayment of Rs24 billion would slightly reduce the interest-bearing stock. The plan also addresses the interest liability accrued on outstanding IPP

stock due to late payment surcharges. While NEPRA does not allow DISCOs to pass this cost to consumers, the government envisions a payment of Rs358 billion to power producers through negotiations and PPA revisions, potentially saving around Rs92 billion in markup payments.

While the latest CDMP outlines strategies to prevent further debt accumulation, it notably lacks a comprehensive approach to addressing the existing debt stock.

Bringing the stock down

The widely discussed solution, endorsed by the IMF, involves a debt restructuring approach that would see the government issuing new guarantees to transfer CPPA-G’s payables to IPPs into PHPL, with the government ultimately absorbing PHPL into its budget and recognizing its liabilities as public debt. This approach offers several advantages, particularly given that CPPA payables attract late payment surcharges up to 3-month KIBOR + 4.5%, while PHPL borrowing rates hover around KIBOR + 2%. With government securities currently trading below KIBOR, this restructuring could potentially reduce both debt accumulation and consumer surcharges.

The IMF’s proposed solution for addressing outstanding liabilities relies heavily on proceeds from power asset privatization, recovery of outstanding receivables, and rationalization of subsidies.

However, the success of these measures depends entirely on fiscal prudence and effective privatization—both areas where Pakistan has historically struggled to deliver results. As the sector stands at this critical juncture, the effectiveness of these interventions will largely determine whether Pakistan can break free from its circular debt trap or continue to spiral deeper into financial distress. n

Since the 2022 floods, farmers have been enjoying higher yields.

This Kharif season might buck the trend

The seasons started off with concerns surrounding the availability of water and ended with a monsoon season that was less than inspiring for many crops. What might the carnage look like?

By Abdullah Niazi

On the back of water shortages during the sowing season and heavy monsoon rains close to harvesting, Pakistan’s agricultural sector is bracing for a poor showing in the ongoing Kharif season.

While the results will not be clear until well into next year, initial reports from farmers, the government, and foreign agencies indicate an atmosphere of concern in the days ahead. The Kharif season, which begins with sowing in April and ends with harvesting between October and December, is when some of Pakistan’s most important crops are grown. These include rice, maize, cotton, and sugarcane with the latter two often in competition with each other.

A dip in fortunes for farmers, who have been experiencing high yields ever since the devastating floods of 2022 subsided, might also have lasting impacts on the upcoming Rabi season, in particular the wheat crop. Many farmers are already concerned about the future of the wheat crop ever since the announcement that the support price for wheat was being phased out. Many might turn to higher yield oilseeds instead, or might even choose crops that have smaller cycles and plant cover crops in between, making use of their land twice during the Rabi months which start in late October.

Too little and then too much water

This year’s agricultural outcomes for the Kharif season will very much be defined by the issue of timing. During the initial sowing period, there was a very serious shortage of water, and during the harvesting season late rains managed to inundate many areas with too much water.

Back in March this year, an Advisory Committee of the Indus River System Authority (Irsa) said Pakistan could face up to 30-35% water shortages during the upcoming kharif cropping season starting April 1. They warned this would negatively affect some of the key cash crops like cotton and revive inter-provincial controversy over water allocations. However, the water situation improved and eventually the shortage was only around 19% after late monsoon rains in September this year. However, the late rains brought mixed results.

On the one hand, three cash crops including rice and sugarcane - both high delta crops requiring more water - and cotton were set to benefit from the late rains. These three crops alone cover an area of 11.4 million acres in Punjab this year. According to the Punjab Agriculture Department, rice cultivation was at six million acres, sugarcane two million acres and cotton nearly three and a half million acres in Punjab.

But the benefit was limited. Floodwater

inundated almost the entire katcha area from Guddu upstream to Kotri downstream, encompassing a big portion of Punjab’s richest farmlands. While this will improve soil fertility for the Rabi season, particularly to grow wheat, it became a struggle for the existing crops. In many of these areas, significant breeches of water owing to the mismanagement of saline water drains by the irrigation authorities led to many areas becoming waterlogged, and flood like conditions prevailing in them. According to one report, the cotton crop sown on 3.4 million acres in Punjab needed special care in the prevailing situation.

Sindh’s struggles

The situation in Sindh was also bleak. At the start of September, Sindh Agriculture Minister Sardar Mohammad Bux Mehar reported in a preliminary assessment that recent heavy monsoon rains and flooding have caused widespread crop damage, resulting in an estimated Rs86.86 billion loss to farmers in the province.

Mehar reported that 541,351 acres of crops were completely destroyed. Specifically, 293,580 acres of cotton were severely impacted by the downpours.

Rice crops were completely destroyed over 35,271 acres and partially damaged across 269,016 acres. Similarly, date palm groves suffered massive losses on 53,195 acres and partial damage on 32,849 acres. The sugarcane crop was entirely destroyed over 26,382 acres, with partial damage on another 69,689 acres

The heavy rains caused a 21% loss in cotton output and a 41% loss in date palm production. In addition, tomato nurseries experienced a 3.4% loss, sesame crops a 22% loss, onions a 58% loss, chilies a 12% loss, and vegetables suffered an 18% overall loss.

The minister listed the districts most affected by the rains, which include Badin, Dadu, Ghotki, Sukkur, Hyderabad, Larkana, Sanghar, Thatta, Sujawal, Mirpurkhas, Khairpur, Umerkot, Tando Allahyar, Shikarpur, Shaheed Benazirabad, Matiari, Tando Mohammad Khan, and Tharparkar.

Current outlooks

The final numbers for the major Kharif crops are not out yet. However, there are some prevailing predictions. Perhaps the crop facing the music the most is cotton. Cotton production in Pakistan has seen a sharp decline, with total arrivals down 36.84% year-over-year, according to the latest data from the Pakistan Cotton Ginners Association (PCGA). As of November 1, 2024, arrivals totaled 4,291,105 bales, a stark drop from last year’s 6,794,006 bales. Punjab recorded a 38.53% decrease in output, with 1,842,257 bales produced compared to 2,996,921 bales last year. Sindh saw a 35.51% reduction, producing

2,448,848 bales, down from 3,797,085 bales in 2023. Balochistan’s production, meanwhile, stands at 131,800 bales.

As a crop, cotton has been struggling for some time now, and attempts to revive it are made every year. The crop is faced with many issues. There are inadequate price factors, there has been no seed development since 2005, and serious variations in weather patterns such as the ones seen this year are a cause for concern. Flooding, and pests have also been a consistent threat to the crop. Farmers have switched from cotton to sugarcane over time, especially since the textile industry has also gotten used to importing much of its raw cotton needs.

Sugarcane is one crop that seems to be stable this year, especially since it is a water guzzling crop and benefitted from this year’s late monsoon downpours. According to the United States Department for Agriculture, the 2024/25 sugarcane production forecast remains unchanged at 83.5 million metric tons, which is two percent higher than the 2023/24 estimate. This increase in production is attributed to a rise in cane area. Over the past two years, sugarcane has proven to be more profitable than competing crops such as maize and cotton. Additionally, the support prices have encouraged growers to expand their sugarcane planting. Area has increased in Punjab province. Overall weather conditions have been favorable for sugar cane in 2024, with abundant rains and suitable temperatures.

Meanwhile, it will be interesting to see how Pakistan’s rice markets react. On the one hand, the area under yield for rice increased last year thanks to India’s ban on rice exports. However, India has since repudiated that ban.

The 2024/25 (November-December) rice production forecast is increased from 9.5 to a record 10 MMT due to good planting conditions and prospects for adequate irrigation water supplies throughout the growing season. The 2023/24 rice production estimate is revised upwards to a record 9.86 MMT, in accordance with the latest official data. Except for the flood damaged 2022/23 crop, rice production has steadily increased over the past decade. This increase is due to increases in both area and yield. Area has increased as rice has been more profitable vis-à-vis alternative crops. Meanwhile, adoption of hybrid seed varieties are driving yield increases.

However, according to the USDA again, the most critical factor in the final tally will be the extent of the impact that the summer rains will have had.

While the final picture has not emerged, Pakistan has seen a Kharif season that will not inspire confidence amongst farmers. Even if overall crop production is similar to last year, it will be a disappointing outcome particularly because this year Pakistan was supposed to be poised for bumper yields. n

A year after going public very quietly,

Big Bird Foods has made a profit. Here’s what happened

Big Bird Foods has set an early marker for the year by registering a profit for the first quarter. Can this small player in a big market leverage this to grow their business?

By Zain Naeem

In the first financial year since they became a presence on the stock exchange, Big Bird Foods has posted a profit of Rs 27 crores, giving their shareholders earnings of Rs 0.9 per share.

Big Bird is a bit of an oddity in the frozen foods market where financial data

is generally a closely guarded secret, and few companies are publicly traded. In this market, they are the only publicly listed company and they too only listed a year ago. Despite this, the profit Big Bird has posted might not seem like much considering just how large this market is.

There is a glut in the market in terms of competition for frozen foods. The market already has PK meats, K&Ns, Sufi and Dawn

foods just to name a few. By a conservative measure, the frozen food market is worth $730 million in 2024 and it is expected… that this market size will increase to around $1 billion by 2030 with an average growth rate of 5.81%. Currently Big Bird makes up less than 5% of the market but it has been able to see steady growth in terms of revenue growth in recent years. Big Bird will want to capitalize on this

opportunity and increase its market share in the coming year.

This might seem like peanuts in comparison to the rest of the market but this is a growth of 32% from where the company stood last year earning Rs 0.68 per share. More importantly, Big Bird had been suffering losses on the trot for some years. The change in fortunes will mark an important moment for Big Bird. The first quarter performance compliments the annual results for the company where it showed a profit of Rs 84 crores where it had earlier made a loss of Rs 12 crores. The company seems to be coming out of the shadows of its past performance and is setting a new path for itself going forward.

Big Bird’s listing story

The frozen food market is actually one segment where the Pakistani market is quite robust, with K&Ns in particular also an exporter with

the largest share of the market. Which is why one might expect that if a frozen food company goes public, there would be a lot of noise surrounding it.

However, Big Bird did not go through the traditional pomp and pageant of an Initial Public Offering (IPO), instead getting on the stock exchange through a different route.

Essentially, Big Bird took over a company called MetaTech Trading which was listed on the market. Rather than having to go through the process of listing a company from scratch, Big Bird took over the ailing company and then changed its symbol and name to Big Bird Foods. This allowed the listing of Big Bird to take place and it started trading. They shelved the previous functions of MetaTech.

Big Bird was founded in 2011. The company operates end-to-end in the frozen chicken business, and is involved in poultry farming, slaughtering, processing and supply of finished and semi finished products into the market. They have a solid presence in the retail market and their products are available in most large stores. The company boasts a large array of ready to cook chicken products which have established their name and brand in the market.

Changing losing trends

In terms of financial performance, the company has been making losses for the last three years due to shrinking gross margins and operating costs. The company saw losses of Rs 83 crores in 2021, 30 crores in 2022 and 12 crores in 2023. The recent results finally show that the company is turning a corner and becoming profitable. The reason for the losses was due to the fact that the company was establishing itself in a cut throat market and was trying to carve out a space for itself. Now it seems the company is finally gaining a foothold with a steady stream of revenue and profitability.

The latest annual accounts show that the company is expanding its revenue base and earned revenues of Rs 7.2 billion compared to Rs 6 billion in 2023. Even though the company was able to grow revenues by 20%, it saw its cost of goods sold only increase from Rs 5.5 billion to Rs 5.6 billion leading to gross profits clocking in at Rs 1.6 billion. The gross profits almost tripled from where they were a year ago coming in at only Rs 57 crores. Due to inflationary pressures, Big Bird saw its distribution and administrative expenses grow. Due to high gross profits, the company still saw its operating profits go from Rs 31 crores in 2023 to Rs 1.2 billion in 2024. The company was also able to reduce its finance costs which led profit after tax to register at Rs 84 crores compared to a year ago when the company suffered a loss of Rs 12 crores.

Things seem to be going from good to better for the company as the first quarter results show that the company has been able to increase its revenues from Rs 1.8 billion in the first quarter of 2024 to Rs 2.2 billion in the recent quarter ended. With similar gross profit margins, the company earned Rs 49 crores in gross profit compared to Rs 39 crores one year ago. Even with rising operational costs and expenses, the company was able to show operating profits of Rs 39 crores which had been Rs 32 crores last year. One issue for the company was that it saw an increase in finance cost of around 12% as its interest payments increased from 10 crores to 11 crores this year. Regardless of this increase, the company still ended up earning profits of Rs 27 crores compared to Rs 20 crores last year. The company was still able to see its bottom line grow by 35% as it saw an increase in its revenues. The upward trajectory seems to be subsisting for the time being.

How they did it

This trend can be expected to continue as well as the company is signing contracts with long term customers like Johnny & Jugnu, Pizza Junction and Al Khan Catering in Lahore. The company already has its own store outlets which are selling its products. The company has also been able to secure contracts with new retail outlets in Lahore and Karachi which are allowing it to expand its revenue base. The company estimates that these contracts will yield an additional revenue of Rs 80 crores to Rs 1 billion to the annual sales of the company which will further increase the potential revenues.

Big Bird has also introduced a new product in its portfolio by offering raw fish filets and raw fish fingers as part of its product line. Big Bird feels that there is a growing consumer demand in this area and wants to cater to these demands by supplying fish based products. There are estimates that the fish and seafood industry is around 700,000 tons on an annual basis and it is growing between 4 and 5% per annum. Big Bird wants to tap into this market by providing these products initially before expanding further.

In addition to the local market, Big Bird is an approved supplier for Saudi Arabia and is part of the supply chain of McDonald’s in Qatar and Oman. The company also exports products in Hong Kong and China through direct and indirect means. Big Bird is also contracted to big corporate brands like Jalal Sons, Kababjees, Kitchen Cuisine, Hyperstar, Alfatah, Serena Hotel, Dawn Foods, KFC and McDonalds. The company is looking to establish itself in the market as a stable supplier and aiming to be the sole supplier to many of its biggest clients who are sourcing their raw materials from multiple sources.

Lahore’s smog isn’t difficult to understand. Neither is the solution to it.

The causes of smog are clear: bad fuel, crop burning, and dirty sources of energy. The answers aren’t all that complicated, and they don’t necessarily have to involve India

By Abdullah Niazi

Nawaz Sharif has long been a believer in normalising diplomatic and trade ties with India. He is perhaps the only major political figure in Pakistan openly advocating for better relations with India.

So it was not particularly surprising when his daughter Maryam Nawaz, also incidentally the chief minister of Punjab, expressed an interest in pursuing better India-Pakistan relations by reaching out to her Indian counterpart.

What was just a little confusing was why she reached out to the Chief Minister of Indian Punjab over the issue of air pollution. Lahore is currently engulfed in a blanket of toxic air the likes of which has not been seen since 2016 when the issue of smog first visibly emerged in the city. It is not just the capital of the province that is struck. Faisalabad, Sahiwal, Sialkot, and a number of other cities are facing the same problem. It is a problem that extends beyond Pakistan, and is felt acutely in South Asia.

In 2023, Bangladesh recorded the worst air quality of 134 countries monitored by the Swiss climate group, IQAir. Pakistan and India were close behind, with the report showing that South Asia suffers from the worst pollution in the world overall. But the smog issue is India is most felt far away from Punjab, with New Delhi and the Haryana region much bigger problem areas than Indian Punjab.

So why would Maryam Nawaz’s counterpart be interested in helping her tackle a problem that is affecting the other side of the border? Why would he want to ban crop burning in his province, possibly upsetting his rural votebank, when it will not do him much good? The answer is he most likely is not. Which is probably why there has been no response from Chandigarh.

The idea of climate diplomacy is well and good. The issue is it is not the best approach to dealing with a problem that has become lifeand-death for anyone living in Lahore. Smog is actually a very simple problem to understand and cure. Many cities around the world have done it for a very long time, and there is a roadmap. So what is it?

Understanding the scale of the problem

Allow us to begin with an exercise in contextualisation. It is easy to become desensitised if you live in Lahore. Just last week, the Air Quality Index (AQI) in Lahore crossed 1600 in some areas. The World Health Organisation considers an AQI of over 100 to be a risk to health for sensitive groups such as children, the elderly, and those with chronic respiratory illness.

And that is just a number. Think of it this way. Back in June 2023, wildfires broke out in Canada close to the American border, and winds blew south and got trapped in New York City. For a period of 3-4 days, the Big Apple became the most polluted city in the world, a title currently held by Lahore. This event, which was temporary and had a very definite external root, caused panic in the city. Authorities distributed a million N-95 masks for free, the Mayor called an emergency, and residents were advised to stay indoors until the wave passed. What was the AQI during this entire time? At its worst, it hit a high of close to 250. That is a number that would be considered a very good day in Lahore at this point.

This desensitisation is exactly why it is worth more closely understanding what the smog is. The first thing to understand here is that the air quality in Lahore isn’t just bad in the winter months. It is bad all year around. According to the Environmental Protection Department (EPD) of Punjab, the ambient air quality of the capital city Lahore in the year 2022 revealed that there were only 17 days of good or satisfactory AQI (PM2.5) out of the total 309 monitored days.

The air we breathe in contains particulate matter — small, microscopic bits of different substances. Particulate matter that is less than 10 microns (for context, one micron one-thousandth of a millimetre) in diameter is inhalable by the human lungs. And once these very small particles are inside your lungs in enough quantities they can cause adverse health effects.

Now imagine that the air we breathe every single day contains these particles that are less than 10 microns. With every single breath you take there is poison entering your lungs. And it gets worse. You see, 10 microns or a particulate matter reading of “PM 10” is already bad for you. But when the particulate matter gets to a value of 2.5 microns or less (which is what we refer to when saying PM2.5) is categorised as “Fine Particulate Matter.”

Now the more Fine Particulate Matter you have in the air, the worse your air quality is. And this amount of particulate matter is constant throughout the air. In the winter months, however, a thin layer of the atmosphere near the earth becomes cooler than that above it. As a result pollutants are trapped at ground level until there is a change in the weather.

So this is what you have. Lahore as a city and Punjab at large is producing toxic fumes and throwing them into the air every single day of the year. For most of the year they do not notice just how adversely this affects them. But for a quarter of the year stretching from at least November to January, the cold air traps these toxic fumes turning the province into a deadly hot-box of disease. During these months the smog’s threat to health and life is worse.

The effects are clear. According to a report of the World Health Organisation (WHO), the exceeding levels of air pollution have resulted in the loss of 5.3 and 4.8 years of life expectancy from 1998-2016 among populations of Lahore and Faisalabad cities, respectively. The rate of deaths attributable to air pollution (including indoor PM2.5, and ozone) in Pakistan is also well above global averages. The World Bank estimates Pakistan’s annual burden of disease from outdoor air pollution to be responsible for around 22,000 premature adult deaths.

The source of the poison

Punjab’s smog problem is entirely the creation of years of neglect and bad policy implementation. And it is human-made in a very direct way. A lot of the environmental issues faced by the global south in today’s day and age are caused by emissions from the global north. According to the Center for Global Development, developed countries are responsible for 79% of historical carbon emissions. Yet studies have shown that residents in least developed countries have 10 times more chances of being affected by these climate disasters than those in wealthy countries.

But the smog problem is entirely removed from this reality. Instead it is a bit of a localised environmental disaster. The air quality in and around Lahore and the other districts of Punjab is bad because of pollutants within. The fine particulate matter in the air is high because it is released from automobiles, industrial units, and the burning of crops. The data on what causes the smog is limited but the information available is quite clear. The main work on this is a 2018 study conducted by the Food and Agriculture Organisation (FAO). The study found that the main polluting sectors include transport at 43%, factories and industrial burning at 25%, agriculture at 20%, and power at 12%.

Cars:

The most obvious pollutant is the transport sector. When it comes to smog this is the big bad wolf everyone talks about. And the data is quite clear. Air quality in Punjab from 1998 to 2023 has fallen consistently. Over this same 25 year period, the increase in the number of vehicles on the road has been astronomical. According to a government report, while private transport rose by 332%, public transport increased by only 165% and road networks by a mere 6% in the past 25 years.

“There have been a lot of reasons for this increase,” explains academic Sanval Nasim. “Incomes have increased over time and people that were once using bicycles are using motorbikes instead. Then there is the issue that public

transport has not expanded so people have come to rely on motorbikes to get to their places of work and travel in a city that is growing and expanding every single day.”